Railroad 101 & The Port and Railroad Relationship gravity due to the presence of a high proportion...

38

Presentation to Association of Pacific Ports, 2015 Winter Conference Lihue, Hawaii Eric B. Winters, P.E. T.Y. Lin International Railroad 101 & The Port and Railroad Relationship January 17 th , 2015

Transcript of Railroad 101 & The Port and Railroad Relationship gravity due to the presence of a high proportion...

Presentation to

Association of Pacific Ports, 2015 Winter Conference

Lihue, Hawaii

Eric B. Winters, P.E.

T.Y. Lin International

Railroad 101 &

The Port and

Railroad

Relationship

January 17th, 2015

Brief History of

Railroads

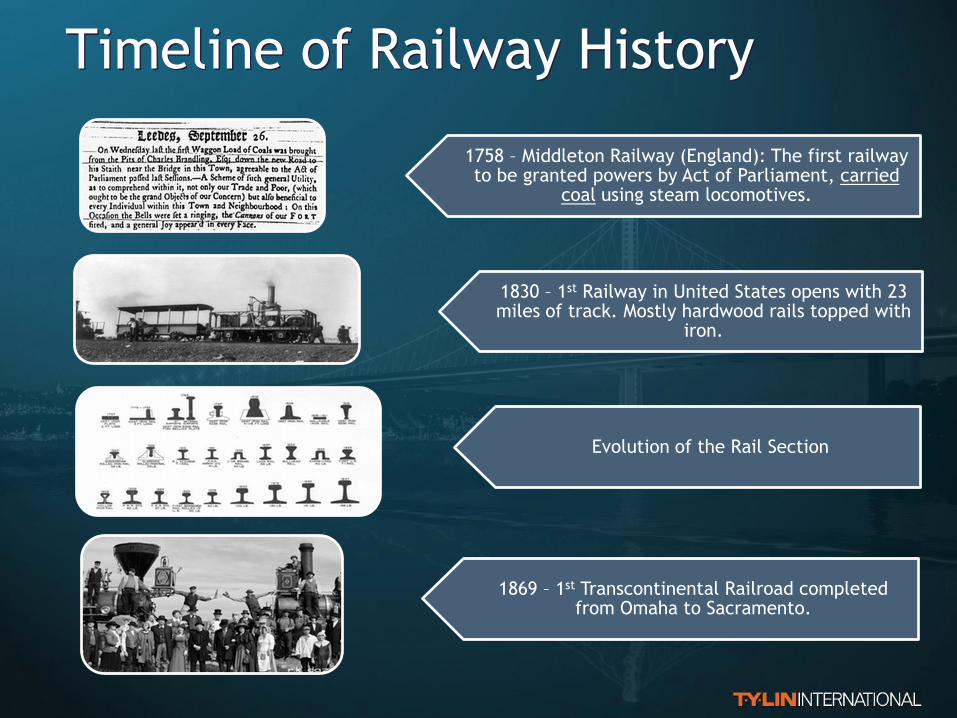

Timeline of Railway History

1758 – Middleton Railway (England): The first railway to be granted powers by Act of Parliament, carried

coal using steam locomotives.

1830 – 1st Railway in United States opens with 23 miles of track. Mostly hardwood rails topped with

iron.

Evolution of the Rail Section

1869 – 1st Transcontinental Railroad completed from Omaha to Sacramento.

Timeline of Railway History (cont)

1937-41 - Magnetic levitation (maglev) train patents awarded in Germany to Hermann Kemper, with design

propelled by linear motors.

1946 - U.S. railroads begin rapidly replacing their rolling stock with diesel-electric units. Process not completed

until the mid 1960s.

1950s and 1960s: Drastic decline in passenger travel in the United States, due to automobiles and also airplanes.

1980 Staggers Act – Federal Law that reduced federal regulation of railroads

Capacity and Investment

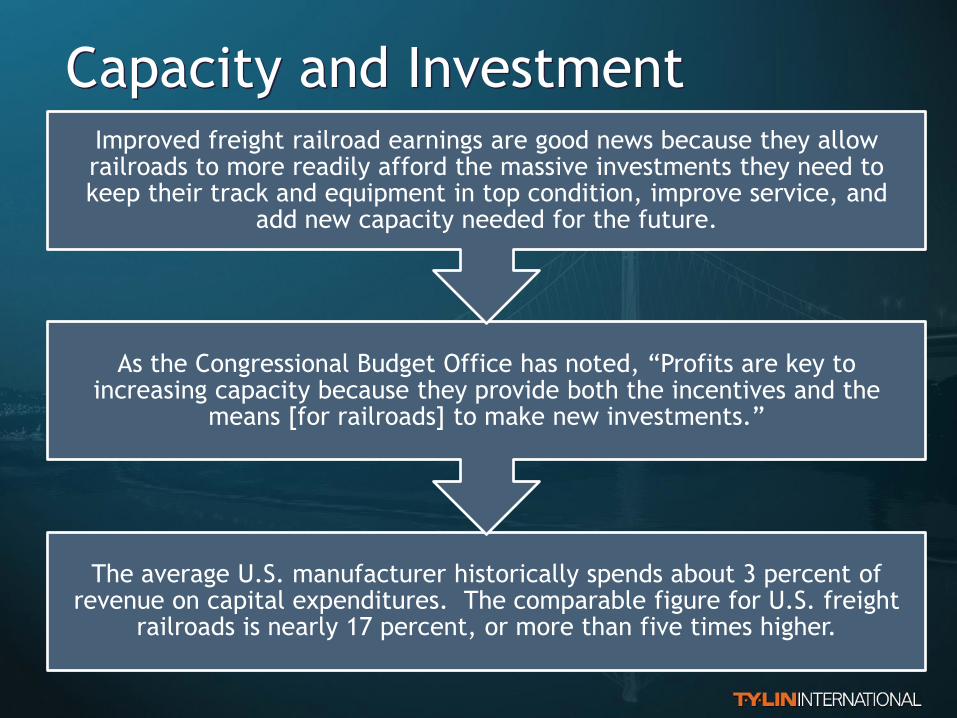

The average U.S. manufacturer historically spends about 3 percent of revenue on capital expenditures. The comparable figure for U.S. freight

railroads is nearly 17 percent, or more than five times higher.

As the Congressional Budget Office has noted, “Profits are key to increasing capacity because they provide both the incentives and the

means [for railroads] to make new investments.”

Improved freight railroad earnings are good news because they allow railroads to more readily afford the massive investments they need to keep their track and equipment in top condition, improve service, and

add new capacity needed for the future.

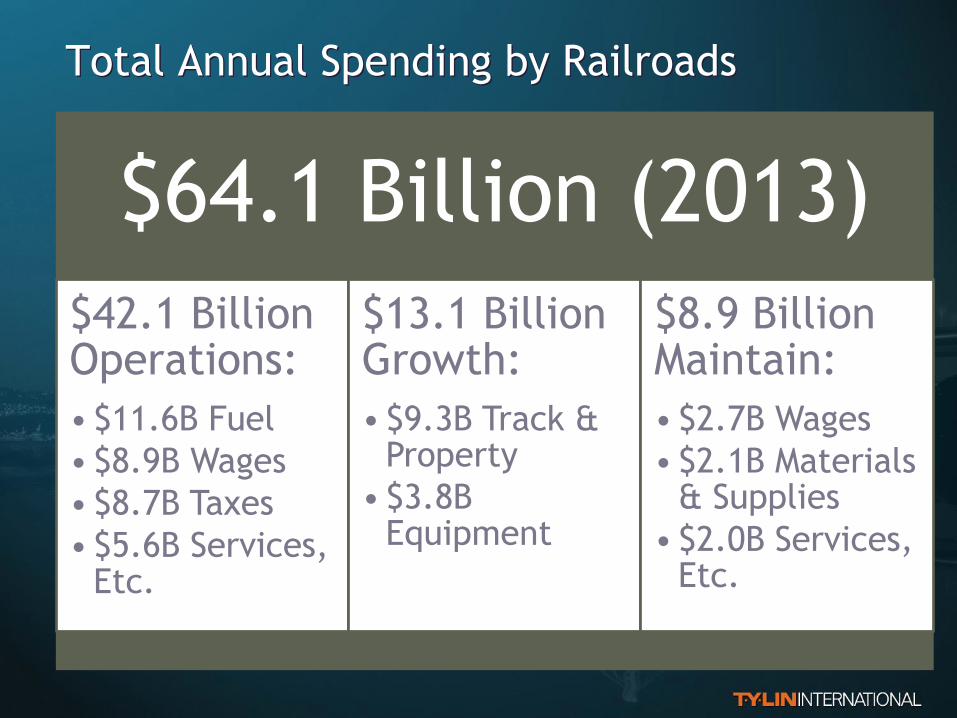

Total Annual Spending by Railroads

$64.1 Billion (2013)

$42.1 Billion Operations:

• $11.6B Fuel

• $8.9B Wages

• $8.7B Taxes

• $5.6B Services, Etc.

$13.1 Billion Growth:

• $9.3B Track & Property

• $3.8B Equipment

$8.9 Billion Maintain:

• $2.7B Wages

• $2.1B Materials & Supplies

• $2.0B Services, Etc.

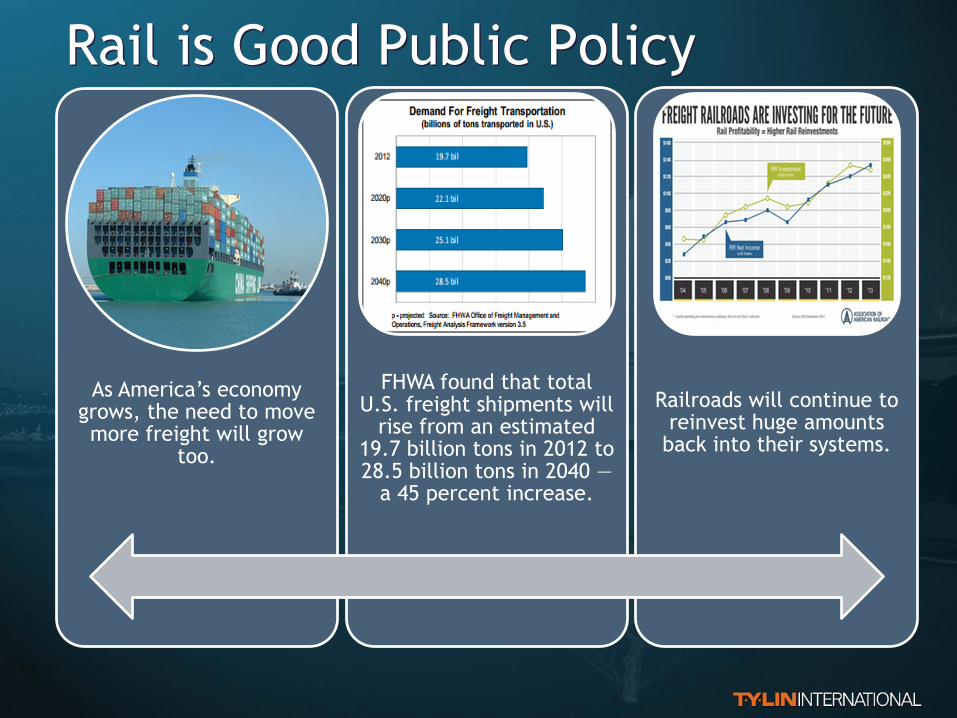

Rail is Good Public Policy

As America’s economy grows, the need to move more freight will grow

too.

FHWA found that total U.S. freight shipments will

rise from an estimated 19.7 billion tons in 2012 to 28.5 billion tons in 2040 —

a 45 percent increase.

Railroads will continue to reinvest huge amounts

back into their systems.

How can Policymakers Help?

Keep reasonable regulation.

Engage in public-private partnerships.

Retain existing truck size and weight limits.

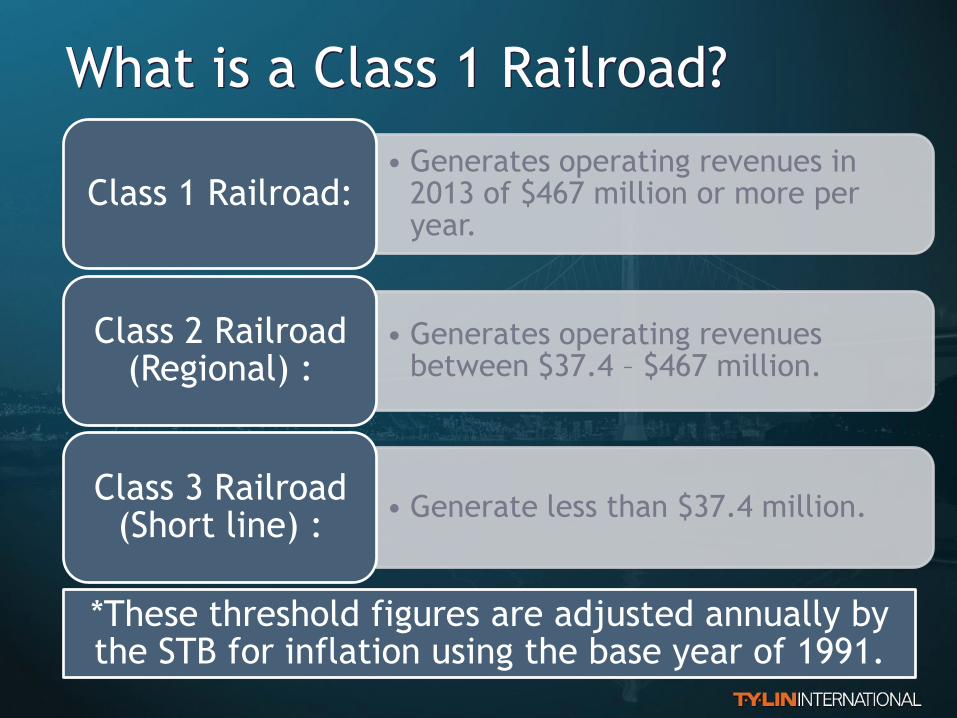

• Generates operating revenues in 2013 of $467 million or more per year.

Class 1 Railroad:

• Generates operating revenues between $37.4 – $467 million.

Class 2 Railroad (Regional) :

• Generate less than $37.4 million. Class 3 Railroad

(Short line) :

*These threshold figures are adjusted annually by the STB for inflation using the base year of 1991.

What is a Class 1 Railroad?

2014 Freight by Volume

• 17.0 million units Trailers & Containers

• 6.3 million carloads Coal

• 2.2 million carloads Chemicals

• 1.3 million carloads Autos

• 1.6 million carloads Grain

• 1.2 million carloads Petroleum

*As reported by the AAR

Ports and the

Railroad

Relationship

OEM Operations

Engineering

Maintenance

Intermodal/Container Yards

Massive overhead container cranes.

Straddle cranes or side loaders.

Support/storage tracks.

Parking/storage areas.

Gate areas.

Coal

In 2013, energy sources & percent share of electricity generation in the United States were

Coal 39% Natural Gas

27% Nuclear 19%

Hydropower 7%

Renewable 6%

Projections estimate demand for coal will increase 21% by 2030; therefore hauling coal will continue to play a major

role in the future of the Railroad Industry.

No single commodity is more important to America’s railroads than coal.

Coal Facilities

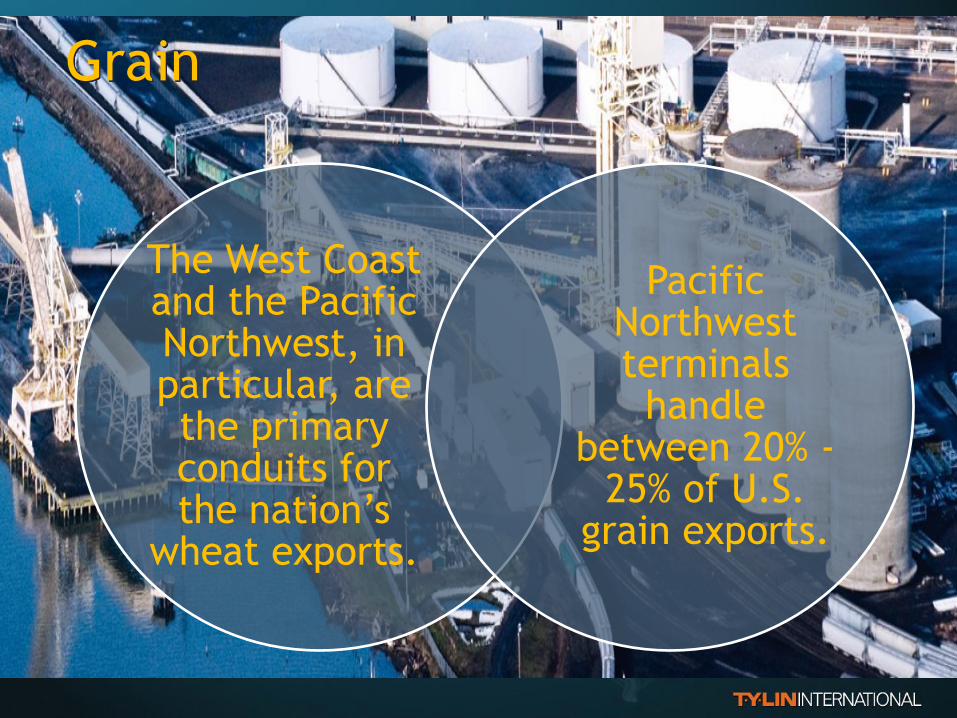

Grain

The West Coast and the Pacific Northwest, in particular, are the primary conduits for the nation’s

wheat exports.

Pacific Northwest terminals handle

between 20% - 25% of U.S.

grain exports.

Railroad Operations that affect design

Port and Terminal Operators should

have a basic understanding of the railroad operations when receiving and handling railroad

cars including

Type, Size, and Number of cars to be delivered.

How the cars will be handled

within the terminal

How the cars should be assembled for pickup.

What is the position of the train prior to

departure?

Is the terminal the

origin of train?

Time needed for

inspections (air test)

Will any maintenance

be performed at the terminal.

Track Design Criteria that affects footprint

Facility Footprint

Maximum Horizontal Curvature

Maximum Grade & Vertical Rate of Change

Track Centers

Walkways (No.1 & No.2)

Access Roads

(Railroad & Port Staff)

Crossings (Not

public)

Each Railroad will have its own Design Criteria, e.g.

•BNSF Guideline for Industrial Track Projects, (DGFITP).

•UPRR/BNSF Common Standards for Grade Separations.

•UPRR/BNSF Common Standards for turnouts.

Railroad Design Criteria

Walkways & Track Sections

Alternatives Development Phase Include car spot detail showing train car positions during

arrival & departure; including the locomotive units. Count the number of cars shown to verify capacity requirements.

Review construction phasing per alternative before

selecting preferred alternative including; Construction staging areas.

Haul roads within the terminal.

Demolition phase.

Areas of impact per phase.

Duration of each phase.

Must identify impacts to existing operations

An Alternative is NOT valid until the impacts of

construction are identified, evaluated and accepted.

Constructability (a part of Engineering)

Constructability (or buildability), the integration of

construction expertise into all phases of a project.

DON’T WAIT UNTIL PRE-CONSTRUCTION.

Can benefit cost, schedule, quality, and other key

objectives of the project.

Constructability is not just review of completed

drawings; it is not criticism of the designer; nor is it

optimizing construction at the expense of other

activities. Constructability involves thinking about how

to build a project even before it is designed..

Owners need to be aware of the impacts to their existing

facilities and operations during construction in order to

evaluate the true costs of construction.

Vancouver Wharves

Port of Vancouver, Washington

WVFA Project 2 — Utility Relocation

WVFA Projects 4 and 7 — Relocation of the Bulk Unloading Facility

WVFA Project 5 — Property Acquisition

WVFA Project 6 — Terminal 3 Rail Access

WVFA Project 8 — Grain Subdivision Phase B

WVFA Project 9 — Grain Track Unit Train Improvements Phase A

WVFA Project 10 — Bulk Facility/Subaru Track Relocation

WVFA Project 11 — Grain Track Unit Train Improvements Phase B

WVFA Project 12 — Grain Track Unit Train Improvements Phase C

WVFA Projects 13, 14 and 15 — Malting Facility Relocation

WFVA Project 19 — Gateway Avenue Overpass

WVFA Project 20 — BNSF Construction and Maintenance Agreement

Port of Long Beach

Port of Los Angeles

Maintenance

All facilities require maintenance, Railroad facilities are

no different.

FRA Code of Federal Regulations (CFR) Title 49, Part

213, Subpart 233 – Track Inspections Tracks other than Main & Sidings require Monthly inspections with at

least 20 calendar days between inspections.

Include agreements for inspections and maintenance of

track owned by the Port.

Conclusions

OEM: Communication – Communication – Communication

Operations

• Train movements (arrival , internal & departure), train position.

• Required railroad procedures at the terminal; air & brake tests, car inspection, bad orders & maintenance. (Fueling?)

• Port operations around railcars

• Emergency procedures

Engineering

• Track geometry & track centers

• Walkways & Access Roads

• Lighting for nighttime operations

• Yard Air

• Crossings

• Constructability

Maintenance

• Who is inspecting, and who is maintaining.

Questions

Contact Information:

Eric B. Winters, P.E.

15440 Laguna Canyon Road

Suite 270

Irvine, CA 92618

Email: [email protected]

Mahalo for your time and attention!

Additional Information

Where do we get our Coal?

Appalachian Region (West Virginia & Pennsylvania) 25%

Interior Region (Illinois & Kentucky) 17%

Western Region (Wyoming) 58%

The Powder River Basin (PRB) is an area in southeast Montana and northeast Wyoming known for its natural coal deposits.

Powder River Basin coal is low-sulfur, subbituminous coal. While it contains 15 times less sulfur than Eastern (Appalachian) coal, it also has fewer Btu’s of energy or a lower “heat rate,” which means that coal-fired power plants need to burn nearly 50 percent more of it to match the power output from Eastern coal.

Power River Basin

Cool Coal Facts

There are currently plans to develop the largest coal

export facility in North America at Cherry Point, in

northwest Washington state.

Coal mined from the Powder River Basin would be

hauled by trains along BNSF rail lines.

The coal train corridor extends from mines in Montana

and Wyoming through Sandpoint, Idaho to Spokane,

down through the Columbia River Gorge, then up along

the Puget Sound coast, passing through Longview,

Tacoma, Seattle, Edmonds, Everett, Mt. Vernon,

Bellingham, Ferndale and all points in between.

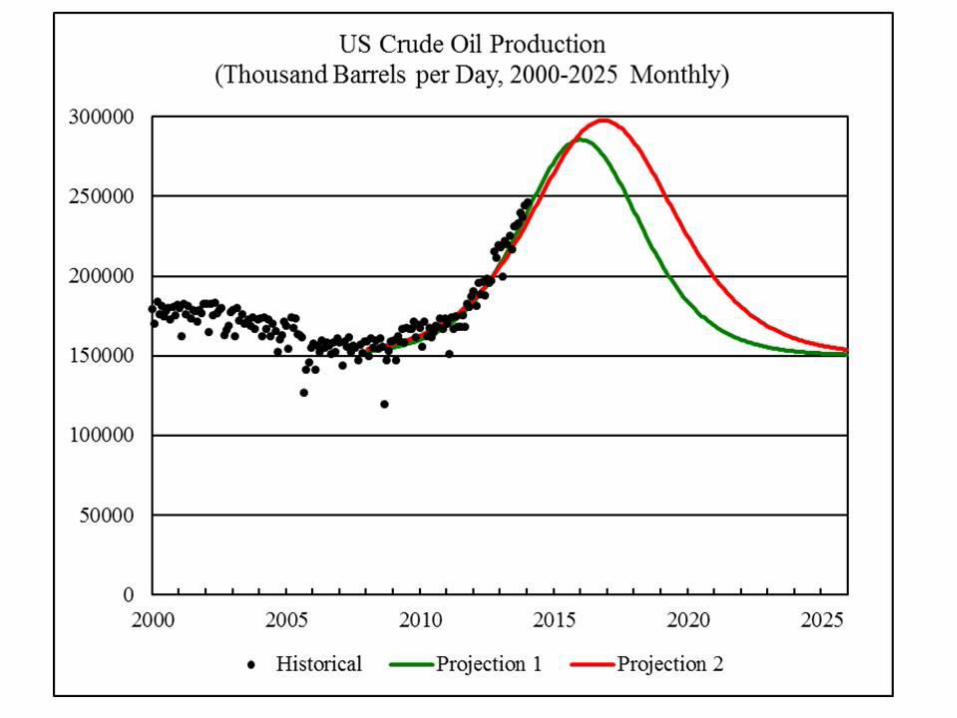

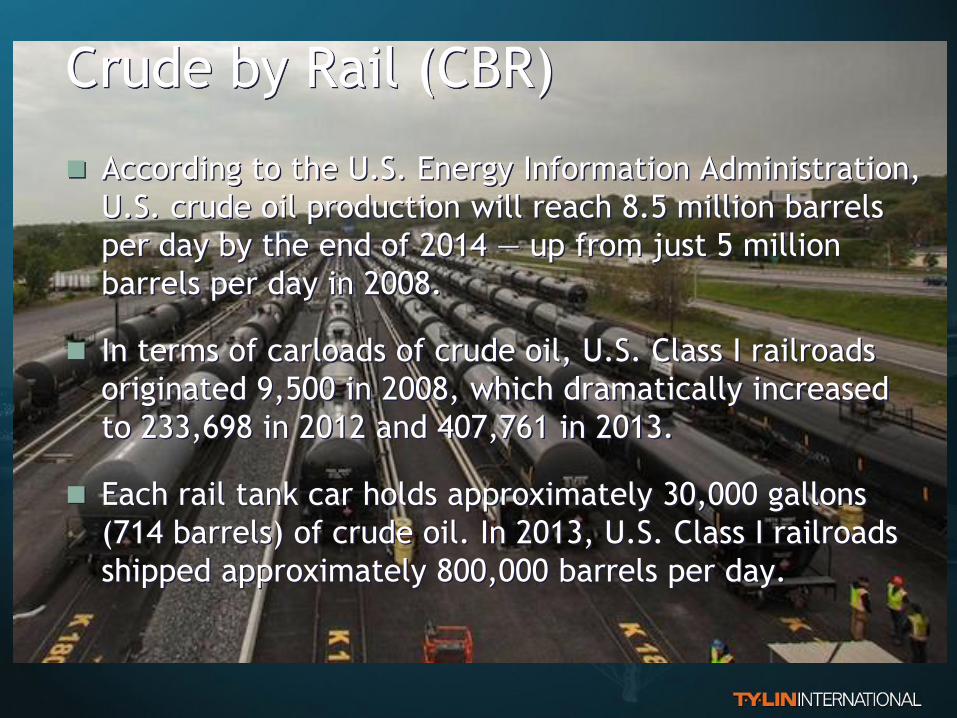

Crude by Rail (CBR)

According to the U.S. Energy Information Administration,

U.S. crude oil production will reach 8.5 million barrels

per day by the end of 2014 — up from just 5 million

barrels per day in 2008.

In terms of carloads of crude oil, U.S. Class I railroads

originated 9,500 in 2008, which dramatically increased

to 233,698 in 2012 and 407,761 in 2013.

Each rail tank car holds approximately 30,000 gallons

(714 barrels) of crude oil. In 2013, U.S. Class I railroads

shipped approximately 800,000 barrels per day.

Crude Oil: Light or Heavy?

Light crude oil is liquid petroleum that has a low

density and flows freely at room temperature. It has a low viscosity, low specific gravity and high

API gravity due to the presence of a high proportion

of light hydrocarbon fractions.

It generally has a low wax content.

Light crude oil receives a higher price than heavy

crude oil on commodity markets because it produces

a higher percentage of gasoline and diesel fuel when

converted into products by an oil refinery.

Crude Oil: Sweet vs. Sour The terms sweet and sour are a reference to the sulfur content of crude oil.

Early prospectors would taste oil to determine its quality, with low sulfur oil

actually tasting sweet.

Sweet Crude

Sweet Crude is currently considered sweet if it contains less than 0.5%

sulfur.

Sweet crude is easier to refine and safer to extract and transport than sour

crude. Because sulfur is corrosive, light crude also causes less damage to

refineries and thus results in lower maintenance costs over time. Due to all

these factors, sweet crude commands up to a $15 dollar premium per barrel

over sour.

Major locations where sweet crude is found include the Appalachian Basin

in Eastern North America, Western Texas, the Bakken Formation of North

Dakota and Saskatchewan, the North Sea of Europe, North Africa, Australia,

and the Far East including Indonesia.

Sweet vs. Sour Crude Oil

Sour Crude

Sour crude oil will have greater than 0.5% sulfur and some of this will be in

the form of hydrogen sulfide. Sour crude also contains more carbon dioxide.

Most sulfur in crude is actually bonded to carbon atoms, nevertheless, high

quantities of hydrogen sulfide in sour crude can pose serious health

problems or even be fatal.

Hydrogen sulfide is famous for its “rotten egg” smell, which is only noticed

at low concentrations.

At moderate concentrations, hydrogen sulfide can cause respiratory and

nerve damage. At high concentrations, it is instantly fatal. Hydrogen sulfide

is so much of a risk that sour crude has to be stabilized via removal of

hydrogen sulfide before it can be transported by oil tankers.

Sour crude is more common in the Gulf of Mexico, Mexico, South America,

and Canada. Crude produced by OPEC Member Nations also tends to be

relatively sour, with an average sulfur content of 1.77%.