Quant GST Thematic 1.0: GST passage: AIADMK holds...

14

June 7, 2016 Quant GST Thematic 1.0: GST passage: AIADMK holds key… Research Analyst Amit Gupta [email protected] Raj Deepak Singh [email protected] Sanjay Manyal [email protected]

Transcript of Quant GST Thematic 1.0: GST passage: AIADMK holds...

June 7, 2016

Quant GST Thematic 1.0:

GST passage: AIADMK holds key…

Research AnalystAmit Gupta [email protected] Deepak Singh [email protected] Manyal [email protected]

Rajya Sabha electoral process

• The present strength of the Rajya Sabha is 245, out of which 233 are representatives of the states andUnion territories of Delhi and Puducherry while 12 are nominated by the President. The membersnominated by the President are persons who have special knowledge or practical experience in the fieldsof literature, science, art and social service

Electoral process:

• The representatives of the states and union territories in the Rajya Sabha are elected by the method ofindirect election. The representatives of Rajya Sabha are elected by the members of the legislativeassembly of that State, in accordance with the system of proportional representation by means of a singletransferable vote

Biennial-election

• Rajya Sabha is a permanent House and is not subject to dissolution. A member who is elected for a fullterm serves for a period of six years. However, one-third of the members of the Rajya Sabha retire afterp y , jyevery second year. The election held to fill a vacancy arising apart from the retirement of a member iscalled a ‘by-election’. A member elected in a by-election remains a member for the remainder of the termof the member who had resigned or died or been disqualified from being a member of the House

Current electionsCurrent elections

• In June 2016, 55 Rajya members would retire and be replaced by 57 members. The additional two seatsare for the one vacated by an independent member from Karnataka while the other is on account of theresignation of Congress MP Anand Sharma from Rajasthan

2

Party wise position in Rajya Sabha – current and post June 2016UPAUPAParty Wise Position Current Numbers Outgoing Members Confirm Wins Tentative Wins Post Election ChangeIndian National Congress 63 14 7 2 58CPI(M) 8 0 0 0 8NCP 6 2 1 0 5DMK 4 2 2 0 4RJD 1 0 2 0 3Jharkhand Mukti Morcha 1 0 0 1 2 -3

INLD 1 0 0 0 1IUML 1 0 0 0 1Janta Dal (S) 1 0 0 0 1CPI 1 0 0 0 1

87 18 12 3 84NDAParty Wise Position Current Numbers Outgoing Members Confirm Wins Tentative Wins Post Election ChangeBJP 47 12 15 1 51BJP 47 12 15 1 51Nominated 10 0 0 0 10BJD 7 2 3 0 8TDP 7 2 2 0 7Independent 6 2 0 1 5SAD 3 1 1 0 3SS 3 1 1 0 3J&K PDP 2 0 0 0 2

4J&K PDP 2 0 0 0 2BPF 1 0 0 0 1Kerala Congress (M) 1 0 0 0 1NPF 1 0 0 0 1RPI(A) 1 0 0 0 1SDF 1 0 0 0 1

90 20 22 2 94OTHERSParty Wise Position Current Numbers Outgoing Members Confirm Wins Tentative Wins Post Election ChangeSamajwadi Party 16 3 6 1 20Trinamool Congress 13 0 0 0 13AIADMK 12 3 4 0 13Janta Dal(U) 13 5 2 0 10BSP 9 6 2 0 5TRS 1 0 2 0 3YRS C 0 0 1 0 1

1

3

YRS Congress 0 0 1 0 164 17 17 1 65

Total 241 55 51 6 243 2

Party wise stand on GST in current format

Parties in favour of GST Parties against GST

Party Seats in Rajya SabhaBharatiya Janata Party (BJP ) 51Samajwadi Party (SP ) 20All I di T i l C (AITC ) 13

Party Seats in Rajya SabhaAIADMK * 13Communist Party of India (CPI(M) ) 8Dravida Munnetra Kazagham (DMK ) 4

Parties who are against GST and want changes

All India Trinamool Congress (AITC ) 13Janata Dal (United) (JD(U) ) 10Nominated members 10Biju Janata Dal (BJD ) 8Telugu Desam Party (TDP ) 7Bahujan Samaj Party (BSP ) 5

Dravida Munnetra Kazagham (DMK ) 4Communist Party of India (CPI ) 1Total 26

P i h d i ill l U d id d

Bahujan Samaj Party (BSP ) 5Nationalist Congress Party (NCP ) 5Independent 5Shiromani Akali Dal (SAD ) 3Telangana Rashtra Samithi (TRS ) 3Shiv Sena (SS ) 3

Party Seats in Rajya SabhaIndian National Congress (INC ) 58Total 58

Parties whose stand is still not clear – UndecidedShiv Sena (SS ) 3J&K Peoples Democratic Party (J&K PDP ) 2Bodoland People's Front (BPF ) 1Naga Peoples Front (NPF ) 1Sikkim Democratic Front (SDF ) 1Kerala Congress (M) (KC(M) ) 1

Party Seats in Rajya SabhaRashtriya Janata Dal (RJD ) 3Jharkhand Mukti Morcha (JMM ) 2Indian National Lok Dal (INLD ) 1Kerala Congress (M) (KC(M) ) 1

Republican Party of India (A) (RPI(A) ) 1Total 150

Indian National Lok Dal (INLD ) 1Indian Union Muslim League (IUML ) 1Janata Dal (Secular) (JD(S) ) 1YRS Congress 1Total 9

Note: We have assumed Congress will win two contestedseats from Karnataka and UP while SP, JMM and BJP will win * AIADMK is considered in against. However, if it

4

one each from UP, Jharkhand and Rajasthan, respectively.One independent member may get elected from Haryana

gchanges its stance it would have a significant impact onoutcome

Various scenarios in way of GST bill: AIADMK holds key

Scenario 1: Congress and AIADMK vote against the bill Scenario 2: Congress abstains from voting

Total Votes 243 Required 162Current support 150 Left & DMK 13Others (undecided) 9 Congress 58

Total 185 Required 123Current support 150 Left & DMK 13Others (undecided) 9 AIADMK 13

Scenario 3: AIADMK abstains and Congress & Left Scenario 4: Left and Congress vote against the bill but

( ) gTotal in favour 150 AIADMK 13Outcome: GST will not pass in Rajya Sabha

( )Total in favour 150Outcome: GST will be passed

Scenario 3: AIADMK abstains and Congress & Left vote against the bill

Sce o e d Co g e o e g e b buAIADMK comes in favour

Total 243 Required 162Current support 150 Left & DMK 13AIADMK 13 Congress 58Others (undecided) 9

Total 230 Required 153Current support 150 Left & DMK 13Others (undecided) 9 Congress 58

Highlights:

1) We believe the AIADMK will play a pivotal role in the passage of the GST bill. Even if Congress votes against the

Others (undecided) 9Total in favour 163Outcome: GST will be passed

Total in favour 159Outcome: GST may pass if others support the bill

bill, support from AIADMK either through abstaining or voting in favour of the bill would help clear the GST bill inRajya Sabha

2) We believe the GST bill will not be cleared only if both Congress and AIADMK vote against it. In case either ofthese parties abstain, the bill is likely to go through with the support of others

5

50% states supposed to pass supplementary bill…BJP/Alli d* R l d t t N (BJP & C ) St t Whi h lik l t t th billBJP/Allied* Ruled states Non - (BJP & Congress) States: Which are likely to accept the billMaharashtra West BangalMadhya Pradesh Uttar PradeshRajasthan OdishaHaryana TelanganaG j t Bih If GST is passed in RajyaGujarat BiharGoaChhattisgarhJharkhandAndhra Pradesh*Punjab*

If GST is passed in RajyaSabha, it will be easily becleared by the mandated50% states as 20 out of 29states and two unionPunjab

Jammu &Kashmir*Assam*Sikkim*Nagaland*Arunachal Pradesh*

states and two unionterritories are ruled byeither NDA or with statesin favour of the bill. In such

i GST ll illArunachal PradeshTotal 20

Congress Ruled States Non BJP/Congress States: Which are likely to reject the billPuducherry Tamil NaduKarnataka Tripura

a scenario, GST rollout willnot be an issue once RajyaSabha clears the bill

Uttarakhand KeralaHimachal Pradesh DelhiMeghalayaMizoramManipurT t l 11

Source: ICICIdirect.com Research

Total 11

Sectoral impact of GSTIndustries Impact on Sector Current Applied Indirect Tax Recommended GST rate Stocks to Benefit

At present, small cars (< 4 metres & engineWe believe GST would have a positive impact on Auto sector as the benefit of lower At present, small cars (< 4 metres & engine size of <1200 cc for petrol & <1500 cc for diesel) are taxed at ~30% (which comprises 12.5% excise duty + CST 2% + National Calamity contingent duty 1% + VAT in the range of 12.5%-14.5% + road tax in the range of 3%-20%). The Sedans & SUVs are taxed ~45% & ~52% respectively.

We believe GST would have a positive impact on Auto sector as the benefit of lower taxation (GST < 20%) would be passed on the consumers by way of lowering the vehicular price by 10%-20%.

GST < 20%M&M, Tata Motors,

Ashok Leyland, Maruti Suzuki

There would be level playing field, as it would not restrict OEM's from procuring quality & good material from vendor which are located outside its manfacturing state. At present 2% CST is levied on such transaction resulting into higher input cost for OEMs.

In case of motorcycle the effective tax rate stands ~30%.

GST < 20% Bajaj Auto, Hero Motocorp, Eicher Motors

We believe Auto Ancillary industry would also have a positive impact of GST. Apart from lower taxation, more uniform tax structure resulting into higher cost & tax for unorgnaised players would tend to benefit orgainsed players in terms of market share

At present, spare parts industry are currently d 28%

GST < 20%

Amara Raja, Exide Inds, Apollo Tyre, JK Tyre, B lk i h I d B h

45% & 52% respectively. Auto

unorgnaised players would tend to benefit orgainsed players in terms of market share going forward.

taxed at ~28% Balkrishna Ind, Bosch, Mahindra CIE

Financial Services Financial services will not be having any direct impact. Fee based services will get expensive for the customers to the extent of variation in GST over current service tax rate.

Service tax: 14% -

Consumer Durable

Currently consumer goods manufacturer are entails to pay Indirect taxes such as excise, VAT, CST, Octroi. However with the introduction of GST, indirect tax liability of At present consumer durable manufacturers

(without consideration of tax incentives) taxed GST 17 18%Bajaj Electricals, Havells

Consumer Durable the comoany would reduce substaintially, which would in turn augurs well either in terms of higher volume growth or better margins.

(without consideration of tax incentives) taxed at ~25%

GST 17-18%India, Voltas, V-guard

With the introduction of GST, FMCG companies with categories like Biscuits, Atta and packaged foods, would benefit organised players by bringing unorganised players under GST purview.and creating level playing field

Currently most unorganised players are exempted to pay excise duty on biscuits

~12% for essential goods Brittania, ITC

Government appointed panel recommends one demerit rate of 40% on tobacco and tobacco products with the flexibility to levy additional excise duty over & above GST.

C l ITC 51% (25 26% VAT S ifi 40% d i i d bFMCG tobacco products with the flexibility to levy additional excise duty over & above GST. We believe some part of the excise duty would be subsumed in GST. We also believe the GST rate could be static for atleast 2-3 years after its implementation, which could give some flexibility to the company in terms of price hikes.

Currently ITC 51% (25-26% VAT + Specific Excise duty)

40% demerit tax + excise duty by central government

Neutral

Introduction of GST would result in supply chain benefits for FMCG Industry as centralisation of warehouses would reduce operational cost substaintially

HUL, ITC, Dabur, Marico

Construction /

Currently, there is huge pricing difference between organised and unroganised players due to clandestine sales and tax evasion. Once GST comes into the picture, the Century Plyboard,

FMCG

7

Construction / Building Material

due to clandestine sales and tax evasion. Once GST comes into the picture, the organised player will get level playing field especially in verticals such as Tiles (Unorganised market: 40-45%) and plywood (Unorganised market: 70%-75%)

Excise Duty: 12.5% + State VAT: 12.35% GST 18% Kajaria Ceramics, & Somany Ceramics

..conti.

The logistics services are charged a service tax of 14.5% which are billed to the customers. However, post implementation of GST the rate is expected at 18%. This is also expected to be billed to customer. Hence, the quantitative impact would be neutral in nature.

Service tax @ 14.5% (incl. 0.5% swachh bharat cess)

GST < 20% Gati, Blue Dart

The sevice tax is paid on 4th or 5th of the month, however it is collected from the customer once the debtors are due. Hence the working captial cycle would be a bit elongatedQualitatively with GST implementation there would be a shift from a unorganized to

Logistic

organized market. GST would create a semaless movement of goods across which would reduce logistics costs. Further, due to consolidation of warehouses the larger players with larger warehouses will tend to benefit.Hotel rooms are subject to service tax of 8.4%. Luxury tax varies from state to state of 4-12.5%. So aggregate tax is around 12.4-20.5%.With the implementation of GST and anticipated tax rate of 18% will negatively impact Hotel sector. However, compliance cost will be lower due to uniform tax structure.

Service tax on rooms: 8.4% luxury tax on rooms : 4-12.5%

GST < 20%

The aggregate tax on F&B is 20.1. With the implementation of GST, the tax rate will be lower and help in reducing compliance

VAT on food : 14.5% Service tax on food bill: 5 6%

Hotel

lower and help in reducing compliance. Service tax on food bill: 5.6%GST proposes to impose 40% tax on aerated drinks compared to VAT of 20%. This will lead to higher pricing of non alcoholic beverages.

VAT on non alcholic beverage: 20%

Aviation

Sales tax in ATF ranges from 4-30% across states. However, majority of states charge sales tax in the range of 20-30%. Thus, with GST implementation the tax rate on ATF will be reduced and positively impact aviation sector.

ATF Sales tax : 4-30% GST < 20%

Textile & Apparel

We believe GST will be negative for Textile & Apparel sector assuming GST rate around 18-20%.Textile products doesn't have any excise duty, GST will result in higher taxes for the sector. On the flip side it will help organised players to have a level playing field

No Excise Duty on Textile & Apparel products. Sales tax of 2% on Yarn with no taxes on fabric segment. Other taxes levied includesTextile & Apparel

with unorganized sector which operates with thin margins dominated by cash transactions. GST isn't applicable on exports so would not impact textile exporting companies.

segment. Other taxes levied includes VAT(4.2%) along with surcharge & octroi. Total taxes excluding Service tax is ~7-8%.

RetailNon Apparel retailers can benefit from GST as it current tax stucture is much higher than proposed GST rate of 18-20%.

VAT 12% with Excise & other taxes total taxes are ~26% which is substantially higher than expected GST rate.

GST, will safeguard media companies across genres such as cable distributors, DTH, movie exhibitors, distributors from the brunt of double taxation by paying service tax to the Centre and entertainment tax to the state government. GST will lead to one uniform

1) 23-26% of entertainment tax on net ticketing revenues by multiplexes, 9-10% VAT , 14%

i tPVR Limited, Inox

Media / Telecomg

tax levy for companies and would be a positive for PVR, Eros, Hathway and Dish. In addition, the input tax credit offset available will further tone down the overall tax rate. The DTH players would get room for increase in the ARPU's in-line with the cable players as they increase the rates to pass on the impact of the GST.

service tax2) 5-6% entertainment tax by DTH, 14% service tax3) Service tax 14%

Leisure, Eros International, Dish TV

Cement

As cement companies supplies cement in home state and nearby states, they are subject to different tax rates across the state which impact cement prices. The aggregate indirect tax in the industry is ~24-26%.With GST in place, the effective rate will be lowered and help in lowering cement prices. Also compliance cost of cement companies will be substantially lowered on account of uniform tax structure

Excise duty: 10-12.3% VAT : 12.5% other taxes : 1.3% Total effective tax rate : 24-26%

GST < 20%

8

companies will be substantially lowered on account of uniform tax structure.

Deal Team – At Your ServiceDerivatives and Quantitative Outlook

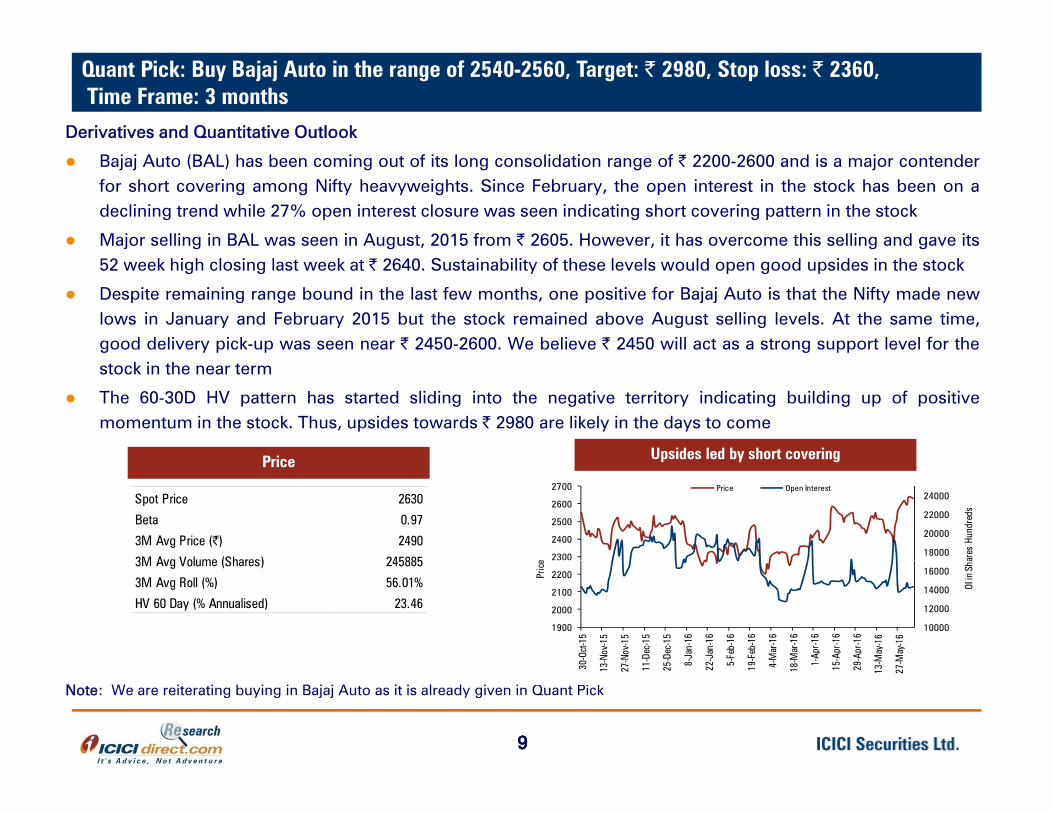

Quant Pick: Buy Bajaj Auto in the range of 2540-2560, Target: | 2980, Stop loss: | 2360,Time Frame: 3 months

Bajaj Auto (BAL) has been coming out of its long consolidation range of | 2200-2600 and is a major contenderfor short covering among Nifty heavyweights. Since February, the open interest in the stock has been on adeclining trend while 27% open interest closure was seen indicating short covering pattern in the stock

Major selling in BAL was seen in August, 2015 from | 2605. However, it has overcome this selling and gave its52 week high closing last week at | 2640. Sustainability of these levels would open good upsides in the stock

Despite remaining range bound in the last few months, one positive for Bajaj Auto is that the Nifty made newlows in January and February 2015 but the stock remained above August selling levels. At the same time,good delivery pick-up was seen near | 2450-2600. We believe | 2450 will act as a strong support level for thestock in the near term

The 60-30D HV pattern has started sliding into the negative territory indicating building up of positivemomentum in the stock. Thus, upsides towards | 2980 are likely in the days to come

P i Upsides led by short coveringPrice Upsides led by short covering

18000

20000

22000

24000

2300

2400

2500

2600

2700

ares

Hund

reds

e

Price Open Interest

Spot Price 2630

Beta 0.97

3M Avg Price (|) 2490

3M Avg Volume (Shares) 245885

10000

12000

14000

16000

1900

2000

2100

22000-

Oct-1

5

-Nov

-15

-Nov

-15

-Dec

-15

5-De

c-15

8-Ja

n-16

2-Ja

n-16

5-Fe

b-16

9-Fe

b-16

-Mar

-16

-Mar

-16

1-Ap

r-16

5-Ap

r-16

9-Ap

r-16

-May

-16

-May

-16

OI in

Sh a

Pric

e3M Avg Volume (Shares) 245885

3M Avg Roll (%) 56.01%

HV 60 Day (% Annualised) 23.46

9

Note: We are reiterating buying in Bajaj Auto as it is already given in Quant Pick

9

30 13 27 11 25 8 22 5 19 4 18

1 15 29 13-

27-

Deal Team – At Your ServiceDerivatives and Quantitative Outlook

C t t k j t f l ith i t t b ki i th t t d f th

Quant Pick : Buy Ambuja Cement in the range of 227-231, Target: | 274, Stop loss: | 207,Time Frame: 3 months

Cement stocks were major outperformers along with private sector banking in the recent up trend of themarket. Stocks like Ambuja Cement gained close to 20% from their February lows amid sustained deliverybased buying. We expect the current momentum in the space to continue towards its 2014 high levels

The stock witnessed six month high delivery based buying on May 26, 2016 near | 220. Follow up buying isl l id h k h l d d h l l Si M h A b j C hclearly evident as the stock has already surpassed these levels. Since March, Ambuja Cement has seen some

fatigue near | 230. We believe the stock will find further momentum once it is able to sustain these levels

Open interest in Ambuja Cement has increased sharply during the up move seen in the March series. Despitemarginal liquidation, open interest in the stock is still high indicating prevailing long positions in the stock

The 60D HV remains in a declining trend for the stock. The spread is still positive with respect to 30D volatility.There is ample room for the near term volatility to subside from current levels, which should help the stock tomove higher

L OI i i k

Spot Price 229

Beta 1.02

3M Avg Price (|) 224

M A V l (Sh ) 0

Price

80000

100000

120000

215

225

235

245

sHu

ndre

ds

Price Open Interest

Long OI intact in stock

Note: Call initiated on iClick2Gain on June 06 2016

3M Avg Volume (Shares) 2304836

3M Avg Roll (%) 50.62%

HV 60 Day (% Annualised) 25.75

0

20000

40000

60000

175

185

195

205

215

t-15

v-15

v-15

c-15

c-15

n-16

n-16

b-16

b-16 r-1

6

r-16

r-16

r-16

r-16

y-16

y-16

OI in

Sha

re

Pric

e

10

Note: Call initiated on iClick2Gain on June 06, 2016

10

30-O

ct

13-N

ov

27-N

ov

11-D

ec

25-D

ec

8-Ja

n

22-J

an

5-Fe

b

19-F

eb

4-M

ar

18-M

ar

1-Ap

r

15-A

pr

29-A

pr

13-M

ay

27-M

ay

Deal Team – At Your ServiceDerivatives and Quantitative Outlook

FMCG d d bl t k h i d i th li li ht t th t f d d

Quant Pick : Buy Godrej Industries in the range of | 357-363, Target: | 428 , Stop loss: | 324, Time Frame: 3 months

FMCG and consumer durable stocks have remained in the limelight at the onset of monsoon and recoveredsharply. Further strengthening in the space is likely to be seen if the GST bill is passed in the upper house.Godrej Industries is one such stock, which remained range bound for quite some time and is now likely tobreach the range on the higher side. We expect the stock to move towards | 430 levels in the days to come

Th i t t i G d j I d t i h ti d t d li i th l t l f th i di ti lThe open interest in Godrej Industries has continued to decline in the last couple of months indicating closureof short positions. Current OI in the stock is lowest since June 2015 and fresh long accumulation is likely totake the stock higher

Noteworthy delivery based buying was observed in the stock near | 340 levels in the last couple of months.Af h l l h k did b h h l l W b li h i i bi i h kAfter the quarterly results, the stock did not breach these levels. We believe the positive bias in the stockshould be maintained while declines towards these levels remain buying opportunities

The 60D-30D HV pattern has started sliding into the negative territory indicating building up of positivemomentum in the stock. We believe there is ample room for volatility to subside in the stock

Price Recovery led by short covering

Spot Price 362

Beta 0.96

3M Avg Price (|) 35225000

30000

35000

40000

45000

350

370

390

Hund

reds

Price Open Interest

3M Avg Volume (Shares) 278235

3M Avg Roll (%) 74.00%

HV 60 Day (% Annualised) 21.41

0

5000

10000

15000

20000

25000

250

270

290

310

330

15 15 15 15 15 -16

-16

-16

-16

-16

-16

-16

-16

-16 16 16

OI in

Sha

res

Pric

e

11

Note: Call initiated on iClick2Gain on June 06, 2016

11

30-O

ct-

13-N

ov-

27-N

ov-

11-D

ec-

25-D

ec-

8-Ja

n-

22-J

an-

5-Fe

b-

19-F

eb-

4-M

ar-

18-M

ar-

1-Ap

r-

15-A

pr-

29-A

pr-

13-M

ay-

27-M

ay-

Pankaj Pandey Head – Research [email protected] Research Desk,ICICI Securities Limited,1st Floor, Akruti Trade Centre,Road no.7, MIDCAndheri (East)Mumbai – 400 093research@icicidirect [email protected]

12

DisclaimerANALYST CERTIFICATION

W /I A it G t B E MBA (Fi ) R j D k Si h BE MBA (Fi ) A Ah d MBA (Fi ) R h A l t th d thWe /I, Amit Gupta B.E, MBA (Finance), Raj Deepak Singh BE, MBA (Finance), Azeem Ahmad MBA (Fin) Research Analysts, authors and thenames subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about thesubject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specificrecommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:ICICI Securities Limited (ICICI Securities) is a Sebi registered Research Analyst having registration no. INH000000990. ICICI Securities Limited(ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distributionof financial products. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has itsof financial products. ICICI Securities is a wholly owned subsidiary of ICICI Bank which is India s largest private sector bank and has itsvarious subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fundmanagement, etc. (“associates”), the details in respect of which are available on www.icicibank.com.ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets inIndia. We and our associates might have investment banking and other business relationship with a significant percentage of companiescovered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and theirrelatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report

d i f ti t i d h i i t i tl fid ti l d t l l f th l t d i i t d t b lt d iand information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way,transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without priorwritten consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securitiesisunder no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may preventICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and suchsuspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might beacting in an advisory capacity to this company, or in certain other circumstances.This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has

f f fbeen made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shallnot be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financialinstruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICISecurities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal,accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. Thesecurities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investmentdecisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken insubstitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks.Th l d i b f h i i f i h h ICICIThe value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICISecurities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is notnecessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated beforeinvesting in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements arenot predictions and may be subject to change without notice.ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might havebeen mandated by the subject company for any other assignment in the past twelve months.ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period

13

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the periodpreceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporatefinance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchantbanking or brokerage services from the companies mentioned in the report in the past twelve months.ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report.ICICI Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third partyin connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material conflictof interest at the time of publication of this report.It is confirmed that Amit Gupta B E MBA(Finance) Raj Deepak Singh BE MBA(Finance) Azeem Ahmad MBA (Fin) Research Analysts ofIt is confirmed that Amit Gupta B.E, MBA(Finance), Raj Deepak Singh BE, MBA(Finance), Azeem Ahmad MBA (Fin), Research Analysts ofthis report have not received any compensation from the companies mentioned in the report in the preceding twelve months.Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage servicetransactions.ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Companymentioned in the report as of the last day of the month preceding the publication of the research report.Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficialownership in various companies including the subject company/companies mentioned in this report.ownership in various companies including the subject company/companies mentioned in this report.It is confirmed that Amit Gupta B.E, MBA(Finance), Raj Deepak Singh BE, MBA(Finance), Azeem Ahmad MBA (Fin), Research Analysts donot serve as an officer, director or employee of the companies mentioned in the report.ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the inf,ormation presented inthis report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity ResearchWe submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity ResearchAnalysis activities.This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in anylocality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation orwhich would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securitiesdescribed herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession thisdocument may come are required to inform themselves of and to observe such restriction.

14