RAK & Shinepukur Ceramics Working-Capital Structure.

20

1 | Page “Working Capital Management Efficiency of Ceramics Industry in BANGLADESH” Independent University, Bangladesh Submitted to Dr. Md. Abdul Hannan Mia Faculty of Financial Management (MBA 511, Sec-04) School of Business Independent University, Bangladesh Submitted by Name ID Farabi Ahmed 121-121-8 Marzan Bin Azad 141-067-3 MD. Shoriful Alom Sarkar 142-063-2 Date of Submission: 8 th April, 2015

-

Upload

farabi-ahmed -

Category

Data & Analytics

-

view

34 -

download

0

Transcript of RAK & Shinepukur Ceramics Working-Capital Structure.

1 | P a g e

“Working Capital Management Efficiency of

Ceramics Industry in BANGLADESH”

Independent University, Bangladesh

Submitted to

Dr. Md. Abdul Hannan Mia Faculty of Financial Management (MBA 511, Sec-04)

School of Business

Independent University, Bangladesh

Submitted by

Name ID

Farabi Ahmed 121-121-8

Marzan Bin Azad 141-067-3

MD. Shoriful Alom Sarkar 142-063-2

Date of Submission: 8th April, 2015

2 | P a g e

Letter of Transmittal

8th

April, 2015.

Dr. Md. Abdul Hannan Mia

Financial Management (MBA 511, Sec-04)

Faculty Member of School of Business,

Independent University Bangladesh.

Subject: A report on Working Capital Management Efficiency of Ceramics Industry in

Bangladesh.

Dear Sir,

With due respect, I would like to inform you that I have completed report on “Working Capital

Management Efficiency of Ceramics Industry in Bangladesh”. It is immense pleasure for me

because I have successfully completed this report by receiving your continues guideline as a

supervisor.

I have endeavored to prepare this report from my level of best to accumulate relevant &

insightful information. If I am included any wrong information in unconsciously so please

forgive me as your student. It is a great experience for me to make this report. I have tried to

make the report comprehensively within the schedule time & limited recourse.

You’re sincerely,

.......................................

Farabi Ahmed

Marzan Bin Azad

Md. Shoriful Alom Sarkar

3 | P a g e

Working Capital Management Efficiency Between

RAK Ceramics Limited

&

Shinepukur Ceramics Limited

4 | P a g e

Table of Contents

No Subject Page No Marks Carrying

1 Abstract 6 2

2 Introduction 6 1

3 Literature Reviews 8 – 11 5

4 Objective & Methodology 11 – 12 2

5 Data Analysis 12 – 15 5

6 Findings (with BAR chart) 15 – 18 2

7 Conclusion & Recommendations 19 1

8 References (APA format) 20 2

Total: 20 Marks

5 | P a g e

Acknowledgement

All the praise and admiration for Almighty ALLAH the most gracious, most merciful that has

enabled us for successful completion and submission of this report timely. It is indeed a great

pleasure and honor on our part to have the opportunity to submit this report.

We would like to express profound gratitude and indebtedness to our honorable supervisor “Dr.

Md. Abdul Hannan Mia.” Associate Professor, Faculty of Business Administration,

Independent University, Bangladesh, for his direct concern, professional guidance,

encouragement during our analytical work and for his critical suggestions and corrections of the

manuscript in the preparation of this report.

Finally, we would like to thank our group members for their unconditional support, without them

we would not have been able to make it this far.

6 | P a g e

1. ABSTRACT

Among all the problems of financial management, the problems of working capital management

have probably been recognized as the most crucial one. It is because of the fact that working

capital always helps a business concern to gain vitality and life strength. The objective of this

study is to critically evaluate working capital management as practiced in the selected firms of

the Ceramics Industries. To achieve this goal the study also examines the policy and practices of

cash management, evaluate the principles, procedures and techniques of inventory management,

receivable management and payable management. But the study does not examine the political

and economic impacts on the working capital management. From the analysis we can conclude

that Ceramics Industries operated in Bangladesh are efficiently deal with their liquidity

preferences and investment criteria and this is due to the competitive nature of this industry.

2. INTRODUCTION

The aim of this study is to investigate the impact of working capital policies on financial

performances in two leading ceramics industries in Bangladesh. The importance of efficient

working capital management cannot be denied in any type of business organizations. The

extensive literature indicates that it has impacts directly on corporate liquidity (Kim, Mauer and

Sherman 1998; and Opler, Pinkowitz, Stulz, and Williamson 1999) and profitability (e.g., Shin

and Soenen 1998; Deloof 2003; Lazaridis and Tryfonidis 2006).

Capital is what makes or breaks a business, and no business can run successfully without enough

capital to cover both short- and long-term needs. Maintaining sufficient levels of short-term

capital is a constantly ongoing challenge, and in today’s turbulent financial markets and

uncertain business climate external financing has become both harder and more costly to obtain.

Companies are therefore increasingly shifting away from traditional sources of external

financing and turning their eyes towards their own organizations for ways of improving liquidity.

7 | P a g e

One efficient but often overlooked way of doing so is to reduce the amount of capital tied-up in

operations, that is, to improve the working capital management of the company.

Working capital is a financial metric of operating liquidity which describes the amount of cash

tied up in operations and defines the short term condition of a company. A positive working

capital position is required for the continuous running of a company’s operations, i.e. to pay

short term debt obligations and to cover operational expenses. A company with a negative

working capital balance is unable to cover its short-term liabilities with its current assets.

The ceramics industry is a growing manufacturing sector in Bangladesh. The industry started

during the late 1950s when the first ceramic industrial plants were established. The industry

mainly produces tableware, sanitary ware and tiles. As of 2011, there were 21 ceramic industrial

units throughout Bangladesh, employing about 500,000 people. In the first nine months of the

2013-14 fiscal years, Bangladesh exported about US$36 million worth of goods after meeting

80% of the domestic demand. The main export destinations are the EU, USA and the Middle-

East.

RAK Ceramics (Bangladesh) Limited, a UAE-Bangladesh joint venture company, was

incorporated in Bangladesh on 26 November, 1998 as a private company limited by shares under

the Companies Act 1994. The name of the Company was thereafter changed to its name from

RAK Ceramics (Bangladesh) Private Limited to RAK Ceramics (Bangladesh) Limited as per

resolution passed in extraordinary general meeting on 10 June 2008, certificate issued by the

Registrar of Joint Stock Companies dated 11 February, 2009. It is engaged in manufacturing and

marketing of ceramics tiles, bathroom sets and all types of sanitary ware. It has started its

commercial production on 12 November, 2000. The core business of RAK Ceramics

(Bangladesh) Limited is to manufacture and sell of tiles and sanitary wares. The company has

over 1000 models active in the ceramic and porcelain tile business and regularly adds several

new designs to the product portfolio.

SHINEPUKUR Ceramics Limited (SCL) is a member of BEXIMCO Group which is the

Largest Private Sector Business Conglomerate in Bangladesh with about over 48,000 people

worldwide in the permanent payroll, have over 300,000 shareholders, handling a diversified

8 | P a g e

range of merchandise to and from Bangladesh. SHINEPUKUR Ceramics was registered in

Bangladesh in 1997 and the Plants were commissioned in 1998.Commercial production of

Porcelain Tableware started in April 1999 and Bone China in November 1999. SCL is located in

the BEXIMCO Industrial Park, near Dhaka Export Processing Zone (DEPZ), 40 Km from

Capital Dhaka City.

In such a context, examining the type of working capital financing policies and that of working

capital investment policies is of paramount importance in the ceramics industries in Bangladesh.

Moreover, the question of measuring the impact of these policies on the financial performances

of the firms is also imperative in the context of the sample firms.

Working capital policies are mainly of two types via; working capital investment policy and

working capital financing policy. Working capital investment policy refers to the determination

of the amount of working capital to be invested in various current assets viz; inventory, cash,

receivables, marketable securities, prepaid expenses etc. That is, the allocation of total working

capital in to the major components of working policy is known as working capital investment

policy. But working capital financing policy refers to the policy which is applied in financing the

working capital. That is, in financing the working capital whether the firm would use the hedging

policy, conservative policy or moderate policy.

3. LITERATURE REVIEWS

Kieschnick and LaPlante (2012) provide evidence linking working capital management

to shareholder wealth. They find that the incremental dollar invested in net operating capital is

less valuable than the incremental dollar held in cash for the average firm. The findings

reported in the paper further suggest that the valuation of the incremental dollar invested in net

operating working is significantly influenced by a firm’s future sales expectations, its debt load,

its financial constraints, and its bankruptcy risk.

Zubairi H. J. (2010), in his literature concluded that, a firm can enhance its profitability

9 | P a g e

either by increasing its currents assets or by reducing its current liabilities. He also mentioned

that, the firm size is found to have a significant and direct effect on profitability of automobile

firms in Pakistan. The key factor for improving industry profitability in the future appears to be

increase in capacity utilization which can be got further impetus if interest rates also decline.

Harford, Mansi, Maxwell, D’Mello, Krishnaswami and Larkin (2008) find that the availability

of external financing is a determinant of liquidity. Thus restricted access to capital markets

requires firms to hold larger cash reserves. Other studies show that firms with weaker corporate

governance structures hold smaller cash reserves. Furthermore firms with excess cash holding

as well as weak shareholder rights undertake more acquisitions.

Lazaridis D. I. and Tryfonidis M. D. (2005) mentioned that there is statistical significance

between profitability, measured through gross operating profit, and the cash conversion cycle.

Managers can create profits for their companies by handling correctly the cash conversion

cycle and keeping each different component (accounts receivables, accounts payables,

inventory) to an optimum level.

Eljelly, (2004): elucidated that efficient liquidity management involves planning and controlling

current assets and current liabilities in such a manner that eliminates the risk of inability to meet

due short-term obligations and avoids excessive investment in these assets. The relation between

profitability and liquidity was examined, as measured by current ratio and cash gap (cash

conversion cycle) on a sample of joint stock companies in Saudi Arabia using correlation and

regression analysis. The study found that the cash conversion cycle was of more importance as a

measure of liquidity than the current ratio that affects profitability. The size variable was found

to have significant effect on profitability at the industry level. The results were stable and had

important implications for liquidity management in various Saudi companies. First, it was clear

that there was a negative relationship between profitability and liquidity indicators such as

current ratio and cash gap in the Saudi sample examined. Second, the study also revealed that

there was great variation among industries with respect to the significant measure of liquidity.

Deloof, (2003): discussed that most firms had a large amount of cash invested in working capital.

It can therefore be expected that the way in which working capital is managed will have a

significant impact on profitability of those firms. Using correlation and regression tests he found

a significant negative relationship between gross operating income and the number of days

accounts receivable, inventories and accounts payable of Belgian firms. On basis of these results

10 | P a g e

he suggested that managers could create value for their shareholders by reducing the number of

days’ accounts receivable and inventories to a reasonable minimum. The negative relationship

between accounts payable and profitability is consistent with the view that less profitable firms

wait longer to pay their bills.

Ghosh and Maji, (2003): in this paper made an attempt to examine the efficiency of working

capital management of the Indian cement companies during 1992 – 1993 to 2001 – 2002. For

measuring the efficiency of working capital management, performance, utilization, and overall

efficiency indices were calculated instead of using some common working capital management

ratios. Setting industry norms as target-efficiency levels of the individual firms, this paper also

tested the speed of achieving that target level of efficiency by an individual firm during the

period of study. Findings of the study indicated that the Indian Cement Industry as a whole did

not perform remarkably well during this period.

Kim, Mauer and Sherman (1998) and Opler, Pinkowitz, Stulz, Williamson (1999), Chiou et al.

(2006) and D’Mello, Krishnaswami and Larkin (2008) find that the availability of external

financing is a determinant of liquidity. Thus restricted access to capital markets requires firms to

hold larger cash reserves.

Osisioma (1997) defines proper working capital management as “the regulation, adjustment, and

control of the balance of current assets and current liabilities of a firm such that maturing

obligations are met, and the fixed assets are properly serviced”

Smith and Begemann (1997): emphasized that those who promoted working capital theory

shared that profitability and liquidity comprised the salient goals of working capital

management. The problem arose because the maximization of the firm's returns could seriously

threaten its liquidity, and the pursuit of liquidity had a tendency to dilute returns.

Shin and Soenen, (1998): highlighted that efficient Working Capital Management was very

important for creating value for the shareholders. The way working capital was managed had a

significant impact on both profitability and liquidity. The relationship between the length of Net

Trading Cycle, corporate profitability and risk adjusted stock return was examined using

correlation and regression analysis, by industry and capital intensity. They found a strong

11 | P a g e

negative relationship between lengths of the firm’s net-trading Cycle and its profitability. In

addition, shorter net trade cycles were associated with higher risk adjusted stock returns.

4. Objectives and Methodology

4.1 Objectives

The study aimed at the following objectives which were the questions whose answers we were

investigating throughout the paper:

To identify the existing short term financial objectives and policies of RAK Ceramics

and SHINEPUKUR Ceramics

To examine the factors influencing inventory, receivables and cash policies in the sample

firms

To analyze the actual positions of the working capital in the sample firms during the

study period 2010 to 2012.

To evaluate the working capital financing and investment patterns in the sample firms

in order to measure the effectiveness of the working capital policies during the study

period

To measure the relationship as well as impact of working capital policies on

financial performances measured in terms of Return on Equity (ROE).

4.2 Methodology

4.2.1 Target Population

The target population for fulfilling the objectives was the two leading ceramics Companies

operating in Bangladesh which are enlisted in Dhaka Stock Exchange.

4.2.2 Sample Size

12 | P a g e

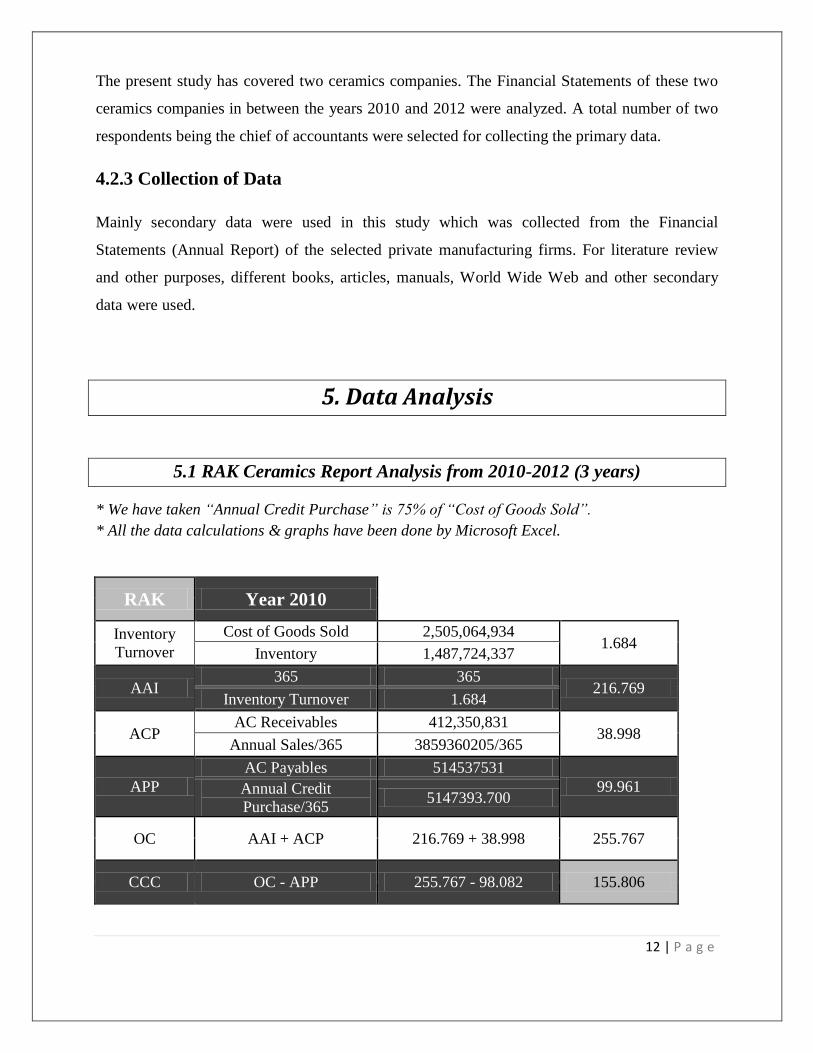

The present study has covered two ceramics companies. The Financial Statements of these two

ceramics companies in between the years 2010 and 2012 were analyzed. A total number of two

respondents being the chief of accountants were selected for collecting the primary data.

4.2.3 Collection of Data

Mainly secondary data were used in this study which was collected from the Financial

Statements (Annual Report) of the selected private manufacturing firms. For literature review

and other purposes, different books, articles, manuals, World Wide Web and other secondary

data were used.

5. Data Analysis

5.1 RAK Ceramics Report Analysis from 2010-2012 (3 years)

* We have taken “Annual Credit Purchase” is 75% of “Cost of Goods Sold”.

* All the data calculations & graphs have been done by Microsoft Excel.

RAK Year 2010

Inventory

Turnover

Cost of Goods Sold 2,505,064,934 1.684

Inventory 1,487,724,337

AAI 365 365

216.769 Inventory Turnover 1.684

ACP AC Receivables 412,350,831

38.998 Annual Sales/365 3859360205/365

APP

AC Payables 514537531

99.961 Annual Credit

Purchase/365 5147393.700

OC AAI + ACP 216.769 + 38.998 255.767

CCC OC - APP 255.767 - 98.082 155.806

13 | P a g e

RAK Year 2011

Inventory

Turnover

Cost of Goods Sold 2,693,596,290 1.625

Inventory 1,658,062,569

AAI 365 365

224.678 Inventory Turnover 1.625

ACP AC Receivables 21,322,847

32.524 Annual Sales/365 239,296,253/365

APP

AC Payables 306963146

55.461 Annual Credit

Purchase/365 5534786.897

OC AAI + ACP 224.684 + 32.524 257.202

CCC OC - APP 257.529 - 1.679 201.742

RAK Year 2012

Inventory

Turnover

Cost of Goods Sold 2,979,160,088 1.676

Inventory 1,777,888,718

AAI 365 365

217.823 Inventory Turnover 1.676

ACP AC Receivables 21,836,636

29.176 Annual Sales/365 273183325/365

APP

AC Payables 197523746

32.267 Annual Credit

Purchase/365 6121561.825

OC AAI + ACP 106.859 + 29.176 246.999

CCC OC - APP 136.034 - 97.112 214.732

14 | P a g e

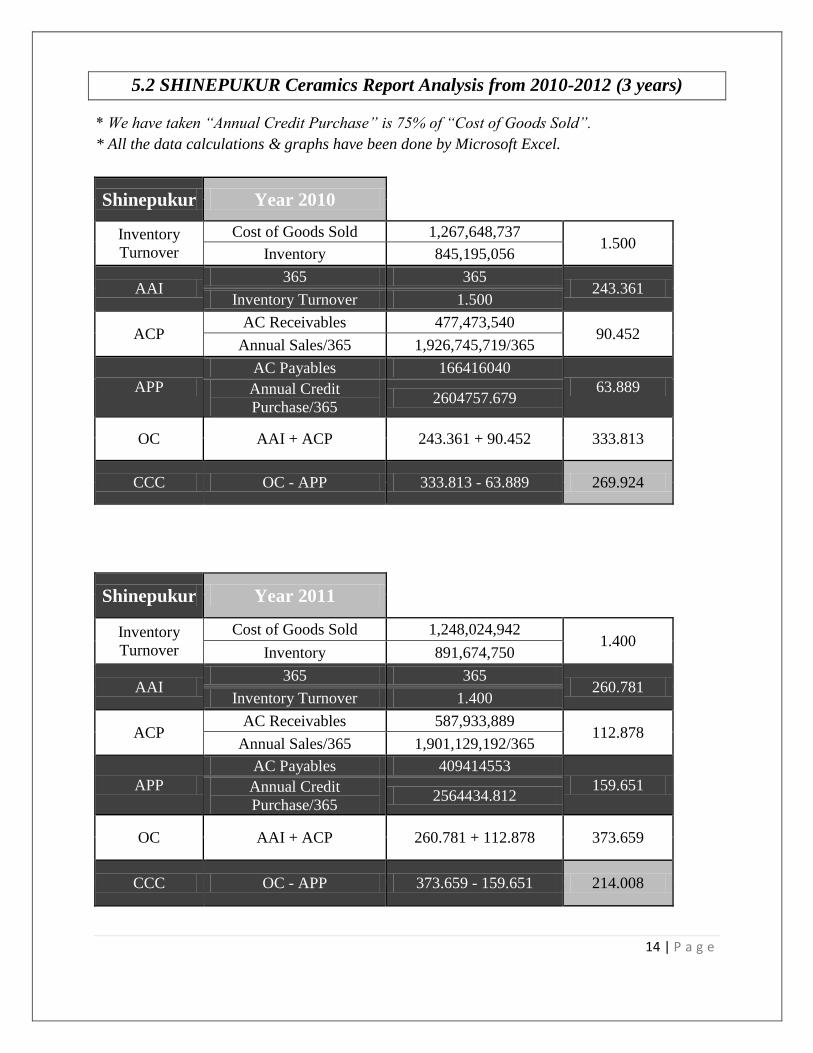

5.2 SHINEPUKUR Ceramics Report Analysis from 2010-2012 (3 years)

* We have taken “Annual Credit Purchase” is 75% of “Cost of Goods Sold”.

* All the data calculations & graphs have been done by Microsoft Excel.

Shinepukur Year 2010

Inventory

Turnover

Cost of Goods Sold 1,267,648,737 1.500

Inventory 845,195,056

AAI 365 365

243.361 Inventory Turnover 1.500

ACP AC Receivables 477,473,540

90.452 Annual Sales/365 1,926,745,719/365

APP

AC Payables 166416040

63.889 Annual Credit

Purchase/365 2604757.679

OC AAI + ACP 243.361 + 90.452 333.813

CCC OC - APP 333.813 - 63.889 269.924

Shinepukur Year 2011

Inventory

Turnover

Cost of Goods Sold 1,248,024,942 1.400

Inventory 891,674,750

AAI 365 365

260.781 Inventory Turnover 1.400

ACP AC Receivables 587,933,889

112.878 Annual Sales/365 1,901,129,192/365

APP

AC Payables 409414553

159.651 Annual Credit

Purchase/365 2564434.812

OC AAI + ACP 260.781 + 112.878 373.659

CCC OC - APP 373.659 - 159.651 214.008

15 | P a g e

Shinepukur Year 2012

Inventory

Turnover

Cost of Goods Sold 1,268,312,998 1.501

Inventory 845,059,407

AAI 365 365

243.194 Inventory Turnover 1.501

ACP AC Receivables 853,413,145

160.371 Annual Sales/365 1,942,350,752/365

APP

AC Payables 445028986

170.763 Annual Credit

Purchase/365 2606122.599

OC AAI + ACP 243.194 + 160.371 403.565

CCC OC - APP 403.565 - 170.763 232.802

6. Findings (with BAR chart)

6.1 Average Age of Inventory (AAI):

16 | P a g e

Above from the analysis we find out that, In 2010 SHINEPUKUR’s “Avg. Age of Inventory”

was 243.361 days where RAK was 216.769 days, In 2011 SHINEPUKUR was 260.781 days

where RAK was 224.684 days, and In 2012 SHINEPUKUR was 243.194 days where RAK was

217.823 days.

So, RAK is performing better than SHINEPUKUR all those 3 years.

6.2 Average Collection Period (ACP):

Above from the analysis we find out that, In 2010 SHINEPUKUR’s “Avg. Collection Period”

was 90.452 days where RAK was 38.998 days, In 2011 SHINEPUKUR was 112.878 days

where RAK was 32.524 days, and In 2012 SHINEPUKUR was 160.371 days where RAK was

29.176 days.

So, RAK is performing very much better than SHINEPUKUR. Their performance of

“Collections” gradually increases.

17 | P a g e

6.3 Average Payment Period (APP):

Above from the analysis we find out that, In 2010 SHINEPUKUR’s “Avg. Payment Period”

was 63.889 days where RAK was 99.961 days, In 2011 SHINEPUKUR was 159.651 days

where RAK was 55.461 days, and In 2012 SHINEPUKUR was 170.763 days where RAK was

32.267 days.

So, SHINEPUKUR was performed better than RAK in 2010. But after 2010 they had gradually

fallen down. RAK was start performing too much better than SHINEPUKUR from 2011. In

2012 their performance is huge better that SHINEPUKUR for Paying Payment.

6.4 Operating Cycle (OC):

18 | P a g e

Above from the analysis we find out that, In 2010 SHINEPUKUR’s “Operating Cycle” was

333.813 days where RAK was 255.767 days, In 2011 SHINEPUKUR was 373.659 days where

RAK was 257.202 days, and In 2012 SHINEPUKUR was 403.565 days where RAK was

246.999 days.

So, SHINEPUKUR was performed lower and lower year by year on those 3 years than RAK.

They were taking long time for OC. But on the other hand RAK’s OC performance gradually

increases. They complete their Operating Cycle in short time than SHINEPUKUR.

6.5 Cash Conversion Cycle (CCC):

Above from the analysis we find out that, In 2010 SHINEPUKUR’s “Cash Conversion Cycle”

was 269.924 days where RAK was 155.806 days, In 2011 SHINEPUKUR was 214.008 days

where RAK was 201.742 days, and In 2012 SHINEPUKUR was 214.732 days where RAK was

232.802 days.

So, SHINEPUKUR was performed better than RAK in year 2010. But on next year their CCC

got increased gradually which is not good at all. On the other hand CCC of RAK was not good

than SHINEPUKUR in 2010, but from 2011 they come back to the track and gradually

decreases there CCC timing and on 2012 they stand far better that SHINEPUKUR for CCC.

## So, RAK is much better than SHINEPUKUR.

19 | P a g e

7. Conclusion & Recommendations

Working capital management is important part in firm financial management decision.

The ability of the firm to operate continuously for longer period depends on how they deal with

working capital. The optimal level of working capital management is could be achieve by firm

that manage the tradeoff between profitability and liquidity.

We have done our analysis is all efficiency measures Average Age of Inventory (AAI),

Average Collection Period (ACP), Average Payment Period (APP), Operating Cycle (OC)

& Cash Conversion Cycle (CCC) .The RAK Ceramics Ltd are significant increase in Accounts

Receivables and Accounts Payable in days compare than Shinepukur Ceramics Ltd. The

Shinepukur Ceramics Ltd also increases some measures such as in 2010 their AAI ratio was

good. But their increasing point is not betters then the RAK Ceramics Ltd.

So, at last we want to say after the all sort of CCC analysis that RAK CERAMICS LTD was

performed really better in SHINEPUKUR CERAMICS LTD in 2010, 2011, 2012.

20 | P a g e

8. References (APA format)

1. Annual Reports (2010, 2011, 2012) of RAK Ceramics Ltd. Available at

http://rakcerambd.com/investors_anual.php

2. Annual Reports (2010, 2011, 2012) of Shinepukur Ceramics Ltd. Available at

http://www.shinepukur.com/index.php?p=inv_annual

3. Deloof, M. (2003). Does working capital management affect profitability of Belgian

firms? Journal of Business Finance & Accounting 30 (4), pp. 573-587.

4. Gitman & Zutter (Eds .). (2014), Principal of Managerial Finance, 13th

Edition, Boston,

United States: Pearson.

5. Harford, J. (1999). Corporate cash reserves and acquisitions. Journal of Finance 54, pp.

1969–1997.

6. Kieschnick, Robert L., Laplante, Mark and Moussawi, Rabih, Working Capital

Management and Shareholder Wealth (April 27, 2012). Available at

SSRN:http://ssrn.com/abstract=1431165 or http://dx.doi.org/10.2139/ssrn.1431165.

7. Kim, Chang-Soo, David Mauer, and Ann Sherman, 1998, the determinants of corporate

liquidity: Theory and evidence, Journal of Financial and Quantitative Analysis 33, 335-

359.

8. Opler, Tim, Lee Pinkowitz, René Stulz, and Rohan Williamson, 1999, The determinants

and implications of corporate cash holdings, Journal of Financial Economics 52, 3-46.

9. Shin, Hyun-Han, and René Stulz, 1998, Are internal capital markets efficient? Quarterly

Journal of Economics 113, 531-552.

10. Zubairi, H. J. (2010), Impact of working capital management and capital structure

on profitability of automobile firms in Pakistan, www.ssrn.com.