R eady. Aim - FTI Consulting · R eady. Aim... critical thinking ... 14 rulebooks for a New...

42

Issue 4 As profits surge and cash stockpiles grow, so do pressures on companies to put all that capital to work. Why they should not delay. Ready. Aim... CRITICAL THINKING AT THE CRITICAL TIME ™ 02 risks, riots and rewards As Asia evolves, expect turbulence as well as returns 07 will the euro survive? Two experts debate whether this marriage can be saved 26 pressure points The right way for boards to respond to shareholder concerns 34 restricted access How the rules of lending have changed ALSO: FTI JOURNAL Issue 4

Transcript of R eady. Aim - FTI Consulting · R eady. Aim... critical thinking ... 14 rulebooks for a New...

Issue 4

As profits surge and cash stockpiles grow, so do pressures on companies to put all that capital to work. Why they should not delay.

Ready. Aim...

c r i t i c a l t h i n k i n g a t t h e c r i t i c a l t i m e ™

02 risks,riotsandrewardsAs Asia evolves, expect turbulence as well as returns

07willtheeurosurvive?Two experts debate whether this marriage can be saved

26pressurepointsThe right way for boards to respond to shareholder concerns

34restrictedaccessHow the rules of lending have changed

al SO:

Ft

i J

OU

rn

al

Issue 4

Presorted Standard MailU.S. Postage

PAIDS. Hackensack, NJ

Permit #648

fticonsulting.comftijournal.com

l e t t e r f ro m t h e c e o

A lmost every article one reads about the global economic recovery and the return of corporate profits mentions the mountains of cash that companies have accumulated as they wait to invest it at the

right time and in the right place. The numbers are impressive. Worldwide, nonfinancial corporations have $4 trillion in cash, up 38% from 2007. In the United States alone, corporations accrued profits of $1.66 trillion in 2010 (the highest on record), with 59% of U.S. CEOs expecting to increase capital spending in the first half of 2011.

But news reports often overlook a subject that ultimately may be even more important in deciding who the winners (and losers) will be as the recovery gains momentum in 2011: When should companies deploy their cash? We think this question is so important that much of this current issue is devoted to exploring it from several different angles.

In our feature “Ready. Aim...” we consider where the money may end up, such as funding stock repurchases and direct payments to shareholders, underwriting capital expansions and acquisitions, and paying for a push into new markets. These days, activist shareholders tend to have their own notions about the most productive use for idle cash, and in “Pressure Points,” veteran board members discuss how best to respond to shareholder pressure. Finally, “Restricted Access” looks at the other side of the corporate balance sheet, as companies face a significantly altered post-freeze environment for borrowing.

I hope you’ll find this issue of FTI Journal useful as you assess what lies ahead in 2011 and beyond. We would be grateful to hear any comments you have about this issue, as well as suggestions for future issues. Please don’t hesitate to share your thoughts.

Jack DunnPresident and CEO

turning point

Editorial Board

DeLain gray Corporate Finance/restructuring

neal Hochberg Forensic and Litigation Consulting

John Klick Economic Consulting

Seth rierson technology

Edward reillyStrategic Communications

Sue BrownStrategic Communications

Adam Cohen technology

randall EisenbergCorporate Finance/restructuring

thomas FedorekForensic and Litigation Consulting

Melissa Kresse Strategic Communications

fticonsulting.com [email protected]

The views expressed in the following articles are those of the authors and not necessarily those of

FTI Consulting, Inc. or its other professionals.

CO

UR

TES

y O

F FT

I C

On

SU

lTIn

g

FTICONSULTING.COM

c o n t e n t s

GLOBA LPER SPECTIV E

02r isk s,r io t sa n dr ewa r dsDiverse challenges, many of them unexpected, could slow Asia’s inexorable rise. Investors need to be wary, well informed and unafraid.

FTIFILES

07 w il lt h eeu rosu rv i v e?Critics point to a growing gap between eurozone nations. But supporters warn of dire consequences if the center does not hold.

11 crossi ngt h eli n eBritain’s new anticorruption statute puts companies on the spot for the actions of anyone working on their behalf. And ignorance is no excuse.

14 ru l ebook sforach a ngi ngwor l dNew thought leadership offerings propose solutions to some of today’s most vexing issues.

16 de t ec t i ngfr au di nr e a lt i m eMultinationals face compliance issues that boil down to one requirement: using technology to detect wrongdoing at any time, in any place.

FEAT u R ES

18 r e a dy.a i m ...As profits surge and cash stockpiles grow, so do pressures on companies to put all that capital to work. Why they should not delay.

26pr e ssu r epoi n t sActivist shareholders are training their sights on how businesses deploy cash and run their operations. Corporate directors discuss the best ways to respond and a board’s proper role in helping companies prosper.

34 r e st r ic t edacce ssBanks are lending again, but new banking regulations, loan structures and products, coupled with more conservative bankers, make for tough going.

1

© 2011 FTI Consulting

Cover: Dan Saelinger for FTI Journal

I s s u e 4

#2

Risk is back. The more prudent of you might say it never went away! But I would argue that

the events that began in 2007–08 have fundamentally shifted investor expectations, as we have been assaulted by four system-shaking credit crises. We are not the men or women we were.

Gillian Tett in the Financial Times recently offered this four-step typology, which I rather like:

First, we faced a credit risk when a part of the American domestic mortgage market went into default.

Second, a liquidity crisis was brought on by counter-party risk. The fall of Lehman Brothers was its most visible

manifestation, along with the rescue of AIG, but inside the crisis the fact that the wheels seemed about to come off the capital markets was more mundane but perhaps more frightening. We all

remember the last months of 2008 and early 2009 when a simple letter of credit for routine trade exports became almost unobtainable. As Prime Minister Gordon Brown’s envoy for the G-20 at the time, I remember the scramble to get some official money behind the world’s oldest, and until then most routine, international financial transaction. World trade plummeted 20%. In a globalized world, we feared, if trade stops, the world stops.

Third: Last year investors saw their safe haven, sovereign debt, buffeted by weakness in the eurozone. This year, that credit crisis continues to play itself out as so-called rescue packages still avoid addressing the real sustainability of the public finances in Greece or Ireland or Portugal or even U.S. municipal finances. The recent Economist cover spoofing fictitious U.S. state names, such as Califoreclosia, New Yoke, No Hopeshire, Mess (for Massachusetts), Horrida and I.O.U.wa, is the satirist’s and cartoonist’s art at its most effective. It tells a story we would prefer to overlook: America’s states are drowning in red ink.

g l o ba l p e rs p e c t i v e

Diverse challenges, many of them unexpected, could slow Asia’s inexorable rise. Investors need to be wary, well informed and unafraid.

maRk malloch-bRown

chairman, global affairs, Fti consulting

mark.malloch-brown @fticonsulting.com

CO

Ur

TeS

Y O

F FT

I C

ON

SU

LTIN

G

RIsks, RIots AnD RewARDs

the events that began in 2007–08 have fundamentally shifted investor expectations, as we have been assaulted by four system-shaking credit

crises. We are not the men or women we were.

#3FTICONSULTING.COM

And hence to the fourth crisis: geopolitical risk. The Arab world is convulsed. Petrol flirts with $100 a barrel. Food prices have risen above their 2008 peak. Natural disasters are omnipresent. It’s suddenly a dangerous place out there.

So what have these four crises done to expectations and a generation of investors, especially those looking at Asia? The answer is not simply bulls vs. bears. rather, I believe we have undergone an undernoticed shift in psychology that makes us warier of indiscriminate grand trends in investing, embracing whole countries or sectors, and more cautious and careful “opportunity pickers.” Of course, trends still matter: Are we shifting our global economy onto an IT-enabled platform? Almost certainly, so that gives the technology sector a step up before you get to evaluate individual companies. Similarly, the long-term future of high-growth markets — namely Asia, Latin America and parts of Africa — seems on a stronger trajectory than, say, europe or North America.

SEEKING MARKETS WITH MORALSBut let me scratch a bit further at this somber new psychology before applying the same lessons to Asia in particular. In my view, two of the apparently hardwired assumptions about the recent past that came from the 1989 fall of the Berlin Wall have been changed by the 2007–11 credit shock. First, governments are no longer necessarily safer than

companies, which throw on its head the most basic principle of portfolio allocation between safe but low-return government bonds and corporate debt and equity. And that came to pass in considerable part because the socialization of Western bank bad debt has implications for Western political systems that have not yet played out. Look out, for example, for the return of hard-left political parties demanding much more draconian anti–Wall Street

and -business measures than anything we have seen so far.

Gordon Brown, who, as england’s Chancellor of the exchequer, presided over the dramatic expansion of the London financial services sector, in his post–prime ministerial memoir waxes angrily about irresponsible and reckless banker greed and demands markets with morals. For a man from Adam Smith’s hometown whose political career is behind him, a call for morals may be enough. I suspect younger Labour leaders harbor hopes for taking a clenched fist to markets.O

LIve

r M

UN

dAY

two of the apparently hardwired assumptions about the recent past that came from the

1989fall of the berlin Wall have been changed by the 2007–11 credit shock.

i s s u e 4

Tunisia’s and egypt’s lessons for Asia?The first thing to say is that it

probably is not the democracy deficit that will trip up Asia in the way it recently has the Arab world. For all its exceptionalism, Beijing remains sharply attentive and responsive to local issues, as though its political life depended on it — and it probably does.

rather, the roots of Asia’s risks are growing income inequality, border disputes, environmental and natural resource pressures, and the scramble to control the strategic commodities that feed the Asian manufacturing engine. On each, there are clouds. Though east Asian incomes have increased by 1,100% between 1970 and 2010 compared with an average of 184% in developing countries, income inequalities have also grown sharply in a number of east Asian countries. These inequalities create new disparities, new winners and losers and new tensions. The 2010 confrontation in Bangkok between angry rural supporters of the opposition and the more prosperous urban groups that supported the government reflected this reality, and it clearly lies behind many of the tens of thousands of social protests each year in China.

Asia entered the 21st century with a positively european, beginning-of-the-20th-century list of unresolved border and sovereignty disputes: the South China Sea, Taiwan, Kashmir, the Korean Peninsula and so on. If europe’s experience a hundred years earlier tells us anything, such disputes are exacerbated by differential rates

In this way, the “popular capitalism” model of growth that drove social cohesion in europe from Margaret Thatcher’s day onward — where people got richer, bought their own houses, put a second car in the garage and saw their children off to fine, and largely free, university educations — may be ending in tears.

SHADOWS OVER ASIA’S RISEAlthough Asia has embarked on a similar inclusive period of political and economic growth, where, despite vast income disparities, everybody feels they could be part of an American-style aspirational dream — where each generation is better off than its predecessors — it, too, will be affected if european markets grind to a halt

and a new “them” and “us” politics metastasizes from europe into Asia.

But at a time when we are anxiously peering through the telescope and trying to understand future risk, we need to look hard at Asia and the geopolitical factors that threaten to cast long shadows over Asia’s rise. What are

#4

g l o ba l p e rs p e c t i v e

percentage by which incomes in east asian

countries increased between 1970 and

2010, though income inequalities have grown

sharply in a number of these countries

1,100

OLI

ver

MU

Nd

AY

#5FTICONSULTING.COM

of economic growth. Germany’s industrial success fed its resentment at unsatisfactory border arrangements. It wanted more room and power. The other analogy to europe is that when a region is a global economic powerhouse, its disputes have a nasty habit of going global. Germany’s border grudges led us into two world wars.

The region also faces destabilizing environmental and resource trends: Water scarcity in India is one of several factors having a major impact on Indian agricultural productivity; changing dietary habits in China, India and the rest of the region with the substitution of meat for grain requires heavy increases in the use of both grain and water. environmental destruction of the Indonesian rain forests has made this one of the top hot spots for global climate change. The fact that more than 80% of the world’s natural disasters occurred in Asia in the past few years indicates how population growth, poor location of expanding human settlements, soil degradation and the loss of forest cover are combining with more extreme weather patterns to create an enhanced level of human vulnerability to natural disaster.

Beyond these kinds of issues, as Asia faces new competitors, Africa embarks on a low-cost, commodity-export-led boom backed by a lot of internal diversification. Many Asian countries seek strategic partnerships to secure access to Africa’s minerals and energy, but this also forces them into mounting a much more global national foreign policy than in the past. There

African continent. Without the same ambition for political control, this Asian scramble for African resources emulates europe’s similar late-19th-century scramble. Asia has its hands full.

INVESTORS, TREAD CAREFULLYWhat does all this mean for the investor? My own view is that none of this undermines the long-term bet on Asia, but it does suggest that investors should be discriminating. The world is a tricky place. Although Asia’s concentration of people, wealth and growth makes it an indispensable centerpiece of any global investment strategy, that strategy must be accompanied by a tolerance for risk and the tools to manage it. Too many Western investors still assume that growth will banish politics and that a vast consumer suburbanization is under way across this large and varied region. This way of thinking assumes that with

are Indian peacekeepers in Congo, Chinese traders and development experts in Malawi, and both countries’ engineers and diplomats, along with those of South Korea and Malaysia, pursuing resource deals across the

income inequalities create new disparities, new winners and losers and new tensions, and these

inequalities clearly lie behind many of the tens of thousands of social protests each year in china.

i s s u e 4

#6

g l o ba l p e rs p e c t i v e

thinking that growth equals stability. If the political system is not expanding to represent both the new middle class as well as those who fear they are getting left behind, prepare for trouble. Asia has enough variety of political systems operating effectively that the key test is not a neat Western democratic form but broad representation, accountability and legitimacy.

GROWING PAINSGrowth will propel this region forward, as well as Africa, Latin America and other emerging regions, even as the mature Western markets fall back. But at times this growth will fall into that category of things we warn our children about: Be careful what you wish for because growth brings the stresses and strains of new inequalities, resource scarcities, infrastructure bottlenecks, inflation, pressure on borders from growing populations, and competition between countries.

In the long run, people will look back and see a generation of difficulties and wonder why we had not seen it coming, and why, when it came, some probably lost sight of the more lasting truth. These difficulties were growing pains and not a lasting threat to Asia’s rise. What investors must surely do is keep their heads and hold on to their wallets in the coming years, while never losing faith in the region’s transformation. Markets have never been so global and yet local knowledge so important.

growth, every country will become a Singapore or a Hong Kong, forgetting that both have unique histories and geographical opportunities that enabled them to become high-end service providers and trade centers for their regions. Neither is a replicable model for its much larger, teeming neighbors that are still struggling to make growth inclusive and government viewed as fair and legitimate. For much of Asia, the real dramas of development, political as well as economic, lie ahead.

For the investor, this is not a reason to stop but rather to proceed through these dangerous seas with the right charts. Above all, it requires rigorous understanding of individual corporate strategic plans, financial strength and market positioning. The big trends are sufficiently prone to geopolitical shock, sector risk and continued financial volatility that the lifeboat is the investment target within the trend. Is it the IT company that will survive a bubble

or the construction business that can now weather a long downturn? And in cases where the investment is essentially a bet on a country’s stability and growth, investors need to do their homework, and above all not fall victim to the wishful

fticonsulting.com

For much of asia, the real dramas of development lie ahead. For the investor, this requires rigorous understanding of individual corporate strategic

plans, financial strength and market positioning.

C r i t i C a l i n t e l l i g e n C e

e C o n o m i C C o n s u lt i n g

will the euro survive?Critics point to a growing gap between eurozone nations. But supporters warn of dire consequences if the center does not hold.

P OI N TVicky Pryce, Senior Managing Director, economic consulting, FTi consulting; [email protected] 2002, when euro notes and coins entered circulation, the dominant view among the 15 (now 23) member states using the currency was that it represented a big step toward ensuring peace and prosperity for the Continent. What people in individual European countries tended to overlook was

c O u N T e r P OI N TGrahaM BiShoP, an economic consultant specializing in european financial markets and former adviser on european financial affairs at citigroup in LondonAmid a serious and worsening European debt crisis, the euro this year is likely to face the greatest challenges to its survival since the inception of the unified currency a decade ago. The eurozone’s collective decision to offer massive support to Greece in 2010 was merely

7

mAT

ThIA

s k

ulk

A/C

or

bIs

#8

f t i f i l e s e C o n o m i C C o n s u lt i n g

a prelude to what lies ahead — with no fewer than six states (Greece, Ireland, spain, Portugal, Italy and belgium) now deemed at risk of defaulting on their obligations and thus probably needing new infusions of eurozone assistance.

Yet most eurozone leaders seem not to have realized the magnitude of the challenges ahead — or to have grasped the consequences of failure. Consider, for example, the likely result if the financially stronger European states offer anything less than full financial commitment to euro preservation by continuing to help the weaker states. In June 2010, banks in Austria, France, Germany and the Netherlands had nearly one-quarter of their overall loans tied up in those weaker economies. should the countries drop the euro and default on those loans, worth an estimated €1.9 trillion, the impact would be catastrophic for both the banks and their home countries.

And what of the countries that desert the euro and attempt to reinstate their old currencies? Those currencies inevitably would face rapid, severe devaluation. If Greeks, for example, caught wind of such a change, fearing the disastrous consequences of a return to the drachma on their personal accounts, they would naturally transfer their assets to Germany or another eurozone state. Try as Greece might to close its economic borders, this flight of capital, made simple and inexpensive by technology and the euro, would be almost impossible to prevent.

that a single currency brings greater interference by members of the union in each state’s monetary, fiscal and political affairs. Tension over such intrusions, coming to the fore in the wake of sovereign debt crises in Greece, Ireland and elsewhere, casts serious doubt on the survival of the euro as the single currency for most of Europe.

During the next few years, member states will do whatever they can to avoid a split because the practical inconveniences would be enormous. Weaker countries, such as Greece, would face a radical devaluation of their currency and essentially would have to close their fiscal borders to prevent a flight of money. stronger nations, such as Germany, would suffer as well. The inevitable rise in a German-dominated currency would make exports — a cornerstone of the German economy — far less competitive on the world market.

That’s why leaders of financially robust member nations will continue to support bailouts despite grumbling from their citizens about shouldering the lion’s share of the cost; it’s also why weaker nations, such as Greece and Ireland, will continue to accept austerity measures despite protests from their citizens about cuts in government services.

but over the longer term, say, a decade or so, the survival of the euro in its current form will become much more problematic. In order for the bailouts to succeed and the single currency

Percentage by which unit labor costs in greece

have increased since it locked in its exchange rate with the euro in 2001, compared with

germany’s less than 70%

240

P o i n t ( C o n t ’ d ) C o u n t e r P o i n t ( C o n t ’ d )

FTICONSULTING.COM #9

The result would be an immediate liquidity crisis crippling those countries’ banking systems.

For all of its troubles, the euro — and a financial system that enables its daily use by 330 million people — is a major component of the region’s single market, which lets residents purchase goods and services seamlessly across borders. Though some observers contend that European unity could survive a split in the currency, it’s more likely that any sense of political oneness would be destroyed amid waves of recriminations over ruined economies.

Preserving that essential system won’t be easy, but clearly this is not a time for timid solutions. by the end of this year, the eurozone is likely to emerge as a distinct political federation that, at its

to remain viable, the productivity gap between weaker and stronger countries must close significantly. Yet during the past decade, technological advances and wage moderation have helped Germany widen the gap with southern Europe in terms of manufacturing unit labor costs, a standard measure of export competitiveness. since 2001, when Greece locked in its exchange rate with the euro, its unit labor costs have increased by more than 240%, according to the organisation for Economic Co-operation and Development, while Germany’s costs have risen less than 70%.

Prior to the euro, weaker countries could make up for lower productivity with currency depreciation, which made their exports comparatively cheap on the

P o i n t ( C o n t ’ d ) C o u n t e r P o i n t ( C o n t ’ d )

Keeping the euro intact won’t be easy, but it could be crucial.

mE

DIo

ImA

GE

s/P

ho

ToD

IsC

/GE

TTY

i s s u e 4

#10

f t i f i l e s e C o n o m i C C o n s u lt i n g

heart, has tightly centralized economic governance. For example, because taxes are such a vital revenue resource for any state, it is probable that there will be moves toward a single set of accounting standards to promote tax harmonization from country to country — a major step toward implementing a more centralized European financial authority. Another likely step will be the arrival of Europe-wide government bonds in 2011. Issued by the European Financial stability Facility and backed by the authority and control of a combined Europe, these bonds would begin to replace the patchwork of risky single-country bonds and add greater stability to the European debt system. steps toward greater economic governance of the entire eurozone by central authorities may also include the power to assess the fiscal policies of individual member states, mandate budget and spending changes as needed, and issue sanctions for failing to comply.

These changes will inevitably be contentious and difficult, but they will also bring needed stability and uniformity to the European economic system. In the end the euro will survive, not because the choices are easy or the road smooth, but because it must. one leader who does seem to understand the urgency of this issue is President Nicolas sarkozy of France, who noted recently that “the end of the euro would be the end of Europe.” his warning hardly seems overstated.

international market. When everybody is being paid in euros, however, debtor nations must resort to starker alternatives: lower wages, higher taxes and a resulting drop in the standard of living. Consequently, countries such as Greece, spain and Portugal will need major structural reforms if they are to succeed in making their industries more competitive. such reforms, which may include pushing back the retirement age and deregulating labor markets, are accompanied by serious political costs, especially if populations feel the policies are being imposed from the outside.

An eventual split in the euro ultimately might be the best thing for all concerned. one possibility is for the stronger economic countries to keep the euro while the weaker ones go their own way. After the initial shocks, the monetary balance would probably return to its pre-euro state, with countries such as Greece and Portugal making up for their lower productivity through currency depreciation and cheaper exports.

It’s important not to mistake the end of the euro as a single currency with the end of the European union. member nations’ commitment to the Eu is unshakable; they see it as essential in maintaining peace on the Continent and in representing European interests and values around the world. The euro, on the other hand, could simply go down as a grand dream that eventually ran into the wall of economic reality.

P o i n t ( C o n t ’ d ) C o u n t e r P o i n t ( C o n t ’ d )

FTICONSULTING.COM #11

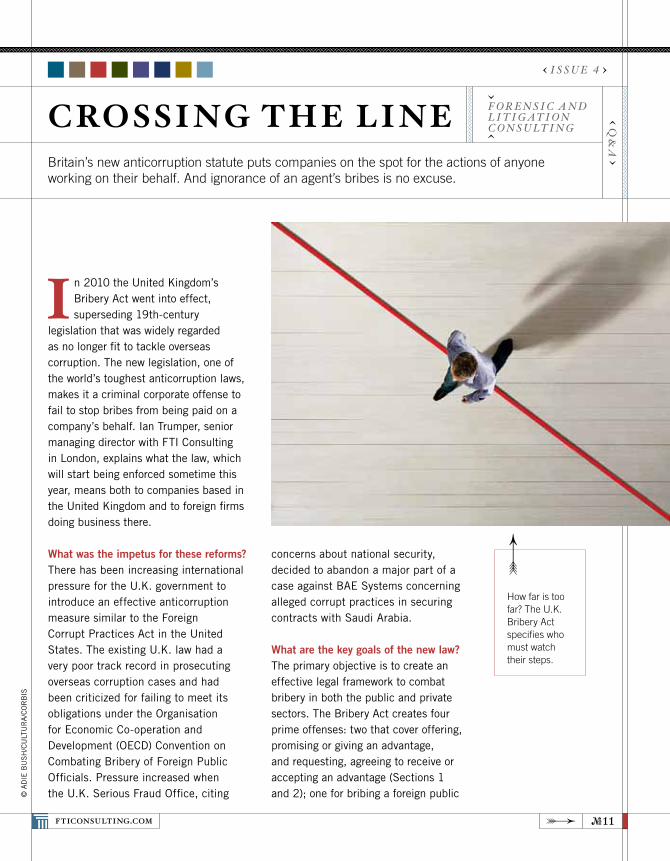

F o r e n s i c a n d l i t i g at i o n c o n s u lt i n g q

&a

concerns about national security, decided to abandon a major part of a case against BAE Systems concerning alleged corrupt practices in securing contracts with Saudi Arabia.

What are the key goals of the new law?The primary objective is to create an effective legal framework to combat bribery in both the public and private sectors. The Bribery Act creates four prime offenses: two that cover offering, promising or giving an advantage, and requesting, agreeing to receive or accepting an advantage (Sections 1 and 2); one for bribing a foreign public

I n 2010 the United Kingdom’s Bribery Act went into effect, superseding 19th-century

legislation that was widely regarded as no longer fit to tackle overseas corruption. The new legislation, one of the world’s toughest anticorruption laws, makes it a criminal corporate offense to fail to stop bribes from being paid on a company’s behalf. Ian Trumper, senior managing director with FTI Consulting in London, explains what the law, which will start being enforced sometime this year, means both to companies based in the United Kingdom and to foreign firms doing business there.

What was the impetus for these reforms?There has been increasing international pressure for the U.K. government to introduce an effective anticorruption measure similar to the Foreign Corrupt Practices Act in the United States. The existing U.K. law had a very poor track record in prosecuting overseas corruption cases and had been criticized for failing to meet its obligations under the Organisation for Economic Co-operation and Development (OECD) Convention on Combating Bribery of Foreign Public Officials. Pressure increased when the U.K. Serious Fraud Office, citing

Britain’s new anticorruption statute puts companies on the spot for the actions of anyone working on their behalf. And ignorance of an agent’s bribes is no excuse.

crossIng the l Ine

© A

DIE

BU

Sh

/CU

LTU

rA

/CO

rB

IS

How far is too far? The U.K. Bribery Act specifies who must watch their steps.

i s s u e 4

#12

F t i F i l e s F o r e n s i c a n d l i t i g at i o n c o n s u lt i n g

What does that mean for companies based in the United Kingdom?You have to look at specific wording within Sections 6 and 7 to understand the new law’s significance. For example, in Section 6 there is no test for improper performance, so if you offer anyone working in a public capacity a financial reward with the intention of influencing that person to obtain or retain business, that is an offense — even if that person does nothing improper. But there’s no definition of what constitutes a “financial or other advantage.” What if a company pays for a government official to fly overseas to inspect its manufacturing plant or to attend a business meeting? Where do you draw the line between bona fide marketing to display a company’s capabilities and more lavish expenditures that may influence the official’s decision? There also is no exemption for de minimis payments, including facilitation payments.

In addition, companies are questioning what constitutes adequate procedures under Section 7 and how much responsibility they must take for the actions of overseas subsidiaries, agents and suppliers. What if you are working with an agent and you don’t know that person is paying a bribe? The new law has been drafted to enable prosecutions of bribery; the onus is on the company to prove its defense.

The defense to a charge under Section 7 is the ability to demonstrate that the company had adequate procedures in place to stop bribes from

someone for such an action. These types of bribes already were illegal, but under the new law it will be easier to bring charges. The offense of bribing a foreign public official brings the U.K. law into line with the OECD Convention, which criminalizes bribes intended to influence a public official in obtaining or retaining business.

But if the first three offenses merely clarified or modified existing legislation, the fourth is entirely new. Under Section 7, any corporation with a business presence in the United Kingdom can be held criminally liable if any person associated with it, including any of its employees or agents anywhere in the world, is found guilty of giving or receiving a bribe. The only defense will be that the organization had put adequate procedures in place to prevent such bribery.

official (Section 6); and a corporate offense of failing to prevent a bribe from being paid (Section 7).

The first two offenses cover bribes in both the public and private sectors, but a person (or corporation) is guilty only if there was an intention to induce another to do something improper or to reward

“Where do you draw the line between bona fide marketing to display a company’s

capabilities and more lavish expenditures that may influence the official’s decision?”

FTICONSULTING.COM #13

of Sponsoring Organizations model. [COSO of the Treadway Commission provides international guidance on organizational governance, business ethics, internal controls and financial reporting.] In essence the advice was to assess a business’s corruption risks, devise appropriate control and compliance procedures, and implement continuous monitoring. These principles were accompanied by some examples of appropriate procedures. Transparency International, with funding from FTI Consulting, also published guidance that sought to provide practical advice.

In recent weeks there has been a lot of lobbying by businesses arguing that there is insufficient guidance on certain features of the act, particularly about facilitation payments and marketing expenditure. The government’s publication on the adequate procedures has been delayed, as has guidance from the Ministry of Justice on prosecution policy. As a result, the act, which was due to come into force in April, is more likely to become effective as of early summer.

being paid. [These provisions are similar to accounting rules in the United States that focus on ensuring that there are policies and procedures in place to prevent fraud or embezzlement.] It may be difficult, however, for a company to convince a prosecutor that its procedures were adequate.

What are the implications for companies based outside the United Kingdom?The jurisdictional reach of this law is very wide. Anyone who is a U.K. resident and any company incorporated in the United Kingdom is subject to the act. Beyond that, though, if you have a place of business in the United Kingdom, Section 7 applies. For example, if a U.S. or Chinese company carried on only a small part of its business in the United Kingdom, say, through a small representative office, and that company is shown to have paid bribes in Africa, the company could be prosecuted in the United Kingdom. My own view is that enforcement will continue to focus on companies with extensive operations in the United Kingdom. But I think we can see the United Kingdom following the approach of the U.S. Department of Justice on Foreign Corrupt Practices Act investigations — many more cases being settled through large fines, with some individuals being prosecuted.

What procedures should companies implement to ensure that they remain in compliance with the new law?The U.K. government has published draft guidance based on the Committee

If just one employee oversteps the limits of the new law, the whole company could be held accountable.

SYM

Ph

On

IE/g

ETT

Y

i s s u e 4

t h o u g h t l e a d e rs h i p

spo

tl

igh

t Rulebooks fo R a Changing Wo Rld

#14

f t i f i l e s

M anaging through crisis has never been easy. But in today’s increasingly complex,

interconnected world, the challenges have grown ever more daunting. Climate change, poverty, terrorism, and financial and credit instability are just a few of the intractable issues confronting both heads of state and corporate chieftains, for whom the stakes have never been higher. Two FTI Consulting experts have recently published their perspectives on the issues.

The Unfinished Global RevolUTion: The PURsUiT of a new inTeRnaTional PoliTics (Penguin Press, 2011). Lord Mark Malloch-Brown lays out a road map for navigating an uncertain future. FTI Consulting’s chairman of global affairs, Malloch-

Brown draws from a wealth of experience on the international stage — as a World Bank vice president, head of the United Nations Development Programme and deputy secretary-general to U.N. Secretary-General Kofi Annan. A former journalist, Malloch-Brown also has served as minister of state in the Foreign and Commonwealth Office of the United Kingdom with responsibility for Africa, Asia and the United Nations.

In The Unfinished Global Revolution, Malloch-Brown argues that, just as the worldwide economic crisis of 2008 demonstrated that a global economy requires global financial institutions, today’s political and social challenges demand unprecedented international cooperation. In the 21st century, trade, technology, economics and social change continually push people of disparate geographies and cultures together, but national governments aren’t equipped to handle the complex global issues they face, and there are no international organizations empowered to fill the void. Changing that won’t be easy, given the suspicions people and their political leaders have of the U.N. and its like.

Part of the remedy, says Malloch-Brown, is a “simple global social contract” through which individuals, corporations and governments can establish powerful international

New thought leadership offerings propose solutions to some of today’s vexing issues.

FrO

M L

eFT

: C

OU

rTe

Sy

OF

Pe

NG

UIN

Pr

eS

S; C

OU

rTe

Sy

OF

KO

GA

N P

AG

e

Authors Mark Malloch-Brown and Shaun O’Callaghan draw on decades of experience in the financial realm.

FTICONSULTING.COM #15

a period of upheaval resulting from shifting consumer preferences, economic recession, management scandal or some other kind of shake-up. Whatever the cause, crisis presents an opportunity for managers to become leaders and to develop a recovery plan that will put the organization back on its feet as painlessly and productively as possible.

O’Callaghan outlines five key areas of leadership he considers mandatory in building a successful recovery plan: beginning anew by making the right promises to stakeholders, including customers, investors and lenders, employees and suppliers; gathering a range of alternative perspectives, no matter how contrary; developing core business skills necessary for recovery, including cash flow and time management, strategy development, sales management and cost-base restructuring; delivering results through savvy relationship building; and rebuilding trust through authentic communication with all stakeholders.

One of the most common mistakes managers make is failing to recognize and challenge their own assumptions about a business, O’Callaghan says. For example, had CeOs of financial firms questioned their assumptions — that the wholesale lending spigot would remain open and that property values would continue to climb — the 2008 housing market collapse might have been averted. While hindsight is always 20/20, Turnaround Leadership contends that with the right tools in their belts, corporate leaders can be prepared for whatever comes their way.

institutions that value human rights and the rule of law, and offer a voice for participating nations. Through intimate portraits of politicians he has advised and observed, including Bill Clinton, George W. Bush, Jacques Chirac and Tony Blair — and through an engaging political history of governments that have failed to live up to the demands their citizens place on them — Malloch-Brown offers an agenda for managing globalization. And he suggests that the corporate leaders of tomorrow won’t be the imperial CeOs of yesteryear, but rather visionaries who can reach across cultures and engage shareholders to build alliances, bringing together apparently disparate interests. That leadership will require a multicultural sensibility, emotional intelligence, and an ability to listen, persuade and understand different points of view.

TURnaRoUnd leadeRshiP: MakinG decisions, RebUildinG TRUsT and deliveRinG ResUlTs afTeR a cRisis (Kogan Page Ltd., 2010). Shaun O’Callaghan, senior managing director in FTI Consulting’s Corporate Finance/ restructuring business segment, lays out a proposed framework for coping with crisis, drawing on more than 15 years of experience as an adviser, executive and board director and as a founder of Quartet research, a leadership research and development organization for senior executives.

In Turnaround Leadership, O’Callaghan starts with the premise that all companies, if they’re in business long enough, eventually will go through

Crisis presents an opportunity for managers to become leaders and to develop a recovery plan that will put the organization back on its feet as painlessly and productively as possible.

i s s u e 4

#16

f t i f i l e s

detecting fraud in real time

a perfect storm is brewing in the regulatory compliance arena. The push for stronger

regulatory oversight ignited by corporate and Wall Street scandals is finally coming to fruition, with government agencies around the globe becoming more aggressive about — and more adept at — identifying and pursuing regulatory violations.

Three forces are converging to shape this new regulatory environment. First, regulatory bodies are employing sophisticated technology to detect and

prosecute transgressions. The U.S. Securities and Exchange Commission’s Office on Market Intelligence, for example, has equipped its new task force on market abuse with the technology to conduct “Facebook investigations,” essentially mining data on traders’ personal relationships and communications to flag potential

incidents of insider trading. Second, a “whistle-blower lotto” provision in the Dodd-Frank Wall Street Reform and Consumer Protection Act offers informants a bounty of 10% to 30% of any fine of more than $1 million resulting from a tip. And third, penalties for paying bribes in foreign markets are poised to escalate significantly under the U.K. Bribery Act of 2010.

the importance of Being integratedThis trend of intensifying exposure to myriad regulatory actions around the globe strongly suggests a need for multinational corporations — the most likely targets for government enforcement action — to develop integrated compliance programs that collect and monitor data in real time. Such systems could, for example, automatically monitor vendors and transactions, flagging those involving people or firms on government watch lists. If a company suspects a particular kind of violation, a custom inquiry can be written to mine the data and identify transactions for internal and compliance review.

Deterring violations or detecting them early through a comprehensive, integrated program is a crucial first line

Joe Looby senior Managing Director,

technology, fti Consulting [email protected]

Multinationals today face proliferating compliance issues that essentially come down to one requirement: putting technology in place to detect wrongdoing at any time and in any location.

A compliance program could flag transactions involving people or firms on government watch lists.

if a company suspects a particular kind of violation, a custom inquiry can be written to mine the data.

te

Ch

no

lo

gy

FTICONSULTING.COM #17

settled a U.S. Foreign Corrupt Practices Act charge by the SEC for approximately $185 million, almost half of that penalty. An effective compliance program is a defense under the new U.K. Bribery Act.

understanding good practicesIn May 2010 the Organisation of Economic Co-operation and Development released “Good Practice Guidance” for antibribery compliance programs. The document outlines what companies are expected to do regarding antibribery policies, training, internal controls, reporting systems, discipline for violations, compliance incentives and accountability for program management. It also emphasizes the importance of having periodic third-party audits of compliance measures and reviews to ensure that programs keep up with evolving technology and with national and international standards.

For multinational companies operating in this increasingly aggressive regulatory environment, now is the time to rethink their approach to compliance on a global scale.

of defense. Yet many large multinationals continue to employ piecemeal, often incompatible systems. That’s particularly likely when a company has grown through multiple acquisitions or has taken a decentralized approach to managing foreign subsidiaries. For example, if a U.S. company using Oracle’s financial management software buys a European firm running SAP and then buys a company in Asia that relies on a proprietary or a bespoke financial system, it may hope to avoid the thorny issue of integrating the three systems. But that leaves its internal audit team facing the manual and ad hoc challenge of collecting and interpreting data from each system. In today’s regulatory environment, that kind of disjointed effort is unlikely to succeed because companies need an effective way to deter and detect violations enterprisewide.

New technology provides a better solution, letting a company connect the dots — collecting and analyzing transaction data from disparate financial systems in real time. Responding to government investigations often costs millions of dollars in time and resources — and any resulting penalties, or criminal and civil judgments, can double or triple the bill, not to mention the impact on a brand or a corporate reputation. Establishing effective real-time automated compliance controls can also reduce external audit and insurance fees. And penalties may be lighter when a company can show it has an effective compliance program in place. That might have saved DaimlerChrysler, which

Regulatory winds have shifted, and companies dare not miss signs of fraud anywhere in their operations.

YAM

AD

A T

AR

O/G

ETT

Y

i s s u e 4

c o v e r s t o r y

After three years of hunkering down, deferring unnecessary investment and cutting costs, companies around the world are sitting on record levels of cash to spend as the global economy strengthens.

Gordon McCoun, ViCe ChairMan and Senior ManaGinG direCtor, StrateGiC CoMMuniCationS, Fti ConSultinG. [email protected] by dan SaelinGer

ready. aim...

moves boosted corporate earnings, and companies’ coffers swelled. In Europe, for instance, cash makes up 12% of total assets on corporate balance sheets and is almost a third higher than at any point in the last economic cycle, according to UBS. Globally, nonfinancial corporations are sitting on $4 trillion in cash today, a full trillion dollars more than they had on their books in 2007, according to Citigroup’s Corporate Finance Advisory Group.

Yet, while the National Bureau of Economic Research in the United States reports that the recession officially ended in June 2009, many companies

B y sitting on mountains of cash until the recession has safely passed, companies may think

they are acting prudently. On the contrary, they could be setting themselves up to be overtaken by competitors that have been strategically using their financial resources to make acquisitions, launch new products and create more efficient ways of doing business.

Over the course of the 2007–09 recession, as credit markets froze and revenue plunged, companies jettisoned millions of workers and took the scalpel to their budgets, especially in Europe and the United States. Of course, those

19

#20

c o v e r s t o r y

President Obama implored CEOs to start investing and hiring, pointing out that “American companies have nearly $2 trillion [in liquid assets] sitting on their balance sheets.”

Yet the most important reason for getting off the sidelines and deploying that cash is neither shareholder pressure nor political cajoling. It is that companies will lose competitive advantage. According to numerous studies, companies that emerged in the best shape from past recessions had invested more and saved less than their competitors. As a 2002 McKinsey & Co. study found, the companies that came out of the 1990–91 recession the strongest had outspent peers in R&D (by more than double) and acquisitions while maintaining cash balances 40% lower than their competitors’. By spending their cash on pursuing market share, developing new products and opening new markets, they had significantly strengthened their competitive positions.

It isn’t too late for companies that have been conservative with their cash to catch up. But the window of opportunity is closing.

Spending CaSh in all the right plaCeSA number of companies have used the recession of 2007–09 to enhance their prospects. Even though the days of economic turmoil are not far behind them, they are already reaping the benefits of their contrarian investing

have maintained a viselike grip on liquid capital. Whether they worry about a double-dip recession, a lack of investment opportunities or the need to rearm against Asian competitors, their financial prudence risks becoming a liability. The reason: Competitors are already investing strategically and are gaining substantial ground. In industry after industry, companies like Netflix, W.R. Grace, Banner Health and Maersk have used the recession to invest aggressively in new products, markets and operations. As the global economy recovers, these companies will have first-mover advantages that will be hard for others to overtake. Firms that keep hoarding cash face a big risk of being left behind competitively and frustrating multiple constituencies that want them to deploy their capital.

Because returns on cash are at historic lows, investors are taking a dim view of many companies’ cash positions. A survey by the law firm Schulte Roth & Zabel in late 2010 showed that excessive cash positions would be the primary catalyst of investor activism over the next 12 months. Political pressure is being brought to bear as well. In February 2011, in an address to the U.S. Chamber of Commerce,

The companies that came out of the

1990–91 recession the strongest had outspent

their peers in R&D (by more than double)

and acquisitions while maintaining cash

balances 40% lower than their competitors’.

i s s u e 0 4

FTICONSULTING.COM

had available to make investments in emerging markets,” says the firm’s chief financial officer, Hudson La Force.

These lessons apply to companies that are as different from process manufacturers like Grace as baseball is from cricket. Take Banner Health, a $4.7 billion (revenue) U.S. healthcare provider that owns 22 hospitals. In the recession, the company not only had to contend with flat or declining patient volumes, but it also had to prepare for the healthcare industry’s looming day of reckoning: healthcare reform legislation. Hospital systems

ways. How they invested in the downturn while most of their competitors pulled back is instructive.

Consider the case of W.R. Grace. As the recession took hold in 2008, the $2.6 billion (revenue) global specialty chemicals company moved quickly to slash working capital and operating costs. By reducing net working capital days by half (from 106 to 53), Grace freed up $350 million in cash, an amount that was triple its 2007 operating earnings. As the credit markets tightened, that cash became pivotal to Grace’s overseas expansion. The U.S.-based company bought and acquired manufacturing capacity in growing markets from China to Saudi Arabia to Brazil.

Those investments are already paying off. In 2010, Grace’s sales from overseas markets increased 13% over 2009 — more than four times the firm’s overall growth (3%). More important, the company, whose products include catalysts for oil refineries and plastics manufacturers, expects emerging markets to be virtually the only source of growth in those two industries over the next three to five years. Grace’s new factories are critical to its participation in that growth.

Grace’s lesson: Reinvesting cash strategically is as important as reducing costs and working capital to free up that cash. “There is a direct correlation between the reductions we made in working capital and the cash we

#21

#22

c o v e r s t o r y

have aggressively deployed their cash during the recession provide useful insights on where to look.

I’ll organize these stories into three categories: new products, new markets, and redistributing work around the world.

New products. Netflix is the world’s largest movie subscription service. The firm has gone from launch in 1997 to $2 billion in annual revenue today and has 12 million subscribers. It is led by Reed Hastings, its CEO and co-founder.

Hastings has long believed that, although DVD rental by mail will be a source of growth for Netflix for many years, subscribers will increasingly want the immediate response of movies streamed over the Internet to their television screens. In 2007, Netflix began investing in software that would enable streaming on other companies’ devices, such as Blu-ray players, set-top boxes, game consoles and TiVo DVRs. Netflix was faced with a big investment, one that could have appeared untenable as the economy began backsliding into recession. But the company didn’t flinch, making streaming a focus of its research and development efforts. Between 2007 and 2009, Netflix doubled R&D spending from $70 million to $140 million. Meanwhile, it ran down its cash balance by two-thirds, from $400 million at the close of 2006 to $134 million at the end of 2009.

Today, Netflix’s investments during the bleak years look prescient. In the

like Banner face a future of declining public and private reimbursements for treatments and hospital stays. And because future reimbursements will be tied to the quality of care, Banner’s senior management knew the company had to upgrade facilities and medical equipment. Indeed, it has — to the tune of more than $1 billion in construction projects for new and existing hospitals.

W.R. Grace and Banner Health could have conserved their cash until the financial storm had long passed. The stockpiles of cash that companies around the world are sitting on today suggest that many firms have done just that. Yet both companies decided to invest and strengthen their competitive positions. They and other companies that exit the recession having laid the building blocks for growth are likely to outrun competitors that continue to hoard their cash.

deCiding Where to inveSt: the StorieS of netflix, polo ralph lauren and maerSkSo if companies decide it’s better to spend strategically today than continue to save, where should companies invest? To be sure, the answer will be different for every firm. The right opportunities depend upon a firm’s unique circumstances: the markets in which it sees the greatest potential, its core capabilities and competitive position, the unfilled needs of its customers and more. The stories of companies that

trillions of dollars in cash held by

nonfinancial corporations around

the world, a full trillion dollars more

than in 2007

4

FTICONSULTING.COM #23

really run the risk of falling behind,” says CFO La Force.

Polo Ralph Lauren is another global company that took this to heart three years ago and ramped up its investments in Asia-Pacific. The $5 billion (revenue) apparel and fragrances company began buying its Asian licensees in 2008, believing the product range they offered was too narrow and their inventories too low. With sales of luxury consumer goods exploding in Asia, the company needed to capture a bigger share of the pie. At the beginning of this year, it acquired its South Korean distributor, the seventh successive purchase of a Polo Ralph Lauren licensee in Asia. In a February earnings call, COO Roger Farah made it clear that the firm’s $1.3 billion in cash and investments was at its disposal for more investments in Asian markets. Analysts and investors appear to have no problems with that. The stock has risen from the $70s last July to more than $120 this February.

redistributiNg work arouNd

the world. This investment category is less obvious than the other two, and many companies have ignored it. But others have made substantial investments and have seen sizable

third quarter of 2010, two-thirds of its subscribers were streaming movies online, nearly double the number in mid-2009. The company’s revenue last year was 80% higher than 2007’s, and profits have soared 140%. At the end of 2010, Netflix’s cash position was on the mend, rising to $194 million. These numbers have clearly dazzled investors. Netflix’s stock more than tripled in value in 2010 alone. Since 2007, the share price has risen tenfold.

New markets. History shows that recessions spread pain unevenly around the globe. While demand can be moribund in a company’s home market, emerging economies can offer lucrative opportunities. The combined gross domestic product of the BRIC countries (Brazil, Russia, India and China), for instance, is now almost 70% of Europe’s aggregate GDP. But what’s more remarkable about the $11 trillion BRIC GDP is its impressive growth. Between 2000 and 2008, the BRIC countries contributed almost 30% to global growth, compared with 16% in the previous decade. Since the start of the crisis in 2007, the BRIC countries’ contribution has risen to 45%, according to analysis by Goldman Sachs.

Companies like Grace believe that rapid growth requires participation in emerging markets. “If you are a global company, as we are, and you are not investing in these markets today, you

History shows that recessions spread

pain unevenly around the globe.

While demand can be moribund

in a company’s home market, emerging

economies can offer lucrative opportunities.

i s s u e 4

#24

c o v e r s t o r y

and energy firm, Maersk has been slowly but steadily building global “shared services” operations since 2003. Based in six centers in India, China, the Philippines and Denmark, these operations have enabled Maersk to standardize and reduce the costs of support functions, such as finance, accounting, human resources and IT. In 2008 the global economic downturn produced the most challenging year ever in the container business. In response, as well as taking aggressive steps to cut costs, Maersk accelerated its investments in shared services. The company set a target of increasing the share of finance and accounting work done by the centers from 30% to 70%. Over 18 months Maersk hired 1,200 additional people for shared services, absorbing finance and accounting operations from 85 countries. The result: The operations are better standardized; the costs of those operations were reduced by 10% in 2010; the savings will increase as the remaining countries are rolled in and the new processes stabilize; and Maersk has a cost structure that better positions it to compete as the global economy recovers.

getting paSt the oBStaCleS to inveSting in lean timeSShould every company follow the lead of Netflix, Maersk, Polo Ralph Lauren and W.R. Grace and make major investments in new products, markets or operations

returns. It is about redistributing the work of an organization — the activities of the finance department, information technology, customer service and other support functions — to take advantage of such conditions as lower labor costs and preferential tax treatments in other regions.

A great example is the $60 billion Danish conglomerate A.P. Moller-Maersk Group. A major ocean shipping

There is risk in doing nothing: Companies

that are neither acquirers nor acquired

may be marginalized by their shrinking

market share, or shareholders might

force a sale, breakup or return of capital.

FTICONSULTING.COM #25

that is consolidating. But there is risk in doing nothing: Companies that are neither acquirers nor acquired may be marginalized by their shrinking market share, or their shareholders may take the decision out of management’s hands by forcing a sale, breakup or return of capital.

We continually hear executives argue against investing too soon. “The economy could tank again.” “Domestic markets are flat.” “Overseas markets are risky.” “We are in a mature sector.” “Deals are too expensive,” and so on.

While there is truth in all of these objections, leading companies have managed around them, and in many cases investors are rewarding them for it. Several recent acquirers have seen the values of their shares increase after they announced acquisitions, in contrast to the normal market reaction. Danaher Corp.’s stock rose on the announcement of its acquisition of Beckman Coulter Inc. in February, despite paying a 45% premium on Beckman shares. Cliffs Natural Resources Inc. stock rose nearly 3% on Jan. 11 after it announced the purchase of Consolidated Thompson Iron Mines Ltd.

At some point, the majority will follow the minority, and a stampede will commence. Several indicators say it is about to begin. History tells us that companies that deploy their cash before their slower-moving competitors can overtake them.

in spite of uncertain economic times? Shouldn’t some companies hang on to their cash until better times are clearly ahead? For most, we think not. Almost every company has opportunities for growth in bad times as well as good. Take the chemicals industry. Even though it doesn’t seem like a sector with high potential during a global manufacturing downturn, W.R. Grace found prosperity in distant lands.

In any event, it isn’t necessary to hold on to a pile of cash for future needs such as making an acquisition. As Tenet Healthcare chairman Edward Kangas says in our roundtable discussion in this edition, “It’s generally better to arrange a large line of credit for that purpose than to keep a lot of cash.”

Highly leveraged companies may have more urgent priorities for their cash, such as shrinking their debt. Firms uncertain about repaying maturing loans might consider refinancing and extending maturity dates first. (See “Restricted Access,” page 34.) But once they’ve straightened out their capital structures, even these companies should seek profitable investment opportunities.

We do excuse some companies from investing during the downturn. Managers in mature sectors with more capital than they can profitably invest should consider returning it to shareholders through share repurchases or dividend increases. Or they might consider merging or being acquired, especially if they operate in a sector

catalyst for investor activism over the next 12 months: excessive cash positions

No. 1

i s s u e 4

#26

ro u n d ta b l e

A trillion dollars is hard to miss, and with almost that much cash on the books, U.S.

corporations have attracted the attention of hedge funds and other activist

shareholders who want to know just how companies plan to put the money to work. According to Moody’s, U.S. nonfinancial companies had $943 billion in cash on their balance sheets at mid-year 2010, up from $775 billion at the end of 2008, and with interest rates at historic lows, that stockpile of dollars isn’t adding much value to the companies that hold it. Activist shareholders are pressing corporate management and boards to buy back shares, increase dividends, make acquisitions or otherwise deploy the cash in ways that explicitly benefit shareholders.

But that pressure puts directors in an uncomfortable position. Board members well remember the depths of the recent recession, when credit markets froze and liquidity was precious. They understand the need to invest in the business but want to

Pre ssure P oints.

Activist shareholders are training their sights on how businesses deploy cash and

run their operations. In this roundtable, corporate directors discuss the best ways

to respond and a board’s proper role in helping companies compete and prosper.

po

rTr

AiT

S: M

ich

Ae

l e

dw

Ar

dS

fo

r f

ti j

ou

rn

al;

fin

An

ciA

l r

ep

or

T: M

Ar

c v

olk

/ge

TTy;

no

TeB

oo

k: g

eTT

y; l

Ap

Top

: ©

Bil

l M

ile

S p

ho

Tog

rA

ph

y/g

eTT

y

Seven directors of boards as diverse as PetSmart, accenture and tenet Healthcare offered their views on communicating with shareholders.

be prudent and responsible, as global competition is fierce and the economy is susceptible to another decline. At the same time, trends in regulation and corporate governance, such as “say on pay” and proxy access, are giving shareholders more input into strategic and other corporate matters. if boards fail to heed the complaints of shareholders, activists could launch proxy fights or propose slates of directors who might disrupt corporate functions or result in the ouster of company officers.

So as global economies improve and visibility into the future increases, how should boards respond to the tradeoff between preserving liquidity and pursuing investment during 2011? And beyond that, what should a board’s role be in setting strategy, working with management and monitoring performance? for insights, fti journal convened a roundtable of veteran board members. Meeting in fTi consulting’s Manhattan office, the panel included robert dinerstein, chairman of crossbow ventures and a former vice-chairman of UBS investment Bank; rita foley, director of dresser-rand and petSmart; Stuart r. levine, director of Broadridge financial Solutions; and david Meachin, chairman and ceo of cross Border enterprises. Unable to attend but weighing in during separate interviews were edward A. kangas, chairman of the board of Tenet healthcare; philip r. lochner, who serves on the boards of clarcor, cMS energy, crane co. and gentiva health Services; and Blythe Mcgarvie, ceo of

consulting firm lif group and a board member for Accenture, The Travelers, viacom and wawa.

FTI Journal (FTIJ): In a recent survey of activist shareholders and corporate executives, the law firm Schulte Roth & Zabel found that both groups expect shareholder activism to increase during 2011, though they disagreed about what issues will provoke that activism. Activists said excessive cash holdings will be the primary catalyst, whereas executives thought financial performance would be the main catalyst. What is the sentiment of your boards? Are you concerned that activists will force you to change strategy and/or make premature decisions to commit capital?

DAvID MeAchIn: if you sit on a big cash position for several years, you could have a huge political problem. But this is not a time to throw around a lot of cash just because activists tell you to spend. The economy still is deeply troubled, and it will be a long, slow process before the markets fully recover. And with the global marketplace becoming increasingly competitive, companies need to have a big cash war chest. There are any number of western-educated Asian executives who now are running companies back home. They are very dedicated, and they have employees who will work hard for comparatively low pay. To meet that competition, many U.S. companies may have to spend money acquiring smaller businesses. Say you are a big pharmaceutical company. you

#28

ro u n d ta b l e

CEO of consulting firm LIF Group and board member for Accenture, The Travelers, Viacom and Wawa

Blythe McGarvie

Director of Dresser-Rand and PetSmart

rita Foley

Board member for Clarcor, CMS Energy, Crane Co. and Gentiva Health Services

PhiliP r. lochner

#29FTICONSULTING.COM

particularly china, is not waiting to expand its reach into new markets. one of the best uses of cash now is to travel around the world looking for innovative products, services and processes that you can use in your own business.

eDWARD A. KAngAS: if a company is generating strong cash flow and has more than adequate cash on hand, shareholders are going to want to

know its plans for using that capital. one way to articulate that is to use return on invested capital to compare internal and external uses of cash. But if the roic on a stock buyback or dividend is much higher than you get from acquisitions or r&d, investors will question your priorities, and it will hurt the valuation of the company and its stock price. And though some companies want to keep “dry powder” for game-changing acquisitions, it’s generally better to arrange a large line of credit for that purpose rather than to keep a lot of cash.

FTIJ: By the time activist shareholders knock at your door, it may be too late

could spend $1.8 billion developing a drug that may not succeed — or you could buy a small company that has strong research and development and a solid pipeline of new drugs.

STUART R. LevIne: Shareholders should give us advice, and we should listen. But at the end of the day, it is the responsibility of the chief executive and the board to make strategic decisions. Boards should develop long-term strategies that ensure shareholder value through r&d, M&A and organic growth.

FTIJ: In the wake of the financial crisis, how should boards look at the issue of holding cash vs. putting it to work?

BLyThe McgARvIe: Since the crisis began in 2008, corporate boards and managers have needed to answer three questions: has the company restructured its debt to take advantage of some of the lowest interest rates in years? have we reconsidered our discount rate when computing net present value analysis for potential investments? And what is a reasonable threshold, or “investment rate hurdle,” to use when comparing various potential investments?

with interest rates so low, most companies can invest in their operations or in acquisitions for much higher returns than can be made in money markets. with returns on cash low, this is exactly the right time to invest in developing markets and in products to remain competitive and to capture market share. The rest of the world,

“the rest of the world is not waiting to expand its reach. one of the best uses of cash now is to travel around the

world looking for innovative products, services and processes that you can use in your own business.”

i S S u e 4

#30

ro u n d ta b l e

real value. And while they’re often seen as just wanting share buybacks, the really good activists can help companies improve their approaches to capital allocation.

FTIJ: Are there other effective forums for communicating with shareholders? And is it possible to communicate too much?

LevIne: it’s important to talk with the general counsel about the best way to communicate so you don’t run into problems with fair disclosure regulations. i was a lead director at a company when a hedge fund took a substantial position in the stock. when a manager of the fund reached out to me, i listened for a reasonable amount of time while the investor shared his ideas about strategies on mergers and acquisitions. i thanked him for his ideas and assured him that i had heard his suggestions but explained that it would be inappropriate for me to get into a lengthy conversation. when people ask to talk with an independent board member at Broadridge, we refer the request to the ceo and determine which director would be the most appropriate person to respond, e.g., chairman of compensation, governance or audit.

RoBeRT DIneRSTeIn: There might not be much we can do to change the views of activist shareholders. But we need to find ways to reach retail investors. They have lost confidence in the market, and they are turning to brokers for advice. we need to provide focused

to head off a confrontation. how can companies avoid becoming targets?

RITA FoLey: By maintaining open communication with shareholders, who are less likely to side with activists if they understand your strategy. Some of that will come through individual meetings with investors, but companies also should hold strategy days that are open to all analysts. At these meetings, management can lay out a company’s five-year strategy and explain why it makes sense.

LevIne: Some companies have effectively reviewed strategy through retreats. The sessions are designed to explore the future and are grounded

in the reality of available capital and results. reflecting on investor concerns helps enrich the discussion. This process helps the ceo continue to respond to these issues appropriately.

KAngAS: it’s also important not to generalize about activist investors. They worry boards, which don’t appreciate the scrutiny. But some activists can add

“You can’t ignore Facebook, linkedin and twitter. Someone has to be actively monitoring what is being said about a company in the new

social media and respond accordingly.”

FTICONSULTING.COM

in part because you typically have to compensate people for stock options or other payments they give up when they leave their old jobs. now there could be even more focus on such payouts, and to avoid controversies, companies may put a renewed emphasis on promoting from within. But that will require boards and management to spend more time grooming executives and having a robust succession plan. That could be a positive development.

MeAchIn: whether or not say on pay has an impact, globalization could put pressure on salaries in the United States, which tend to be higher than those at competitors abroad. To compete internationally during the next 20 years, you’ll have to cut costs to the bone and adjust compensation.

FTIJ: What role should a board play in developing strategy — what businesses and markets to be in, how cash is used, how executives are compensated and other important issues? Should the board actually formulate plans or simply oversee management as it develops ideas?

MeAchIn: it used to be that management would give a six-hour powerpoint presentation to the board, which then would essentially give management the go-ahead to proceed with its plans. These days, the ceo and management are still responsible for making strategy, but to compete on a global stage, management has to harness the brainpower of everyone on the board,

communications for the brokers. it no longer is enough just to send out a press release.

FoLey: you also can’t ignore facebook, linkedin and Twitter. Someone has to be actively monitoring what is being said about a company in the new social media and respond accordingly.

FTIJ: one of the hottest topics for the next proxy season involves the “say on pay” provisions of the U.S. financial reform legislation passed last year. Under the rules, companies must give shareholders the right to provide advice on executive compensation. Some people see this as an intrusion on the rights of boards. But there has been an arms race to pay ceos — if one ceo makes a certain amount, competitors feel they must match the figure. could the new rule make boards more thoughtful about compensation policies?

FoLey: Surveys of board members suggest that “say on pay” won’t have a great impact. Similar rules have existed in the United kingdom for a long time, and there hasn’t been much fallout. Many boards already listen to shareholders and are transparent about compensation, so they will have little resistance to change. There will be more pressure to show how you measure executives relative to the business results.

Activist shareholders often complain that companies spend too much to hire senior executives from outside,

Chairman of Crossbow Ventures and former vice-chairman of UBS Investment Bank

roBert Dinerstein

#31

Chairman and CEO of Cross Border Enterprises

DaviD Meachin

Director of Broadridge Financial Solutions

stuart r. levine

Chairman of the board of Tenet Healthcare

eDwarD a. KanGas

i S S u e 4

#32

ro u n d ta b l e

FTIJ: The credit crisis and recession exposed the ignorance of many directors and boards about the companies they oversee. how can directors come to understand a business at a fundamental level? Do they need to go into the field and get their hands dirty?

MeAchIn: Board members should visit plants and operations, and if plants and operations are overseas, that’s where board meetings should be. procter & gamble divides its board into groups and sends three board members to one country and three to another. you don’t have to travel 300 days a year, but board members have to recognize that part of their job today is to travel to wherever major business is done. The point is to get a good understanding of the products and the customers.

FoLey: Board members also need robust training. i serve on a board that includes several ceos with experience in the industry. But everybody had to go through training, which consisted of getting tutorials and visiting clients as well as company facilities. it was helpful because some of those ceos had come up through the financial ranks and were less familiar with the field and with manufacturing.

LevIne: i have served on the board of a nonprofit hospital group for 25 years, and i find that field trips are always helpful. we recently toured a hospital and visited an emergency room and operating theaters. we talked with doctors and nurses. That provided

which needs to be involved in critiquing ideas and ensuring that plans make sense. Also, many board members serve for 10 years or more, while ceos often are there for a much shorter time. So the board must take more responsibility for determining and implementing long-term strategy in case it needs to bridge a management transition.