PwC’s Insurance Insights · PwC’s Insurance Insights Analysis of regulatory changes and impact...

31

PwC’s Insurance Insights Analysis of regulatory changes and impact assessment from August–October 2017

Transcript of PwC’s Insurance Insights · PwC’s Insurance Insights Analysis of regulatory changes and impact...

PwC’s Insurance InsightsAnalysis of regulatory changes and impact assessment from August–October 2017

2 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017 Other key guidelines issued by the IRDAI from August–October 2017 Contacts

The insurance sector witnessed a surge in the collection of new business premium. A snapshot of premium underwritten across general, life and health insurance is presented below along with the current market share from July to September 2017.

• The figures clearly depict the dominance of the public sector in terms of premium collection and market share in both life and general insurance.

• In the case of general insurance, the private sector was neck and neck with public sector undertaking (PSU) insurers, whereas in the case of the life insurance sector, the Life Insurance Corporation of India (LIC) enjoyed a market share nearly three times that of private life insurers.

• In terms of premium collections, the LIC numbers are more than double those of private life insurers.

3 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017 Other key guidelines issued by the IRDAI from August–October 2017 Contacts

Market share up to September 2017

Private life insurers

LIC

74%

26%

Life insurance sector

Source: IRDAI Source: IRDAI

Private life insurers

Premium in crore

For July to Sepember 2016

For July to September 2017

Up to 30 September 2016

Up to 30 September 2017

12335.35 13892.99 21072.99 23841.06

LIC 32568.95 44940.20 55163.17 68224.29

0.0010000.0020000.0030000.0040000.0050000.0060000.0070000.0080000.00

Private life insurers LIC

General insurance sector

Market share up to September 2017

Private sector general insurers

Stand-alone private health insurers

Public sector general insurers

Specialised PSU insurers

44%

4%

44%

8%

0.005000.00

10000.0015000.0020000.0025000.0030000.0035000.00

Private sectorgeneral insurers

Stand-alone private health insurers

Public sectorgeneral insurers

Specialised PSUinsurers

Pre

miu

m in

cro

re IN

R

General insurers

New business premium

For July to September 2016 For July to September 2017

Up to 30 September 2016 Up to 30 September 2017

4 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017 Other key guidelines issued by the IRDAI from August–October 2017 Contacts

1 Central Vigilance Commission. (2017). Vigilance Manual 2017. Retrieved from http://cvc.nic.in/vmn06092017.pdf (last accessed on 21 November 2017)

The Insurance Regulatory and Development Authority (IRDAI [the Authority]) launched the seventh edition of the Vigilance Manual1 with the Central Vigilance Commission (CVC) in September 2017. The highlights of the CVC Vigilance Manual are mentioned below.

• Details of appointment, role, functions and responsibilities of chief vigilance officers

• Complaints handling policy of the CVC and action taken on complaints

• Handling of complaints received under the public interest disclosure and protection of informers (PIDPI) resolution and protection to whistle-blowers

• Introduction to agencies for conducting preliminary enquiries/investigations and preliminary enquiry by departmental agencies

• Enquiry/investigation by the CBI, action on CBI reports and providing assistance to and co-operating with the CBI on enquiries/investigations

• Disciplinary proceedings and suspension, disciplinary rules and penalties

• Specific issues related to public sector banks and insurance companies

• Preventive vigilance

5 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017 Other key guidelines issued by the IRDAI from August–October 2017 Contacts

Current trends in the insurance sector (cyber insurance)

Cyber insurance – the way forward

A cyber insurance policy, also referred to as cyber risk insurance or cyber liability insurance coverage (CLIC), is designed to help an organisation mitigate cyber risk exposure from risks relating to information technology infrastructure and activities by offsetting costs involved with recovery after a cyber-related security breach or cyberattack.

Cyber insurance – its coverage

Cyber insurance typically covers first-party coverage against losses such as data destruction, extortion, theft, hacking and denial of service attacks; liability coverage indemnifying companies for losses caused to others, for example, by errors and omissions, failure to safeguard data or defamation; and other benefits including regular security audit, post-incident public relations and investigative expenses and criminal reward funds.

Current and future market status – global and Indian scenario

As enterprises are moving their IT systems and data to the cloud, on-premise risk becomes smaller and cloud provider-related risk becomes larger. At the same time, insurance data and insurance analytics are growing, making cyber insurance more ‘off-the-shelf’ and creating more opportunities for smaller organisations to benefit from protection through cyber insurance.

The rising number of cyberattacks over the past 2–3 years is the prime factor driving the market. The global cyber insurance market is expected to generate 14 billion USD by 2022. This figure represents a compound annual growth rate (CAGR) of nearly 28% from 2017 to 2022.2

2 Allied Market Research. (2016). Cyber insurance market. Retrieved from https://www.alliedmarketresearch.com/cyber-insurance-market (last accessed on 21 November 2017)

6 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017 Other key guidelines issued by the IRDAI from August–October 2017 Contacts

Checklist for insurance companies when offering coverage

A cyber insurer must identify the risks associated with an organisation if it is to accurately calculate a policy premium. A list of factors that an insurance company must consider is presented below:

• Industry sector, geography, size, solutions supplied and security procedure

• If the organisation has assessed its vulnerability to cyberattacks and is following best practices by enabling defences and controls to protect against attacks as much as possible

• Track records of incidents and previous claims

• The kind and volume of data handled by the organisation

• Employee education in the form of security awareness, especially for phishing and social engineering

As cyber insurance coverage becomes more standardised, an insurer might request an audit of an organisation’s

processes and governance as a condition of coverage.

Limitations

Even though cyber insurance has been in the market for over two decades, companies still face a limited choice of cover. Even with the most comprehensive cyber coverage, companies still have the responsibility to improve their internal privacy and security measures. Ultimately, prevention is still the best form of insurance against a data breach. All organisations should regularly assess their privacy and security risks and then take actions to mitigate the identified gaps.

Conclusion

Given the increasing complexity and likelihood of data breaches, companies are looking for cyber insurance that provides a measure of security. Cyber insurance, unlike traditional insurance, is designed to meet the needs of companies in the digital age. It is one area of insurance where we continue to find innovation.

7 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017 Contacts

Discussion Paper on ‘Telematics and Motor Insurance’ (Exposure Draft)

New technologies hold the potential to transform both related and unrelated industries. One such area that is inevitably affected by innovation and breakthrough technologies is insurance. Insurers and auto manufacturers worldwide have begun to focus on telematics as the next wave of creating deeper customer relationships. This has resulted in a convergence of new business models, leading to a connected lifestyle.

The Authority has launched an exposure draft for comments from sector experts, who have claimed that the Indian motor insurance sector is expected to go through a phase of technological disruption. Undoubtedly, this technological adoption will result in immense benefits but there will also be some disadvantages that the sector will have to accept. We have made an attempt to simplify the advantages and disadvantages that the Indian insurance industry will have face if telematics is practiced.

Ref: IRDAI/NL/PNTC/MISC/179/08/2017 Date of issue: 3 August 2017

8 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface

Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017 Contacts

Paper on ‘Telematics and Motor Insurance’ (Exposure Draft)

Ref: IRDAI/NL/PNTC/MISC/179/08/2017 Date of issue: 3 August 2017

Advantages of telematics to the insurer, policyholder and society

• Better risk assessment and efficient claims services

• Accurate estimation of accident damages and fraud reduction by enabling analysis of driving data

• Next-gen analytical insights through predictive analysis

• Improved profitability and increased retention rate

• Estimation of the severity of an accident within a fraction of time

• Efficient claims handling process and reduction in adjustment expenses

• Awareness of better driving techniques which ultimately leads to better drivers

• Safer roads for all citizens and reduced traffic congestion and pollution

• Tracking of lost and stolen vehicles and cost savings related to personnel, fuel and maintenance

• Geofencing and real-time tracking of cars with the help of GPS

• Only professional installers can fit the telematics device in a vehicle

• Higher premium if a driver clocks up a considerable amount of miles

• Portability of data in case a policyholder switches from one insurer to another

• Privacy of data recorded by the instrument in the vehicle

• Huge cost of implementation which would eventually impact the pricing methodology

Disadvantages of telematics

9 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Date of issue: 2 August 2017

Second Amendment to IRDAI’s (Payment of commission, remuneration or reward to insurance agent or insurance intermediaries) Regulations, 2016 (Exposure Draft)

The Authority, through an exposure draft, released a second amendment to the IRDAI’s (Payment of commission, remuneration or reward to insurance agent or insurance intermediaries) Regulations, 2016, earlier notified on 14 December 2016. The exposure draft concentrates on the remuneration payable to various intermediaries as mentioned below:

• Reward to individual agent or insurance intermediaries by insurers

• Remuneration payable to the insurance marketing firm

• Health insurance (general and stand-alone health insurers)

• Motor (comprehensive) – motor insurance

Based on various representations received from insurers, the Authority,

through this exposure draft, brings to notice the following significant changes.

Implications for insurers

• The Authority limits the maximum commission/remuneration payable to all the intermediaries, as mentioned above.

• The insurance marketing firm (IMF) is entitled to fees for undertaking insurance service activities based on mutual agreement between the IMF and the insurance company. An agreement should be entered into at the outset with the basis of fees clearly addressed.

• The IMF will continue to be governed under the IRDA’s (Insurance Marketing Firm) Regulations, 2015, which are at

variance with the rewards under the IRDAI’s (Payment of commission, remuneration or reward to insurance agent or insurance intermediaries) Regulations, 2016.

• Common service centres (CSCs), Special purpose vehicles (SPVs) and microinsurance agents will continue to be governed under the provisions of their respective regulations.

• The Authority permits commission/remuneration on the motor TP part of the motor (comprehensive) policy from the fourth year of registration of the automobile vehicle.

• In order to improve insurance coverage of these two wheelers, the Authority allows insurers to pay slightly higher commissions/remuneration to insurance agents or insurance intermediaries.

Mandatory compliance

• The Authority mandated insurers implement the above changes from 1 November 2017.

• The Authority invites all stakeholders to offer their comments/suggestions on the proposed regulations for consideration of the same by the IRDAI.

• The comments/suggestions should be submitted by 9 August 2017 in the format attached in the exposure draft.

10 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Ref: IRDA/F&A/OFC/01/2014-15 Date of issue: 4 August 2017 Applicability: All insurers

Clarification regarding IRDAI (Other Forms of Capital) Regulations, 2015

Pursuant to the IRDAI (Other Forms of Capital) Regulations, 2015, some insurers had approached the Authority with proposals for raising capital in other forms such as preference shares and subordinated debt. Based on the guidelines, some insurers issued debentures to raise capital but later approached the Authority seeking clarification on whether they are required to create debenture redemption reserves (DRRs), as envisaged in section 71 of the Companies Act, 2013.

Mandatory compliance

In response to the insurers seeking clarification, the Authority mentioned:

• Insurers raising capital by the issue of debentures shall create a DRR in terms of the Companies Act, 2013, and rules made thereunder and a DRR of 25% of the value of outstanding debentures shall be adequate.

• The a shall be ignored and not considered as a liability for the purpose of computation of solvency margin and ratio.

11 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Date of issue: 8 August 2017 Applicability: All insurers

Report of IRDAI Committee on Risk Based Capital (RBC) Approach and Market Consistent Valuation of Liabilities (MCVL) of Indian Insurance Business3

The Authority formed a committee vide its order Ref: IRDA/ACT/ORD/MISC/116/06/2016 dated 10 June 2016. The Committee had earlier submitted the first part of its report on ‘Market consistent valuation of liability’ on 19 November 2016 and hereby submits part 2/the final part of the report, consisting of the following aspects:

• Pros and cons of the current solvency regime and risk-based capital regime in the insurance sector (life, non-life, stand-alone health insurance and

reinsurance) and recommendation of a suitable approach in the current Indian context.

• The recommended approach with respect to the following aspects:

- Broad time frame for completion of entire exercise under the recommended approach

- Whether the IRDAI will require help of professional actuarial consultants on paid basis during this exercise. If yes, what should be the terms of reference for consultants?

3 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3215&flag=1

12 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Modification to Guidelines on Point of Sales (POS) – Life Insurance

The Authority invites reference to Guidelines on Point of Sales (POS) – Life Insurance Products bearing Ref. No. IRDA/LIFE/GDL/GLD/222/11/2016 dated 7 November 2016 on:

Section 2 (i) – ‘Categories of POS Products’, wherein the description of categories of POS Products is provided

Annexure - I (a) – ‘pure term insurance product with or without return of premium’, wherein the maximum limit of sum assured under the pure term product was capped up to Rs 25 Lakhs (excluding ADB Rider).

Implication for insurers

Based on the feedback received from the insurance industry, the Authority has decided:

• To include the non-linked, non-par health insurance products with fixed benefits under the sec 2(i) categories of POS products. The product parameters for the same are mentioned in Annexure-A attached to this circular. All the other provisions in the referred guidelines are applicable to the POS health products also.

• To relax the upper limit of ‘sum assured on death’ under pure term life insurance product under Annexure - I (a) and hence the modification be read as follows:

- Sum assured on death: Maximum no limit, subject to non-medical underwriting only

Ref: IRDAI/LIFE/CIR/MISC/POS/185/08/2017 Date of issue: 8 August 2017

13 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Guidelines on Transitory Provisions under IRDAI (Appointed Actuary) Regulations, 2017

The Authority has issued the following guidelines on the exercise of power conferred under Regulation 6 and Regulation 13 of the IRDAI (Appointed Actuary) Regulations, 2017, and by sections 14 (2) (e) of the IRDA Act, 1999, as amended from time to time.

• These guidelines shall supersede the guidelines vide IRDAI/Actl/ GDL/MISC/055/03/2016 dated 22 March 2016 on appointment of appointed actuaries and their mentors.

• Also these guidelines shall come into force with immediate effect. The existing arrangements not complying with these guidelines shall cease to exist within a period of three months from the date of publication of these guidelines.

The Authority, under the said guidelines, provides certain leverage to insurers, as mentioned below:

• Exemption for minimum relevant experience required for the appointment of an appointed actuary

• Exemption for minimum experience in annual statutory valuation

• Allowance to an insurer/reinsurer to carry on business without an appointed actuary for a period not exceeding one year

• Conditions for appointment of mentors to appointed actuaries

• Undertaking by an applicant actuary for mentorship

• Certification by the principal officer/CEO of the insurer

• List of actuarial statements/certificates/reports to be submitted to the Authority with due dates by life insurers, general insurers, reinsurers and standalone health insurers

Ref: IRDA/ACT/GDL/MISC/194/08/2017 Date of issue: 17 August 2017 Applicability: To all CEOs of life, general, stand-alone health insurers, reinsurers

14 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Working Group on new standard on Insurance Contracts (equivalent to IFRS 17 Insurance Contracts)

Introduction

The Authority has formulated a working group for the early adoption of the new standard on insurance contracts in India which is the equivalent of IFRS 17, Insurance Contracts, promulgated by the International Accounting Standards Board (IASB) on 18 May 2017.

The terms of reference for the working group are as under:

• Review the new standard ‘IFRS 17, Insurance Contracts’ and identify relevant areas/aspects which require suitable adoption in the Indian context.

• Identify changes arising out of the new standard on insurance contracts:

- To be carried out in the draft regulations/formats recommended by the Implementation Group vide their report dated 29 December 2016

- To be carried out in other regulations/guidelines, etc.

• Any other aspects that may arise in the course of implementation of the standard in the insurance sector.

The Authority mandates the working group to report within three months of this order.

Ref: IRDA/F&A/ORD/ACTSI 184 I 08 12017 Date of issue: 21 August 2017

15 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Right to Information Act, 2005

IntroductionThe IRDAI is obliged to provide information to the public in accordance with the provisions of the Right to Information Act (RTI), 2005. The right to information includes access to information, which is held by or under the control of any public authority and includes the right to inspect the work, document, records, taking notes, extracts or certified copies of documents/records and certified samples of the materials and obtaining information which is also stored in electronic form.

The IRDAI’s obligation under the act is to provide information to the public in accordance with the RTI Act, 2005. Under the said act, the IRDAI has taken the following measures to create awareness amongst the public of their right in accordance with the RTI Act.

IRDAI websiteThe IRDAI maintains an active website (http://www.irdai.gov.in) and the site is updated regularly with information pertaining to acts, regulations, information relating to insurers/

reinsurers, agents, training institutes, appointed actuaries, surveyors, third-party administrators, insurance brokers, corporate agents, insurance council and ombudsmen, annual report/IRDA journal and press releases.

Complaints against insurance companiesThe IRDAI has provided a separate channel for lodging complaints against the deficiency of services rendered by insurance companies to its nodal offices and further to insurance ombudsmen, if required. For further details on the Insurance Ombudsman Scheme and their contact numbers, the public can visit http://www.gbic.co.in/ombudsman.html.

Complaints from policyholdersPolicyholders are required to approach the grievance/customer complaints cell of the concerned insurer and can further reach out to the IRDAI grievance cell in case of unsatisfactory response from the insurer. Policyholders may visit http://www.policyholder.gov.in/Report.aspx# for details on the IRDAI grievance cell.

Making an application under the RTI Act, 2005Citizens of India will have to make the request for information in writing, clearly specifying the information sought under the RTI, 2005. The IRDAI has defined the process as to how and where an application needs to be filed. Also, as per the act, information will be furnished only to citizens of India. Every policyholder applying for such information will have to pay for the application as per requirements of the RTI Act. The IRDAI will reply to such applications within 30 days from date of receipt of the application for information.

The RTI, 2005, under sections 8 and 9, exempts certain categories of information from disclosures to the public by the IRDAI. The members also have a right to appeal in case they are not satisfied with the information provided/information not provided by the IRDAI. The members can further make an appeal to the Central Information Commissioner appointed in terms of chapter 3 of the RTI Act, 2005, in case they are not satisfied with the decision of the appellate authority within the IRDAI.

Ref: IRDA/GEN/08/2007 Date of issue: 23 August 2017

16 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Constitution of Central Database of Licensed Insurance sales persons in India (ENVOY) at IIB

Introduction

The Authority invites reference to Circular No. IRDAI/INT/CIR/CDB/160/07/2017, dated 12 July 2017, which lays down the roadmap for the constitution of a central database of all insurance salespersons in India at the Insurance Information Bureau of India (IIBI). Insurers and intermediaries

have been advised to upload requisite details, including the Aadhaar number, of such persons on the database of the IIBI.

The next phase is ready at the IIBI, and requisite details pertaining to the following entities working on their behalf shall be uploaded to the IIB by all insurance intermediaries:

• Broker qualified persons,

• Specified persons of corporate persons, and

• Authorised verifiers of web aggregators

Ref: IRDAI/INT/CIR/CDB/197/08/2017 Date of issue: 24 August 2017 Applicability: To All Insurers, All Insurance Intermediaries

17 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Non-participation/unsatisfactory participation of certain insurance companies on Lok Adalats/MACT and Servicing of policy holder

Introduction

Keeping in mind the seriousness of the issues and to strengthen the faith of the citizens in the insurance sector, the Authority mandates all insurance companies to ensure the following:

• Attend MCAT/court cases promptly and properly wherever summons are received from the hon’ble courts.

• Participate in Lok Adalats whenever they are held.

• Strictly adhere to the IRDAI’s Protection of Policyholders Regulations, 2017.

• Maintain a correspondence office address with the policyholders, especially in dealing with claims matters such as proper service of summons.

The IRDAI, under section 34 of the Insurance Act, 1938, would take action deemed necessary in case an insurer fails to comply with the said process

Ref: IRDA/NL/CIR/MISC/206/8/2017 Date of issue: 31 August 2017 Applicability: To all general insurance companiess

18 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Guidelines on Motor Insurance Service Provider

Ref: IRDA/ INT/GDL/MISP/202/08/2017 Date of issue: 31 August 2017

Introduction

Based on the examination of the report submitted by the committee constituted for motor dealer payout on 31 May 2016, the Authority frames the guidelines on motor insurance service providers (MISPs). The guidelines are issued under section 34 of the Insurance Act, 1938, and section 14 of the IRDA Act, 1999, and are known as Guidelines on Motor Insurance Service Provider and will come into force from 1 November 2017.

The objective defined for rolling out such a guideline is to recognise the role of the automotive dealer in distributing and servicing motor insurance policies so as to have regulatory oversight over their activities connected to insurance.

19 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Guidelines on Motor Insurance Service Provider

Ref: IRDA/ INT/GDL/MISP/202/08/2017 Date of issue: 31 August 2017

Implications for insurers, insurance intermediaries and MISPs

• The Authority lays down the criteria for eligibility conditions for the appointment of an MISP, responsibility of the sponsoring entity and MISP, training and examination of the MISP, renewal of permission and review of operations of the MISP.

• The Authority also lays down a code of conduct for the MISP in the form of dos and don’ts that need to be abided mandatorily by the MISP.

• The Authority defines the obligations on insurers and their intermediaries who are in

association with their respective MISP.

• The minimum operational conditions that need to be met by the MISP in terms of an agreement with the sponsors, disclosures, product and pricing, distribution fees, remittance of fees, compliance to anti-money laundering (AML) and KYC norms, creation of an e-insurance account and the issuance of e-insurance policies, grievances management, reporting requirements, MISP database, penalties and existing arrangements.

Key compliances on the part of insurers and insurers intermediaries as sponsors of the MISP:

Statement of compliance from the CEO/principal officer, the compliance officer and CFO of the insurer on the payment of the remuneration and rewards to the intermediary and MISP.

• Insurers to conduct monthly audit through an independent auditor on the payment of remuneration to the intermediary and MISP and the placement of an audit report to the audit committee.

• Submission of an enrolment report at the end of each day on the Authority’s IIB portal by the insurer and its intermediary.

• The sponsoring entities should review the controls, systems, procedures and safeguards deployed

by the MISP at least once a year. The review report should be placed before the board of the sponsoring entity.

• The MISP should comply with the IRDAI’s (Issuance of e-insurance policies) Regulation, 2016.

• The MISP should comply with AML and KYC-related matters at all times.

• The MISP should submit periodical returns as required by the Authority.

• The MISP shall maintain records pertaining to operations for a period of at least seven years from the date of issuance of an insurance policy or from the date of its termination of appointment as an MISP, whichever is later.

20 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Clarification on Aadhaar based e-KYC

Introduction

The Authority has issued a circular on the exercise of powers conferred under section 14 (1) of the IRDAI Act, 1999.

Implications and compliances for insurers

• Based on the procedure prescribing the e-KYC authentication of Aadhaar numbers by the Unique Identification Authority of India (UIDAI) in the Aadhaar (Authentication) Regulations,

2016, insurers shall perform the verification of the client through an ‘e-KYC authentication facility’ provided by the UIDAI—that is, authentication through biometrics (fingerprint or iris scanning) and/or through a one time password (OTP) received on a client’s mobile number or on e-mail address registered with the UIDAI.

• The information downloaded from the UIDAI shall be considered as sufficient information for the purpose of KYC verification.

• In case any material difference is observed either in the name or the photograph in Aadhaar is not clear, the insurer shall carry out additional due diligence and maintain a record of the additional documents sought pursuant to such due diligence.

• The records of KYC information so received shall be maintained by the insurers as per the Prevention of Money Laundering (PML) Rules, 2005, (amended from time to time) and the Authority’s circular/guidelines on AML/combating the finance of terrorism (CFT).

Ref: IRDA/SDD/MISC/CIR/204/08/2017 Date of issue: 31 August 2017 Applicability: To life and general insurers (including stand-alone health insurers)

21 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Clarifications on Guidelines on insurance e-commerce and electronic issuance of insurance policies

Introduction

The Authority looking into the issues raised by the stakeholders has issued the following clarifications pertaining to:

• Revised guidelines on insurance repositories and electronic issuance of insurance policies dated 29.05.2015

• Guidelines on insurance e-commerce dated 9 March 2017

Revised guidelines on insurance repositories and electronic issuance of insurance policies dated 29.05.2015

• Electronic signature: The Authority permits validation by an OTP for e-insurance account (eIA) opening

as an alternative to e-signature under clause 60(b) and Annexure 11 of the revised guidelines on insurance repositories and electronic issuance of insurance policies dated 29.05.2015.

• OTP-based e-KYC for opening of (eIA): Compliance with the KYC/AML guidelines issued by the Authority can be undertaken by optional facilities mentioned in the guidelines.

• Email ID/mobile number: In order to bring consistency between the earlier issued guidelines, the Authority allows opening of eIA on the basis of either email ID or mobile number with only one OTP being sent to the email id/mobile number.

Guidelines on insurance e-commerce dated 9th March, 2017

• Clause on e-PAN facility offered by the NSDL for compliance to the KYC/AML guidelines issued by the Authority now stands deleted as it is not one of the recognised modes for KYC/AML compliance.

• Opening of e-insurance account for all policies that are sold on the ISNP platform has to be necessarily and compulsorily followed up with opening of an e-insurance account within 15 days post selling of insurance policies.

Any non-compliance will be seen as a violation of the aforesaid guidelines.

Ref: IRDA/ BRK/ CIR/ INSRE/ 211/ 09/ 2017 Date of issue: 7 September 2017 Applicability: To CEO’s of all insurers, insurance intermediaries and insurance repositories

22 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Publishing of Death Claims data / Death Claims paid ratios in “Insurance Advertisements”

Introduction

The Authority intends to bring uniformity across the industry in the method followed to arrive at death claims paid data (i.e. death claims paid ratios) while publishing them in insurance advertisements as defined in the IRDA (Insurance Advertisements and Disclosure) Regulation, 2000. The Authority issues the below mentioned instructions to use/publish only annual figures of death claim paid ratios based on the number of policies alone.

• The figures shall reflect the entire financial year and shall be based

upon the latest IRDAI annual report (or) latest annual audited final figures submitted to the Authority.

• The data for individual and group polices shall not be clubbed together. The insurance advertisements for group products shall reflect only the group death claims paid ratio and those for individual products shall reflect only the individual death claims paid ratio.

• In advertisements promoting the company’s brand without reference to products, only individual death claims paid ratio may be used.

Ref: IRDAI/LIFE/CIR/MISC/215/09/2017 Date of issue: 15 September 2017 Applicability: To the CEOs of all life insurers

23 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

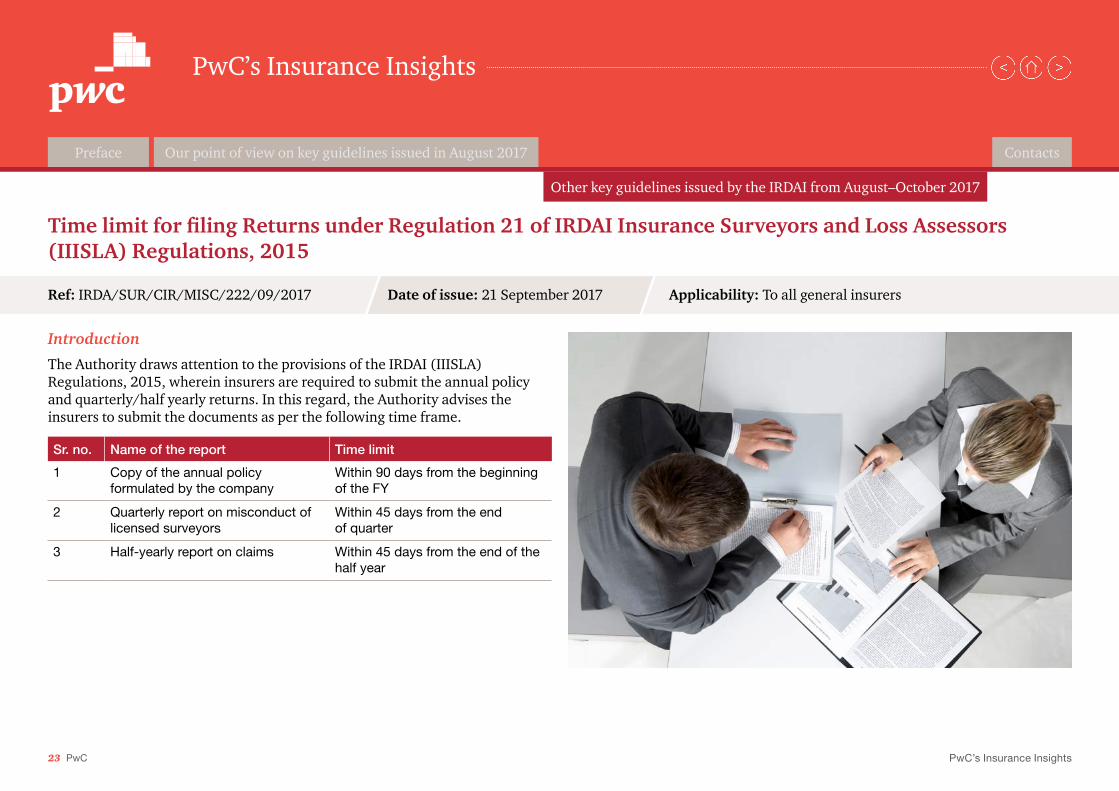

Time limit for filing Returns under Regulation 21 of IRDAI Insurance Surveyors and Loss Assessors (IIISLA) Regulations, 2015

Introduction

The Authority draws attention to the provisions of the IRDAI (IIISLA) Regulations, 2015, wherein insurers are required to submit the annual policy and quarterly/half yearly returns. In this regard, the Authority advises the insurers to submit the documents as per the following time frame.

Ref: IRDA/SUR/CIR/MISC/222/09/2017 Date of issue: 21 September 2017 Applicability: To all general insurers

Sr. no. Name of the report Time limit

1 Copy of the annual policy formulated by the company

Within 90 days from the beginning of the FY

2 Quarterly report on misconduct of licensed surveyors

Within 45 days from the end of quarter

3 Half-yearly report on claims Within 45 days from the end of the half year

24 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Exposure Draft on “Guidelines for Independent Assessment of Statutory Actuarial Valuation”

Introduction

The insurers carrying out life, general and health insurance business need to value their insurance business liability every year by appointed actuary of the insurer. This is also applicable to the reinsurers operating reinsurance business.

• As per the existing assets, liabilities and solvency margin regulations, the appointed actuaries of the insurers are solely responsible for the insurance liability number incorporated in the balance sheet. The number determined for insurance liability is an outcome of assumptions used, model set and judgment of the appointed actuary. This number is usually directly adopted by the external auditors by

providing a qualifying statement in the audit report that the appointed actuary of the insurer is responsible for the same.

• As a result, there is no statutory review of the insurance liability figures by an independent assessor to avoid any error, fraud, material misstatement in the reported liability figure, when such liability figure constitutes a significant part of the balance sheet of the insurer.

• There appears to be a gap in existing norms. To address this, the Authority has prepared the ‘Exposure draft on Guidelines for Independent Assessment of Statutory Actuarial Valuation’.

Implications on the insurers

• The insurer/reinsurer completed 10 years of operations since the date of incorporation till the end of last financial year.

• The Authority specifically has mentioned the names of the life, general insurers and reinsurer.

• These guidelines shall come into force from the financial year ending on 31 March 2018.

• The board shall appoint the independent assessor of actuarial valuation on recommendation of the appointed actuary.

• Insurers will have to abide by the eligibility conditions before appointing the independent assessor.

• The Authority also defines the scope of independent assessment of actuarial valuation.

• The Authority also defines the topics to be covered in the independent assessment of the actuarial report, submission of report and mandatory compliances by the independent assessors of actuarial valuation.

The Authority hereby requests all stakeholders to offer their comments/suggestions on the draft guidelines for consideration of the same by the Authority. The comments/suggestions in MS Word format should reach the Authority by 13.10.2017 in the format attached to the undersigned by e-mail at [email protected].

Ref: IRDAI/ACTL/MISC/IASAV/09/2017 Date of issue: 25 September 2017

25 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Submission of Crop Insurance Data

Introduction

The Authority invites attention to ref. no. IRDAI/NL/Anl/Crop Ins./2/2016-17 dated 9 February 2017 and keeping in view the importance of crop insurance and related schemes introduced by the government, the existing data formats have been revised so as to meet the emerging analytical requirements.

Mandatory compliance

In this connection, general insurers (except ECGC and stand-alone health insurers) are advised to submit the data to the Authority in the formats

prescribed in the circular within 30 days of completion of each quarter (end of June, September, December and March)/financial year, as applicable.

Further, insurers are advised to furnish data w.e.f. 1 April 2016 and thereafter as applicable in the above-mentioned formats. The data is to be submitted in respect of each season commencing 1 April 2016 until all outstanding claims are disposed of.

The soft copies of the revised formats (Form A-L) are hosted on the website of the IRDAI.

Ref: IRDA/NL/CIR/MISC/230/10//2017 Date of issue: 10 October 2017 Applicability: To all the general insurers (except ECGC and stand-alone health insurers)

26 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Compliance on Guidelines related to Information and Cyber Security

Introduction

The Authority draws insurers’ attention to IRDAI Circular Ref: IRDA/IT/GDL/MISC/082/04/2017 dated 7 April 2017 setting out guidelines on information and cyber security for insurers. From the feedback/updates received from insurers, it is observed that many of the insurers have still not finalised their gap analysis report, cyber crisis management plan and board-approved information and cyber security policy. Ensuring that the information and computer technology (ICT) infrastructure of insurers are fully secured is of paramount

importance. Any vulnerabilities to ICT may result in compromise on confidentiality of policyholder-related information and exposure to sensitive information of the insurance sector and the financial markets in general. This would have serious repercussions not only for the insurance sector but also for the financial system of the country as a whole.

The Authority therefore mandates all the insurers to provide a confirmation of having noted the above and plan of action proposed to be submitted to [email protected] by 17 October 2017.

Ref: IRDA/IT/CIR/MISC/232/10/2017 Date of issue: 12 October 2017 Applicability: CMDs/CEOs – life insurers, general insurers and health insurers

27 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Motor Insurance Service Provider guidelines

Introduction

In light of circular Ref. IRDA/INT/GDL/MISP/202/08/2017 dated 3 August 2017, the Authority observed that certain insurers/intermediaries are seeking to advance the agreements and tie-ups due on or after 1 November 2017 in a bid to avoid following the guidelines for those agreements. The Authority notifies that any attempt to undermine the guidelines without paying heed to their objective will be viewed seriously by the IRDAI and the matter will be dealt with strictly.

The Authority also iterates that both commission and fees cannot be paid under the same policy.

Ref: IRDA/INT/CIR/MISP/235/10/2017 Date of issue: 17 October 2017 Applicability: To all insurance intermediaries

28 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Inclusion of Indemnity based Health Insurance Product through PoS – General Insurers and Standalone Health Insurers

Introduction

The Authority received requests from many insurers to allow indemnity-based health insurance products to be sold through point of sale (PoS).

On examination, the Authority, under the powers vested with it under clause V (1) (f) of the said guidelines, has decided to allow individual indemnity-based health insurance products to be solicited through the PoS channel with the following conditions:

• The indemnity-based health insurance products may be offered to only individual policyholders excluding groups and government scheme.

• 5 lakh INR per life/individual will be the maximum sum insured.

• The number of such products that can be filed as PoS products is capped at 3 (three) per insurance company.

• Since health indemnity products follow a different process than health benefit products, which were hitherto included in the PoS channel, the PoS may be educated about the process involved in preferring claims, particularly cashless claims, who in turn shall educate the holder of the indemnity-based health insurance product.

Ref: IRDA/INT/CIR/PSP/239/2017 Date of issue: 25 October 2017 Applicability: To all CEOs of non-life and health insurers

29 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017

Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Insurance Regulatory and Development Authority of India (Payment of commission or remuneration or reward to insurance agents and insurance intermediaries) (Second Amendment) Regulations, 2017

The Authority intends to increase the maximum commission or remuneration as a percentage of premium that is allowed for general insurance (motor). The Authority hereby made necessary regulations called the ‘Insurance Regulatory and Development Authority of India (Payment of commission or remuneration

or reward to insurance agents and insurance intermediaries) (Second Amendment) Regulations, 2017. The maximum commission payable for general insurance (motor) is as per the table below.

Date of issue: 30 October 2017

Sr. no. Year Maximum commission/remuneration payable to insurance agents/insurance intermediaries

Motor (comprehensive) Motor (stand-alone TP)

Other than 2-wheeler 2-wheeler Other than 2-wheeler 2-wheeler

1 Certificate of registration – 1st to 3rd year 15% (OD portion) + (Nil - TP portion)

17.5% (OD portion) + (Nil - TP portion)

2.5% 2.5%

2 Certificate of registration – 4th year onwards 15% (OD portion) + 2.5% (TP portion)

17.5% (OD portion) + (Nil - TP portion)

2.5% 2.5%

30 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Preface Our point of view on key guidelines issued in August 2017 Other key guidelines issued by the IRDAI from August–October 2017

Contacts

Vivek Iyer Partner [email protected] Mobile: +91 9167745318

Dnyanesh Pandit Director [email protected] Mobile: +91 9819446928

Joydeep K Roy Partner [email protected] Mobile: +91 9821611173

Saigeeta Bhargava Associate Director [email protected] Mobile: +91-9560518833

Yugal Mehta Manager [email protected] Mobile: +91 9970163293

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 158 countries with more than 2,36,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com

In India, PwC has offices in these cities: Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.com/in

PwC refers to the PwC International network and/or one or more of its member firms, each of which is a separate, independent and distinct legal entity. Please see www.pwc.com/structure for further details.

© 2017 PwC. All rights reserved

About PwC

pwc.inData Classification: DC0

This document does not constitute professional advice. The information in this document has been obtained or derived from sources believed by PricewaterhouseCoopers Private Limited (PwCPL) to be reliable but PwCPL does not represent that this information is accurate or complete. Any opinions or estimates contained in this document represent the judgment of PwCPL at this time and are subject to change without notice. Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication. PwCPL neither accepts or assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decisions readers may take or decide not to or fail to take.

© 2017 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

VB/November2017-11288