Q2 2021 An independent report by BVA BDRC, August 2021

136

Q2 2021 An independent report by BVA BDRC, August 2021

Transcript of Q2 2021 An independent report by BVA BDRC, August 2021

Q2 2021

An independent report by BVA BDRC, August 2021

Over 170,000 SME interviews have been

conducted since the survey started in Q2 2011,

across 40 waves of interviewing. Major changes

were made to the questionnaire for Q1 2018.

The report and supporting data is made available

to all interested parties as a basis for decision

making and strategy setting. It is used by

Government, the Bank of England, the banks, trade

bodies and academics.

The SME Finance Monitor Q2 2021

2

This survey was commissioned to provide a robust and respected independent source of information on the demand

for, and availability of, finance for SMEs in the UK.

Find out more at www.sme-finance-monitor.co.uk

The core study covers:

•Borrowing events in the past 12 months

•The appetite for new/renewed facilities

•The outcome of applications made

•Reasons for not borrowing

•Future plans, including demand for future finance

•Awareness of support and finance initiatives

3

A brief timeline to remind us of what has happened in the first half of 2021 – from national lockdowns to “Freedom Day” (nearly)

April Non-essential retail re-

opens, including

hairdressers. 10% of adults

now double vaccinated

May More indoor and

outdoor gatherings allowed,

restaurants re-open, travel

“traffic light” system set up

June “Freedom Day”

delayed, Delta strain now

dominant, 62% of adults

double vaccinated

Jan England enters 3rd

national lockdown. 17% of

adults had their first vaccine

jab by month end

Feb Hotel quarantine for red

list countries, Government

announces roadmap for

lifting lockdown

March Schools re-open,

outdoor gatherings allowed

for 6 people/2 h/holds. CBIL

& BBL applications close

Oct 3 tier system and new

JSS scheme announced.

National lockdown

announced for Nov 5th

Nov National lockdown,

furlough/ BBL/ CBILs

extended again, vaccine

success announced

Dec Kent variant discovered

and Tier 4 created, Christmas

plans revised/cancelled.

Transition period ended

Q420

Q121

Q221

Q2 2020 was a real shock to the SME system. Broadly speaking, sentiment in Q3 was a bit better, with little change in

Q4, and Hospitality and Transport consistently the most likely to report issues.

This pack updates the story with data to Q2 2021 and is designed primarily to explore:

• Data from the Covid related questions run from Q2 2020

• How SMEs have responded so far to Covid 19 and it’s impact on their business, comparing annual results over time to

those for 2020 and the first half of 2021.

• Additional analysis to build understanding of how different parts of the economy have been impacted with analysis by

sector and region

• A focus on repayment of debt and concerns around this, from the new questions added this year

The presentation today will introduce you to some key themes from the SME Finance Monitor.

Much more detail can be found in the full chart pack which will be circulated after this session.

Are we in the recovery phase yet?

4

Setting the scene: How SMEs are currently feeling

5

42% 41%

32%

24%

60%

52%54%

56%

32%

69%

Plan to grow Good business mood Income stable or increased Future offers oportunities Happy that have enough

funding

Q4 20 Q2 21

Across a range of five key metrics, SME sentiment improved between Q4 2020 and Q2 2021

6

Sentiment summary: Q4 2020 to Q2 2021

All SMEs: Total score of plan to grow/ good business mood/ Income to be stable or increased/ future offers opportunities / not worried about

having enough funding for next months

The combined percentage score has increased from 196 to 258 between Q4

2020 and Q2 2021, an increase of +32%.

192% 205%234% 224%

251%273%

311%281%

0 1-9 10-49 50-249

Q4 20 Q2 21

On a combined basis, larger SMEs with 10-49 employees remained were more likely to see a positive future impact.

7

Positive future impact summary score

All SMEs: Total score of plan to grow/ good business mood/ Income to be stable or increased/ future offers opportunities / not worried about

having enough funding for next months

Q420

Q221

218%200% 195%

236%

126% 132%

222% 211%186%

288%258% 266%

244%226% 214%

277% 283%251%

Agr Mfg Constr Wle/Ret Hot/Rest Trans Prop/BSv Health Other Com

Q4 20 Q2 21

By sector: Those in the Hospitality and Transport sectors remained less likely than their peers to be feeling positive, but have closed some of the gap as their scores increased. With little change in sentiment, those in Wholesale/Retail have moved from above to below average

8

Positive future impact summary score

All SMEs: Total score of plan to grow/ good business mood/ Income to be stable or increased/ future offers opportunities / not worried about

having enough funding for next months

Q420

Q221

225%202%

239%

191%213% 199%

219%191% 183%

281% 268%286%

254% 268% 275% 261% 259% 245%

Export only Import only Fully intl Domestic only Starts 2-5 yrs 6-9 yrs 10-15 yrs 15yrs+

Q4 20 Q2 21

The mood of fully international SMEs has not improved as fast as their peers, but they remained above average. Those trading for 6-9 yrs also reported a smaller improvement

9

Positive future impact summary score

All SMEs: Total score of plan to grow/ good business mood/ Income to be stable or increased/ future offers opportunities / not worried about

having enough funding for next months

Q420

Q221

61% 59%67%

58% 60%

16% 17% 16%9% 9%

All 0 1-9 10-49 50-249

Borrowing more Concerned repay

As mood and conditions improve, use of finance was also higher: In Q2 2021, 61% of finance users said they were using more finance now than pre-pandemic (with 36% borrowing for the first time). A minority of finance users were concerned about their general ability to repay funds

10

Concerns about using finance: All those using external finance Q2 2021

All SMEs using external finance Q2 2021

45%Use finance: 41% 57% 65% 35%

Today’s presentation

11

The trading context

External funding: attitudes to and use of, alongside alternatives

Demand for finance: need, applications and impact of Covid

The future: growth, barriers and future appetite for finance

The immediate impact of Covid 19

Today’s presentation

12

The trading context

External funding: attitudes to and use of, alongside alternatives

Demand for finance: need, applications and impact of Covid

The future: growth, barriers and future appetite for finance

The immediate impact of Covid 19

There has been an improvement in the ‘mood’ of businesses, with half now in a good mood, up from a quarter in Q2 2020 and increasing by size of SME

13

Mood about the business from Q2 2020

CV1 Base : All SMEs Q2 2021 4252 865/1403/1318/664

49%

32% 33% 34%23%

27%

27% 26% 26%

23%

17%

27% 27% 27%

32%

8%13% 14% 12%

22%

Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

24%26%

34%

42%38%

47%

52%

58%

39%41%

55%57%

37%

43%

56%

62%

51%

59%

75%

70%

0 emps 1-9 emps 10-49 emps 50-249 emps

Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

Mood 7-10

Mood 7-8

Mood 5-6

Mood 0-4

Mood 9-10

Mood 7-10 25% 40% 41% 39% 54%

37%

27%

19%

27%

12%16%

33%

28%

19%

57%

46%43%

45%

16%

23%

50%

37%33%

69%

58%61%

52%

46%

38%

54%56% 56%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q2 20 Q4 20 Q2 21

Those in Agriculture remained more likely to be in a good mood. Amongst those struggling, Hospitality saw more of an improvement in mood than Transport

14

Sector summary: Mood 7-10

CV1 Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

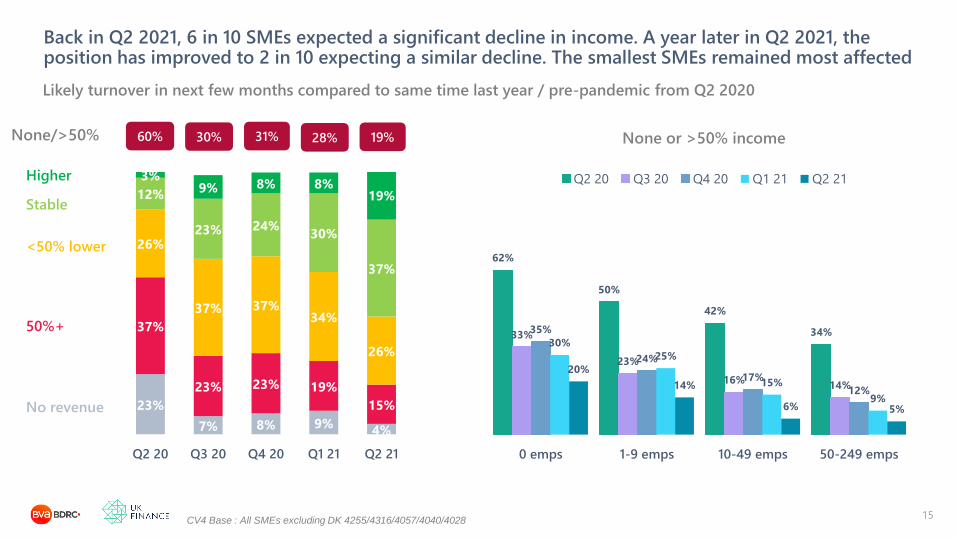

Back in Q2 2021, 6 in 10 SMEs expected a significant decline in income. A year later in Q2 2021, the position has improved to 2 in 10 expecting a similar decline. The smallest SMEs remained most affected

15

Likely turnover in next few months compared to same time last year / pre-pandemic from Q2 2020

CV4 Base : All SMEs excluding DK 4255/4316/4057/4040/4028

23%

7% 8% 9%4%

37%

23% 23% 19%

15%

26%

37% 37%34%

26%

12%

23% 24%30%

37%

3%9% 8% 8%

19%

Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

No revenue

<50% lower

50%+

Higher

Stable

None/>50% 60% 30% 31%

62%

50%

42%

34%33%

23%

16%14%

35%

24%

17%

12%

30%

25%

15%

9%

20%

14%

6% 5%

0 emps 1-9 emps 10-49 emps 50-249 emps

Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

None or >50% income28% 19%

42%

62%65%

43%

78%

65%

54%

63%65%

18%

32%

24%

29%

57%54%

21%

30%

44%

5%

14% 15%13%

23%25%

19%17%

23%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q2 20 Q4 20 Q2 21

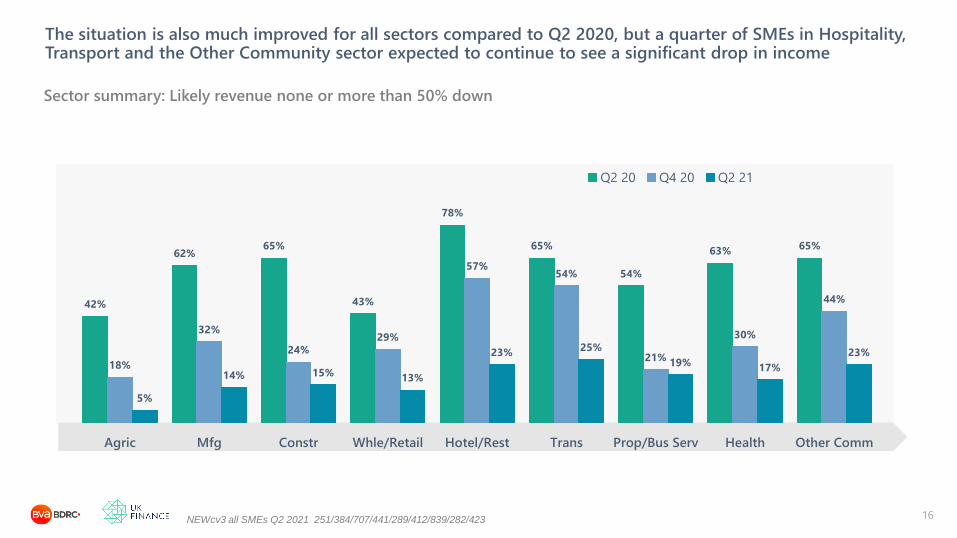

The situation is also much improved for all sectors compared to Q2 2020, but a quarter of SMEs in Hospitality, Transport and the Other Community sector expected to continue to see a significant drop in income

16

Sector summary: Likely revenue none or more than 50% down

NEWcv3 all SMEs Q2 2021 251/384/707/441/289/412/839/282/423

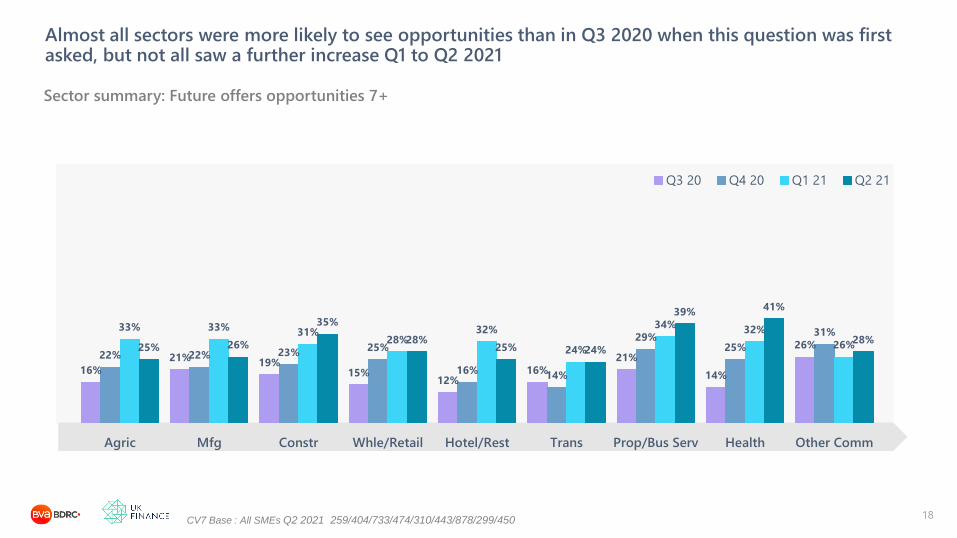

There has been a steady increase in the proportion expecting the future to offer opportunities rather than threats, both overall and across all size bands

17

Does the future offer opportunities or threats – from Q3 2020

CV7 Base : All SMEs Q2 2021 4252 865/1403/1318/664

32%25% 21% 17%

49%

50%49%

50%

11%14%

17%18%

8% 10% 14% 14%

Q3 20 Q4 20 Q1 21 Q2 21

19% 19% 17% 17%24% 25% 26% 23%

30% 31% 34%26%

32% 33% 33%26%

0 emps 1-9 emps 10-49 emps 50-249 emps

Q3 20 Q4 20 Q1 21 Q2 21

Offers opportunities 7+Offers opp. 7+ 19% 24%

7-8

5-6

Only offers threats 1-4

Offers opportunities 9-10

31% 32%

SMEs that have seen a steady

increase in future opportunities

include those in Health (now 41%),

Property/Business Services (39%)

and Construction (now 35%)

16%

21%19%

15%12%

16%

21%

14%

26%22% 22% 23%

25%

16%14%

29%25%

31%33% 33%

31%28%

32%

24%

34%32%

26%25% 26%

35%

28%25% 24%

39%41%

28%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q3 20 Q4 20 Q1 21 Q2 21

Almost all sectors were more likely to see opportunities than in Q3 2020 when this question was first asked, but not all saw a further increase Q1 to Q2 2021

18

Sector summary: Future offers opportunities 7+

CV7 Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

61%

5%

59%

16%

12%

58%

14%

6%

Staff on furlough

Made staff redundant

May have to make staff

redundant (New Q3)

Q2 20 Q4 20 Q2 21

Compared to Q4 2020, fewer employers thought they would be making redundancies in the future. Those with 50-249 employees remained the most likely to be contemplating redundancies

19

How business has been impacted – All employers from Q2 2020

QCv3a – all employers Q2 2021 3385

All sectors reported an improving picture compared to Q4 2020, but a quarter of SMEs in Hospitality,

Transport and the Other Community sector either have or may have to, make redundancies

Larger SMEs were more likely to

have staff on furlough – 53% of

those with 1-9 emps compared

to 80% with 10-49 emps and

82% with 50-249 emps.

Larger SMEs were also more likely to have made, or be

contemplating, redundancies (36%) and this was unchanged

from Q3 2020.

Overall, 17% of employers either had or were contemplating

making redundancies, back in line with Q3 2020.

18%15%

29%

35%

23%20%

37%41%

22%18%

35% 35%

17%15%

26%

36%

All 1-9 emps 10-49 emps 50-249 emps

Q3 20 Q4 20 Q1 21 Q2 21

The proportion of employers that had made, or might have to make, redundancies, was back in line with Q3 2020. It remained most common amongst the larger employers

20

Made or may make employees redundant from Q3 2020

Cv3a all SMEs Q2 2021 3385 1403/1318/664

All sectors reported an improving picture compared to Q4 2020, but a quarter of SMEs

in Hospitality, Transport and the Other Community sector either have or may have to,

make redundancies

9%

18%16% 16%

26%24%

17%13%

19%

10%

26%

19%

24%

35%

30%

21%

10%

28%

10%

25%

18%20%

27%

22% 22%18%

27%

7%

20%

13%

19%

25%23%

14%

8%

25%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q3 20 Q4 20

All sectors reported an improving picture compared to Q4 2020, but a quarter of SMEs in Hospitality, Transport and the Other Community sector either had or may have to, make redundancies

21

Made or may make employees redundant from Q3 2020

Cv3a all SMEs Q2 2021 3385

68% 67% 62%54%52% 52% 45% 38%

46% 43%30% 23%

0 emps 1-9 emps 10-49 emps 50-249 emps

Q2 20 Q4 20 Q2 21

“Impact of the pandemic” remained the top barrier in Q2 2021, declining somewhat by size of SME

22

Main barriers (8-10) to running business in next 12 months –Q2 2021:

Q93 Barriers to running business as would want in next 12 months

Base : All SMEs Q2 2021 4250 865/1403/1318/664

45%

21%

21%

18%

10%

10%

9%

8%

6%

Impact of pandemic

The current economic climate

Legislation,regulation, red tape

Political uncertainty/future govt policy

Cash flow / late payment

Recruiting and retaining staff

Changes in value of sterling

Access to external finance

Availablity of relevant advice

In Q2 when this question was first asked,

68% of SMEs cited the pandemic as a main

barrier. The decline over time to 45% in Q2

2021 was seen across all size bands, with the

largest SMEs less likely to see it as a barrier

In Q2, concern remained highest amongst

those in Hospitality and Transport, where 6

in 10 were concerned compared to a quarter

of those in Agriculture

There has been an improvement over time, but SMEs in the Hospitality and Transport sectors continued to report the highest levels of concern, notably compared to those in Agriculture

23

6 in 10 SMEs in the Hospitality and Transport sectors rate the effect of the pandemic as

a major barrier to their business, with relatively little change over time, compared to 23%

in Agriculture. Levels of concern in Wholesale/retail; and Business Services appears to

have plateaued in recent quarters

Sector summary: % “Impact of pandemic” 8-10 barrier over time

Q93 Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

57%

68%

74%

64%

87%

70%

60%

68%71%

35%

45%42%

45%

72% 70%

46%

54%

64%

23%

39%35%

42%

60%64%

44% 43% 45%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q2 20 Q4 20 Q2 21

The immediate impact of Covid 19- Key findings

24

Whilst the impact of the pandemic remained the key barrier to running the business, it was mentioned by 45%

of SMEs compared to 68% in Q2 2020. Around 1 in 5 thought their turnover would be reduced by 50% or

more for the coming months, but again this was a further improvement on the 6 in 10 expecting such a

reduction in Q2 of 2020. Overall, 17% of employers either had or were contemplating making redundancies,

back in line with Q3 2020 and lower than the 23% planning such action in Q4 2020.

Over half of SMEs were in a positive mood about their business, twice the level seen in Q2 of 2020. 1 in 3 felt the

future offered more opportunities than threats, up from 1 in 5 in Q3 2020

Q2 2020 was a shock to the SME system. Sentiment in Q3 was somewhat better, with little change in Q4.

Moving into 2021, sentiment and expectations have improved and whilst those in Hospitality and Transport

remained the worst affected on many metrics, their position has improved

Today’s presentation

25

The trading context

External funding: attitudes to and use of, alongside alternatives

Demand for finance: need, applications and impact of Covid

The future: growth, barriers and future appetite for finance

The immediate impact of Covid 19

37% 40% 42% 39% 40% 42% 39% 37% 34% 34% 25% 16% 13% 15%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

After declining in the second half of 2020, the proportion reporting growth stabilised at around 1 in 6, with little to choose between size bands and all at lower levels than seen pre-pandemic

26

Annual time series: % reporting growth in previous 12 months

Q81 all SMEs excl Starts and DK Q2 2021 3910 724/1246/1286/654

18%

22%

18%

14%

50-249 emps

10-49 emps

1-9 emps

0 emps

All SMEs

54%

48%

42%

35%

In Q2 2021,very few in the Hospitality sector have reported any growth (5%), with a continued decline for

those in Wholesale/Retail (now 15%) and a more stable position since Q4 2020 elsewhere. A fifth of those in

Agriculture and Property/Business Services reported growth

37%35% 34%

41% 40%

35%37%

47%

36%

23%

39%

26%

44%

34% 35% 34%

41%

36%33%

13% 12%

21%

3%

10%

21%18%

16%

21%

13% 14% 15%

5%8%

20%

15%19%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

2019 Q2 20 Q4 20 Q2 21

Very few in the Hospitality sector reported any growth, with a continued decline for those in Wholesale/Retail and a more stable position since Q4 2020 elsewhere

27

Sector summary: Grown – over time

cv3 all SMEs excl Starts and DK Q2 2021 252/374/675/424/274/424/808/265/414

After the sharp increase to Q4 2020 in SMEs reporting a decline in growth, the picture into 2021 was stable, but at the higher levels seen in Q4 2020

28

Annual time series: Performance in previous 12 months

Q81 all SMEs excl Starts and DK Q2 2021 3910

Grown

Stayed same

Declined

As the effect of the pandemic continues to be felt, more SMEs are reporting an impact on their growth in

the previous 12 months. 15% had grown, in line with the lowest levels seen since Q4 2020 on the Monitor

and over half, 60%, had declined, one of the highest levels seen to date

21% 19% 14% 12% 10% 11%17% 19% 21% 22%

46%

61% 64% 60%

42% 41%44% 51% 50% 47%

44% 44% 45% 44%

29%

23%23%

25%

37% 40% 42%39% 40% 42% 39% 37% 34% 34%

25%16% 13% 15%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

The proportion reporting a decline in Q2 2021 was in line with Q4 2020, with larger SMEs in particular less likely to be reporting a decline than in Q1 2021, albeit still well above pre-pandemic levels

29

Annual time series: % reporting decline in previous 12 months

Q81 all SMEs excl Starts and DK Q2 2021 3910 724/1246/1286/654

The proportion reporting a decline increased to 64% in Q1 2021 and across all size bands except

the largest SMEs. The overall figure was slightly lower in Q2 2021 as fewer larger SMEs in particular

reported a decline (although still well above pre-pandemic levels) In Q2 2021, 84% in the

Hospitality sector and 73% in Transport reported a decline.

42%

48%

59%

61%

All SMEs

50-249 emps 13%

10-49 emps 14%

1-9 emps 19%

0 emps 22%

21% 19% 14% 12% 10% 11% 17% 19% 21% 22% 46% 61% 64% 60%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

14%

20%18% 18%

20% 19% 20%

8%

21%20%18% 18%

15%

34%

24%27%

10%

29%

37%

62% 62%

56%

86%

74%

52%

63% 62%

41%

58%

49%

59%

84%

73%

57%

62%

67%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

2019 Q2 20 Q4 20 Q2 21

SMEs in Hospitality and Transport remained the most likely to report a decline with little change since Q4, as Construction reported a slightly improving picture

30

Sector summary: Declined – over time

Q81 all SMEs excl Starts and DK Q2 2021 252/374/675/424/274/424/808/265/414

In Q2 2021, 8 in 10 Hospitality SMEs and 7 in 10 in Transport reported that they had declined in size. As

on other metrics, those in Agriculture remained less affected, but 4 in 10 now report a decline and the

proportion in Property/Business Services has increased to almost 6 in 10.

70% 77% 80% 80% 82% 78% 82% 79% 69% 60%

2013 2014 2015 2016 2017 2018 2019 2020 Q1 21 Q2 21

30%

28%

34%

40%

51%

39%

36%

47%

53%

42%

52%

49%

60%

69%

66%

64%

61%

71%

77%

75%

All

0 emps

1-9 emps

10-49 emps

50-249 emps

2018

2019

2020

H1 21

60% of SMEs reported a profit, the lowest level seen to date but with signs of improvement in Q2 2021 for the larger SMEs. Two thirds of SMEs said improving profit margins was a key priority

31

Annual time series: % making a profit (excl DK)

Q115/84 All SMEs Q2 2021 4252 865/1403/1318/664

The proportion of SMEs making a profit has reduced in 2021,

as the impact of the pandemic is felt in year-end results. The

median profit made was £10,000 in Q2 and has been £10-

12k since Q1 2020 compared to £8-9k in 2019.

75%80%

66%

57%

50-249

10-49

1-9

0

All SMEs

81%

80%

72%

67%

Improving profit margin a key priority: over time

In H1 2021, 64% of SMEs said improving profit margins was

a key priority for them and this proportion has increased

over time (from 30% in 2018) overall, and for all sizes of SME

81% 81%85%

76% 74%

80%84% 86%

78%77%81% 80% 78%

72%77%

83%80%

73%71%66%

70%

63%

44%

53%

70%

61% 62%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

2019 2020 H1 21

SMEs in Hospitality and Transport were much less likely to report having made a profit than their peers, as the impact of the pandemic starts to be reflected in annual profit figures

32

Sector summary: Made a profit – over time

Q115 all SMEs excl DK H1 2021 419/639/1130/717/450/680/1412/444/667

In H1 2021, those in Hospitality were the least likely to repot having made a profit. Improving profit

margins was a priority for the majority of SMEs in each sector, ranging from 57% in Health to 70% in

Hospitality (v 61% in Transport)

55% 54% 54% 55% 57% 56%60%

52% 54% 56%

13%16% 17%

14% 16% 15% 16% 16%19% 17%

38% 37% 37% 36% 34% 33% 35%

42%

45%

43%

12% 11% 10% 11%15% 15% 17%

2013 2014 2015 2016 2017 2018 2019 2020 Q1 21 Q2 21

In 2021 to date, levels of innovation were maintained at the higher level seen in 2020, levels of planning were back in line and there has been a further slight increase in the use of mentors

33

Annual time series: Business management

Q84 Base : All SMEs Q2 2021 4252 865/1403/1318/664

International

Plan

Innovate

Mentors

Innovation 2012 2019 2020 Q1 21 Q2 21

New product 17% 15% 17% 22% 20%

Impr. process 35% 30% 38% 40% 39%

Any

innovation

All 0

emps

1-9

emps

10-49

emps

50-249

emps

2012 40% 36% 49% 60% 70%

2019 35% 31% 43% 51% 50%

2020 42% 39% 50% 60% 63%

H1 2021 44% 42% 49% 62% 62%

All sectors were more likely to have been innovative in H1 2021 than in 2019, notably those in

Hospitality (51% from 43% in 2019). Those in Construction remained the least likely to have

innovated (33% from 25% in 2019) along with Transport (36% from 30%) with other sectors 39-50%.

30%

40%

25%

45%

43%

30%

36%

34%

41%

41%

44%

31%

48%

50%

38%

46%

47%

47%

39%

48%

33%

49%

51%

36%

49%

44%

50%

Agric

Mfg

Constr

Whle/Retail

Hotel/Rest

Trans

Prop/Bus Serv

Health

Other Comm

2019

2020

H1 21

All sectors saw an increase in innovation 2019-20 with those gains maintained in H1 2021. For most sectors, levels of planning increased slightly but remained below 2019 levels

34

Innovation

Q84 all SMEs H1 2021 518/804/1455/943/599/887/1803/613/891

58%

60%

55%

69%

71%

61%

57%

65%

56%

55%

55%

43%

63%

63%

53%

54%

49%

50%

60%

56%

46%

62%

63%

52%

59%

57%

51%

Agric

Mfg

Constr

Whle/Retail

Hotel/Rest

Trans

Prop/Bus Serv

Health

Other Comm

Planning

22% 21% 17%

28%23% 25% 23% 19%

53% 55%

48%

50%51% 51% 51%

50%

25% 25%

35%

22% 26% 24% 26%31%

2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

9% 8% 7%14% 10% 11% 11% 7%

37% 36%31%

38%36% 36% 36%

31%

55% 55%62%

48%54% 53% 53%

62%

2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

Trust in main bank fell in Q2 2020 but by Q2 2021 was back in line with the start of the pandemic. Trust in the banking industry remained at lower levels, but also somewhat better than Q2 2020

35

Level of trust by size over time

Q24b Base : All SMEs Q2 2021 4250

High level of trust 8-10

Medium level of trust 5-7

Low level of trust 1-4

Trust in main bank Trust in banking industry

A low level of trust in main bank was seen

more often amongst SMEs with 0 or 1-9

employees (7-8%), or those in

Wholesale/Retail (10%)

A low level of trust in banking was seen more

often amongst SMEs with 0 employees (20%),

Transport (23%) and also Wholesale/Retail

and Property/Business Services (both 21%)

19% 20% 17%11% 6%

50% 51%50%

48%51%

31% 30% 33%41% 43%

All 0 Emp 1-9 emp 10-49

emp

50-249

emp

7% 7% 8% 6% 2%

31% 30% 32%26% 31%

62% 62% 60%68% 67%

All 0 Emp 1-9 emp 10-49

emp

50-249

emp

Levels of trust in main bank were slightly higher amongst larger SMEs, with trust in the banking industry increasing more clearly by size of SME

36

Level of trust by size Q2 2021

Q24b Base : All SMEs Q2 2021 4252 865/1403/1318/664

High level of trust 8-10

Medium level of trust 5-7

Low level of trust 1-4

Trust in main bank Trust in banking industry

8% 7% 8% 10% 8% 8% 7% 5% 4%

32% 36% 33% 28% 29% 28% 30% 33%29%

60% 57% 59% 62% 63% 64% 62% 61% 67%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

High

Medium

Low

There was little difference by sector in levels of trust in their main bank

37

Sector summary: Level of trust in main bank Q2 2021

Q24b Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

18% 15% 17% 21% 16%23% 21%

13% 15%

51%50% 49% 46% 51%

45% 53%56% 53%

31% 35% 34% 33% 33% 32%26% 31% 32%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

High

Medium

Low

Trust in the banking industry was lower than for main bank across all sectors, again with relatively little to choose between them

38

Sector summary: Level of trust in banking industry Q2 2021

Q24c Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

62% of SMEs had a high level of trust in their main bank in Q2 2021, an improvement from 48% in Q2 2020 and

back to levels seen in Q1 2020. Trust in the banking industry more generally remained lower than for the main

bank at 31%, but again this was higher than in Q2 2020 when 22% had a high level of trust

The trading context - Key findings

39

Reported growth in the last 12 months remained low in Q2 2021 at 15%, but little changed from Q4 2020. 6 in

10 SMEs reported a decline, again little changed since Q4 2020 but much higher than seen pre-pandemic.

Fewer SMEs reported making a profit (60% in Q2 2021) but improving profit margins has become more of a

priority (63% of all SMEs). Those in Hospitality or Transport remained more likely to report a decline and less

likely to have made a profit

As SMEs seek to cope with the “new normal”, levels of innovation remained higher than previously seen: 43%

had been innovative, with 20% introducing a new product or service and 39% improving a business process.

Those who had been innovative were slightly more likely to have made a profit and to have grown than those

who had not

Today’s presentation

40

The trading context

External funding: attitudes to and use of, alongside alternatives

Demand for finance: need, applications and impact of Covid

The future: growth, barriers and future appetite for finance

The immediate impact of Covid 19

Attitudes to finance

41

80%73%

55%52% 51%

42% 41%37%

29%

85%80%

68%

57%51%

43%37%

41%

33%

86%82%

68%63%

57%

46%

36%43%

37%

Plan what can

afford

Accept slower

growth

Future

uncertain so

cautious

Cost of credit

discourage

Never think to

use more

finance

Prepared to

take risks to

succeed

Difficult for us

to get finance

Ambition to be

significantly

bigger

Happy to use

finance to grow

2019 2020 H1 21

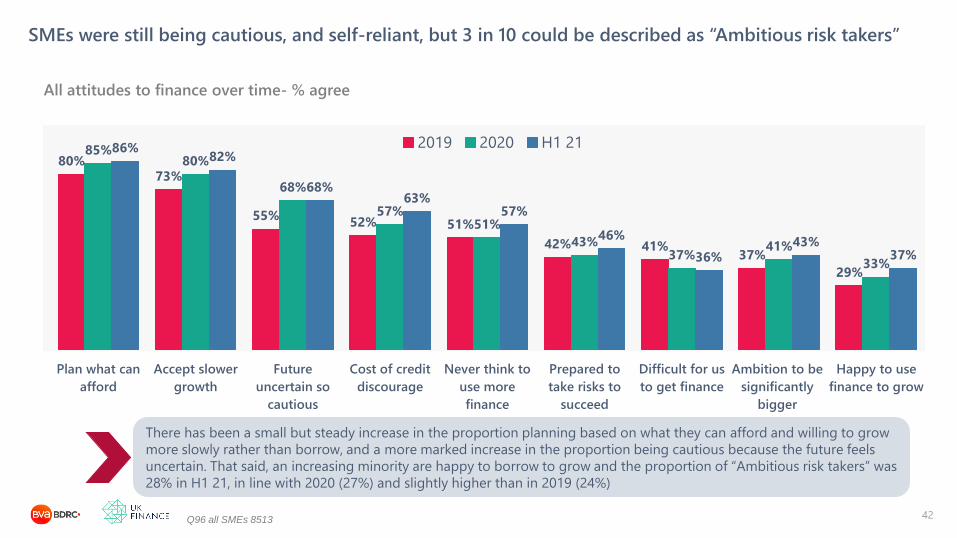

SMEs were still being cautious, and self-reliant, but 3 in 10 could be described as “Ambitious risk takers”

42

All attitudes to finance over time- % agree

Q96 all SMEs 8513

There has been a small but steady increase in the proportion planning based on what they can afford and willing to grow

more slowly rather than borrow, and a more marked increase in the proportion being cautious because the future feels

uncertain. That said, an increasing minority are happy to borrow to grow and the proportion of “Ambitious risk takers” was

28% in H1 21, in line with 2020 (27%) and slightly higher than in 2019 (24%)

Smaller SMEs have become more likely to meet the definition of an Ambitious risk taker, the largest SMEs somewhat less likely

43

In challenging trading conditions, more smaller SMEs have met the definition of an Ambitious

risk taker – an SMEs that wants to be significantly bigger and is prepared to take risks to be

successful. Those in Wholesale/Retail (33%) and Manufacturing (31%) were the most likely to

meet the definition of an Ambitious risk taker, both higher than in 2019.

Ambitious risk takers, over time

Q96 Base : All SMEs H1 2021 8513 1715/2813/2721/1264

24%21%

29%35%

42%

27% 25%

33%36% 38%

28% 26%

34%37% 36%

All SMEs 0 emps 1-9 emps 10-49 emps 50-249 emps

2019 2020 H1 21

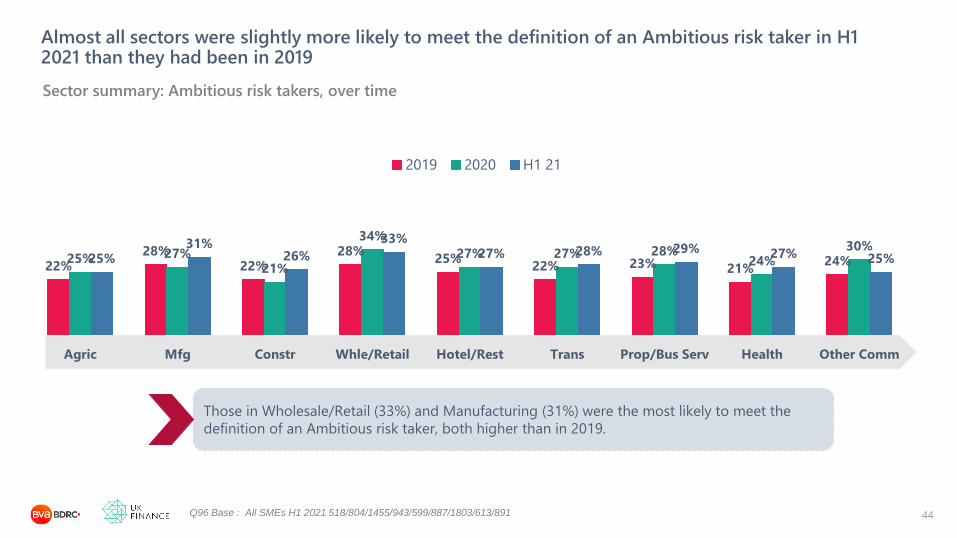

Almost all sectors were slightly more likely to meet the definition of an Ambitious risk taker in H1 2021 than they had been in 2019

44

Those in Wholesale/Retail (33%) and Manufacturing (31%) were the most likely to meet the

definition of an Ambitious risk taker, both higher than in 2019.

Sector summary: Ambitious risk takers, over time

Q96 Base : All SMEs H1 2021 518/804/1455/943/599/887/1803/613/891

22%28%

22%28%

25%22% 23% 21%

24%25% 27%21%

34%

27% 27% 28%24%

30%25%

31%26%

33%27% 28% 29% 27% 25%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

2019 2020 H1 21

42% 45% 43% 34% 32% 29% 29% 31% 34% 37% 38% 36%

H2 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

The proportion happy to borrow to grow increased during 2020 for all but the largest SMEs and has been broadly stable in 2021

45

Annual time series: Happy to borrow to grow

Q96 Base All SMEs Q2 2021 4252 865/1403/1318/664

50-249 emps

10-49 emps

1-9 emps

0 emps

All SMEs

44%

55%

44%

33%

57%

56%

49%

39%

The proportion of SMEs happy to borrow to grow improved during 2020 and has remained stable in

2021 and across all size bands. In H1 21, 49% of those in Transport were happy to borrow to grow,

compared to 29% in Health.

All sectors were at least slightly happier to borrow to grow in H1 2021 than in 2019, notably those in Transport

46

Half of those in Transport are happy to borrow to grow, with around 4 in 10 in most other

sectors, with the exception of Health (29%), Other Community (33%) and Property/Business

Services (34%)

Sector summary: Happy to borrow to grow, over time

Q96 Base : All SMEs H1 2021 518/804/1455/943/599/887/1803/613/891

34% 35%

27%

36%32% 30%

26% 27% 28%

39%

32%28%

42%38%

34%31%

27%33%

43%39% 37% 39% 40%

49%

34%29%

33%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

2019 2020 H1 21

16% 17% 21% 20% 28% 18% 16% 22%

39% 40%46% 47%

43%53% 53% 44%

24% 23% 16% 16% 11% 16% 17% 16%

21% 20%18% 16% 18%

17% 21% 21%

2015 2016 2017 2018 2019 2020 Q1 21 Q2 21

Appetite for finance increased slightly 2019-2020 as more SMEs who were not using finance said they were happy to borrow to grow. This was maintained into 2021 as more SMEs using finance said they were also happy to borrow to grow

Annual time series– use of, and appetite for, external finance

Base : All SMEs Q2 2021 4250

Previous analysis has shown that using finance is a good predictor of applying for more. The previous increase

in use of finance in 2019 saw more SMEs in the “using finance but not willing to borrow to grow” group (28%).

When use of finance increased again from the second half of 2020, this resulted in an increase in both those

also willing to borrow to grow to 21% and those not willing to 22%.

47

Using external finance and

happy to use to grow

Using external finance but

not happy to use to grow

Not using external finance

but happy to use to grow

Not using external finance and

not happy to use to grow

Use of external finance

48

44% 41% 37% 37% 37% 38% 36% 45% 32% 30% 40% 44% 42% 45%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

Overall use of finance was 45% in Q2 2021, boosted by increased use of bank loans and grants. Use was higher than in Q4 2020 for all SMEs except those with 50-249 employees

49

Annual time series: Currently using any external finance

Q15 all SMEs Q2 2021 4252 865/1403/1318/664

50-249 emps

10-49 emps

1-9 emps

0 emps

All SMEs

After a period of overall stability, use of external finance increased in 2019 to 45% but then dropped to 30-32% in the first

half of 2020 and across all sizes. Since then, increased use of loans and grants in particular has seen the overall proportion

increase to 45%, and across all but the largest size band

35%

65%

57%

37%

74%

70%

58%

38%

The struggling sectors, Hospitality and Transport, remained the most likely to be using finance overall, with no clear pattern by sector

50

There is no clear pattern by sector over time – In Q2 2021 a few sectors were less likely to be

using finance than in 2019, most were broadly in line and some were ahead

Sector summary: Use of external finance over time

Q15 Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

56%

44%48%

52%48% 46%

37%

56%

42%41%

28% 28%

41%

47%

36%

27%22%

25%

51%

43%39%

43%

60%57%

40% 38%42%

52%48%

43%

55% 55%

47%42%

32%

42%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

2019 Q2 20 Q4 20 Q2 21

44%41%

37% 37% 37% 38%36%

45%

32%30%

40%44%

42%45%

36%32%

29% 30% 30% 31% 32%

39%

26% 25%

32% 31% 32% 31%

18% 18% 17% 17% 16%18%

12%16%

14% 13%

21%

26% 25%27%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

As use of any external finance increased from Q3 2020, use of core finance was stable with more use being made of “other” forms of finance, typically a grant

51

Time series: Core and other financial products

Q15/ Base : All respondents Q2 2021 4250

Use of core finance dropped from 39% for 2019 as a whole to 25% in Q2 2020, but recovered

somewhat due to higher use of loans. Use of ‘other’ forms of finance was boosted by more use being

made of grants (from 4% in Q2 2020 to 16% in Q2 2021)

Use any external finance now OtherCore products

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

There has been a marked increase in use of loans/commercial mortgages since Q1 2020. Use of ‘other’ forms of finance was boosted by an increase in grants (from 4% to 16%)

52

Annual time series: Main forms of finance used

Q15 all SMEs Q2 2021 4250

Leasing/HP

Credit cards

Bank loan/Mtge

Overdraft

The proportion of SMEs using 2 or more forms of finance

fell from 17% in 2019 to 11% in Q2 2020, but recovered by

Q4 to 19% and 18% in Q2 21. Amongst those using any

finance, the proportion using 2 or more forms was 41% in

Q2 21, only slightly higher than the 38% reported in Q2 20

9%

9%

18%

9%

6%

18%

10%

22%

Use of finance 2019 Q2 20 Q4 20 Q2 21

No finance 55% 70% 56% 55%

1 product 28% 19% 25% 26%

2 or more products 17% 11% 19% 18%

44% 41% 37% 37% 37% 38% 36% 45% 32% 30% 40% 44% 42% 45%

34%40%

43%47% 47% 47% 48%

42%

51%

41% 39%

32%37% 38%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

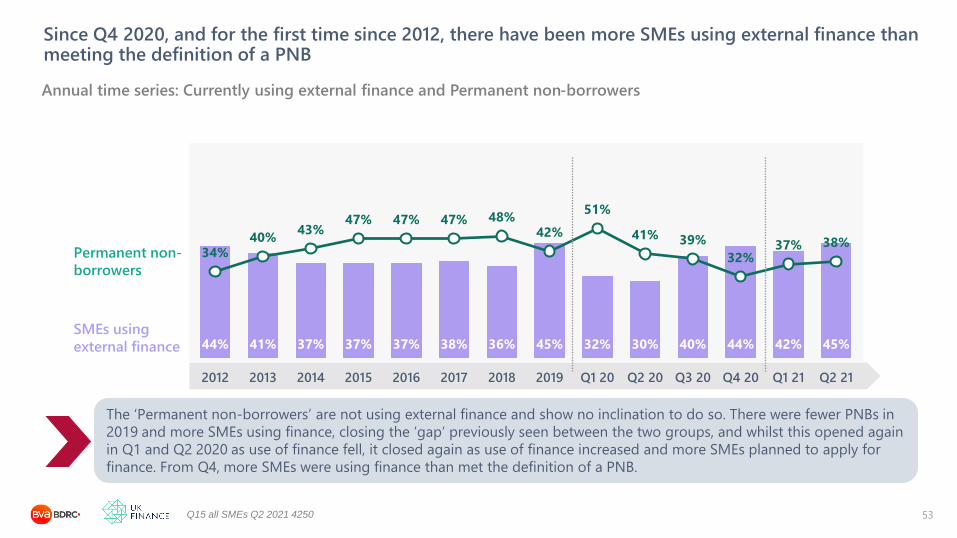

Since Q4 2020, and for the first time since 2012, there have been more SMEs using external finance than meeting the definition of a PNB

53

Annual time series: Currently using external finance and Permanent non-borrowers

Q15 all SMEs Q2 2021 4250

The ‘Permanent non-borrowers’ are not using external finance and show no inclination to do so. There were fewer PNBs in

2019 and more SMEs using finance, closing the ‘gap’ previously seen between the two groups, and whilst this opened again

in Q1 and Q2 2020 as use of finance fell, it closed again as use of finance increased and more SMEs planned to apply for

finance. From Q4, more SMEs were using finance than met the definition of a PNB.

Permanent non-

borrowers

SMEs using

external finance

55% 49% 49% 46% 49% 42% 50% 49% 57%

28%33% 36% 38% 37%

44%38%

32% 30%

2013 2014 2015 2016 2017 2018 2019 2020 Q2 21

35% 32% 32% 33% 34% 34% 43% 32% 41%

44% 48% 51% 50% 51% 50%44% 44% 41%

2013 2014 2015 2016 2017 2018 2019 2020 Q2 21

67%61% 60% 59%

64%54%

60% 58%65%

22% 26% 29% 30% 27%36%

31% 28% 24%

2013 2014 2015 2016 2017 2018 2019 2020 Q2 21

73%63% 61% 64%

73% 77% 77%

58%

35%17%

26% 28% 26% 22% 19% 19%

32%

51%

2013 2014 2015 2016 2017 2018 2019 2020 Q2 21

The relationship between PNBs and users of finance varied by size of SME. The largest SMEs have become more likely to meet the definition of a PNB

54

Annual time series: Currently using external finance and Permanent non-borrowers

Q15 all SMEs Q2 2021 4252 865/1403/1318/664

Permanent non-

borrowers

SMEs using

external finance0 emps 1-9 emps

10-49 emps 50-249 emps

All sectors, except Health and Property/Business Services, were more likely to be using finance in Q2 2021 than to meet the definition of a PNB

55

While those in Health are now much more likely to be a PNB than to use finance, the

opposite is true for those in Hospitality or Wholesale/Retail

Sector summary: Use finance and PNBs Q2 2021

Q84

Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

52% 48% 43% 55% 55% 47% 42% 32% 42%

35%39% 37%

30%25%

32%

45%

55%

34%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Use finance PNB

Alternative sources of funding

56

45%32% 30%

40% 44% 42% 45%

16%

19% 21%

18%17% 17%

17%

8%

10% 11%

15% 13% 14%14%

2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

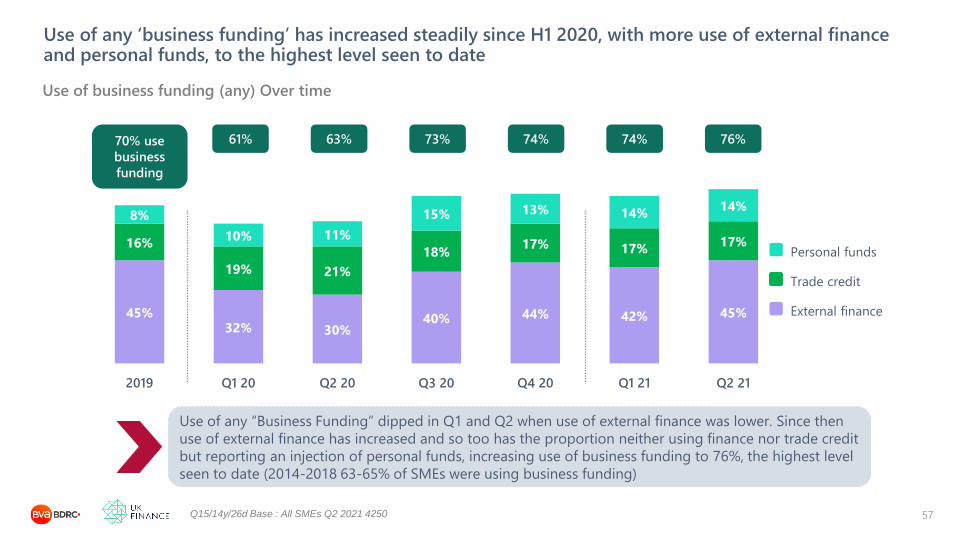

Use of any ‘business funding’ has increased steadily since H1 2020, with more use of external finance and personal funds, to the highest level seen to date

57

Use of business funding (any) Over time

Q15/14y/26d Base : All SMEs Q2 2021 4250

Personal funds

Trade credit

External finance

70% use

business

funding

Use of any “Business Funding” dipped in Q1 and Q2 when use of external finance was lower. Since then

use of external finance has increased and so too has the proportion neither using finance nor trade credit

but reporting an injection of personal funds, increasing use of business funding to 76%, the highest level

seen to date (2014-2018 63-65% of SMEs were using business funding)

61% 63% 73% 74% 74% 76%

45%

17%

14%

All SMEs

For the smallest SMEs, personal funds were as important as trade credit within their business funding mix, with larger SMEs more likely to be using trade credit

58

Use of business funding (any) Q2 2021

Q15/14y/26d Base : All SMEs Q2 2021 4252 865/1403/1318/664

Personal funds

Trade credit

External finance

76% use business

funding

41%

57%65%

35%

16%

20%

26%

27%

16%

7%

2%

0 Emp 1-9 emp 10-49 emp 50-249 emp

73% 84% 91% 64%

Business funding 0 emps 1-9 10-49 50-249

2019 67% 77% 84% 91%

2020 64% 78% 86% 87%

H1 2021 72% 82% 89% 69%

52% 48% 43%55% 55%

47% 42%32%

42%

11% 23%24%

24%13%

12% 17%

10%

13%

14%7% 11%

7%16%

17% 14%

23%

14%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

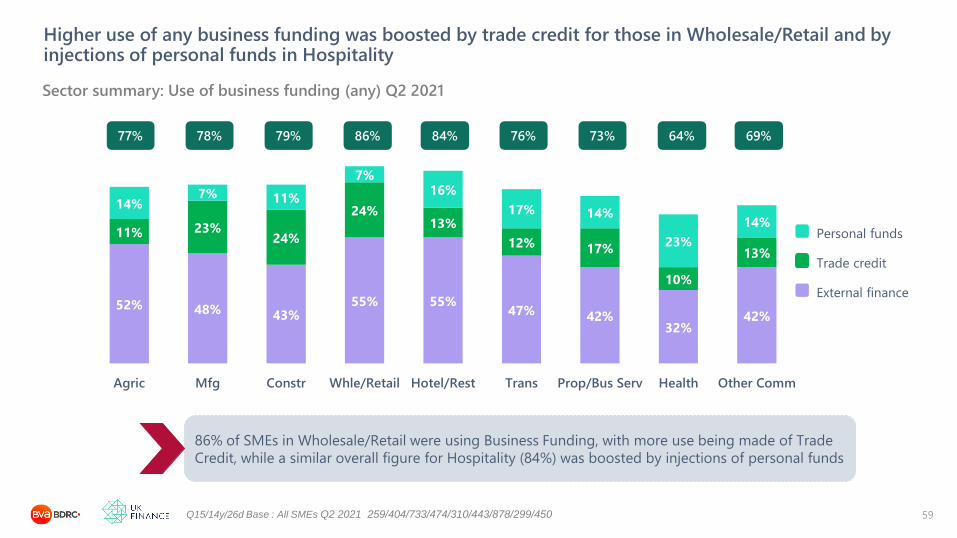

Higher use of any business funding was boosted by trade credit for those in Wholesale/Retail and by injections of personal funds in Hospitality

59

Sector summary: Use of business funding (any) Q2 2021

Q15/14y/26d Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

Personal funds

Trade credit

External finance

86% of SMEs in Wholesale/Retail were using Business Funding, with more use being made of Trade

Credit, while a similar overall figure for Hospitality (84%) was boosted by injections of personal funds

77% 78% 79% 86% 84% 76% 73% 64% 69%

4 in 10 SMEs had injected personal funds, back to levels seen in 2012-13, but with more SMEs having felt that they had to inject the funds (28%) rather than choosing to (12%)

60

Time series: Injections of personal funds in previous 12 months

Q15d2 Base : All respondents Q2 2021 4250

Any injection

of funds

Felt had to

inject funds

Chose to

inject funds17% 19%

14%

14%17% 16% 16%

13% 12%11% 15%

13%11% 12%

25%20%

15%

13%11%

13% 13%11% 12%

18%

23%25% 27% 28%

43%

38%

29%27% 28% 29% 29%

24% 24%

29%

38% 38% 38%40%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

Injections of personal funds Q2 2021:

• By size , 43% with 0 employees and 33% with 1-9 employees (both up from a quarter in Q2 2020), decreasing

by size to 6% with 50-249 employees

• By sector more likely in Hospitality and Transport (both 47%) or Health (45%), compared 33-42% elsewhere

31% 33% 33% 35% 34% 37% 36% 36% 37% 36% 36% 39%

2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 20 Q2 20

Use of any trade credit has increased very slightly, with a marked increase in use for those with 10-49 employees, but larger SMEs have become less likely to be using it.

61

Annual time series: Using trade credit

Q14 Base : All SMEs Q2 2021 4252 865/1403/1318/664

50-249 emps 58%

10-49 emps 58%

1-9 emps 45%

0 emps 26%

All SMEs

56%

81%

55%

33%

Using trade credit Q2 2021

• By size , from 3 in 10 of the 0 employee SMEs to 8 in 10 with 10-49 employees

• By sector it was used much more by those in Wholesale/Retail (61%), Construction (52%) and Manufacturing

(50%), compared to 15% in Health

16% 17% 20% 24% 22% 25% 23% 23% 23% 28% 29% 33% 35% 31%

10% 10%14%

17%14%

18%15% 16% 16%

19%22% 24% 26%

23%

32% 33%38%

41% 41%44% 42% 44% 42%

53%47%

56%60%

56%

66% 66% 68% 70% 72% 73% 75% 76%

67%

84%79%

83% 84% 86%

77%80% 82% 81% 82%

90% 91% 94% 89% 88% 88%93% 91% 95%

2012 2013 2014 2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

The proportion with £10,000 or more in credit balances increased to 35% at the start of 2021, but was slightly lower in Q2 as fewer of the smaller SMEs held such sums

62

Annual time series: £10k or more of credit balances held over time

Q117 Base : All SMEs excl DK Q2 2021 1812 429/664/473/246

50-249 emps

10-49 emps

1-9 emps

0 emps

All SMEs

Holding £10k+ of credit balances Q2 2021:

• By size, from 23% 0 employee SMEs to 95% with 50-249 employees

• By sector those in Wholesale/Retail were twice as likely to hold such sums (40%) as those in Health (20%)

36% 33% 33% 34%

47% 47%42% 45%

40%35%

26% 24%

40% 37% 35% 37%

20% 23%

46% 50% 52%61%

37% 33% 34%

15%26%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Personal funds £10k+ CB Trade credit

Between 6 and 8 in 10 in each sector used one or more of these additional forms of funding, with trade credit much more prevalent in certain sectors than others

63

Sector summary: Alternative funding Q2 2021

all SMEs Q2 2021 259/404/733/474/310/443/878/299/450

Use of any of these alternative forms of funding varied from 59% in Health to 81% in Wholesale/Retail with large

variations in the use of trade credit in particular.

71% 71% 74% 81% 71% 74% 70% 59% 62%

35%29%

51%

63%52%

All 0 emps 1-9 emps 10-49 emps 50-249 emps

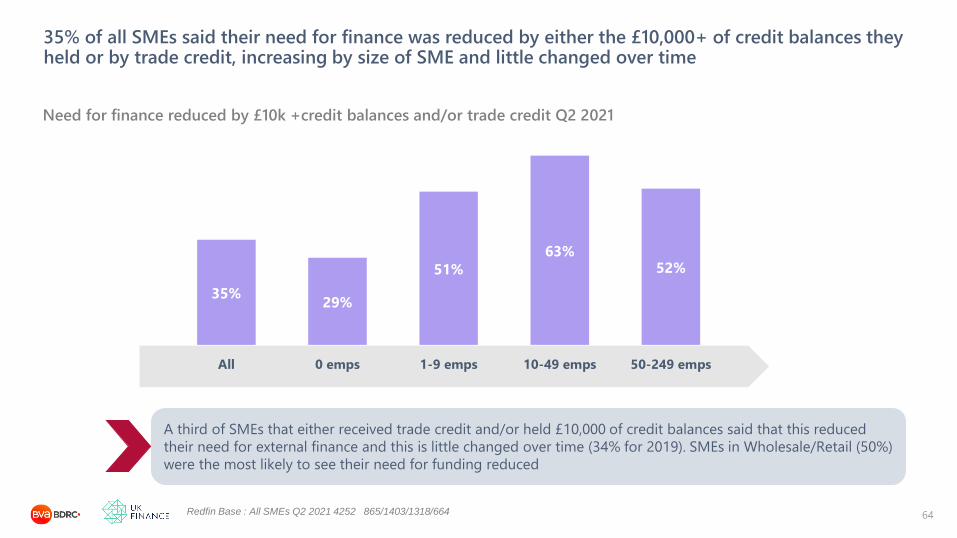

35% of all SMEs said their need for finance was reduced by either the £10,000+ of credit balances they held or by trade credit, increasing by size of SME and little changed over time

64

Need for finance reduced by £10k +credit balances and/or trade credit Q2 2021

Redfin Base : All SMEs Q2 2021 4252 865/1403/1318/664

A third of SMEs that either received trade credit and/or held £10,000 of credit balances said that this reduced

their need for external finance and this is little changed over time (34% for 2019). SMEs in Wholesale/Retail (50%)

were the most likely to see their need for funding reduced

34%

41% 42% 40%

51%

40%

30%27%

24% 24%

32%37%

43%38%

46%

34%

26%29%

20%25%

34% 36%39% 40%

50%

31%34% 33%

14%

20%

All Agric Mfg Constr W/Ret H/Rest Trans Prop/BS Health Other Com

2019 2020 H1 21

SMEs in Wholesale/Retail remained the most likely to say their need for finance was reduced by either the £10,000+ of credit balances or trade credit

65

The equivalent of a third of SMEs said their need for finance was reduced, little changed.

over time. Those in Hospitality have become somewhat less likely to say their need for

finance has been reduced, as have those in Health

Sector summary: Need for finance reduced by £10k +credit balances and/or trade credit over time

Q84 Base : All SMEs H1 2021 518/804/1455/943/599/887/1803/613/891

External funding -Key findings

66

Attitudinally SMEs remained somewhat self-reliant about finance, with two thirds feeling the future was

uncertain and hence caution was required. That said, the proportion happy to borrow to grow increased to

37% in H1 2021, somewhat higher than the 3 in 10 seen immediately prior to the pandemic. 1 in 5 SMEs were

both using finance and happy to borrow to grow, back to levels seen in 2015-16, while just over 1 in 4 met the

definition of an “Ambitious risk taker”, slightly higher than in 2019

Injections of personal funds into the business had also increased again, to 40% of SMEs, with the highest

proportion to date, 28%, feeling that they had to inject funds. A fairly stable third of SMEs had access to £10k

or more of credit balances and around 4 in 10 had access to trade credit (including 8 in 10 of those with 10-49

employees, who were also more likely to say that trade credit/credit balances reduced their need for external

finance)

45% of SMEs were using finance, back to levels seen in 2019, due to increased use of loans and grants in

particular. As a result there were more SMEs using finance than meeting the definition of a PNB (38% in Q2

2021), which was not typically the case pre-pandemic. There has been a decline in use of external finance

amongst the largest SMEs and they were less likely to be using any “business funding” than their peers, but

remained the most likely to hold £10,000 or more of credit balances

Today’s presentation

67

The trading context

External funding: attitudes to and use of, alongside alternatives

Demand for finance: need, applications and impact of Covid

The future: growth, barriers and future appetite for finance

The immediate impact of Covid 19

Need for finance increased during 2020 and again in the first half of 2021, for all but the largest SMEs

68

Had a need for external funding (whether applied or not) – over time

Q25 all SMEs Q2 2021 4252 865/1403/1318/664

From a very low base in 2019, need for finance increase markedly during 2020 and again in Q1

and Q2 of 2021, with little to choose between size of SME with the exception of the largest SMEs.

All sectors saw an increased need for finance in 2020 and there have been further increases in

2021, albeit not a consistent pattern across all sectors

3%2%

6%5%

3%

9%8%

10% 10%8%

15%14%

16%18%

9%

15%14%

18%

15%

7%

All 0 emps 1-9 emps 10-49 emps 50-249 emps

2019 2020 Q1 21 Q2 21

6%

2%3%

5%6%

2%3%

1%

5%

9%7%

6%8%

12%13%

9%7%

10%9%

17%

12% 12%

21%

25%

12%13%

17%15%

17%15% 15%

18%

13% 13%

10%

18%

Agric Mfg Constr W/Ret H/Rest Trans Prop/BS Health Other Com

2019 2020 Q1 21 Q2 21

All sectors have seen an increased need for funding since 2019, with further increases in 2021 although not to a consistent pattern across all sectors

69

Although still a minority of SMEs, all sectors saw an increased need for finance in 2020.

There have been further increases in 2021, albeit not a consistent pattern across all

sectors

Sector summary: Had a need for external funding (whether applied or not) – over time

Q24 Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

In H1 2021, there continued to be a focus on funding for cash flow and a greater role for the main bank, with limited evidence of self funding as 8 in 10 of those with a need made an application for funding

70

Behaviour in the 12 months prior to interview

Base varies, those who took no action excluded after each stage * from Q2 2020 this includes “Coping with impact of Covid 19”

Q2-4 20: 10%

81%*

24%

55%

38%

81%

67%

80%

65%

12%

Reported a funding need

To fund Cash flow

To fund Bus Devlpt

Spoke to bank/advisor

Spoke to main bank

Considered applying

To main bank

Applied

To main bank

Self funded element

2019: 3%

49%

58%

43%

18%

63%

37%

57%

29%

29%

2018: 4%

42%

58%

41%

21%

67%

48%

63%

40%

13%

Q1-2 21: 15%

85%*

19%

49%

28%

86%

70%

83%

66%

8%

78% 77%

Q39/57 Base : All Type 1a/b applications with a response 1232/1620/1652/1552/3033/3251/2935

Analysis by application period showed an increasing success rate for applications made during 2020 and 2021 to date

71

Global success rate: all applications reported from Q1 2018 to date, occurring in the 18 mth application periods shown

16% 18% 21%26%

14% 12% 12%

6% 5%5%

4%

2%1% 1%

1% 1%1%

2%

1%1% 1%

7% 6%6%

4%

3%3% 2%

70% 70% 67% 65%

80% 84% 85%

Q1 17-Q2 18 Q3 17-Q4 18 Q1 18-Q2 19 Q3 18-Q4 19 Q1 19-Q2 20 Q3 19-Q4 20 Q1 20-Q2 21

74% 71% 84%

Offered but declined

No facility

Offered what wanted and took it

Have facility after issues

Different product from provider

2790 applications reported as made in 2020 had a success rate of 89% For the 145

reported for 2021 to date the success rate was 78%

88% 88%

89%

Q39/57 Base : All Type 1a/b applications with a response 178/1961/116/35/21CARE RE SMALL BASE

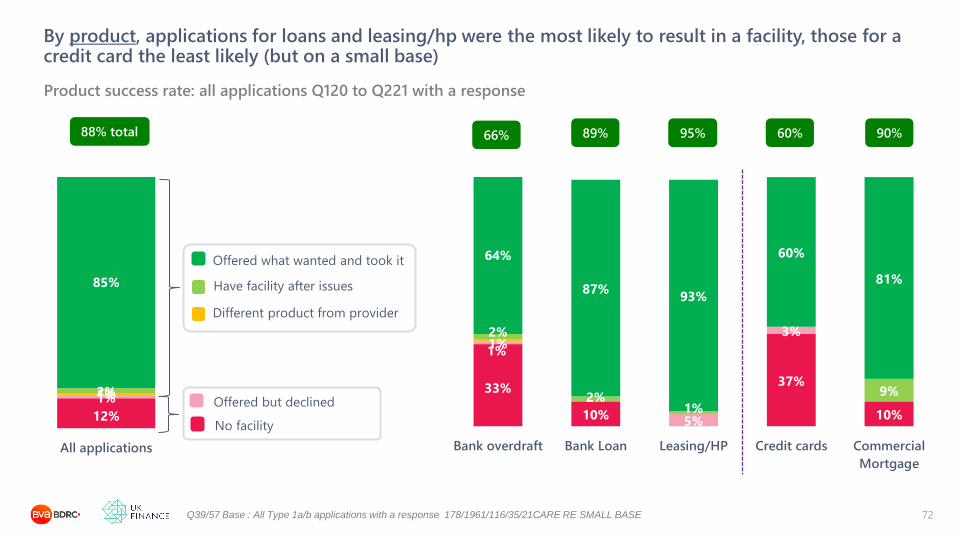

By product, applications for loans and leasing/hp were the most likely to result in a facility, those for a credit card the least likely (but on a small base)

72

Product success rate: all applications Q120 to Q221 with a response

33%

10%

37%

10%

1%

5%

3%

1%

2%

2%1%

9%

64%

87%93%

60%

81%

Bank overdraft Bank Loan Leasing/HP Credit cards Commercial

Mortgage

95% 60% 90%88% total

12%

1%1%2%

85%

All applications

Offered but declined

No facility

Offered what wanted and took it

Have facility after issues

Different product from provider

66%

77%

65%

99%

76%

61%

95%

73%

80%

88%

66%

89%

95%

Bank overdraft

Bank Loan

Leasing HP

Q117-Q218 Q118-Q219 Q119-Q220 Q1 20-Q221

Success rates for bank loans have increased markedly for more recent applications, those for leasing were broadly stable and those for overdrafts were now lower than for bank loans

73

Success rates for key products

Q39/57 Base : All Type 1a/b applications with a response Q120-Q221 178/1961/116

Around two thirds of applications for bank overdrafts were successful. Success rates for loans initially dipped

but recent applications have been much more likely to be successful (no doubt affected by the Government

backed lending schemes), moving them ahead of bank overdrafts and boosting the overall success rates.

80% 84% 83% 83% 85% 83% 84% 80% 77% 76% 78%

3%2% 2% 2% 1% 1% 1%

2% 3% 4% 3%

17% 13% 15% 14% 13% 15% 14% 18% 19% 20% 19%

2015 2016 2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

The increase in past borrowing events in 2020 has been maintained into 2021, albeit most SMEs met the definition of a Happy non-seeker.

74Pastfin Base : All SMEs Q2 2021 4250

Annual time series: Borrowing profile past

Looking back over the past 12 months, most SMEs have been “Happy non-seekers” of finance, as they

have in previous years, but that proportion has declined back to 2015 levels, as the proportion reporting

a borrowing event increased.

Had any event Would be seekers Happy non-seekers

SMEs with 1-9 or 10-49 employees were more likely to report a past borrowing event

75Pastfin Base : All SMEs Q2 2021 4250 865/1403/1318/664

Borrowing profile past by size of SME Q2 2021

Had any event Would be seekers Happy non-seekers

78% 79% 73% 74%88%

3% 3%3% 1%

19% 18% 24% 25%12%

All 0 emps 1-9 emps 10-49 emps 50-249 emps

17% 16% 14% 16% 15% 20% 23% 24% 22%

2017 2018 2019 Q1 20 Q2 20 Q3 20 Q4 20 Q1 20 Q2 20

By Q4 2020, almost a quarter of SMEs reported having had any appetite for finance in the previous 12 months and this was maintained into 2021, but with declining appetite for the largest SMEs.

76

Annual time series: Any appetite for finance in past 12 months (Borrowing event or Would-be seeker)

Q14 Base : All SMEs Q2 2021 4252 865/1403/1318/664

50-249 emps 26%

10-49 emps 25%

1-9 emps 22%

0 emps 16%

All SMEs

12%

26%27%

21%

75% 76% 76% 76% 77% 73% 79% 83% 82%

3% 4% 2% 2% 2% 4%3%

6% 3%22% 20% 22% 22% 21% 23% 17%

11% 15%

Agric Mfg Constr W/Ret H/Rest Trans Prop/BS Health Other Com

Past appetite for finance varied little by sector, with the exception of lower appetite amongst the Property/Business Services, Health and Other Community sectors

77Pastfin

Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

Borrowing profile past by sector Q2 2021

In all sectors the majority of SMEs met the definition of a ‘Happy non-seeker’ and there were

limited number of ‘Would-be seekers’ who felt something had stopped them from applying

Had any event Would be seekers Happy non-seekers

Pandemic related funding

78

In Q2 2021, almost half of SMEs were aware of either Pay as you Grow and/or the Recovery Loan Scheme

79AW1 All SMEs Q2 2021 4252 865/1403/1318/664

Awareness of new schemes – Q2 2021

33%

32%

45%

Pay as you grow

Recovery Loan

scheme

Aware of either

Q2 Initial awareness of the new schemes was high

compared to other initiatives previously tested and

increased with size:

Aware of

either

0

emps

1-9

emps

10-49

emps

50-249

emps

Q2 2021 44% 47% 49% 55%

In Q2 2021:

• Awareness by sector ranged from 55% in the

Hospitality sector to 37% in Construction

• It was slightly higher for those using any finance

(50% v 41% not using)

• 58% of those with a government backed facility

themselves were aware (46% of PAYG and 37%

of the Recovery Loan)

As the availability of some Government backed schemes ended, the proportion of SMEs that had applied for pandemic related funding was stable in H1 2021

80BB1 All SMEs Q2 2021 4252 865/1403/1318/664

Specific approaches re funding for pandemic impact lending – over time

11%

3%

12%

74%

18%

2%

6%

74%

21%

2%

4%

74%

18%

2%

4%

76%

18%

1%

3%

78%

Approached main bank about

finance

Approached another finance

provider

Not approached but considering

No plans to approach

Q2 20

Q3 20

Q4 20

Q1 21

Q2 21

Most SMEs approached their main bank for funding.

The proportion making any approach increased from

14% in Q2 to 23% in Q4 2020 and was 19% in Q2 2021:

Any

approach

0

emps

1-9

emps

10-49

emps

50-249

emps

Q2 2020* 12% 21% 27% 21%

Q4 2020 20% 31% 30% 15%

Q2 2021 16% 29% 35% 15%

In H2 2020, 13% of those who had not reported a

borrowing event earlier went on to say they had

approached a provider for Covid related funding, and

the proportion was similar in H1 2021 (12%). This

would boost the proportion of all SMEs with any

borrowing event to 29% in both periods.

17% 17% 17%

25% 25%28%

19% 17% 16%17% 18% 19%

28%

40%

29%24%

13%

20%

13%18% 18%

28%

35%31%

16%13%

16%19%

24%19% 21%

27% 26%

20%

9% 11%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q3 20 Q4 20 Q1 21 Q2 21

SMEs in the Hospitality and Transport sectors were the most likely to have approached a lender for pandemic related finance

81

Sector summary: Pandemic impact lending– Any approach from Q3 2020 to Q2 2021

BB1 all SMEs Q2 2021 259/404/733/474/310/443/878/299/450

SMEs in the Hospitality and Transport remained more likely to have made an

approach for Covid related funding, with increased mention of applications in Q2

2021 from those in Manufacturing

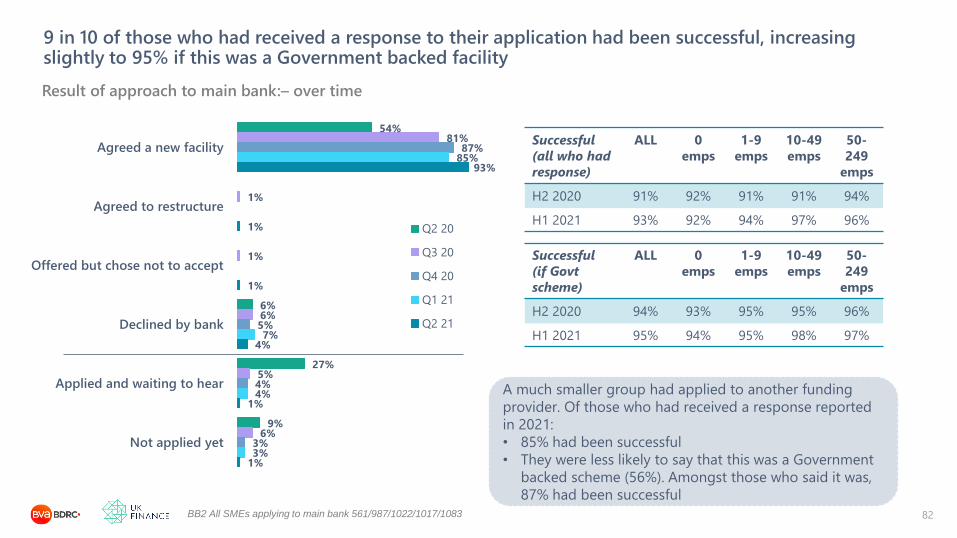

9 in 10 of those who had received a response to their application had been successful, increasing slightly to 95% if this was a Government backed facility

82BB2 All SMEs applying to main bank 561/987/1022/1017/1083

Result of approach to main bank:– over time

54%

6%

27%

9%

81%

1%

1%

6%

5%

6%

87%

5%

4%

3%

85%

7%

4%

3%

93%

1%

1%

4%

1%

1%

Agreed a new facility

Agreed to restructure

Offered but chose not to accept

Declined by bank

Applied and waiting to hear

Not applied yet

Q2 20

Q3 20

Q4 20

Q1 21

Q2 21

A much smaller group had applied to another funding

provider. Of those who had received a response reported

in 2021:

• 85% had been successful

• They were less likely to say that this was a Government

backed scheme (56%). Amongst those who said it was,

87% had been successful

Successful

(all who had

response)

ALL 0

emps

1-9

emps

10-49

emps

50-

249

emps

H2 2020 91% 92% 91% 91% 94%

H1 2021 93% 92% 94% 97% 96%

Successful

(if Govt

scheme)

ALL 0

emps

1-9

emps

10-49

emps

50-

249

emps

H2 2020 94% 93% 95% 95% 96%

H1 2021 95% 94% 95% 98% 97%

45% of successful applicants said that most or all of the funds they received had been spent

83BB2b All SMEs applying to main bank and getting facility 428/890/928/1035

How much of facility has been spent– all who were successful at main bank over time

Around 4 in 10 SMEs have spent all or most of

the funding they received and this remained

more likely to be the case for smaller SMEs:

23%

18%

17%

7%

13%

19%

4%

20%

15%

15%

12%

13%

24%

2%

22%

21%

14%

10%

11%

21%

31%

14%

20%

7%

7%

22%

All of it has been spent

Most of it

Half of it

A quarter of it

Very little

None of it has been spent

Not received yet

Q3 20

Q4 20

Q1 21

Q2 21

All/most

spent

0

emps

1-9

emps

10-49

emps

50-249

emps

Q3 2020 46% 35% 25% 21%

Q4 2020 35% 36% 23% 28%

Q1 2021 51% 32% 30% 36%

Q2 2021 48% 40% 39% 32%

Whilst those in Hospitality have struggled

more with the pandemic, 35% had spent all or

most of the funding obtained, compared to

60% in Agriculture sector and 53% in Transport

40% 42%38%

44%

30%

41%

25% 24%

52%60%

47% 49%43%

35%

53%

33%

46% 49%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

H2 20 H1 21

In H1 2021, SMEs with funding in Agriculture and Transport were more likely than other sectors to have spent all or most of the funding received

84

Sector summary: Spent all or most of funding received from main bank H2 2020 and H1 2021

BB2b all SMEs asked question H1 21 109/186/361/210/200/245/367/84/201

Whilst those in Hospitality have struggled more with the pandemic, and were

somewhat more likely to have sought funding, they were less likely than their peers to

have spent all or most of the funding obtained

The impact of the pandemic on external funding

85

21%

Q14b All SMEs Q2 2021 4250 865/1403/1318/664

A fifth of SMEs were using more finance than pre-pandemic , with 1 in 10 now borrowing where they weren’t before

86

Change in use of external finance – all SMEs Q2 2021

66%71%

53%40%

57%

2%1%

2%

2%

11%10%

13%

22%

14%

3% 2%

4% 7%

14%

7% 5%

12% 18%

14%11% 10% 17% 11%

All 0 emps 1-9 emp 10-49 emps 50-249 emps

17% 33%

Using less finance

No funding/Grants/DK

Taken on extra finance

Same facilities used more

Same amount of finance

1 in 5 of all SMEs are making more use of finance than they were pre-

pandemic (6 in 10 of those using any external finance) including 1 in

10 using finance for the first time: such SMEs are typically smaller,

younger, more likely to be in a poor mood about their business and 3

in 10 are worried about how they will repay their borrowing.

36% 28%

Started borrowing

12% of all SMEs are borrowing more than

£25,000, increasing by size of SME from

7% to 43% of those with 10-49 emps. This

is twice the level reported in H1 2020 (6%)

19%

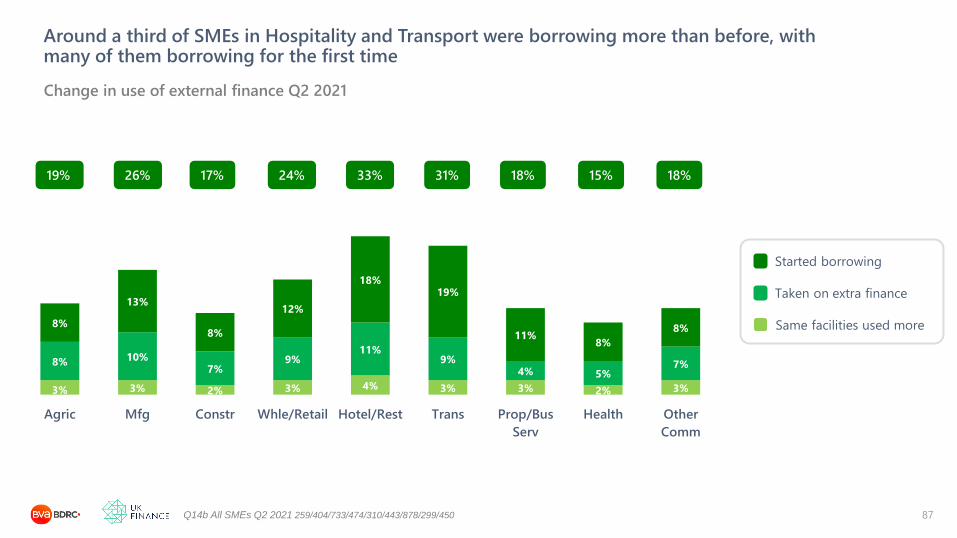

Q14b All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

Around a third of SMEs in Hospitality and Transport were borrowing more than before, with many of them borrowing for the first time

87

Change in use of external finance Q2 2021

3% 3% 2% 3% 4% 3% 3% 2% 3%

8% 10%7%

9%11%

9%4% 5%

7%

8%

13%

8%

12%

18%19%

11%8%

8%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus

Serv

Health Other

Comm

26% 17%

Taken on extra finance

Same facilities used more

24% 33%

Started borrowing

31% 18% 15% 18%

Those using any form of finance were twice as likely to have spoken to their bank about pandemic funding, increasing to 7 in 10 of those who were borrowing where they weren’t before. In almost all instances this approach was for a Government backed scheme and was successful

88BB1 All SMEs using finance Q2 2021 2041 485/522/248/690

Specific approaches re funding for pandemic impact lending – by use of finance Q2 2021

78%

52%

29% 32%

70%

83%

3%

4%

4%6%

5%19%

44%

68% 62%

30%

13%

All All using finance New borrowers Extra borrowing More use of facilities Similar to before

Any approach

Considered

No plans to approach

Almost all approaches were to the main bank and in 99% of cases this was for Government backed

borrowing. 96% of applications were successful (including for first time borrowers)

18%13%

25%31%

40%

19%10%

29%

49% 46%

28%19%

43%

60% 62%

28%17%

48%

63%72%

All 0 emps 1-9 emps 10-49 emps 50-249 emps

Q1 20 Q2 20 Q4 20 Q2 21

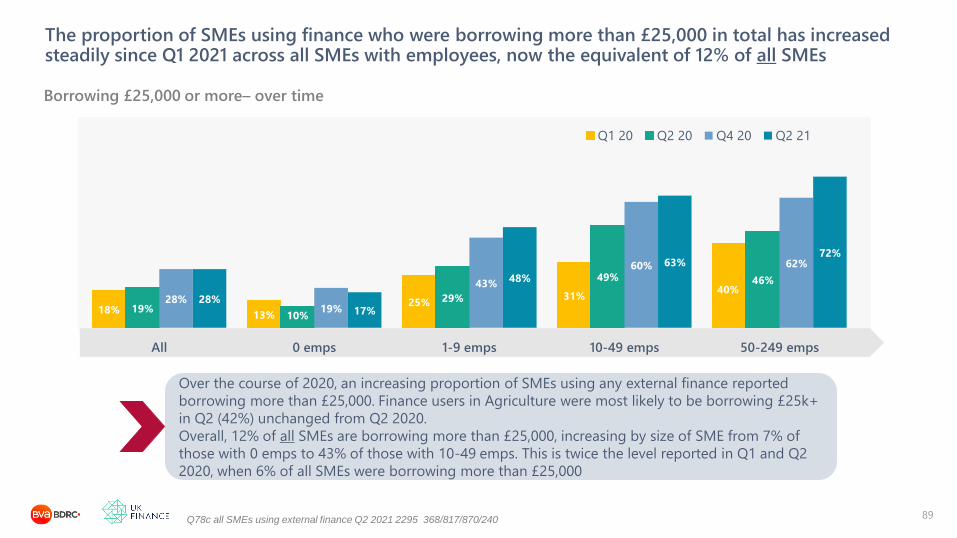

The proportion of SMEs using finance who were borrowing more than £25,000 in total has increased steadily since Q1 2021 across all SMEs with employees, now the equivalent of 12% of all SMEs

89

Borrowing £25,000 or more– over time

Q78c all SMEs using external finance Q2 2021 2295 368/817/870/240

Over the course of 2020, an increasing proportion of SMEs using any external finance reported

borrowing more than £25,000. Finance users in Agriculture were most likely to be borrowing £25k+

in Q2 (42%) unchanged from Q2 2020.

Overall, 12% of all SMEs are borrowing more than £25,000, increasing by size of SME from 7% of

those with 0 emps to 43% of those with 10-49 emps. This is twice the level reported in Q1 and Q2

2020, when 6% of all SMEs were borrowing more than £25,000

26%17% 10%

27%

27%18% 18%

28%

13%

45%

18% 17% 20%

34%23%

15% 10% 12%

43%

24%29%

36%

49%

28% 27%16% 16%

42%

28%19%

37% 35% 37%27%

10%20%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q1 20 Q2 20 Q4 20 Q2 21

There was no consistent pattern by sector in the proportion of SMEs using finance who were borrowing more than £25,000 in total

90

Borrowing £25,000 or more– over time

Q78c all SMEs using external finance Q2 2021 161/218/415/259/179/254/429/128/252

As with use of external finance, there is no consistent pattern by sector – Construction and

Hospitality have seen a reduction in the proportion borrowing more than £25,000 between Q4 2020

and Q2 2021, while there has been a steady increase for those in Transport

14% 14% 15% 8%4%

29% 30% 30% 27%19%

24% 24% 25%16% 10%16% 17% 16% 9% 9%

All 0 emps 1-9 emps 10-49 emps 50-249 emps

Q1 20 Q2 20 Q4 20 Q2 21

The proportion of SMEs using finance who were concerned about their ability to repay doubled between Q1 and Q2 2020, but has declined again since, to the equivalent of 7% of all SMEs

91

Concerned about ability to repay finance over next 12 months – over time

Q78c all SMEs using external finance Q2 2021 2295 368/817/870/240

After a sharp increase in concern between Q1 and Q2 2020, levels of concern about ability to repay

have declined and in Q2 2021 were only slightly higher than they were in Q1 2020. In Q2, 28% in

Manufacturing using finance were concerned about their ability to repay, compared to 8% in

Construction, 9% in the Other Community sector and15-25% of other sectors.

This is the equivalent of 7% of all SMEs being concerned about their ability to repay, down from

10% in Q4 2020 but still higher than the 4% who were concerned in Q1 2020

21%

8% 8%20%

25%

11% 9% 14%

27%25% 26%

39%

22%

44%

29%25% 22% 24%

15% 16% 18% 15%

40%

27%

10%

25% 25%22%28%

8%19%

25% 22%15% 16%

9%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Q1 20 Q2 20 Q4 20 Q2 21

Compared to Q1 2020, users of finance in Manufacturing were more concerned about their ability to repay, as were those in Transport

92

Sector summary: Concerned about ability to repay finance over next 12 months – over time

Q78c all SMEs using external finance Q2 2021 161/218/415/259/179/254/429/128/252

Users of finance showed no clear pattern by sector in being concerned about their ability to repay. Taking Q1

2020 as a benchmark for Q2 2021, those in Manufacturing were more concerned than before (and the most

concerned sector), as were those in Transport and to a lesser extent Property/Business Services. By contrast,

those in the Other Community sector were now much less concerned than before.

When first asked in Q4 2020, 3 in 10 SMEs were worried about whether they had enough funding in place for their business. In Q2 2021 the proportion was lower at 2 in 10

93

Those already using external finance were more concerned about whether they had enough funding in place (27%) than

those who are not currently using external funding (19%). Levels of concern for both groups declined by size of SME.

Concern was highest in the Hospitality and Transport sectors plus the Other Community sector, and notably for those

who were already using external finance. 30% of those borrowing for the first time or who had taken on extra

borrowing were also concerned

Agree that worried will have enough funding in place to fund the business in next 6 months

Q96 Base : All SMEs Q2 2021 4252 865/1403/1318/664

30% 30% 30%

22%

14%

28% 29%27%

19%

8%

22%24%

20%

13%

8%

All SMEs 0 emps 1-9 emps 10-49 emps 50-249 emps

Q4 20 Q1 21 Q2 21

Those already using finance remained more likely to be worried that they had enough funding than those not currently using finance, but at lower levels than in Q4 (when 38% were concerned)

94

Those already using external finance were more concerned about whether they had enough funding in place (27%) than

those who are not currently using external funding (19%) with levels of concern declining by size of SME.

Finance users in the Transport, Hospitality and the Other Community sectors remained more concerned about whether

they had enough funding, but at lower levels than in Q4 2020. Amongst SMEs in Hospitality or Construction there was

no difference in levels of concern by whether they were using finance or not.

Agree that worried will have enough funding in place to fund the business in next 6 months: Q2 2021

Q96 Base : All SMEs Q2 2021 4252 865/1403/1318/664

22% 24% 20% 13% 8%

27%29%

23%

14%10%

19% 20%17%

11%

7%

All SMEs 0 emps 1-9 emps 10-49 emps 50-249 emps

Worried Use finance No finance

A third of SMEs in the Transport sector currently using finance were worried about whether they have enough funding in place (but down from half in Q4 2020)

95

Finance users in the Transport, Hospitality and the Other Community sectors remained more

concerned about whether they had enough funding, but at lower levels than in Q4 when half of

them were concerned. There was no difference in levels of concern amongst SMEs in Hospitality or

Construction by whether they were using finance or not.

Agree that worried will have enough funding in place to fund the business going forward – Q2 2021

Q96 Base : All SMEs Q2 2021 259/404/733/474/310/443/878/299/450

16% 24% 23% 24% 29% 25% 21% 18% 23%

19%

28%24%

27%30%

33%

24%27%

31%

12%

20% 22% 21%

27%

18% 19%

14%16%

Agric Mfg Constr Whle/Retail Hotel/Rest Trans Prop/Bus Serv Health Other Comm

Worried Use finance No finance

Across all lending, 1 in 10 SMEs expressed concern about being able to meet repayments. Half had already spoken, or planned to speak, to their lender