Purchase Loans

127

Purchase Loans Purchase Loans 1 8/4/2009

description

Purchase Loans. Purchase Loans. Minimum Cash Investment Under HERA, minimum cash investment = 3.5% of lesser of sales price or appraised value . Minimum cash investment is down payment only. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.2.A.2.c - PowerPoint PPT Presentation

Transcript of Purchase Loans

Purchase LoansPurchase Loans

18/4/2009

2

Purchase LoansPurchase LoansMinimum Cash InvestmentMinimum Cash Investment Under HERA, minimum cash investment Under HERA, minimum cash investment

= 3.5% of = 3.5% of lesser of sales price or lesser of sales price or appraised valueappraised value..

Minimum cash investment is down Minimum cash investment is down payment only. payment only. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.2.A.2.c

Neither closing costs nor prepaids paid by Neither closing costs nor prepaids paid by borrower count towards 3.5% minimum cash borrower count towards 3.5% minimum cash investment. investment. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.2.A.2.d8/4/2009

Purchase LoansPurchase Loans

So what does that mean to you and So what does that mean to you and your borrowers?your borrowers?

38/4/2009

Purchase LoansPurchase Loans

Minimum Cash InvestmentMinimum Cash Investment

Prior to 01/01/09, 3.0% x $120,000 =Prior to 01/01/09, 3.0% x $120,000 =

$3,600.$3,600.

Since 01/01/09, 3.5% x $120,000 Since 01/01/09, 3.5% x $120,000 ==

$4,200. $4,200.

So the difference is only So the difference is only $600$600, right?, right?

48/4/2009

5

Purchase LoansPurchase Loans

Calculating Maximum MortgageCalculating Maximum Mortgage Assume county maximum mortgage Assume county maximum mortgage

limit of $271,050. limit of $271,050. Assume $120,000 sales price.Assume $120,000 sales price. Assume $125,000 value.Assume $125,000 value. Assume $1,500 in closing costs and Assume $1,500 in closing costs and

$1,500 in prepaids.$1,500 in prepaids. Assume no seller concessions.Assume no seller concessions.

8/4/2009

6

Purchase LoansPurchase Loans

Calculating Maximum MortgageCalculating Maximum Mortgage

Pre-1/1/09Pre-1/1/09 1/1/091/1/09

Sales Price/ValueSales Price/Value $120,000 $120,000 $120,000 $120,000

x .9775x .9775 x .9650x .9650

Maximum MortgageMaximum Mortgage $117,300$117,300 $115,800$115,800

8/4/2009

7

Purchase LoansPurchase LoansPre-1/1/09Pre-1/1/09 1/1/091/1/09

Sale PriceSale Price $120,000$120,000 $120,000 $120,000

+ Closing Cost+ Closing Cost 1,500 1,500 1,500 1,500

Acquisition CostAcquisition Cost $121,500$121,500 $121,500 $121,500

- Maximum Mortgage -- Maximum Mortgage - 117,300 117,300 -115,800-115,800

$ 4,200$ 4,200 $ 5,700 $ 5,700

+ Prepaids+ Prepaids $ 1,500$ 1,500 $ 1,500$ 1,500

Total Cash RequiredTotal Cash Required $ 5,700$ 5,700 $ $ 7,2007,200

8/4/2009

Purchase LoansPurchase Loans

Remember…Remember… There is no minimum cash investment There is no minimum cash investment

requirement on refinance loans. It requirement on refinance loans. It applies only to purchases.applies only to purchases.

On REO properties being financed with On REO properties being financed with FHA mortgage insurance, special FHA mortgage insurance, special financing provisions may apply, such as financing provisions may apply, such as $100 down. Where these provisions $100 down. Where these provisions are offered, they supersede the 3.5% are offered, they supersede the 3.5% minimum cash investment requirement. minimum cash investment requirement.

88/4/2009

9

Purchase LoansPurchase LoansSeller ContributionsSeller Contributions Seller (or other “interested party”) Seller (or other “interested party”)

may contribute up to 6% of sales price may contribute up to 6% of sales price toward borrower’s closing costs and toward borrower’s closing costs and prepaids. prepaids.

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.2.A.3.b

But …But …

8/4/2009

Purchase LoansPurchase Loans

Not to the borrowers 3.5% Not to the borrowers 3.5% minimum cash investment.minimum cash investment.

Sellers, builders, realtors, lenders or Sellers, builders, realtors, lenders or entities associated with them may entities associated with them may provide neither gifts nor loans, provide neither gifts nor loans, neither directly nor indirectly.neither directly nor indirectly.

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.5.B.4.c

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.5.B.7.b8/4/2009 10

11

Purchase LoansPurchase LoansAcceptable Sources of Borrower’s Acceptable Sources of Borrower’s

Cash InvestmentCash Investment Borrower’s own savingsBorrower’s own savings A gift from a relative, employer, A gift from a relative, employer,

union or qualified non-profit.union or qualified non-profit. Secondary financing or collateralized Secondary financing or collateralized

loans from government agencies or loans from government agencies or qualified non-profits.qualified non-profits.

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.5.B.1.b

8/4/2009

Purchase LoansPurchase Loans

Who’s missing from this list of Who’s missing from this list of sources?sources?

128/4/2009

Purchase LoansPurchase Loans

And many other seller-funded And many other seller-funded non-profitsnon-profits

138/4/2009

14

Purchase LoansPurchase Loans

Unacceptable Source of Borrower’s Cash Unacceptable Source of Borrower’s Cash InvestmentInvestment

In no case shall the funds required…consist, in In no case shall the funds required…consist, in whole or in part, of funds provided by any of whole or in part, of funds provided by any of the following parties before, during, or after the following parties before, during, or after closing of the property sale:closing of the property sale:(i) The seller or any other person or entity (i) The seller or any other person or entity that financiallythat financiallybenefits from the transaction.benefits from the transaction.(ii) Any third party or entity that is (ii) Any third party or entity that is reimbursed, directlyreimbursed, directlyor indirectly, by any of the parties described or indirectly, by any of the parties described in clause (i).in clause (i).

8/4/2009

Purchase LoansPurchase Loans

Unacceptable Sources of Unacceptable Sources of Borrower’s Cash Investment Borrower’s Cash Investment

HERA goes on to say thatHERA goes on to say that

This subparagraph shall apply only to This subparagraph shall apply only to mortgages for which the mortgagee mortgages for which the mortgagee has issued credit approval for the has issued credit approval for the borrower on or after October 1, borrower on or after October 1, 2008.2008.

8/4/2009 15

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit ML 09-15ML 09-15. .

http://www.hud.gov/offices/adm/hudclips/letters/mortgagee/index.cfm

Provides policy guidance on using Provides policy guidance on using the tax credit with FHA purchase the tax credit with FHA purchase loans.loans.

Information on the tax credit itself is Information on the tax credit itself is available at available at http://www.irs.gov/newsroom/article/0,,id=204671,00.html?portlet7

8/4/2009 16

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit Government agencies and non-profit Government agencies and non-profit

instrumentalities of government can instrumentalities of government can offer offer tax credit advances tax credit advances secured by a secured by a 22ndnd lien on the property . lien on the property .

FHA-approved lenders, FHA-approved FHA-approved lenders, FHA-approved non-profits, government agencies and non-profits, government agencies and non-profit instrumentalities of non-profit instrumentalities of government can government can purchase the tax purchase the tax creditcredit anticipated by the borrower. anticipated by the borrower.

8/4/2009 17

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit If the entity purchasing the tax credit If the entity purchasing the tax credit

benefits from the loan transaction, benefits from the loan transaction, either directly or indirectly through either directly or indirectly through another party, the proceeds may not another party, the proceeds may not be used for the borrower’s down be used for the borrower’s down payment.payment.

Such proceeds may be used for Such proceeds may be used for additional downpayment beyond the additional downpayment beyond the 3.5% or for closing costs and prepaids.3.5% or for closing costs and prepaids.

8/4/2009 18

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit

An entity financially benefitting from An entity financially benefitting from the transaction includes the FHA-the transaction includes the FHA-approved lender and the seller. approved lender and the seller.

The seller could not, for example, The seller could not, for example, advance funds to a non-profit to advance funds to a non-profit to purchase the tax credit from the purchase the tax credit from the borrower to provide the 3.5% borrower to provide the 3.5% minimum cash investment.minimum cash investment.

8/4/2009 19

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit

Tax Credit AdvancesTax Credit Advances Tax credit advance may not result in Tax credit advance may not result in

cash back to the borrower.cash back to the borrower. 22ndnd lien may not exceed sum of down lien may not exceed sum of down

payment, closing costs and prepaids.payment, closing costs and prepaids. May or may not involve monthly May or may not involve monthly

payments.payments.

8/4/2009 20

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit

Purchasing the Tax CreditPurchasing the Tax Credit Proceeds of tax credit purchase may Proceeds of tax credit purchase may

not exceed anticipated tax credit not exceed anticipated tax credit due.due.

Tax credit purchase fees should not Tax credit purchase fees should not exceed 2.5% of anticipated credit.exceed 2.5% of anticipated credit.

Borrower must certify that tax credit Borrower must certify that tax credit will not be subject to any offsets.will not be subject to any offsets.

8/4/2009 21

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit

Purchasing the Tax CreditPurchasing the Tax Credit Name and EIN of entity purchasing Name and EIN of entity purchasing

tax credit, credit amount, and fee tax credit, credit amount, and fee paid must be entered in FHA paid must be entered in FHA ConnectionConnection

Documentation supporting data Documentation supporting data entered must be included in case entered must be included in case file. file.

8/4/2009 22

Using the $8,000 Tax CreditUsing the $8,000 Tax Credit

8/4/2009 23

Insured Loans on HUD Insured Loans on HUD REOsREOs

ML 00-27ML 00-27. . http://www.hud.gov/offices/adm/hudclips/letters/mortgagee/2000ml.cfm

Provides basic instructions for processing Provides basic instructions for processing applications for FHA-insured financing to applications for FHA-insured financing to purchase HUD REO properties.purchase HUD REO properties.

Additional information available at site of Additional information available at site of HUD’s contractor at HUD’s contractor at http://www.nhmsi.com/

248/4/2009

Insured Loans on HUD Insured Loans on HUD REOsREOs

8/4/2009 25

Insured Loans on HUD Insured Loans on HUD REOsREOs

Current Sales IncentivesCurrent Sales Incentives Most properties offered for sale with FHA Most properties offered for sale with FHA

financing available permit a down payment financing available permit a down payment of $100.of $100.

$2,500 credit will be provided at $2,500 credit will be provided at settlement on all properties with a sales settlement on all properties with a sales price price >> $25,000. $25,000.

Borrower may request that FHA pay Borrower may request that FHA pay closing costs not to exceed 3% of sales closing costs not to exceed 3% of sales price. price.

8/4/2009 26

Insured Loans on HUD Insured Loans on HUD REOsREOs

HUD REO Sales Contract, Form HUD-HUD REO Sales Contract, Form HUD-95489548

Must be signed by a representative of Must be signed by a representative of MCB.MCB.

Have the box on line 4 checked indicating Have the box on line 4 checked indicating that borrower is applying for FHA that borrower is applying for FHA financing. financing.

Down payment amount on Line 4 may be Down payment amount on Line 4 may be left blank unless borrower is applying left blank unless borrower is applying under $100 down program. under $100 down program.

8/4/2009 27

Insured Loans on HUD Insured Loans on HUD REOsREOs

HUD REO Sales Contract, Form HUD-HUD REO Sales Contract, Form HUD-9548 9548

If borrower is requesting that HUD pay If borrower is requesting that HUD pay closing costs, that amount must be stated closing costs, that amount must be stated on Line 5 of sales contract.on Line 5 of sales contract.

$2,500 credit will be provided $2,500 credit will be provided automatically; it need not be listed on automatically; it need not be listed on sales contract.sales contract.

$2,500 is in addition to any amount $2,500 is in addition to any amount identified on Line 5.identified on Line 5.

8/4/2009 28

Insured Loans on HUD Insured Loans on HUD REOsREOs

Case NumbersCase Numbers Lender must obtain new case number.Lender must obtain new case number. Select Select HUD REO HUD REO for Processing Type.for Processing Type. When prompted, enter former FHA When prompted, enter former FHA

case number (from sales contract).case number (from sales contract). Appraisal assignment field will not Appraisal assignment field will not

allow entry.allow entry.

8/4/2009 29

Insured Loans on HUD Insured Loans on HUD REOsREOs

Down PaymentDown Payment If sales contract specifies $100 for down If sales contract specifies $100 for down

payment amount on Line 4, loan may be payment amount on Line 4, loan may be processed on that basis.processed on that basis.

If Line 4 is blank for down payment If Line 4 is blank for down payment amount, process under standard amount, process under standard procedures (down payment = 3.5% of procedures (down payment = 3.5% of lesser of value or sales price).lesser of value or sales price).

See ML 00-27 for instructions on sales See ML 00-27 for instructions on sales discounts.discounts.

8/4/2009 30

Insured Loans on HUD Insured Loans on HUD REOsREOs

AppraisalsAppraisals Do not order a new appraisal.Do not order a new appraisal. Appraisal prepared for MCB must be Appraisal prepared for MCB must be

used to calculated maximum mortgage.used to calculated maximum mortgage. To obtain a copy of appraisal, send an e-To obtain a copy of appraisal, send an e-

mail to MCB.mail to MCB. Send request under lender’s corporate e-Send request under lender’s corporate e-

mail account and include full contact mail account and include full contact information. information.

8/4/2009 31

Insured Loans on HUD Insured Loans on HUD REOsREOs

AppraisalsAppraisals

A new appraisal may be ordered only where: A new appraisal may be ordered only where: As-repaired appraisal is required for a 203k; As-repaired appraisal is required for a 203k;

oror The M&M’s appraisal was more than 6 The M&M’s appraisal was more than 6

months old at the time the sales contract was months old at the time the sales contract was signed; signed; oror

Property is being sold with $100 down and Property is being sold with $100 down and sales price exceeds value. Submit appraisal sales price exceeds value. Submit appraisal to MCB who will advise if higher value may to MCB who will advise if higher value may be used.be used.

328/4/2009

Insured Loans on HUD Insured Loans on HUD REOsREOs

Lead-Based PaintLead-Based Paint If property built between 1950 and If property built between 1950 and

1978 and borrower is applying for 1978 and borrower is applying for FHA financing under Section 203(b), FHA financing under Section 203(b), lead-based paint inspection must be lead-based paint inspection must be performed at no cost to borrower.performed at no cost to borrower.

Allow two weeks after sales contract Allow two weeks after sales contract is signed for completion of inspection.is signed for completion of inspection.

8/4/2009 33

Insured Loans on HUD Insured Loans on HUD REOsREOs

Lead-Based PaintLead-Based Paint If property built before 1960 and paint If property built before 1960 and paint

requires stabilization, MCB will effect requires stabilization, MCB will effect repairs, probably delaying settlement.repairs, probably delaying settlement.

Upon completion, borrower will receive Upon completion, borrower will receive a Clearance Certificate.a Clearance Certificate.

If borrower applying for 203(k) If borrower applying for 203(k) financing, work write-up must include financing, work write-up must include lead-based paint repairs. lead-based paint repairs.

8/4/2009 34

Insured Loans on HUD Insured Loans on HUD REOsREOs

HUD REO PropertiesHUD REO Properties Underwriter must underwrite an Underwriter must underwrite an

REO appraisal just as he or she does REO appraisal just as he or she does a regular appraisal.a regular appraisal.

Make best effort to ensure that REO Make best effort to ensure that REO property meets MPR.property meets MPR.

Discuss repair issues with HUD’s Discuss repair issues with HUD’s M&M contractor.M&M contractor.

8/4/2009 35

Refinance LoansRefinance Loans

Refinance loans are a little Refinance loans are a little different.different.

368/4/2009

37

Refinance LoansRefinance Loans FHA offers refinances of both FHA and FHA offers refinances of both FHA and

non-FHA loans.non-FHA loans. FHA offers both cash-out and rate and FHA offers both cash-out and rate and

term refinances.term refinances. For existing FHA loans, a special non-For existing FHA loans, a special non-

credit qualifying refinance option is credit qualifying refinance option is available.available.

Mortgage calculation worksheets Mortgage calculation worksheets available at available at http://www.hud.gov/offices/hsg/sfh/trn/training.cfm

8/4/2009

38

Rate and Term RefinancesRate and Term Refinances Any non-FHA or FHA loan can be Any non-FHA or FHA loan can be

refinancedrefinanced. . A borrower is eligible to refinance the A borrower is eligible to refinance the

loan, as long as he/she has legal title, even loan, as long as he/she has legal title, even if he/she is not originally on the loan. if he/she is not originally on the loan. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.A.1.a

Cash back at closing may not exceed $500.Cash back at closing may not exceed $500.http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.1.b

8/4/2009

Rate and Term RefinancesRate and Term Refinances

Full credit-qualifying.Full credit-qualifying. Loan must be current for the month Loan must be current for the month

due.due. Full appraisal. Required repairs Full appraisal. Required repairs

must be completed before closing. must be completed before closing. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.1.a

8/4/2009 39

Rate and Term RefinancesRate and Term Refinances

No seasoning requirement for senior No seasoning requirement for senior lien being refinanced. lien being refinanced.

For non-FHA loans where property For non-FHA loans where property was purchased within the last 12 was purchased within the last 12 months, mortgage amount based on months, mortgage amount based on lesser of appraised value or sales lesser of appraised value or sales price.price.http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.1.e

8/4/2009 40

Rate and Term RefinancesRate and Term Refinances Subordinate liens, including lines of Subordinate liens, including lines of

credit, regardless of when taken, may credit, regardless of when taken, may remain outstanding (but subordinate remain outstanding (but subordinate to the FHA-insured mortgage.to the FHA-insured mortgage.

New subordinate liens may be placed New subordinate liens may be placed behind the FHA-insured mortgage and behind the FHA-insured mortgage and are subject to no CLTV cap. are subject to no CLTV cap.

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.1.c

418/4/2009

Rate and Term RefinancesRate and Term Refinances

Mortgage amount Mortgage amount not including not including UFMIP UFMIP may not exceed may not exceed

Applicable county maximum.Applicable county maximum. Lesser ofLesser of

-- 97.75% of appraised value, or…97.75% of appraised value, or…-- the sum of the following:the sum of the following:

428/4/2009

Rate and Term RefinancesRate and Term Refinances

Can be included in new mortgage.Can be included in new mortgage. http://www.fhaoutreach.gov/FHAHandbook

/prod/infomap.asp?address=4155-1.3.B.1.b Existing first lienExisting first lien Purchase money second mortgagePurchase money second mortgage Junior liens over 12 months oldJunior liens over 12 months old Closing costs and prepaid expensesClosing costs and prepaid expenses Discount pointsDiscount points

438/4/2009

Rate and Term RefinancesRate and Term Refinances

Can be included in new mortgage.Can be included in new mortgage. Borrower paid repairs required by the Borrower paid repairs required by the

appraisal.appraisal. Interest charged by the servicing lender Interest charged by the servicing lender

when the payoff will not likely be when the payoff will not likely be received on the first day of the month.received on the first day of the month.

Prepayment penalties.Prepayment penalties. Accrued late charges and escrow Accrued late charges and escrow

shortages.shortages.

448/4/2009

Rate and Term RefinancesRate and Term Refinances

Cannot be included in new Cannot be included in new mortgage.mortgage.

Any portion of the funds of an equity Any portion of the funds of an equity line of credit in excess of $1,000 line of credit in excess of $1,000 that was advanced within the past that was advanced within the past 12 months that was for purposes 12 months that was for purposes other than repairs and rehabilitation other than repairs and rehabilitation of the property.of the property.

458/4/2009

Rate and Term RefinancesRate and Term Refinances

Prepaid expenses may include…Prepaid expenses may include… Per diem interest to the end of the Per diem interest to the end of the

month on the new loan.month on the new loan. Hazard insurance premium deposits.Hazard insurance premium deposits. Monthly mortgage insurance Monthly mortgage insurance

premiums.premiums. Any real estate tax deposits needed Any real estate tax deposits needed

to to establish the escrow account.establish the escrow account.

468/4/2009

Rate and Term RefinancesRate and Term Refinances

Calculating Maximum MortgageCalculating Maximum Mortgage Assume county maximum mortgage Assume county maximum mortgage

limit of $271,050. limit of $271,050. Assume $125,000 value.Assume $125,000 value. Assume $100,000 1Assume $100,000 1stst lien and lien and

$20,000 2$20,000 2ndnd lien lien Assume $2,000 in closing costs and Assume $2,000 in closing costs and

$2,000 in prepaids.$2,000 in prepaids.

478/4/2009

Rate and Term RefinancesRate and Term Refinances

Calculating Maximum MortgageCalculating Maximum Mortgage

Appraised ValueAppraised Value $125,000$125,000

x . 9775x . 9775

Maximum MortgageMaximum Mortgage $122,187$122,187

488/4/2009

Rate and Term RefinancesRate and Term Refinances

Calculating Maximum MortgageCalculating Maximum Mortgage

1st Lien Payoff1st Lien Payoff $ 99,000$ 99,000

2nd Lien Payoff2nd Lien Payoff 19,000 19,000

Closing CostsClosing Costs 2,000 2,000

Pre-PaidsPre-Paids 2,000 2,000

TotalTotal $122,000$122,000

498/4/2009

Rate and Term RefinancesRate and Term Refinances

Insured Mortgage AmountInsured Mortgage Amount

Maximum MortgageMaximum Mortgage $122,000$122,000

+ UFMIP (1.75%)+ UFMIP (1.75%) 2,135 2,135

Insured MortgageInsured Mortgage $124,135$124,135

LTVLTV 99.31% 99.31%

508/4/2009

Rate and Term RefinancesRate and Term Refinances

DocumentationDocumentation Credit report should clearly indicate Credit report should clearly indicate

that loan was current at the time it that loan was current at the time it was refinanced. If not, lender should was refinanced. If not, lender should provide other documentation that provide other documentation that loan was current.loan was current.

Recommended that case file include Recommended that case file include payoff statement from any liens being payoff statement from any liens being refinanced. refinanced.

518/4/2009

Cash-Out Refinances Cash-Out Refinances

ML 05-43ML 05-43. Increased maximum LTV . Increased maximum LTV on cash-out refinances to 95%.on cash-out refinances to 95%.

ML 08-09ML 08-09. Restricted 95% cash-out . Restricted 95% cash-out refinances to maximum mortgage of refinances to maximum mortgage of $417,000 effective 04/01/08.$417,000 effective 04/01/08.

ML 08-40ML 08-40. Second appraisal . Second appraisal required for cash-out refinances required for cash-out refinances where LTV exceeds 85% effective where LTV exceeds 85% effective 01/01/09. 01/01/09.

8/4/2009 52

Cash-Out Refinances Cash-Out Refinances

ML 09-08ML 09-08. LTV limited to 85% . LTV limited to 85% effective 04/01/09.effective 04/01/09.

http://www.hud.gov/offices/adm/hudclips/letters/mortgagee/index.cfm

Incorporated into 4155.1.Incorporated into 4155.1.

8/4/2009 53

54

Cash-Out Refinances Cash-Out Refinances Properties owned free and clear are Properties owned free and clear are

eligible. eligible. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.2.a

Must be current for the month due. Must be current for the month due. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.2.b

Non-occupying co-borrower may not Non-occupying co-borrower may not be added. be added. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.2.c

8/4/2009

Cash-Out Refinances Cash-Out Refinances Full credit-qualifying. Full Full credit-qualifying. Full

appraisal.appraisal. If located in declining area If located in declining area andand

mortgage exceeds $417,000, second mortgage exceeds $417,000, second appraisal required.appraisal required.

If property purchased within the last If property purchased within the last 12 months, maximum mortgage 12 months, maximum mortgage based on 85% of the lesser of based on 85% of the lesser of appraised value or sales priceappraised value or sales price

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.2.f8/4/2009 55

56

Cash-Out RefinancesCash-Out Refinances

New secondary financing may be New secondary financing may be added, but CLTV for 1added, but CLTV for 1stst mortgage and mortgage and newnew subordinate financing limited to subordinate financing limited to 85%.85%.

No CLTV restrictions on No CLTV restrictions on existingexisting secondary financing.secondary financing.

Modified 2nds not considered new Modified 2nds not considered new 2nds. 2nds.

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.3.B.2.e

8/4/2009

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

For existing FHA loans only.For existing FHA loans only. Non-credit-qualifying. Non-credit-qualifying.

http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.1.g

Should reduce monthly principal and Should reduce monthly principal and interest payment. Cash back to the interest payment. Cash back to the borrower at closing may not exceed borrower at closing may not exceed $500. $500. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.1.a

578/4/2009

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Exceptions To Reduced Monthly Exceptions To Reduced Monthly PaymentPayment

Refinancing to shorter term where Refinancing to shorter term where monthly payment does increase by more monthly payment does increase by more than 20% than 20% http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.4.b

ARM to fixed rate where monthly ARM to fixed rate where monthly payment does increase by more than payment does increase by more than 20% 20% http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.4.e8/4/2009 58

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Mortgage must be current for the Mortgage must be current for the month due.month due.http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.4.c

No new subordinate financing. No new subordinate financing. Existing subordinate financing may Existing subordinate financing may remain in place. No limits on CLTV. remain in place. No limits on CLTV. http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.3

8/4/2009 59

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Scoring through TOTAL is not Scoring through TOTAL is not recommended. If scored, file must recommended. If scored, file must contain documentation for data entered contain documentation for data entered in TOTAL. in TOTAL. ML 04-44ML 04-44. .

If appraisal performed, underwriter may If appraisal performed, underwriter may waive repair requirements except for waive repair requirements except for lead-based paint. Lender may, at its lead-based paint. Lender may, at its option, require that repairs be completed.option, require that repairs be completed.http://www.fhaoutreach.gov/FHAHandbook/prohttp://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.C.1.cd/infomap.asp?address=4155-1.6.C.1.c

8/4/2009 60

61

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Maximum Mortgage Amount on Maximum Mortgage Amount on Streamlines With AppraisalStreamlines With Appraisal

Lesser of principal balance, accrued Lesser of principal balance, accrued interest, fees, charges and escrows interest, fees, charges and escrows oror 97.75% of appraised value. 97.75% of appraised value.

http://www.fhaoutreach.gov/http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?FHAHandbook/prod/infomap.asp?address=4155-1.3.C.3.aaddress=4155-1.3.C.3.a

8/4/2009

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Maximum Mortgage Amount on Maximum Mortgage Amount on Streamlines Without AppraisalStreamlines Without Appraisal

Lesser of principal balance, accrued Lesser of principal balance, accrued interest, fees, charges and escrows interest, fees, charges and escrows oror original insured mortgage original insured mortgage amount. amount.

http://www.fhaoutreach.gov/http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?FHAHandbook/prod/infomap.asp?address=4155-1.3.C.2.caddress=4155-1.3.C.2.c

8/4/2009 62

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Maximum TermsMaximum Terms Streamline With AppraisalStreamline With Appraisal

30 years.30 years. Streamline Without AppraisalStreamline Without Appraisal

Lesser of 30 years or remaining Lesser of 30 years or remaining term of existing loan plus 12 years. term of existing loan plus 12 years. http://www.fhaoutreach.gov/FHAHandboohttp://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-k/prod/infomap.asp?address=4155-1.3.C.2.b1.3.C.2.b

8/4/2009 63

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Maximum Mortgage On A Streamline Maximum Mortgage On A Streamline Without AppraisalWithout Appraisal

Original Insured Loan Amount Original Insured Loan Amount (inc. financed UFMIP) of $100,000 @ (inc. financed UFMIP) of $100,000 @ 6.5%.6.5%.

Monthly P&I payment = $632.00Monthly P&I payment = $632.00 Principal BalancePrincipal Balance$98,500.$98,500. Current interest rate 5.5%.Current interest rate 5.5%.

8/4/2009 64

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Principal BalancePrincipal Balance $ 98,500$ 98,500

Closing CostsClosing Costs + 1,500 + 1,500

PrepaidsPrepaids + 1,000+ 1,000

$101,000$101,000

UFMIP CreditUFMIP Credit - 1,100- 1,100

Mortgage AmountMortgage Amount $ 99,900$ 99,900

(not inc. UFMIP)(not inc. UFMIP)

8/4/2009 65

FHA to FHA Streamline FHA to FHA Streamline RefinancesRefinances

Mortgage Not Including UFMIPMortgage Not Including UFMIP $ $ 99,90099,900

UFMIP (1.5%)UFMIP (1.5%) + 1,498+ 1,498

Insured Loan AmountInsured Loan Amount$101,398$101,398

Monthly P&I @ Monthly P&I @ 5.5% = 5.5% = $575.94$575.94..

8/4/2009 66

Hope for HomeownersHope for Homeowners

HH44HH

678/4/2009

Hope for HomeownersHope for Homeowners

Authorized by Housing and Economic Authorized by Housing and Economic Recovery Act of 2008 (HERA).Recovery Act of 2008 (HERA).

Modified by Emergency Economic Modified by Emergency Economic Stabilization Act of 2008 (EESA).Stabilization Act of 2008 (EESA).

Modified by Helping Families Save Modified by Helping Families Save Their Homes Act of 2009Their Homes Act of 2009..

ML 08-29, ML 09-03ML 08-29, ML 09-03. Program . Program effective 10/01/08.effective 10/01/08.

688/4/2009

69

Hope for HomeownersHope for Homeowners

EligibilityEligibility Any type of loan originated on or before Any type of loan originated on or before

January 1, 2008 is eligible, FHA or non-January 1, 2008 is eligible, FHA or non-FHA.FHA.

Existing loan may be current, Existing loan may be current, delinquent, or in foreclosure.delinquent, or in foreclosure.

Owner occupants only. No second Owner occupants only. No second homes, no investment properties.homes, no investment properties.

2-4 Unit properties are eligible.2-4 Unit properties are eligible.

8/4/2009

70

Hope for HomeownersHope for Homeowners

EligibilityEligibility Participation in program by existing lien-Participation in program by existing lien-

holders is strictly voluntary.holders is strictly voluntary. If they participate they must:If they participate they must:

-- Waive or forgive all penalties and Waive or forgive all penalties and fees relatedfees related

to default or delinquency.to default or delinquency.-- Accept proceeds of new FHA loan as Accept proceeds of new FHA loan as

satisfaction of all existing liens.satisfaction of all existing liens.

8/4/2009

71

Hope for HomeownersHope for Homeowners

EligibilityEligibility Debt to income ratio for all existing Debt to income ratio for all existing

mortgages must be greater than 31% mortgages must be greater than 31% based on payments as of the date of based on payments as of the date of application for H4Happlication for H4H..

Ratio takes into account all mortgages Ratio takes into account all mortgages and escrows, whether included in and escrows, whether included in existing loans or not.existing loans or not.

Borrower must have net worth of less Borrower must have net worth of less than $1,000,000than $1,000,000..

8/4/2009

Hope for HomeownersHope for Homeowners

H4H LoanH4H Loan Mortgage limits apply nationally.Mortgage limits apply nationally. 1 Unit 2 Unit 3 Unit 4 1 Unit 2 Unit 3 Unit 4

UnitUnit $550,440 $704,682 $851,796 $550,440 $704,682 $851,796 $1,058,574$1,058,574

Loan must be fixed rate. No ARMs.Loan must be fixed rate. No ARMs. Term must be not less than 30 years Term must be not less than 30 years

and not more than 40 years.and not more than 40 years.

728/4/2009

Hope for HomeownersHope for Homeowners

Ratios on H4H Loan may not Ratios on H4H Loan may not exceed…exceed…

31% front ratio and 43% back ratio 31% front ratio and 43% back ratio if LTV is between 90% and 96.5%if LTV is between 90% and 96.5%

38% front ratio and 50% back ratio 38% front ratio and 50% back ratio if LTV is less than 90%.if LTV is less than 90%.

738/4/2009

74

Hope for HomeownersHope for Homeowners

Mortgage Insurance PremiumsMortgage Insurance Premiums UFMIP UFMIP not to not to exceed 3%.exceed 3%. Annual MIP Annual MIP not to not to exceed of 1.5% of exceed of 1.5% of

outstanding loan balance.outstanding loan balance.

8/4/2009

75

Hope for HomeownersHope for Homeowners

Secondary FinancingSecondary Financing Not permitted at time loan closes. Not permitted at time loan closes.

All liens must be extinguished at the All liens must be extinguished at the time the H4H loan closes.time the H4H loan closes.

Permitted after closing only where Permitted after closing only where health and safety conditions exist health and safety conditions exist and/or failure to repair will cause and/or failure to repair will cause property deterioration. property deterioration.

8/4/2009

76

Hope for HomeownersHope for Homeowners

Equity SharingEquity Sharing Initial equity is the difference between Initial equity is the difference between

the appraised value at the time of loan the appraised value at the time of loan closing and the original mortgage closing and the original mortgage amount.amount.

For example… 2008 ValueFor example… 2008 Value$120,000$120,000 2008 Mortgage 2008 Mortgage 115,800 115,800

Initial Equity Initial Equity $ 4,200$ 4,200

8/4/2009

77

Hope for HomeownersHope for Homeowners

Equity SharingEquity Sharing Equity sharing under this example …Equity sharing under this example … During YearDuring Year FHA Share Borrower FHA Share Borrower

ShareShare 11 $4,200 $4,200 $ 0$ 022 3,780 3,780 420 42033 3,360 3,360 840 84044 2,940 2,940 1,260 1,260

5 5 2,520 2,520 1,680 1,6806 and later6 and later 2,100 2,100

2,1002,100

8/4/2009

78

Hope for HomeownersHope for Homeowners

Shared AppreciationShared Appreciation Permits FHA to share Permits FHA to share up to up to 50% of any 50% of any

appreciation.appreciation. FHA may share appreciation with FHA may share appreciation with or or

assign appreciation rights toassign appreciation rights to former former lien-holders lien-holders to induce loan write-downsto induce loan write-downs..

Profit-sharing capped at appraised value Profit-sharing capped at appraised value when the existing loan was madewhen the existing loan was made..

8/4/2009

79

Hope for HomeownersHope for Homeowners

Former Subordinate Lien-HoldersFormer Subordinate Lien-Holders Borrower will not owe any of his/her Borrower will not owe any of his/her

share of appreciation to former lien-share of appreciation to former lien-holders.holders.

Permits financial incentives for Permits financial incentives for servicers, originators and borrowers servicers, originators and borrowers to participateto participate..

8/4/2009

FHA Rehabilitation FHA Rehabilitation ProgramProgram

808/4/2009

81

FHA Rehabilitation FHA Rehabilitation ProgramProgram

What is Section 203k?What is Section 203k? One loan to finance both acquisition One loan to finance both acquisition

and rehab of a property.and rehab of a property. Mortgage amount is based on Mortgage amount is based on

projected value of the property with projected value of the property with the work completed.the work completed.

Repair escrow account created and Repair escrow account created and repairs completed repairs completed afterafter closing. closing.

8/4/2009

82

FHA Rehabilitation FHA Rehabilitation ProgramProgram

Eligible UsesEligible Uses To purchase a home and rehab it.To purchase a home and rehab it. To refinance a mortgage and rehab a To refinance a mortgage and rehab a

home.home. To purchase a home on another site, move To purchase a home on another site, move

it onto a new foundation, and rehab it.it onto a new foundation, and rehab it. Mortgage calculation worksheet available Mortgage calculation worksheet available

at at http://www.hud.gov/offices/hsg/sfh/trn/training.cfhttp://www.hud.gov/offices/hsg/sfh/trn/training.cfmm

8/4/2009

FHA Rehabilitation FHA Rehabilitation ProgramProgram

Maximum mortgage amount based on Maximum mortgage amount based on the the lesser lesser of the following:of the following:

As Is property value (may use sales price As Is property value (may use sales price on a purchase), plus cost of repairs; oron a purchase), plus cost of repairs; or

Existing debt on a refinance, plus the Existing debt on a refinance, plus the repair costs; or repair costs; or

110 percent of the "after improved" value.110 percent of the "after improved" value. http://www.fhaoutreach.gov/FHAHandbook/http://www.fhaoutreach.gov/FHAHandbook/

prod/infomap.asp?address=4155-2.1.C.5.hprod/infomap.asp?address=4155-2.1.C.5.h

8/4/2009 83

FHA Rehabilitation FHA Rehabilitation ProgramProgram

Down payment on purchase loans Down payment on purchase loans based on 3.5% of the lesser of …based on 3.5% of the lesser of …

Sales price plus rehab costs; orSales price plus rehab costs; or As-is value plus rehab costs; orAs-is value plus rehab costs; or 110% of as-repaired value.110% of as-repaired value.

8/4/2009 84

85

FHA Rehabilitation FHA Rehabilitation ProgramProgram

Regular Section 203kRegular Section 203k Minimum repairs of $5,000. No Minimum repairs of $5,000. No

maximum on repairs.maximum on repairs. Must use 203k Consultant to Must use 203k Consultant to

prepare detailed work write-up and prepare detailed work write-up and to conduct inspections of work.to conduct inspections of work.

Few limitations on the type of Few limitations on the type of repairs.repairs.

8/4/2009

86

FHA Rehabilitation FHA Rehabilitation ProgramProgram

Streamline 203kStreamline 203k ML 05-50ML 05-50.. No minimum amount of repairs. No minimum amount of repairs.

Maximum repairs of $35,000.Maximum repairs of $35,000. 203k Consultant not required.203k Consultant not required. If repair amount under $15,000 no If repair amount under $15,000 no

33rdrd party inspections required. party inspections required. No additions or structural repairs.No additions or structural repairs.

8/4/2009

FHA Rehabilitation FHA Rehabilitation ProgramProgram

How about commercial space on a How about commercial space on a 203k?203k?

1 Story property1 Story property

25%25% 2 Story property2 Story property

49%49% 3 Story property3 Story property

33%33%

8/4/2009 87

FHA Rehabilitation FHA Rehabilitation ProgramProgram

Test your 203k knowledge.Test your 203k knowledge.

Where the property involves Where the property involves commercial space, the following commercial space, the following policy applies…policy applies…

8/4/2009 88

FHA Rehabilitation FHA Rehabilitation ProgramProgram

% of repairs spent of commercial space % of repairs spent of commercial space may not exceed % of commercial space.may not exceed % of commercial space.

NoNo..

203k funds may only be expended on 203k funds may only be expended on health and safety repairs of commercial health and safety repairs of commercial space.space.

No.No.

203k funds may not be expended on repair 203k funds may not be expended on repair of the commercial space.of the commercial space.

Yes.Yes.

8/4/2009 89

FHA Rehabilitation FHA Rehabilitation ProgramProgram

May be Streamline refinanced providedMay be Streamline refinanced provided Fully executed certificate of completion is Fully executed certificate of completion is

issued. issued. Escrow account is closed with a final Escrow account is closed with a final

release. release. Required close out information is entered Required close out information is entered

in FHA Connection.in FHA Connection. http://www.fhaoutreach.gov/FHAHandbook/http://www.fhaoutreach.gov/FHAHandbook/

prod/infomap.asp?address=4155-1.6.C.4.iprod/infomap.asp?address=4155-1.6.C.4.i

8/4/2009 90

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

FHA has a special program for FHA has a special program for senior citizens who own their senior citizens who own their home.home.

918/4/2009

92

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Home Equity Conversion Mortgage Home Equity Conversion Mortgage (HECM)(HECM)

Allows seniors to tap into the equity in Allows seniors to tap into the equity in their homes.their homes.

No payment is ever required of No payment is ever required of borrower. Borrower can never be borrower. Borrower can never be forced from home, or forced to sell.forced from home, or forced to sell.

Only after borrower dies or permanently Only after borrower dies or permanently moves must loan be satisfied.moves must loan be satisfied.

8/4/2009

93

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

HECM Eligibility and QualifyingHECM Eligibility and Qualifying All borrowers must be at least 62 All borrowers must be at least 62

years old.years old. No credit underwriting. Amount of No credit underwriting. Amount of

loan calculated through a formula loan calculated through a formula using the age of the youngest using the age of the youngest borrower, the value of the home, borrower, the value of the home, interest rate and anticipated interest rate and anticipated appreciation.appreciation.

8/4/2009

94

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Ways To Receive Loan ProceedsWays To Receive Loan Proceeds Lump sum.Lump sum. Line of Credit.Line of Credit. Regular monthly payments Regular monthly payments toto

borrower.borrower. Combination of these.Combination of these.

8/4/2009

95

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Housing CounselingHousing Counseling ML 08-12ML 08-12, , ML 08-28ML 08-28, , ML 09-10ML 09-10.. Borrowers must receive housing Borrowers must receive housing

counseling counseling beforebefore a loan application a loan application can be processed.can be processed.

Borrowers may be charged by Borrowers may be charged by agencies for counseling. Fee may be agencies for counseling. Fee may be paid out of loan proceeds if borrower paid out of loan proceeds if borrower agrees.agrees.

8/4/2009

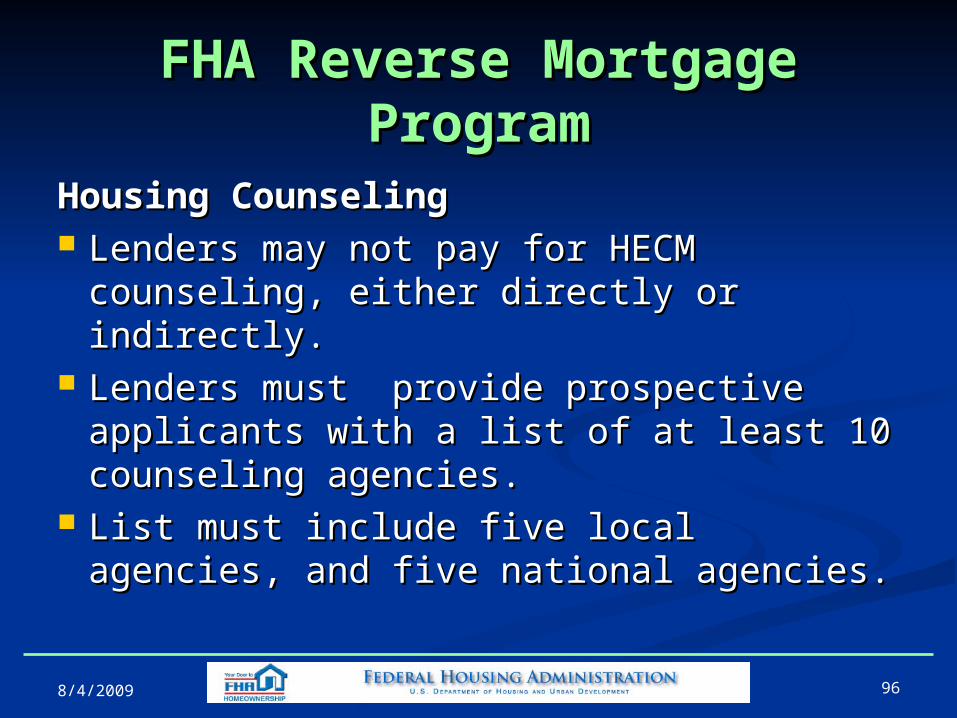

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Housing CounselingHousing Counseling Lenders may not pay for HECM Lenders may not pay for HECM

counseling, either directly or counseling, either directly or indirectly.indirectly.

Lenders must provide prospective Lenders must provide prospective applicants with a list of at least 10 applicants with a list of at least 10 counseling agencies.counseling agencies.

List must include five local agencies, List must include five local agencies, and five national agencies.and five national agencies.

8/4/2009 96

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Housing CounselingHousing Counseling The list of HUD-Approved Housing The list of HUD-Approved Housing

Counseling Agencies can be found atCounseling Agencies can be found athttp://www.hud.gov/offices/hsg/sfh/hecm/hechttp://www.hud.gov/offices/hsg/sfh/hecm/hecmlist.cfm ormlist.cfm or

Use the National HECM Housing Counseling Use the National HECM Housing Counseling Network atNetwork athttp://www.hud.gov/offices/hsg/sfh/hcc/hccprhttp://www.hud.gov/offices/hsg/sfh/hcc/hccprof18.cfmof18.cfm

8/4/2009 97

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Maximum Claim AmountMaximum Claim Amount Maximum claim nationally is set by Maximum claim nationally is set by

HERA at 100% of conforming loan HERA at 100% of conforming loan ($417,000) effective November 6, ($417,000) effective November 6, 2008. 2008. ML 08-35ML 08-35..

Temporarily increased by ARRA to Temporarily increased by ARRA to 150% of conforming loan limit 150% of conforming loan limit ($625,500) effective 02/24/09 - ($625,500) effective 02/24/09 - 12/31/09. 12/31/09. ML 09-07ML 09-07..

988/4/2009

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

Origination fee may not exceed 2% of Origination fee may not exceed 2% of maximum claim amount up to $200,000, maximum claim amount up to $200,000, then 1% of maximum claim amount then 1% of maximum claim amount above $200,000, but not to exceed above $200,000, but not to exceed $6,000. $6,000. ML 08-34ML 08-34..

Mortgagee and other parties barred from Mortgagee and other parties barred from requiring, directly or indirectly, the requiring, directly or indirectly, the purchase of other financial or insurance purchase of other financial or insurance products as a condition of HECM products as a condition of HECM approval. approval. ML 08-24ML 08-24. .

998/4/2009

FHA Reverse Mortgage FHA Reverse Mortgage ProgramProgram

HECMs may be used to purchase a HECMs may be used to purchase a property and obtain a HECM in a property and obtain a HECM in a single transaction.single transaction.ML 09-11.ML 09-11.

HERAHERA authorizes HECMs on co-ops. authorizes HECMs on co-ops. FHA is currently working on FHA is currently working on regulations to implement these regulations to implement these provisions. Co-op association will have provisions. Co-op association will have to approve use of HECMs in co-op.to approve use of HECMs in co-op.

1008/4/2009

Energy Efficient MortgagesEnergy Efficient Mortgages

1018/4/2009

102

Energy Efficient MortgagesEnergy Efficient Mortgages

What Is an Energy-Efficient Mortgage?What Is an Energy-Efficient Mortgage? A mortgage which includes improvements A mortgage which includes improvements

to save energy.to save energy. A borrower can finance into an already A borrower can finance into an already

approved FHA loan, 100% of the cost of approved FHA loan, 100% of the cost of eligible cost-effective energy eligible cost-effective energy improvements.improvements.

http://www.fhaoutreach.gov/FHAHandbook/http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.D#1prod/infomap.asp?address=4155-1.6.D#1

8/4/2009

103

Energy Efficient MortgagesEnergy Efficient Mortgages No additional borrower qualifying or No additional borrower qualifying or

appraisal. appraisal. http://www.fhaoutreach.gov/FHAHandbook/prod/ihttp://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.D.2.bnfomap.asp?address=4155-1.6.D.2.b

5% of the lesser of property value, or 115% 5% of the lesser of property value, or 115% of the median area price, or 150% of the of the median area price, or 150% of the conforming loan limit can be added onto conforming loan limit can be added onto the approved mortgage amount. the approved mortgage amount. ML 09-ML 09-1818. . http://www.hud.gov/offices/adm/hudclips/lehttp://www.hud.gov/offices/adm/hudclips/letters/mortgagee/index.cfmtters/mortgagee/index.cfm

8/4/2009

Energy Efficient MortgagesEnergy Efficient Mortgages

Improvements where the value of Improvements where the value of the energy saved is MORE than the the energy saved is MORE than the cost of the energy improvements cost of the energy improvements (including maintenance) qualify.(including maintenance) qualify.

4155.14155.1 6.D.2.d6.D.2.d

8/4/2009 104

105

Energy Efficient MortgagesEnergy Efficient MortgagesEnergy ImprovementsEnergy Improvements Energy improvements that are cost Energy improvements that are cost

effective.effective. A qualified rater uses a tool known as a A qualified rater uses a tool known as a

Home Energy Rating System (HERS).Home Energy Rating System (HERS). HERS report outlines improvements, HERS report outlines improvements,

costs and energy savings. costs and energy savings. http://www.fhaoutreach.gov/FHAHandbook/prhttp://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-1.6.D.2.god/infomap.asp?address=4155-1.6.D.2.g

All improvements must be completed.All improvements must be completed.

8/4/2009

Energy Efficient MortgagesEnergy Efficient Mortgages

How can I find a HERS rater?How can I find a HERS rater? Through Energy StarThrough Energy Star

http://www.energystar.gov/index.cfm?http://www.energystar.gov/index.cfm?fuseaction=new_homes_partners.shofuseaction=new_homes_partners.showHomesSearchwHomesSearch

Through the Residential Energy Through the Residential Energy Servicers NetworkServicers Networkhttp://www.natresnet.org/http://www.natresnet.org/

8/4/2009 106

Case TransfersCase Transfers FHA expects lenders to cooperate in FHA expects lenders to cooperate in

effecting a timely transfer through FHA effecting a timely transfer through FHA Connection.Connection.

Borrowers may not be charged a fee to Borrowers may not be charged a fee to effect the transfer.effect the transfer.

The transferring lender must provide a The transferring lender must provide a copy of the appraisal to the new lender copy of the appraisal to the new lender at no charge.at no charge.

http://www.fhaoutreach.gov/FHAHandbook/http://www.fhaoutreach.gov/FHAHandbook/prod/infomap.asp?address=4155-2.1.D.5prod/infomap.asp?address=4155-2.1.D.5..

8/4/2009 107

Case TransfersCase Transfers

Other Processing DocumentsOther Processing Documents Other processing documents need not Other processing documents need not

be provided to the new lender.be provided to the new lender. If processing documents are If processing documents are

transferred, a fee may be negotiated transferred, a fee may be negotiated between the two lenders. between the two lenders.

No charges for Streamline Refinances.No charges for Streamline Refinances. The transferring lender may retain any The transferring lender may retain any

lock-in fee paid by the borrower.lock-in fee paid by the borrower.

8/4/2009 108

Case TransfersCase Transfers

If the lenders will not cooperate on the If the lenders will not cooperate on the transfer…transfer…

Lender requesting a transfer should Lender requesting a transfer should prepare a letter to HOC requesting prepare a letter to HOC requesting cancellation of case. cancellation of case.

Fax letter to:Fax letter to:215-656-3434 (DE, DC, MD, 215-656-3434 (DE, DC, MD, MIMI, PA, VA , PA, VA WV)WV)215-656-3438 (CT, ME, MA, NH, NJ, NY, 215-656-3438 (CT, ME, MA, NH, NJ, NY,

OH, RI, VT). OH, RI, VT).

8/4/2009 109

Case TransfersCase Transfers

Letter requesting cancellation Letter requesting cancellation should include…should include…

Steps taken to try to resolve the Steps taken to try to resolve the issue.issue.

Any fees requested by transferring Any fees requested by transferring lenders.lenders.

A letter signed by the borrower A letter signed by the borrower requesting the transfer.requesting the transfer.

8/4/2009 110

Case TransfersCase Transfers

When the case number is transferred…When the case number is transferred… The new lender may use the same The new lender may use the same

appraisal provided it is not more than six appraisal provided it is not more than six months old.months old.

A revised appraisal with the name of the A revised appraisal with the name of the new lender is not required.new lender is not required.

The new lender should reimburse the The new lender should reimburse the former lender for the cost of the appraisal, former lender for the cost of the appraisal, but no additional fee is due the appraiser. but no additional fee is due the appraiser.

8/4/2009 111

Case TransfersCase Transfers

Where a new borrower and a new Where a new borrower and a new sales contract are involved…sales contract are involved…

The same appraisal may be used The same appraisal may be used provided it is not more than six provided it is not more than six months old.months old.

The appraiser does not have to The appraiser does not have to analyze the new sales contract.analyze the new sales contract.

8/4/2009 112

Case TransfersCase Transfers

Where a new borrower and a new Where a new borrower and a new sales contract are involved…sales contract are involved…

The new lender should collect the The new lender should collect the appraisal fee from the new borrower, appraisal fee from the new borrower, and then reimburse the former lender and then reimburse the former lender for the cost of the appraisalfor the cost of the appraisal

No additional fee is due the appraiser.No additional fee is due the appraiser. http://www.fhaoutreach.gov/FHAHandbook/http://www.fhaoutreach.gov/FHAHandbook/

prod/infomap.asp?address=4155-2.1.D.5.bprod/infomap.asp?address=4155-2.1.D.5.b

8/4/2009 113

Neighborhood WatchNeighborhood Watch

Your tool to track your FHA book Your tool to track your FHA book of business, and those of your of business, and those of your competitors.competitors.

1148/4/2009

115

Neighborhood WatchNeighborhood Watch

Provides reports on FHA loans with a Provides reports on FHA loans with a beginning amortization date for a beginning amortization date for a rolling 24 month period.rolling 24 month period.

Reports can be pulled for a single Reports can be pulled for a single lender or all lenders, at the institution lender or all lenders, at the institution level or at the branch level.level or at the branch level.

Reports can be pulled at the national Reports can be pulled at the national level down to a single zip code. level down to a single zip code.

8/4/2009

116

Neighborhood WatchNeighborhood Watch

8/4/2009

FHA ConnectionFHA Connection

6/8/2009 117

FHA ConnectionFHA Connection

6/8/2009 118

FHA ConnectionFHA Connection

6/8/2009 119

120

FHA ConnectionFHA Connection

6/8/2009

FHA ConnectionFHA Connection

6/8/2009 121

FHA ConnectionFHA Connection

6/8/2009 122

FHA ConnectionFHA Connection

6/8/2009 123

124

Neighborhood WatchNeighborhood Watch

Access is available to lenders Access is available to lenders through FHA Connection. After through FHA Connection. After logging in, click on logging in, click on Single Family Single Family FHAFHA, and on the next screen, click , and on the next screen, click on on Neighborhood WatchNeighborhood Watch..

Or, access the public site at Or, access the public site at https://entp.hud.gov/sfnw/public/https://entp.hud.gov/sfnw/public/

8/4/2009

Where to Get More Where to Get More InformationInformation

1258/4/2009

126

Where to Get More Where to Get More InformationInformation

1-800-CALLFHA1-800-CALLFHA (225-5342) (225-5342): The source for : The source for all FHA questions.all FHA questions.

www.fhaoutreach.gov/FHAFAQwww.fhaoutreach.gov/FHAFAQ Over 1,300 on-line frequently asked questions. Over 1,300 on-line frequently asked questions.

www.fha.govwww.fha.gov Up-to-date info about FHA programs and more. Up-to-date info about FHA programs and more.

http://www.hud.gov/offices/adm/hudclips/http://www.hud.gov/offices/adm/hudclips/index.cfm. Mortgagee letters, handbooks and index.cfm. Mortgagee letters, handbooks and more.more.

8/4/2009

That’s all. That’s all.

Questions?Questions?

1278/4/2009