Q2 2015 Investor Presentation - DRAFT 20150820 v2 Q2 2015 Group revenue of $408.1m (Q2 2014:...

20

www.kcadeutag.com KCA Deutag is a leading international drilling and engineering company working onshore and offshore with a focus on safety, quality and operational performance Second Quarter 2015 Investor Presentation

Transcript of Q2 2015 Investor Presentation - DRAFT 20150820 v2 Q2 2015 Group revenue of $408.1m (Q2 2014:...

www.kcadeutag.com

KCA Deutag is a leading international drilling and engineering

company working onshore and offshore with a focus on safety,

quality and operational performance

Second Quarter 2015

Investor Presentation

Disclaimer

1

The distribution of this presentation in certain jurisdictions may be restricted by law. Persons into whose possession this presentation comes are required to inform themselves about and to observe any such restrictions.

This presentation contains forward-looking statements concerning KCA Deutag. These forward-looking statements are based on management’s current expectations, estimates and projections. They are subject to a number of assumptions and involve known and unknown risks, uncertainties and other factors that may cause actual results and developments to differ materially from any future results and developments expressed or implied by such forward-looking statements. KCA DEUTAG has no obligation to periodically update or release any revisions to the forward-looking statements contained in this presentation to reflect events or circumstances after the date of this presentation.

2

1 Q2 Key Highlights

2 Business Update

3 Business Unit Financials

4 Group Results

5 Summary

Agenda

Q2 Key highlights

KCA Deutag is a leading international drilling and engineering company working onshore and offshore with a focus on safety, quality and operational performance

1

2015 YTD Group revenue and EBITDA of $874.3m (Q2 2014 YTD: $1,054.7m) and $141.3m (Q2 2014 YTD: $169.8m) respectively.Q2 2015 Group revenue of $408.1m (Q2 2014: $540.9m) and Q2 2015 EBITDA of $65.2m (Q2 2014: $89.0m) respectively

2Contract backlog of $7.6bn (at 1 August 2015) across a blue chip customer base

3A further new build rig spudded ahead of schedule in Russia on 16 April.Three remaining new build rigs in Oman and Brunei remain on track for delivery in 2015 completing our new rig delivery programme

4$50m of committed funding from KCAD Holdings I limited shareholders still available for draw down if required

5

Cost reduction programme continues to deliver an ongoing benefit to EBITDA with further initiatives to improve efficiency and reduce costs being implemented

3

Business update

4

Bentec Platform services RDS

1 LTM EBITDA, % split of total including MODUs, before corporate costs/ other of $38.4m.Note: MODUs LTM EBITDA $22.1m represented 6.8% of total EBITDA before corporate costs.

Integrated land drilling Integrated land drilling Offshore drilling services & designOffshore drilling services & design

• No further change to Platforms portfolio activity since Q1

• A slight increase in activity in Norway equipment rental business, but still below previous results

• Reduced capex spend by oil majors continues to impact activity

• Significant reductions in headcount implemented to counteract the reduced revenue levels

• Strong H1 backlog continues from previous orders

• Good capacity usage for 2015

• Tendering activity continuing to secure 2016 capacity

• International markets much less volatile than US, however certain markets have been more heavily impacted

• Continuing strong activity in Middle East, Russia and Algeria

• Lower activity in Nigeria and Europe where utilisation is very soft

$140.7m / 43.3% of total¹ $40.0m / 12.3% of total¹ $94.0m / 28.9% of total¹ $27.8m / 8.6% of total¹

Land drilling Bentec

Cost saving initiatives continue

5

1. A drive to reduce staff costs and discretionary spending which has delivered significant savings

a) Salary reduction and salary freezes across the business

b) c.250 redundancies worldwide in overhead positions

c) Significant reduction in discretionary spending

2. Reducing costs in supply chain delivered through a companywide initiative across all operations and business units

3. Significant senior management focus on working capital and the full delivery of the various cost reduction initiatives

a) Bi-weekly 13 week cash forecasting process

b) Monthly BU review meetings with KPI & forecasting updates

Houston

Ben Loyaljack-up rig

Baku

London

Stavanger

Bad Bentheim

Tyumen

Nizwa

Ben Rinnesjack-up rig

St. Johns

Bergen

Dubai

Land Drilling Platform Services RDS offices MODUs BentecRegional offices

A diversified portfolio of assets

Aberdeen (HQ)

Map excludes work over land rigs, defined as being below 900HP.

PRESENCE IN KEY AREAS

North Sea /Norway27 Plat.

Europe & Caspian7 Rigs

7 CaspianPlat.

Russia17 Rigs

Middle East

14 Rigs

Angola3 Plat.

Africa14 Rigs

RussiaSakhalin3 Plat.

Brunei 1 Rig

Myanmar1 Plat.

127

56 5141

16

0

30

60

90

120

150

Europe NorthAfrica

MiddleEast

North Sea Russia

Ye

ars

LTM Q2 2015 EBITDA split by region

6

7

IADC industry average 0.752 for 2014

1Total Recordable Incident Rate per 200,000 man hours. This is a rolling 12 month average.2 KCAD Total Recordable Incident Rate is directly comparable with IADC’s Total Recordables (RCRD) statistic. Note: IADC stands for International Association of Drilling Contractors.

• Sustained progress made on improving TRIR performance, which is well below IADC industry average

• Maintaining good annual safety performance

Health, safety and environmental performance

KCAD TRIR at end of Q2 2015 was 0.321 injuries per 200,000 man hours worked

8

Despite market environment, backlog remains strong

NB: Backlog figures exclude revenue generated in the year to date.

Total contract backlog as at 1 May 2015

Contract backlog by BU as at 1 May 2015

$M $M

Total contract backlog as at 1 August 2015

Contract backlog by BU as at 1 August 2015

9

• Lower revenues and EBITDA compared to Q2 2014 and Q1 2015

• Successfully delivered and spudded a new build rig in Russia

• Our operations in Russia, Algeria and Oman continue to enjoy high levels of utilisation and EBITDA

• Our European, Nigerian and Kurdistan businesses continue to see weakening utilisation, largely due to the wider market environment

• Overall our utilisation for the quarter was 74%, in line with the prior quarter

Financial Performance to 30 June 2015

Land Drilling

1 EBITDA is shown before and after allocation of central support costs (such as HR, Supply Chain and IT costs) to the operational business segments. 2014 and 2015 are presented on the same basis.

Q2 2015 Q2 2014 Q2 2015 Q2 2014

Result Result YTD YTD

$m $m $m % $m $m $m %

Revenue 157.5 188.9 (31.4) -16.6% 304.2 356.9 (52.7) -14.8%

EBITDA

pre support allocation 36.6 48.4 (11.8) -24.4% 77.0 86.9 (9.9) -11.4%

Support cost allocation (2.0) (2.8) 0.8 -29.8% (4.5) (5.6) 1.1 -18.8%

EBITDA

post support allocation 34.6 45.6 (11.0) -24.1% 72.4 81.3 (8.9) -10.9%

margin 22.0% 24.1% 23.8% 22.8%

Variance Variance

Bentec

10

• Revenues and EBITDA lower than Q2 2014

• Bentec maintains a reasonable backlog which will ensure that the business has a good level of utilisation through to the end of the year

• Currently in final stages of completion of 7 rigs for a client in Algeria and 3 rigs for KCAD in Oman and Brunei

• Now ramping up the work on the 3 rigs for a customer in Russia and 1 rig for a customer in Azerbaijan

• Tendering activity ongoing to secure order backlog for 2016

Financial Performance to 30 June 2015

1 EBITDA is shown before and after allocation of central support costs (such as HR, Supply Chain and IT costs) to the operational business segments. EBITDA is also shown before eliminations. 2014 and 2015 are presented on the same basis.

Q2 2015 Q2 2014 Q2 2015 Q2 2014

Result Result YTD YTD

$m $m $m % $m $m $m %

Revenue 50.2 63.7 (13.5) -21.2% 140.5 90.0 50.5 56.1%

EBITDA

pre support allocation 4.7 6.9 (2.3) -32.9% 16.0 7.8 8.2 NM

Support cost allocation (0.5) (0.7) 0.3 -37.0% (1.0) (1.4) 0.4 -31.4%

EBITDA

post support allocation 4.2 6.2 (2.0) -32.4% 15.0 6.4 8.6 NM

margin 8.4% 9.8% 10.7% 7.1%

Variance Variance

Platform Services

11

Financial Performance to 30 June 2015

• Continued good performance given current market conditions

• Our Angola, Myanmar and Canada operations experienced flat activity quarter on quarter, whereas Azerbaijan and Sakhalin saw lower EBITDA due to currency devaluation and the impact of client contract adjustments

• Our Norway business saw a small improvement on Q1 2015 due to stronger equipment rental activity

1 EBITDA is shown before and after allocation of central support costs (such as HR, Supply Chain and IT costs) to the operational business segments. 2014 and 2015 are presented on the same basis.

Q2 2015 Q2 2014 Q2 2015 Q2 2014

Result Result YTD YTD

$m $m $m % $m $m $m %

Revenue 172.2 208.2 (36.0) -17.3% 362.0 396.9 (34.9) -8.8%

EBITDA

pre support allocation 21.3 25.7 (4.4) -17.1% 45.8 50.8 (5.0) -9.8%

Support cost allocation (1.4) (2.0) 0.6 -28.9% (3.2) (3.9) 0.7 -17.6%

EBITDA

post support allocation 19.9 23.7 (3.8) -16.1% 42.6 46.9 (4.3) -9.2%

margin 11.6% 11.4% 11.8% 11.8%

Variance Variance

RDS

12

Financial Performance to 30 June 2015

• Activity levels significantly reduced, primarily due to a lack of opportunities for Greenfield projects

• We continue to reduce costs in this business as projects reduce in size

• Brownfield activity is more resilient, however projects tend to be smaller and we are seeing increased pressure on prices

1 EBITDA is shown before and after allocation of central support costs (such as HR, Supply Chain and IT costs) to the operational business segments. 2014 and 2015 are presented on the same basis.

Q2 2015 Q2 2014 Q2 2015 Q2 2014

Result Result YTD YTD

$m $m $m % $m $m $m %

Revenue 39.6 82.8 (43.2) -52.2% 99.2 178.8 (79.6) -44.5%

EBITDA

pre support allocation 5.1 15.1 (10.0) -66.1% 14.0 32.8 (18.8) -57.3%

Support cost allocation (0.5) (0.7) 0.2 -29.3% (1.1) (1.4) 0.3 -19.4%

EBITDA

post support allocation 4.6 14.4 (9.8) -68.0% 12.9 31.4 (18.5) -59.0%

margin 11.6% 17.4% 13.0% 17.6%

Variance Variance

MODUs

13

• Improved performance over Q1 2015 when the Ben Loyal jack up rig experienced damage to one of its legs and was therefore off day rate for a period. The rig was back to work in April and is currently working under a short-term contract extension at a reduced day rate

• The Ben Rinnes continues to operate offshore Angola

• The self-erecting tender barges, which were sold in Q4 2014, contributed $7.5m of the EBITDA before support allocation during H1 2014

Financial Performance to 30 June 2015

1 EBITDA is shown before and after allocation of central support costs (such as HR, Supply Chain and IT costs) to the operational business segments. 2014 and 2015 are presented on the same basis.

Q2 2015 Q2 2014 Q2 2015 Q2 2014

Result Result YTD YTD

$m $m $m % $m $m $m %

Revenue 22.4 35.6 (13.2) -37.1% 43.6 76.3 (32.7) -42.9%

EBITDA

pre support allocation 7.5 5.4 2.1 40.1% 13.0 18.0 (4.9) -27.5%

Support cost allocation (0.3) (0.5) 0.2 -42.9% (0.7) (1.0) 0.4 -35.1%

EBITDA

post support allocation 7.2 4.8 2.4 49.1% 12.3 16.9 (4.6) -27.0%

margin 32.1% 13.6% 28.3% 22.2%

Variance Variance

Group ResultsFinancial Performance to 30 June 2015

14

Revenue and EBITDA ($m) Q2 2015$m

Q2 2014$m

2015 YTD$m

2014YTD$m

Revenue from business units 442.1 579.1 949.8 1,099.2

Eliminations (34.0) (38.2) (75.5) (44.5)

Total revenue 408.1 540.9 874.3 1,054.7

EBITDA from business units 70.5 94.7 155.2 182.8

Eliminations (0.1) (1.1) (1.3) (1.1)

Corporate costs/other (4.4) (5.5) (9.9) (11.8)

Exchange (0.8) 0.9 (2.7) (0.1)

Total EBITDA 65.2 89.0 141.3 169.8

Q2 2015 Q2 2014 2015 YTD 2014 YTD

$'m $'m $'m $'m

Cash flow from operating activities 84.4 42.1 150.1 123.8

Capital expenditure (24.5) (61.1) (80.4) (83.5)

Proceeds from sale of Fixed Assets 2.2 0.5 3.1 3.7

Interest received 4.6 0.4 8.4 0.4

Other (3.5) (2.4) 2.7 (0.7)

Acquisition of non-controlling interests 0.0 0.0 (25.0) 0.0

Cash flow from investing activities (21.2) (62.6) (91.2) (80.1)

Interest paid (49.6) (50.1) (62.5) (54.1)

Foreign exchange (10.2) (4.9) (4.5) (5.9)

Net Cash flow before debt

drawdown/(repayment)3.4 (75.5) (8.1) (16.3)

Drawdown/(repayment) of debt and debt

issuance costs(4.6) (81.2) (16.5) (82.8)

Net cash flow (1.2) (156.7) (24.6) (99.1)

Cash flow and working capitalFinancial Performance to 30 June 2015

15

Working Capital2

9

1Denotes the effect of foreign exchange rate changes on cash and bank overdrafts.2Deltas denote current quarter working capital movement compared to the same period in the prior year

Free Cash Flow

9

• Cashflow from working capital improved due to collections by Bentec for the rigs delivered to Algeria since the year end

• In addition there is a favourable working capital impact of lower levels of activity and lower cash taxes

• Excluding the rights issue accounting between Holdings and Alpha:

• The working capital cashflow of $34m inflow would have been a $58m inflow

• The capital expenditure of $24.5m would have been $48.5m

1

16

2015 committed and contracted growth capex

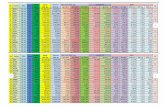

Rig Country Cost ($m)1 Contract length Status

Rig 1 Oman c.31 5yrs + 2x1yr options Operating

Rig 2 Oman c.31 5yrs + 2x1yr options Operating

Rig 3 Oman c.31 5yrs + 2x1yr options Operating

Rig 4 Russia c.30 3yrs + 3x1yr options Operating

Rig 5 Brunei c.37 3yrs + 3x1yr options In construction

Rig 6 Russia c.29 3yrs Operating

Rig 7 Oman c.31 5yrs + 2x1yr options In construction

Rig 8 Oman c.31 5yrs + 2x1yr options In construction

New build land rigs schedule

New build land rig contracts

• All ongoing capex projects were initiated in 2014 and are supported by long term contracts

• Up front contributions of $40m received from clients

• The 2015 growth capex plan is almost complete, with no new growth capex commitments currently proposed

• Maintenance capex spend for 2015 $80m - $85m

Construction Operational

All new build capital expenditure is targeted at a minimum 18% IRR

• Total 2015 capex spend on ongoing new build construction projects c.$130m

• Remaining capex spend in 2015 c.$54m

• All contracts remain in place without any re-negotiation of terms

PO

Rig R'cd Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

1 2014

2 2014

3 2014

4 2014

5 2014

6 2014

7 2014

8 2014

20152014

1 Excludes cost of mobilisation given this is reimbursed by client

17

Capital structureNet leverage as at 30 June 2015

1 All facilities have ratings outlooks of positive / stable.2 Based on Q2 2015 LTM EBITDA of $286 m.3 Revolver is split $75/$175m non cash/cash, the amount shown represents the cash element.

Utilisation30th June 2015

Coupon MaturityFacility Rating1

Recovery Rating

Net Leverage2

Revolver ($250m)3 41.7 L+400 May-19 B3/B 3/3 0.15x

Senior Secured Term Loan 371.3 L(100)+525 May-20 B3/B 3/3 1.30x

Total Bank Debt 413.0 1.44x

UK Finance Senior Secured Notes 375.0 7.250% May-21 B3/B 3/3 1.31x

Globe Luxembourg Senior Secured Notes

500.0 9.625% May-18 B3/B 3/3 1.75x

Total Institutional Debt 1,288.0 4.50x

Finance lease & other debt 12.2 - Aug-18 - - 0.04x

Gross Debt 1,300.2 4.55x

Cash 45.4 0.16x

Net Debt 1,254.8 4.38x

Closing remarks

18

• Stable Q2 performance in the current challenging market conditions

• $50m of committed funding from our shareholders still available for draw down if required

• Successful start up of 5 of the 8 new build rigs, with 3 more on track for delivery in 2015

• Cost initiatives delivering bottom line savings

• Strong backlog position at $7.6bn across a blue chip company base