Q1 - Orca Exploration · Orca Exploration Group Inc. 2009 Q1 Interim ... Major work was completed...

36

Orca Exploration Group Inc 2009 Q1 Interim Report Q1

Transcript of Q1 - Orca Exploration · Orca Exploration Group Inc. 2009 Q1 Interim ... Major work was completed...

Orca Exploration Group Inc.�

2009 Q1 Interim Report

Q1

Highlights 1

President & CEO’s letter to shareholders 3

MD&A 6

Financial statements 22

Notes to the consolidated financial statements 26

Orca Exploration Group Inc. is a well-financed, international public company

engaged in hydrocarbon exploration, development and marketing.� The Company’s

operations are directed from offices in Dar es Salaam, Tanzania.�

Orca’s focus is on the exploration, production, development and marketing of natural gas

to meet Tanzania’s growing power and industrial energy needs.�

Orca Exploration trades on the TSXV under the trading symbols ORC.B and ORC.A

This interim report contains certain forward-looking statements based on current expectations, but which involve risks and uncertainties.� Actual results may differ materially.� All financial information is reported in U.�S.� dollars (US$), unless otherwise noted.�

1

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

Orca Exploration Group Inc.

HIGHLIGHTS

FINANCIAL AND OPERATING HIGHLIGHTS

THREE MONTHS ENDED 31-Mar 2009 31-Mar 2008 Change

Financial (US$’000 except where otherwise stated)

Revenue 4,443 5,284 (16%)

Profit before taxation 322 270 19%

Operating netback (US$/mcf) 2.18 2.�21 (1%)

Cash and cash equivalents 9,710 12,521 (22%)

Working capital 9,154 8,297 10%

Shareholders’ equity 64,684 72,053 (10%)

(Loss) per share – basic and diluted (US$) (0.01) (0.�00) n/m

Funds from operations before working capital changes 1,458 2,391 (39%)

Funds per share from operations before working capital changes - basic and diluted (US$) 0.05 0.�08 (38%)

Outstanding Shares (‘000)

Class A shares 1,751 1,751 0%

Class B shares 27,788 27,863 0%

Options 2,797 2,847 (2%)

Operating

Additional Gas sold – industrial (MMscf) 360 322 12%

Additional Gas sold – power (MMscf) 1,570 1,983 (21%)

Average price per mcf – industrial (US$) 7.91 11.�55 (32%)

Average price per mcf – power (US$) 2.39 2.�05 17%

GLOSSARY

mcf Thousands of standard cubic feet

MMscf Millions of standard cubic feet

Bcf Billions of standard cubic feet

Tcf Trillions of standard cubic feet

MMscfd Millions of standard cubic feet per day

Mmbtu Millions of British thermal units

HHV High heat value

1P Proven reserves

2P Proven and probable reserves

3P Proven, probable and possible reserves

GIIP Gas initially in place

Kwh Kilowatt hour

MW Megawatt

US$ US dollars

Orca Exploration Group Inc.

HIGHLIGHTS

• IncreasedcapacityofthegasprocessingplantonSongoSongoIslandby29%to90MMscfd.

Actingasoperator,Orcamadeequipmentandfacilitieschangesapprovedbytheownerofthe

facilities,SongasLimited.Thecapacityoftheplantwasre-ratedbyLloydsRegisterto55MMscfd

pertrain,withaplantlimitof90MMscfdinJanuary2009anditisforecastthattheadditional

capacitywillbeutilisedinthesecondhalfof2009.

• Increasedprofitbeforetaxationby19%toUS$0.32million(Q12008:US$0.27million)despite

a16%decreaseinrevenue.FundsfromoperationsbeforeworkingcapitalchangeswereUS$1.5

million(Q12008:US$2.4million).

• IncreasedQ12009salesofAdditionalGastoDaresSalaamindustrialcustomersby12%to360

MMscfor4.0MMscfd(Q12008:322MMscfor3.5MMscfd).Giventhedeclineinworldoilprices,

averageindustrialpricesweredown32%atUS$7.91/mcf(Q12008:US$11.55/mcf),butremained

robustovertheperiod,andarelargelyprotectedbyafloorgaspricewhichshieldssalesfrom

lowoilprices.

• Q12009salesofAdditionalGastothepowersectordeclinedby21%to1,570MMscfor17.4

MMscfd(Q12008:1,983Mmscfor21.8MMscfd)primarilyduetoinsufficienttransmission

capacityfromthenew102MWWärtsiläpowerplantduringthequarter.Theaveragepricefor

thegasincreased17%toUS$2.39/mcf(Q12008:US$2.05/mcf)inlinewithlongtermpricing

agreements.

• CommencedthesaleofAdditionalGastotheWazoHillcementplantaheadofschedule.

ItisexpectedthatsalestoWazoHillwillaverage2MMscfdfromQ22009.Potentiallysalescould

exceed5MMscfdduring2009iftheownersoftheplant,TanzanianPortlandCementCompany,

determinethatthereissufficientdemandtooperateallitskilnssimultaneously.

• Connected4newindustrialcustomersandadded1kilometretothelowpressuregasdistribution

systematDaresSalaam.

• ContinuedconstructionofCNGfacilitiesinDaresSalaam,consistingofacompressor,avehicle

refuellingdispenserandtwotrailerfillingfacilitiesatthe“MotherStation”andthree

“DaughterStations”forthesupplyofsomeindustries,hotelsandoneinstitutionatacostof

US$2.5million.TheCNGfacilitiesareexpectedtobeoperationalattheendofQ22009andlead

to0.7MMscfdofCNGsales.

3

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

Medium and longer term demand for Additional Gas

produced by Orca Exploration from Tanzania’s Songo Songo field

continues to show steady and significant growth.� Prospects for a

sustained increase in gas demand by both the power and industrial

sectors remain excellent.�

Currently the maximum demand for Orca’s Additional Gas by the

power sector is approximately 28 MMscfd.� This is expected to

increase by 32% to 37 MMscfd in Q4 2009 when the new 45 MW

Tegeta power plant becomes operational.�

The number of Orca’s industrial customers in the Dar es Salaam

area continues to grow with 4 new customers connected in Q1 2009.�

This brings the total number of industrial customers connected to

24, and a total of 31 customers contracted.� New markets are also

being developed to reach beyond Orca’s low pressure gas distri-

bution system at Dar es Salaam with the construction of new CNG

compression and distribution facilities that are scheduled to be in

operation by the end of Q2 2009.�

To ensure that Orca is positioned to meet these demands, Orca

took decisive steps in Q1 2009 to increase the capacity of the infra-

structure that processes and transports gas from the Songo Songo

field to Dar es Salaam.� The overall system capacity has now been

increased by 29% to 90 MMscfd.� This enables the Company to sell

and deliver up to 45 MMscfd of Additional Gas compared with 25-30

MMscfd before the system capacity was increased.� This capacity

increase removes a major constraint that had previously limited

the Company’s ability to fully meet gas demand on some occasions

during 2008.�

Orca is currently undertaking additional work on the gas processing

facilities to increase capacity to 110 MMscfd by the end of 2009.�

Each of the gas processing trains has been tested and certified

to 55 MMscfd by Lloyds Register, but there is a plant limit of 90

MMscfd.� The Company is simultaneously conducting pipeline tests

and engineering studies to assess whether the high pressure

pipeline that transport the gas from the Songo Songo field to Dar es

Salaam has sufficient capacity to handle these additional processed

volumes.�

Since 2006, Songas Limited has been looking to increase the capacity

of its infrastructure by installing two additional gas processing

trains.� In the event that the planned expansion by Songas does not

proceed, Orca is developing a contingency plan to expand the gas

processing capability and pipeline capacity to 200 MMscfd.� This

production level would be consistent with the forecast peak demand

that could be met with current 2P Songo Songo reserves.� If Orca

decided to proceed with the contingency plan, the Company would

seek third party finance for the expansion, with the objective of

having the project in place by 2012.�

POWER SECTOR

The Tanzanian electricity utility, TANESCO, is currently entering

a transitional phase.� The emergency gas fired generation that

was introduced in 2006 (Dowans 120 MWs and Aggreko 48 MWs)

is now being replaced by permanent generation capacity.� As a

result, Tanzania currently has 148 MWs of generation operating on

Additional Gas compared to 210 MWs at this time last year.� This is

insufficient to meet current electricity demand and it is anticipated

that there will be load shedding during the latter part of 2009.� The

situation will become acute if power transmission constraints with

the existing facilities persist.� In Q1 2009 the Wärtsilä 102 MW power

plant was only able to operate at approximately 50% capacity.�

TANESCO has taken steps to rectify the short term power generation

shortfall.� An additional 45 MWs of permanent generation is under

construction at Tegeta in Dar es Salaam and is expected to be

operational in Q4 2009.� In addition, TANESCO has tendered for a

new 100 MW power plant with the objective of it being operational

in 2010.� This plant, along with the existing gas fired generation,

will be supplied with Additional Gas under the Portfolio Gas

Sales Agreement with Orca that was initialled in June 2008.� This

agreement is currently being updated to take into account the

change in generation capacity mix and infrastructure development

considerations.�

PRESIDENT & CEO’S LETTER TO SHAREHOLDERS

Opposite page: Orca is supplying Additional Gas to the new US$100 million Kiln 4 constructed at Dar es Salaam by the Tanzania Portland Cement Company. The kiln is currently being commissioned and is expected to be in operation in June 2009.

5

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

Over the longer term the Tanzanian Power Sector Master Plan is

projecting annual growth in electricity demand of 7% to 10% per

annum.� This equates to approximately 100 MWs of new generation

being added annually until 2016.� To meet this demand, TANESCO has

started planning for the construction of a 200 – 250 MW power plant

at Kinyerezi, Dar es Salaam.� If built, this plant would require approxi-

mately 40 - 50 MMscfd.� Negotiation of the Kinyerezi power plant gas

supply contract is expected to commence in the second half of 2009,

once the initialed contracts are signed.� TANESCO has indicated that

it is targeting Kinyerezi being operational by 2012.�

INDUSTRIAL SECTOR

The Company has commenced selling gas to Tanzania Portland

Cement Company (“TPCC”), the owner of the expanded Wazo Hill

cement plant in Dar es Salaam.� The new US$100 million Kiln 4 is

expected to be fully operational in June 2009 and will consume a

minimum of 2 MMscfd for the remainder of the year.� Orca is currently

discussing the possibility of further gas sales to TPCC later in 2009

to enable all of its kilns to operate simultaneously before two of the

kilns are shut down for major maintenance.�

Orca continues to increase the number of its industrial customers.�

During Q1 2009, 4 new industrial customers were connected adding

0.�2 MMscfd of demand and increasing the total customers connected

to 24, with a total of 31 customers contracted.� The low pressure

pipeline system was extended by 1 kilometer to connect these

customers and now totals 43 kilometers.�

Due to the diversified nature of Orca’s customers, the current global

recession is not expected to have a significant impact on 2009

industrial sales.�

COMPRESSED NATURAL GAS (CNG)

Major work was completed in Q1 2009 on the new CNG “Mother

Station” in Dar es Salaam consisting of a compressor, a vehicle

refueling dispenser and two trailer filling facilities.� Three “Daughter

Stations” are also being added to supply some Dar es Salaam

industries, hotels and one institution beyond the reach of Orca’s low

pressure gas pipeline.� The CNG facilities, being constructed at a cost

of US$2.�5 million, are expected to be operational at the end of Q2

2009 and lead to 0.�7 MMscfd of CNG sales.� CNG deliveries outside

Dar es Salaam will commence with supply to the Mikocheni region,

followed by supply to the City of Morogoro.�

FINANCIAL RESULTS

The Company generated funds flow

before working capital changes of

US$1.�5 million during Q1 2009 despite lower gas sales to the power

sector and a decrease in the price of gas to industrial customers.�

Increases are expected to continue through 2009 as the Wazo Hill

cement plant consumes more gas and Tanzania enters its dry season

during which gas fired power generation increases.�

Orca is also cutting General and Administrative (“G&A”) costs.� In

Q1 2009, this resulted in a reduction in G&A despite there being an

increase in personnel in Tanzania to manage growth in downstream

gas activities and customers.�

The Company currently has cash on hand of approximately US$9.�7

million and working capital of US$9.�2 million.�

OUTLOOK

During 2009, Orca’s management will focus on monetising the

Company’s proven (1P) Additional Gas reserves that increased by

26% at the end of 2008 to 389 Bcf (2P reserves: 491 Bcf).�

Your Company is a leader in developing Tanzania’s natural gas reserves

and in ventures that are increasing Tanzania’s domestic energy self-

reliance.� Despite economic uncertainties in other parts of the world,

this is the right time to be developing and marketing hydrocarbon

resources in Tanzania and in sub-Saharan Africa.� The demand for

cleaner, lower cost fossil fuels is growing, the Songo Songo gas

production infrastructure continues to be developed and our team of

dedicated employees is working to add additional gas reserves.�

As always, management is aware that Orca Exploration’s vitality is

always dependent on our skilled and dedicated employees and our

loyal shareholders.� We look forward to continued growth and profit-

ability over the course of 2009.�

loyal shareholders.�

Peter R.� Clutterbuck President and CEO

28 May 2009

Photo below: Orca continues to add industrial customers to its low-pressure gas distribution system at Dar es Salaam and to expand gas distribution into other cities using CNG trailers for transport.

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

NON-GAAP MEASURES

THE COMPANY EVALUATES ITS PERFORMANCE BASED ON FUNDS FLOW FROM OPERATING ACTIVITIES AND OPERATING NETBACKS.� FUNDS FLOW FROM OPERATING ACTIVITIES IS A NON-GAAP (GENERALLY ACCEPTED ACCOUNTING PRINCIPLES) TERM THAT REPRESENTS CASH FLOW FROM OPERATIONS BEFORE WORKING CAPITAL ADJUSTMENTS.� IT IS A KEY MEASURE AS IT DEMONSTRATES THE COMPANY’S ABILITY TO GENERATE CASH NECESSARY TO ACHIEVE GROWTH THROUGH CAPITAL INVESTMENTS.� ORCA EXPLORATION ALSO ASSESSES ITS PERFORMANCE UTILIZING OPERATING NETBACKS.� OPERATING NETBACKS REPRESENT THE PROFIT MARGIN ASSOCIATED WITH THE PRODUCTION AND SALE OF ADDITIONAL GAS AND IS CALCULATED AS REVENUES LESS RINGMAIN TARIFF, GOVERNMENT PARASTATAL’S REVENUE SHARE, OPERATING AND DISTRIBUTION COSTS FOR ONE THOUSAND STANDARD CUBIC FEET OF ADDITIONAL GAS.� THIS IS A KEY MEASURE AS IT DEMONSTRATES THE PROFIT GENERATED FROM EACH UNIT OF PRODUCTION, AND IS WIDELY USED BY THE INVESTMENT COMMUNITY.� THESE NON-GAAP MEASURES ARE NOT STANDARDISED AND THEREFORE MAY NOT BE COMPARABLE TO SIMILAR MEASUREMENTS OF OTHER ENTITIES.�

ADDITIONAL INFORMATION REGARDING ORCA EXPLORATION GROUP INC IS AVAILABLE UNDER THE COMPANY’S PROFILE ON SEDAR AT www.�sedar.�com.�

BACKGROUND

Orca Exploration’s principal operating asset is its interest in a Production Sharing Agreement (“PSA”) with the Tanzania Petroleum Development Corporation (“TPDC”) in Tanzania.� This PSA covers the production and marketing of certain gas from the Songo Songo gas field.�

The gas in the Songo Songo field is divided between Protected Gas and Additional Gas.� The Protected Gas is owned by TPDC and is sold under a 20-year gas agreement to Songas Limited (“Songas”).� Songas is the owner of the infrastructure that enables the gas to be delivered to Dar es Salaam, namely a gas processing plant on Songo Songo Island, 232 kilometers of pipeline to Dar es Salaam and a 16 kilometer spur to the Wazo Hill Cement Plant.�

Songas utilizes the Protected Gas (maximum 45.�1 MMscfd) as feedstock for its gas turbine electricity generators at Ubungo, for onward sale to the Wazo Hill cement plant and for electrification of some villages along the pipeline route.� Orca Exploration receives no revenue for the Protected Gas delivered to Songas and operates the field and gas processing plant on a ‘no gain no loss’ basis.�

Orca Exploration has the right to produce and market all gas in the Songo Songo field in excess of the Protected Gas requirements (“Additional Gas”).�

FORWARD LOOKING STATEMENTS

THIS MDA OF FINANCIAL CONDITIONS AND RESULTS OF OPERATIONS FOR THE THREE MONTHS ENDED 31 MARCH 2009 SHOULD BE READ IN CONJUNCTION WITH THE AUDITED FINANCIAL STATEMENTS AND NOTES THERETO FOR YEAR ENDED 31 DECEMBER 2008.� THIS MDA IS BASED ON THE INFORMATION AVAILABLE ON 28 MAY 2009.�

CERTAIN STATEMENTS IN THIS MD&A INCLUDING (I) STATEMENTS THAT MAY CONTAIN WORDS SUCH AS “ANTICIPATE”, “COULD”, “EXPECT”, “SEEK”, “MAY” “INTEND”, “WILL”, “BELIEVE”, “SHOULD”, “PROJECT”, “FORECAST”, “PLAN” AND SIMILAR EXPRESSIONS, INCLUDING THE NEGATIVES THEREOF, (II) STATEMENTS THAT ARE BASED ON CURRENT EXPECTATIONS AND ESTIMATES ABOUT THE MARKETS IN WHICH ORCA OPERATES AND (III) STATEMENTS OF BELIEF, INTENTIONS AND EXPEC-TATIONS ABOUT DEVELOPMENTS, RESULTS AND EVENTS THAT WILL OR MAY OCCUR IN THE FUTURE, CONSTITUTE “FORWARD-LOOKING STATEMENTS” AND ARE BASED ON CERTAIN ASSUMPTIONS AND ANALYSIS MADE BY ORCA.� FORWARD-LOOKING STATEMENTS IN THIS MD&A INCLUDE, BUT ARE NOT LIMITED TO, STATEMENTS WITH RESPECT TO FUTURE CAPITAL EXPENDITURES, INCLUDING THE AMOUNT, NATURE AND TIMING THEREOF; NATURAL GAS PRICES AND DEMAND.�

SUCH FORWARD-LOOKING STATEMENTS ARE SUBJECT TO IMPORTANT RISKS AND UNCERTAINTIES, WHICH ARE DIFFICULT TO PREDICT AND THAT MAY AFFECT ORCA’S OPERATIONS, INCLUDING, BUT NOT LIMITED TO: THE IMPACT OF GENERAL ECONOMIC CONDITIONS IN TANZANIA AND CANADA; INDUSTRY CONDITIONS, INCLUDING THE ADOPTION OF NEW ENVIRONMENTAL, SAFETY AND OTHER LAWS AND REGULATIONS AND CHANGES IN HOW THEY ARE INTERPRETED AND ENFORCED; VOLATILITY OF NATURAL GAS PRICES; NATURAL GAS PRODUCT SUPPLY AND DEMAND; RISKS INHERENT IN ORCA’S ABILITY TO GENERATE SUFFICIENT CASH FLOW FROM OPERATIONS TO MEET ITS CURRENT AND FUTURE OBLIGATIONS; INCREASED COMPETITION; THE FLUCTUATION IN FOREIGN EXCHANGE OR INTEREST RATES; STOCK MARKET VOLATILITY; AND OTHER FACTORS, MANY OF WHICH ARE BEYOND THE CONTROL OF ORCA.�

ORCA’S ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS COULD DIFFER MATERIALLY FROM THOSE EXPRESSED IN, OR IMPLIED BY, THESE FORWARD-LOOKING STATEMENTS AND, ACCORDINGLY, NO ASSURANCE CAN BE GIVEN THAT ANY OF THE EVENTS ANTICIPATED BY THE FORWARD-LOOKING STATEMENTS WILL TRANSPIRE OR OCCUR, OR IF ANY OF THEM DO TRANSPIRE OR OCCUR, WHAT BENEFITS ORCA WILL DERIVE THEREFROM.� SUBJECT TO APPLICABLE LAW, ORCA DISCLAIMS ANY INTENTION OR OBLIGATION TO UPDATE OR REVISE ANY FORWARD-LOOKING STATEMENTS, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE.� ALL FORWARD-LOOKING STATEMENTS CONTAINED IN THIS DOCUMENT ARE EXPRESSLY QUALIFIED BY THIS CAUTIONARY STATEMENT.�

Management’s Discussion & Analysis

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

7

(d) By 31 July 2009, the Government of Tanzania (“GoT”) can request Orca Exploration to sell 100 Bcf of Additional Gas for the generation of electricity over a period of 20 years from the start of its commercial use, subject to a maximum of 6 Bcf per annum or 20 MMscfd (“Reserved Gas”).� In the event that the GoT does not nominate by 31 July 2009, or consumption of the Reserved Gas has not commenced within three years of the nomination date, then the reservation shall terminate.� Where Reserved Gas is utilized, TPDC and the Company will receive a price that is no greater than 75% of the market price of the lowest cost alternative fuel delivered at the facility to receive Reserved Gas or the price of the lowest cost alternative fuel at Ubungo.� Under the terms of the initialled ARGA, sales under the ARGA and PGSA are considered Reserved Gas.�

(e) “Insufficiency” occurs if there is insufficient gas from the Discovery Blocks to supply the Protected Gas requirements or is so expensive to develop that its cost exceeds the market price of alternative fuels at Ubungo.�

Where there have been third party sales of Additional Gas by Orca Exploration and TPDC from the Discovery Blocks prior to the occurrence of the Insufficiency, Orca Exploration and TPDC shall be jointly liable for the Insufficiency and shall satisfy its related liability by either replacing the Indemnified Volume (as defined in (f) below) at the Protected Gas price with natural gas from other sources; or by paying money damages equal to the difference between: (a) the market price for a quantity of alternative fuel that is appropriate for the five gas turbine electricity generators at Ubungo without significant modifica-tion together with the costs of any modification; and (b) the sum of the price for such volume of Protected Gas (at US$0.�55/Mmbtu) and the amount of transportation revenues previously credited by Songas to the electricity utility, TANESCO, for the gas volumes.�

(f) The “Indemnified Volume” means the lesser of the total volume of Additional Gas sales supplied from the Discovery Blocks prior to an Insufficiency and the Insufficiency Volume.� “Insufficiency Volume” means the volume of natural gas determined by multiplying the average of the annual Protected Gas volumes for the three years prior to the Insufficiency by 110% and multiplied by the number of remaining years (initial term of 20 years) of the power purchase agreement entered into between Songas and TANESCO in relation to the five gas turbine electricity generators at Ubungo from the date of the Insufficiency.�

As discussed in (c) above, an Insufficiency Agreement has been negotiated with TPDC, Songas and TANESCO that reduces these potential liabilities.� The Insufficiency Agreement is expected to be signed at the same time as the long term power contracts.�

Principal terms of the PSA and related agreements

The principal terms of the Songo Songo PSA and related agreements are as follows:

Obligations and restrictions

(a) The Company has the right to conduct petroleum operations, market and sell all Additional Gas produced and share the net revenue with TPDC for a term of 25 years expiring in October 2026.�

(b) The PSA covers the two licenses in which the Songo Songo field is located (“Discovery Blocks”).�

The Proven Section is essentially the area covered by the Songo Songo field within the Discovery Blocks.�

(c) No sales of Additional Gas may be made from the Discovery Blocks if in Orca Exploration’s reasonable judgment such sales would jeopardise the supply of Protected Gas.� Any Additional Gas contracts entered into are subject to interruption.� Songas has the right to request that the Company and TPDC obtain security reasonably acceptable to Songas prior to making any sales of Additional Gas from the Discovery Block to secure the Company’s and TPDC’s obligations in respect of Insufficiency (see (e) below).�

In June 2008, the Company initialled two long term power contracts with TANESCO, the owner of the Ubungo power plant, Songas Limited and the Ministry of Energy and Minerals for the supply of approximately 30 - 45 MMscfd for power generation.� The first of the contracts (Amended and Restated Gas Agreement (“ARGA”)) covers the supply of gas to the sixth turbine at the Ubungo power plant and provides for a maximum of approximately 9 MMscfd until July 2024.� The second initialled contract (Portfolio Gas Sales Agreement (“PGSA”)) covers the supply of Additional Gas sales to a portfolio of gas fired generation in Tanzania.�

The ARGA provides clarification of the Protected Gas volumes and removes all terms dealing with the security of the Protected Gas and the consequences of any insufficiency to a new Insufficiency Agreement (“IA”).� The IA specifies terms under which Songas may demand cash security in order to keep them whole in the event of a Protected Gas insufficiency.� Once the IA is signed, it will govern the basis for determining security.� Under the provisional terms of the IA, when it is calculated that funding is required, the Company shall fund an escrow account at a rate of US$2/Mmbtu on all industrial Additional Gas sales out of its and TPDC’s share of revenue and TANESCO shall contribute the same amount on Additional Gas sales to the power sector.� The funds provide security for Songas in the event of an insufficiency of Protected Gas.� The Company is actively monitoring the reservoir and does not anticipate that a liability will occur in this respect.�

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

Access and development of infrastructure

(g) The Company is able to utilise the Songas infrastructure including the gas processing plant and main pipeline to Dar es Salaam.� Access to the pipeline and gas processing plant is open and can be utilized by any third party who wishes to process or transport gas.�

Songas is not required to incur capital costs with respect to additional processing and transportation facilities unless the construction and operation of the facilities are, in the reasonable opinion of Songas, financially viable.� If Songas is unable to finance such facilities, Songas shall permit the seller of the gas to construct the facilities at its expense, provided that, the facilities are designed, engineered and constructed in accordance with good pipeline and oilfield practices.�

Revenue sharing terms and taxation

(h) 75% of the gross revenues less processing and pipeline tariffs and direct sales taxes in any year (“Net Revenues”) can be used to recover past costs incurred.� Costs recovered out of Net Revenues are termed “Cost Gas”.�

The Company pays and recovers all costs of exploring, developing and operating the Additional Gas with two exceptions: (i) TPDC may recover reasonable market and market research costs as defined under the PSA; and (ii) TPDC has the right to elect to participate in the drilling of at least one well for Additional Gas in the Discovery Blocks for which there is a development program as detailed in the Additional Gas plans as submitted to the Ministry of Energy and Minerals (“Additional Gas Plan”) subject to TPDC being able to elect to participate in a development program only once and TPDC having to pay a proportion of the costs of such development program by committing to pay between 5% and 20% of the total costs (“Specified Proportion”).� If TPDC does not notify the Company within 90 days of notice from the Company that the Ministry of Energy and Minerals (“MEM”) has approved the Additional Gas Plan, then TPDC is deemed not to have elected.� If TPDC elects to participate, then it will be entitled to a rateable proportion of the Cost Gas and their profit share percentage increases by the Specified Proportion for that development program.�

TPDC has indicated that they wish to exercise their right to ‘back in’ to the field development by contributing 20% of the cost of SS-10 and the cost of future wells in return for a 20% increase in the profit share percentage for the production emanating from these wells.� The implications and workings of the ‘back in’ are still to be discussed in detail with TPDC and there may be the need for reserve modifications once these

discussions are concluded.� For the purpose of the reserves certification as at 31 December 2008, it has been assumed that they will ‘back in’ for 20% and this is reflected in the Company’s net reserve position.� However, the financial statements have not taken account of any reimbursement for the SS-10 capital expenditure incurred, pending the finalisation of the terms of the ‘back in’.�

(i) The price payable to Songas for the general processing and transportation of the gas is 17.�5% of the price of gas delivered to a third party less any direct taxes payable by the customer that are included in the gas price less any tariffs paid for non-Songas owned distribution facilities (“Songas Outlet Price”).�

In September 2001, the GoT, made a formal request to the World Bank for funds to increase the diameter of the onshore pipeline from 12 inches to 16 inches at a projected incremental cost of US$3.�5 million.� The World Bank agreed to finance this increase and accordingly the pipeline capacity was increased from circa 65 MMscfd to 105 MMscfd.� The tariff that is payable to GoT for this incremental capacity has yet to be formally agreed, but the Company expects it to be 17.�5% of the Songas Outlet Price.�

In October 2008, Songas submitted a third tariff application to the regulator, EWURA, to cover the financing and operating costs of the third and fourth train which is forecast to increase the gas processing capacity to 140 MMscfd.� On 27 February 2009, EWURA issued an order that sees the introduction of flat rate tariffs from 1 January 2010.� The tariff level will be set at a rate that enables Songas to make a rate of return on their investment as determined by EWURA.� Songas may challenge this order and there is no certainty that they will finance the third and fourth train.� The Company is negotiating the long term gas price to the power sector based on the price of gas at the Wellhead.� As a consequence, the Company is not impacted by the changes to the tariff paid to Songas in respect of sales to the power sector.�

(j) The cost of maintaining the wells and flowlines is split between the Protected Gas and Additional Gas users in proportion to the volume of their respective sales.� The cost of operating the gas processing plant and the pipeline to Dar es Salaam is covered through the payment of the pipeline tariff.�

(k) Profits on sales from the Proven Section (“Profit Gas”) are shared between TPDC and the Company, the proportion of which is dependent on the average daily volumes of Additional Gas sold or cumulative production.�

The Company receives a higher share of the net revenues after cost recovery, the higher the cumulative production or the average daily sales, whichever is higher.� The profit share is a minimum of 25% and a maximum of 55%.�

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

9

Operatorship

(m) The Company is appointed to develop, produce and process Protected Gas and operate and maintain the gas production facilities and processing plant, including the staffing, procurement, capital improvements, contract maintenance, maintain books and records, prepare reports, maintain permits, handle waste, liaise with GoT and take all necessary safe, health and environmental precautions all in accordance with good oilfield practices.� In return, the Company is paid or reimbursed by Songas so that the Company neither benefits nor suffers a loss as a result of its performance.�

(n) In the event of loss arising from Songas’ failure to perform and the loss is not fully compensated by Songas, Orca Exploration, CDC or insurance coverage, then Orca Exploration is liable to a performance and operation guarantee of US$2.�5 million when (i) the loss is caused by the gross negligence or willful misconduct of the Company, its subsidiaries or employees, and (ii) Songas has insufficient funds to cure the loss and operate the project.�

Average daily sales

of Additional Gas

Cumulative sales of

Additional Gas

TPDC’s share of

Profit Gas

Company’s share of

Profit Gas

MMscfd Bcf % %

0 - 20 0 – 125 75 25

> 20 <= 30 > 125 <= 250 70 30

> 30 <= 40 > 250 <= 375 65 35

> 40 <= 50 > 375 <= 500 60 40

> 50 > 500 45 55

For Additional Gas produced outside of the Proven Section, the Company’s profit share increases to 55%.�

Where TPDC elects to participate in a development program, their profit share percentage increases by the Specified Proportion (for that development program) with a correspond-ing decrease in the Company’s percentage share of Profit Gas.�

The Company is liable to income tax.� Where income tax is payable, there is a corresponding deduction in the amount of the Profit Gas payable to TPDC.�

(l) Additional Profits Tax is payable where the Company has recovered its costs plus a specified return out of Cost Gas revenues and Profit Gas revenues.� As a result: (i) no Additional Profits Tax is payable until the Company recovers all its costs out of Additional Gas revenues plus an annual return of 25% plus the percentage change in the United States Industrial Goods Producer Price Index (“PPI”); and (ii) the maximum Additional Profits Tax rate is 55% of the Company’s Profit Gas when costs have been recovered with an annual return of 35% plus PPI return.� The PSA is, therefore, structured to encourage the Company to develop the market and the gas fields in the knowledge that the profit share can increase with larger daily gas sales and that the costs will be recovered with a 25% plus PPI annual return before Additional Profits Tax becomes payable.� Additional Profits Tax can have a significant negative impact on the project economics if only limited capital expenditure is incurred.�

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

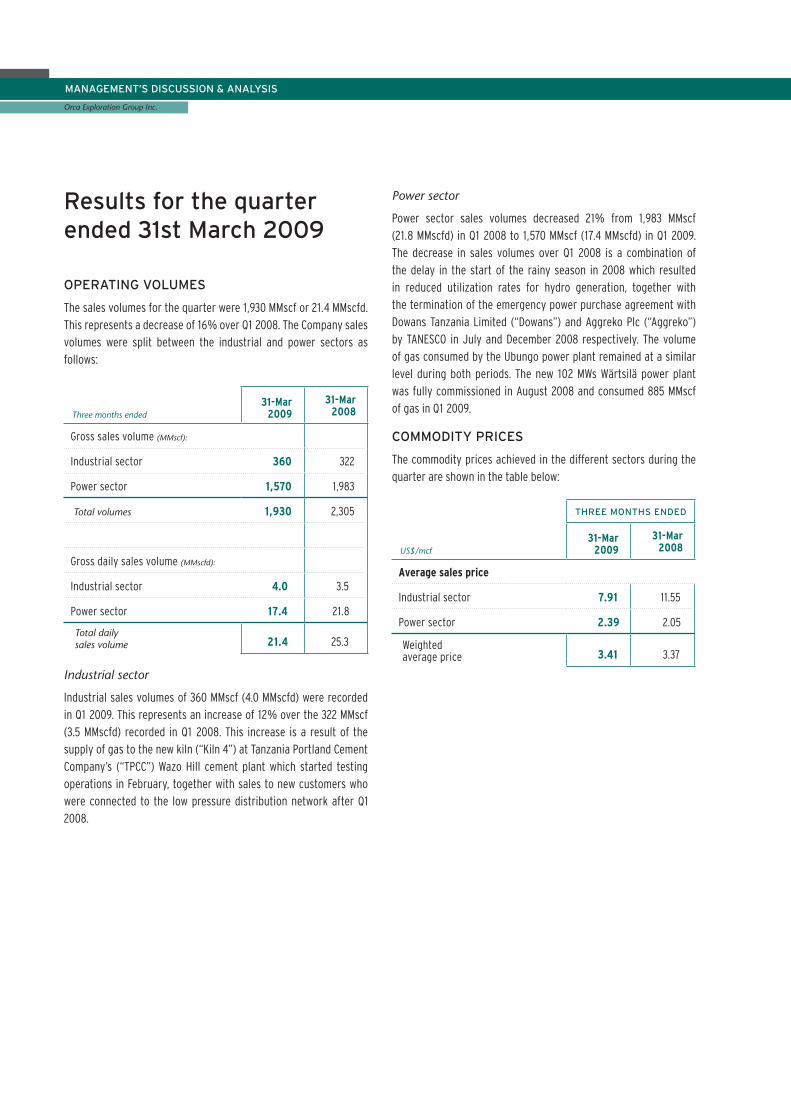

Results for the quarter ended 31st March 2009

OPERATING VOLUMES

The sales volumes for the quarter were 1,930 MMscf or 21.�4 MMscfd.� This represents a decrease of 16% over Q1 2008.� The Company sales volumes were split between the industrial and power sectors as follows:

Three months ended31-Mar

200931-Mar

2008

Gross sales volume (MMscf):

Industrial sector 360 322

Power sector 1,570 1,983

Total volumes 1,930 2,305

Gross daily sales volume (MMscfd):

Industrial sector 4.0 3.�5

Power sector 17.4 21.�8

Total daily sales volume 21.4 25.�3

Industrial sector

Industrial sales volumes of 360 MMscf (4.�0 MMscfd) were recorded in Q1 2009.� This represents an increase of 12% over the 322 MMscf (3.�5 MMscfd) recorded in Q1 2008.� This increase is a result of the supply of gas to the new kiln (“Kiln 4”) at Tanzania Portland Cement Company’s (“TPCC”) Wazo Hill cement plant which started testing operations in February, together with sales to new customers who were connected to the low pressure distribution network after Q1 2008.�

Power sector

Power sector sales volumes decreased 21% from 1,983 MMscf (21.�8 MMscfd) in Q1 2008 to 1,570 MMscf (17.�4 MMscfd) in Q1 2009.� The decrease in sales volumes over Q1 2008 is a combination of the delay in the start of the rainy season in 2008 which resulted in reduced utilization rates for hydro generation, together with the termination of the emergency power purchase agreement with Dowans Tanzania Limited (“Dowans”) and Aggreko Plc (“Aggreko”) by TANESCO in July and December 2008 respectively.� The volume of gas consumed by the Ubungo power plant remained at a similar level during both periods.� The new 102 MWs Wärtsilä power plant was fully commissioned in August 2008 and consumed 885 MMscf of gas in Q1 2009.�

COMMODITY PRICES

The commodity prices achieved in the different sectors during the quarter are shown in the table below:

US$/mcf

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Average sales price

Industrial sector 7.91 11.�55

Power sector 2.39 2.�05

Weighted average price 3.41 3.�37

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

11

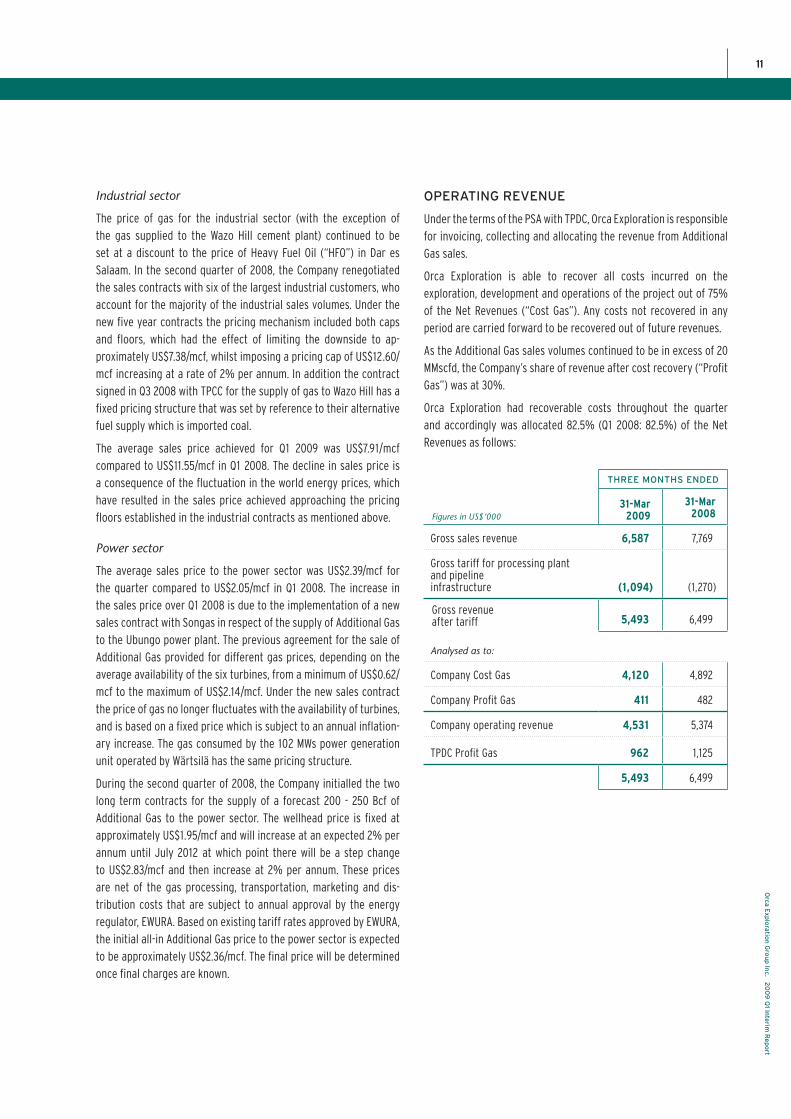

Industrial sector

The price of gas for the industrial sector (with the exception of the gas supplied to the Wazo Hill cement plant) continued to be set at a discount to the price of Heavy Fuel Oil (“HFO”) in Dar es Salaam.� In the second quarter of 2008, the Company renegotiated the sales contracts with six of the largest industrial customers, who account for the majority of the industrial sales volumes.� Under the new five year contracts the pricing mechanism included both caps and floors, which had the effect of limiting the downside to ap-proximately US$7.�38/mcf, whilst imposing a pricing cap of US$12.�60/mcf increasing at a rate of 2% per annum.� In addition the contract signed in Q3 2008 with TPCC for the supply of gas to Wazo Hill has a fixed pricing structure that was set by reference to their alternative fuel supply which is imported coal.�

The average sales price achieved for Q1 2009 was US$7.�91/mcf compared to US$11.�55/mcf in Q1 2008.� The decline in sales price is a consequence of the fluctuation in the world energy prices, which have resulted in the sales price achieved approaching the pricing floors established in the industrial contracts as mentioned above.�

Power sector

The average sales price to the power sector was US$2.�39/mcf for the quarter compared to US$2.�05/mcf in Q1 2008.� The increase in the sales price over Q1 2008 is due to the implementation of a new sales contract with Songas in respect of the supply of Additional Gas to the Ubungo power plant.� The previous agreement for the sale of Additional Gas provided for different gas prices, depending on the average availability of the six turbines, from a minimum of US$0.�62/mcf to the maximum of US$2.�14/mcf.� Under the new sales contract the price of gas no longer fluctuates with the availability of turbines, and is based on a fixed price which is subject to an annual inflation-ary increase.� The gas consumed by the 102 MWs power generation unit operated by Wärtsilä has the same pricing structure.�

During the second quarter of 2008, the Company initialled the two long term contracts for the supply of a forecast 200 - 250 Bcf of Additional Gas to the power sector.� The wellhead price is fixed at approximately US$1.�95/mcf and will increase at an expected 2% per annum until July 2012 at which point there will be a step change to US$2.�83/mcf and then increase at 2% per annum.� These prices are net of the gas processing, transportation, marketing and dis-tribution costs that are subject to annual approval by the energy regulator, EWURA.� Based on existing tariff rates approved by EWURA, the initial all-in Additional Gas price to the power sector is expected to be approximately US$2.�36/mcf.� The final price will be determined once final charges are known.�

OPERATING REVENUE

Under the terms of the PSA with TPDC, Orca Exploration is responsible for invoicing, collecting and allocating the revenue from Additional Gas sales.�

Orca Exploration is able to recover all costs incurred on the exploration, development and operations of the project out of 75% of the Net Revenues (“Cost Gas”).� Any costs not recovered in any period are carried forward to be recovered out of future revenues.�

As the Additional Gas sales volumes continued to be in excess of 20 MMscfd, the Company’s share of revenue after cost recovery (“Profit Gas”) was at 30%.�

Orca Exploration had recoverable costs throughout the quarter and accordingly was allocated 82.�5% (Q1 2008: 82.�5%) of the Net Revenues as follows:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Gross sales revenue 6,587 7,769

Gross tariff for processing plant and pipeline infrastructure (1,094) (1,270)

Gross revenue after tariff 5,493 6,499

Analysed as to:

Company Cost Gas 4,120 4,892

Company Profit Gas 411 482

Company operating revenue 4,531 5,374

TPDC Profit Gas 962 1,125

5,493 6,499

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

The Company’s revenue reported for the quarter amounted to US$4,443,000 after adjusting the Company’s operating revenue of US$4,531,000 by:

i) US$ nil for current income tax.� The Company is liable for income tax in Tanzania, but the income tax is recoverable out of TPDC’s Profit Gas when the tax is payable.� To account for this, revenue is adjusted to reflect the current income tax charge or loss.�

ii) US$88,000 for the deferred effect of Additional Profits Tax.� This tax is considered a royalty and is netted against revenue.�

Revenue per the income statement may be reconciled to the operating revenue as follows:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Industrial sector 2,847 3,713

Power sector 3,740 4,056

Gross sales revenue 6,587 7,769

Processing and transportation tariff (1,094) (1,270)

TPDC share of revenue (962) (1,125)

Company operating revenue 4,531 5,374

Additional Profits Tax (88) (90)

Current income tax adjustment – –

Revenue 4,443 5,284

Processing and Transportation Tariff

Under the terms of the project agreements, the current tariff paid for processing and transporting the Additional Gas is calculated as 17.�5% of the price of gas at the Songas main pipeline in Dar es Salaam (“Songas Outlet Price”).�

In calculating the Songas Outlet Price for the industrial customers, an average amount of US$1.�47/mcf (“Ringmain Tariff”) (Q1 2008: US$1.�52/mcf) has been deducted from the achieved industrial sales price of US$7.�91/mcf (Q1 2008: US$11.�55/mcf) to reflect the gas price that would be achievable at the Songas main pipeline.� The Ringmain Tariff represents the amount that would be required to compensate a third party distributor of the gas for constructing the connections from the Songas main pipeline to the industrial customers.� No deduction has been made for sales to the power sector since the gas is not transported through the Company’s own infrastructure.�

To enable the Company to supply 30-45 MMscfd of Additional Gas to the power sector under the initialled long term power contracts, Songas is planning to install a third and fourth gas processing train on Songo Songo Island conditional on a satisfactory economic return as approved by the energy regulator, EWURA.� EWURA issued their order on 26 February 2009.� It is forecast that Songas will not proceed on the terms laid down by EWURA and that the installation of the third and fourth trains will not proceed as envisaged.�

Despite this, the regulatory process is likely to lead to a new tariff regime being introduced that will be subject to annual amendments.� A flat rate gas processing and transportation tariff may be introduced from 1 January 2010 that will be set at a rate that enables Songas to make a rate of return on their investment as determined by EWURA.� The Company will pass on any increase or decrease in the EWURA approved charges to TANESCO/Songas in respect of sales to the power sector.� This protocol insulates Orca Exploration from any increases in the gas processing and pipeline infrastructure costs.�

PRODUCTION AND DISTRIBUTION EXPENSES

The well maintenance costs are allocated between Protected and Additional Gas based on the proportion of their respective sales during the quarter.� The total costs for the maintenance for the quarter was US$138,000 (Q1 2008: US$100,000) and US$52,000 (Q1 2008: US$42,000) was allocated for the Additional Gas.�

Other field and operating costs include an apportionment of the annual PSA licence costs and some costs associated with the evaluation of the reserves.�

The direct costs of maintaining the Ringmain distribution pipeline and pressure reduction station (security, insurance and personnel) is forecast to be approximately US$0.�7 million per annum in its current form.�

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

13

ADMINISTRATIVE EXPENSES

The administrative expenses (“G&A”) may be analysed as follows:

(Figures in US$’000)

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Employee costs 567 494

Consultants 647 565

Travel and accommodation 136 174

Communications 20 1 1

Office 283 188

Insurance 53 70

Auditing and taxation 44 51

Depreciation 23 16

Reporting, regulatory and corporate 71 55

1,844 1,624

Marketing costs and legal fees 739 831

Stock based compensation 462 640

Net general and administrative expenses 3,045 3,095

These costs are summarized in the table below:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Share of well maintenance 52 42

Other field and operating costs 105 79

Ringmain distribution pipeline 148 155

Production and distribution expenses 305 276

OPERATING NETBACKS

The netback per mcf before general and administrative costs, overheads, tax and Additional Profits Tax may be analysed as follows:

(Amounts in US$/mcf)

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Gas price – industrial 7.91 11.�55

Gas price – power 2.39 2.�05

Weighted average price for gas 3.41 3.�37

Tariff (after allowance for the Ringmain Tariff) (0.57) (0.�55)

TPDC Profit Gas (0.50) (0.�49)

Net selling price 2.34 2.�33

Well maintenance and other operating costs (0.08) (0.�05)

Ringmain distribution pipeline (0.08) (0.�07)

Operating netback 2.18 2.�21

The operating netback for the quarter was US$2.�18/mcf (Q1 2008: US$2.�21/mcf), a decrease of 1% over Q1 2008.�

The decrease in operating netback compared to Q1 2008 is a consequence of the increase in the cost base on an mcf basis as a result of lower sales volume offsetting the increase in the average sales price.� The average sales price increased as a result of the favourable sales mix in the quarter with 19% of the sales volumes being derived from the industrial sector compared to 14% in Q1 2008.�

The operating netbacks are currently benefiting from the recovery of 75% of the Net Revenues as Cost Gas.�

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

G&A averaged approximately US$1.�0 million per month for Q1 2009, and was marginally lower than Q1 2008.� G&A per mcf increased to US$1.�58/mcf (Q1 2008: US$1.�34/mcf).� Whilst a large proportion of G&A is relatively fixed in nature and therefore declines on a mcf basis as volumes produced increase, costs have continued to be incurred on the negotiation of the power contracts, and on legal and arbitration proceedings against a third party contractor for breaches of contract that occurred during the drilling of the SS-10 well in 2007.� The main variances to Q1 2008 are summarized below:

Employee Costs

The increase in the level of employee costs from Q1 2008 is a consequence of the hiring of new local staff in Tanzania including the employment of an additional expat to oversee the next phase of the infrastructure expansion.�

Consultants

During Q1 2008 some consultancy costs were capitalized as they related to the seismic acquisition work undertaken on Exploration Area EA5 in Uganda.� This has resulted in the Q1 2009 consultancy costs being slightly higher.�

Office costs

The increase in office costs from Q1 2008 is a result of the expansion of the marketing development activities which led to the establish-ment of a second office location in Dar es Salaam.�

Marketing costs and legal fees

The decrease in marketing and legal fees compared to Q1 2008 is a consequence of the reduced costs incurred on the negotiation of long term power contracts and on applications to EWURA.�

Stock based compensation

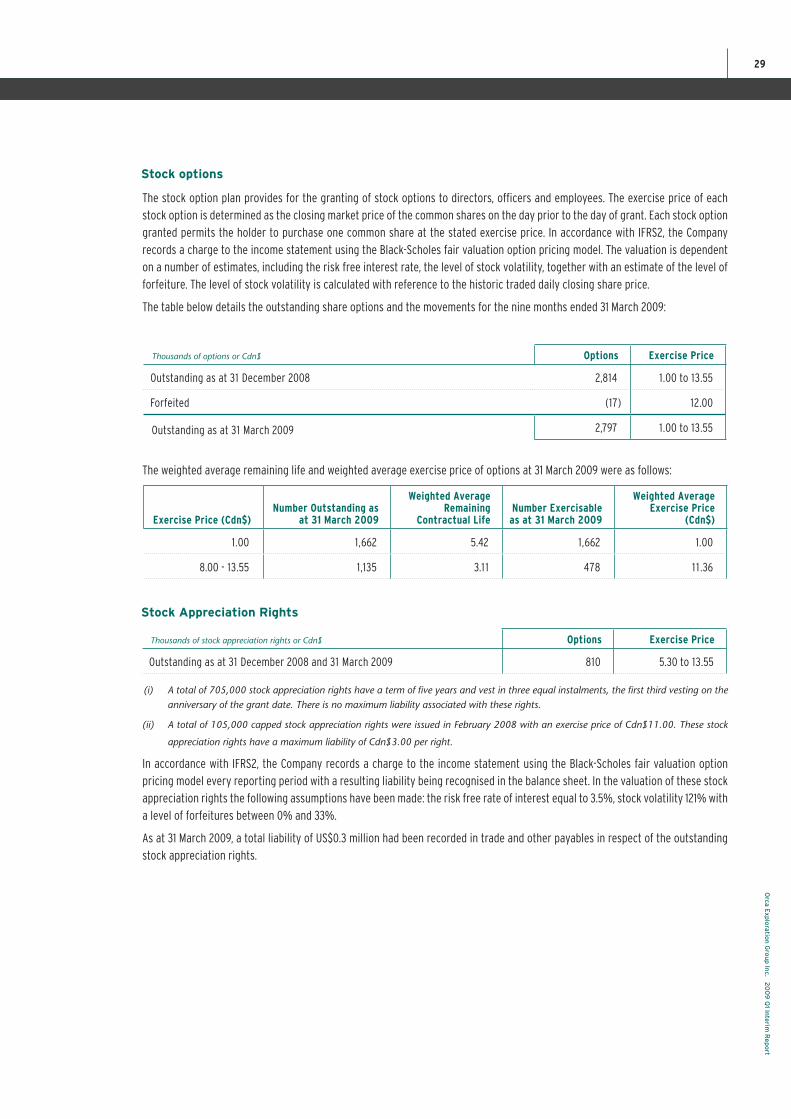

A total of 2,797,000 stock options were issued and outstanding at the end of Q1 2009 following the forfeiture of 17,000 options in March.� Of these options 1,662,000 were issued in 2004 and were fully expensed by the end of 2007.� The remaining 1,135,000 were issued to certain directors, officers and employees of the Company during 2007 with exercise prices between Cdn$8.�00 and Cdn$13.�55.� All of the stock options currently issued have been valued using the Black-Scholes option pricing model and vest over three years from the date of grant.� A total charge of US$0.�22 million was recorded for the 1,135,000 stock options that were issued in 2007.� The decline compared to Q1 2008 is a consequence of the IFRS-2 accounting treatment for the allocation of the costs which sees the majority of the costs being charged in the first two years from the date of grant.�

A total of 810,000 stock appreciation rights were in issue at the end of Q1 2009.� Of these 105,000 are capped with a maximum payout of Cdn$3 per right.� As stock appreciation rights are settled in cash they are re-valued at each reporting date using the Black-Scholes option pricing model.� As at 31 March 2009 the following assumptions were used; stock volatility 121%, a risk free interest rate of 3.�5% and a closing stock price of Cdn$3.�50.� The stock appreciation rights in issue have an exercise price ranging from Cdn$5.�30 to Cdn$13.�55.� All the uncapped stock appreciation rights have a 5 year term and vest in three equal annual instalments from the date of grant.� A charge of US$0.�17 million was recorded in Q1 2009 compared to a charge of US$0.�24 million in Q1 2008 in respect of these stock appreciation rights.� The decrease in the charge is the result of the decrease in the stock market price of the Company’s shares since 31 March 2008.�

In April 2007, 200,000 Class B treasury stock were awarded to a newly appointed officer.� These shares are held in escrow and vest to the officer in three equal annual instalments, the first third vesting in full on 7 April 2007.� A charge of US$70,000 was expensed in the quarter.� All of the 200,000 Class B shares are now fully vested.�

The total stock based compensation charges may be summarized as follows:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Stock options 226 503

Stock appreciation rights 166 241

Treasury stock 70 151

462 895

Capitalized – (255)

462 640

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

15

Additional Profits Tax

Under the terms of the PSA, in the event that all costs have been recovered with an annual return of 25% plus the percentage change in the United States Industrial Goods Producer Price Index, an Additional Profits Tax (“APT”) is payable.�

The Company provides for APT by forecasting the total APT payable as a proportion of the forecast Profit Gas over the term of PSA licence.� The effective APT rate has been calculated to be 20%.� Accordingly, US$88,000 has been netted off revenue for the quarter ended 31 March 2009 (Q1 2008: US$90,000).�

Management does not anticipate that any APT will be payable in 2009, as the forecast revenues will not be sufficient to recover the costs brought forward as inflated by 25% plus the percentage change in the United States Industrial Goods Producer Price Index and the forecast expenditures for 2009.� The actual APT that will be paid is dependent on the achieved value of the Additional Gas sales and the quantum and timing of the operating costs and capital expenditure programme.�

The APT can have a significant negative impact on the Songo Songo project economics as measured by the net present value of the cash flow streams.� Higher revenue in the initial years leads to a rapid payback of the project costs and consequently accelerates the payment of the APT that can account for up to 55% of the Company’s profit share.� Therefore, the terms of the PSA rewards the Company for taking higher risks by incurring capital expenditure in advance of revenue generation.�

NET FINANCING CHARGES

Interest income has fallen as a consequence of lower cash balances and a reduction in the rate of interest received.�

The relatively small loss on foreign exchange experienced in the quarter is a result of the stabilization of the USD against the Tanzanian Shilling.� Despite the gas sales price being denominated in US Dollars, the invoices are submitted in Tanzanian Schillings.� Therefore, there is an exchange exposure between the time that the invoices are submitted and the date that the payment is received.�

The movement in net financing charge is summarized in the table below:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Finance income

Interest income 16 45

16 45

Finance charges

Foreign exchange loss (34) (282)

(34) (282)

Net financing charge (18) (237)

TAXATION

Income Tax

Under the terms of the PSA with TPDC, the Company is liable for income tax in Tanzania at the corporate tax rate of 30%.� However, where income tax is payable, this is recovered from TPDC by deducting an amount from TPDC’s profit share.� This is reflected in the accounts by adjusting the Company’s revenue by the appropriate amount in the following quarter.�

As at 31 March 2009, there were temporary differences between the carrying value of the assets and liabilities for financial reporting purposes and the amounts used for taxation purposes under the Income Tax Act 2004.� Applying the 30% Tanzanian tax rate, the Company has recognised a deferred tax liability of US$6.�0 million which represents an additional charge of US$0.�5 million for the quarter.� This tax has no impact on cash flow until it becomes a current income tax at which point the tax is paid to the Commis-sioner of Taxes and recovered from TPDC’s share of Profit Gas in the following quarter.�

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

DEPLETION AND DEPRECIATION

The Natural Gas Properties are depleted using the unit of production method based on the production for the period as a percentage of the total future production from the Songo Songo proven reserves.� As at 31 December 2008 the proven reserves as evaluated by the independent reservoir engineers, McDaniel & Associates Consultants Ltd were 389.�4 Bcf on a life of licence basis.� This resulted in a depletion charge of US$0.�38/mcf in Q1 2009.� In Q1 2008 a depletion charge of US$0.�61/mcf was recorded based on proven reserves on a life of licence basis of 308.�6 Bcf.�

Non-Natural Gas Properties are depreciated as follows:

Leasehold improvements Over remaining life of the lease

Computer equipment 3 years

Vehicles 3 years

Fixtures and fittings 3 years

CARRYING VALUE OF ASSETS

Capitalised costs are periodically assessed to determine whether it is likely that such costs will be recovered in the future.� To the extent that these capitalised costs are unlikely to be recovered in the future, they are written off and charged to earnings.�

FUNDS GENERATED BY OPERATIONS

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

(Loss) /profit after taxation (168) (143)

Adjustments (1) 1,626 2,534

Funds from operations before working capital changes 1,458 2,391

Working capital adjustments 446 (1,555)

Net cash flows from operating activities 1,904 836

Net cash flows used in investing activities (2,624) (4,828)

Net cash flows used in financing activities (156) (2)

Net decrease in cash and cash equivalents (876) (3,994)

(1) Please refer to consolidated statement of cash flows for breakdown

The US$0.�9 million decline in cash and cash equivalents is a result of a US$1.�5 million increase in funds from operations before working capital changes being offset by US$1.�9 million of capital expenditure incurred during the quarter resulting in a US$0.�4 million reduction in cash.� A total of US$0.�15 million was incurred on the repurchase of shares under the normal course issuer bid and there was an overall net cash reduction of US$0.�3 million in working capital as a consequence of the US$5.�2 million reduction in trade and other payables being offset by a decrease of US$4.�9 million in trade and other receivables.�

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

17

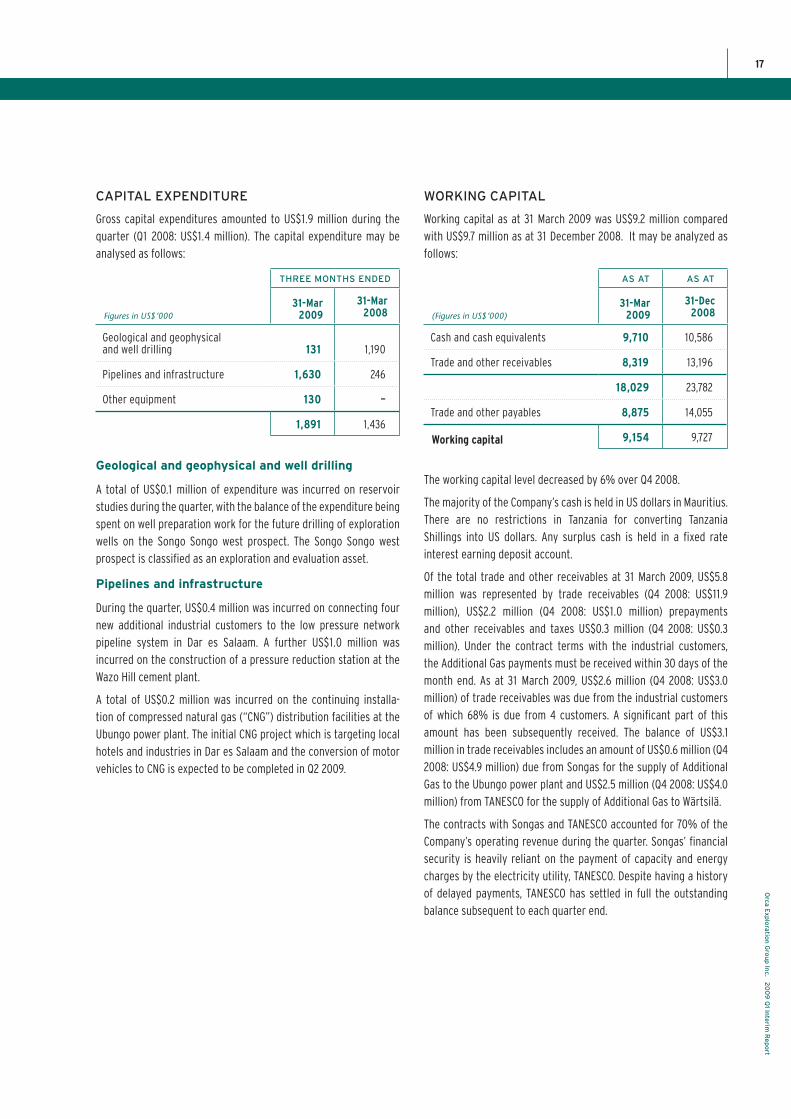

WORKING CAPITAL

Working capital as at 31 March 2009 was US$9.�2 million compared with US$9.�7 million as at 31 December 2008.� It may be analyzed as follows:

(Figures in US$’000)

AS AT AS AT

31-Mar 2009

31-Dec 2008

Cash and cash equivalents 9,710 10,586

Trade and other receivables 8,319 13,196

18,029 23,782

Trade and other payables 8,875 14,055

Working capital 9,154 9,727

The working capital level decreased by 6% over Q4 2008.�

The majority of the Company’s cash is held in US dollars in Mauritius.� There are no restrictions in Tanzania for converting Tanzania Shillings into US dollars.� Any surplus cash is held in a fixed rate interest earning deposit account.�

Of the total trade and other receivables at 31 March 2009, US$5.�8 million was represented by trade receivables (Q4 2008: US$11.�9 million), US$2.�2 million (Q4 2008: US$1.�0 million) prepayments and other receivables and taxes US$0.�3 million (Q4 2008: US$0.�3 million).� Under the contract terms with the industrial customers, the Additional Gas payments must be received within 30 days of the month end.� As at 31 March 2009, US$2.�6 million (Q4 2008: US$3.�0 million) of trade receivables was due from the industrial customers of which 68% is due from 4 customers.� A significant part of this amount has been subsequently received.� The balance of US$3.�1 million in trade receivables includes an amount of US$0.�6 million (Q4 2008: US$4.�9 million) due from Songas for the supply of Additional Gas to the Ubungo power plant and US$2.�5 million (Q4 2008: US$4.�0 million) from TANESCO for the supply of Additional Gas to Wärtsilä.�

The contracts with Songas and TANESCO accounted for 70% of the Company’s operating revenue during the quarter.� Songas’ financial security is heavily reliant on the payment of capacity and energy charges by the electricity utility, TANESCO.� Despite having a history of delayed payments, TANESCO has settled in full the outstanding balance subsequent to each quarter end.�

CAPITAL EXPENDITURE

Gross capital expenditures amounted to US$1.�9 million during the quarter (Q1 2008: US$1.�4 million).� The capital expenditure may be analysed as follows:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Geological and geophysical and well drilling 131 1,190

Pipelines and infrastructure 1,630 246

Other equipment 130 –

1,891 1,436

Geological and geophysical and well drilling

A total of US$0.�1 million of expenditure was incurred on reservoir studies during the quarter, with the balance of the expenditure being spent on well preparation work for the future drilling of exploration wells on the Songo Songo west prospect.� The Songo Songo west prospect is classified as an exploration and evaluation asset.�

Pipelines and infrastructure

During the quarter, US$0.�4 million was incurred on connecting four new additional industrial customers to the low pressure network pipeline system in Dar es Salaam.� A further US$1.�0 million was incurred on the construction of a pressure reduction station at the Wazo Hill cement plant.�

A total of US$0.�2 million was incurred on the continuing installa-tion of compressed natural gas (“CNG”) distribution facilities at the Ubungo power plant.� The initial CNG project which is targeting local hotels and industries in Dar es Salaam and the conversion of motor vehicles to CNG is expected to be completed in Q2 2009.�

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

CONTRACTUAL OBLIGATIONS AND COMMITTED CAPITAL INVESTMENT

Capital Investment

Re-rating of the Songas processing plant

Orca Exploration is committed to paying Songas US$0.�5 million on successful completion and operation of the gas processing facilities at 90 MMscfd together with a further US$0.�5 million on the first anniversary of the successful completion of the project.� The gas processing plant was re-rated from 70 MMscfd to 90 MMscfd by Lloyds Register in January 2009.� The re-rating was approved by Songas in Q1 2009, but the plant has not yet been operated above 70 MMscfd.�

Wazo Hill cement plant

Orca Exploration signed a five year contract with TPCC, a subsidiary of Heidelberg Cement, for the supply of gas to a new US$100 million kiln at its Wazo Hill plant in Dar es Salaam.� In order to honour this contract, Orca Exploration committed to install a pressure reduction station at Wazo Hill, a total of US$1.�0 million has been incurred on this during the quarter.� It is estimated that US$0.�4 million will be required to complete the project.�

Compressed natural gas

In Q3 2008, Orca Exploration ordered US$2.�5 million of CNG facilities, consisting of a compressor, a vehicle dispenser and two trailer filling facilities to deliver 0.�7 MMscfd of CNG to industrial customers in Dar es Salaam.� The facilities are expected to be operational during Q2 2009.� A total of US$2.�5 million had been spent on this project by the end of Q1 2009.� It is estimated that an additional US$0.�3 million will be required to complete the project.�

Funding

Management forecasts that the Company will be able to meet its 2009 US$11.�0 million capital expenditure program through the use of existing cash balances and self-generated cash flows.� The Company currently has no bank borrowings and there is scope for utilising debt funding once the longer term contracts for the supply of gas to the power sector are in place.�

Contractual Obligations

Protected Gas

Under the terms of the original gas agreement for the Songo Songo project (“Gas Agreement”), in the event that there is a shortfall/insufficiency in Protected Gas as a consequence of the sale of Additional Gas, then the Company is liable to pay the difference between the price of Protected Gas (US$0.�55/Mmbtu) and the price of an alternative feedstock multiplied by the volumes of Protected Gas up to a maximum of the volume of Additional Gas sold (25.�7 Bcf as at 31 March 2009).�

The Gas Agreement has been amended by an initialled Amended and Restated Gas Agreement (“ARGA”).� The ARGA provides clarification of the Protected Gas volumes and removes all terms dealing with the security of the Protected Gas and the consequences of any in-sufficiency to a new Insufficiency Agreement (“IA”).� The IA specifies terms under which Songas may demand cash security in order to keep them whole in the event of a Protected Gas insufficiency.� Once the Insufficiency Agreement is signed, it will govern the basis for determining security.� Under the provisional terms of the IA, when it is calculated that funding is required, the Company shall fund an escrow account at a rate of US$2/Mmbtu on all industrial Additional Gas sales out of its and TPDC share of revenue, and TANESCO shall contribute the same amount on Additional Gas sales to the power sector.� The funds provide security for Songas in the event of an in-sufficiency of Protected Gas.� The Company is actively monitoring the reservoir and does not anticipate that a liability will occur in this respect.�

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

19

Back in

TPDC has indicated that they wish to exercise their right to ‘back in’ to the field development by contributing 20% of the costs of the future wells including SS-10 in return for a 20% increase in the profit share percentage for the production emanating from these wells.� The implications and workings of the ‘back in’ are still to be discussed in detail with TPDC and there may be the need for reserve modifications once these discussions are concluded.� For the purpose of the reserves certification, it has been assumed that they will ‘back in’ for 20% and this is reflected in the Company’s net reserve position.� However, the financial statements do not take account of any reimbursement for the SS-10 capital expenditure, pending the finalisation of the terms of the ‘back in’.�

Operating leases

The Company has entered into two five year rental agreements that expire on 30 November 2012 and 30 November 2013 respectively at a cost of approximately US$0.�2 million per annum for the use of offices in Dar es Salaam.�

Off Balance Sheet Arrangements

As at 31 March 2009, the Company had no off-balance sheet arrange-ments.�

Related Party Transactions

One of the non executive Directors is a partner at a law firm.� During the quarter, the Company incurred US$37,500 to this firm for services provided on legal services.� The transactions with this related party was made at the exchange amount.�

Shareholders’ Equity and Outstanding Share Data

Number of shares (‘000)

AS AT AS AT

31-Mar 2009

31-Dec 2008

Shares outstanding

Class A shares 1,751 1,751

Class B shares 27,788 27,863

29,539 29,614

Convertible securities

Stock options 2,797 2,814

Diluted Class A and Class B shares 32,336 32,428

Weighted average

Class A and Class B shares 29,587 29,614

Convertible securities

Stock options 1,095 1,425

Weighted average diluted Class A and Class B shares 30,682 31,039

Shares outstanding

No stock options were issued or exercised during the quarter.� A total of 17,000 options were cancelled by way of forfeiture during the quarter.�

As at 28 May 2009, there were a total of 1,751,195 Class A shares and 27,788,428 Class B shares outstanding.�

During Q1 2009, 75,000 Class B shares were purchased pursuant to a normal course issuer bid.�

Orca Exploration Group Inc.

MANAGEMENT’S DISCUSSION & ANALYSIS

SUMMARY QUARTERLY RESULTS

The following is a summary of the results for the Company for the last eight quarters:

(Figures in US$’000 except where otherwise stated)

2009 2008 2007

Q1 Q4 Q3 Q2 Q1 Q4 Q3 Q2

Financial

Revenue 4,443 6,371 7,301 4,826 5,284 5,562 6,363 3,021

(Loss)/profit after taxation (168) 12 816 (10,208) (143) 284 1,942 (609)

Operating netback (US$/mcf) 2.18 2.�32 2.�79 3.�44 2.�21 2.�27 2.�30 2.�79

Working capital 9,154 9,727 8,705 6,094 8,297 7,299 20,939 (3,050)

Shareholders’ equity 64,684 64,712 64,142 62,824 72,053 71,544 70,996 38,291

(Loss)/profit per share – basic and diluted (US$) (0.01) 0.�00 0.�03 (0.�35) 0.�00 0.�01 0.�07 (0.�02)

Capital expenditures

Geological and geophysical and well drilling 131 (987) 419 2,851 1,190 16,323 10,426 13,723

Pipeline and infrastructure 1,630 2,217 705 979 246 469 314 1,205

Power development – 13 4 21 – 4 7 26

Other equipment 130 31 51 – – – 108 35

Operating

Additional Gas sold – industrial (MMscf) 360 392 425 336 322 364 442 397

Additional Gas sold – power (MMscf) 1,570 2,149 2,097 956 1,983 2,152 1,974 745

Average price per mcf – industrial (US$) 7.91 10.�08 13.�29 12.�97 11.�55 11.�08 9.�58 8.�61

Average price per mcf – power (US$) 2.39 2.�39 2.�41 2.�93 2.�05 2.�19 2.�19 2.�17

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

21

Orca Exploration Group Inc.

CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

Consolidated Income Statements (unaudited)

(thousands of US dollars except per share amounts)

THREE MONTHS ENDED

NOTE31-Mar

200931-Mar

2008

Revenue 4,443 5,284

Cost of sales

Production and distribution expenses (305) (276)

Depletion expense (753) (1,406)

3,385 3,602

Administrative expenses (3,045) (3,095)

Net financing charges (18) (237)

Profit before taxation 322 270

Taxation 1 (490) (413)

(Loss) after taxation (168) (143)

(Loss) per share

Basic and diluted (US$) (0.01) (0.�00) See accompanying notes to the interim consolidated financial statements.

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

23

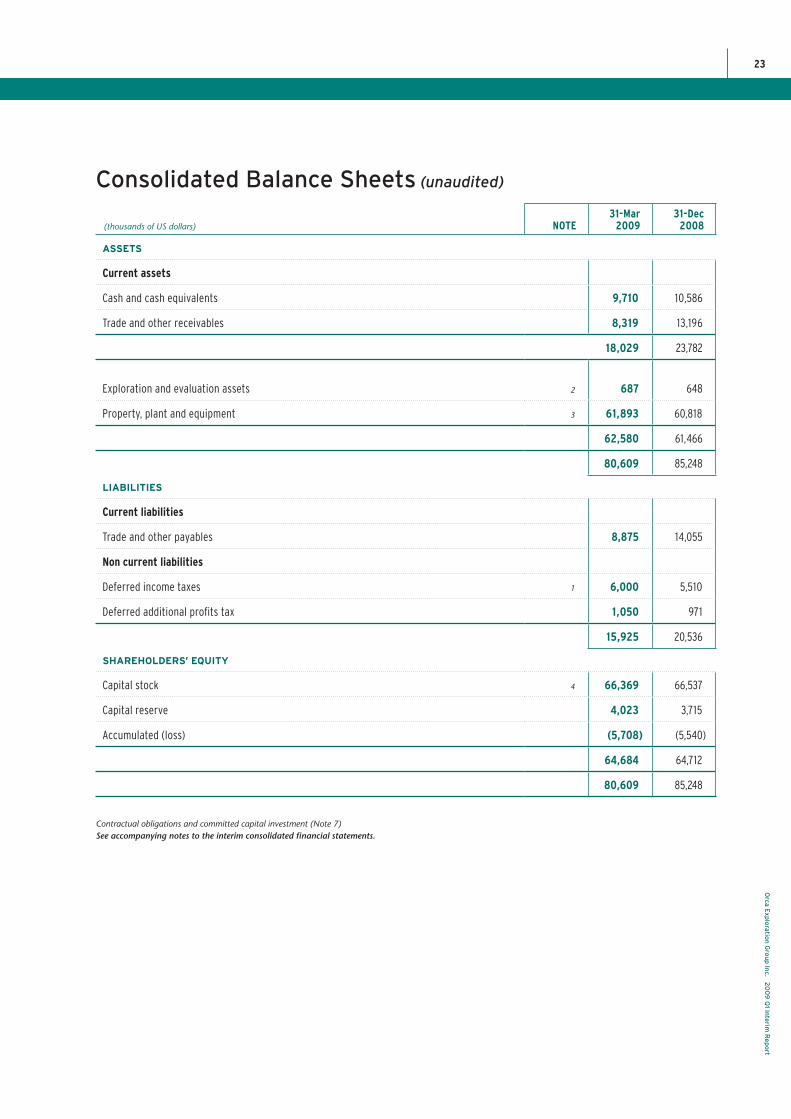

Consolidated Balance Sheets (unaudited)

(thousands of US dollars) NOTE31-Mar

200931-Dec

2008

ASSETS

Current assets

Cash and cash equivalents 9,710 10,586

Trade and other receivables 8,319 13,196

18,029 23,782

Exploration and evaluation assets 2 687 648

Property, plant and equipment 3 61,893 60,818

62,580 61,466

80,609 85,248

LIABILITIES

Current liabilities

Trade and other payables 8,875 14,055

Non current liabilities

Deferred income taxes 1 6,000 5,510

Deferred additional profits tax 1,050 971

15,925 20,536

SHAREHOLDERS’ EQUITY

Capital stock 4 66,369 66,537

Capital reserve 4,023 3,715

Accumulated (loss) (5,708) (5,540)

64,684 64,712

80,609 85,248

Contractual obligations and committed capital investment (Note 7) See accompanying notes to the interim consolidated financial statements.

Orca Exploration Group Inc.

CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

Consolidated Statements of Cash Flows (unaudited)

(thousands of US dollars)

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

CASH FLOWS FROM OPERATING ACTIVITIES

(Loss) after taxation (168) (143)

Adjustment for :

Depletion and depreciation 777 1,422

Stock-based compensation 296 654

Deferred income taxes 490 413

Deferred additional profits tax 79 90

Interest income (16) (45)

1,458 2,391

Decrease in trade and other receivables 4,877 939

Decrease in trade and other payables (4,431) (2,494)

Net cash flows from operating activities 1,904 836

CASH FLOWS USED IN INVESTING ACTIVITIES

Exploration and evaluation expenditures (39) (419)

Property, plant and equipment expenditures (1,852) (1,017)

Interest income 16 45

Decrease in trade and other payables (749) (3,437)

Net cash used in investing activities (2,624) (4,828)

CASH FLOWS USED IN FINANCING ACTIVITIES

Normal course issuer bid (156) (2)

Net cash used in financing activities (156) (2)

Decrease in cash and cash equivalents (876) (3,994)

Cash and cash equivalents at the beginning of the period 10,586 16,515

Cash and cash equivalents at the end of the period 9,710 12,521

See accompanying notes to the interim consolidated financial statements.

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

25

Statement of Changes in Shareholders’ Equity (unaudited)

(thousands of US dollars) Capital stock Capital reserveAccumulated

Income/(loss) Total

Balance as at 1 January 2008 66,538 1,023 3,983 71,544

Stock-based compensation – 654 – 654

Normal course issuer bid (1) (1) – (2)

Loss for the period – – (143) (143)

Balance as at 31 March 2008 66,537 1,676 3,840 72,053

(thousands of US dollars) Capital stock Capital reserveAccumulated

Income/(loss) Total

Note 4

Balance as at 1 January 2009 66,537 3,715 (5,540) 64,712

Stock-based compensation – 296 – 296

Normal course issuer bid (168) 12 – (156)

Loss for the period – – (168) (168)

Balance as at 31 March 2009 66,369 4,023 (5,708) 64,684

See accompanying notes to the interim consolidated financial statements.

Orca Exploration Group Inc.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Notes to the Consolidated Financial Statements (unaudited)

Basis of preparation

The interim consolidated financial statements are measured and presented in US dollars as the main operating cash flows are linked to this currency through the commodity price.�

The same accounting policies and methods of computation have been followed as the audited consolidated financial statements at 31 December 2008.� The interim consolidated financial statements for the three months ended 31 March 2009 should be read in conjunction with the audited consolidated financial statements and related notes for the year ended 31 December 2008.�

Management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period.� Actual results could differ from these estimates.�

Statement of compliance

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and interpretations issued by the Standing Interpretations Committee of the IASB.� These principles differ in certain respects from those in Canada as described in note 5.�

1 TAXATION

Under the terms of the Production Sharing Agreement with TPDC, the Company is liable to pay income tax at the corporate rate of 30% on profits generated in Tanzania.� The amount paid is then recovered in full from TPDC by adjusting their share of profit gas.�

The tax charge is as follows:

Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Current tax – –

Deferred tax 490 413

490 413

Tax Rate Reconciliation Figures in US$’000

THREE MONTHS ENDED

31-Mar 2009

31-Mar 2008

Profit before taxation 322 270

Provision for income tax calculated at the statutory rate of 30% 97 81

Add/(deduct) the tax effect of non-deductible income tax items:

Administrative and operating expenses 241 160

Stock based compensation 138 145

Permanent differences 14 27

490 413

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

27

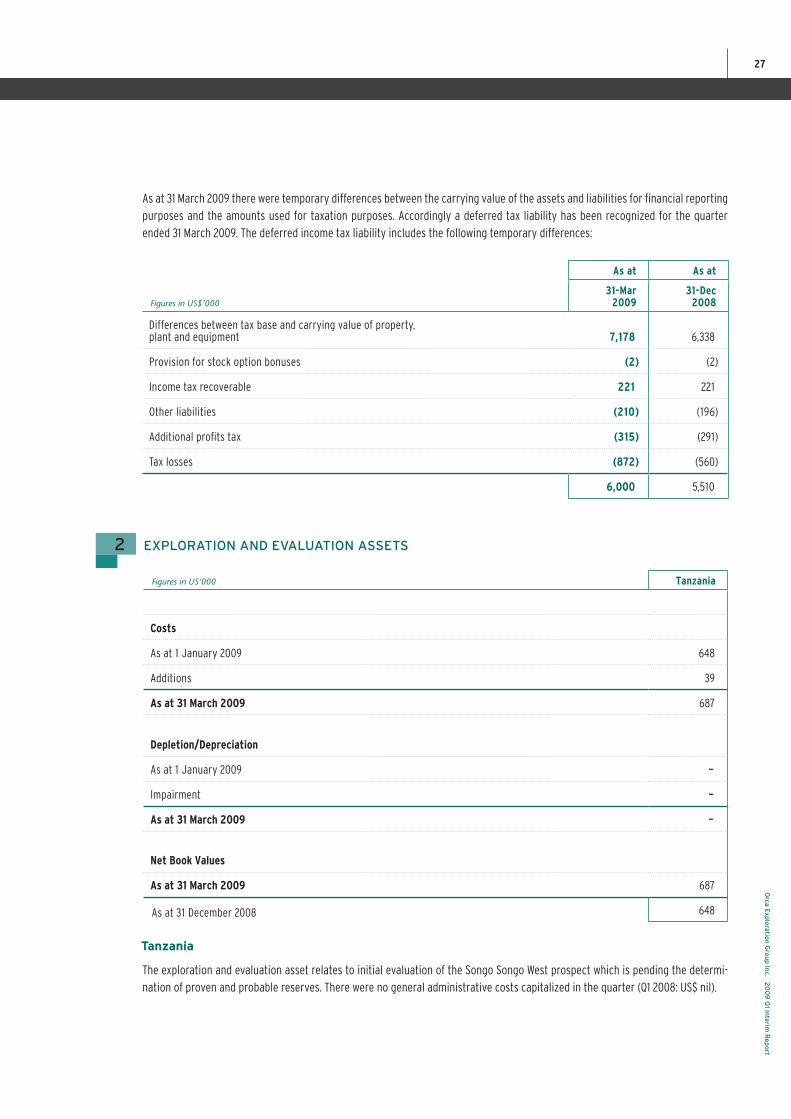

As at 31 March 2009 there were temporary differences between the carrying value of the assets and liabilities for financial reporting purposes and the amounts used for taxation purposes.� Accordingly a deferred tax liability has been recognized for the quarter ended 31 March 2009.� The deferred income tax liability includes the following temporary differences:

Figures in US$’000

As at As at

31-Mar 2009

31-Dec 2008

Differences between tax base and carrying value of property, plant and equipment 7,178 6,338

Provision for stock option bonuses (2) (2)

Income tax recoverable 221 221

Other liabilities (210) (196)

Additional profits tax (315) (291)

Tax losses (872) (560)

6,000 5,510

2 EXPLORATION AND EVALUATION ASSETS

Figures in US’000 Tanzania

Costs

As at 1 January 2009 648

Additions 39

As at 31 March 2009 687

Depletion/Depreciation

As at 1 January 2009 –

Impairment –

As at 31 March 2009 –

Net Book Values

As at 31 March 2009 687

As at 31 December 2008 648

Tanzania

The exploration and evaluation asset relates to initial evaluation of the Songo Songo West prospect which is pending the determi-nation of proven and probable reserves.� There were no general administrative costs capitalized in the quarter (Q1 2008: US$ nil).�

Orca Exploration Group Inc.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

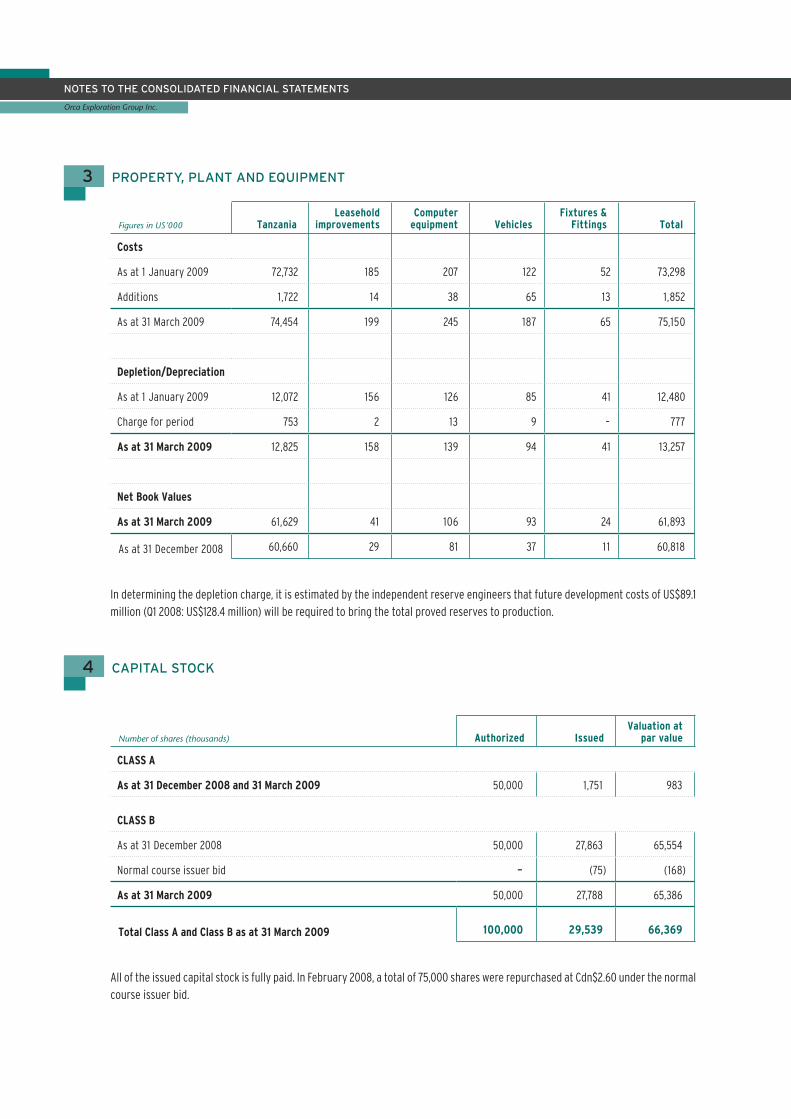

3 PROPERTY, PLANT AND EQUIPMENT

Figures in US’000 TanzaniaLeasehold

improvementsComputer

equipment VehiclesFixtures &

Fittings Total

Costs

As at 1 January 2009 72,732 185 207 122 52 73,298

Additions 1,722 14 38 65 13 1,852

As at 31 March 2009 74,454 199 245 187 65 75,150

Depletion/Depreciation

As at 1 January 2009 12,072 156 126 85 41 12,480

Charge for period 753 2 13 9 – 777

As at 31 March 2009 12,825 158 139 94 41 13,257

Net Book Values

As at 31 March 2009 61,629 41 106 93 24 61,893

As at 31 December 2008 60,660 29 81 37 1 1 60,818

In determining the depletion charge, it is estimated by the independent reserve engineers that future development costs of US$89.�1 million (Q1 2008: US$128.�4 million) will be required to bring the total proved reserves to production.�

4 CAPITAL STOCK

Number of shares (thousands) Authorized IssuedValuation at

par value

CLASS A

As at 31 December 2008 and 31 March 2009 50,000 1,751 983

CLASS B

As at 31 December 2008 50,000 27,863 65,554

Normal course issuer bid – (75) (168)

As at 31 March 2009 50,000 27,788 65,386

Total Class A and Class B as at 31 March 2009 100,000 29,539 66,369

All of the issued capital stock is fully paid.� In February 2008, a total of 75,000 shares were repurchased at Cdn$2.�60 under the normal course issuer bid.�

Orca E

xplo

ration

Gro

up

Inc. 2

00

9 Q

1 Inte

rim R

ep

ort

29

Stock options