QDI Strategies: Brand and Channel Strategy Project Example

26

COPYRIGHT 2015 QDI STRATEGIES, INC. QDI: Brand and Channel Strategy Leverage Project Example

-

Upload

michael-barr -

Category

Marketing

-

view

3.266 -

download

3

Transcript of QDI Strategies: Brand and Channel Strategy Project Example

COPYRIGHT 2015 QDI STRATEGIES, INC.

QDI: Brand and Channel Strategy Leverage

Project Example

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand & Channel Strategy Options

• One of QDI’s clients had grown very rapidly by selling several of their brands through Home Depot. However, this also resulted in lower margins, declining sales in the specialty channels, and a sense that the value of their lead brand had declined.

• The client and QDI put together a team to look at their brand position and alternative channel and brand strategies.

• This presentation highlights the models QDI developed to drive the channel and brand strategy discussions. The presentation shows examples of alternative strategies with operating profits that exceed the base line strategy by as much as $30 Million. It also shows it is possible to reverse the brand deterioration that was happening to all of their brands.

Methodology to Support Brand & Channel Strategy

Decisions for Profit Maximization

COPYRIGHT 2015 QDI STRATEGIES, INC.

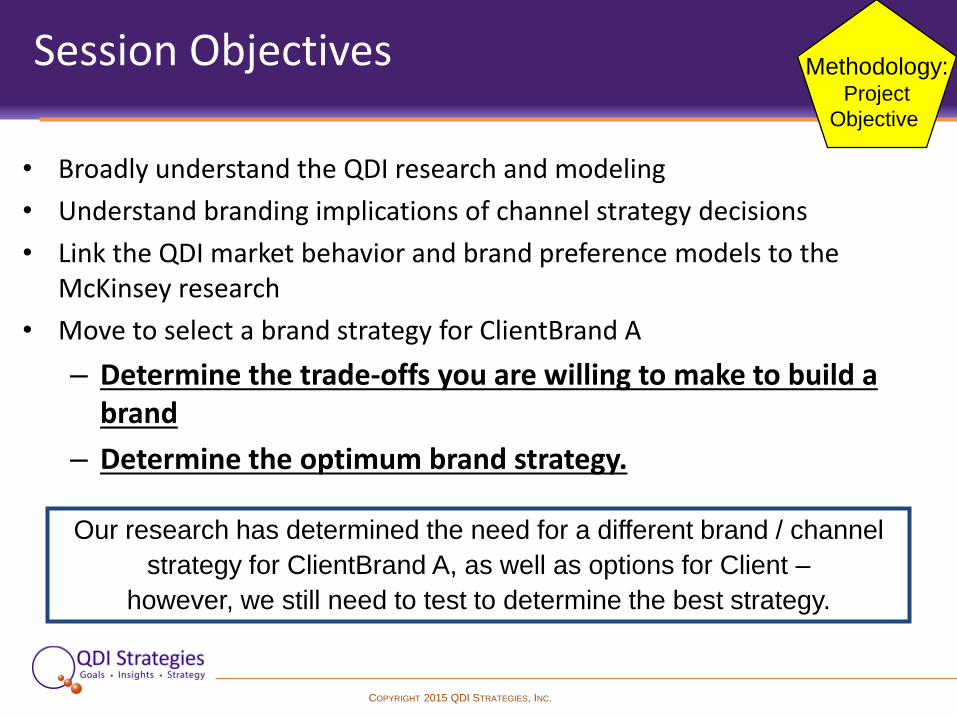

Session Objectives

• Broadly understand the QDI research and modeling

• Understand branding implications of channel strategy decisions

• Link the QDI market behavior and brand preference models to the McKinsey research

• Move to select a brand strategy for ClientBrand A

– Determine the trade-offs you are willing to make to build a brand

– Determine the optimum brand strategy.

Our research has determined the need for a different brand / channel

strategy for ClientBrand A, as well as options for Client –

however, we still need to test to determine the best strategy.

Methodology: Project

Objective

COPYRIGHT 2015 QDI STRATEGIES, INC.

QDI Research and Modeling

• Market research – Quantitative brand preference and shopping behavior research

• 400 contractors & 400 DIY

– Qualitative research

• Approximately 75 each of interviews

– Contractors / Cabinet shops / DIY consumers / Industrial distributors / Channels

– Analog interview to understand how other manufacturers are dealing with market power, particularly partnering

• Market modeling – Switching behavior

– Channel value

– Market performance projections, based on alternative strategies

Methodology: Project

Approach

COPYRIGHT 2015 QDI STRATEGIES, INC.

Market Dynamics

• Channel Structure

– Home Depot will grow to about 1/3 of the total market in 2003

• Home Depot is gaining presence and is expected to grow its share by 25% over next 3 years, from 28.2% – 34.1%

– Lowe’s and Sears are the only other significant companies in the market, each with about 10% of the market

• Lowe’s is gaining presence and is expected to grow its share by 21.6% over next 3 years, from 10.4% - 12.7%

• Sears is holding its own at about 10%

– The industrial channel is the fourth major player with thousands of companies that, together, account for about 20% of the market

– Sears is a much more significant player in the professional and Sophisticated DIY segments than previously believed

Methodology: Understand

Market

Behavior

COPYRIGHT 2015 QDI STRATEGIES, INC.

Market Dynamics

• ClientBrand A brand dynamics – A “project buyer” market exists that is different than the “cradle-to-grave”

model that ClientBrand A’s Strategy is based on

– Asian sourcing and aggressive purchasing by Home Depot have pushed the market pricing down to levels where traditional professional tools (table saws) are now available at DIY prices ($99)

– Both have significant, negative impact on traditional “cradle-to-grave” branding strategy

• Client dynamics – Linking ClientBrand B, ClientBrand A and ClientBrand C has weakened the

channel power of each organization

– Many in the market believe ClientBrand A has lost focus in the combination

– Channel and brand decisions have continued to be made independently within Client

Methodology: Understand

Market

Behavior

COPYRIGHT 2015 QDI STRATEGIES, INC.

Client Decisions

• Client needs to make some brand and channel decisions

• The combination of channel power, brand power and channel conflict establish Client’s channel strategy alternatives – ClientBrand B is a powerful brand that most channels must stock

– ClientBrand A is losing power, and only holds an enviable position within the high-end, professional market

– ClientBrand C has no brand power, as it has (historically) been a quasi-private label

• The three brands together have a weak power position, with less than 32% of revenue from product lines with high-brand power positions

• The result is that Client is forced to operate from a position of weakness – Client is being forced to “pick a partner” for the ClientBrand A DIY and ClientBrand C

product lines in situations that involve high levels of channel conflict and high-power channels

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

Client’s Brands Have Less Than a 32% Power Position

42%

18%

7%4%

28%

0%

20%

40%

60%

80%

100%

% of Sales

Client Brand Power Positions

ClientBrand B

ClientBrand A Industrial

ClientBrand B - Low Share

ClientBrand A DIY

ClientBrand C

Potential Repositioning

of ClientBrand A &

ClientBrand B as High-

Power Brands

High Power

Low Power

Brand power is a function of consumer preference

• The degree of preference for the brand by customers who prefer it

• The percentage of customers who prefer that brand versus other brands

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

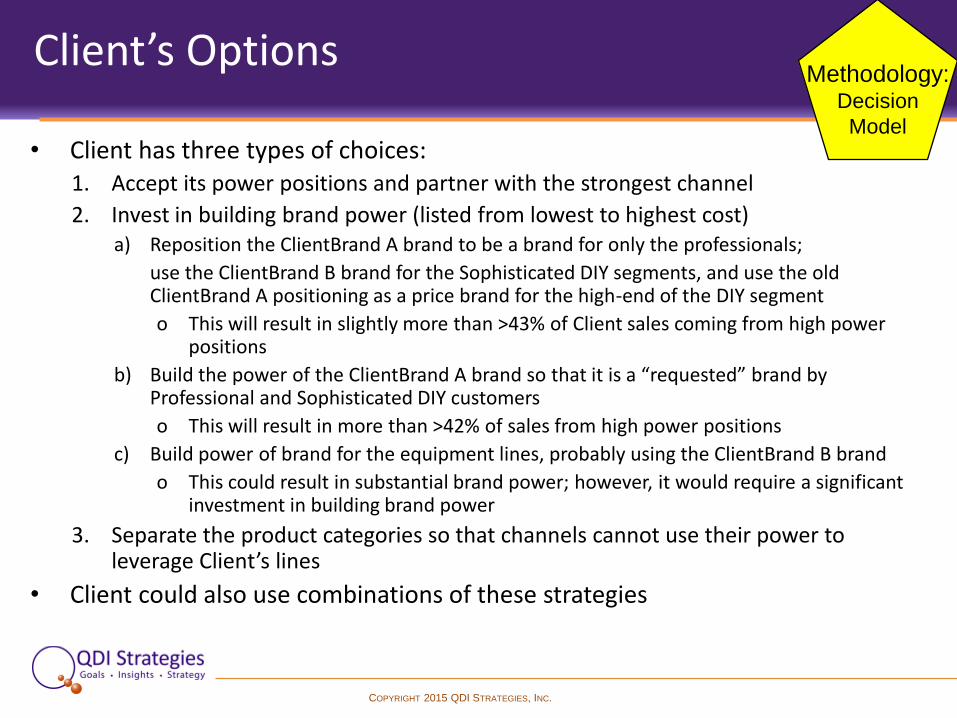

Client’s Options

• Client has three types of choices: 1. Accept its power positions and partner with the strongest channel

2. Invest in building brand power (listed from lowest to highest cost) a) Reposition the ClientBrand A brand to be a brand for only the professionals;

use the ClientBrand B brand for the Sophisticated DIY segments, and use the old ClientBrand A positioning as a price brand for the high-end of the DIY segment

o This will result in slightly more than >43% of Client sales coming from high power positions

b) Build the power of the ClientBrand A brand so that it is a “requested” brand by Professional and Sophisticated DIY customers

o This will result in more than >42% of sales from high power positions

c) Build power of brand for the equipment lines, probably using the ClientBrand B brand

o This could result in substantial brand power; however, it would require a significant investment in building brand power

3. Separate the product categories so that channels cannot use their power to leverage Client’s lines

• Client could also use combinations of these strategies

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

Each Strategy Has a Different Impact on Client’s Brand Power

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Base 2000 Base 2003 Strategy B +ClientBrandC Chnls +

Small Sears

Strategy A-4+ Sears +

ClientBrandC Chnls

44% 44% 42% 39%

24% 21%17% 18%

32% 35%42% 43%

% of Sales from each Brand Power Position

Alternative Strategies

Market Power Strategy Results

High Power - ClientBrand B's 1s +50% of ClientBrand B's 2s and 3s +

Industrial Line

Medium Power - ClientBrand A's 1s -(ClientBrand A 1 Industrial) and

ClientBrand C to Channels O/T HD -L - S (in Base Strategies - 60% of

ClientBrand A's 1s Move to HighPower in Strategy B and A-4)

Low Power - All Other Products

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

Client Trade-Offs

• Each strategy option has a different impact on business performance,

based on the following measures:

– Brand power – as measured by the customer’s preference for a brand (and, conversely, a channel’s cost - or difficulty - in dropping a brand)

• Brand power also results in higher manufacturer margins, as evidenced by the margins or ClientBrand B “1” products (40%), versus ClientBrand A “1” products (31%)

– Channel power – the ability of a manufacturer to select his own channels and to implement channel strategies that are consistent with his overall marketing strategy (based on the percentage of a manufacturer’s total sales that are both high-brand power - and within the specific channel)

– Operating performance • Contribution margins (after all marketing and G&A expenses)

• Total operating profit dollars

• Sales growth / share growth

• Client needs to determine the relative importance of each of these outcomes

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand Strategy Issues to Consider

• Strategic positioning vs. competition

– Don’t copy Brand 5 / Brand 1

– Don’t lose position to Brand 6

• Channel reactions

– Home Depot will not let you build a brand at their expense

– Lowe’s will have to be sold on any ClientBrand A strategy

• Consumer / contractor reactions

– Unknown value of ClientBrand A brand franchise, relative to ClientBrand B and Brand 1, when they are offered in place of ClientBrand A

• Business performance impact

– Different strategies have different outcomes in QDI models

ClientBrand B Space

ClientBrand A

Space

XYZ by ClientBrand

A

ClientBrand A Pro?

ClientBrand B?

Both?

Or ClientBrand A

ClientBrand A Pro?

ClientBrand B?

Both?

Or ClientBrand A?

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

Level-Set Questions

• Has the research convinced you: – That you need a ClientBrand A brand strategy?

– That there is a significant risk of switching ClientBrand A customers to ClientBrand B – they may have been loyal to ClientBrand A, and the switch may make them available to Brand 1, possibly giving Brand 1 1/3 – 1/2 of our ClientBrand A business?

– That you should aggressively expand ClientBrand C sales - outside of Home Depot, Lowe’s and Sears?

– That you should give the ClientBrand B brand of equipment, exclusively, to Home Depot?

– That a Sears strategy is possible, consistent with ClientBrand A strategies and consistent with building your channel power?

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

Models We have Build

• Projection of Sales & Profit by Product line & Channel – Three year analysis

– Examine profit impact of alternatives

• by product line & channel over time

– Examine Profit Contribution by Channel (marketing Cost)

• Projection of market shares within a channel based on consumer preference – Measures share/sales impact of alternative channel strategies

• By product lines within the channel

– Will use the model for scenario planning

• Projection of EVA channel – Can be adjusted for different channel strategies

Methodology: Decision

Model

COPYRIGHT 2015 QDI STRATEGIES, INC.

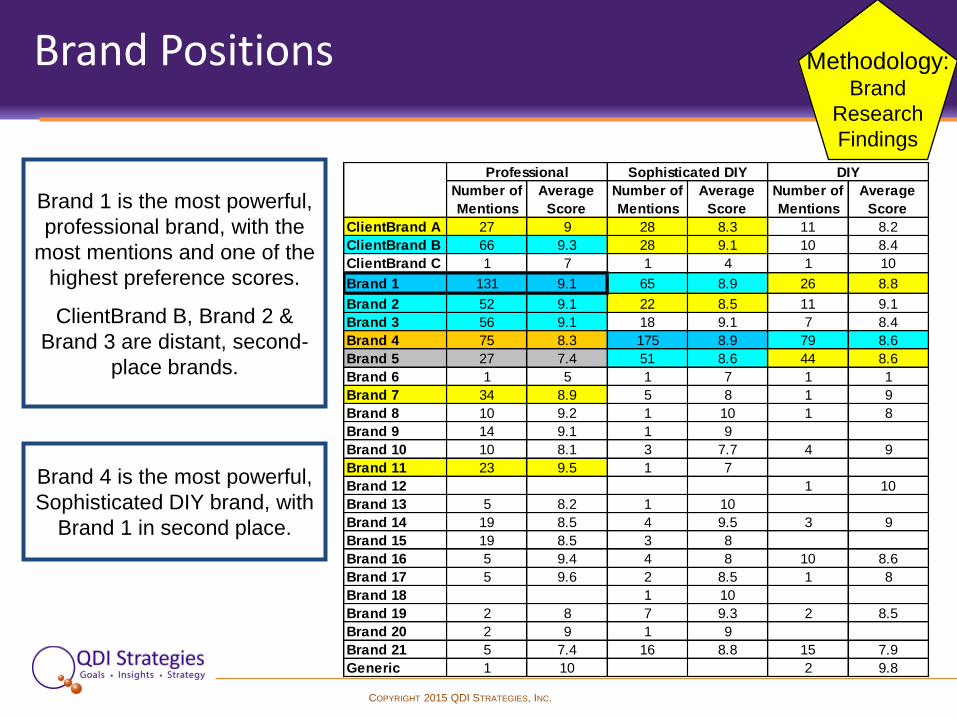

Brand Positions

Brand 1 is the most powerful,

professional brand, with the

most mentions and one of the

highest preference scores.

ClientBrand B, Brand 2 &

Brand 3 are distant, second-

place brands.

Brand 4 is the most powerful,

Sophisticated DIY brand, with

Brand 1 in second place.

Number of

Mentions

Average

Score

Number of

Mentions

Average

Score

Number of

Mentions

Average

Score

ClientBrand A 27 9 28 8.3 11 8.2

ClientBrand B 66 9.3 28 9.1 10 8.4

ClientBrand C 1 7 1 4 1 10

Brand 1 131 9.1 65 8.9 26 8.8

Brand 2 52 9.1 22 8.5 11 9.1

Brand 3 56 9.1 18 9.1 7 8.4

Brand 4 75 8.3 175 8.9 79 8.6

Brand 5 27 7.4 51 8.6 44 8.6

Brand 6 1 5 1 7 1 1

Brand 7 34 8.9 5 8 1 9

Brand 8 10 9.2 1 10 1 8

Brand 9 14 9.1 1 9

Brand 10 10 8.1 3 7.7 4 9

Brand 11 23 9.5 1 7

Brand 12 1 10

Brand 13 5 8.2 1 10

Brand 14 19 8.5 4 9.5 3 9

Brand 15 19 8.5 3 8

Brand 16 5 9.4 4 8 10 8.6

Brand 17 5 9.6 2 8.5 1 8

Brand 18 1 10

Brand 19 2 8 7 9.3 2 8.5

Brand 20 2 9 1 9

Brand 21 5 7.4 16 8.8 15 7.9

Generic 1 10 2 9.8

Professional Sophisticated DIY DIY

Methodology: Brand

Research

Findings

COPYRIGHT 2015 QDI STRATEGIES, INC.

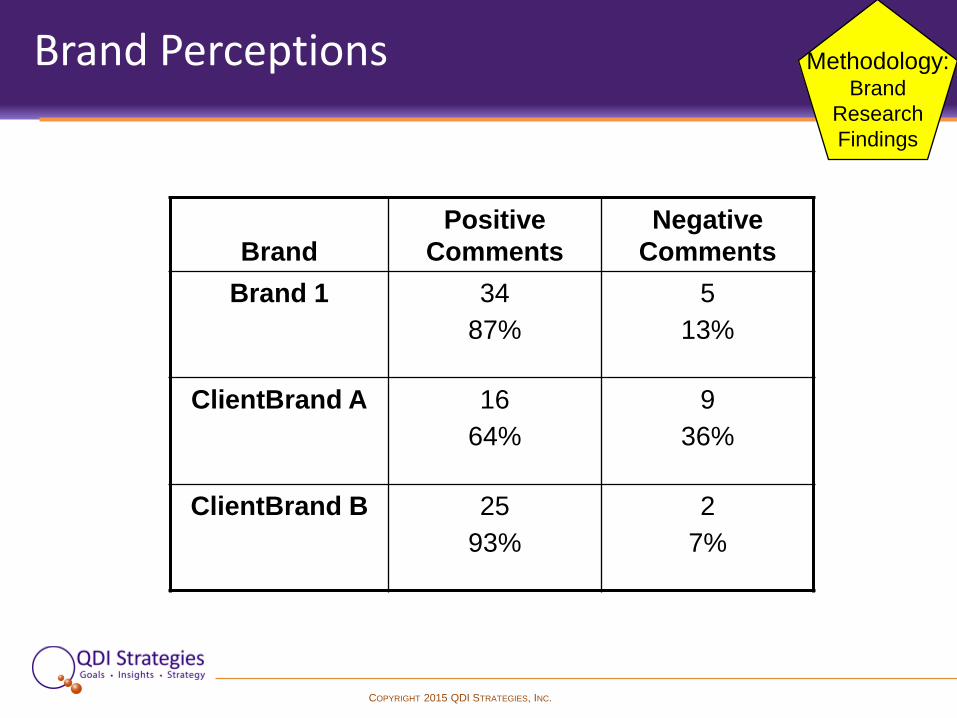

Brand Perceptions

Brand

Positive

Comments

Negative

Comments

Brand 1 34

87%

5

13%

ClientBrand A 16

64%

9

36%

ClientBrand B 25

93%

2

7%

Methodology: Brand

Research

Findings

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand Perception by Channel

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

ProfClientBrand

B

ProfClientBrand

A

SophClientBrand

B

SophClientBrand

A

DIYClientBrand

B

DIYClientBrand

A

Score of their #1 Preferred Brand

Home Depot

Lowe's

Methodology: Brand

Research

Findings

Brand A scored

significantly lower

overall and lowest in

Home Depot

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand 1 Threat

• Brand 1’s offerings cover the most of the ClientBrand B & ClientBrand A range

– Brand 1 is leveraging high-share to take the position of broad, tool-line supplier

• Brand 1’s addition of pneumatic nailers (as reported by ClientBrand B) would make Brand 1’s offering a direct competitor to all of Client’s offering, except for the ClientBrand C equipment line

• QDI believes Brand 1 is a direct threat to Client’s position

– Client may be the most vulnerable of Brand 1’s full line competitors and, consequently, targeted by Brand 1

Methodology: Brand

Research

Findings

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand Power Findings

• ClientBrand B and ClientBrand A both have strong brand franchises with

professionals, however, ClientBrand B’s is stronger

• A significant percentage of professional ClientBrand A owners also own ClientBrand B tools

– It may be possible to switch these ClientBrand A customers to products under the ClientBrand B brand

– However, a single brand strategy for the core portion of the market is similar to Brand 1’s -- it will be difficult for Client to out-spend or out-maneuver Brand 1, competing head-to-head

• In any brand strategy:

– You must improve the ClientBrand A image – suggest a ClientBrand A Pro line

– You must consider your strategy in light of

• The channels’ reactions

• Competitive position

Methodology: Brand

Research

Findings

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand Strategy Values

Potentially, high presence As long as channels will allow supplier to

work with competitor (at a product or

company level)

No marginal staying power

No price premium

Channel-Differentiated Brand

Channel differentiator, due to

different name on products,

sold in different channels

Presence within a channel

Possibly, presence across multiple

channels If there are no alternatives

If alternatives, you get one channel

Higher % margins If no other credible brand alternatives

Quality Position Brand

Quality positioning, due to a

credible brand High-value position to the

brand owner

Low-value position to the

manufacturer

High-channel presence

High-channel staying power

Higher % and $ margins

End-User Brand

Unique / significantly-

differentiated product positions

High

Brand

Power

Low

Brand

Power

Methodology: Brand

Research

Findings

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand wins – exerts

pressure on

channel

Brand wins tug-of-

war with channel

Sell to all channels

as an OEM supplier

Pick a partner

Channel Conflict and Brand Power Impact on Channel Strategy

ClientBrand B 1s

Home Depot

Lowe’s, Sears

ClientBrand A

ClientBrand C

Home Depot

Lowe’s, Sears

ClientBrand C

(historically)

Mass Merchants

Hardware / AG

ClientBrand B 1s

Mass Merchants

Hardware / AG

ClientBrands A & C must either pick a partner in these

channels or create greater brand power.

Degree of Channel Conflict L H

Brand

Power

L

H

Methodology: Brand

Research

Findings

COPYRIGHT 2015 QDI STRATEGIES, INC.

Brand and Channel Strategy Alternatives

Methodology: Strategy

Option

Models

COPYRIGHT 2015 QDI STRATEGIES, INC.

Use STAFDA

to build brands

and counteract

Depot

Use Sears and Lowe’s as a

Sophisticated

Strategy

Strategy Implications

Lever

ClientBrand B

for Contractors

Go Low-End with ClientBrand A

Go High-End With ClientBrand A - Plus

Lever Dept. Channel Position

Methodology: Strategy

Option

Models

COPYRIGHT 2015 QDI STRATEGIES, INC.

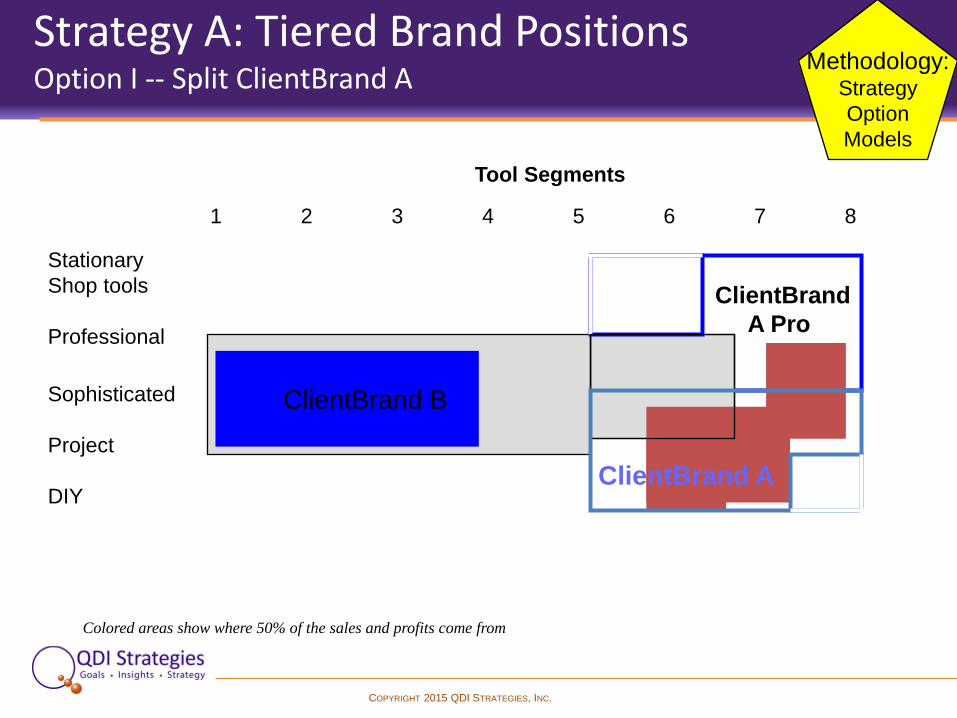

Strategy A: Tiered Brand Positions Option I -- Split ClientBrand A

ClientBrand

A Pro

ClientBrand B ClientBrand B

1 2 3 4 5 6 7 8

Stationary

Shop tools

Professional

Sophisticated

Project

DIY

ClientBrand A

Colored areas show where 50% of the sales and profits come from

Tool Segments

Methodology: Strategy

Option

Models

COPYRIGHT 2015 QDI STRATEGIES, INC.

ClientBrand

A

Strategy B – ClientBrand A & Lowe’s Strategy ClientBrand B for Depot, New ClientBrand A Image with Lowe's

STAFDA Home Depot Lowe’s Sears

Stationary

Shop tools

Professional

Sophisticated

Project

DIY

Colored areas show where 50% of the sales and profits come from

ClientBrand A

ClientBrand B

ClientBrand B is the Contractor / Pro brand. We favor ClientBrand

B in Home Depot, giving them ClientBrand B equipment. We’ll

build a new, woodworking image with Lowe's and Sears. To

preserve the brand image, we remove the $99 ClientBrand A

products from Home Depot.

Methodology: Strategy

Option

Models

COPYRIGHT 2015 QDI STRATEGIES, INC.

Get To Know Us

• Exploratory Meeting

- No-cost discussion of the issues you are facing and our perspective

• Customized research

- Have us design a study for you

• Strategy project

- Have us design a project to address your strategic issues

Contact Information

QDI Strategies, Inc.

1580 S. Milwaukee Avenue, Suite 620

Libertyville, IL 60606

847-566-2020

www.qdistrategies.com

Steve Bassill

President