Rabo International Advisory Services (RIAS) BV Understanding of cooperative & Lessons learned Di...

71

Rabo International Advisory Services (RIAS) BV Understanding of cooperative & Lessons learned Di Linh June 2011

-

Upload

shauna-merritt -

Category

Documents

-

view

215 -

download

1

Transcript of Rabo International Advisory Services (RIAS) BV Understanding of cooperative & Lessons learned Di...

Rabo International Advisory Services (RIAS) BV

Understanding of cooperative & Lessons learned

Di Linh June 2011

Rabo International Advisory Services (RIAS) BV

2

Content of the workshop

Opening: The project context

Part 1: Definition & objective & 7 operational principles

Part 2: Distinguishing cooperatives

Part 3: Cooperative of producers & organizational structure.

Part 4: Responsibility of DB, CB & manager

Part 5: Recognition of a cooperative

Part 6: Differences between cooperative and stock enterprise

Part 7: Differences of cooperative laws between VN & ICA

Part 8: Key success factors of a cooperative

Part 9: Three economic principles

Part 10: Capitalization & Zero Loss policies

Part 11: Business strategy of the Lam Vien cooperative

Part 12: Lessons learned

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

4

Coffee Supply Chain Vietnam

Farmer

Farmer Farmer

Collectors

Farmer

Collectors/ Processors

Processors/ Exporters

Processors

Trade Buyers

Exporters

Roasters

Rabo International Advisory Services (RIAS) BV

5

Farmers Collection & Wholesale Processors Retailers/

Exporters

Commodity Flow

Price Mechanism

Commodity Flow and Price Mechanism

Rabo International Advisory Services (RIAS) BV

6

Background of the project of Quality & Sustainability Improvement of Robusta Production & Trade

Strengthening the organizational capacity in the Vietnamese coffee sector

•improving the way farmers are organized and work together

•more efficient supply chain

•professionalization

•scale up the farmers’ capacities and reach creditworthiness

•interesting for both farmers and the international companies that process coffee

Rabo International Advisory Services (RIAS) BV

Proposed Cooperative Model

Develop a producers cooperative:– bridge the gap between the individual small farmer and

the big market

– Set up according to the requirements of industrial organization:

– maximize the market revenues for members and minimize cost of production for the members.

– be efficient and well-organized

Necessary:

– farmer members have to understand the cooperative and to comply with its business policy.

7

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

Definition

A cooperative is an autonomous association of persons united voluntarily to meet their common economic, social & cultural needs and aspirations through a jointly-owned and democratically-controlled enterprise.

(International Cooperative Alliance (ICA) - 1995)

Rabo International Advisory Services (RIAS) BV

Primary Objective

The primary objective of a cooperative is to maximize the benefits , which members derive from their business transactions with the co-operative.

(International Cooperative Alliance (ICA)

Rabo International Advisory Services (RIAS) BV

Characters of a cooperative

• An enterprise of members• Cooperate on common needs

The first objective of cooperative is to satisfy the needs of members via the economic transactions.

• Equitable distribution of surplusMembers cooperate on the equality to contribute their personal resources to the economic activities of the cooperative.

The cooperative financial resources for its activities are established from the members’ contribution .

Members are legally responsible within their financial contributions (qualifying shares). However, total assets of cooperative belong to members.

11

Rabo International Advisory Services (RIAS) BV

Seven operational principles (ICA)

The cooperative principles are guidelines by which cooperatives put their values into practice.

1. Voluntary and Open Membership

2. Democratic Member Control

3. Members’ economic Participation

4. Autonomy and Independence

5. Education, Training & Information

6. Cooperation Among Cooperatives

7. Concern for Community

Rabo International Advisory Services (RIAS) BV

Seven operational principles

1. Voluntary and Open Membership: Cooperatives are voluntary organizations, open to all persons able to use their services and willing to accept the responsibilities of membership, without gender, social, racial, political, or religious discrimination.

2. Democratic Member Control: Cooperatives are democratically controlled by their members who actively participate in setting their policies and making decisions. Men and women serving as elected representatives are accountable to membership. In primary cooperatives, members have equal voting rights (one member, one vote). The other cooperatives are also organized in a democratic maner with plural voting rights in accordance with the ratio of transactions of members to the cooperative. (proportionality principle).

(ICA)

Rabo International Advisory Services (RIAS) BV

Seven operational principles

3. Members’ economic Participation: Members contribute equitably to, and democratically control, the capital of their cooperative. At least, part of that capital is usually the common & indivisible property of the cooperative. Members allocate surpluses for some following purposes: development, reservation, benefiting members in proportion to their transactions with the cooperative, and supporting other activities approved by the membership.

4. Autonomy and Independence: Cooperatives are autonomous, self-help organizations controlled by their members. If they enter into agreements with other organizations, including governments, or raise capital from external sources, they do so on terms that ensure democratic control by their members and maintain their cooperative autonomy.

(ICA)

Rabo International Advisory Services (RIAS) BV

Seven operational principles

5. Education, Training & Information: Cooperatives provide education and training for their members, elected representatives, managers, employees. So they can contribute effectively to the development of their cooperatives. They inform the general public – particularly young people or leaders – about the nature and benefits of co-operation.

6. Cooperation Among Cooperatives: Cooperatives serve their members most effectively and strengthen the co-operative movement by working together through local, national, regional, and international structures.

7. Concern for Community: Cooperatives work for the sustainable development of their communities through policies approved by their members.

(ICA)

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

1. Distinguishing cooperatives on the basis of economic relations

Based on the economic relations between the members and their cooperative, there are 3 basic types of cooperatives

Cooperatives of consumers (cooperative supermarkets, electricity, cable, water supply..)Cooperatives of producers (agricultural products, agricultural product processing...)Cooperatives of workers (handicrafts, forestry, labor cooperatives…)

17

Rabo International Advisory Services (RIAS) BV

Differences between producers’, workers’ and consumers’cooperatives

The differences between these three types of cooperative enterprises can be illustrated using the example of a coffee processing plant.

The management goals of the plant will be differ greatly depending on whether it is owned by a coffee producers’cooperative, a consumers’ cooperative or a workers’ cooperative.

18

Rabo International Advisory Services (RIAS) BV

Distinguishing cooperatives on the basis of economic relations Cooperative of producers

If this enterprise is collectively owned by coffee producers, it will seek through its management to:

pay the highest possible price for coffee supplied by its members.

minimize its production costs at low as possible.

and maximize the selling price of its products to consumers, if market conditions allow.

19

Rabo International Advisory Services (RIAS) BV

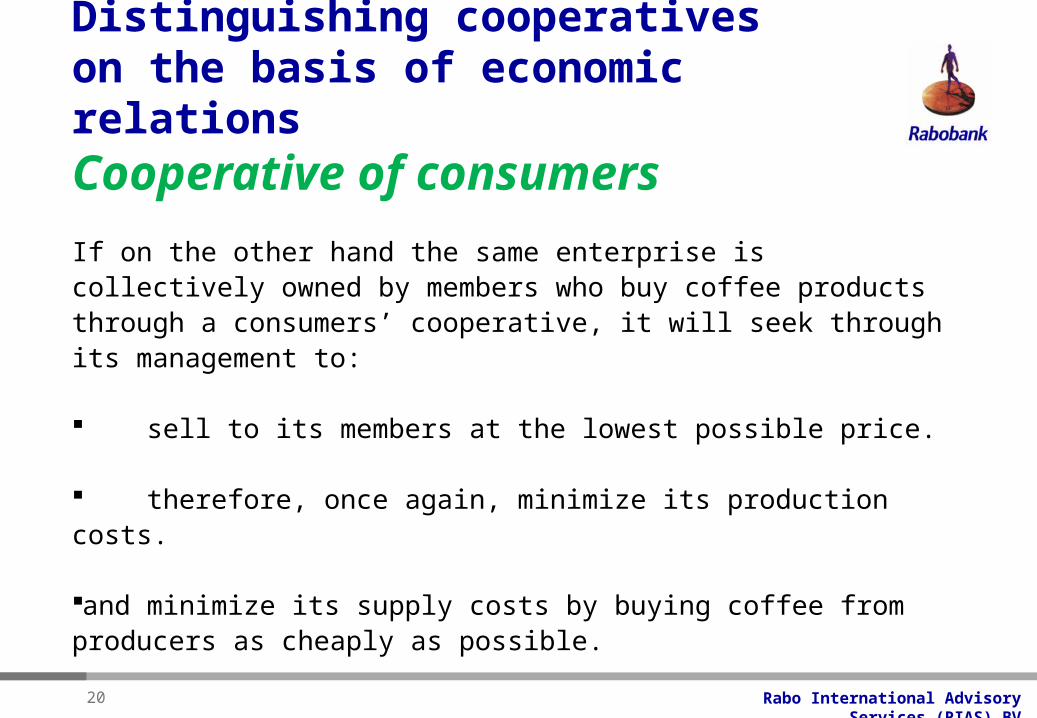

Distinguishing cooperatives on the basis of economic relations Cooperative of consumers

If on the other hand the same enterprise is collectively owned by members who buy coffee products through a consumers’ cooperative, it will seek through its management to:

sell to its members at the lowest possible price.

therefore, once again, minimize its production costs.

and minimize its supply costs by buying coffee from producers as cheaply as possible.

20

Rabo International Advisory Services (RIAS) BV

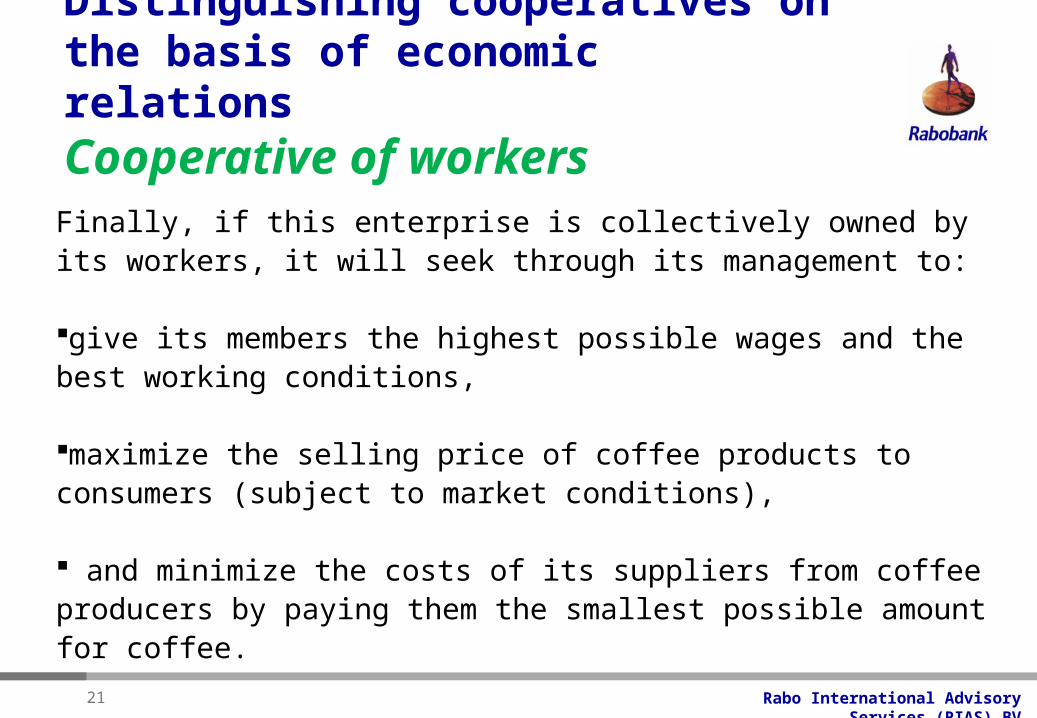

Distinguishing cooperatives on the basis of economic relations Cooperative of workersFinally, if this enterprise is collectively owned by its workers, it will seek through its management to:

give its members the highest possible wages and the best working conditions,

maximize the selling price of coffee products to consumers (subject to market conditions),

and minimize the costs of its suppliers from coffee producers by paying them the smallest possible amount for coffee.

21

Rabo International Advisory Services (RIAS) BV

2. Distinguishing cooperatives on the basis of their governance & management methods

This last typology allows a distinction to be drawn between the three major ways to experience and participate in cooperative democracy. There are accordingly three ways to govern and manage a cooperative:

1.Cooperative operation of the first type: a cooperative governed AND managed on a voluntary basis by representatives of the supplier or consumer user-members.

2.Cooperative operation of the second type: a cooperative governed voluntarily by elected representatives of the supplier or consumer user-members, BUT managed by employees.

3.Cooperative operation of the third type: governed AND managed by elected representatives of the worker member-users.

22

Rabo International Advisory Services (RIAS) BV

Distinguishing cooperatives on the basis of their governance & management methods

Coopertive of the first type

23

Elected officers

Members

Cooperative of the 1st type: The activities of the enterprise are performed on a volunteer basis by the association members

Rabo International Advisory Services (RIAS) BV

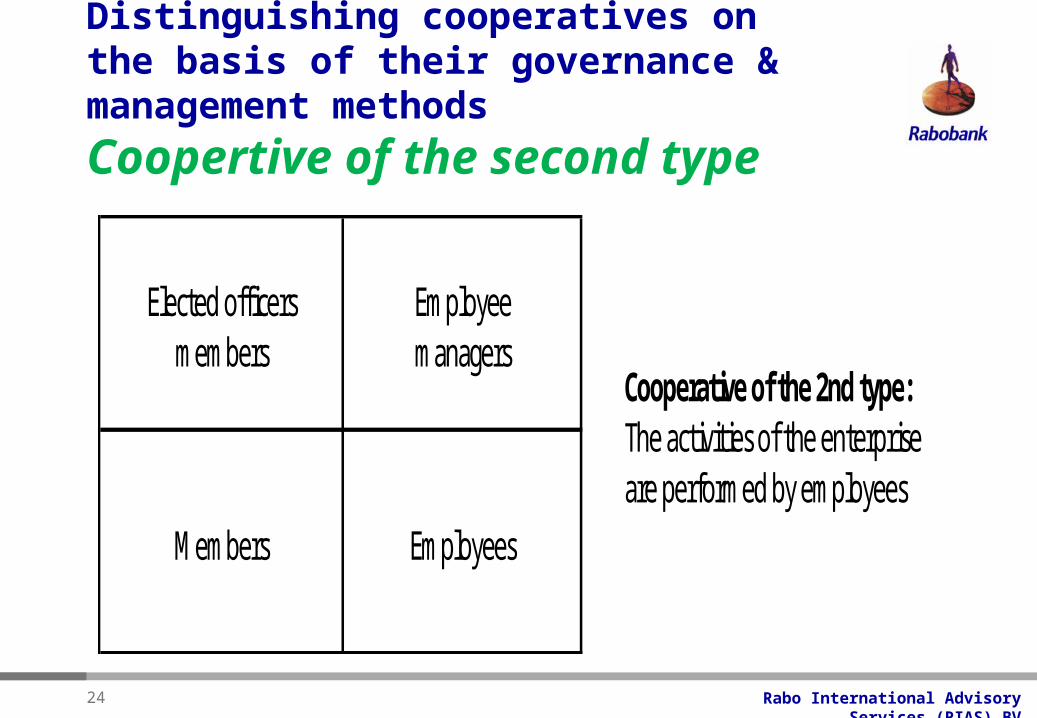

Distinguishing cooperatives on the basis of their governance & management methods

Coopertive of the second type

24

Elected officers members

Employee managers

Members Employees

Cooperative of the 2nd type: The activities of the enterprise are performed by employees

Rabo International Advisory Services (RIAS) BV

Distinguishing cooperatives on the basis of their governance & management methods

Coopertive of the third type

25

Elected officers managers members &

employees

Employee members

Cooperative of the 3rd type: (workers' cooperative) The activities of the enterprise are performed by salaried members

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

Elect

Members

MANAGEMENT

Manager

Hire

StaffServe

Hire

Control Board

RemuneratedVoluntary

Board of directors

GOVERNANCE

COOPERATIVESTRUCTURE

Rabo International Advisory Services (RIAS) BV

28

COOPERATIVE OF PRODUCERS

The cooperative is established by supplier members or consumer members. The cooperative is governed by representatives elected from members, but managed by employees.

This is the most common type, operating with a permanent work force.

Rabo International Advisory Services (RIAS) BV

29

COOPERATIVE OF PRODUCERS

These cooperatives operate with 4 types of persons making up a character of quadrilateral cooperatives, evented Henri Desroches, allows us to identify the issues affecting the relations between these four groups:

•Members: naturally, who are the cooperative’s joint owners. Members expect to maximize their interests by the economic transactions with their cooperative.

•Director Board: elected officers, who look after the interests of members.

•Senior manager (or CEO): whose mandate is to manage the cooperative in the best interests of the members.

•Employees: who provide services to the membership.

Rabo International Advisory Services (RIAS) BV

Example: Cooperative of Robusta coffee producers

If this enterprise is collectively owned by coffee producer members, it will seek, through its management, to:

•Provide technical support & inputs services to members at the lowest possible prices to help them lower their coffee production costs.

•Assist members to sell coffee at the fair price & safest to ensure the application of zero-loss policy.

• Minimize the operation costs. Sell coffee at highest prices as possible to increase the margin for the coopertive.

•Total margin (profit) of the cooperative belongs to members.

30

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

32

Statutes / Bylaws

• The Statutes are the “Civil Law” of the cooperative;

• The Statutes determine and fine-tune the respective responsibilities and duties of the cooperative organs. The Statutes are determined and changed exclusively by the General Meeting through a qualified majority;

• By-laws are auxiliary stipulations, determined by the General Meeting and subject to change by normal majority.

32

Rabo International Advisory Services (RIAS) BV

33

Responsibilities General Meeting

• Determines “will and goals” of the members;• Determines Statutes/Articles of Association, and by-laws;• Determines basic decisions, like supply contract,

financial regulations with members, etc.• Appoints, dismisses Board of Directors and Supervisory

Board;• Approves annual report and discharges Board of

Directors and Supervisory Board• Does not interfere with day-to-day operations;• Makes binding decisions at its own right, without

regression to the members-farmers; • General Meeting is based on COMMUNICATION AND

CONSENSUS building.

33

Rabo International Advisory Services (RIAS) BV

34

Responsibilities Board of Directors

• Look after the interests of members;

• Represents the cooperative in law and business matters;

• Is the policy preparing body of the cooperative;

• Is responsible to the General Meeting and Control Board;

• Appoints/dismisses and discharges the professional manager.34

Rabo International Advisory Services (RIAS) BV

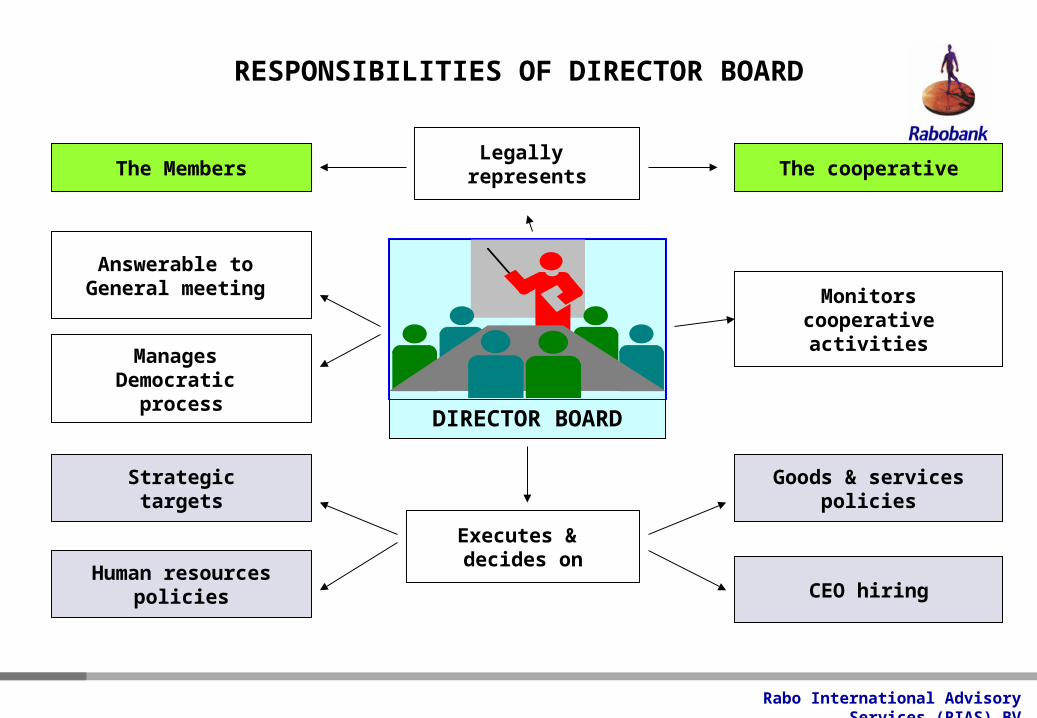

Legally represents

Answerable to General meeting

Executes & decides on

RESPONSIBILITIES OF DIRECTOR BOARD

DIRECTOR BOARD

Monitorscooperative

activities

Strategictargets

Human resourcespolicies CEO hiring

Goods & servicespolicies

The Members The cooperative

Manages Democratic

process

Rabo International Advisory Services (RIAS) BV

36

Responsibilities of Control Board

• Controls the Board of Directors’ financial performance and policy; can call in external professional auditor, legal and other experts;

• Controls the Board of Directors with regard to statutory /association matters;

• Advises the Board of Directors, on request or by own initiative.

36

Rabo International Advisory Services (RIAS) BV

37

Responsibilities of manager

• The manager is responsible to professionally administer & manage daily works of cooperative.

• Prepare the coop policies and business strategy, and implement the approved strategies via the authorization of DB;

• Be assigned & dismissed by the DB;

• Represent for the cooperative as per the authorizational levels;

• To be invited to participate in DB meetings, but is not entitled to vote.

37

Rabo International Advisory Services (RIAS) BV

Rights of members

• Member has the right to attend the cooperative general meeting & any other meeting invited by DB.

• Member has the right to use the cooperative services. Voting right is single voting or proportional voting (belonged to the cooperative statutes)

• Member can be voluntary or appointed candidate of DB election.

• Member has the right to receive “surplus distribution” from the business results, as per the proportion of business transaction with the cooperative & the rate decided by DB.

38

Rabo International Advisory Services (RIAS) BV

Responsibilities of members

• Participate in the general meeting, or other meetings organized by the cooperative.

• Priorly use the cooperative services in household production activities. E.g. I am a member of producing & trading coffee, I have responsibility to sell my coffee to the cooperative, not sell to private collectors.

• Once to be elected in the DB, member needs to carry out obligations honestly and responsibly.

• To study the laws, policies & related information, in order to understand better about the cooperative activities.

• Commit & ensure to implement the economic principles of cooperative. The most importance is the zero-loss and capitalization policies.

39

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

Cooperative recognition

Three main points distinguish cooperatives from companies:

– Method of participating in ownership;

– Method of participating in authority;

– Method of participating in business results.

Rabo International Advisory Services (RIAS) BV

Method of participating in authority

• The method of participating in the decision-making authoritiy of a cooperative is described by the rule of equal voting or proportionally plural voting.

• Participation by the member in decision-making authority is also expressed through election of a board of directors which administers the cooperative on behalf of the members and in that regard exercises the powers conferred on it by statute.

Rabo International Advisory Services (RIAS) BV

Method of participating in ownership

• The member participates in ownership of the cooperative by subscribing for a minimum number of qualifying shares defined in the cooperative’s articles and by-laws.

• These shares are registered and may not be transferred except in accordance with the terms and conditions prescribed in the cooperative’s by-laws.

• Participation in the ownership of a cooperative confers a right to use the services provided by the cooperative. This participation in ownership is defined by the concept of the user-owner member and is the principal characteristic of the cooperative.

Rabo International Advisory Services (RIAS) BV

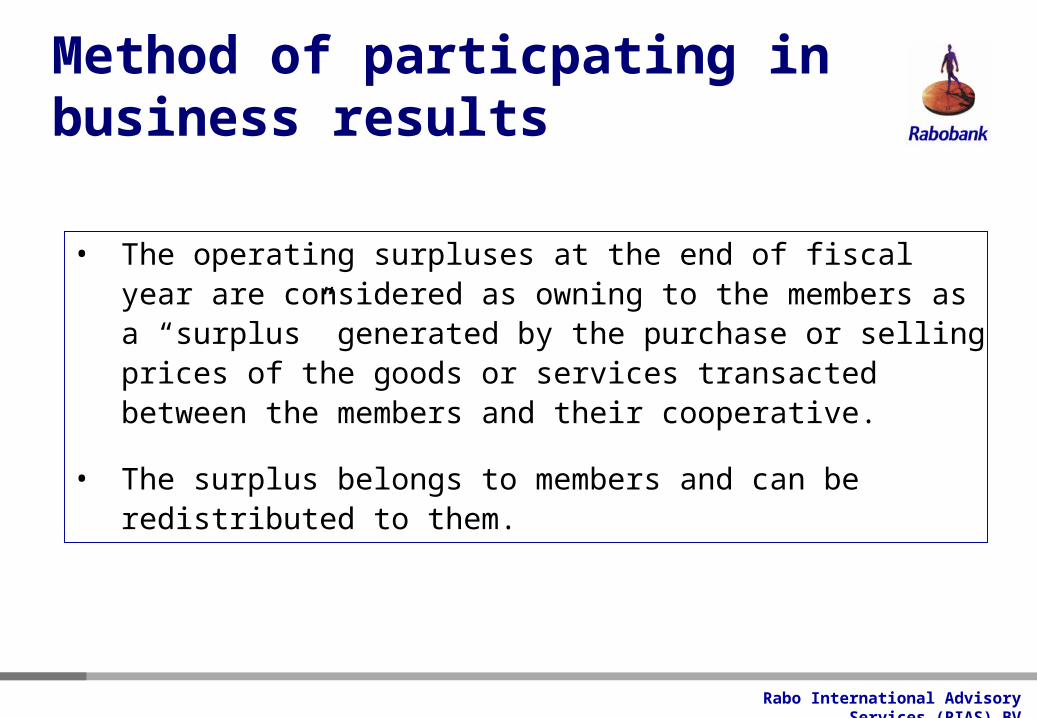

Method of particpating in business results

• The operating surpluses at the end of fiscal year are considered as owning to the members as a “surplus” generated by the purchase or selling prices of the goods or services transacted between the members and their cooperative.

• The surplus belongs to members and can be redistributed to them.

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

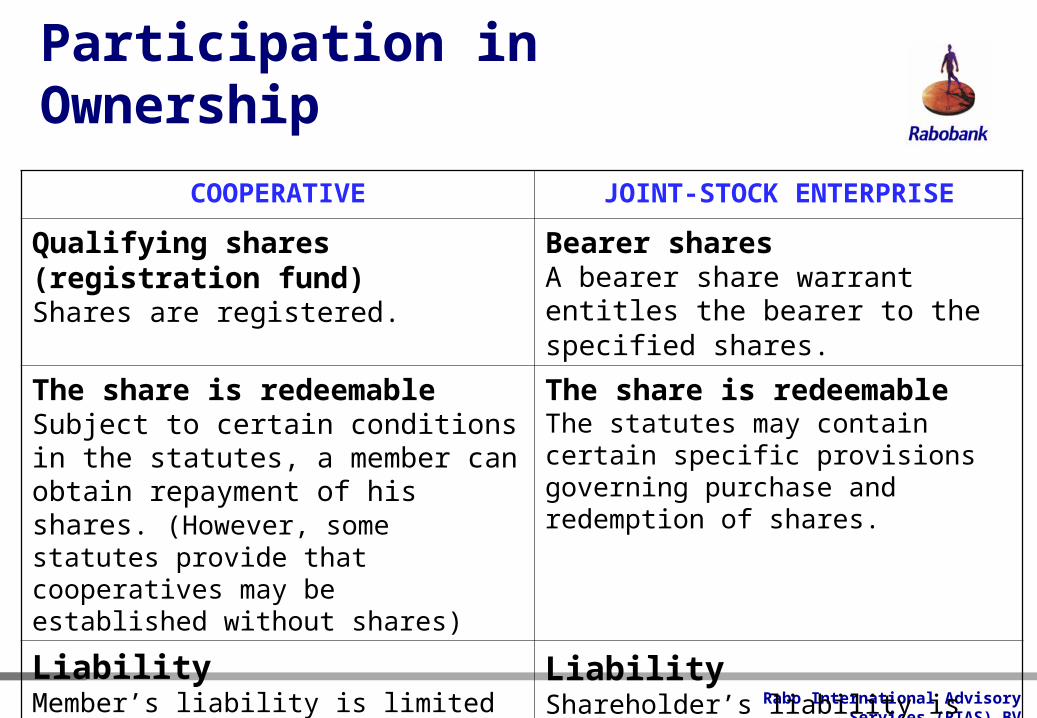

Participation in Ownership

COOPERATIVE JOINT-STOCK ENTERPRISE

Qualifying shares (registration fund)Shares are registered.

Bearer sharesA bearer share warrant entitles the bearer to the specified shares.

The share is redeemableSubject to certain conditions in the statutes, a member can obtain repayment of his shares. (However, some statutes provide that cooperatives may be established without shares)

The share is redeemableThe statutes may contain certain specific provisions governing purchase and redemption of shares.

Liability Member’s liability is limited the their total subscription for shares.

Liability Shareholder’s liability is limited to the capital subscribed for.

Rabo International Advisory Services (RIAS) BV

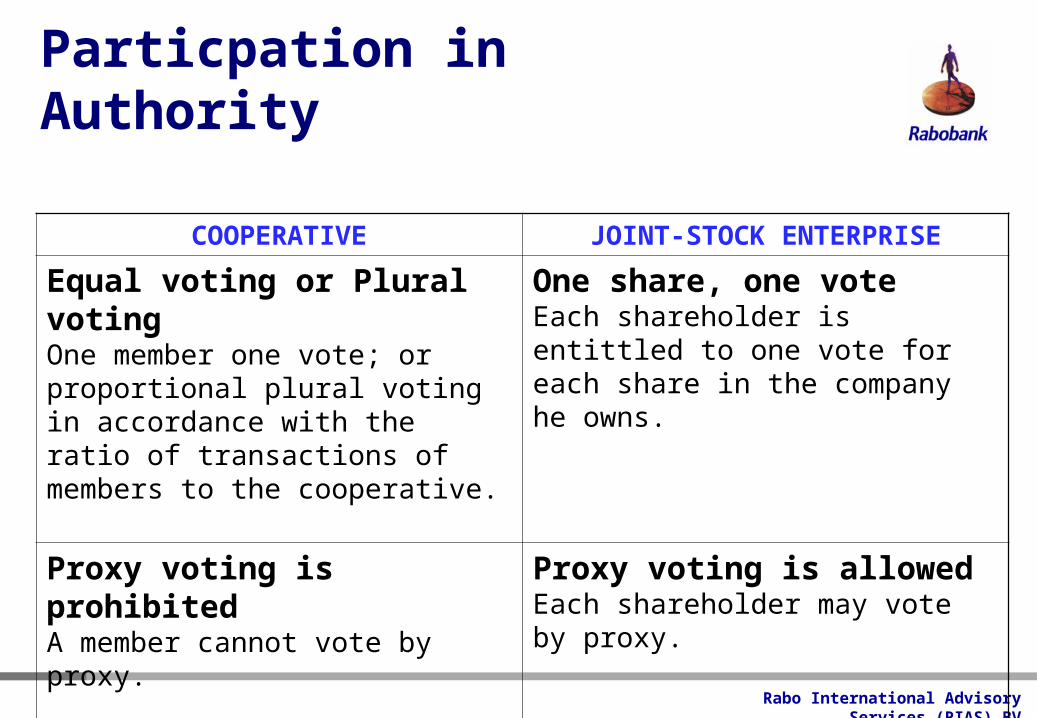

Particpation in Authority

COOPERATIVE JOINT-STOCK ENTERPRISE

Equal voting or Plural voting One member one vote; or proportional plural voting in accordance with the ratio of transactions of members to the cooperative.

One share, one voteEach shareholder is entittled to one vote for each share in the company he owns.

Proxy voting is prohibited A member cannot vote by proxy.

Proxy voting is allowedEach shareholder may vote by proxy.

Rabo International Advisory Services (RIAS) BV

Participation in Business Results

COOPERATIVE JOINT-STOCK ENTERPRISE

No capital gain is allowed on a membership shareSome statutes may provide that the reserve cannot be divided among the members. Only the amounts paid by resigning or expelled members on their shares are repayable to them.

A capital gain is allowed on a common shareA shareholder can sell his shares to another person at a mutual agreed price.

Allocation of surpluses or overpaymentsAnnual surpluses are allocated to the reserve or among the members in the form of proportion to the transaction carried out by each member with the cooperative.

Allocation of profitsProfits can be distributed in the form of dividends in accordance with the rights provided for the various classes of shares, or can be reinvested in the company.

Rabo International Advisory Services (RIAS) BV

MAIN DIFFERENT POINTS BETWEEN

COOPERATIVE & JOINT-STOCK ENTERPRISE

COOPERATIVE JOINT-STOCK ENTERPRISE

Qualifying shares (registration fund) Bearer shares

The share is redeemable The share is redeemable

One member, one vote (or proportional voting).

One share, one vote.

Proxy voting is prohibited Proxy voting is allowed

No capital gain is allowed on a membership share

A capital gain is allowed on a common or bearer share

Surplus is distributed on the proportion of economic transactions with the cooperative.

Profit is distributed to dividends.

Rabo International Advisory Services (RIAS) BV

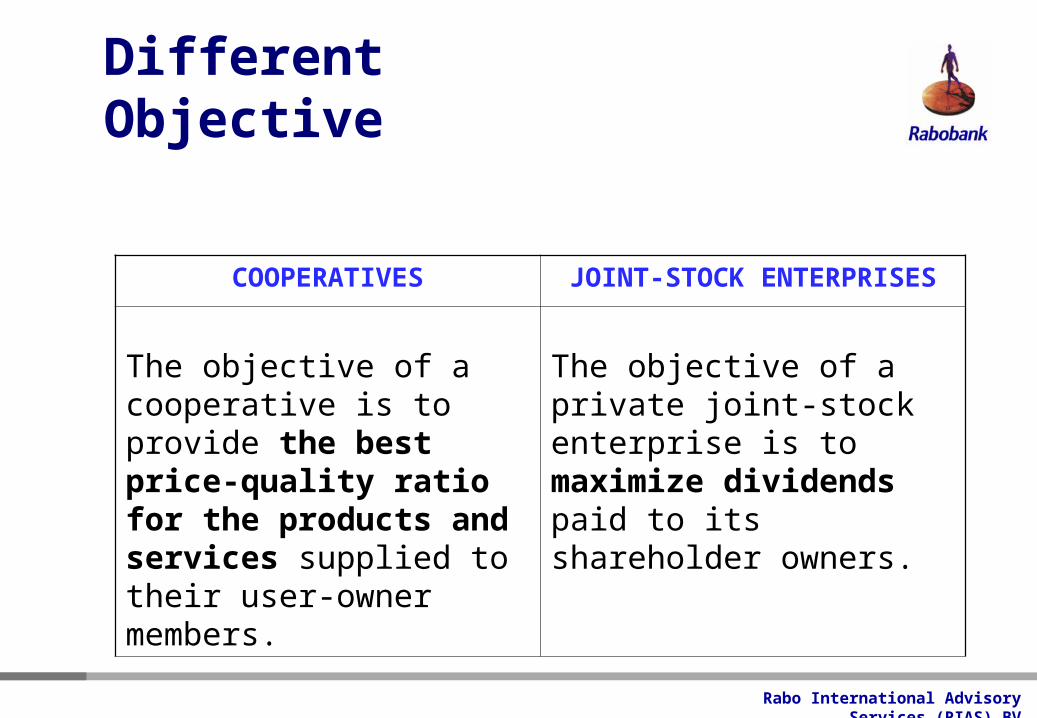

Different Objective

COOPERATIVES JOINT-STOCK ENTERPRISES

The objective of a cooperative is to provide the best price-quality ratio for the products and services supplied to their user-owner members.

The objective of a private joint-stock enterprise is to maximize dividends paid to its shareholder owners.

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

PRINCIPLES OF COOPERATIVES

VIETNAM COOP LAW (Article 5) INTERNATIONAL COOP LAW

1. Voluntariness 1. Voluntary & Open Membership

2. Democracy, equality and publicity 2. Democratic Member Control

3. Members’ Economic Participation

3. Autonomy, self-responsibility and mutual benefits

4. Autonomy & Independence

5. Education, Training & Information

4. Cooperation and community development

6. Co-operation Among Co-operatives

7. Concern for Community

Lessons learnt : With these above principles, the existing cooperatives in VN:•do not care to open to all persons who are able to use the cooperative services. •do not pay high attention on training to members.

Rabo International Advisory Services (RIAS) BV

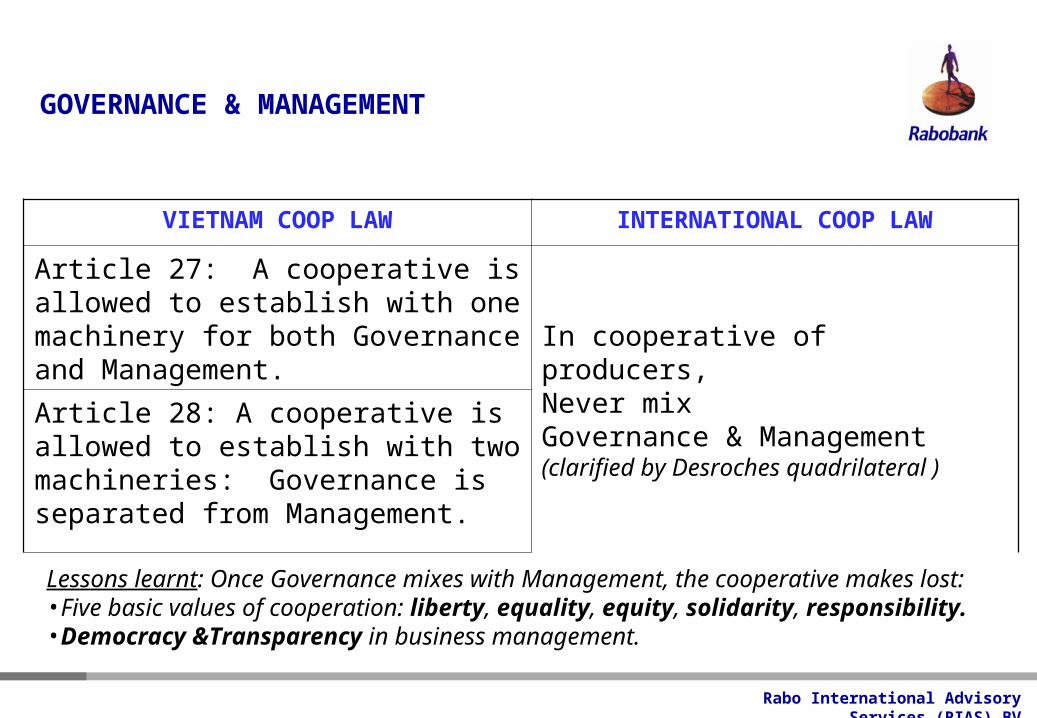

GOVERNANCE & MANAGEMENT

VIETNAM COOP LAW INTERNATIONAL COOP LAW

Article 27: A cooperative is allowed to establish with one machinery for both Governance and Management. In cooperative of producers,

Never mixGovernance & Management(clarified by Desroches quadrilateral )

Article 28: A cooperative is allowed to establish with two machineries: Governance is separated from Management.

Lessons learnt: Once Governance mixes with Management, the cooperative makes lost:•Five basic values of cooperation: liberty, equality, equity, solidarity, responsibility. •Democracy &Transparency in business management.

Rabo International Advisory Services (RIAS) BV

SURPLUS DISTRIBUTION TO MEMBERS

VIETNAM COOP LAW INTERNATIONAL COOP LAW

Article 5 & 37: mentioning the surplus distribution to members, firstly for capital contribution, secondly for labor contribution, and the remaining (if yes) for the use of cooperative services.

The surplus distribution to members will be made on the proportion of transactions (turnover) made with the cooperative.

Lessons learnt: Actually, these articles in VN law makes the existing cooperatives not only challenged, but also worst than stock enterprises: •Conflicts are unavoidable between the passive and active shareholders in the same organization. (In fact, passive shareholders are not allowed in the cooperative)•The membership and ownership can’t be defined from the real members who use cooperative services. •In such a situation, the obligation of members to sell their products to cooperative becomes meaningless.

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

56

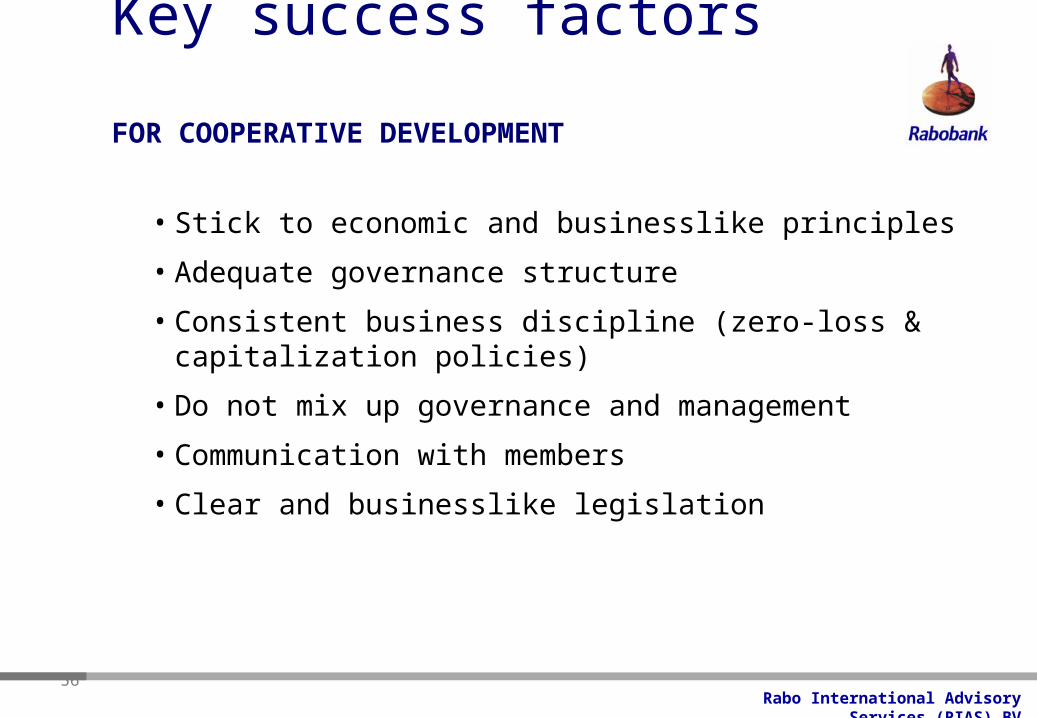

Key success factors FOR COOPERATIVE DEVELOPMENT

• Stick to economic and businesslike principles

• Adequate governance structure

• Consistent business discipline (zero-loss & capitalization policies)

• Do not mix up governance and management

• Communication with members

• Clear and businesslike legislation

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

To guarantee the success and sustainable development of a cooperative, the cooperative Rabobank - Netherlands has particularly focussed on three following economic principles, which the cooperative has to be always respected.

Three Economic Principles(Rabobank)

1. Serve at cost2. Proportional principle3. Principle of self – financing

Rabo International Advisory Services (RIAS) BV

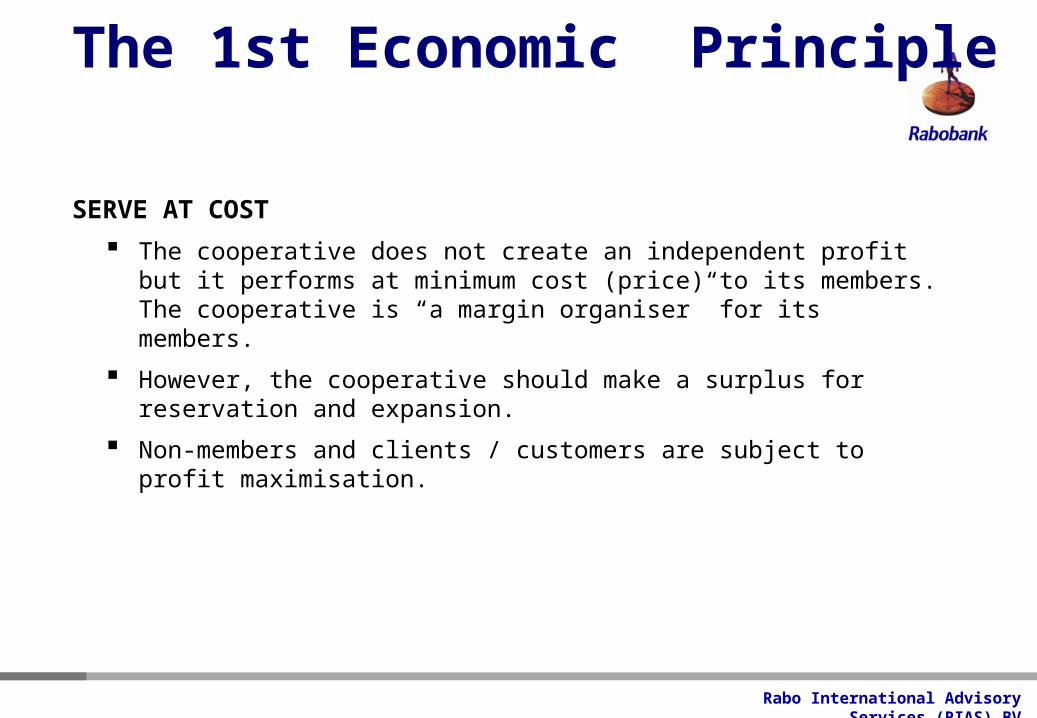

The 1st Economic Principle

SERVE AT COST

The cooperative does not create an independent profit but it performs at minimum cost (price) to its members. The cooperative is “a margin organiser” for its members.

However, the cooperative should make a surplus for reservation and expansion.

Non-members and clients / customers are subject to profit maximisation.

Rabo International Advisory Services (RIAS) BV

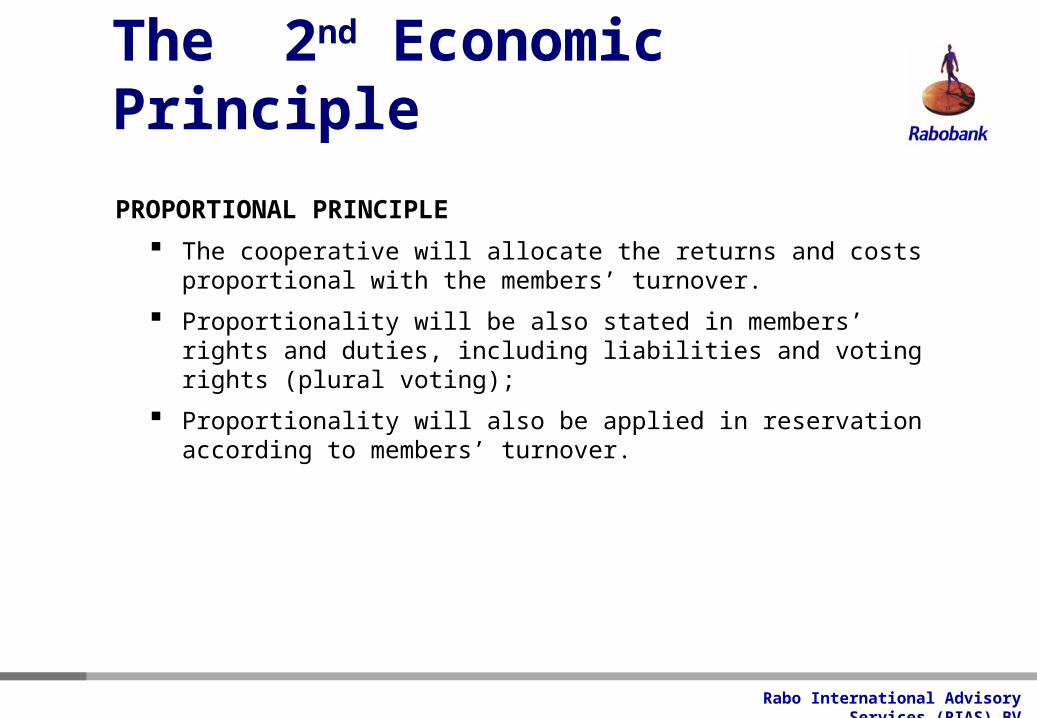

The 2nd Economic Principle

PROPORTIONAL PRINCIPLE

The cooperative will allocate the returns and costs proportional with the members’ turnover.

Proportionality will be also stated in members’ rights and duties, including liabilities and voting rights (plural voting);

Proportionality will also be applied in reservation according to members’ turnover.

Rabo International Advisory Services (RIAS) BV

The 3rd Economic PrinciplePRINCIPLE OF SELF – FINANCING

The cooperative cannot, for its main business objective, attract risk bearing capital from external investors, because this would conflict fundamentally with the members’ interests.

Members have to provide themselves the risk bearing capital.

For secondary operations, external participation is possible (joint ventures etc.).

The self - financing principle is realised through liabilities, annual reservations, members’ accounts etc.

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

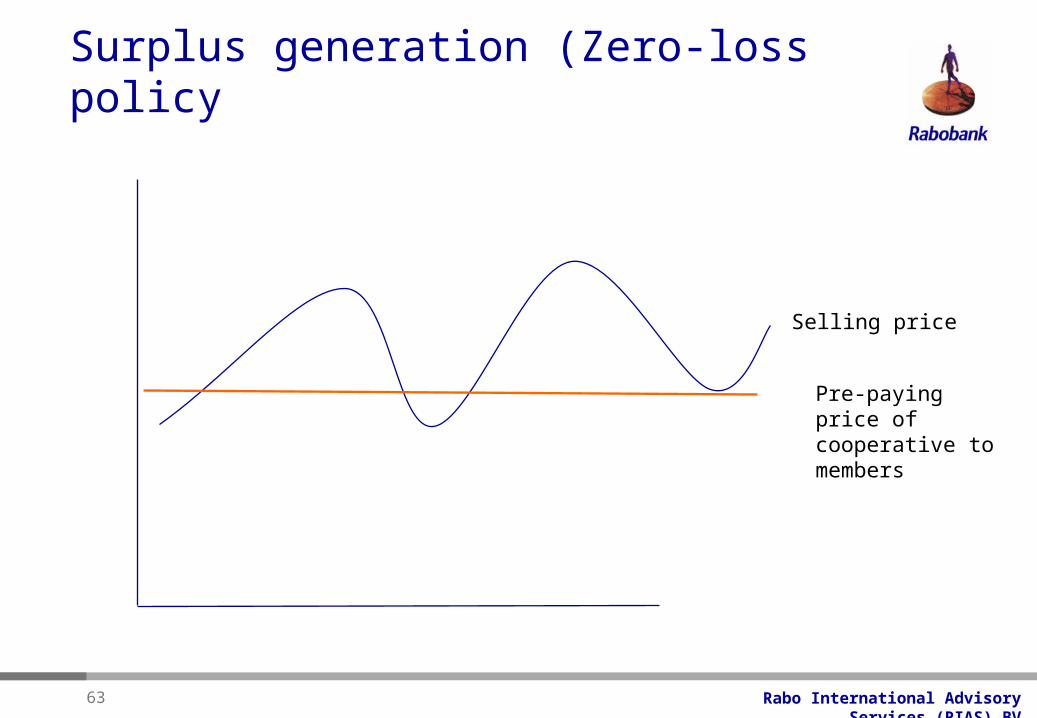

63

Surplus generation (Zero-loss policy

Selling price

Pre-paying price of cooperative to members

Rabo International Advisory Services (RIAS) BV

64

Surplus generation (Zero Loss Policy)

Jan Dec

Pre-paying priceto Members

Selling price of coop

Margin to covercost of operations

Rabo International Advisory Services (RIAS) BV

65

Capitalisation requires a consistent reservation policy

Available to Members

+

Cost of purchasing products

Surplus for members

After payment

Member Account

General Res.

Operation cost

Total Sales & Services income

Total income from sales & services

Cost of purchasing products

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

67

Strategy of the Lâm Viên cooperative

• Provide to members 100% of fertilizers with good quality and at fair prices.

• Pre-finance 50% of the labor costs

• To be responsible in marketing of the coffee of members

Rabo International Advisory Services (RIAS) BV

68

Pricing policy Lam Vien I

Free coffee for marketing

Total Sales & Services income

Total coffee production at farm

20% cash at deposit

60% to be deposited to coop

40% farmer

Coffee as repayment for inputs

80% after sale transaction completed

Rabo International Advisory Services (RIAS) BV

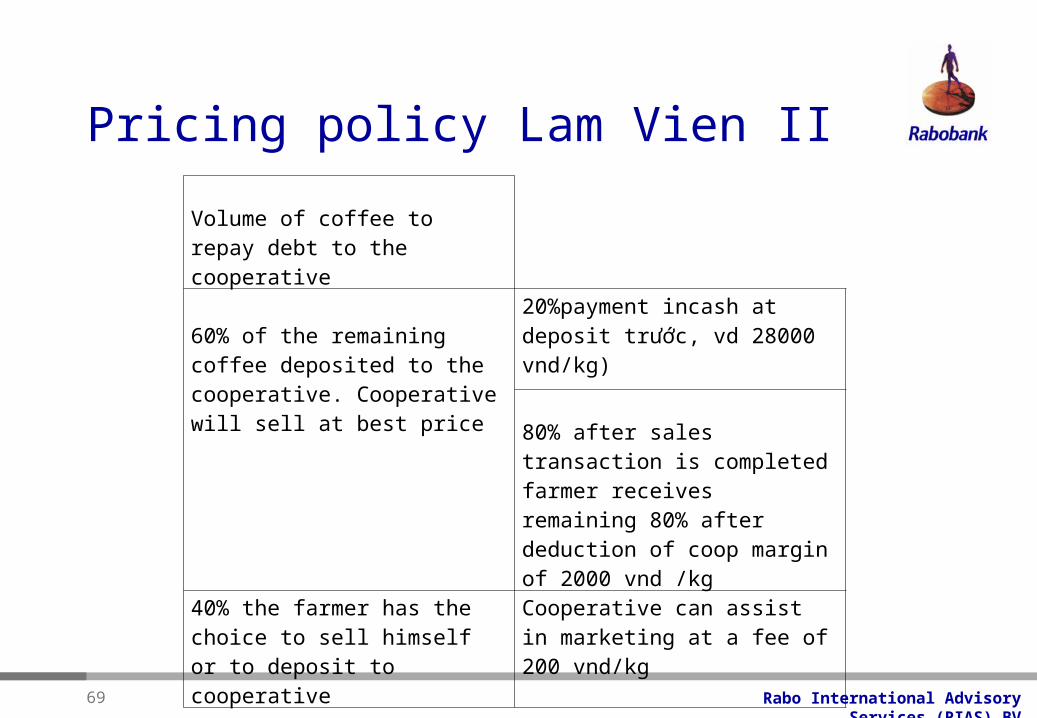

Pricing policy Lam Vien II

Volume of coffee to repay debt to the cooperative

60% of the remaining coffee deposited to the cooperative. Cooperative will sell at best price

20%payment incash at deposit trước, vd 28000 vnd/kg)

80% after sales transaction is completed farmer receives remaining 80% after deduction of coop margin of 2000 vnd /kg

40% the farmer has the choice to sell himself or to deposit to cooperative

Cooperative can assist in marketing at a fee of 200 vnd/kg

69

Rabo International Advisory Services (RIAS) BV

Rabo International Advisory Services (RIAS) BV

Lessons learned

• Communication with members

• Member Commitment

• Bank’s readiness to finance Coop

71