Q3’13 Global IPO update - Ernst & Young€¦ · Page 3 1Q15 Global IPO update Table of contents...

32

1Q15 Global IPO update January – March 2015

Transcript of Q3’13 Global IPO update - Ernst & Young€¦ · Page 3 1Q15 Global IPO update Table of contents...

1Q15 Global IPO update January – March 2015

Page 2 1Q15 Global IPO update

Table of contents

Section Content Slides

1 2015 January – March highlights 4-8

2 Global IPO activity trends Global analysis

Regional analysis

Industry analysis

Stock exchange analysis

10-14

3 PE-backed IPO activity 16-19

4 Appendices 21-30

Page 3 1Q15 Global IPO update

Table of contents

Section Content Slides

1 2015 January – March highlights 4-8

2 Global IPO activity trends Global analysis

Regional analysis

Industry analysis

Stock exchange analysis

10-14

3 PE-backed IPO activity 16-19

4 Appendices 21-30

Page 4 1Q15 Global IPO update

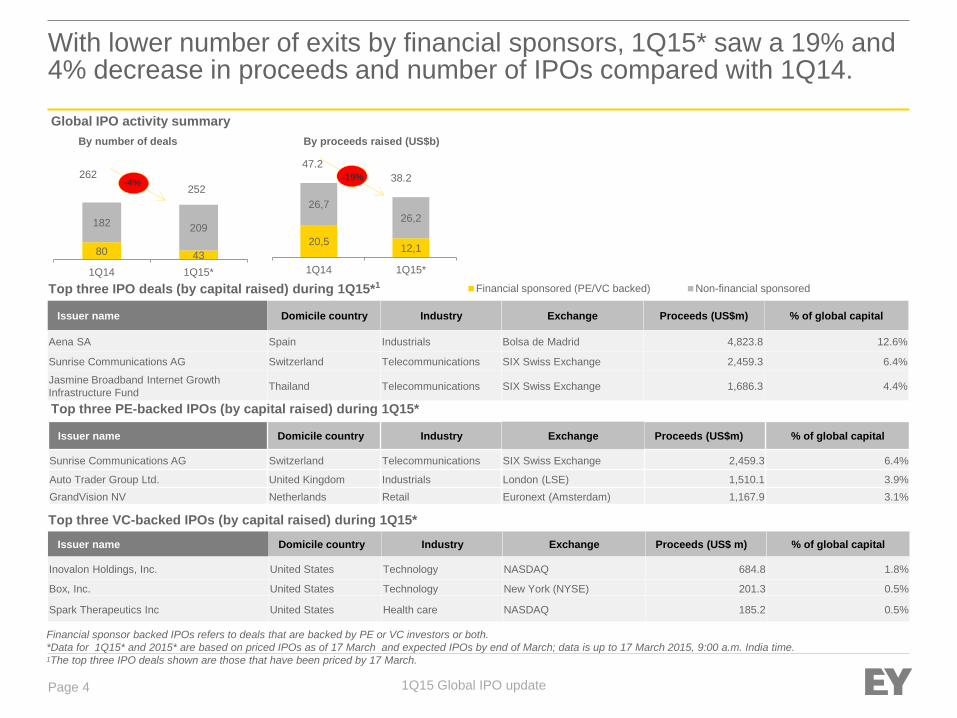

20,5 12,1

26,7

26,2

1Q14 1Q15*

47.2

-19%

80 43

182 209

1Q14 1Q15*

262

With lower number of exits by financial sponsors, 1Q15* saw a 19% and 4% decrease in proceeds and number of IPOs compared with 1Q14.

Financial sponsor backed IPOs refers to deals that are backed by PE or VC investors or both.

*Data for 1Q15* and 2015* are based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time. 1The top three IPO deals shown are those that have been priced by 17 March.

Issuer name Domicile country Industry Exchange Proceeds (US$m) % of global capital

Aena SA Spain Industrials Bolsa de Madrid 4,823.8 12.6%

Sunrise Communications AG Switzerland Telecommunications SIX Swiss Exchange 2,459.3 6.4%

Jasmine Broadband Internet Growth

Infrastructure Fund Thailand Telecommunications SIX Swiss Exchange 1,686.3 4.4%

Issuer name Domicile country Industry Exchange Proceeds (US$m) % of global capital

Sunrise Communications AG Switzerland Telecommunications SIX Swiss Exchange 2,459.3 6.4%

Auto Trader Group Ltd. United Kingdom Industrials London (LSE) 1,510.1 3.9%

GrandVision NV Netherlands Retail Euronext (Amsterdam) 1,167.9 3.1%

Issuer name Domicile country Industry Exchange Proceeds (US$ m) % of global capital

Inovalon Holdings, Inc. United States Technology NASDAQ 684.8 1.8%

Box, Inc. United States Technology New York (NYSE) 201.3 0.5%

Spark Therapeutics Inc United States Health care NASDAQ 185.2 0.5%

Global IPO activity summary

By number of deals By proceeds raised (US$b)

Financial sponsored (PE/VC backed) Non-financial sponsoredTop three IPO deals (by capital raised) during 1Q15*1

Top three PE-backed IPOs (by capital raised) during 1Q15*

Top three VC-backed IPOs (by capital raised) during 1Q15*

252 38.2 -4%

Page 5 1Q15 Global IPO update

Global IPO activity To access this infographic in PDF format, please go to EY’s IPO webpages (ey.com/ipo) to access the EY Global IPO Trends: 2015 Q1 report.

Page 6 1Q15 Global IPO update

Asia-Pacific1 and Greater China2 IPO activity To access this infographic in PDF format, please go to EY’s IPO webpages (ey.com/ipo) to access the EY Global IPO Trends: 2015 Q1 report.

1Based in IPO activity on Asia-Pacific stock exchanges. 2Based in IPO activity on Greater China stock exchanges (i.e.,, Shanghai Stock Exchange, Shenzhen Stock

Exchange – the Mainboard, SME and ChiNext, Hong Kong Stock Exchange – Main Board, GEM and Taiwanese Stock Exchange).

Page 7 1Q15 Global IPO update

EMEIA1 and UK2 IPO activity To access this infographic in PDF format, please go to EY’s IPO webpages (ey.com/ipo) to access the EY Global IPO Trends: 2015 Q1 report.

1Based in IPO activity on EMEIA stock exchanges. 2Based in IPO activity on London Main Market and Alternative Investment Market (AIM).

Page 8 1Q15 Global IPO update

EMEIA1 and UK2 IPO activity To access this infographic in PDF format, please go to EY’s IPO webpages (ey.com/ipo) to access the EY Global IPO Trends: 2015 Q1 report.

1Based in IPO activity on EMEIA stock exchanges. 2Based in IPO activity on London Main Market and Alternative Investment Market (AIM).

Page 9 1Q15 Global IPO update

US IPO activity1 To access this infographic in PDF format, please go to EY’s IPO webpages (ey.com/ipo) to access the EY Global IPO Trends: 2015 Q1 report.

1Based in IPO activity on US stock exchanges: NYSE, NASDAQ

Page 10 1Q15 Global IPO update

Table of contents

Section Content Slides

1 2015 January – March highlights 4-8

2 Global IPO activity trends Global analysis

Regional analysis

Industry analysis

Stock exchange analysis

10-14

3 PE-backed IPO activity 16-19

4 Appendices 21-30

Page 11 1Q15 Global IPO update

Global IPO activity trends IPO activity saw a dip in 1Q15* compared with 1Q14, with proceeds and deal numbers decreasing by 19% and 4%, respectively.

Quarterly IPO activity (1Q11-1Q15*)

Global IPO activity (2011-2015*) % of cross-border listings

$ 46,9 $ 65,4 $ 28,7 $ 29,2 $ 18,0 $ 43,8 $ 29,6 $ 37,2 $ 24,4 $ 46,3 $ 25,6 $ 74,9 $ 47.2 $ 72,7 $ 67,4 $ 72,0 $ 38.2

306

384

293

260

203

243

192 201 163

205 202

325

262

335

277

367

252

0

50

100

150

200

250

300

350

400

450

0

10

20

30

40

50

60

70

80

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b) Number of deals

9,2%

10,3%

9,9%

8,4%

8,8%

9,2%

9,6%

10,0%

10,4%

2013 2014 2015*

Cross-border listing

$ 170,2 $ 128,6 $ 171,1 $ 259,2 $ 38,2

1.243

839 895

1.241

252

0

200

400

600

800

1.000

1.200

1.400

0

50

100

150

200

250

3002011

2012

2013

2014

2015*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b) Number of deals

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 12 1Q15 Global IPO update

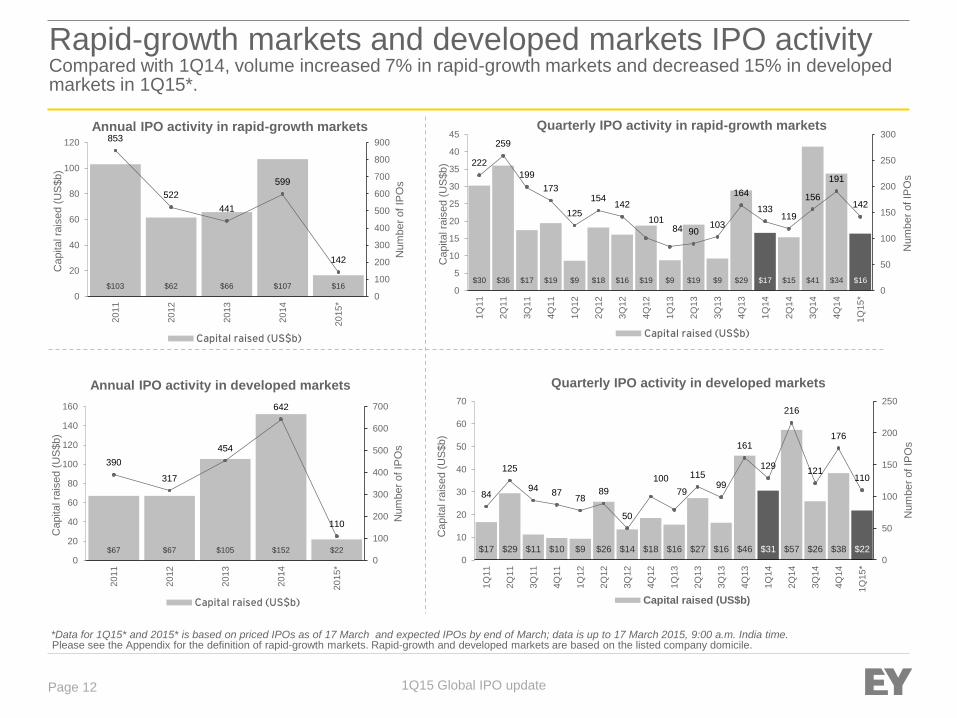

Rapid-growth markets and developed markets IPO activity Compared with 1Q14, volume increased 7% in rapid-growth markets and decreased 15% in developed markets in 1Q15*.

Please see the Appendix for the definition of rapid-growth markets. Rapid-growth and developed markets are based on the listed company domicile.

$30 $36 $17 $19 $9 $18 $16 $19 $9 $19 $9 $29 $17 $15 $41 $34 $16

222

259

199

173

125

154 142

101 84 90

103

164

133 119

156

191

142

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

40

45

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Quarterly IPO activity in rapid-growth markets

Capital raised (US$b)

$17 $29 $11 $10 $9 $26 $14 $18 $16 $27 $16 $46 $31 $57 $26 $38 $22

84

125

94 87

78 89

50

100

79

115 99

161

129

216

121

176

110

0

50

100

150

200

250

0

10

20

30

40

50

60

70

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Quarterly IPO activity in developed markets

Capital raised (US$b)

$67 $67 $105 $152 $22

390

317

454

642

110

0

100

200

300

400

500

600

700

0

20

40

60

80

100

120

140

160

20

11

20

12

20

13

20

14

20

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Annual IPO activity in developed markets

Capital raised (US$b)

$103 $62 $66 $107 $16

853

522

441

599

142

0

100

200

300

400

500

600

700

800

900

0

20

40

60

80

100

120

20

11

20

12

20

13

20

14

20

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Annual IPO activity in rapid-growth markets

Capital raised (US$b)

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 13 1Q15 Global IPO update

Industry analysis Most industries had smaller-sized IPOs in 1Q15* compared with 1Q14; industrials sector led global activity in 1Q15* by proceeds as well as by deal number.

103.4 232.9

426.2

72.7 2,072.8

272.3 184.5

217.5 127.0

197.5 79.7

330.9 202.5

65.4 51.8

247.9 142.1

83.7 50.5

295.8

107.6 34.8

1Q14 1Q15*

Average deal size (US$m)

13

11

23

22

54

14

32

16

15

5

21

36

14

13

26

13

38

12

35

22

20

2

12

45

Consumer staples

Media andentertainment

Materials

Real estate

Health care

Retail

Technology

Consumer products

Financials

Telecommunications

Energy

Industrials

1Q15* 1Q14

1,4

3,3

1,9

5,5

3,5

4,6

6,3

3,5

4,1

0,4

9,1

3,7

0,5

1,2

1,3

1,8

2,0

2,4

2,8

2,8

3,7

4,1

5,1

10,5

Consumer staples

Media andentertainment

Materials

Real estate

Health care

Retail

Technology

Consumer products

Financials

Telecommunications

Energy

Industrials

1Q15* 1Q14

Number of IPOs Capital raised (US$b)

431.5

91.2

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 14 1Q15 Global IPO update

Exchange analysis – summary EMEIA exchanges led in terms of capital raised, while Asia-Pacific exchanges dominated global IPO activity in terms of deal volume in 1Q15*.

Regional share by capital raised (US$b)

Regional share by number of IPOs

Greater China exchanges led in terms of total proceeds raised (US$9.2b); US (US$5.6b) and Spain (US$5.3b) ranked second and third,

respectively.

There were eight deals with capital raised above US$1b. Four of these deals listed on European exchanges while three listed on Asian

exchanges. US exchanges accounted for only one such deal.

Greater China exchanges (94 deals) led globally in terms of deal number, followed by the US (38 deals) and Japan (24 deals), which ranked

second and third, respectively.

1Greater China exchanges includes Mainland China exchanges (70 deals raised US$7.9b), Hong Kong Main Market and Growth Enterprise Market (22 deals raised US$1.3b) and

Taiwan exchange (2 deals raised US$51m).

Based on the listed company exchange.

Asia-Pacific EMEIA Americas

0,3

0,9

2,1

3,0

9,2

Indonesia

Japan

Thailand

Malaysia

Greater China

15%

25%

39%

46%

41%

41%

32%

34%

44%

34%

29%

20%

1Q15*

1Q14

2014

2013

3

8

11

24

94

South Korea

Thailand

Australia

Japan

Greater China

1,1

1,3

2,5

3,4

5,3

France

Netherlands

Switzerland

UK

Spain

4

7

8

9

17

Italy

India

Sweden

France

UK

0,01

5,6

Canada

US

2

38

Canada

US

16%

28%

25%

31%

57%

44%

46%

42%

27%

28%

29%

27%

1Q15*

1Q14

2014

2013

Americas Asia-Pacific EMEIA

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 15 1Q15 Global IPO update

1Q14 1Q15*

Stock exchange analysis Shenzhen and Shanghai exchanges led global IPO activity by deal numbers in 1Q15*.

*Data based on domicile of the exchange, regardless of the listed company domicile. Euronext includes Euronext (Amsterdam), Euronext (Paris) and Lisbon; NASDAQ OMX includes

Copenhagen and Stockholm; and Shenzhen includes Shenzhen (SZSE) includes the Main Board, SME Board and ChiNext.

Capital raised (US$b)

Number of

IPOs

93

9

11

13

14

17

25

35

35

All other exchanges

London (LSE)

Australia (ASX)

New York (NYSE)

Hong Kong (HKEx)

Tokyo MOTHERS

NASDAQ

Shenzhen (SZSE)

Shanghai (SSE)

10,3

2,4

2,5

2,5

3,0

3,3

3,5

5,3

5,4

All other exchanges

Shenzhen (SZSE)

Euronext

SIX Swiss Exchange

Bursa Malaysia

London (LSE)

New York (NYSE)

Bolsa de Madrid

Shanghai (SSE)

9,9

3,1

3,2

3,3

3,6

4,6

4,9

5,9

8,7

All other exchanges

NASDAQ OMX

Euronext

NASDAQ

Shenzhen (SZSE)

Tokyo (TSE)

London (LSE)

Hong Kong (HKEx)

New York (NYSE)

91

6

10

10

15

17

26

42

45

All other exchanges

Euronext

Bombay SME

London (LSE)

Hong Kong (HKEx)

London (AIM)

New York (NYSE)

Shenzhen (SZSE)

NASDAQ

Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 16 1Q15 Global IPO update

Table of contents

Section Content Slides

1 2015 January – March highlights 4-8

2 Global IPO activity trends Global analysis

Regional analysis

Industry analysis

Stock exchange analysis

10-14

3 PE-backed IPO activity 16-19

4 Appendices 21-30

Page 17 1Q15 Global IPO update

Global PE IPO activity trends PE-backed IPOs saw a record year in 2014, but muted activity to date in 2015.

*EMEA refers to Europe, Middle East and African exchanges. India is included within Asia-Pacific.

Quarterly PE-backed IPO activity (2012-1Q’15*)

Annual global PE-backed IPOs by region (capital raised)

Key insights PE firms continue to take advantage of a strong environment for exits.

After several years of concerns centering around PE’s ability to exit from

the buildup of companies acquired during the 2006-2007 time period, PE

activity is now reaching a state of equilibrium.

PE firms are particularly active in the IPO markets. 2014 was a new record

year, breaking the record set in 2013. In 2014, PE-backed deals

dramatically surpassed expectations of 2013. In 2014, raising a

remarkable US$109.9b across 211 separate offerings.

Indeed, exits of all sorts were the lead story for PE investors. Through

trade sales, secondaries and IPOs, PE firms sold stakes in more than

1,200 companies valued at US$470.6b, a new global record, and an

increase of 70% versus 2013.

29 37 31

80 96 99 92

10 31

86 62 69

103 88

7

6 10 12

30 28

40 66

37 21

51

42 36

49 53

3

9 13 6

40

56

60

58

4 4

19

13 6

35

70

16

0

50

100

150

200

250

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015YTD*

Num

ber

of deals

Americas Asia-Pacific EMEA*

$6 $7 $7 $15 $21 $23 $21

$3 $10 $16

$30 $15

$35 $33

$1

$1 $1 $1

$8 $3

$7 $16

$4

$6 $9

$6

$4

$6

$43

$1 $1 $4 $2

$8 $14

$20 $21

$3

$1

$10 $3

$2

$18

$34

$7

$0

$20

$40

$60

$80

$100

$120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015YTD*

Capital ra

ised (

US

$b)

Americas Asia-Pacific EMEA*

$6 $7 $4 $5 $8 $15 $8 $28 $17 $37 $41 $14 $9

35 30 20 25

33

47 36

71

40

82

41 48

26

0

20

40

60

80

100

0

10

20

30

40

50

Num

ber

of deals

Capital ra

ised (

US

$b)

Capital raised (US$b) Number of deals

Annual global PE-backed IPOs by region (number of deals)

Page 18 1Q15 Global IPO update

335

562

545

625

435

359

543

644

599

634

720

121

227

318

335

384

199

83

249

301

322

299

350

57

149

180

197

216

51

56

156

117

110

187

211

26

0 200 400 600 800 1.000 1.200 1.400

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1Q15*

Strategic sales Secondary sales IPOs

Global PE exit trends IPOs remain strong; strategic acquirers step up as bidders for PE assets.

1EMEA refers to Europe, Middle East and African exchanges. India is included within Asia-Pacific.

“Strategic sales” are sales to corporations (i.e., M&A) while “secondary sales” are sales to other PE firms.

*1Q15* shows IPOs that have been priced by 17 March

Key insights PE investors are likely to continue focusing on exits in 2015. While firms have made great strides over the last 12 to 18 months in reducing the size of

their PE portfolios and achieving liquidity on many long-held positions, a significant amount of work remains to be done. In 2014, PE exits outpaced new

acquisitions by a ratio of roughly 1.7:1.

According to PitchBook, PE firms hold majority stakes in more than 13,000 companies globally, 45% of which have been held in excess of five years.

Despite recent volatility in the global equities markets, IPOs remain poised to be a primary exit route for many of these companies.

Strategic acquirers have become far more active in recent months; this is evident in higher valuations for M&A transactions and the number of sales to

trade buyers for PE assets.

Indeed, on the buyside, valuations are among the greatest concern for PE buyers in the present market.

Annual global PE exits by deal volume (2004-1Q15*)

$74,9

$143,3

$89,5

$143,6

$111,6

$51,9

$155,1

$182,1

$148,5

$158,8

$296,6

$57,3

$60,3

$68,1

$91,9

$158,2

$28.5

$12.8 $65,9

$53,5

$69,9

$58,7

$34.7

$11,4

$31,6

$38,4

$50,0

$57,7

$9,9

$16,8

$35,5

$38,8

$22,0

$58,5

$110,0

$9,4

$0 $100 $200 $300 $400 $500 $600

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1Q15*

Strategic sales Secondary sales IPOs

Annual global PE exits by deal value (US$m) (2004-1Q15*)

IPOs as % of

PE exits

12.0

23.1%

21.1%

9.2%

14.2%

13.8%

20.2%

6.6%

16.1%

21.6%

15.4%

18.9%

IPOs as % of

PE exits

12.7%

16.5%

16.7%

10.7%

11.0%

16.4%

11.2%

7.4%

17.6%

18.3%

16.9%

20.9%

Page 19 1Q15 Global IPO update

PE exit trends by region Americas and EMEA1 see significant increase in exit activity.

119

169

181

201

115

95

231

219

248

234

305

41

103

140

126

160

77

27

114

123

176

135

178

21

80

96

99

92

10

31

86

62

69

103

88

7

0 200 400 600

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1Q15*

Strategic sales Secondary sales IPOs

187

338

294

325

262

193

223

303

246

283

316

65

118

172

195

208

110

50

118

157

126

144

158

35

40

56

60

58

4

4 19

13

6

35

70

16

0 200 400 600 800

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1Q15*

Strategic sales Secondary sales IPOs

33,3

76,3

43,4

59,8

59,1

23,7

84,1

73,4

76,9

99,7

148,3

34,6

31,0

27,0

25,2

68,0

$4.1

$2.5

29,7

14,4

44,4

28,3

$24.6

6,5

15,3

21,2

23,4

21,3

2,8

10,1

16,2

29,8

15,3

34,6

32,7

1,2

0 50 100 150 200 250

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1Q15*

Strategic sales Secondary sales IPOs

33,9

51,7

40,9

71,0

46,5

20,9

56,1

76,5

57,8

44,0

113,9

18,5

28,9

40,6

65,6

83,8

21,8

$8.9

34,5

31,9

21,4

28,4

$9.5

4,6

8,2

14,4

20,1

20,9

3,2

0,8

10,2

3,1

2,3

17,8

34,5

7,3

0 50 100 150 200

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1Q15*

Strategic sales Secondary sales IPOs

Americas PE exits by deal volume (2004-1Q15*)

EMEA1 PE exits by deal volume (2004-1Q15*)

10.1%

15.4%

21.8%

14.1%

15.4%

20,0%

20.2%

5.0%

20.3%

24.4%

23.7%

26.4%

IPOs as % of

PE exits

IPOs as % of

PE exits

2.7%

14.8%

21.8%

11.2%

25.4%

12.4%

27.8%

4.2%

14.3%

25.4%

17.0%

19.1%

Americas PE exits by deal value (US$m) (2004-1Q15*)

IPOs as % of

PE exits

13.8%

12.8%

7.6%

1.6%

2.7%

5.3%

1.6%

1.1%

9.8%

10.9%

9.9%

11.6%

IPOs as % of

PE exits EMEA1 PE exits by deal value (US$m) (2004-1Q15*)

24.1%

19.5%

18.5%

2.8%

2.8%

10.1%

2.6%

4.4%

11.9%

15.9%

13.5%

11.7%

“Strategic sales” are sales to corporations (i.e., M&A) while “secondary sales” are sales to other PE firms.

*1Q15* shows IPOs that have been priced by 17 March.

1EMEA refers to Europe, Middle East and African exchanges. India is included within Asia-Pacific.

Page 20 1Q15 Global IPO update

PE exit trends by region US value up dramatically in 2014, though number of deals declines. EMEA1 sees continued strength, as Asia-Pacific continues to work through China backlog.

29

55

70

99

58

71

89

122

105

117

99

15

6

6

14

16

12

6

17

21

20

20

14

1

30

28

40

66

37

21

51

42

36

49

53

3

0 100 200

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015 YTD

Strategic sales Secondary sales IPOs

7,7

15,3

5,2

12,8

6,0

7,3

15,0

32,3

13,7

15,1

34,4

4,2

0,4

0,5

1,0

6,3

2,6

1,4

1,7

7,2

4,0

2,0

1,7

0.3

8,1

2,8

6,5

15,6

3,9

5,8

9,1

5,9

4,4

6,0

0,9

0 10 20 30 40 50

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015 YTD

Strategic sales Secondary sales IPOs

Key insights ► European strength continues as sponsors work out of pre-recession era deals. PE firms took 70 companies public during 2014, which was a new record,

and strength has continued into the new year, with an additional 16 PE-backed companies listing on regional exchanges.

► Asia-Pacific continues to gain strength from stronger equities markets in the second half of 2014, as well as the reopening of the IPO window in Mainland

China. With the window effectively closed throughout 2013, firms had to decide whether to wait out the shutdown or pursue alternative exits such as trade

sales and secondary buyouts. China was the source of the largest PE-backed deal in history, when the long-anticipated Alibaba IPO went effective at

US$25.0b. Indeed, it wasn’t just the largest PE-backed IPO of all time; it was the largest IPO ever, surpassing the US$22.1b offering by the Agricultural

Bank of China in 2010. The company, which was backed by a range of sponsors including Silver Lake, General Atlantic, China Investment Corporation,

CITIC Capital Management, The Canada Pension Plan Investment Board and others, highlights some key trends in the PE asset class: 1) the increasingly

important role that growth capital is playing; and 2) it underscores the importance and the potential of emerging markets such as China to the asset class.

► The Americas region saw a marked uptick in value in 2014, although the number of deals fell to 88 from 103. Activity in the first three months of 2015 has

been muted. Some observers cite lower oil prices as a potential source of the slowdown.

IPOs as % of

PE exits IPOs as % of

PE exits

15.8%

31.9%

26.3%

22.4%

22.7%

32.3%

21.4%

34.6%

36.5%

32.3%

31.5%

46.2%

16.2%

54,2%

25.8%

19.7%

12.9%

35.3%

40.2%

30.3%

44.8%

51.1%

15.1%

50.0%

Asia-Pacific PE exits by deal volume (2004-1Q15*) Asia-Pacific PE exits by deal value (US$m) (2004-1Q15*)

“Strategic sales” are sales to corporations (i.e., M&A) while “secondary sales” are sales to other PE firms. 1EMEA refers to Europe, Middle East and African exchanges. India is included within Asia-Pacific.

*1Q15* shows IPOs that have been priced by 17 March.

Page 21 1Q15 Global IPO update

Table of contents

Section Content Slides

1 2015 January – March highlights 4-8

2 Global IPO activity trends Global analysis

Regional analysis

Industry analysis

Stock exchange analysis

10-14

3 PE-backed IPO activity 16-19

4 Appendices 21-30

Page 22 1Q15 Global IPO update

Asia-Pacific1 IPO activity trends IPO activity increased by 25% in 1Q15* in terms of volume while it decreased by 18% in terms of value when compared with levels seen in 1Q141.

Former state-owned enterprise (SOE) IPO activity in Asia-

Pacific (2007-1Q15*)

1Q15* Asia-Pacific IPOs by sector

IPO pricing and performance: 1Q15* IPOs

Measures 1Q15* IPOs

% of IPOs priced within or above initial pricing range 99.2%

First-day average return +39.6%

% change of offer price vs. 17 March +158.3%

Median post-IPO market cap US$166.9m

Hang Seng Index – 2015 YTD returns +1.5%

Shanghai SE Composite Index – 2015 YTD returns +6.6%

Nikkei 225 – 2015 YTD returns +10.3%

Sectors Number of

deals Proceeds (US$m)

Industrials 32 2,146.0

Technology 25 1,136.6

Materials 17 1,024.1

Consumer products 15 1,244.1

Health care 11 577.7

Financials 8 2,475.6

Real estate 8 933.5

Retail 8 541.6

Energy 7 3,218.4

Media and entertainment 7 537.6

Consumer staples 6 274.3

Telecommunications 1 1,686.3

Grand Total 145 15,795.8

Asia-Pacific IPO activity (2007-1Q15*)

1Based in IPO activity on Asia-Pacific stock exchanges. More information on 1Q15, please see the Asia-Pacific infographic on slide 6.

$125 $32 $72 $179 $88 $56 $59 $83 $16

760

350 347

746

675

437

376

564

145

0

100

200

300

400

500

600

700

800

0

20

40

60

80

100

120

140

160

180

200

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

1Q

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b)

$65 $14 $22 $54 $1 $12 $11 $17 $0

69

27 24

73

4 7 8

11

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

1Q

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b)

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 23 1Q15 Global IPO update

EMEIA1 IPO activity trends EMEIA IPO activity on the main markets improved in 1Q15*, compared with 1Q14.

EMEIA financial sponsor-backed IPO activity (2007-1Q15*)

Annual EMEIA IPO activity (2007-1Q15*)

1Based in IPO activity on EMEIA stock exchanges. See Appendix for definitions of main market and junior market.

$126 $36 $14 $48 $33 $16 $34 $75 $17

823

310

112

354 353

209 240

365

67

0

100

200

300

400

500

600

700

800

900

0

20

40

60

80

100

120

140

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

1Q

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b)

$22 $3 $2 $11 $4 $3 $17 $36 $9

101

15 8

37 30

14

38

77

20

0

20

40

60

80

100

120

0

5

10

15

20

25

30

35

40

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

1Q

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b)

1Q15* EMEIA IPOs by sector

IPO pricing and performance: 1Q15* IPOs

Measures 1Q15* IPOs

% of IPOs priced within or above initial pricing range 97.7%

EMEIA main markets’ IPOs – first-day average return +10.2%

EMEIA main markets’ IPO – % change of offer price vs.

17 March +20.8%

EMEIA main markets’ IPO – median post-IPO market cap US$412.5m

FTSE 100 – 2015 YTD returns +3.6%

DAX – 2015 YTD returns +24.1%

CAC – 2015 YTD returns +18.5%

Sectors Number of

deals Proceeds (US$m)

Industrials 11 7,644.6

Consumer staples 8 212.5

Health care 8 181.4

Consumer products 7 1,549.2

Financials 7 946.1

Materials 7 258.0

Media and entertainment 6 648.5

Technology 6 632.5

Retail 3 1,767.2

Energy 2 512.3

Telecommunications 1 2,459.3

Real estate 1 2.4

Grand Total 67 16,813.9

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 24 1Q15 Global IPO update

US1 IPO activity trends Financial sponsor-backed activity went down considerably in 1Q15*, compared with 1Q14.

US financial sponsor-backed IPO activity (2007-1Q15*)

Annual US IPO activity (2007-1Q15*)

1Based in IPO activity on US stock exchanges: NYSE, NASDAQ and NYSE – AMEX

$50 $27 $27 $43 $40 $47 $62 $96 $6

214

35

65

162

124 133

226

291

38

0

50

100

150

200

250

300

350

0

20

40

60

80

100

120

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b)

$24 $3 $10 $17 $30 $32 $41 $70 $3

124

13

36

108

80 87

144

185

21

0

20

40

60

80

100

120

140

160

180

200

0

10

20

30

40

50

60

70

80

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

*

Num

ber

of IP

Os

Capital ra

ised (

US

$b)

Capital raised (US$b)

1Q15* US IPOs by sector

IPO pricing and performance: 1Q15* IPOs

Measures 1Q15* IPOs

% of IPOs priced within or above initial filing range 63.0%

First day average return +19.0%

% change of offer price vs. 17 March +19.0%

Median post-IPO market cap US$294.0m

S&P 500 – 2015 YTD returns +1.1%

DJIA – 2015 YTD returns +0.9%

CBOE Volatility Index® (VIX®) - change from 1 Jan. -18.7%

Sectors Number of

deals Proceeds (US$m)

Health care 18 1,196.6

Financials 5 268.3

Technology 4 1,020.8

Real estate 4 911.2

Energy 2 1,383.1

Industrials 2 689.1

Materials 2 31.2

Retail 1 120.8

Grand Total 38 5,621.0

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 25 1Q15 Global IPO update

Pricing range Ninety-four percent of global IPOs1 were priced within or above the initial filing range in 1Q15* compared with 92% in 1Q14.

1Chart shows the number of open-price IPOs with deal value above US$50m that are priced above, below or within their initial filing range. For 3% of IPOs, this range is not applicable.

12% 11% 14% 16% 9% 7%

3% 11% 10% 10% 7% 7% 6% 6% 5% 9% 11%

8% 11% 7% 6%

12% 9% 10% 8%

12% 14% 14%

6%

87% 88% 86% 84%

91%

74%

95%

86% 85% 88% 90% 90%

88% 88% 92% 83% 83% 87%

85% 90%

85%

83%

80% 82% 85%

82% 78% 80%

89%

1% 1%

19%

2% 3% 5% 2% 3% 3% 6% 5% 4%

8% 6% 5% 4% 3% 9%

5% 11%

8% 7% 6% 8% 6% 5%

2%

12%

22%

32%

42%

52%

62%

72%

82%

92%

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

*

Num

ber

of deals

Below In range Above

227 276 171 84 52 84 141 288 282 313 296 474 306 384 293 260 203 243 192 201 163 205 202 325 262 335 276 359 Total

number of

IPOs

89% of global IPOs in 1Q15* were priced within their initial filing range, 5% were priced above their initial filing range and 6% of IPOs were

priced below their initial filing range.

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 26 1Q15 Global IPO update

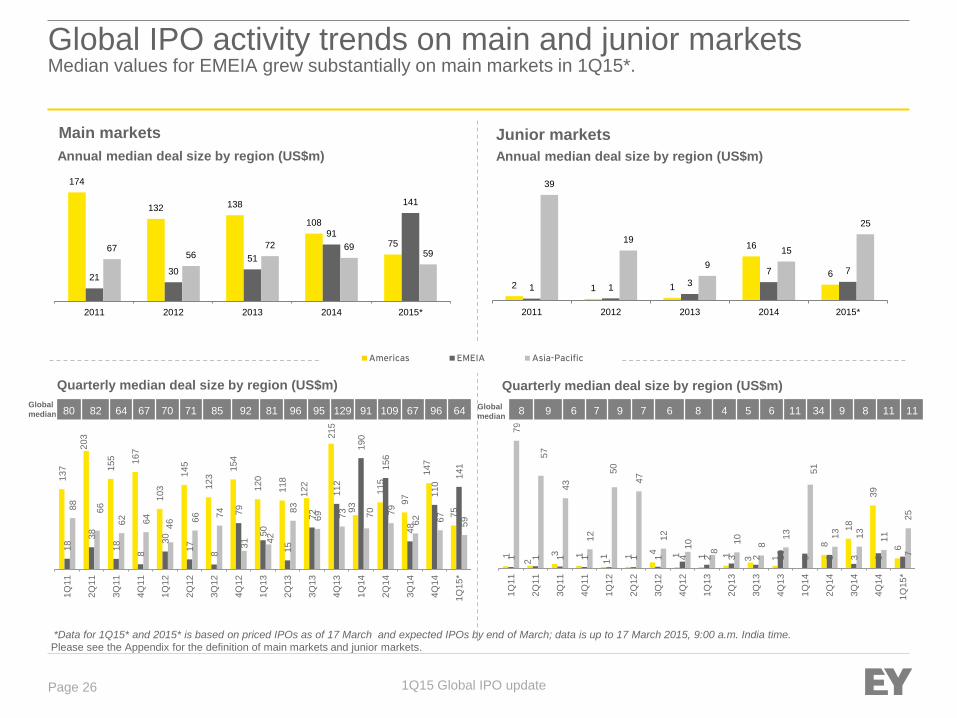

Global IPO activity trends on main and junior markets Median values for EMEIA grew substantially on main markets in 1Q15*.

Please see the Appendix for the definition of main markets and junior markets.

Annual median deal size by region (US$m)

Quarterly median deal size by region (US$m)

Americas EMEIA Asia-Pacific

Main markets Junior markets

Annual median deal size by region (US$m)

Global

median

Global

median

Quarterly median deal size by region (US$m)

174

132 138

108

75

21 30

51

91

141

67 56

72 69 59

2011 2012 2013 2014 2015*

137

203

155

167

103

145

123 1

54

120

118

122

215

93

115

97

147

75

18 3

8

18

8

30

17

8

79

50

15

72

112

190

156

48

110 1

41

88

66

62

64

46 66

74

31

42

83

69

73

70

79

62

67

59

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

*

2 1 1

16

6

1 1 3

7 7

39

19

9

15

25

2011 2012 2013 2014 2015*

1

2 3

1

1

1 4

1

1 1

3

1

8

18

39

6

1

1

1

1

1 1

1

4

2

3

2

10

9

8

3

9 7

79

57

43

12

50

47

12

10

8 1

0

8 1

3

51

13

13

11

25

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

*

8 9 6 7 9 7 6 8 4 5 6 11 34 9 8 11 11 80 82 64 67 70 71 85 92 81 96 95 129 91 109 67 96 64

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 27 1Q15 Global IPO update

Appendix: key global IPO statistics (US$)

1Percentage change from 2010 to 2011 2Percentage change from 2011 to 2012 3Percentage change from 2012 to 2013 4Percentage change from 2013 to 2014

5Consumer products includes consumer services 6Throughout slides, financial sponsor backed IPOs refer to IPOs backed by PE and/or VC funds. In 1Q15, there were 43 IPOs raising US$12.1b.

Please see Appendix for the list of stock exchanges. *Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

2011 2012 2013 2014 1Q15*

Number of deals 1,243 (▼ 9%1) 839 (▼ 33%2) 895 (▲7%3) 1241 (▲38.7%4) 252

Capital raised $170.2b (▼ 40%1) $128.6b (▼ 24%2) $171.1b (▲33%3) $259.2b (▲51.5%4) $38.2b

Average deal size $137.0m $153.3m $191.1m $208.9m $151.8m

PE-backed IPOs 119 deals, $38.3b 107 deals, $19.4b 185 deals, $58.3b 211 deals, $109.9b 30 deals, $10.5b

VC-backed IPOs 143 deals, $17.3b 92 deals, $23.2b 129 deals, $14.1b 159 deals, $22.8b 17 deals, $2.1b

Top 5 sectors

(number of deals)

Materials (271)

Industrials (215)

Technology (146)

Energy (101)

Consumer products 5(98)

Materials (143)

Industrials (135)

Technology (115)

Energy (63)

Consumer staples (58)

Industrials (117)

Technology (115)

Real estate (100)

Health care (100)

Financials (92)

Health care (198)

Technology (169)

Industrials (146)

Consumer products

(111)

Materials (106)

Industrials (45)

Health care (38)

Technology (35)

Materials (26)

Consumer products (22)

Top 5 sectors

(capital raised)

Materials ($29.2b)

Industrials ($27.0b)

Energy ($20.8b)

Financials ($15.9b)

Technology ($15.5b)

Technology ($23.1b)

Industrials ($20.2b)

Financial ($19.4b)

Real estate ($12.5b)

Energy ($12.1b)

Financials ($28.6b)

Real estate ($27.0b)

Energy ($22.0b)

Industrials ($18.9b)

Health care ($12.4b)

Technology ($50.6b)

Financials ($43.2b)

Energy ($31.4b)

Real estate ($27.2b)

Health care ($22.6b)

Industrials ($10.5b)

Energy ($5.1b)

Telecommunications ($4.1b)

Financials ($3.7b)

Consumer products ($2.8b)

Top 5 exchanges

(number of deals)

Warsaw – New Connect

(136)

Shenzhen – ChiNext (128)

Shenzhen – SME (115)

Australian (101)

Hong Kong (68)

New York (78)

Shenzhen – ChiNext (74)

Warsaw – New Connect (62)

Shenzhen (55)

NASDAQ (54)

New York (116)

NASDAQ (109)

Hong Kong (76)

London AIM (54)

Australian (52)

NASDAQ (174)

New York (117)

Hong Kong (90)

London AIM (74)

Australian (70)

Shanghai SSE (35)

NASDAQ (25)

Shenzhen – Chinext (23)

Tokyo Mothers (17)

Hong Kong (14)

Top 5 exchanges

(capital raised)

New York ($30.5b)

Hong Kong ($25.3b)

Shenzhen ($15.7b)

Shanghai ($15.1b)

London ($13.9b)

New York ($24.0b)

NASDAQ ($22.6b)

Tokyo ($12.2b)

Hong Kong ($11.5b)

Bursa Malaysia ($7.6b)

New York ($45.8b)

Hong Kong ($21.4b)

NASDAQ ($15.8b)

London ($12.9b)

Tokyo ($9.3b)

New York ($73.8b)

Hong Kong ($29.1b)

NASDAQ ($22.2b)

London ($19.4b)

Australian ($16.0b)

Shanghai SSE ($5.4b)

Bolsa de Madrid ($5.3b)

New York ($3.5b)

London LSE ($3.3b)

Bursa Malaysia ($3.0b)

Page 28 1Q15 Global IPO update

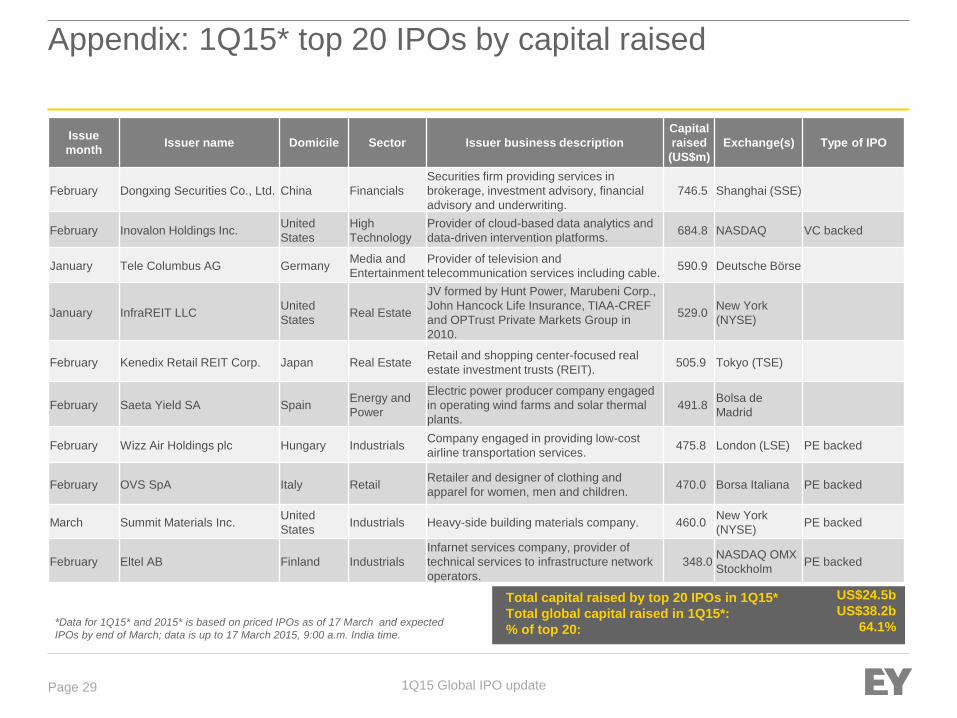

Appendix: 1Q15* top 20 IPOs by capital raised

Issue

month Issuer name Domicile Sector Issuer business description

Capital

raised

(US$m)

Exchange(s) Type of IPO

February Aena SA Spain Industrials Airports operator. 4,823.8 Bolsa de

Madrid Former SOE

March 1MDB Energy Sdn Bhd Malaysia Energy Financial vehicle created for the purchase

of Tanjong by 1Malaysia Development. 3,000.0

Bursa

Malaysia

February Sunrise Communications AG Switzerland Telecommunicat

ions

Fixed-line telecommunications services

provider. 2,459.3

SIX Swiss

Exchange PE backed

February Jasmine Broadband Internet

Growth Infrastructure Fund Thailand

Telecommunicat

ions

Infrastructure Fund invest in fiber-optic

network for broadband internet. 1,686.3 Thailand (SET)

March Orient Securities Co., Ltd.

(China) China Financials

Provider of financial services, including

securities brokerage. 1,629.1

Shanghai

(SSE)

March Auto Trader Group Ltd. United

Kingdom Industrials

Provider of online motoring digital

marketplace for motor vehicle buyers and

sellers.

1,510.1 London (LSE) PE backed

February Columbia Pipeline Partners LP United States Energy Owns, operates and develops a portfolio

of pipelines for natural gas transmission. 1,238.2

New York

(NYSE)

February GrandVision NV Netherlands Retail Retailer of optical products. 1,167.9 Euronext

(Amsterdam)

PE backed

February Elis SA - Groupe Elis France Consumer

Products

Provides rental and cleaning of uniforms,

linens, water coolers and espresso coffee

machine, sanitary equipment and floor

protection.

966.8 Euronext

(Paris)

PE backed

March HKBN Ltd. Hong Kong,

China

Consumer

Products

Provider of fibre broadband services in

Hong Kong. 748.4

Hong Kong

(HKEx)

*Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 29 1Q15 Global IPO update

Appendix: 1Q15* top 20 IPOs by capital raised

Issue

month Issuer name Domicile Sector Issuer business description

Capital

raised

(US$m)

Exchange(s) Type of IPO

February Dongxing Securities Co., Ltd. China Financials

Securities firm providing services in

brokerage, investment advisory, financial

advisory and underwriting.

746.5 Shanghai (SSE)

February Inovalon Holdings Inc. United

States

High

Technology

Provider of cloud-based data analytics and

data-driven intervention platforms. 684.8 NASDAQ VC backed

January Tele Columbus AG Germany Media and

Entertainment

Provider of television and

telecommunication services including cable. 590.9 Deutsche Börse

January InfraREIT LLC United

States Real Estate

JV formed by Hunt Power, Marubeni Corp.,

John Hancock Life Insurance, TIAA-CREF

and OPTrust Private Markets Group in

2010.

529.0 New York

(NYSE)

February Kenedix Retail REIT Corp. Japan Real Estate Retail and shopping center-focused real

estate investment trusts (REIT). 505.9 Tokyo (TSE)

February Saeta Yield SA Spain Energy and

Power

Electric power producer company engaged

in operating wind farms and solar thermal

plants.

491.8 Bolsa de

Madrid

February Wizz Air Holdings plc Hungary Industrials Company engaged in providing low-cost

airline transportation services. 475.8 London (LSE) PE backed

February OVS SpA Italy Retail Retailer and designer of clothing and

apparel for women, men and children. 470.0 Borsa Italiana PE backed

March Summit Materials Inc. United

States Industrials Heavy-side building materials company. 460.0

New York

(NYSE) PE backed

February Eltel AB Finland Industrials

Infarnet services company, provider of

technical services to infrastructure network

operators.

348.0 NASDAQ OMX

Stockholm PE backed

Total capital raised by top 20 IPOs in 1Q15*

Total global capital raised in 1Q15*:

% of top 20:

US$24.5b

US$38.2b

64.1% *Data for 1Q15* and 2015* is based on priced IPOs as of 17 March and expected

IPOs by end of March; data is up to 17 March 2015, 9:00 a.m. India time.

Page 30 1Q15 Global IPO update

Appendix: definitions

► Geographic definitions:

► Asia includes Bangladesh, Greater China, Indonesia, Japan, Laos, Malaysia, Philippines, Singapore, South Korea, Sri Lanka, Thailand and Vietnam.

► Greater China includes mainland China, Hong Kong, Macau and Taiwan.

► Asia-Pacific includes Asia (as stated above) plus Australia, New Zealand, Fuji and Papua New Guinea.

► Central and South America includes Argentina, Bermuda, Brazil, Chile, Colombia, Ecuador, Jamaica, Mexico, Peru and Puerto Rico.

► EMEIA includes Armenia, Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary,

Iceland, India, Ireland, Isle of Man, Italy, Kazakhstan, Luxembourg, Lithuania, Netherlands, Norway, Pakistan, Poland, Portugal, Russian Federation, Spain,

Sweden, Switzerland, Turkey, Ukraine and United Kingdom plus the Middle East and Africa countries listed below.

► Middle East includes Bahrain, Iran, Israel, Jordan, Kuwait, Oman, Qatar, Saudi Arabia, Syria, United Arab Emirates and Yemen.

► Africa includes Algeria, Botswana, Egypt, Ghana, Kenya, Madagascar, Malawi, Morocco, Namibia, Rwanda, South Africa, Tanzania, Tunisia, Uganda,

Zambia and Zimbabwe.

► North America consists of the United States and Canada.

► Emerging markets or rapid-growth markets include issuers from Argentina, Armenia, Bangladesh, Bolivia, Brazil, Bulgaria, Chile, Colombia,

Croatia, Cyprus, Egypt, Ethiopia, Greater China, Hungary, India, Indonesia, Ireland, Israel, Kenya, Kuwait, Kazakhstan, Laos, Lithuania,

Malaysia, Mauritius, Mexico, Namibia, Pakistan, Peru, Philippines, Poland, Qatar, Russian Federation, Saudi Arabia, Sierra Leone, Singapore,

Slovenia, South Africa, South Korea, Sri Lanka, Tanzania, Thailand, Tunisia, Turkey, Ukraine, United Arab Emirates, Vietnam and Zambia.

► Developed markets include issuers from Australia, Austria, Belgium, Bermuda, Canada, Denmark, Finland, France, Germany, Greece,

Guernsey, Isle of Man, Italy, Japan, Jersey, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, United

Kingdom and United States.

► State-owned enterprise (SOE) privatizations refers to former state-owned entities that have completed their IPO listings to become public

companies.

► Many stock exchanges have set up main markets and junior markets. Main markets are where medium and large IPOs (by capital raised)

are usually listed and traded. Junior markets are where small-cap companies or smaller IPOs are listed or traded. Stock exchanges without

junior markets are classified as main markets.

► Junior markets include:

► Americas: American, Canadian National Stock Exchange, Toronto Venture Exchange and Jamaica.

► Asia-Pacific: Malaysia ACE Market, Bombay SME, Hong Kong Growth Enterprise Market, Japan JASDAQ, Korea KOSDAQ, Thailand Market for Alternative

Investment, National SME, Shenzhen ChiNext, Singapore Catalist, Tokyo Stock Exchange MOTHERS Index.

► EMEA: Alternext, London Alternative Investment Market, Germany's Frankfurt Entry Standard, Spain's Mercado Alternativo Bursatil, NASDAQ OMX First

North, Warsaw New Connect, Johannesburg Alternative Market.

Global IPO press release and Global IPO update slides – 2015 Q1 Date published: 20 March 2015

For PR inquiries, please contact:

Will Brewster

Associate Director, EY Global Media Relations

+44 (0) 207 980 0812

For information about EY’s IPO services and our IPO point of view, please contact:

Dr. Martin Steinbach

Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft

Mergenthalerallee 3-5, 65760 Eschborn, Germany

Office: +49 (0) 6196 996 11574

Mobile: +49 (0) 160 939 11574

Produced by Global Markets — EY Knowledge:

Anshul Singh, Market Performance, Global Markets – EY Knowledge

+91 124 619 2943

Contributors include: Akriti Kapoor, Harshit Takkar

This report was requested by:

Eva Chan, Manager – Global IPO Center, Strategic Growth Markets

+44 (0) 207 980 0254

Visit the EY Knowledge CHS for help accessing and using knowledge tools and services.

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services.

The insights and quality services we deliver help build trust and confidence

in the capital markets and in economies the world over. We develop

outstanding leaders who team to deliver our promises to all of our

stakeholders. In so doing, we play a critical role in building a better working

world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the

member firms of Ernst & Young Global Limited, each of which is a separate

legal entity. Ernst & Young Global Limited, a UK company limited by

guarantee, does not provide services to clients. For more information about

our organization, please visit ey.com.

About EY's IPO services

EY is a leader in helping to take companies public worldwide. With

decades of experience our global network is dedicated to serving market

leaders and helping businesses evaluate the pros and cons of an IPO. We

demystify the process by offering IPO readiness assessments, IPO

preparation, project management and execution services, all of which help

prepare you for life in the public spotlight. Our Global IPO Center of

Excellence is a virtual hub which provides access to our IPO knowledge,

tools, thought leadership and contacts from around the world in one easy-

to-use source. www.ey.com/ipocenter

© 2015 EYGM Limited.

All Rights Reserved.

EYG no. CY0882

ED None

This material has been prepared for general information purposes only and is not intended to

be relied upon as accounting, tax or other professional advice. Please refer to your advisors

for specific advice.

www.ey.com/ipocenter