Pulp, Paper and Paperboard Markets Gradual Upturn Underway after Recent Downturn UNECE Market...

30

Pulp, Paper and Paperboard Markets Gradual Upturn Underway after Recent Downturn UNECE Market Discussion, September 2002

-

Upload

elaine-patrick -

Category

Documents

-

view

217 -

download

1

Transcript of Pulp, Paper and Paperboard Markets Gradual Upturn Underway after Recent Downturn UNECE Market...

Pulp, Paper and Paperboard Markets

Gradual Upturn Underwayafter Recent Downturn

UNECE Market Discussion, September 2002

A steep downturn in industrial production (and GDP growth) in North America and Europe resulted in receding demands for paper & paperboard in packaging and print advertising media in 2001

An upturn appears underway in 2002 for pulp, paper and paperboard markets, but recovery is likely to be gradual

North American paperboard output in the first half of 2002 is up by about 1% relative to first half 2001

The upturn in paperboard output follows the upturn in overall industrial production

3,300

3,500

3,700

3,900

1997 1998 1999 2000 2001 2002

Mo

nth

ly P

rod

uc

tio

n (

'00

0 m

.t.)

-10

-5

0

5

10

Ye

ar-

ove

r-ye

ar

cha

ng

e (

%)

U.S. Paperboard Prod., 5-mo. avg.Industrial Production (% Change)

Sources: AF&PA, U.S. Federal Reserve

Paperboard production declined with industrial production, but an upturn is underway

North American paper output in the first half of 2002 was down by about - 6% relative to first half 2001

An upturn in paper production is underway but lagging, mainly due to steep declines in advertising expenditures in 2001

2,900

3,100

3,300

3,500

1997 1998 1999 2000 2001 2002

Mon

thly

pro

duct

ion

('000

m.t

.)

-10

-5

0

5

10

Yea

r-ov

er-y

ear

chan

ge (

%)

U.S. Paper Production, 5-mo. avg.Industrial Production (% Change)

Sources: AF&PA, U.S. Federal Reserve, McCann Erickson

Advertising Spending

-7%

11%8%8%7%

2%(f)

-10

-5

0

5

10

15

'97 '98 '99 '00 '01 '02

% C

han

ge

The recent downturn follows a period of consolidation and structural change within the pulp & paper sector.

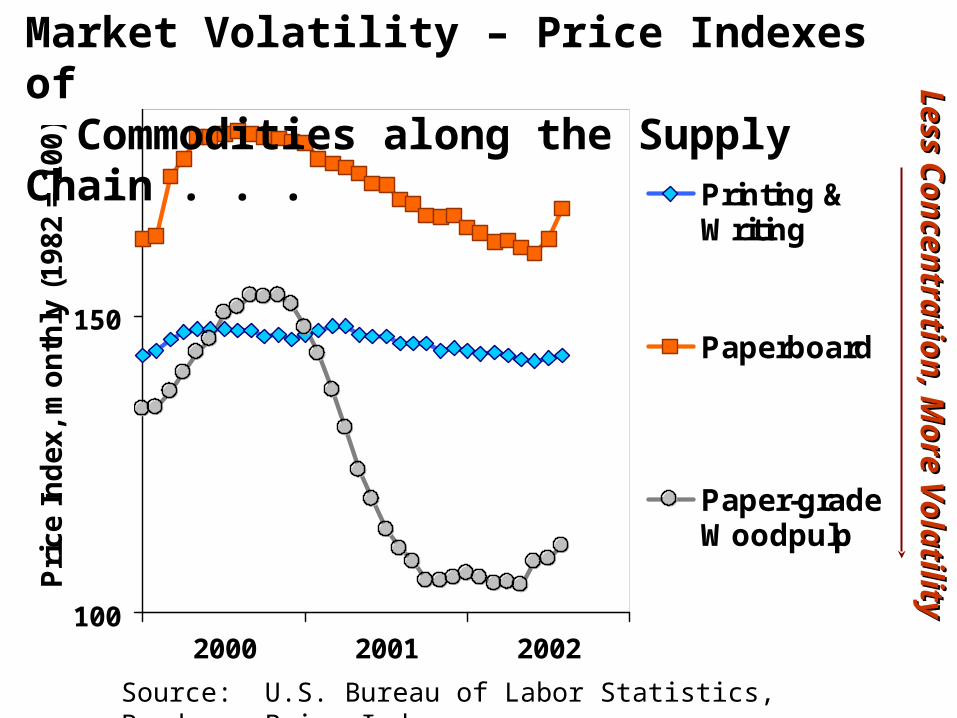

With higher capacity concentration in paper & paperboard, price impacts of the downturn were offset by strategic adjustments (mill closures, etc.), and price volatility was passed down along the supply chain . . .

Consolidation Trends – Capacity Shares of ‘Top 3 Companies’ in North America . . .

Source: Miller Freeman

44

38

3127

57 58

43

29

0

10

20

30

40

50

60

Pe

rce

nt

of

To

tal

Ca

pa

cit

y

1991 2001

Coated Papers

Uncoated FreeSheet

Linerboard

Market Pulp

100

150

2000 2001 2002

Pri

ce I

nd

ex,

mo

nth

ly (

1982

= 1

00)

Printing &Writing

Paperboard

Paper-gradeWoodpulp

Market Volatility – Price Indexes of Commodities along the Supply Chain . . .

Source: U.S. Bureau of Labor Statistics, Producer Price Indexes

Less C

on

centratio

n, M

ore V

olatility

Less C

on

centratio

n, M

ore V

olatility

The global pulp market collapsed from mid-year 2000 through 2001, but turned upward in the first half of 2002

In the past several months, pulp prices have subsided with another short-term buildup of pulp inventory, but the longer term (futures) outlook remains positive with a declining inventory trend

Norscan Pulp Inventory, NBSK List prices & Futures

0

500

1,000

1,500

2,000

2,500

Ju

n 9

7

Se

p 9

7

De

c 9

7

Ma

r 98

Ju

n 9

8

Se

p 9

8

De

c 9

8

Ma

r 99

Ju

n 9

9

Se

p 9

9

De

c 9

9

Ma

r 00

Ju

n 0

0

Se

p 0

0

De

c 0

0

Ma

r 01

Ju

n 0

1

Se

p 0

1

De

c 0

1

Ma

r 02

Ju

n 0

2

Se

p 0

2

De

c 0

2

Ma

r 03

Ju

n 0

3

Se

p 0

3

De

c 0

3

'000 Tonnes

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$/tonneNorscan Inventory

NBSK list - Europe

3-mo. NBSK (weekly)

Futures (June 02)

Futures (Sept 02)

prices turned up in 1st half 2002, then subsided market views long-term as “deteriorated but positive”

Sources: PPPC, PULPEX

Other Aspects of the Downturn:

EU/EFTA production dropped -3% as consumption fell by -4% in 2001

Growth rates for the Russian Federation also dropped, although growth remained positive; the trade balance drifted into a deficit

U.S. purchases and production of paper & paperboard dropped by >10% since 1999

Industry profits were severely impacted (as were capacity growth and investment) although profits turned upward in 2002

Long-term sustainability of pulpwood demand becomes an issue for the United States

-4%

-2%

0%

2%

4%

6%

8%

1998 1999 2000 2001

ProductionConsumption

EU/EFTA – Paper & paperboard trendsChange from one year earlier

Source: UNECE

Growth in production and Growth in production and consumption both subsidedconsumption both subsided

0%

10%

20%

30%

40%

1998 1999 2000 2001

ProductionConsumption

Russian Federation – Paper & paperboardChange from one year earlier

Source: UNECE

Production lagging; Production lagging; Growth declined but Growth declined but remained positiveremained positive

Russia's pulp and paper exports and Imports in 2000-2001 (million USD)

-100

-50

0

50

100

150

200

250

300

1st qtr.2000

2nd qtr.2000

3rd qtr.2000

4th qtr.2000

1st qtr.2001

2nd qtr.2001

3rd qtr.2001

4th qtr.2001

Mill

ion

US

$

Exports Imports Total trade balance

Sources: State Customs Committee, PPB Express

6,000

6,500

7,000

7,500

8,000

1997 1998 1999 2000 2001 2002

Mo

nth

ly P

rod

uct

ion

('0

00 m

.t.)

Paper & Paperboard PurchasesPaper & Paperboard Production

Source: AF&PA

Down Down more than more than 10% since 199910% since 1999(largest drop since 1970s)(largest drop since 1970s)

5-month 5-month movingmovingaveragesaverages

-2

-1

0

1

2

3

4

I 95

II 95

III 95

IV 9

5

I 96

II 96

III 96

IV 9

6

I 97

II 97

III 97

IV 9

7

I 98

II 98

III 98

IV 9

8

I 99

II 99

III 99

IV 9

9

I 00

II 00

III 00

IV 0

0

I 01

II 01

III 01

IV 0

1

I 02

II 02

III 02B

illio

ns

of

Do

llars

After-Tax Profits, Paper & Allied Products, Quarterly

Source: U.S. Department of Commerce

The downturn in profits was severe in 2001, although profits improved in 2002

2001/2000: -89%2001/2000: -89%2002/2001: +23% (22002/2001: +23% (2ndnd Qtr.) Qtr.)

Linear Polynomial

3.0%

2.7%2.9% 2.8%

0.6% 0.6%

1.4%

-1.3%

-2%

-1%

0%

1%

2%

3%

4%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

An

nu

al G

row

th in

Cap

acit

y

With receding demand, weak exports and a flood of imports, U.S.paper industry capital investment declined, and capacity growthground to a halt.

In 2001, for the first time in many decades, U.S. capacity actually declined. Very little capacity growth is anticipated in the next several years.

U.S. Capacity Growth

Source: AF&PA

0

5

10

15

20

25

1984 1987 1990 1993 1996 1999 2002

$/cu

bic

met

er

ALA FLA

GA LA

N.C. VA

S.C. AVG.

Southern pine pulpwood Southern pine pulpwood stumpage prices have dropped stumpage prices have dropped by more than 50% since 1998:by more than 50% since 1998:

Southern Pine PulpwoodStumpage (nominal $)

Supply Side:

• Plantations • Thinning • Drought • Beetles • Recycling • Sawmill Residues

Demand Side:

• Purchases • Production • Exports • Imports • Pulpwood Exports

Source: Timber Mart-South

0

60

120

180

240

1970 1980 1990 2000 2010 2020

Pu

lpw

oo

d, M

illio

ns

of

cu

bic

me

ters

0

20

40

60

80

Wo

od

Pu

lp, M

illio

ns

of

m.t

.

Actual Pulpwood (F.S., FRA)

Projected Pulpwood (RPA)

Actual Wood Pulp (AF&PA) Projected Wood Pulp (RPA)

U.S. Woodpulp Production and Pulpwood Receipts at Pulp Mills, Historical and Projected

Woodpulp production and pulpwood receipts Woodpulp production and pulpwood receipts have declined by ~15% since the mid-1990s. have declined by ~15% since the mid-1990s. Both are projected to recover Both are projected to recover graduallygradually, not , not reaching previous peak levels until after 2020.reaching previous peak levels until after 2020.

Macro Perspectives:

An upturn in GDP & industrial output is clearly underway, but a secondary slowdown or “double-dip” is still viewed as a concern. There is still a long climb ahead to full recovery of growth in GDP and industrial output

-1%

0%

1%

2%

3%

4%

5%

III98

IV98

I99

II99

III99

IV99

I00

II00

III00

IV00

I01

II01

III01

IV01

I02

II02

U.S. GDP – Change from one year earlier, quarterly

Source: U.S. Department of Commerce

Upturn underway but “double-dip” still a threat

0%

1%

2%

3%

4%

III98

IV98

I99

II99

III99

IV99

I00

II00

III00

IV00

I01

II01

III01

IV01

I02

II02

EU-15 GDP – Change from one year earlier, quarterly

Source: Eurostat

European GDP upturn lagging and less certain

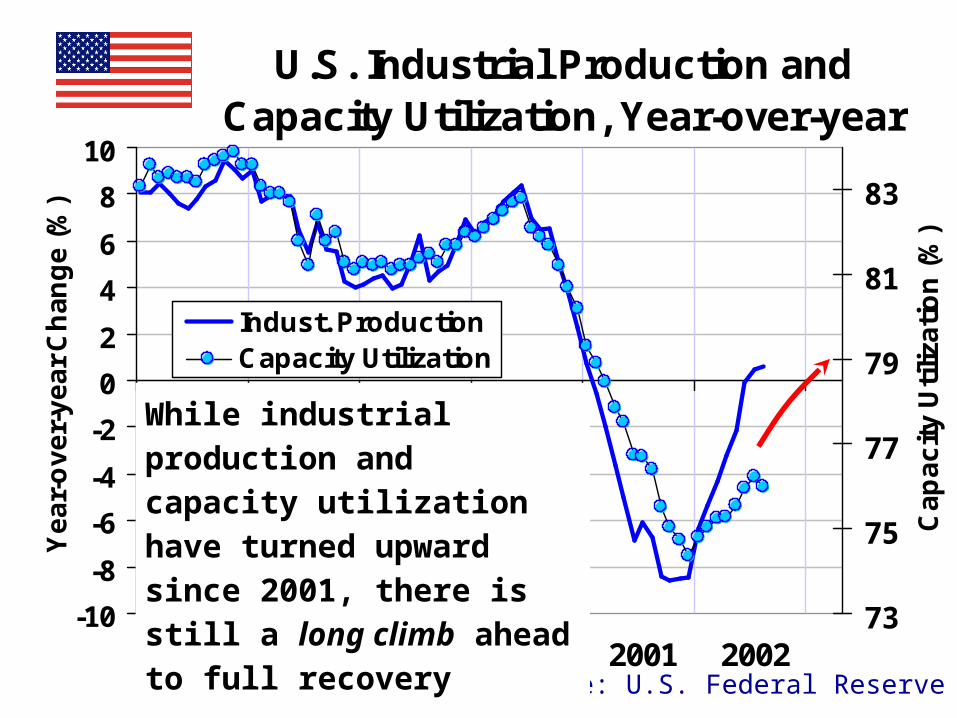

U.S. Industrial Production and Capacity Utilization, Year-over-year

-10

-8

-6

-4

-2

0

2

4

6

8

10

1997 1998 1999 2000 2001 2002

Ye

ar-

ov

er-

ye

ar

Ch

an

ge

(%

)

73

75

77

79

81

83

Ca

pa

cit

y U

tiliz

ati

on

(%

)

Indust. ProductionCapacity Utilization

Source: U.S. Federal Reserve

While industrial production and capacity utilization have turned upward since 2001, there is still a long climb ahead to full recovery

-10

-8

-6

-4

-2

0

2

EU-15 & euro zone industrial production – Change from one year earlier, monthly

U.S. industrial production – Change from one year earlier, monthly

Source: Eurostat

Source: Federal Reserve

EU-15

euro zone

80

85

90

95

100

105

110

115

1995 1996 1997 1998 1999 2000 2001 2002

Do

llar

Ind

ex

0

5

10

15

20

25

30

35

Mo

nth

ly D

efi

cit

(B

illi

on

s,

'82 $

)

.

Real Broad Dollar Index

Real Trade Deficit in Goods

Federal Funds Rate (%)

01234567

1995 1996 1997 1998 1999 2000 2001 2002

Despite dramatic reductionsDespite dramatic reductionsin interest rates by thein interest rates by theFederal Reserve, theFederal Reserve, theU.S. Dollar andU.S. Dollar andTrade DeficitTrade Deficitremain veryremain veryhighhigh

Summary:

Economic outlook is positive but said to be . . .

“slow and uneven” (Federal Reserve)

or

“deteriorated but positive” (IFO World Survey)

gradual recovery appears most likely for pulp & paper markets markets

9

12

15

18

21

1996 1997 1998 1999 2000 2001

Mil

lio

ns

of

To

ns

Exports Imports

Paper & Paperboard Trade:

Data Sources: AF&PA and Commerce Dept.Data include “paper, paperboard & products”

The U.S. trade deficit in paper & board has widened significantly since 1997 . . .

Sources: Capital Project Spending Trend – Pulp & Paper (Paperloop) Project Report Depreciation (Paper & Allied Products) – Bureau of Census

U.S. Pulp & Paper Industry Capital Spending & Depreciation

0

3

6

9

12

15

1996 1997 1998 1999 2000 2001 2002

Bil

lio

ns

of

Do

lla

rs

Capital Project Spending Depreciation

Trends show declining capital spending, now well below equipment depreciation levels . . .

(Planned)

Value of Goods Imports, quarterly

100

150

200

250

300

350

1996 1997 1998 1999 2000 2001 2002

Bil

lio

ns

of

Do

lla

rs

Source: U.S. Department of Commerce, BEA

?Imports subsided in 2000 - U.S. role as a “global engine of growth” diminished

. . . but value of goods imports surged again recently