QP Case Report - PR Newswire MMSmms.prnasia.com/hkicpa/20141207/winning/1st_runner-… · ·...

36

CASE REPORT 2014 QP Case Analysis competition (PRC) Tango Co. CEO Kay COO Lena CFO Jade External Consultant Yaphet

Transcript of QP Case Report - PR Newswire MMSmms.prnasia.com/hkicpa/20141207/winning/1st_runner-… · ·...

CASE REPORT

2014 QP Case Analysis competition (PRC)

Tango Co.

CEO Kay

COO Lena

CFO Jade

External Consultant Yaphet

Is the investment in Tango promising?

Content

Operational Performance

Financial Performance

SWOT Analysis & Strategy Development

Internal Valuation

Ethical Dilemma

4

3

2

1

5

Operational Performance

3C Model

Company

Customer

Competitor

01

“Cash Cow”

Business “Dog”

Business “Star”

Business

ompany C

• High market share

• Low growth rate

• Generate cash to support

other departments

• Low market share

• Low growth rate

• Decline in Hong Kong

and Singapore market.

• Low market share

• High growth rate

• Great develop potential

with further expansion

Beauty & facial

Spa & massage

Retail products Slimming

&

fitness

High-end customers High stress groups Customers with discretionary

spending capacity

Number of wealthy families

and professional women

increases throughout South

East Asia.

Customers need services to

relax deeply and to shut off

the brain-chatter from the

daily stresses.

ustomer C

Beauty and facial division

Slimming and fitness division Spa and massage division Retail products division

People who cannot afford expensive

courses of treatment are doing ‘the

next best thing’ by buying luxury

treatment products.

ompetitor C

Competitive

Rivalry

-- Porter’s Five Forces

Threat of new

entrants

Threat of

substitutes

New entrants can hardly gain a foothold in the market

• However, foreign giant companies with long history and good reputation will be

strong competitors once entering Asia market.

Tango’s products and services are highly complementary

• Skincare can be done through both facial treatments and consumption of products

• Slimming can be done through both slimming courses and spa and massage

Strengths

• Low costs

• Specialized market

• Flexible purchasing channel

Weaknesses

• Small capital size

• Less brand recognition

• Poor change management

Situation of existing competitors

BCG Business Model:

Company

Customer

Competitor

Cost Analysis

Ratio Analysis

Segmental Analysis

Financial Performance 02

Cost Analysis

(2)

(3)

COST Analysis

The decline in

profit was mainly

due to increasing

operating costs. 7.92%

Employee benefit

expenses

Bank charges

Advertising and

marketing

Other operating expenses

15.38%

20%

23.26%

Due to high employee turnover in the

industry, employee benefit expenses is

unavoidable to retain Tango’s top

beauticians and medical experts. So, It

is hard and unreasonable to reduce this

type of expense.

7.98%

Cost Analysis

(2)

(3)

COST Analysis

56%

9%

5% 2%

28%

%of detailed costs towards operating cost

Employee benefitexpenses

Other operatingexpenses

Bank charges

Advertising andmarketing

Others

56% Employee benefit expenses

Ratio Analysis

(1)

(3)

Current ratio

Inventory turnover

Receivable turnover

Basic earning ratio

ROE

ROA

P/E ratio

M/B ratio

EPS

-30 -25 -20 -15 -10 -5 0 +5

RATIO Analysis

Solvency Ratio

Profitability Ratio

Market Value Ratio

Ratio Analysis

(1)

(3)

Inventory turnover

ROA

M/B ratio

-30 -25 -20 -15 -10 -5 0 +5

1.76%

-25.86%

-17.29%

Solvency Ratio

Profitability Ratio

Market Value Ratio RATIO Analysis

Segmental

Analysis

Beauty and facial

Slimming and fitness

Spa and massage

Retail products

(2)

(1)

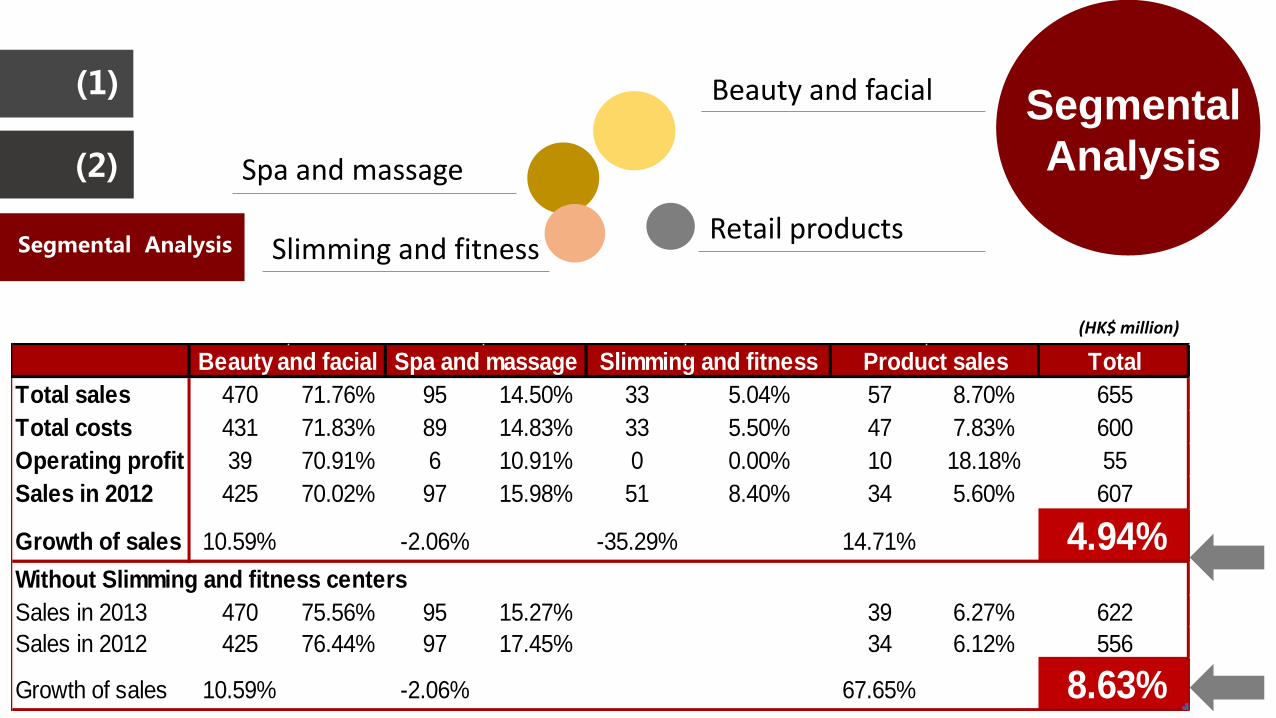

Segmental Analysis

Total

Total sales 470 71.76% 95 14.50% 33 5.04% 57 8.70% 655

Total costs 431 71.83% 89 14.83% 33 5.50% 47 7.83% 600

Operating profit 39 70.91% 6 10.91% 0 0.00% 10 18.18% 55

Sales in 2012 425 70.02% 97 15.98% 51 8.40% 34 5.60% 607

Growth of sales 10.59% -2.06% -35.29% 14.71% 4.94%Without Slimming and fitness centers

Sales in 2013 470 75.56% 95 15.27% 39 6.27% 622

Sales in 2012 425 76.44% 97 17.45% 34 6.12% 556

Growth of sales 10.59% -2.06% 67.65% 8.63%

Product salesSlimming and fitnessSpa and massageBeauty and facial

(HK$ million)

Total

Total sales 470 71.76% 95 14.50% 33 5.04% 57 8.70% 655

Total costs 431 71.83% 89 14.83% 33 5.50% 47 7.83% 600

Operating profit 39 70.91% 6 10.91% 0 0.00% 10 18.18% 55

Sales in 2012 425 70.02% 97 15.98% 51 8.40% 34 5.60% 607

Growth of sales 10.59% -2.06% -35.29% 14.71% 4.94%Without Slimming and fitness centers

Sales in 2013 470 75.56% 95 15.27% 39 6.27% 622

Sales in 2012 425 76.44% 97 17.45% 34 6.12% 556

Growth of sales 10.59% -2.06% 67.65% 8.63%

Product salesSlimming and fitnessSpa and massageBeauty and facial

(HK$ million)

Segmental

Analysis (2)

(1)

Segmental Analysis

Showing by the table, growth rate of sales without

Slimming and Fitness Centres is 8.63%, while

the original growth rate is 4.94%.

3.69%

The Company can

perform better if it sells

out or closes down this

division.

Four Strengths • Cash rich position

• Large capital size • High liquidity

• High dividend payment

Strategy Development

SWOT Analysis

Expansion Strategies

Penetration Strategies

03

O S

T W

• High quality products and professional services

• Leading position in the industry

• High financial and operational liquidity

• Stable customer groups

• Strong brand

• Decline of the Slimming and Fitness Centres

• Defective cost management

• Potential market in Mainland China

• Growth trend of products retail in beauty industry

• E-commerce is widely accepted

• Insufficiently satisfied male market

• Small and specialized competitors

• Entrance of giant foreign firms

• Changing of consumers’ tastes

Increasing Outlets

Mainland China

Hong Kong & Singapore

Rising living standard – increasing number of potential customers

Expand business in big cities - Beijing, Shanghai and Shenzhen

High rental cost - economical to locate new outlets in suburbs

New concepts - “human and nature harmony” and “traditional Chinese regimen”

Fresh air and beautiful sceneries

Expansion Strategies Exploring new market

Raising market share

Introduce Male Products and Services

1. Spa and massage services

2. Slimming and fitness courses

3. Facial services

- Boxing, Muay Thai and gym exercises

- Basic massage as well as family services

- Depending on customers’ acceptance

Time Line

Exploring Male Market

Expansion Strategies Exploring new market

Raising market share

Develope Online Platform

Cooperate with Taobao T-mall (Tianmao) Flagship Store

Rapid development and widely acceptance of online shopping

Serve markets outside Hong Kong with low cost and few geographic limitations

Expansion Strategies Exploring new market

Rising market share

Enrich Import Sources

Importing products from other countries

e.g. Italy, Australia, Japan and South Korea - good reputation in the field

Japanese products - good at makeup & high quality standard

South Korean products - reputation in skincare & lower price level

With products from different countries:

• Different features and specialties - satisfy various demands

• Diversified products – stabilize products sources & hedge cost rising risk

Penetration Strategies Improving existing products & services

Better serving existing customers

Asian Features

Special design for Asians

Services - scrapping therapy, dietary therapy and Moxibustion

Products - Chinese medicine ingredients

Without chemical additives - safety

With Asian features, Tango can:

• Better serve Asian customers

• Superior in competition with foreign entrants

Penetration Strategies Improving existing products & services

Better serving existing customers

Market Segmentation

Three-level Retail Outlets

High level - products priced for over HK$1,000

Middle level - products priced around HK$500 to HK$1,000

Low level - products priced between ¥300 to¥500

With clear segmented market, customers can:

• Save searching cost

• Choose proper products based on purchasing power

Penetration Strategies Improving existing products & services

Better serving existing customers

( For Mainland China market )

Providing a wide range of health and beauty services & products to markets both inside and outside Hong Kong.

Vision

Internal Valuation

Cash Flow Forecasting

Scenario Analysis

04

Cash Flow Forecasting 2014 2015 2016 2017 2018 2019-2023 2024-2028 2029-2033

Profit before interest and tax 55 8.50% 59.68 64.75 70.25 76.22 82.70 531.69 799.48 1,202.14

Depreciation 26 9.00% 28.34 30.89 33.67 36.70 40.00 260.96 401.52 617.79

Increase in inventory (1) 15.00% (1.15) (1.32) (1.52) (1.75) (2.01) (15.60) (31.37) (63.09)

Increase in receivables,

deposits and prepayments (33) 10.00% (36.30) (39.93) (43.92) (48.32) (53.15) (356.91) (574.81) (925.74)

Increase in trade payables

and accruals 5 8.00% 5.40 5.83 6.30 6.80 7.35 46.55 68.39 100.49

Increase in deferred revenue 71 8.50% 77.04 83.58 90.69 98.40 106.76 686.36 1,032.05 1,551.85

Net purchase of PPE (39) 10.00% (42.90) (47.19) (51.91) (57.10) (62.81) (421.81) (679.32) (1,094.06)

Increase in cash before

interest and tax84 90.10 96.61 103.55 110.96 118.84 731.24 1,015.94 1,389.38

7.26% 7.23% 7.19% 7.15% 7.11% 6.97% 6.69% 6.31%

6.79%78.35 73.05 68.09 63.44 59.09 239.23 165.37 112.55

859.16

Cash Flow Forecasting

Growth Rate

Average Growth Rate

Present Value of future cash flows

Total present value of future cash flows

2013Change rate

(HK$ million)

• Discount rate: 15% which is the return Tango promises to investors

• Business expansion strategies are taken.

• 8.5% growth in EBIT because it is the growth of Sales

without Slimming and fitness centres

Scenario Analysis Boom Decline 2014-2017 2018-2033 2014-2017 2018-2033

Profit before interest and tax 55 10.00% 5.00% 280.78 3,184.36 248.91 1,660.65

Depreciation 26 10.00% 5.00% 132.73 1,505.33 117.67 785.03

Increase in inventory (1) 18.00% 0.00% (6.15) (166.87) (4.00) (16.00)

Increase in receivables,

deposits and prepayments(33) 15.00% 8.00% (189.50) (3,698.24) (160.60) (1,470.36)

Increase in trade payables

and accruals5 10.00% 7.00% 25.53 289.49 23.75 195.57

Increase in deferred

revenue71 15.00% 6.00% 407.71 7,956.81 329.23 2,439.25

Net purchase of PPE (39) 15.00% 5.00% (223.95) (4,370.64) (176.50) (1,177.55)

Increase in cash before

interest and tax84 427.14 4,700.24 378.47 2,416.60

9.68% 4.51%

1,098.89 733.8

Decline

Average Growth Rate

Present value of total future cash flows

Cash Flow Forecasting 2013Change rate Boom

(HK$ million)

• Discount rate: 15% which is the return Tango promises to investors.

• Boom (decline) situation is defined as one-third increasing (decreasing) in market factors relative to normal situation.

Ethical Dilemma

05

Blood Transfusion

Treatment

Disclosure of refund

Ethical Dilemma

05

Accept/ Reject the proposal Whether launch blood transfusion treatment to minimize potential refund

derived from closing down Slimming and Fitness Centres.

Disclosure/ Nondisclosure the refund Whether disclose the refund which has impacts on the transparency of

the Company’s financial reports.

COO

Business Angle

• Increase profits of the Company

• Keep original customers

• Eliminate potential refund

If launch

• Customers’ safety can be better

protected

• Build a responsible company image

If not launch

1. Solution

on

Proposal

Disclose refund Close the division in a

controllable speed

Postpone launch

Action Plan

Business angle

Reject the proposal !

• Enhance transparency

• Responsible for investors

Long-run

HK$20 Million Refund !

Short-run

Not disclose

• Decorate the company’s

financial performance

Disclose

• Face financial burden

2. Solution

on

Refund

Consultant

Regulatory Angle

Company Ordinance Cap.622 s.456(1)

A director must exercise reasonable care, skill and diligence that would be

exercised by a reasonably diligent person.

Common Law

A director, owes to the company a fiduciary duty, must act honestly and in

good faith when exercising all of the powers conferred upon him by the

Article of Association.

• Care about minor shareholders • Meet the standard of disclosure requirement

• Can not gain personal benefit from using of his position as a director • Can not hide information to attract more investors without fully disclosure

Duty of skill and care

Fiduciary duties

CPA Angle

CFO

• Fundamental principles under HKICPA Code of Ethics • Threats and safeguards of self-interest • Conflict of interests

S100.5:Five Fundamental Principles: Integrity, Objectivity, Professional competence & due care,

Confidentiality and Professional behavior.

S300.5:A professional accountant in business is expected to encourage an ethics-based culture in

an employing organization that emphasizes the importance that CFO places on ethical behavior.

S300.6: A professional accountant in business shall not knowingly engage in any business,

occupation, or activity that impairs or might impair integrity, objective or the good reputation of the

profession and as a result would be incompatible with the fundamental principles.

S300.8 of Code of Ethics, incentive compensation arguments was included in the self-interest

threats for a professional accountant in business.

HKICPA Code of Ethics

Statement 1.203:A practice should not accept or continue an

engagement in which there is a significant conflict of interest between the practice and its clients.

Professional Ethic Statement

Refund will be disclosed

Conclusion

Leading position in the industry

Responsible company

Internal valuation 4 4

3

1

5

Balance interests of all stakeholders

Multi-businesses and stable financial performance

Under-valued by market

2 Strategy development Expansion strategies and penetration strategies

The investment in Tango is promising !

Q&A