Q1 2014 Inflation Report MB-final - Bangko Sentral Ng ... · Inflation Report is published by the...

71

i

Transcript of Q1 2014 Inflation Report MB-final - Bangko Sentral Ng ... · Inflation Report is published by the...

i

i

FOREWORD

he primary objective of monetary policy is to promote a low and stable rate of inflation conducive to a balanced and sustainable economic growth. The adoption in January

2002 of the inflation targeting framework for monetary policy was aimed at helping to fulfill this objective.

One of the key features of inflation targeting is greater transparency, which means greater disclosure and communication by the BSP of its policy actions and decisions. This Inflation Report is published by the BSP as part of its transparency mechanisms under inflation targeting. The objectives of this Inflation Report are: (i) to identify the risks to price stability and discuss their implications for monetary policy; and (ii) to document the economic analysis behind the formulation of monetary policy and convey to the public the overall thinking behind the BSP’s decisions on monetary policy. The broad aim is to make monetary policy easier for the public to understand and enable them to better monitor the BSP’s commitment to the inflation target, thereby helping both in anchoring inflation expectations and encouraging informed debate on monetary policy issues.

The government’s target for annual headline inflation under the inflation targeting

framework has been maintained at 4.0 percent ± 1.0 percentage point (ppt) for 2013‐2014. For 2015‐2016, the medium‐term inflation target was set at 3.0 percent ± 1.0 ppt by the Development Budget Coordination Committee (DBCC) to be consistent with the desired disinflation path over the medium term, favorable trends in the structure of inflation, and expected higher capacity of the economy for growth under a low inflation environment.

The report is published on a quarterly basis, presenting a survey of the various factors

affecting inflation. These include recent price and cost developments, inflation expectations, prospects for aggregate demand and output, labor market conditions, monetary and financial market conditions, fiscal developments, and the international environment. A section is devoted to a discussion of monetary policy developments in the most recent, as well as a comprehensive analysis of the BSP’s view of the inflation outlook for the policy horizon.

The Monetary Board approved this Inflation Report at its meeting on 10 April 2014.

AMANDO M. TETANGCO, JR. Governor

28 April 2014

T

ii

List of Acronyms, Abbreviations, and Symbols AE Advanced economyAFF AHFF AMCs

Agriculture, Fishery, and ForestryAgriculture, Hunting, Forestry and Fishing Asset Management Companies

AP Asia PacificAL Auto Loans BAS Bureau of Agricultural StatisticsBES BGC BIR

Business Expectations SurveyBonifacio Global City Bureau of Internal Revenue

BIS Bank for International SettlementsBOC Bureau of Customs BPO Business Process OutsourcingBTr Bureau of the TreasuryCAMPI Chamber of Automotive Manufacturers of the Philippines, Inc. CAR Capital Adequacy RatioCBD Central Business DistrictCCRs Credit Card Receivables CES Consumer Expectations Survey CDS Credit Default SwapsCI Confidence IndexCPI DAA DDA DBCC DOF EIA

Consumer Price Index Deferred Accounting Adjustment Demand Deposit Account Development Budget Coordination Committee Department of Finance Energy Information Administration

EM Emerging Market EMBI ERC

JP Morgan Emerging Market Bond IndexEnergy Regulatory Commission

EU European Union FAO FPI

Food and Agriculture OrganizationFood Price Index

GDP Gross Domestic Product GNI Gross National IncomeGRAM GS

Generation Rate Adjustment MechanismGovernment Securities

ICERA Incremental Currency Exchange Rate AdjustmentIEA International Energy AgencyIMF International Monetary Fund IPP Independent Power ProducerLFS Labor Force SurveyLPG Liquefied Petroleum GasLTFRB Land Transportation Franchising and Regulatory Board

iii

MB Monetary BoardMEM MENA

Multi‐Equation Model Middle East and North Africa

Meralco Manila Electric CompanyMISSI Monthly Integrated Survey of Selected Industries MTP NBQBs

Major Trading PartnerNon‐Bank Financial Institutions with Quasi‐Banking Functions

NCCP National Council for Commuters’ Protection NDA NEDA NEER

Net Domestic AssetsNational Economic and Development Authority Nominal Effective Exchange Rate

NFA Net Foreign Assets; National Food AuthorityNG NGCP

National Government National Grid Corporation of the Philippines

NPC National Power CorporationNPI Net Primary IncomeNPLs Non‐performing loansNSO O&O

National Statistics OfficeOffshoring and Outsourcing

OECD Organization for Economic Cooperation and Development OPEC OF

Organization of the Petroleum Exporting Countries Overseas Filipinos

PBR PCE PMI PSALM

Performance‐Based RatePersonal Consumption Expenditure Purchasing Managers’ Index Power Sector Assets and Liabilities Management Corporation

PSEi Philippine Stock Exchange Composite Index PSIC Philippine Standard Industrial ClassificationRB RDA

Rural BanksReserve Deposit Account

REER Real Effective Exchange RateROP Republic of the PhilippinesRP RR

Repurchase Reserve Requirement

RREL Residential and Real Estate LoansRRP RWA

Reverse Repurchase Risk Weighted Assets

SEM SMS

Single‐Equation ModelShort Message Service

SDA Special Deposit AccountTCS TLP

Transportation, Communications, and StorageTotal Loan Portfolio

U/KBs VAPI VOP

Universal/commercial banks Value of production index Volume of production index

WEO WESM

World Economic Outlook Wholesale Electricity Spot Market

iv

THE MONETARY POLICY OF THE BANGKO SENTRAL NG PILIPINAS

The BSP Mandate The BSP’s main responsibility is to formulate and implement policy in the areas of money, banking and credit, with the primary objective of maintaining stable prices conducive to a balanced and sustainable economic growth in the Philippines. The BSP also aims to promote and preserve monetary stability and the convertibility of the national currency. Monetary Policy Instruments The BSP’s primary monetary policy instrument is its overnight reverse repurchase (RRP) or borrowing rate. Other instruments to implement the desired monetary policy stance to achieve the inflation target include (a) increasing/decreasing the reserve requirement; (b) encouraging/discouraging deposits in the special deposit account (SDA) facility by banks and trust entities of BSP‐supervised financial institutions; (c) adjusting the rediscount rate on loans extended to banking institutions on a short‐term basis against eligible collateral of banks’ borrowers; and (d) outright sales/purchases of the BSP’s holdings of government securities. Policy Target The BSP’s target for monetary policy uses the Consumer Price Index (CPI) or headline inflation rate, which is compiled and released to the public by the National Statistics Office (NSO). The policy target is set by the Development Budget Coordination Committee (DBCC)1 in consultation with the BSP. The inflation target for 2014 was set at 4.0 percent ± 1.0 ppt. For 2015‐2016, the medium‐term inflation target was reduced to 3.0 percent ± 1.0 ppt.2 BSP’s Explanation Clauses These are the predefined set of acceptable circumstances under which an inflation‐targeting central bank may fail to achieve its inflation target. These clauses reflect the fact that there are limits to the effectiveness of monetary policy and that deviations from the inflation target may sometimes occur because of factors beyond the control of the central bank. Under the inflation targeting framework of the BSP, these exemptions include inflation pressures arising from: (a) volatility in the prices of agricultural products; (b) natural calamities or events that affect a major part of the economy; (c) volatility in the prices of oil products; and (d) significant government policy changes that directly affect prices such as changes in the tax structure, incentives, and subsidies.

1 The DBCC, created under Executive Order (E.O.) No. 232 dated 14 May 1970, is an inter‐agency committee tasked primarily to formulate the National Government's fiscal program. It is composed of the Office of the President (OP), Department of Budget and Management (DBM), National Economic and Development Authority (NEDA), and the Department of Finance (DOF). The BSP attends the Committee meetings as a resource agency.

2 The inflation target range for 2015‐2016 was announced on 13 December 2012.

v

The Monetary Board The powers and functions of the BSP, such as the conduct of monetary policy and the supervision over the banking system, are exercised by its Monetary Board, which has seven members appointed by the President of the Philippines. Starting in 2012, the Monetary Board will hold eight (8) monetary policy meetings in a year to review and decide on the stance of monetary policy. Prior to 2012, monetary policy meetings were held every six weeks while prior to July 2006, meetings were held every four weeks during the 2002 – July 2006 period.

Chairman Amando M. Tetangco, Jr. Members Cesar V. Purisima

Alfredo C. Antonio

Ignacio R. Bunye3

Peter B. Favila

Felipe M. Medalla

Armando L. Suratos

The Advisory Committee The Advisory Committee was established as an integral part of the institutional setting for inflation targeting. It is tasked to deliberate, discuss, and make recommendations on monetary policy to the Monetary Board. Like the Monetary Board, the Committee will meet eight times a year (beginning in January 2012) but may also meet between regular meetings, whenever deemed necessary.

Chairman Amando M. Tetangco, Jr.Governor

Members Diwa C. Guinigundo

Deputy Governor Monetary Stability Sector

Nestor A. Espenilla, Jr. Deputy Governor Supervision and Examination Sector

Ma. Cyd N. Tuaño‐Amador

Assistant Governor Monetary Policy Sub‐Sector

Ma. Ramona GDT Santiago Assistant Governor Treasury Department

3 Appointment as Monetary Board member is until 16 February 2014.

vi

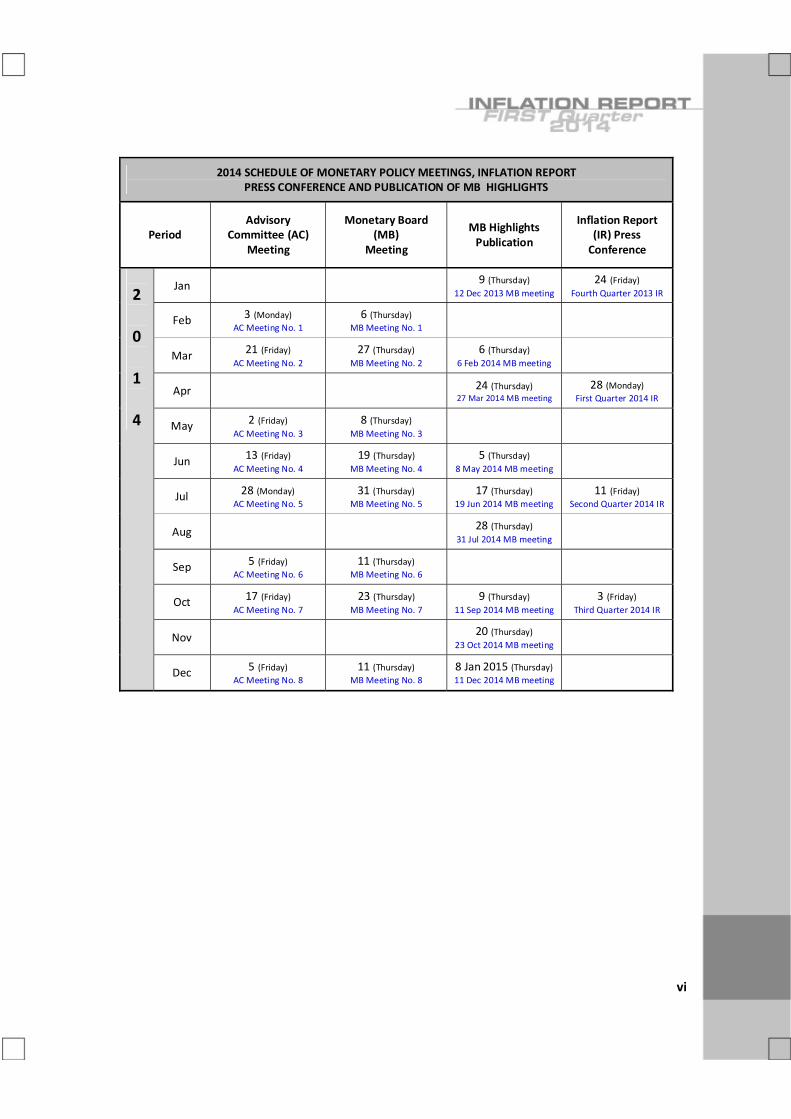

2014 SCHEDULE OF MONETARY POLICY MEETINGS, INFLATION REPORT PRESS CONFERENCE AND PUBLICATION OF MB HIGHLIGHTS

Period Advisory

Committee (AC) Meeting

Monetary Board (MB)

Meeting

MB Highlights Publication

Inflation Report (IR) Press Conference

2 0 1 4

Jan 9 (Thursday) 12 Dec 2013 MB meeting

24 (Friday) Fourth Quarter 2013 IR

Feb 3 (Monday) AC Meeting No. 1

6 (Thursday) MB Meeting No. 1

Mar 21 (Friday) AC Meeting No. 2

27 (Thursday) MB Meeting No. 2

6 (Thursday) 6 Feb 2014 MB meeting

Apr 24 (Thursday) 27 Mar 2014 MB meeting

28 (Monday) First Quarter 2014 IR

May 2 (Friday) AC Meeting No. 3

8 (Thursday) MB Meeting No. 3

Jun 13 (Friday) AC Meeting No. 4

19 (Thursday) MB Meeting No. 4

5 (Thursday) 8 May 2014 MB meeting

Jul 28 (Monday) AC Meeting No. 5

31 (Thursday) MB Meeting No. 5

17 (Thursday) 19 Jun 2014 MB meeting

11 (Friday) Second Quarter 2014 IR

Aug 28 (Thursday) 31 Jul 2014 MB meeting

Sep 5 (Friday) AC Meeting No. 6

11 (Thursday) MB Meeting No. 6

Oct 17 (Friday) AC Meeting No. 7

23 (Thursday) MB Meeting No. 7

9 (Thursday) 11 Sep 2014 MB meeting

3 (Friday) Third Quarter 2014 IR

Nov 20 (Thursday) 23 Oct 2014 MB meeting

Dec 5 (Friday) AC Meeting No. 8

11 (Thursday) MB Meeting No. 8

8 Jan 2015 (Thursday) 11 Dec 2014 MB meeting

vii

CONTENTS

Overview 1

I. Inflation and Real Sector Developments 3

Prices 3

Private Sector Economists’ Inflation Forecasts 5

Aggregate Demand and Supply 10

Aggregate Demand 10

Box Article: Decomposing Sources of Economic Growth in the Philippines Other Demand Indicators

12

16 Aggregate Supply 23

Labor Market Conditions 24

II. Monetary and Financial Market Conditions

26

Domestic Liquidity and Credit Conditions 26

Interest Rates 31

Financial Market Conditions

33

Banking System 36

Exchange Rate 39

III. Fiscal Developments IV. External Developments

42 43

V. Monetary Policy Developments

47

VI. Inflation Outlook 48

BSP Inflation Forecasts Risks to the Inflation Outlook

VII. Implications for the Monetary Policy Stance

Summary of Monetary Policy Decisions

48 51 54

56

1

OVERVIEW4

Headline inflation rises on higher food and non‐food inflation. Year‐on‐year (y‐o‐y) headline inflation rate increased to 4.1 percent in Q1 2014 from 3.4 percent in the previous quarter. The resulting year‐to‐date (ytd) inflation rate of 4.1 percent was within the Government’s inflation target range of 4.0 percent ± 1.0 ppt for 2014. The uptick in headline inflation could be attributed to higher food inflation as the prices of most food commodities increased owing to some tightness in the domestic supply conditions. Similarly, higher electricity rates and domestic petroleum prices contributed to increased non‐food inflation. The official core inflation along with two out of three alternative measures of core inflation estimated by the BSP likewise rose in Q1 2014 relative to the rates registered in the previous quarter. The official core inflation was slightly higher at 3.0 percent during the review quarter from 2.9 percent in Q4 2013. The number of items with inflation rates greater than the threshold of 5.0 percent also increased and accounted for a higher proportion of the CPI basket. Domestic demand conditions remain buoyant. The Philippine economy continued to expand at an above‐trend rate in Q4 2013, growing by 6.5 percent to bring the full‐year 2013 GDP growth to 7.2 percent, which is above the Government’s growth target of 6.0–7.0 percent for the year. Output growth was driven by robust household spending, exports, and capital formation (particularly durable equipment) on the expenditure side; and by solid gains in the services sector on the production side. At the same time, higher‐frequency demand indicators continued to show positive readings in the first quarter. Vehicle sales posted strong growth during the quarter, buoyed by brisk consumer demand and attractive financing options offered by industry players. Energy sales also continued to rise, albeit at a slower pace, on account of increased consumption by the industrial and commercial sectors, while capacity utilization in manufacturing is steady above 80 percent. The composite Philippine Purchasing Managers’ Index (PMI) likewise remained firmly above the 50 point‐expansion threshold at 58.2 in February, reflecting increased PMI recorded across all sectors relative to their end‐Q4 2013 levels. Similarly, the outlook of businesses and consumers for the following quarter turned more favorable, supporting the continued strength of aggregate demand in the coming months amid sustained credit growth and ample liquidity in the financial system. The global growth profile is broadly steady. The economic recovery in most advanced economies (AEs) has picked up steadily, while the growth momentum in key emerging economies has moderated over the last few months. In the US, the economy continues to show signs of solidifying growth, supported by strong private consumption and non‐residential investment. The expansion in Japan has also proceeded at a stable pace, aided by accommodative monetary and fiscal policies. At the same time, the ongoing recovery in the euro area has gained traction owing largely to improving domestic demand alongside rising business and consumer confidence. By contrast, a range of indicators point to softening economic momentum in China, while growth conditions in India remain subdued. Going forward, global economic prospects are expected to improve broadly, but the risks to the growth outlook remain tilted to the downside. Increased volatility in financial markets in view of the uncertainty in the pace of the US Federal Reserve’s (US Fed) tapering of its monetary stimulus will be a key source of risks for emerging economies. Meanwhile, global inflation pressures remain broadly subdued. The inflation environment in AEs continues to be benign, as output gaps are expected to stay substantial even with the pickup in activity. However, inflation has risen in some emerging markets (EMs) owing to domestic supply factors.

Local financial markets experience bouts of volatility but regain some stability. Market sentiment during the quarter in review was driven largely by concerns over the extent and duration of US Fed’s

4 The analysis in this report is based on information as of 31 March 2014.

2

tapering of its quantitative easing (QE) measures and potential abrupt adjustments in its policy stance as recovery in the US firms up. Indications of a further economic slowdown in China likewise dampened investor confidence. Nonetheless, markets started to rally by mid‐quarter owing to positive domestic economic reports suggesting sustained resiliency of Philippine macroeconomic fundamentals along with expectations of continued strong corporate earnings. The US Fed pronouncement to scale back stimulus in measured steps further propelled optimism in the local bourse. Philippine sovereign spreads narrowed relative to previous quarter’s average, while the spread on Philippine credit default swaps (CDS) continued to trade lower relative to those of our neighbors in the region. The Philippine Stock Exchange index (PSEi) also began to recover gains lost in the last month of 2013 as the market traded close to the 6,500‐barrier in March. T‐bill auctions during the quarter remained oversubscribed on aggregate, although results reflected investors’ preference for shorter‐dated T‐bills. However, the peso recorded moderate depreciation relative to previous quarter on lingering uncertainty on the external front.

Inflation expectations continue to support the within‐target inflation outlook. Results of the BSP’s survey of private sector economists for March 2014 yielded higher but still broadly within‐target inflation forecasts for 2014‐2015. Analysts expect inflation to rise going forward due largely to factors such as pending electricity rate adjustments, weakening peso, and possible increases in food and oil prices. Results of the March 2014 Consensus Economics inflation forecast survey for the country also showed a higher mean inflation projection for 2014. The BSP maintains key policy rates but adjusts the reserve requirement ratio. The BSP decided to keep its policy interest rates steady during its 3 February and 27 March 2014 monetary policy meetings on the assessment that the future inflation path was likely to stay within the target ranges of 4.0 percent ± 1.0 ppt for 2014 and 3.0 percent ± 1.0 ppt for 2015. At the same time, the MB decided to increase the reserve requirement by one ppt effective on 11 April 2014 to help guard against potential risks to financial stability that could arise from the recent rapid growth in domestic liquidity. Prevailing monetary conditions and inflation dynamics suggest that the space to keep monetary policy settings unchanged is narrowing. Latest baseline projections continue to show average headline inflation settling within the target ranges for 2014 and 2015. However, current assessment of the price environment over the policy horizon indicates that the balance of risks to the inflation outlook remains tilted to the upside, with potential price pressures emanating from pending petitions for adjustments in utility rates and from possible increases in food and oil prices. At the same time, while inflation expectations are still within target, they have trended higher and are moving near the upper end of the target range for 2015. Firm growth dynamics arising from the broad buoyancy of domestic demand also suggest that the economy can accommodate measured adjustments in monetary conditions. Domestic liquidity growth has also remained strong after the full unwinding of the non‐trust account placements in the SDA facility in November with more loanable funds deployed to support domestic economic activity as evident by the robust growth in bank lending. The continued strong liquidity expansion, if sustained, could potentially exert inflationary pressures and contribute to the build‐up of financial stability risks. On the whole, the BSP continues to have monetary policy space to address the challenges that could threaten the inflation objective and stability of the Philippine financial system. Going forward, the BSP will remain guided by its primary objective of maintaining price stability along with safeguarding the resilience of the financial system, and stands ready to deploy appropriate measures as needed to ensure sustainable, non‐inflationary, and inclusive economic growth.

3

I. INFLATION AND REAL SECTOR DEVELOPMENTS

Prices Inflation rises on higher food and non‐food inflation.

0

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013 2014

in percent

Quarterly Headline Inflation (2006=100)

Food Non‐FoodNon‐Alcoholic Beverage Alcoholic Beverage and TobaccoHeadline

Q1 20144.1 pct

Core inflation also increases.

Alternative Core Inflation MeasuresQuarterly averages of year‐on‐year change

QuarterOfficial Headline Inflation

Official Core

Inflation

Trimmed

Mean 1/

Weighted

Median 2/

Net of Volatile

Items 3/ *2011

Q1

Q2

Q3

Q4

2012

Q1

Q2

Q3

Q4

2013

Q1

Q2

Q3

Q4

2014

Q1

4.6

4.5

5.0

4.8

4.7

3.2

3.1

2.9

3.6

3.0

3.0

3.2

2.7

2.4

3.4

4.1

4.3

4.0

4.3

4.4

4.5

3.7

3.5

3.7

4.1

3.4

2.9

3.8

3.0

2.1

2.9

3.0

3.8

3.3

4.0

4.0

3.8

3.2

3.0

3.1

3.4

3.2

2.5

3.0

2.3

2.1

2.6

3.3

3.1

2.9

3.1

3.2

3.1

3.0

2.6

3.2

3.2

3.0

2.3

2.8

2.3

2.0

2.2

2.6

3.6

3.7

3.7

3.5

3.6

3.4

3.0

3.3

3.9

3.4

3.1

3.9

3.2

2.4

2.9

2.81/ The trimmed mean represents the average inflation rate of the (weighted) middle 70 percent in a lowest

to‐highest ranking of year‐on‐year inflation rates for all CPI components.

2/ The weighted median represents the middle inflation rate (corresponding to a cumulative CPI weight of 50 percent) in a lowest‐to‐highest ranking of year‐on‐year inflation rates.

3/ The net of volatile items method excludes the following items: educational services, fruits and vegetables, personal services, rentals, recreational services, rice, and corn.

r/ Revised.

* The series has been recomputed using a new methodology that is aligned with NSO’s method of computing the official core inflation, which re‐weights remaining items to comprise 100 percent of the core basket after excluding non‐core items. The previous methodology retained the weights of volatile items in the CPI basket while keeping their indices constant at 100.0 from month to month.

Source: NSO, BSP estimates

0

20

40

60

80

100

120

0

10

20

30

40

50

60

70

Q12009

Q2 Q3 Q4 Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

CPI Items with Inflation Rates Above Threshold

Cumulative Weight (in %) No. of Items Above 5% Threshold (RHS)

27.2 pct

32 items

Headline and Core Inflation Headline inflation increased further to 4.1 percent in Q1 2014 from the quarter‐ago and year‐ago rates of 3.4 percent and 3.2 percent, respectively. The resulting ytd inflation rate of 4.1 percent was within the Government’s inflation target range of 4.0 percent ± 1.0 ppt for 2014. The continued uptick in headline inflation was due to higher food and non‐food inflation. Food inflation increased to 5.9 percent in Q1 2014 owing to some tightness in the domestic supply conditions, while the rise in non‐food inflation to 2.6 percent could be attributed to higher electricity rates and domestic petroleum prices. Core inflation, which excludes some food and energy items to measure underlying price pressures, rose slightly to 3.0 percent in Q1 2014 from 2.9 percent in Q4 2013. Two out of three alternative measures of core inflation estimated by the BSP were also higher in Q1 2014 relative to the rates registered in the previous quarter. In particular, the trimmed mean and weighted median measures went up to 3.3 percent and 2.6 percent, respectively, from the previous quarter’s 2.6 percent and 2.2 percent. By contrast, the net of volatile items measure declined slightly to 2.8 percent from 2.9 percent in Q4 2013.

Similarly, the number of items with inflation rates greater than the threshold of 5.0 percent (the upper end of the 2014 inflation target) increased further to 32 from 27 items in the previous quarter. These items accounted for a higher proportion of the CPI basket at 27.2 percent compared to the quarter‐ago share of 15.0 percent. Grouping the CPI basket into food and non‐food components, the number of food items above the 5.0 percent‐threshold went up to 13 from 11 items in the previous quarter. Similarly, the number of non‐food items with inflation rates higher than the threshold increased to 19 from 16 items in Q4 2013.

4

Limited domestic supply of key food items drives up food inflation.

Inflation Rates for Selected Food ItemsQuarterly averages in percent (2006=100)

Commodity2013 2014

Q1 Q4 Q1Food and Non‐alcoholic Beverages

2.7 4.0 5.6

Food 2.7 4.1 5.9Bread and Cereals 2.7 6.8 8.6

Rice 1.8 8.3 10.8Corn 5.5 3.7 3.7

Meat 1.8 2.2 2.7Fish 5.3 3.0 4.1Milk, Cheese and Eggs 2.9 1.6 2.2Oils and Fats ‐5.8 ‐4.0 1.3Fruit 4.9 3.9 5.2Vegetables 0.2 5.4 11.0Sugar, Jam, Honey 3.1 ‐2.2 2.5Food Products N.E.C. 3.1 3.4 4.1

Non‐alcoholic Beverages 3.7 1.8 1.7

Source of Basic Data: PSA‐NSO, BSP

Higher electricity rates and domestic petroleum prices contribute to increased non‐food inflation.

Inflation Rates for Selected Non‐Food ItemsQuarterly averages in percent (2006=100)

Commodity2013 2014

Q1 Q4 Q1

Non‐Food 2.8 2.1 2.6

Clothing and Footwear 4.9 3.0 3.5Housing, Water, Electricity, 2.8 2.1 3.2Gas and Other Fuels

Electricity, Gas, and Other Fuels

0.9 2.4 5.8

Furnishings, Household 4.9 2.3 2.7Equipment

Health 3.6 2.6 3.3Transport 0.9 0.8 1.1Communication 0.5 0.0 0.0Recreation and Culture 2.2 2.5 2.5Education 4.4 4.7 4.7Restaurant and Miscellaneous 2.9 2.2 2.1Goods and Services

Source of Basic Data: PSA‐NSO, BSP

Food Inflation Food inflation increased to 5.9 percent in Q1 2014 from the quarter‐ago and year‐ago rates of 4.1 percent and 2.7 percent, respectively, as most food commodities—particularly rice, meat, oils, fruits, and vegetables—posted higher prices due to limited domestic supply. The uptrend in rice prices could be attributed to the decline in buffer stocks following the onset of the lean season. Meanwhile, some tightness in domestic supply conditions, triggered by weather‐related production disruptions, led to higher prices of meat, oils, fruits, and vegetables. Non‐food inflation Non‐food inflation rose to 2.6 percent in Q1 2014 from 2.1 percent in the previous quarter. Higher inflation for electricity, gas and other fuels, as well as transport drove up non‐food inflation. In particular, from 2.4 percent in Q4 2013, electricity, gas, and other fuels inflation went up to 5.8 percent in Q1 2014 due to higher electricity charges and LPG prices. Similarly, transport prices increased by 1.1 percent following a 0.8‐percent rise in the previous quarter, reflecting an upward adjustment in the prices of gasoline and diesel.

5

Private Sector Economists’ Inflation Forecasts Mean inflation forecasts for 2014 to 2015 are higher.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2013 2014

2014 20152016 target range

BSP Private Sector Economists' Survey Mean forecast for full year, in percent

2014: 4.1

2015/2016: 3.8

2015 2016Q2 Q3 FY FY FY

1) Al‐Amanah Islamic Bank 3.80 3.60 3.50 3.50 3.502) Asia ING 4.30 4.50 4.40 3.90 ‐3) Banco De Oro 4.00 3.75 3.50 3.50 3.504) Bangkok Bank 4.20 4.10 4.20 3.75 3.755) Bank of China 3.90 3.80 4.10 4.30 4.606) Bank of Commerce 4.10 4.10 4.10 ‐ ‐7) Bank of the Philippine Islands 4.10 3.50 3.90 4.30 4.108) Chinabank 4.20 4.30 4.30 3.30 3.109) CTBC Bank 4.10 4.00 4.20 3.75 3.7510) Deutsche Bank ‐ ‐ 4.30 3.80 ‐11) Eastwest Bank 4.30 4.30 4.35 4.45 4.5012) Global Source 5.00 5.00 4.80 4.00 ‐13) HSBC 4.09 4.50 4.20 4.30 ‐14) JP Morgan 4.20 4.10 4.10 3.70 ‐15) Korea Exchange Bank 2.90 2.90 2.80 2.90 2.9016) Land Bank of the Phils 3.1‐3.4 3.3‐3.6 3.5‐3.8 3.6‐3.9 3.6‐3.917) Maybank 3.90 3.70 3.80 3.20 3.3018) Maybank‐ATR KimEng 3.90 3.60 3.70 3.50 ‐19) Metrobank ‐ ‐ 4.00 4.00 4.0020) Multinat'l Inv. Banc 4.00 3.80 3.80 3.60 ‐21) Mizuho 4.10 4.00 4.10 4.00 4.0022) Nomura 4.50 4.90 4.70 4.20 ‐23) Philippine Equity Partners 4.40 4.40 4.50 4.10 ‐24) RCBC 4.4‐4.6 4.4‐4.7 4.3‐4.5 3.5‐4.0 4.0‐4.525) Robinsons Bank 4.0‐4.25 4.0‐4.25 4.0‐4.5 3.5‐4.0 3.5‐4.026) Security Bank 4.00 3.50 4.30 4.50 3.8027) Standard Chartered Bank 4.20 4.30 3.90 3.50 3.5028) Union Bank 3.80 3.60 4.20 4.20 4.00

Median Forecast 4.1 4.1 4.2 3.8 3.8Mean Forecast 4.1 4.0 4.1 3.8 3.8High 5.0 5.0 4.8 4.5 4.6Low 2.9 2.9 2.8 2.9 2.9Number of observations 26 26 28 27 18

Government Target

Private Sector Forecasts for Inflation, March 2014Annual Percent Change

2014

4.0±1.0 3.0±1.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

1.0‐2.0 2.1‐3.0 3.1‐4.0 4.1‐5.0 5.1‐6.0 6.1‐7.0

Probability Distribution For Analysts' Inflation Forecasts*2014‐2016

2014 2015 2016

*Probability distributions were averages of those provided by 23 out of 28 respondents.

(Source: BSP Survey)

Results of the BSP’s survey of private sector economists for March 2014 yielded higher mean inflation forecasts for 2014 and 2015 relative to the results in December 2013.5 In particular, the mean inflation forecasts for 2014 and 2015 were higher at 4.1 percent (from 3.9 percent) and 3.8 percent (from 3.6 percent), respectively. Meanwhile, the inflation forecast for 2016 was at 3.8 percent. Analysts expect inflation to rise going forward due largely to pending electricity rate adjustments, weakening peso, and possible increases in food and oil prices. Based on the probability distributions of the forecasts provided by the respondents, a 34.7‐percent chance is ascribed to average inflation for 2014 settling within the 3.1‐4.0 percent range. Meanwhile, there is a 51.7 percent chance that average inflation for 2014 could be within 4.1‐5.0 percent. Similarly, results of the March 2014 Consensus Economics inflation forecast survey for the country showed a higher mean inflation projection for 2014 of 4.2 percent (from 3.9 percent in December 2013).6 Respondents expect inflation to average at 3.9 percent in 2015.

5 There were 28 respondents in the BSP’s survey of private sector economists in March 2014. 6 There were 20 respondents in the Consensus Economics’ survey in March 2014.

6

Results of the Q1 2014 BES indicate more respondents anticipating inflation to increase over the current and following quarter.

Results of the Q1 2014 CES show that consumers expect higher inflation over the next 12 months.

Results of the Business Expectations Survey (BES) for Q1 2014 indicated that respondents who expected inflation to go up in the current and next quarters continued to outnumber those that held the opposite view. Relative to the previous survey, a higher number of respondents expect inflation to move up in the current quarter (from a diffusion index of 25.0 percent to 43.0 percent). Similarly, the number of respondents that expects inflation to increase in the next quarter (from 18.0 percent to 32.0 percent) increased. Meanwhile, consumers project inflation to increase over the next 12 months on the view that the peso would continue to depreciate against the US dollar. In particular, respondents anticipate inflation to edge higher to 8.4 percent in Q1 2014 from 7.0 percent in Q4 2013.

International oil prices ease on rising US crude oil stockpiles.

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014 2015

Price in US do

llars per barrel

Spot and Estimated Future Prices of Dubai Crude Oil*

*Futures prices derived using Brent crude futures data.

31 December 2013

31 March 2013

0

Forecasts for 2014 global oil demand are mixed.

Energy Prices The average price of Dubai crude oil declined by 2.2 percent quarter‐on‐quarter (q‐o‐q) in Q1 2014 given rising crude oil supply in the US. According to the US Energy Information Administration, US crude oil output increased by 33,000 barrels a day (or 4.0 percent) to 8.2 million barrels in the week ending 14 March, the highest level since May 1988. The increase in oil production was supported by a combination of horizontal drilling and hydraulic fracturing, or fracking, which unlocked supplies in shale formations in the US. Oil prices also declined on a slightly weaker outlook for oil demand amid signs of slowing Chinese economic growth.7 At the same time, the estimated futures prices of Dubai crude oil, which are based on movements in Brent crude oil futures, in Q1 2014 showed a lower path for 2014‐2015 compared to the estimates in Q4 2013. In March 2014, the US Energy Information Administration (EIA)8 projected global demand for 2014 to increase by 1.2 million barrels a day (mmbd), the same in the previous quarter’s

7 According to China’s National Bureau of Statistics, industrial production during the period January to February 2014 dropped by 1 percent compared to the same period in 2013 to 78.78 million metric tons. 8 EIA, March 2014 Short‐Term Energy Outlook, www.eia.doe.gov

7

Domestic prices of petroleum products decrease.

Domestic Retail Pump Prices (peso/liter)*End‐quarter prices

Quarter Gasoline** Kerosene Diesel LPG

2013

Q1

Q2

Q3

Q4

2014

Q1

51.45

51.95

53.20

55.50

53.65

48.45

50.07

51.12

53.07

50.85

39.85

42.30

42.90

45.45

44.45

40.21

36.83

41.25

49.80

41.56

Q‐o‐Q (1.85) (2.22) (1.00) (8.24)

Y‐o‐Y 2.20 2.40 4.60 1.35

* Average retail pump price for the Big Three oil companies—Caltex, Petron, and Shell, Metro Manila prices only.

** Average price for unleaded gasoline

Source: Department of Energy (DOE)

Power rates decrease due to lower generation charges from WESM and IPPs.

estimate. The Organization of the Petroleum Exporting Countries (OPEC)9 projected global demand for 2014 to increase by 1.1 mmbd, higher compared to the previous quarter’s estimate of 1.0 mmbd. Meanwhile, the IEA10 expected 2014 oil demand to increase by 1.1 mmbd in March 2014, from 1.2 mmbd in December 2013. The bulk of the projected increase in world oil consumption over the next two years is still expected to come from non‐Organization for Economic Cooperation and Development (OECD) regions, particularly China. In Q1 2014, the domestic prices of gasoline, kerosene, diesel, and LPG fell by P1.85 per liter, P2.22 per liter, P1.00 per liter, and P8.24 per liter, respectively, relative to their end‐Q4 2013 levels. Meanwhile, compared to year‐ago levels, the domestic prices of gasoline, kerosene, diesel, and LPG prices went up by P2.20 per liter, P2.40 per liter, P4.60 per liter, and P1.35 per liter, respectively. Power Generation charges in the National Capital Region (NCR) declined in Q1 2014 due to the downward adjustments in power rates contracted by Meralco under its Power Supply Agreements (PSAs) along with lower cost of electricity purchased from individual power producers (IPPs) and the Wholesale Electricity Spot Market (WESM). Power rates at the WESM decreased due

9 OPEC, March 2014Monthly Oil Market Report, www.opec.org 10 IEA, March 2014 Oil Market Report, www.iea.org

8

to moderate demand and the resumption to normal operations of the Malampaya11 natural gas plant as well as other major power plants. Transmission charges and other bill components likewise edged lower during the review quarter. Meralco’s planned rate increase for the December 2013 billing owing to high WESM prices was suspended under the Supreme Court’s (SC) 60‐day temporary restraining order (TRO) issued on 23 December 2013. The TRO was subsequently extended from 23 February to 22 April 2014. However, the Energy Regulatory Commission (ERC) issued an order on 3 March 2014 declaring as void the WESM prices for Luzon during the period 26 October‐25 December 2013 as WESM prices in the supply months of November and December 2013 did not qualify as reasonable, rational, and competitive given the confluence of factors accompanying the tight supply situation in the power market. ERC also ordered Philippine Electric Market Corporation (PEMC) to recalculate the WESM prices during the said supply months. Following the said developments, Meralco’s planned rate adjustments for December 2013 and January 2014 will be lower than their earlier requests. Nonetheless, potential sources of upside pressures on electricity charges remain. Existing petitions for rate increases with the ERC include the following: (1) Meralco’s petitions for the refund of generation over‐/under‐recoveries; (2) Power Sector Assets and Liabilities Management’s (PSALM) petition for True‐Up Adjustments of Fuel and Purchased Power Costs (TAFPPC), Foreign Exchange Related Costs (TAFxA) under the Rules for the Automatic Recovery of Monthly Fuel and Purchased Power Costs and Foreign Exchange Related Costs by the National Power Corporation (NPC), and NPC’s Stranded Debt portion of the UC for CY 2011 and 2012; and (3) the National Grid Corporation of the Philippines’ (NGCP) petitions to recover

11 The Malampaya Deep Water Gas‐to‐Power Project is a joint undertaking of the National Government and the private sector, spearheaded by the Department of Energy, developed and operated by Shell Philippines Exploration B.V. (SPEX) on behalf of the joint venture partners Chevron Malampaya LLC and the PNOC Exploration Corporation. The Malampaya project harnesses natural gas (as an alternative for imported fuel) from the deepwater reservoir northwest of Palawan, which provides 2,700 megawatts of electricity for the country’s domestic and industrial power requirements. Malampaya supplies up to 40 percent of natural gas requirement of the three power plants in Luzon. The plant held its maintenance shutdown from 11 November to 10 December 2013.

9

MWSI rate increases while MWCI rate is unchanged.

connection charges and residual sub‐transmission charges (CC/RSTC) for 2011, 2012, and 2013 and the costs of repair on damages caused by force majeure events such as earthquake, flooding, landslides, and lightning incidents that struck the country in 2011‐2012. Water In Q1 2014, the Metropolitan Waterworks and Sewerage System‐Regulatory Office (MWSS‐RO) reported that the all‐in‐water rate charged by Maynilad Water Services, Inc. (MWSI) increased in February 2014 due to the removal of the refund12 from the foreign currency differential adjustment (FCDA)13 component of the water bill. Meanwhile, the Manila Water Company, Inc. (MWCI) all‐in‐water tariff was maintained.14

12 With MWSI’ partial prepayment of its foreign‐currency denominated loan, MWSI incurred savings in interest which was refunded to its customers by reducing the FCDA component of the water tariff from July 2013 to January 2014. 13 The FCDA is a pass‐through mechanism that accounts for foreign exchange gains or losses arising from the payment of foreign‐denominated concession fees and loans to service expansion and improvement. 14 On 12 September 2013, MWSS‐RO approved the downward adjustments in average basic rates of MWCI at P24.57 and MWSI at P30.28 based on the 2012 average basic rates instead of the two concessionaires’ requests for rate increases covered by their Concession Agreements with the Government. Pending the resolution of the dispute notices filed by the two concessionaires with the International Chamber of Commerce questioning MWSS‐RO’s decision, the basic rates of MWCI and MWSI were maintained at P28.29 per cubic meter and P33.97 per cubic meter, respectively.

10

Aggregate Demand and Supply The Philippine economy continues to expand at an above‐trend rate.

Q4 20137.8 pct

Q4 20136.5 pct

0

2

4

6

8

10

12

Q12009

Q2 Q3 Q4 Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4

year‐on‐year growth in

percent

GDP and GNI (At Constant Prices)

GDP GNI

Strong household spending, exports, and capital formation (particularly durable equipment) drive output growth.

5.6 pct

5.7 pct

-5.2 pct

‐40

‐30

‐20

‐10

0

10

20

30

40

50

Q12009

Q2 Q3 Q4 Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4

year‐on‐year growth in

percent in

real terms

GDP‐Expenditure (At Constant Prices)

HH Consumption Govt Spending Capital Formation5.6 pct ‐5.2 pct 5.7 pct

The country’s real gross domestic product (GDP) expanded by 6.5 percent in Q4 2013, bringing the full‐year 2013 GDP growth to 7.2 percent, above the Government’s growth target of 6.0–7.0 percent for the year. On the expenditure side, the expansion was led by household consumption and exports, which contributed 4.2 ppts and 2.4 ppts, respectively, to the output increase. Meanwhile, on the production side, output growth was led by services, contributing 3.6 ppts to real GDP growth. Similarly, gross national income (GNI) increased by 7.8 percent in Q4 2013 on account of higher net primary income (NPI). The NPI accelerated by 15.1 percent, owing to the continued strong inflows of overseas Filipinos’ remittances during the quarter. Full‐year 2013, GNI increased by 7.5 percent. On a seasonally‐adjusted basis, q‐o‐q GDP growth rose by 1.5 percent in Q4 2013 from 1.3 percent (revised) in Q3 2013. Aggregate Demand Household consumption, which accounts for 73.5 percent of the country’s output on the expenditure side, continued to expand at a robust pace of 5.6 percent in Q4 2013, albeit lower relative to its quarter‐ and year‐ago rates of 6.2 percent. The slowdown in household expenditure could be attributed to higher consumer prices, particularly food prices, due largely to tight domestic supply conditions (triggered by weather‐related production disruptions) and holiday season demand. After posting positive growth since Q2 2011, government consumption declined by 5.2 percent in Q4 2013 due to lower disbursements in personnel services and maintenance and other operating expenses.

11

Economic PerformanceAt constant 2000 prices

Growth rate (in percent)

Sector 2012 2013Q4 Q3 Q4

By expenditure itemHousehold consumption 6.2 6.2 5.6Government consumption 9.5 4.6 ‐5.2Capital formation 9.5 15.6 5.7Fixed capital formation 19.7 11.9 7.0

Exports 8.6 12.8 6.4Imports 8.0 16.4 1.9

Source: NSCB

Capital formation posted a slower growth of 5.7 percent in Q4 2013 compared to its quarter‐ and year‐ago rate of 15.6 percent and 9.5 percent, respectively. Investments in construction declined by 0.5 percent after posting favorable growth in the last six quarters. Investments in breeding stock and orchard development continued to fall (‐3.8 percent) for the third consecutive quarter. Meanwhile, changes in inventories posted lower accumulations compared to the previous year, pulling down GDP growth by 0.2 ppt.15 By contrast, higher investments in durable equipment (15.5 percent), buoyed by increased investments in air transport equipment (225.7 percent) and miscellaneous equipment (92.2 percent), helped boost the overall capital formation.

External trade expanded modestly in Q4 2013. Total exports went up by 6.4 percent, lower than the previous quarter’s 13.7 percent increase. Growth in goods exports (6.2 percent) slowed down on account of lower non‐principal exports (‐8.3 percent), while growth in exports of services (7.0 percent) was weakened by the slight contraction in travel (‐0.6 percent). Similarly, total imports recorded a 1.9 percent increase in Q4 2013, lower than the quarter‐ago rate of 16.4 percent. In particular, the weaker growth in goods imports (1.1 percent) reflected the drop in electronic imports (‐39.1 percent), while the decline in miscellaneous import services (‐5.5 percent) held up the expansion in imports of services (4.6 percent).

15 In end‐Q4 2013, total inventories amounted to P22.5 billion compared to P25.9 billion in the previous year.

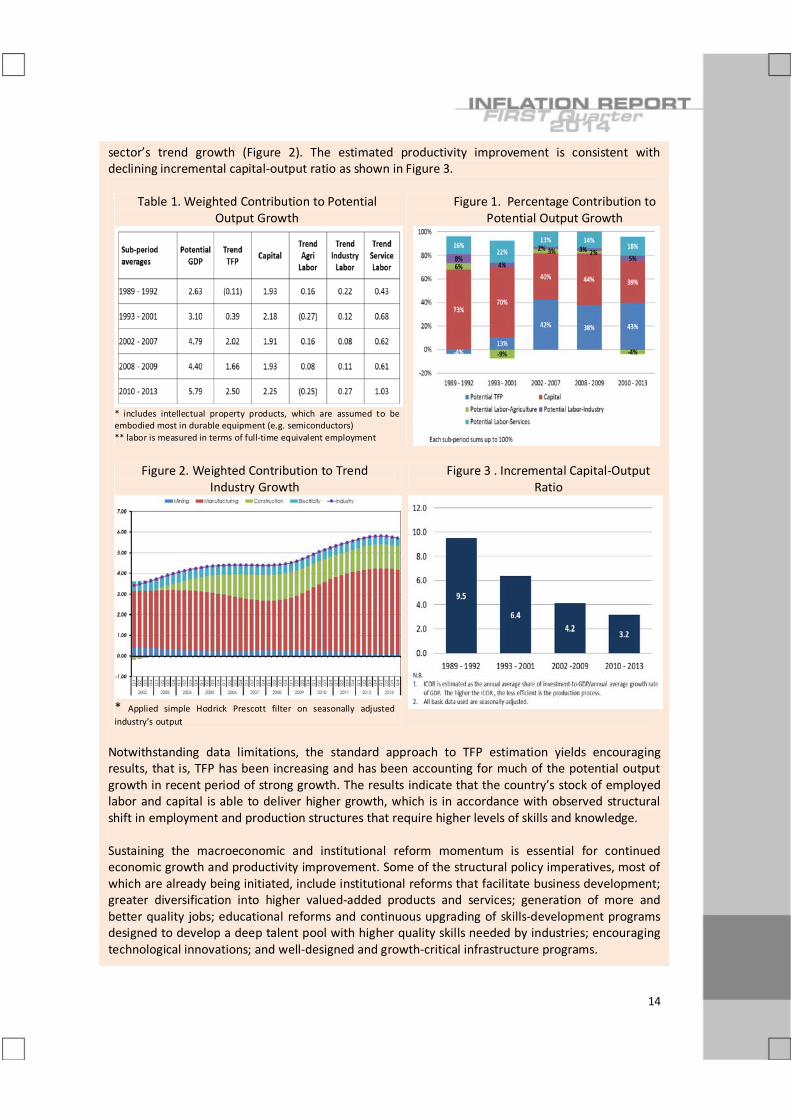

12

BOX ARTICLE: DECOMPOSING SOURCES OF ECONOMIC GROWTH IN THE PHILIPPINES

The literature on Philippine productivity generally points to significant gains in productivity since the early 2000s. However, prior to this period, productivity growth was tepid, in sharp contrast to the experiences of other economies. For the period 1980‐1990, the Asian countries that posted the highest total factor productivity (TFP) growth rates were experienced by the countries with the highest GDP growth rates, i.e., China, Korea, Taiwan, and Thailand (Kawai, 1994). The initial phase of the much‐heralded East Asian economic growth miracle was characterized by capital accumulation, with total factor productivity growth gaining prominence in the subsequent periods (APO, 2011). During the same period, the Philippines posted negative TFP growth rate, contributing to the relatively slower GDP growth rate (Austria, 1998; Cororaton, 2002). There are a number of empirical findings on why the Philippines failed to ride the wave of economic growth that swept across Asia. Among the reasons cited are protectionist policies, policy inconsistency, macroeconomic instability, and institutional weaknesses in the educational, judicial, and property rights system (Austria, 1998; Balisacan and Hill, 2003; Sicat, 2004; and Alba, 2007). Notwithstanding this prognosis, Cororaton (2002) sees productivity gains stemming from the movement of labor out of agriculture into industry and services. Moreover, key structural reform measures were pursued since the early 1990s. These measures pertain to wide‐ranging areas such as the liberalization of the trade regime and foreign exchange regulations, privatization of key government owned corporations and enhancing competition in the banking system, telecommunications and power industries. With these reforms, there have been productivity gains along with GDP growth stabilization and inflation deceleration. Consistent with this, recent BSP staff estimates indicate an improvement in TFP in recent years. Methodology The approach used in estimating TFP is the standard growth accounting method applied on the Cobb‐Douglas aggregate production function.16 Economic growth was decomposed into those arising from the accumulation of labor and capital, with the remainder attributed to contribution from factor productivity growth. The income share of labor was computed based on the National Accounts of the Philippines’ nominal GDP by factor shares. The share of capital was then residually estimated. The estimates presented in this article update and modify those used by Cororaton (2002), which is the most recent study that focuses on the Philippines. Other studies are cross‐country in coverage that assume uniform shares of capital and labor in production across countries (e.g., Park, 2010); or use TFP estimates that are derived from different assumptions and data transformations (e.g., Llanto, 2012). Since there is no official capital stock series, the data on capital were estimated by applying the perpetual inventory method on 2000‐based real gross fixed capital formation (GFCF), with an assumed capital life span of 20 years (i.e., 5 percent depreciation rate).17 Total labor input, on the

16 The Cobb‐Douglas production function takes the form,

where: = GDP = total factor productivity = capital stock = total employment

α = share of capital in production 1-α = share of labor in production

17 Cororaton (2002) used the 1985‐based real gross capital formation (investment) data starting 1946. He assumed 5 percent rate of depreciation. He also estimated three types of capital: machinery, structure, and others. For machinery, investment in durable

13

other hand, has been normalized into full‐time equivalent employment but no adjustment for quality has been made.18 Given that GDP growth rate, capital growth rate, employment growth rate, and the factor shares can be calculated from the data, the total factor productivity growth, unadjusted for cyclical component, has been derived residually.19 To remove the component of TFP that moves with the business cycle, HP filter is applied on unadjusted TFP to get a measure of trend TFP.20 Potential labor supply is derived as the sum of trend sectoral employment and trend hours worked. The capital stock series, being an indicator of overall capacity, is treated as the trend stock. Potential output growth is then derived as the weighted sum of trend growth rates of productivity, potential labor supply, and capital stock.21 Results In analyzing how TFP evolves over time, three sub‐periods, 1989 – 1992; 1993 – 2001 and 2002 – 2013 are examined. The 2002‐2013 period is further sub‐divided into pre‐global financial crisis (GFC), 2008‐2009 GFC, and post‐GFC periods. The estimates show that there has been a general improvement in potential output growth over time, characterized by rising trend TFP growth and factors of production. In the late 1980s to 1992, capital has the highest contribution to potential output growth with TFP having a negative contribution. TFP’s contribution turned positive in 1993 – 2001 and steadily increased over time (Table 1). In terms of percentage contribution, TFP contributed the most beginning 2002, followed by capital and labor services, respectively (Figure 1). This is consistent with the estimates in other studies.22 In terms of sectoral labor contribution, agricultural labor contributed least to growth.23 Industrial labor likewise had a declining contribution to potential output growth, although there has been a reversal in the post global financial crisis period. This could be due to the rebound in manufacturing sub‐sector’s weighted contribution to industrial

equipment was used and for structure, investment in construction was used as bases in deriving initial capital stocks. The sub‐component ‘others’ is residually derived.

18 n

Lh

Lti

tin

tt

⎭⎬⎫

⎩⎨⎧

Σ=

=,

,

1*40

where:

tL = full‐time equivalent employment

tih , = mean hours worked per week

40 = average hours worked in full‐time jobs per week

tiL , = total number of workers who reported for work per industry 19 The log differenced form of the Cobb Douglas production function can be represented in dotted small letters,

. Since and are known, TFP growth ( can be derived residually, i.e.,

20 Alternatively, Kalman filter using capacity utilization as the indicator variable can be used. For the estimation made, simple HP filter is used as there is no sectoral or aggregate measure of capacity utilization for the Philippines. The only available measure of capacity utilization is for the manufacturing sub‐sector.

21 Potential GDP growth is estimated as , as in D’Auria et al (2010). Dotted variables with bar denote trend growth rate.

22 Canlas (2009) reproduced in Llanto (2012), pp 23 – 24 and Asian Productivity Organization (2012), p.78 23 Briones (2013) explained that while there has been an increasing trend in agricultural spending over time, the sector continues to

be beset by weak growth, lack of diversification and competitiveness, tepid productivity growth, and persistent poverty among farmers. He traced the dismal performance to “faulty design and execution of agricultural programs.”

14

sector’s trend growth (Figure 2). The estimated productivity improvement is consistent with declining incremental capital‐output ratio as shown in Figure 3.

Table 1. Weighted Contribution to Potential Output Growth

* includes intellectual property products, which are assumed to be embodied most in durable equipment (e.g. semiconductors) ** labor is measured in terms of full‐time equivalent employment

Figure 1. Percentage Contribution to Potential Output Growth

Figure 2. Weighted Contribution to Trend

Industry Growth

* Applied simple Hodrick Prescott filter on seasonally adjusted industry’s output

Figure 3 . Incremental Capital‐Output Ratio

Notwithstanding data limitations, the standard approach to TFP estimation yields encouraging results, that is, TFP has been increasing and has been accounting for much of the potential output growth in recent period of strong growth. The results indicate that the country’s stock of employed labor and capital is able to deliver higher growth, which is in accordance with observed structural shift in employment and production structures that require higher levels of skills and knowledge. Sustaining the macroeconomic and institutional reform momentum is essential for continued economic growth and productivity improvement. Some of the structural policy imperatives, most of which are already being initiated, include institutional reforms that facilitate business development; greater diversification into higher valued‐added products and services; generation of more and better quality jobs; educational reforms and continuous upgrading of skills‐development programs designed to develop a deep talent pool with higher quality skills needed by industries; encouraging technological innovations; and well‐designed and growth‐critical infrastructure programs.

15

References: Asian Productivity Organization (2012). APO Handbook. Austria, Myrna (1998). Productivity Growth in the Philippines after the Industrial Reforms. Philippine Institute for Development Studies. Discussion Paper No. 98‐26. Briones, Roehlano (2013). Impact Assessment of the Agricultural Production Support Services of the Department of Agriculture (DA) on the Income of Poor Farmers/Fisherfolk: Review of the Evidence. Report submitted to the Department of Budget and Management under the auspices of the Philippine Institute for Development Studies (04 March 2013). Cororaton, Caesar (2002). Total Factor Productivity in the Philippines. Philippine Institute for Development Studies. Discussion Paper No. 2002‐01. D’Auria, F., Denis, C., Havik, K., McMorrow, K., Planas, C., Raciborski, R., Röger, W., and Rossi, A. (2010). The Production Function Methodology for Calculating Potential Growth Rates and Output Gaps. Economic Papers 420, European Commission (July 2010). Gerochi, Hope (2002). Returns to Education in the Philippines. Philippine Review of Economics Vol. XXXIX No. 2 December 2002, pp 37‐72. Isaksson, Anders (2007). Determinants of Total Factor Productivity: A Literature Review. Research and Statistics, United Nations Industrial Development Organization Staff WP 02/2007, July 2007 Kawai, Hiroki (1994). International Comparative Analysis of Economic Growth: Trade Liberalization and Productivity. The Developing Economics XXXII‐4 (December 1994). Llanto, Gilberto (2012). Philippine Productivity Dynamics in the Last Five Decades and Determinants of Total Factor Productivity. Philippine Institute for Development Studies. Discussion Paper No. 2012‐11.

16

Recent indicators of activity suggest buoyant domestic demand. Implied land values continue to trend higher.

Other Demand Indicators Output expansion is expected to be sustained over the near term as higher‐frequency demand indicators continued to show positive readings in the first quarter. Vehicle sales posted strong growth during the quarter, buoyed by brisk consumer demand and attractive financing options offered by industry players. Energy sales also continued to rise on account of increased consumption by the industrial and commercial sectors, while capacity utilization in manufacturing is steady above 80 percent. The PMI likewise remained firmly above the 50 point‐expansion threshold in February, reflecting the significantly higher PMI for services. Similarly, the outlook of businesses and consumers for the following quarter turned more favorable, supporting the continued strength of aggregate demand in the coming months. Property Prices Land Values, Metro Manila Data from Colliers International indicated that implied land values24 in the Makati CBD and Ortigas Center increased in Q4 2013 from their quarter‐ and year‐ago levels. Implied land values in the Makati CBD reached P341,505/sq.m. in Q4 2013, higher by 5.9 percent and 17.0 percent relative to the levels recorded in Q3 2013 and Q4 2012, respectively. Similarly, implied land values in the Ortigas Center rose by 2.6 percent q‐o‐q and 8.0 percent y‐o‐y to P144,683/sq.m. Land values in the Makati CBD are presently at about 80.4 percent of their 1997 levels in nominal terms, but only about 36.6 percent of their 1997 levels in real terms. Likewise, land values in the Ortigas Center were lower than their comparable levels in 1997 in both nominal and real terms by about 74.2 percent and 33.8 percent, respectively.

24 In the absence of reported closed transactions, implied land values based on trends are used by Colliers International to monitor prices.

17

Office vacancy rates tighten. Meanwhile, residential vacancy rates rise.

Vacancy Rates, Metro Manila The office vacancy rate in the Makati CBD declined to 2.3 percent in Q4 2013 from the previous quarter’s rate of 2.8 percent. The office vacancy rate in Q4 2013 was also lower than the 3.5 percent recorded a year ago as all office grades experienced increased take‐up. The office vacancy rate is estimated to remain broadly unchanged up to Q4 2014 given pre‐committed lease agreements in incoming new office supply. The residential vacancy rate in the Makati CBD of 11.0 percent in Q4 2013 was higher than the previous quarter’s rate of 10.1 percent and the year‐ago rate of 10.0 percent. Residential vacancy rates rose as tenants for both luxury and other grade segments explored alternative locations such as the Bonifacio Global City (BGC). The residential vacancy rate in the Makati CBD is expected to decrease to the 9.0‐percent range until Q4 2014 due to limited availability of residential units.

Office rental values trend higher.

Rental Values, Metro Manila25 Monthly office rents in the Makati CBD reached P793/sq.m. in Q4 2013, representing an increase of 1.4 percent from the previous quarter.26 Similarly, monthly office rents in the Makati CBD were higher by 10.2 percent relative to Q4 2012. The increase in rental rates was due to the continued take‐up of office space coupled with limited supply in the Makati CBD. Office rental values for premium grade offices in Q4 2013 were slightly above their 1997 levels in nominal terms. In real terms, office rental values were about 46.1 percent of the comparable levels in 1997.

25 Housing rentals account for 13.8 percent of the 2006‐based CPI basket. The NSO only surveys rentals ranging from around P300‐P10,000/month to compute rent inflation. However, the rental values discussed in this section pertain to high‐end rented properties, which may be considered as indicators of wealth and demand. 26 This was computed as the average of the rental values for the Premium, Grade A and Grade B segments. Premium refers to office space with capital values of P75,000/sq.m. and above; Grade A, between P65,000 and P75,000/sq.m.; and Grade B, P65,000/sq.m. and below.

18

Residential rental values continue to increase. Capital values for office and residential buildings are higher.

Monthly rents for prime 3‐bedroom condominium units in the Makati CBD rose to P805/sq.m. in Q4 2013, registering a 0.6‐percent growth from the previous quarter. Likewise, monthly rents for the 3‐bedroom segment were higher by 11.8 percent compared to the year‐ago level. Residential rental values in Q4 2013 were above their 1997 levels in nominal terms but were only about 77.2 percent of their 1997 levels in real terms.

Jones Lang Lasalle estimates showed that average Grade A office rentals in the Makati CBD and BGC reached P9,887/sq.m. per annum in Q4 2013, an increase of 1.3 percent compared to the previous quarter and 4.3 percent compared to the same quarter in 2012. Office rental values continue to be driven primarily by sustained leasing demand from the offshoring and outsourcing (O&O) sector. Traditional office demand from other sectors namely, information technology, consumer goods, and pharmaceuticals, also contributed to the continued take‐up of office space. Capital Values, Metro Manila Capital values27 for office buildings in the Makati CBD were higher in nominal terms than their quarter‐ and year‐ago levels. Grade A office capital values in the Makati CBD rose to P89,593/sq.m., higher by 2.0 percent and by 5.8 percent compared to their quarter‐ and year‐ago levels, respectively. Grade A office capital values in Q4 2013 were also higher than the 1997 levels in nominal terms. Nevertheless, in real terms, office capital values were about 51.4 percent of the comparable levels in 1997. Capital values for luxury residential buildings in Makati CBD were also higher than their quarter‐ and year‐ago levels. Average prices for luxury residential condominium units increased by 2.2 percent q‐o‐q and 14.4 percent y‐o‐y in

27 The capital value represents the probable price that the property would have fetched if sold on the date of the valuation. The valuation includes imputed land and building value.

19

Q4 2013. Residential capital values for luxury residential buildings28 in Q4 2013 were above their 1997 levels in nominal terms. In real terms, residential capital values were about 63.1 percent of the comparable levels in 1997.

Vehicle sales increase on brisk demand. Growth in overall energy sales slows down on lower residential sales.

Vehicle Sales Overall vehicle sales from the Chamber of Automotive Manufacturers of the Philippines (CAMPI)29 posted double‐digit growth in the first two months of Q1 2014. Vehicle sales increased by 21.4 percent y‐o‐y from a 10.2 percent growth recorded in the previous quarter (October‐November 2013). CAMPI attributed the strong sales of the local automotive industry to continued brisk consumer demand coupled with attractive financing options offered by industry players. Passenger car sales grew by 24.0 percent y‐o‐y in Q1 2014 (January‐February), rising to a total of 10,918 units from 8,808 units sold in the same period in 2013. Meanwhile, commercial vehicle sales, which account for 66.4 percent of total vehicle sales, expanded by 20.2 percent in the first two months of Q1 2014. Commercial vehicles sold during the quarter reached 21,552 units from 17,934 units in the same period of 2013. Energy Sales

Meralco’s energy sales for the first two months of Q1 2014 expanded by 1.7 percent, slower than the 2.5 percent growth reported in the same period a year ago. The energy sales from the industrial sector grew at a faster pace of 4.9 percent (from 4.3 percent in Q1 2013). According to Meralco, growth in industrial energy sales was driven by merchandise exports and increased production of the manufacturing sector.

28 In terms of location, luxury residential units are located within the CBD core and have high quality access to/from and have superior visibility from the main avenue. Meanwhile, in terms of general finish, luxury residential units have premium presentation and maintenance. 29 CAMPI represents the local assemblers and manufacturers of vehicle units in the Philippine automotive industry. The following are the active members of CAMPI, (1) Asian Carmakers Corp., (2) CATS Motors, Inc., (3) Columbian Autocar Corp., (4) Honda Cars Philippines, Inc., (5) Isuzu Philippines Corp., (6) Mitsubishi Motors Philippines Corp., (7) Nissan Motor Philippines Corp., (8) Suzuki Philippines Inc., (9) Toyota Motor Philippines Corp., and (10) Universal Motors Corp. As of July 2013, sales from CAMPI accounted for 85 percent of overall vehicle sales that include sales from the Association of Vehicle Importers and Distributors (AVID).

20

‐10

‐5

0

5

10

15

20

Q1 20

09 Q2

Q3

Q4

Q1 20

10 Q2

Q3

Q4

Q1 20

11 Q2

Q3

Q4

Q1 20

12 Q2

Q3

Q4

Q1 20

13 Q2

Q3

Q4

Q1 20

14

in percent

Meralco Energy SalesIn percent

Q1 20141.7 pct

Capacity utilization in manufacturing remains above 80 percent.

65

70

75

80

85

90

2008 2009 2010 2011 2012 2013 2014

Monthly Average Capacity Utilization for ManufacturingIn percent

January 2014 = 83.2

Source: NSO Manufacturing output posts slower growth.

‐35

‐25

‐15

‐5

5

15

25

35

45

2008 2009 2010 2011 2012 2013 2014

in percent

Volume of Production Value of Production

Source: NSO

Volume and Value Indices of Manufacturing Production

January 20147.2 pct

January 20147.3 pct

Commercial sector energy sales also increased by 2.4 percent (but lower than 2.6 percent in Q1 2013) with the real estate and private services sectors as the main contributors. By contrast, residential energy sales declined by 2.6 percent on lower demand due to cooler temperature. Capacity Utilization The average capacity utilization rate in the manufacturing sector was broadly steady in January 2014 at 83.2 percent, based on the NSO’s Monthly Integrated Survey of Selected Industries (MISSI). The proportion of establishments that operated at 80 percent or more was 56.4 percent in January. Volume and Value of Production Preliminary results of MISSI showed that the value of production index (VaPI) grew by 7.3 percent in January 2014, slower compared to the 20.2 percent growth a month ago. The continued expansion in VaPI was driven by the increased in production values of chemical products, furniture and fixtures, tobacco products, publishing and printing, machinery except electrical, textiles, leather products, fabricated metal products, electrical machinery, non‐metallic mineral products, petroleum products, and rubber and plastic products. Likewise, the volume of production index (VoPI) rose by 7.2 percent in January 2014, but slower than the 25.2 percent (revised) figure in the previous month. The growth in production output was attributed to the increased VoPI of the following items: furniture and fixtures, tobacco products, publishing and printing, machinery

21

except electrical, textiles, fabricated metal products, leather products, chemical products, electrical machinery, and non‐metallic mineral products sectors.

Business sentiment for the following quarter remains bullish.

Business Expectations Survey

Index 2013 2014

Q1 Q2 Q3 Q4 Q1

Business Outlook Index

Current Quarter 41.5 54.9 42.8 52.3 37.8

Next Quarter 56.4 46.2 60.0 40.7 50.8

Source: BSP

Consumer outlook for the current and next quarter is favorable.

Business Expectations Survey Results of the BES30 for Q1 2014 showed a less favorable confidence index (CI) for the current quarter, but a more optimistic index for the next quarter. Overall CI for Q1 2014 declined by 14.5 index points to 37.8 percent from 52.3 percent in the previous quarter. However, the next quarter CI rose by 10.1 index points to 50.8 percent from 40.7 percent a quarter ago, indicating a more positive business outlook in Q2 2014. Business outlook in both NCR and AONCR tracked the sentiment of businesses at the national level—less sanguine in Q1 2014, but more positive in the following quarter. The less favorable outlook of respondents for Q1 2014 was due to expectations of seasonal slowdown in business activity and moderation of consumer demand after Christmas; weaker peso that could hurt importers; adverse effects of typhoon Yolanda on crop production and businesses; rising prices of oil and other utilities; strong market competition; and lack of supply of raw materials. The sentiment of businesses in the Philippines mirrored the weak business outlook in Singapore and China, in contrast to the more buoyant outlook of businesses in the United Kingdom, Germany, Hong Kong SAR, India, and New Zealand. Meanwhile, the business outlook in the US and South Korea was steady in Q1 2014. Consumer Expectations Survey Results of the Consumer Expectations Survey31 (CES) showed favorable consumer sentiment for the current quarter, the next quarter, and the year ahead.

30 The Q1 2014 BES was conducted from 9 January ‐20 February 2014 among 1,525 firms nationwide, drawn from SEC’s’ Top 7000 Corp. in 2010 and Business World’s Top 1000 Corporations in 2012. 31 The Q1 2014 CES was conducted during the period 21 January‐3 February 2014 covering 5,870 households, of which 49.6 percent were from the NCR and 50.4 percent from the AONCR.

22

Consumer Expectations SurveyIndex 2013 2014

Q1 Q2 Q3 Q4 Q1

Current Quarter ‐11.2 ‐5.7 ‐7.9 ‐21.3 ‐18.8

Next 3 months 7.8 4.1 5.7 2.8 5.4

Next 12 months 18.5 16.1 15.8 14.1 19.3

Source: BSP

Overall consumer CI in Q1 2014 improved slightly to ‐18.8 percent from ‐21.3 percent in the previous quarter. The modest improvement (though still negative) in consumer outlook during the quarter was attributed to the availability of more jobs, increased number of employed family members, more investment prospects, higher income, stronger business activity, and good harvests. The upbeat sentiment among consumers in the Philippines mirrored the outlook of consumers in Germany, Indonesia, South Korea, and Taiwan. By contrast, the outlook of consumers in Australia, China, Japan, Thailand, and the United States was less optimistic. Meanwhile, the consumer outlook for Q2 2014 and the year ahead was optimistic with the CI at 5.4 percent and 19.3 percent, respectively. The main reasons for the improved sentiments of consumers were expectations of more job opportunities and good weather conditions in the next quarter.

PMI points to sustained expansion in domestic activity.

58.2

61.1

40

45

50

55

60

65

70

75

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov Dec Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov Dec Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov Dec Jan

Feb

2011 2012 2013 2014

Consolidated PMI Manufacturing Retail/Wholesale Services

Purchasing Managers' Index

55.4

51.6

Purchasing Managers’ Index32 The results of the monthly PMI survey reflects sustained economic expansion in February 2014. The composite PMI remained firmly above the 50‐point threshold at 58.2, higher than the 54.0‐point level recorded in December 2013 and 57.4‐point level posted in the same period in 2013. The higher composite PMI reflected the increased PMI recorded across all sectors—manufacturing, services, and retail and wholesale—in February 2014 relative to December 2013.

32 The PMI for the Philippines is compiled by the Foundation of the Society of Fellows in Supply Management, Inc. (SOFSM), the advocacy arm of PISM.

Source: Philippine Institute of Supply Management (PISM)

23

Export growth rises on higher shipments of manufactures. Exports of GoodsGrowth rate (in percent)

Commodity Group2013

Q3 Q4

Coconut products 18.6 ‐25.2

Sugar and Products 90.6 15.2

Fruits and Vegetables 30.7 ‐2.7

Other Agro‐based products 28.5 58.5

Forest products ‐5.8 10.1

Mineral products 94.2 5.0

Petroleum products 299.6 ‐23.5

Manufactures 1.7 19.4

Special transactions ‐28.8 ‐43.4

Total Exports 8.4 16.1

Source: PSA; BSP Staff Computations Lower imports of capital goods drive down total imports of goods. Imports of GoodsGrowth rate (in percent)

Commodity Group2013

Q3 Q4

Capital Goods 10.6 ‐5.2

Raw Materials & Intermediate Goods

16.7 ‐1.1

Mineral Fuels & Lubricants ‐6.0 ‐2.9

Consumer Goods 2.2 3.5

Special Transactions ‐24.9 7.6

Total Imports 7.6 ‐2.0Source: PSA; BSP Staff Computations

The services sector remains the main driver of output growth on the production side.

External Demand Exports Based on the trade data reported by the Philippine Statistics Authority, exports of goods grew by 16.1 percent in Q4 2013, significantly higher than the 8.4‐percent growth posted in the previous quarter. The improved export performance was driven mainly by higher shipments of manufactures (19.4 percent). Imports Imports of goods declined by 2.0 percent in Q4 2013, a reversal of the 7.6‐percent growth recorded in the previous quarter. The drop in imports can be attributed primarily to lower inward shipments of capital goods (‐5.2 percent) during the quarter. Aggregate Supply The services sector, which comprised 55.3 percent of GDP, continued to increase, albeit at a slower pace of 6.5 percent in Q4 2013 from 7.4 percent in Q3 2013. Notwithstanding the expansion in all sub‐sectors (led by trade and repair of motor vehicles, motorcycles, personal and household goods (7.4 percent)), the slowdown in the services sector was traced largely to the deceleration in the growth of real estate, renting, and business activities, which grew by 6.3 percent in Q4 2013 from 11.7 percent in the previous quarter.

24

1.1 pct

6.5 pct

8.4 pct

‐10

‐5

0

5

10

15

20

Q12009

Q2 Q3 Q4 Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4

year‐on‐year growth in percent in re

al te

rms

GDP‐Production (At Constant Prices)

Agriculture Industry Services

Economic PerformanceAt constant 2000 pricesGrowth rate (in percent)

Sector 2012 2013Q4 Q3 Q4

By industrial originAgri, Hunting, Forestry & Fishing 4.9 0.3 1.1Agriculture and Forestry 5.2 0.3 2.4Fishing 3.4 0.5 ‐4.4

Industry 8.9 8.3 8.4Mining and quarrying 2.8 4.7 ‐10.4Manufacturing 5.5 9.7 12.3Construction 29.9 4.5 ‐0.8Electricity, gas and water supply 3.4 6.7 2.5

Services 6.5 7.4 6.5Transport., Storage, & Comm. 4.4 6.5 6.2Trade 6.6 6.1 7.4Finance 8.8 12.1 9.9Real estate, Rent, & Bus. Act. 6.5 11.7 6.3Public administration & defense 8.2 2.6 0.5Other services 5.8 4.5 5.4

Source: NSCB

The industry sector maintained its growth momentum at 8.4 percent in Q4 2013. Contributing 2.8 ppts to GDP growth, the expansion in the industry sector was driven primarily by higher manufacturing output (12.3 percent). By contrast, after posting positive growth since Q4 2011, output growth in construction declined by 0.8 percent.

The agriculture, hunting, forestry, and fishery (AHFF) sector continued to recover, growing by 1.1 percent in Q4 2013 from 0.3 percent in the previous quarter. The growth in the AHFF reflected mainly the increase in the agriculture and fishery sub‐sector (2.4 percent) due, in turn, to higher palay output (8.1 percent). The increase was, however, curbed by the output decline in the fishing sub‐sector (‐4.4 percent).

Labor Market Conditions

The unemployment rate rises driven by developments in the NCR.

January 20147.5 pct

January 201419.5 pct

0

5

10

15

20

25

2008 2009 2010 2011 2012 2013 2014

in percent

Unemployment and Underemployment

Unemployment Underemployment

Based on the preliminary results of the January 2014 Labor Force Survey (LFS),33 the unemployment rate was estimated at 7.5 percent, higher than the quarter‐ago and year‐ago rate of 6.5 percent and 7.1 percent, respectively. The number of unemployed persons rose by 7.0 percent y‐o‐y in January 2014 after falling by 5.8 percent in October 2013, driven by developments in the NCR. The NCR recorded the highest unemployment rate due to the in‐migration of individuals from rural areas and from disaster‐stricken areas seeking opportunities for employment.34 Meanwhile, the proportion of

33 The January 2014 LFS excludes data on Region VIII. 34 National Economic Development Authority press release entitled, “NEDA pushes for more job opportunities in provinces near disaster‐stricken areas,” available online at http://www.neda.gov.ph/?p=2685.

25

underemployed to total employed persons decreased to 19.5 percent in January 2014 from 20.7 percent in the same period last year.35 The number of employed persons increased slightly by 0.8 percent y‐o‐y, supported by the increase in employment in the agriculture and services sector, which both contributed 0.3 ppt to total employment growth. Nonetheless, the slowdown in employment growth in the services sector (0.2 percent from 1.6 percent in October 2013) restrained in part the increase in both the agriculture (1.1 percent) and industry (2.1 percent) sectors. In terms of major occupation groups, the y‐o‐y increase in the employment level could be traced largely to the higher number of employed officials of government, and farmers and fishermen.

35 Underemployed persons include all employed persons who express the desire to have additional hours of work in their present job or an additional job, or to have a new job with longer working hours. Visibly underemployed persons are those who work for less than 40 hours during the reference period and want additional hours of work.

26

II. MONETARY AND FINANCIAL MARKET CONDITIONS