Puzzlebox comp 2010

25

Puzzle Box Compensation 2010

-

Upload

balancedcomp-llc -

Category

Business

-

view

672 -

download

0

description

The allocation of executive compensation resources is being scrutinized by internal and external forces. Regulations, board governance issues, and the lower margins require new thought processes on the various pieces of the compensation puzzle and how they fit together.

Transcript of Puzzlebox comp 2010

Puzzle Box

Compensation 2010

Above reproach on what is paid and able to respond to inquirers

Balance the need for talent with budget concernsNot dampening morale. At the same time increase productivity

A business model focused on becoming a low cost provider

Compensation is just one piece of the entire business strategy.

Step 1 • Add Supporting Text Here

Step 2 • Add Supporting Text Here

Step 3 • Supporting Text Here

Step 4 • Supporting Text Here

Effecting Compensa

tion Design

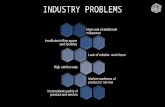

Economy & Industry Issues

Regulations & Board Governance

IssuesNeed for Capital

Need to Retain Those Who Deliver

Your Services

Economy & Banks

• High Unemployment • Significant change in economy

not likely until commercial lending increases

• Not likely with big banks investing in securities almost risk free

• 829 banks on the problem watch list as of June 30, 2010.

• 118 failures by Sept 2010. • 192 enforcement actions by the

Federal Reserve already this year vs. 172 in 2009.

• Estimated that we will go from 7800 banks to 4000 banks. Top 25% will own 75% of all bank assets; up from 67%.

• How do 3,975 banks profitably operate when they only control 25 percent of the banking assets?

Hypothesis

Fewer Community Banks to CompeteA pronounced cultural difference between credit unions and big banks

Consumers will continue to prefer credit unions

Employees will continue to prefer credit unions

Increased pressure for legislation to end the tax free status of credit unionsInflux of bankers for hire in the market

Step 1 • Add Supporting Text Here

Step 2 • Add Supporting Text Here

Step 3 • Supporting Text Here

Step 4 • Supporting Text Here

Recommended Take

Away from the Todd Frank Act of 2010

Independence of Compensation

Committee

Independence of Any Compensation

Consultant

Enhanced Clawbacks

Documented Methodology

Clarify roles of management, Compensation Committee, Board on compensation issues. Establish qualifications & training of committee members

Document methodology & peer groupMirrors the independence standard that applies to audit committee members under Section 301 of the Sarbanes-Oxley Act.

Set Policy for Independence of the Compensation Committee

Governance Best Practices WillIncrease: Knowledge, Skills, Experience of committee members

• Increased focus on board member experience/skills, eliminating weakening performers.

• Access to internal information

• Periodic outside education in executive compensation for new members and refreshers for current members

Governance Best Practices Will Increase: Processes and Oversight

Begin with an audit of Status QuoCommittee & Board may not set other executives’ pay packages and related policies, but it should understand it.

Formal resolution and written definition of independence barring directors and firms doing consulting, legal and other work for credit union.Implement governance protocols, process controls and design features to mitigate risk taking.

Governance Best Practices Will Increase Board-Consultant

Relationship • Interviewed by Committee;

approved by Board• Board use consultant as a

resource “fully” asking recommendations, advantages and disadvantages

• Consultant probes and challenges Board members’ assumptions

• Selected Committee/Board members review working drafts or consultant’s reports before delivered to full Board

The compensation committee retains authority to engage its own compensation consultants and other advisers, and the company must provide sufficient resources for the committee to pay those consultants/advisers Need not follow consultants advice, nor does the advise relieve them of their responsibility to exercise their own judgment.

Independence of Advisors

Other services provided by the consultant’s/adviser’s firm.

The amount of fees received by the consultant’s/adviser’s firm from the company relative to the firm’s total revenues. Identify risks and how this will be monitored and addressed.

The consultant’s/adviser’s firm’s policies to limit conflicts of interest,

Business or personal relationships between the consultant/adviser and any member of the compensation committee, or management

Independence of

Compensation

Advisors

Enhanced Clawbacks

•Requires clawback of incentive compensation awarded to any current or former executive officers within three years of the date of the triggering financial restatement.•No misconduct on the part of the executive officer is required. •Another uncertainty is how the clawback rules will deal with incentive compensation that is based on a number of factors in addition to financial performance.•One of the biggest legal challenges for any clawback policy is establishing an enforceable right against compensation previously paid.

Excessive Compensation

“Covered financial institution” means any financial institution that has $1 billion or more in assets; including private or public companies.

Must disclose to their applicable regulator all incentive compensation plans (i.e., not solely executive officer plans.) for determination whether the incentive plan would encourage excessive risk taking that could lead to a material financial loss.

The Federal Reserve, FDIC, OCC and OTS recently issued their Guidance on Sound Incentive Compensation Policies. They largely focused on key principles for ensuring that incentive comp plans appropriately balance risks with financial performance and compensation rewards. Boards should include “graphic analysis” of this in their compensation policy.

Sound Incentive Compensation Policies

IRC 4958

Sends out thousands of compliance letters annually questioning direct and indirect compensation issues to identify questionable exec comp activities.

The only defense is to invoke the rebuttable presumption of reasonableness clause.Under these rules, an organization may place the burden of proving excessive compensation on the IRS by using disinterested persons to review comparability data to establish compensation, and by properly substantiating the methodology.

Is this what it feels like to be an executive banker these days?

Clarify How Performance Translates into Objective Pay DeterminationsSEC issued more comments

regarding performance targets than any other disclosure topic on executive comp.

The transparency and accountability necessary to create an above-reproach practices can be accomplished by an annual performance evaluation for the CEO that goes beyond meeting financial goals and addresses qualitative matters, such as leadership, relationships with customers, the board and employee engagement.

HR at the senior management table

Compensation Practices Should Embrace a Long-term Horizon• Rewards based on the targets

over a multi-year average, compared to peer group

• Review mix, leverage and design features to ensure a long-term view of performance; perhaps leveraging a percentage of the payout allowing for room to take back based on performance.

Pay For Performance at all Levels• Comp plan supports

organization’s mission, goals & strategy

• Reward short and long-term performance in appropriate balance and based on different measures.

• Review Benefits.

May Be Questionable:

Short-term incentive based solely on Net Income (or ROA, ROE….)

Quarterly bonus payments without “true-up” if full year results fall short.

Should non-exempt employees participate in annual bonus plans based on corporate goals?

Is it really only fair if everyone participates in variable pay?

Everyone gets one week of pay as the annual bonus.

Wait and see if the board thinks we had a good year

Performance Measures Should Change With Company Focus

Loan growthROA/ROECapital RatioCore Funding MixCore Deposit Increase% of Profitable customersInterest Bearing AccountsEfficiency Ratio

Non-financial measures are key indicators of long term successEmployee engagement

measuresCustomer satisfaction

measuresCAMEL ScoresMajor projectsAvg. # Accts/Household Individual Performance

Rating% of EE with Direct DepositsAvg. Risk Rating# Loan ratings that changed

in audits

Credit Union CEOBase $295,695Variable Pay 18%401-k 98%Pension 14%Defined Contri. Pl 86%457(b) 70%457(f) 58%Split Dollar 18%

Medical Coverage 100%Dental/Vision/Life 91%Company Car 57%Cell phone 93%Auto Allowance 61%Pd Spouse Travel 51%Laptop 58%

Community Bank CEOBase $370,811Variable Pay 27%401-K 98%Pension 29%Defined Contri PL 98%Employee Stock Pur. 15%Retire. Profit sharing 20%Roth IRA 28%Medical Coverage 100%Dental/Vision/Life 78%/34%/17%Company Car 58%Cell phone 97%Auto Allowance 72%Pd Spouse Travel 18%Laptop 50%Country Club 58%

CEO PAY $600M - $1BNot adjusted to local market

To create a compensation and performance culture where solid performers are not hurt when the sector is down nor are average performers given the keys to the kingdom when the market is okay.

Hasn’t the goal always been to attract and retain the best talent to deliver long term value to the org.?

Christie Summervill

CEOBalancedComp,

LLC

Helping you establish balance in your compensation

practices316-927-2668

Questions? Comments?

![Mathematics Computation (M-COMP) - mpsri.net1].pdfMathematics Computation (M-COMP) Copyright (c) 2010 Pearson Education, Inc. or its affiliate(s). All rights reserved. 2 Version: 2010](https://static.fdocuments.us/doc/165x107/5aacb13e7f8b9a59658d564f/mathematics-computation-m-comp-mpsrinet-1pdfmathematics-computation-m-comp.jpg)