Q1 Office Bulletin 2012 - Property Price Reports 5,000 10,000 15,000 20,000 25,000 30,000 35,000...

8

CBRE © 2012, CBRE www.cbre.ie Q1 2012 Dublin Office OVERALL COMMENTARY In total, 24,097m 2 of office lettings were signed in Dublin in the first three months of 2012. This represents a 51% decrease in letting activity in the capital compared to the same quarter last year and a decline of some 32% compared to the most recent quarter, Q4 2011. Total take-up of only 5,909m 2 was signed in the suburbs in Q1 2012, which represents a decline of more than 50% on both an annual and quarterly measure. The deterioration in the volume of lettings signed in Dublin in the first quarter of the year is not surprising considering the length of time it is taking to conclude negotiations at present and the fact that many corporate occupiers are curtailing their expansion and relocation requirements until such time as the economic climate is more certain. Nevertheless, several office lettings are in negotiations at present and there are a number of outstanding requirements for office accommodation in the capital which is likely to boost take-up in subsequent quarters. Indeed, overall demand for office accommodation in the capital was up 71% quarter-on-quarter as a result of some large requirements that emerged during Q1 2012. Our research indicates that the quantum of office letting activity in the first three months of the year typically accounts for approximately 20% of annual take-up in the market, which suggests that our forecast of 130,000m 2 of letting activity being achieved in Dublin in 2012 is realistic. More than 75% of the office lettings signed in Dublin during Q1 2012 were located in the city centre, with the Dublin 2/4 district accounting for more than half of the city centre letting activity. Large lettings in the Eastpoint development in Dublin 1 to Arvata and Google boosted the dominance of the Dublin 1/3/7 office district in terms of take-up in the first three months of 2012. These two lettings between them accounted for just less than 30% of total letting activity in Dublin in the three month period. The vacancy rate fell slightly in Q1 2012 to 22.9% with approximately 828,000m 2 of office accommodation being officially marketed to let in the Dublin market at the end of the first quarter of this year. An analysis of the Top 10 largest letting transactions in the quarter reveals net absorption of almost 70%. Four of the ten largest lettings in Q1 comprised companies expanding to larger premises; one was a brand new requirement while the remainder were companies relocating to larger premises. There were 3 office investments sold in the capital during Q1, bringing the total investment spend on offices in Dublin during the quarter to €18.5 million, equating to 92% of the total investment spend in the city in the period. Prime rents in the Dublin office market at the end of Q1 2012 were €296 per square metre and are now expected to stabilise at this level although there is expected to be further downward pressure on rents for non- prime buildings over the course of the year. Meanwhile, prime office yields in Dublin are now approximately 7.25%. Dublin Gross Office Take-Up Q1 2010 – Q1 2012 Quick Stats Q1 Hot Topics • Office take-up in Dublin in the first quarter of 2012 reached 24,097m 2 , representing a decline of 51% compared to the same quarter last year • There were 32 individual lettings signed in the quarter with most comprising relatively small transactions • The vacancy rate in the capital stands at 22.9% at the end of Q1 having fallen slightly in the first three months of 2012 • Prime headline quoting rents in Dublin city centre are now approximately €296 per m 2 and are expected to stabilise at this level • More than 75% of lettings signed in Dublin in Q1 2012 were in the city centre • There was a notable 71% increase in demand for new office premises in the capital quarter-on-quarter as a result of a number of new requirements being enacted Change from previous quarter Availability Take-Up Investment Prime Rents Yields Demand Source: CBRE 0 10,000 20,000 30,000 40,000 50,000 60,000 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 City Centre Suburbs Sq.M.

Transcript of Q1 Office Bulletin 2012 - Property Price Reports 5,000 10,000 15,000 20,000 25,000 30,000 35,000...

CBRE

© 2012, CBRE

www.cbre.ie Q1 2012

Dublin Office

Overall COmmentary In total, 24,097m2 of office lettings were signed in Dublin in the first three months of 2012. This represents a 51% decrease in letting activity in the capital compared to the same quarter last year and a decline of some 32% compared to the most recent quarter, Q4 2011. Total take-up of only 5,909m2 was signed in the suburbs in Q1 2012, which represents a decline of more than 50% on both an annual and quarterly measure. The deterioration in the volume of lettings signed in Dublin in the first quarter of the year is not surprising considering the length of time it is taking to conclude negotiations at present and the fact that many corporate occupiers are curtailing their expansion and relocation requirements until such time as the economic climate is more certain. Nevertheless, several office lettings are in negotiations at present and there are a number of outstanding requirements for office accommodation in the capital which is likely to boost take-up in subsequent quarters. Indeed, overall demand for office accommodation in the capital was up 71% quarter-on-quarter as a result of some large requirements that emerged during Q1 2012.

Our research indicates that the quantum of office letting activity in the first three months of the year typically accounts for approximately 20% of annual take-up in the market, which suggests that our forecast of 130,000m2 of letting activity being achieved in Dublin in 2012 is realistic. More than 75% of the office lettings signed in Dublin during Q1 2012 were located in the city centre, with the Dublin 2/4 district accounting for more than half of the city centre letting activity. Large lettings in the Eastpoint development in Dublin 1 to Arvata and Google boosted the dominance of the Dublin 1/3/7 office district in terms of take-up in the first three months of 2012. These two lettings between them accounted for just less than 30% of total letting activity in Dublin in the three month period.

The vacancy rate fell slightly in Q1 2012 to 22.9% with approximately 828,000m2 of office accommodation being officially marketed to let in the Dublin market at the end of the first quarter of this year. An analysis of the Top 10 largest letting transactions in the quarter reveals net absorption of almost 70%. Four of the ten largest lettings in Q1 comprised companies expanding to larger premises; one was a brand new requirement while the remainder were companies relocating to larger premises.

There were 3 office investments sold in the capital during Q1, bringing the total investment spend on offices in Dublin during the quarter to €18.5 million, equating to 92% of the total investment spend in the city in the period.

Prime rents in the Dublin office market at the end of Q1 2012 were €296 per square metre and are now expected to stabilise at this level although there is expected to be further downward pressure on rents for non-prime buildings over the course of the year. Meanwhile, prime office yields in Dublin are now approximately 7.25%.

Dublin Gross Office take-Up Q1 2010 – Q1 2012

Quick Stats Q1

Hot Topics

• Office take-up in Dublin in the first quarter of 2012 reached 24,097m2, representing a decline of 51% compared to the same quarter last year

• There were 32 individual lettings signed in the quarter with most comprising relatively small transactions

• The vacancy rate in the capital stands at 22.9% at the end of Q1 having fallen slightly in the first three months of 2012

• Prime headline quoting rents in Dublin city centre are now approximately €296 per m2 and are expected to stabilise at this level

• More than 75% of lettings signed in Dublin in Q1 2012 were in the city centre

• There was a notable 71% increase in demand for new office premises in the capital quarter-on-quarter as a result of a number of new requirements being enacted

Change from previous quarter

Availability

Take-Up

Investment

Prime Rents

Yields

Demand

Source: CBRE

0

10,000

20,000

30,000

40,000

50,000

60,000

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012

City Centre Suburbs

Sq.M

.

0

10,000

20,000

30,000

40,000

50,000

60,000

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012

Sq M

-

50,000

100,000

150,000

200,000

250,000

300,000

Dublin 2/4 Dublin 1/3/7 WestSuburbs

Dublin 6/8 IFSC

Sq M

Grade A Secondary In Need of Significant Refurbishment Georgian

SouthSuburbs

NorthSuburbs

Dublin Office availability Q1 2012

37%

17%

28%

14%

4%

Business Services

Financial Services

Computers/Hi-Tech

Manufacturing, Industrial& Energy

Consumer Services & Leisure

Dublin Gross Office take-up by Occupier type Q1 2012

Dublin Q1 Office take-Up 2007-2012

Q1

2012

Page 2

© 2012, CBRE

mar

ketv

iew

Dub

lin O

ffice There were 32 office lettings, extending to 24,097m2

signed in the Dublin office market during Q1 2012. 18,188m2 or 75.5% of overall office take-up in Q1 occurred in the city centre while the suburbs accounted for the remaining 24.5% or 5,909m2 of lettings signed in Dublin in the period.

14 of the 32 lettings signed in Dublin in the first three months of 2012 were to Irish companies accounting for 9,096m2 or 38% of letting activity between them; 11 lettings totalling 9,668m2 were to US companies which accounted for 40% of office take-up in Dublin during Q1 while there were 6 lettings totalling 5,148m2 equating to 21% of Q1 take-up to companies from other jurisdictions. There was only one letting signed in the city to a UK company accounting for 185m2 or 1.0% of take-up in the quarter.

Our research indicates that 32% of the office take-up in Q1 comprised lettings of smaller than 929m2 in size. 12% of the quantum of accommodation let in the period comprised lettings extending to between 929m2 and 1,858m2 in size while 57% of the quantum of office accommodation let occurred in lettings of between 1,858m2 and 4,645m2 in size. There were no lettings of more than 4,645m2 (50,000 sq ft) signed in Dublin in the first quarter of the year. Some of the more significant office lettings signed in Dublin during the period include the letting of 4,088m2 to Arvato at Blocks J and K at Eastpoint Business Park in Dublin 1; the letting of 2,959m2 to Google at Block P at Eastpoint and the letting of 2,539m2 to AIB at Hume House in Dublin 4.

The overall vacancy rate in the capital fell slightly to 22.9% in Q1.

Although there is a complete lack of new office development in Dublin, older office buildings which are being vacated in favour of newer alternatives continue to be added back into the vacant stock. In addition, many companies are attempting to sublet or assign excess accommodation at present and this is maintaining the overall level of availability at relatively high levels despite the underlying level of letting activity. According to our research, there was approximately 828,000m2 of office accommodation being marketed to let in the capital at the end of the first quarter of 2012.

Demand for office space in Dublin rose significantly in Q1 compared to the previous quarter as a result of some new requirements emerging. There was approximately 181,000m2 of outstanding requirements for office accommodation in Dublin at then end of the quarter, with almost 54% expressing a preference to locate in Dublin city centre.

Tenants in the business services sector accounted for the greatest proportion of office lettings signed in Dublin during Q1 2012, accounting for 37% of lettings in the capital in the period. The computers and high tech sector accounted for 28% of letting activity in the period. Tenants in the financial services sector accounted for 17% of lettings signed in Dublin during Q1 while manufacturing, industry and energy tenants accounted for a further 14% of letting activity in Dublin in the period. Interestingly, the public sector and professional companies signed no office lettings in Dublin in the first three months of 2012.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012

Sq M

Dublin 1/3/7 Dublin 2/4 Dublin 6/8 IFSC

45%

22%

30%

1% 2%

Business Services

Financial Services

Computers/Hi-Tech

Manufacturing, Industrial& Energy

Consumer Services & Leisure

City Centre take-up Q1 2012 by tenant Category

200

300

400

500

600

700

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q3 2

012

Q4 2

012

Q1 2

012

673

296

Prime Headline Dublin Office rents Q1 2008 – Q1 2012

CIty Centre marKet

Take-up of some 18,188m2 was achieved in Dublin city centre during the first quarter of 2012, compared to 36,332m2 of lettings in this district in same quarter last year. There were 20 individual lettings signed in Dublin city centre in the three month period, 11 of which were located in the Dublin 2/4 district. In quantum terms, just over half of the office take-up signed in Dublin city centre during Q1 2012 was located in the Dublin 2 and Dublin 4 postcodes. Dublin 1/3/7 accounted for over 40% of city centre take-up in the quarter as a result of the two largest office lettings in the city in Q1 being located in Eastpoint in Dublin 1.

At the end of the quarter, the vacancy rate in Dublin city centre stood at 23%. There was approximately 488,000m2 of office accommodation being marketed to let in the city centre at the end of Q1, of which approximately 56% was located in the Dublin 2/4 postcode. Over 60% of all office accommodation being marketed to let in Dublin city centre is classified as Grade A although there are over 155 different instances of vacancy which suggests that most of this accommodation is relatively small.

According to our research, there is demand for just under 100,000m2 of office accommodation in Dublin city centre at the end of Q1 2012. This equates to just less than 54% of total outstanding requirements for office accommodation in the capital.

Business services tenants accounted for 45% of city centre take-up during Q1 2012 with computers/hi-tech occupiers and financial services companies accounting for a further 30% and 22% of city centre letting activity in the period respectively.

Prime quoting headline office rents in Dublin city centre stabilised at €296 per square metre during Q1, although rents in non-prime buildings are likely to continue to come under further pressure.

Q1 2012

Page 3

© 2012, CBRE

City Centre Office take-Up Q1 2010 – Q1 2012

marketv

iew D

ublin O

ffice

Headlines

• The city centre accounted for more than 75% of overall take-up in Dublin in Q1

• The city centre vacancy rate was 23% at the end of the first quarter while the vacancy rate in Dublin 2/4 was 16.8%

• The two largest office lettings in Dublin in Q1 were located in the Dublin 1/3/7 district in the city centre

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Q1

20

10

Q2

20

10

Q3

20

10

Q4

20

10

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

11

Q1

20

12

Sq M

North Suburbs South Suburbs West Suburbs

0

5,000

10,000

15,000

20,000

25,000

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012

Sq M

Suburban Q1 Office take-up 2007 - 2012

14%

21%54%

11%

Business Services

Computers/Hi-Tech

Manufacturing, Industrial& Energy

Consumer Services & Leisure

Suburban Office take-up by tenant Category Q1 2012

Suburban Office take-up Q1 2010 – Q1 2012

Q1

2012

Page 4

© 2012, CBRE

mar

ketv

iew

Dub

lin O

ffice SUBUrBan marKet

There were only 5,909m2 of lettings signed in the Dublin suburban office market in Q1 2012, which is a disappointing level of letting activity for this submarket. The south suburbs accounted for 52% of overall suburban office take-up in Dublin in the three month period. The west suburbs accounted for a further 25% of take-up in Q1 while the north suburbs accounted for the remaining 23%.

The most significant lettings signed in the suburbs in the first quarter of the year included the letting of 1,966m2 to Mylan in Newenham House in the north suburbs and the letting of 681m2 at Maple House in the south suburbs to Interaction.

There were 12 office lettings signed in the Dublin suburbs in Q1 2012. Business services tenants accounted for 14% of suburban take-up in Q1, while consumer services tenants accounted for 11% of suburban take-up in the quarter. Manufacturing, industry and energy tenants accounted for more than half of suburban take-up in the period, while computers/hi tech companies accounted for a further 21% of letting activity in the suburbs during Q1. There were no lettings to financial tenants or to public sector tenants in the suburbs in the first three months of 2012.

At the end of Q1 2012, total vacant office stock in the Dublin suburbs stood at approximately 340,000m2. Total vacant stock in the south suburbs stood at almost 147,000m2 in Q1 2012, bringing the vacancy rate there to 14.5%, compared to 14.0% at the end of Q4 2011. The vacancy rate in the suburbs overall also increased slightly quarter-on-quarter to 23.2%.

Demand for suburban office accommodation stood at over 83,000m2 as of the end of Q1 2012, compared to 27,000m2 the previous quarter following a number of large requirements being announced. Prime headline quoting rents for office accommodation in the south suburbs were in the order of €172 per square metre at the end of Q1 compared to €151 per square metre in the north suburbs and €134.50 per square metre in the west suburbs of the city.

Headlines

• Suburban take-up accounted for less than 25% of overall Dublin office letting activity in Q1

• Suburban take-up down more than 50% on a quarterly and annual basis in Q1 2012

• Strong increase in demand for suburban office accommodation quarter-on-quarter

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Q2

2002

Q4

2002

Q2

2003

Q4

2003

Q2

2004

Q4

2004

Q2

2005

Q4

2005

Q2

2006

Q4

2006

Q2

2007

Q4

2007

Q2

2008

Q4

2008

Q2

2009

Q4

2009

Q2

2010

Q4

2010

Q2

2011

Q4

2011

(000

's) S

quar

e M

etre

s

Western Europe CEE

160

180

200

220

240

260

280

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

200

= Ja

nuar

y 20

00

-15%

-10%

-5%

0%

5%

10%

15%% Change pa Nominal Terms Index

eU Office rent Index Q4 2002 – Q4 2011

0

5

10

15

20

25

30

35

40

45

50

Kyiv

St P

eter

sbur

g

Sofia

Belg

rade

War

saw

Zagr

eb

Buch

ares

t

Brat

isla

va

Dub

lin

Buda

pest

Fran

kfur

t

Mos

cow

Prag

ue

Barc

elon

a

Am

ster

dam

Mad

rid

Mila

n

Dus

seld

orf

Lisb

on

Brus

sels

Ham

burg

Berl

in

Vie

nna

Lond

on C

ity

Mun

ich

Pari

s

Cop

enha

gen

Lond

on W

est

End

%

Development Pipeline to end 2013 Vacancy Rate Q4 2011

european vacancy & Supply Pipelines Q4 2011

eUrOPean OFFICe marKet

Total office take-up across Europe in the last quarter of 2011 was slightly up on the previous quarter and broadly stable on an annual basis. Overall gross take-up for the full year in 2011 was slightly down on the previous year. However, uncertainty about the economic outlook has been contributing to higher levels of caution among corporate occupiers and hindering leasing activity levels.

The availability of office accommodation across Europe continues to contract. The EU-27 vacancy rate dropped to 10.35% during Q4 2011, down from its peak of 10.46% in the first quarter of 2011. Although supply levels seem past their peak in most cities, weak occupier demand means that the absorption of vacant stock could be a very slow process despite completions running close to their historic lows or in the case of Dublin having come to a complete halt. This is also reflected in the uneven pattern of vacancies across different cities.

Prime office rents remain broadly flat across Europe for the third consecutive quarter in Q4. The CBRE EU-27 Office Rent Index grew by only 0.2% on the previous quarter and by only 1.0% year-on-year. Prime rents remained stable in almost all European markets in Q4 2011, while some cities are still seeing or expect to see some further reductions.

The volume of development completions has fallen sharply across Europe with no significant improvement in prospect over the next two years as weaker demand and weak rental growth, combined with limited access to funding continue to restrict speculative development across the region.

Q1 2012

Page 5

© 2012, CBRE

european Office take-Up Q2 2002 – Q4 2011

marketv

iew D

ublin O

ffice

Headlines

• Office take-up across Europe remains broadly stable although occupiers are unsettled by economic uncertainty

• Availability continues to contract across Europe, albeit slowly

• Prime rents broadly flat across Europe for the third consecutive quarter in Q4

• Development completions 45% below their cyclical peak in Western Europe

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2003 2004 2005 2006 2007 2008 2009 2010 2011 Q1 2012

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Lond

on -

Cen

tral -

Wes

tZu

rich

Gen

eva

Paris

Ile-

de-F

ranc

eSt

ockh

olm

Mun

ich

Ham

burg

Cop

enha

gen

Fran

kfur

tBe

rlin

Dus

seld

orf

Oslo

Vie

nna

Mila

nLo

ndon

- C

entra

l - C

ityA

mste

rdam

Hel

sink

iRo

me

Barc

elon

aM

adrid

Man

ches

ter

Birm

ingh

amEd

inbu

rgh

Gla

sgow

Brus

sels

War

saw

Prag

ueBu

dape

stD

ublin

Lisb

on

Current Yield Cyclical Low Cyclical High

Prime Office yields Q4 2011 vs High/low of Current Cycle

-20

-15

-10

-5

0

5

Dec

-08

Mar

-09

Jun-

09

Sep-0

9

Dec

-09

Mar

-10

Jun-

10

Sep-1

0

Dec

-10

Mar

-11

Jun-

11

Sep-1

1

Dec

-11

%

Total Returns Capital Value Growth

IPD Irish Capital value & total returns Q4 2008 – Q4 2011

Irish Investment Spend 2003 – Q1 2012

Q1

2012

Page 6

© 2012, CBRE

mar

ketv

iew

Dub

lin O

ffice

Headlines

• 3 office investment sales completed in Dublin in Q1 2012

• Welcome measures in Budget 2012 for the investment sector

• Prime office yields now 7.25%

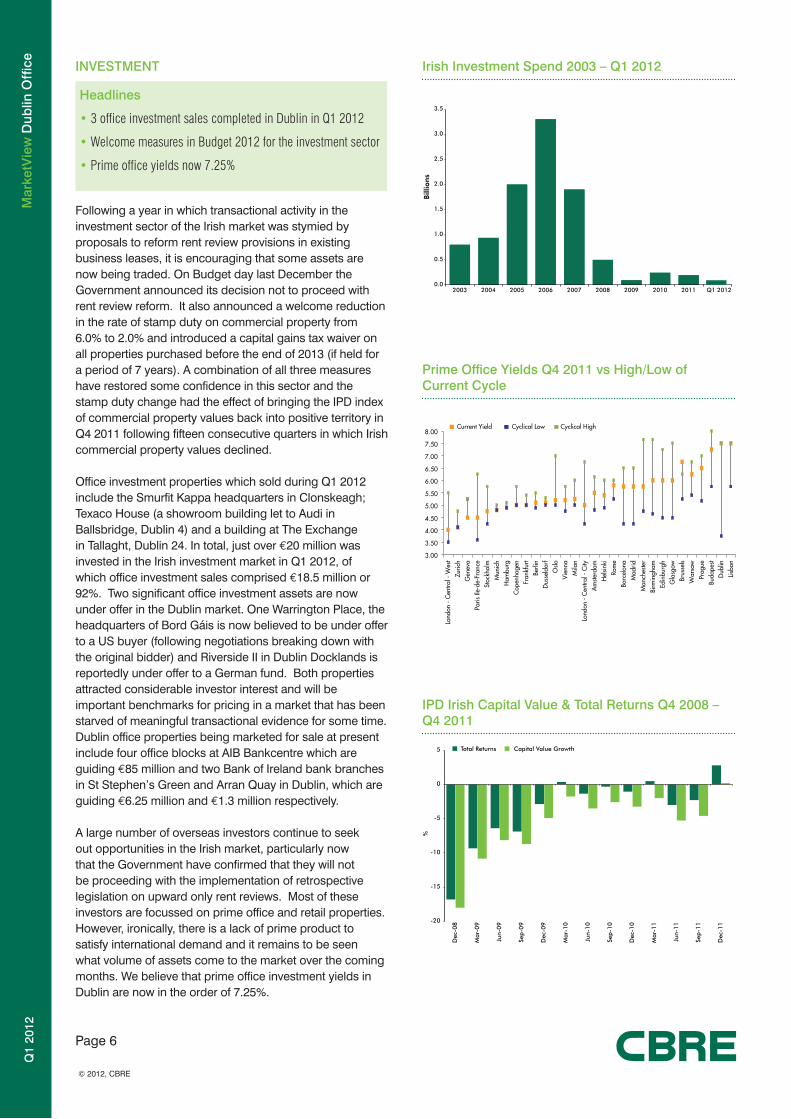

InveStment

Following a year in which transactional activity in the investment sector of the Irish market was stymied by proposals to reform rent review provisions in existing business leases, it is encouraging that some assets are now being traded. On Budget day last December the Government announced its decision not to proceed with rent review reform. It also announced a welcome reduction in the rate of stamp duty on commercial property from 6.0% to 2.0% and introduced a capital gains tax waiver on all properties purchased before the end of 2013 (if held for a period of 7 years). A combination of all three measures have restored some confidence in this sector and the stamp duty change had the effect of bringing the IPD index of commercial property values back into positive territory in Q4 2011 following fifteen consecutive quarters in which Irish commercial property values declined.

Office investment properties which sold during Q1 2012 include the Smurfit Kappa headquarters in Clonskeagh; Texaco House (a showroom building let to Audi in Ballsbridge, Dublin 4) and a building at The Exchange in Tallaght, Dublin 24. In total, just over €20 million was invested in the Irish investment market in Q1 2012, of which office investment sales comprised €18.5 million or 92%. Two significant office investment assets are now under offer in the Dublin market. One Warrington Place, the headquarters of Bord Gáis is now believed to be under offer to a US buyer (following negotiations breaking down with the original bidder) and Riverside II in Dublin Docklands is reportedly under offer to a German fund. Both properties attracted considerable investor interest and will be important benchmarks for pricing in a market that has been starved of meaningful transactional evidence for some time. Dublin office properties being marketed for sale at present include four office blocks at AIB Bankcentre which are guiding €85 million and two Bank of Ireland bank branches in St Stephen’s Green and Arran Quay in Dublin, which are guiding €6.25 million and €1.3 million respectively.

A large number of overseas investors continue to seek out opportunities in the Irish market, particularly now that the Government have confirmed that they will not be proceeding with the implementation of retrospective legislation on upward only rent reviews. Most of these investors are focussed on prime office and retail properties. However, ironically, there is a lack of prime product to satisfy international demand and it remains to be seen what volume of assets come to the market over the coming months. We believe that prime office investment yields in Dublin are now in the order of 7.25%.

nationality of Q1 2012 Dublin Office Occupiers

21%(6 lettings)

1%(1 letting)

40%(11 lettings)

38%(14 lettings)

Irish

US

UK

Other

Q1 2012

Page 7

© 2012, CBRE

marketv

iew D

ublin O

ffice

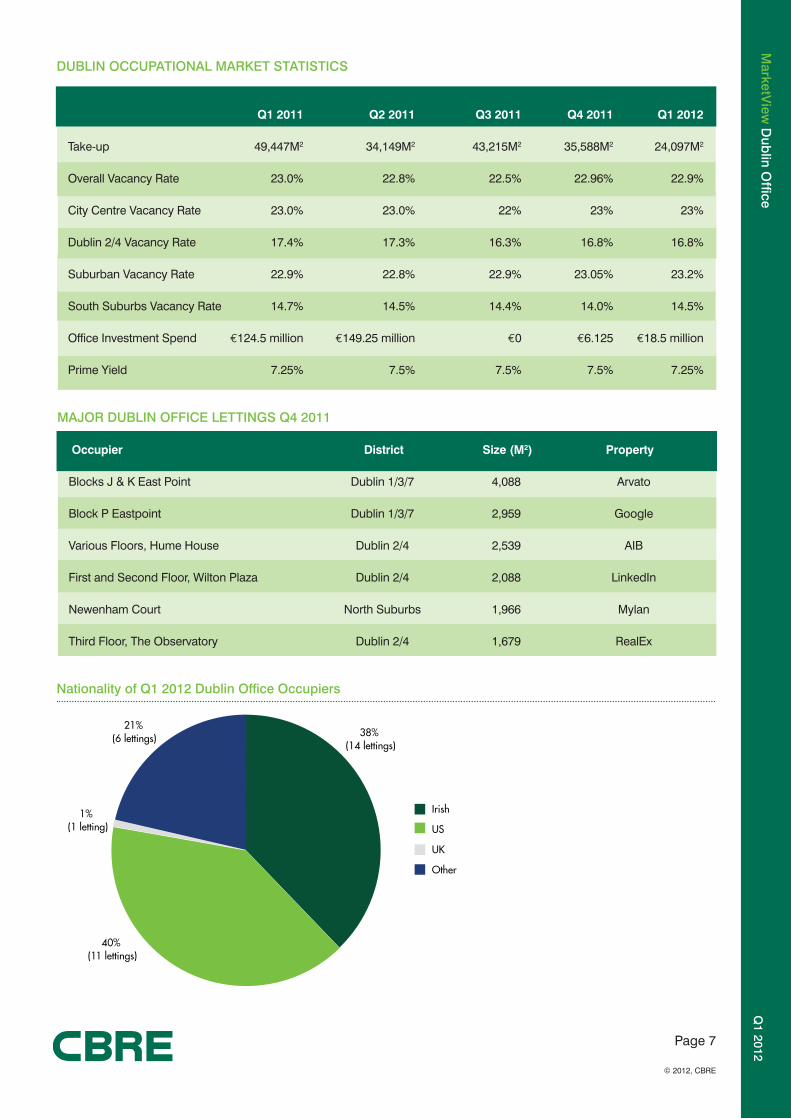

DUBlIn OCCUPatIOnal marKet StatIStICS

Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012

Take-up 49,447M2 34,149M2 43,215M2 35,588M2 24,097M2

Overall Vacancy Rate 23.0% 22.8% 22.5% 22.96% 22.9%

City Centre Vacancy Rate 23.0% 23.0% 22% 23% 23%

Dublin 2/4 Vacancy Rate 17.4% 17.3% 16.3% 16.8% 16.8%

Suburban Vacancy Rate 22.9% 22.8% 22.9% 23.05% 23.2%

South Suburbs Vacancy Rate 14.7% 14.5% 14.4% 14.0% 14.5%

Office Investment Spend €124.5 million €149.25 million €0 €6.125 €18.5 million

Prime Yield 7.25% 7.5% 7.5% 7.5% 7.25%

maJOr DUBlIn OFFICe lettInGS Q4 2011

Occupier District Size (M2) Property

Blocks J & K East Point Dublin 1/3/7 4,088 Arvato

Block P Eastpoint Dublin 1/3/7 2,959 Google

Various Floors, Hume House Dublin 2/4 2,539 AIB

First and Second Floor, Wilton Plaza Dublin 2/4 2,088 LinkedIn

Newenham Court North Suburbs 1,966 Mylan

Third Floor, The Observatory Dublin 2/4 1,679 RealEx

DISClaImer 2012 CBre

Information herein has been obtained from sources believed reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only and do not represent the current or future performance of the market.

This information is designed exclusively for use by CBRE clients, and cannot be reproduced without prior written permission of CBRE Ireland.

Managing DiRECtoRGuy Hollis

tEnant aDViSoRY SERViCES Paddy ConlonSarah Ward

oFFiCE agEnCYWillie DowlingAlan MoranPaddy Cormican

DEVELoPMEnt ConSULtanCYWesley Rothwell

CBREBurlington RoadDublin 4Irelandt: +353 1 618 5500

Marie Hunt Executive Director e: [email protected]

Elaine Linnane Database Managere: [email protected]

For more information regarding the MarketView, please contact:

CBre Dublin research

Suzanne Barrett Associate Director e: [email protected]

Q1

2012

Page 8

© 2012, CBRE

mar

ketv

iew

Dub

lin O

ffice

WE KNOW OFFICES FROM TOP TO BOTTOM

NO ONE KNOWS OFFICES QUITE LIKE

www.cbre.ie

To access market leading advice, talk to CBRE office agency today.