PURSUING SUSTAINABLE GROWTH - Accenture · Gareth introduced the hugely successful Discovery...

20

1 Digital Insurer Network ADAPTING RAPIDLY AT SCALE TO MAXIMIZE CUSTOMER RELEVANCE Fifth Annual Meeting, Paris Innovation Center, June 2018 PURSUING SUSTAINABLE GROWTH Photo credit: Kawika Singson and Chris Hirata

Transcript of PURSUING SUSTAINABLE GROWTH - Accenture · Gareth introduced the hugely successful Discovery...

1

Digital Insurer Network

ADAPTING RAPIDLY AT SCALE TO MAXIMIZE CUSTOMER RELEVANCE

Fifth Annual Meeting, Paris Innovation Center, June 2018

PURSUING SUSTAINABLE GROWTH

Photo credit: Kawika Singson and Chris Hirata

2

This year’s Digital Insurer Network full-day meeting was, as anticipated, a lively gathering of senior executives all confronted by similar issues. The theme was Insurance as a Living Business with the agenda exploring bold pathways to an innovative, hyper-relevant tomorrow. The consensus was that insurers need to become more customer-centric, more data-driven, more agile and more creative. Success stories from outside the industry gave useful perspectives on how others are overcoming these challenges, while real-life examples showed how innovation is negating age-old barriers.

Daniele opened the session with an overview of the disruptors that are transforming the industry. One thing they all have in common, he said, is the pace with which they continue to change. In the face of this uncertainty, insurers’ only sure strategy is for them to become more changeable too. He introduced the concept of the ‘living business’, which is less like an organization and more like an organism – able to swiftly detect changes in the environment, adapt appropriately, and in the longer term evolve to become better suited to the new prevailing conditions. While this may be unsettling for some, for others it is a world teeming with opportunity.

Daniele Presutti, DIN Chairman and Senior MD Insurance, Europe, Accenture

“It really is a great time to be in insurance!”

TACKLING THE CHALLENGES OF BECOMING A LIVING BUSINESS

3

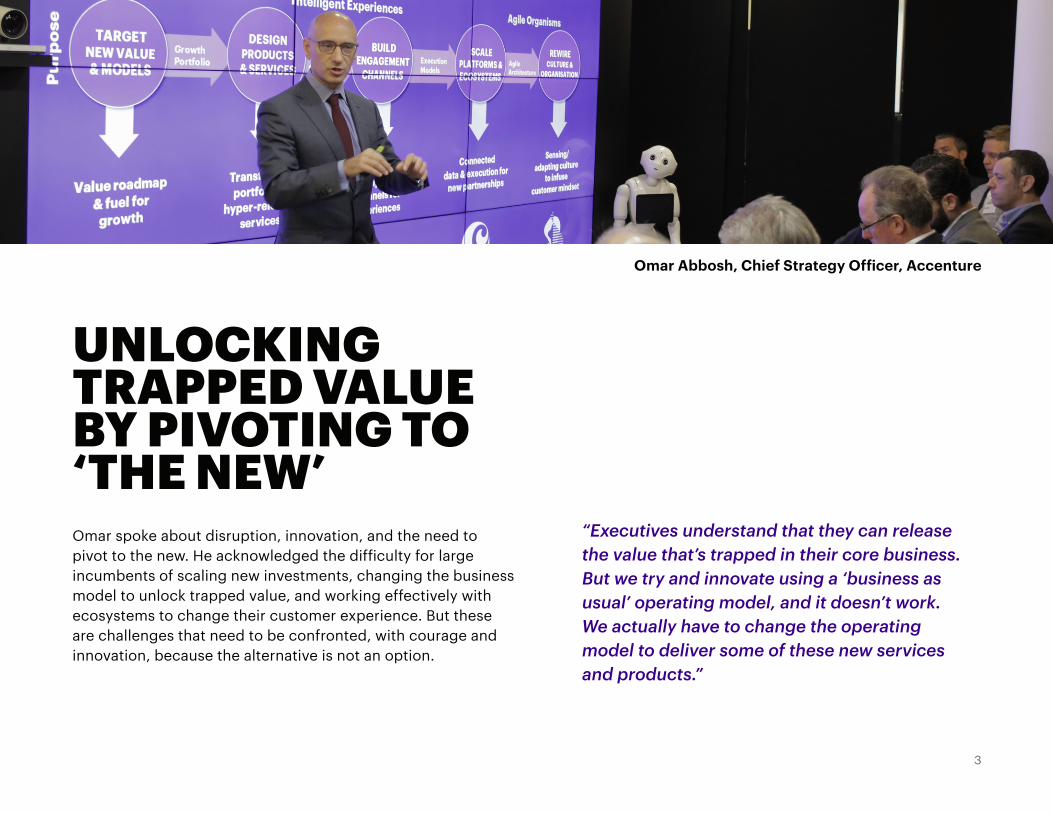

“Executives understand that they can release the value that’s trapped in their core business. But we try and innovate using a ‘business as usual’ operating model, and it doesn’t work. We actually have to change the operating model to deliver some of these new services and products.”

UNLOCKING TRAPPED VALUEBY PIVOTING TO ‘THE NEW’Omar spoke about disruption, innovation, and the need to pivot to the new. He acknowledged the difficulty for large incumbents of scaling new investments, changing the business model to unlock trapped value, and working effectively with ecosystems to change their customer experience. But these are challenges that need to be confronted, with courage and innovation, because the alternative is not an option.

Omar Abbosh, Chief Strategy Officer, Accenture

4

Gareth Friedlander, Head of Research & Development, Discovery Life

Gareth introduced the hugely successful Discovery business model. He explained that while most insurers pump similar inputs into similar underwriting models to derive similar premium quotes, Discovery achieves a competitive advantage by changing the inputs – offering incentives that change people’s behavior, improve their health and lifespan, reduce their claims, and increase their loyalty. The insurer becomes more of a risk manager, and the end result is that everyone wins.

DISCOVERY’S WIN-WIN MODEL CHANGES THE WAY THE GAME IS PLAYED

“The nature of risk I think has shifted over the years, from something that was there to quantify towards something you can mould, something that is behavioral. Risk is not just a numbers game anymore, but actually a behavioral game. With the right incentives and the help of a powerful ecosystem, risk becomes a dynamic variable.”

5

Ashley Benigno, Fjord Group Director, Milan

Similar issues can play out in different ways in different markets.Successful approaches may not be directly replicable elsewhere, but they often offer the key to customizable solutions that do work. Two speakers shared their experiences.

Ashley spoke about the fear of change in a world in which change is accelerating, and what the implications are for change-averse organizations like insurance companies. Irrespective of the markets they service, they should start becoming comfortable with concepts such as personalization, context, risk coach, prediction, proaction and holism.

SIMILAR PAIN POINTS, SHARED SOLUTIONS

“Adaptive insurance is more alive, more dynamic, because it looks at behavioral patterns based on real-time data. It opens the opportunity to become a life coach to your customers, a partner that can help them with their wellbeing and peace of mind. And this dynamism could be reflected in pricing, a bit like Uber surges taken to the nth degree.”

Dr. Pekka Puustinen, Chief Customer Officer, Ilmarinen Mutual Pension Insurance Co.

“It is a totally different kind of world we are in; we should be part of every client’s life every day.”

Pekka told how his company, the leading pensions carrier in Finland, was facing a financial problem: high loss costs in the form of disability pensions. They tackled it by changing their traditional model of interacting almost exclusively with employers and having minimal contact with the end customer. Today they are well on their way to being part of every customer’s life, incentivizing them constantly to improve their health and productivity.

6

Mark Curtis, Chief Client Officer, Fjord

Three speakers addressed the human element. They tackled the topic from different angles, but the take-out was similar: insurers need to pay greater attention not only to their aggregated customer bases, but to the individuals that comprise them.

Mark shared the findings of Fjord’s research into insurance mindsets. The study goes beyond demographics, “which don’t tell you very much about who someone is”, and uses design thinking to segment the market along two key dimensions: how people feel about risk, and how they live their lives. The four primary mindsets that emerge offer insights that can help insurers to develop products and services that effectively address consumers’ attitudes, concerns, needs and lifestyles.

CUSTOMER-CENTRICITY PUTS THE HUMAN ELEMENT IN PRIME POSITION

“I don’t think insurers are going to be able to offer the kind of living services that customers are demanding unless they become less of an organization and more of an organism, less solid and more alive, able to flex and wrap around the customer. This is a technology challenge, but it’s also an organizational challenge.”

7

“Companies no longer have to compromise when considering investment in brand building or the customer experience. You can be as powerful and effective when a consumer isn’t in a category mindset as you can when they’re absolutely in that moment of consumption of a product or service.”

Will spoke about the importance of the human dynamic in everything that insurers do, and the need to understand that dynamic in order to deliver experiences that have value. When empathy and a good positive intent are added to the mix, a virtuous cycle is started that benefits all concerned.

Will Hodge, Executive Strategy Director, Karmarama

Mark Howman, Creative Director, Allen International

Mark showed a video about an imaginary couple whose needs, across a broad spectrum of their daily living, are met by a futuristic insurance company that uses emerging technologies and deep customer-centricity to optimal effect. He believes ecosystems that, in tandem with fluid workforces, offer compelling physical and digital experiences will give rise to new engagement models that position insurance positively in the minds and lives of consumers.

“In the battle of digital over traditional, the industry has focused on price and convenience, at the cost of the customer experience and brand loyalty. This has led to poor advocacy from both customers and agents.”

8

9

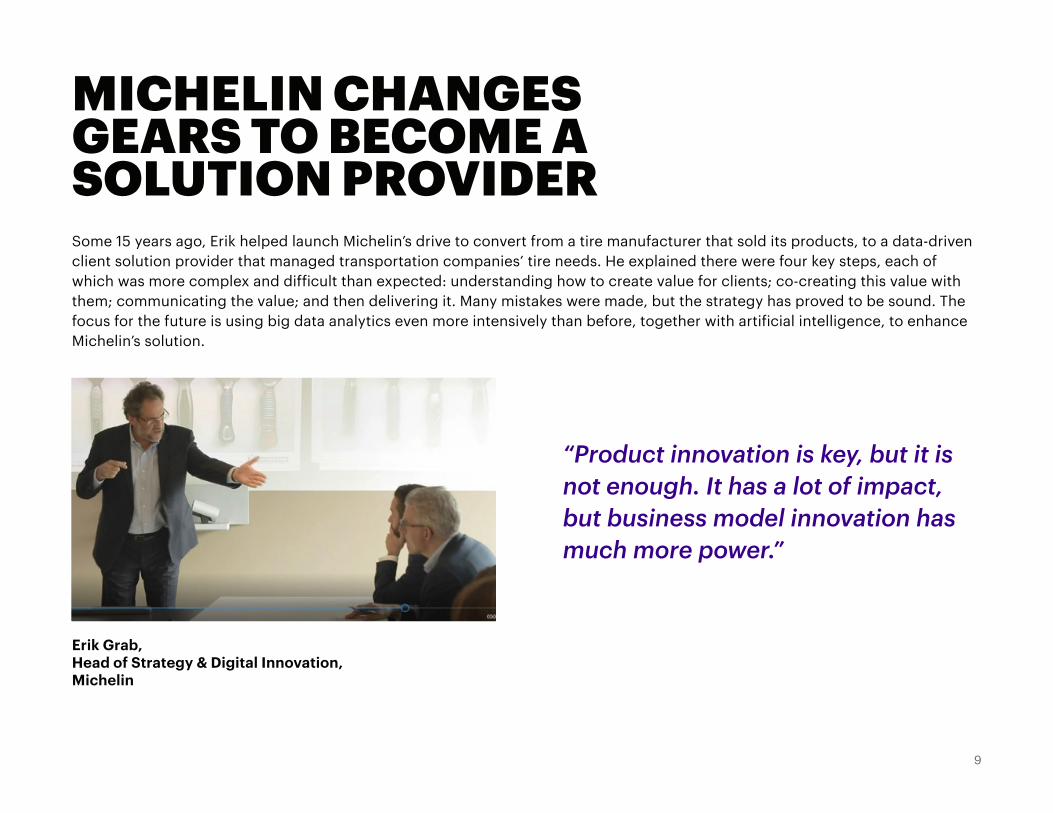

Erik Grab, Head of Strategy & Digital Innovation, Michelin

Some 15 years ago, Erik helped launch Michelin’s drive to convert from a tire manufacturer that sold its products, to a data-driven client solution provider that managed transportation companies’ tire needs. He explained there were four key steps, each of which was more complex and difficult than expected: understanding how to create value for clients; co-creating this value with them; communicating the value; and then delivering it. Many mistakes were made, but the strategy has proved to be sound. The focus for the future is using big data analytics even more intensively than before, together with artificial intelligence, to enhance Michelin’s solution.

MICHELIN CHANGES GEARS TO BECOME A SOLUTION PROVIDER

“Product innovation is key, but it is not enough. It has a lot of impact, but business model innovation has much more power.”

10

Marco examined the building blocks of a data-driven insurance provider and offered a number of key insights. Firstly, insurers can do a lot more with the data they already have. Secondly, advanced analytics is beneficial, but more important is the questions that insurers ask. Thirdly, there is a lot to be gained by intentionally selecting the data that will generate value for the organization. Finally, he noted that insurance companies have the core competencies of the future nested within their existing business models – what they need to do is make a conscious decision to become more data-driven.

Marco Vernocchi, Europe Analytics Lead, Accenture

USING DATA IS NOT THE SAME AS BECOMING TRULY DATA-DRIVEN

Accenture’s partnership with the no. 2 Japanese telecommunications operator KDDI gives each what it needed most. Accenture gained access to KDDI’s vast storehouse and stream of data, while the latter was able to develop innovative ways of unlocking the value in this data. One result, which Takuya presented, is a scaled AI solution that enables JapanTaxi to optimize the dispatching of taxicabs by combining demand predictions with location-based big data. In a country where Uber is effectively excluded, taxi drivers piloting the system increased sales by more than 20 percent. Takuya called on insurers with similarly rich data assets to think innovatively about ways to release its trapped value – to the benefit of customers as well as themselves.

“To succeed, a sushi restaurant needs to excel in four areas: ingredients, chefs, recipes and customer preferences. Getting three of the four right is not good enough. Similarly, to succeed as a data-driven organization, you need to have data, data scientists, algorithms and domain knowledge. Again, you must have all four elements.”

Takuya Kudo, Global Lead for Data Science, Accenture

“Yes it’s important to get more data. But the reality is there is already more than enough data in the average insurance company to extract value. You just need to take an intentional approach to release this trapped value.”

11

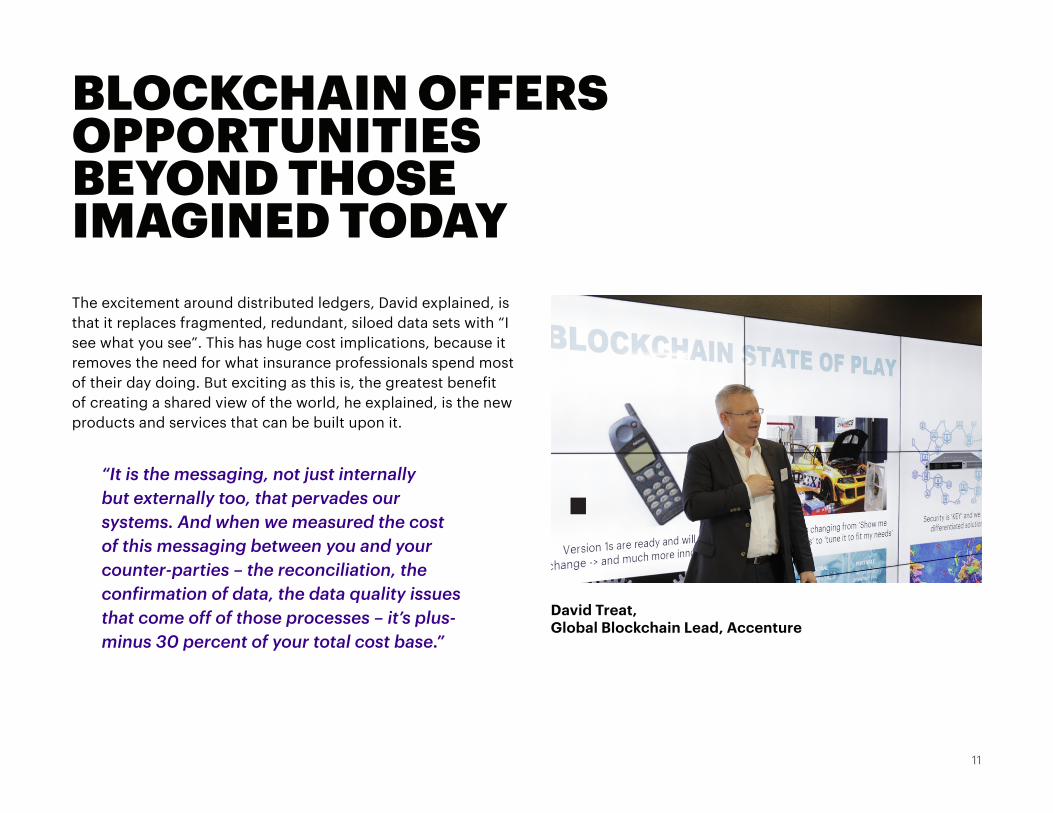

David Treat, Global Blockchain Lead, Accenture

The excitement around distributed ledgers, David explained, is that it replaces fragmented, redundant, siloed data sets with “I see what you see”. This has huge cost implications, because it removes the need for what insurance professionals spend most of their day doing. But exciting as this is, the greatest benefit of creating a shared view of the world, he explained, is the new products and services that can be built upon it.

BLOCKCHAIN OFFERS OPPORTUNITIESBEYOND THOSE IMAGINED TODAY

“It is the messaging, not just internally but externally too, that pervades our systems. And when we measured the cost of this messaging between you and your counter-parties – the reconciliation, the confirmation of data, the data quality issues that come off of those processes – it’s plus-minus 30 percent of your total cost base.”

12

13

“Augmented reality allows you to pull resources and people together much more easily and inexpensively than you could with other approaches.”

LIVE DEMOS – THE FUTURE IN ACTION

Cyrille Bataller, Artificial Intelligence Lead, Accenture

Cyrille gave a demonstration of a software robot consisting of robotic process automation with an AI twist. It executes process work by reading and interpreting what is on the computer screen and executing the appropriate actions. Coupled with text recognition and analysis, a powerful learning capability and an orchestration layer, it has the potential automatically to handle service requests and direct complaints or action requests to suitably skilled professionals.

Augmented reality is finally yielding practical business use cases. We explored the potential for virtual meetings, for accessing building plans for risk assessment and adjustment, for assisting commercial clients in risk avoidance practices, but primarily at this stage for cost-effective immersive training.

“It is not perfect but it is being trained. It is like people, right? They make mistakes, and these robots also make mistakes. But we can tune and measure their accuracy and we can train them, so they don’t make the same mistake again.”

14

“In big organizations, governance and KPIs are running the culture. So if you want to change the culture but you don’t change the KPIs, the bonus scheme, let’s be honest: nothing happens.”

A LIVING BUSINESS DEMANDS A NEW, ADAPTIVE WORKFORCE

Céline Laurenceau, Accenture Strategy Lead,

Talent & Organization France

Céline hosted a panel – including Mien Chu-Lesur, head of HR for Thales Digital Factory, and Accenture’s Roy Jubraj – that explored the complex challenges of developing and managing a workforce capable of capitalizing on the potential of digital: a workforce for a living business. From the need to identify the new skills that will be required, to defining the roles of the future, to developing a culture in which change and novelty are welcomed, to finding and attracting people who want to work in this environment … all of these facets are critical but new and problematic for most insurers.

THE JOURNEY TO BECOMING A LIVING BUSINESS – NEVER A DULL MOMENTIn wrapping up the day’s events, Daniele Presutti told DIN members the first priority in becoming a living business was to have a clear vision of where they want to go.

“This has always been true of any strategic intent, but this time, traditional methods are unlikely to get you there. This time, it’s necessary to look at the challenge from the perspectives of the customer experience and the human experience, and using these insights, to design new customer journeys, new distribution journeys, new workforce journeys … and then embed these into the everyday processes of the organization.”

This presents complicated challenges, but no one was likely to complain that life in insurance, in the future, would be uninteresting.

15

16

Stefano BisonGroup Business Development ManagerGenerali [email protected]

Valérie BompardChief Innovation & Digital Transformation Officer Société Générale [email protected]

Alberto Busetto Head of Connected Insurance Development Generali Italy [email protected]

Frank CoolerFounder, Chairman & [email protected]

Carlalberto CrippaHead of Digital DistributionCattolica [email protected]

Stefano de LiguoroHead of Digital & Direct BusinessZurich – BU [email protected]

Oscar EscuderoHead of Digital Service DeliveryZurich – Technology Delivery [email protected]

Alessandro GarofaloManaging [email protected]

Cyril HaiounHead of Operations, Automation and DigitizationBNP Paribas Cardif Group [email protected]

Nisse Jakob KrenchelHead of InnovationAlm. [email protected]

Koen MolenaarInnovation [email protected]

Elisabet PinillaCIO and Chief Transformation [email protected]

Dr. Pekka PuustinenChief Customer [email protected]

Marcos RodriguezHead of Operations and Business Services Generali [email protected]

Stefan SchulzManager Digital IT - Solutions - Innovation Generali [email protected]

Øivind Skallerud Director: Corporate Development [email protected]

Joris SmeuldersManaging Director & Member of the Board of DirectorsBaloise [email protected]

Jan StrauvenDirector ICT - Digital Transformation Baloise [email protected]

Alessia TruiniHead of Retail and CPI Products and Digital ChannelsIntesa [email protected]

Juha ViljakainenSenior Vice President, UnderwritingOP [email protected]

WHO CAME ALONG

17

Omar AbboshChief Strategy [email protected]

Cyrille BatallerArtificial Intelligence [email protected]

Mien Chu-LesurHR DirectorThales Digital [email protected]

Mark CurtisChief Client [email protected]

Pierre DuffautR&D Associate ManagerAccenture [email protected]

Gareth FriedlanderHead of Research & DevelopmentDiscovery [email protected]

Erik GrabVice President Strategic Anticipation, Innovation & Sustainable [email protected]

Will HodgeExecutive Strategy [email protected]

Mark HowmanCreative DirectorAllen International [email protected]

Roy JubrajHead of [email protected]

Takuya KudoGlobal Lead for Data [email protected]

Céline LaurenceauFunctional Strategy Director T&[email protected]

Daniele PresuttiDIN Chairman, Senior MD Insurance [email protected]

Susie SutherlandGlobal Insurance Marketing [email protected]

David TreatGlobal Blockchain [email protected]

Marco VernocchiEurope Analytics LeadAccenture [email protected]

SPEAKERS AND ACCENTURE ATTENDEES

18

19

ABOUT THE DIN

The Digital Insurer Network (DIN), launched in 2014, is an exclusive forum for insurance leaders responsible for driving their organization’s digital agenda. It spans Europe, Africa and Latin America. Members learn about the latest trends and innovations that are transforming insurance, discuss the impact these are having on their businesses, and share perspectives on how to release the potential value of emerging technologies. The DIN also offers members the opportunity to help guide Accenture’s insurance research program, and discuss pertinent survey findings prior to publication. In addition, it allows them to expand their professional network with other senior executives facing similar challenges.

CONTACT US

Susie SutherlandGlobal Insurance Marketing [email protected]

Daniele PresuttiChairman: Digital Insurer Network, Accenture Europe Insurance Lead [email protected]

ABOUT ACCENTURE

Accenture is a leading global professional services company, providing a broad range of services and solutions in strategy, consulting, digital, technology and operations. Combining unmatched experience and specialized skills across more than 40 industries and all business functions – underpinned by the world’s largest delivery network – Accenture works at the intersection of business and technology to help clients improve their performance and create sustainable value for their stakeholders. With approximately 442,000 people serving clients in more than 120 countries, Accenture drives innovation to improve the way the world works and lives. Visit us at www.accenture.com.

JOIN THE CONVERSATION

Read our blog

20

Copyright © 2018 Accenture All rights reserved.Accenture, its logo, and High Performance Delivered are trademarks of Accenture.