Public Utilities: Power & Railways - Indian Institute of ... · PDF filePublic Utilities:...

46

1 Public Utilities: Power & Railways Cutting the Gordian Knot Module 11 Contemporary Themes in India’s Economic Development and the Economic Survey Arvind Subramanian Chief Economic Adviser 16-06-2017 MINISTRY OF FINANCE GOVERNMENT OF INDIA

Transcript of Public Utilities: Power & Railways - Indian Institute of ... · PDF filePublic Utilities:...

1

Public Utilities: Power & RailwaysCutting the Gordian Knot

Module 11

Contemporary Themes in India’s

Economic Development and the Economic Survey

Arvind Subramanian

Chief Economic Adviser

16-06-2017

MINISTRY OF FINANCE

GOVERNMENT OF INDIA

2

Overview

• Public Utilities

• Power

• Railways

3

Public Utilities- Natural Monopolies

• E.g. – Electricity, Water, Railways, Roadways, Telecom, Internet, Data

etc.

• Require Large Capital Investments

• High fixed costs, Economies of Scale & Long gestation period

• Network effects- Becomes more useful as more people use it (Facebook,

Messaging Apps)

• Hence, tend to be natural monopolies

• Dilemma

• If Public Sector- Inefficiency

• If Private Sector- Monopoly Profits and High Prices

4

Public Utilities-From government ownership to Regulation• Public ownership resulted in efficiency decline (Industrial Policy Resolution,1956)

• Thatcher, Pinochet, Reagan revolution - Public Sector inefficiency + technological

development changed thinking

• Solution to Dilemma: Less Ownership with effective regulation

• Sectors unbundled and opened for private sector but under the aegis of a regulator

• Regulator has to balance the social welfare maximization vs. the profit maximization for the

operator of the business

• Social Welfare involves fairness and equity as well

• Information Asymmetry – Gold Plating & Moral Hazard- Too big to fail

• Standards of Performance

5

2012 2016

https://www.nasa.gov/feature/goddard/2017/new-night-lights-maps-open-up-possible-real-time-applications

6

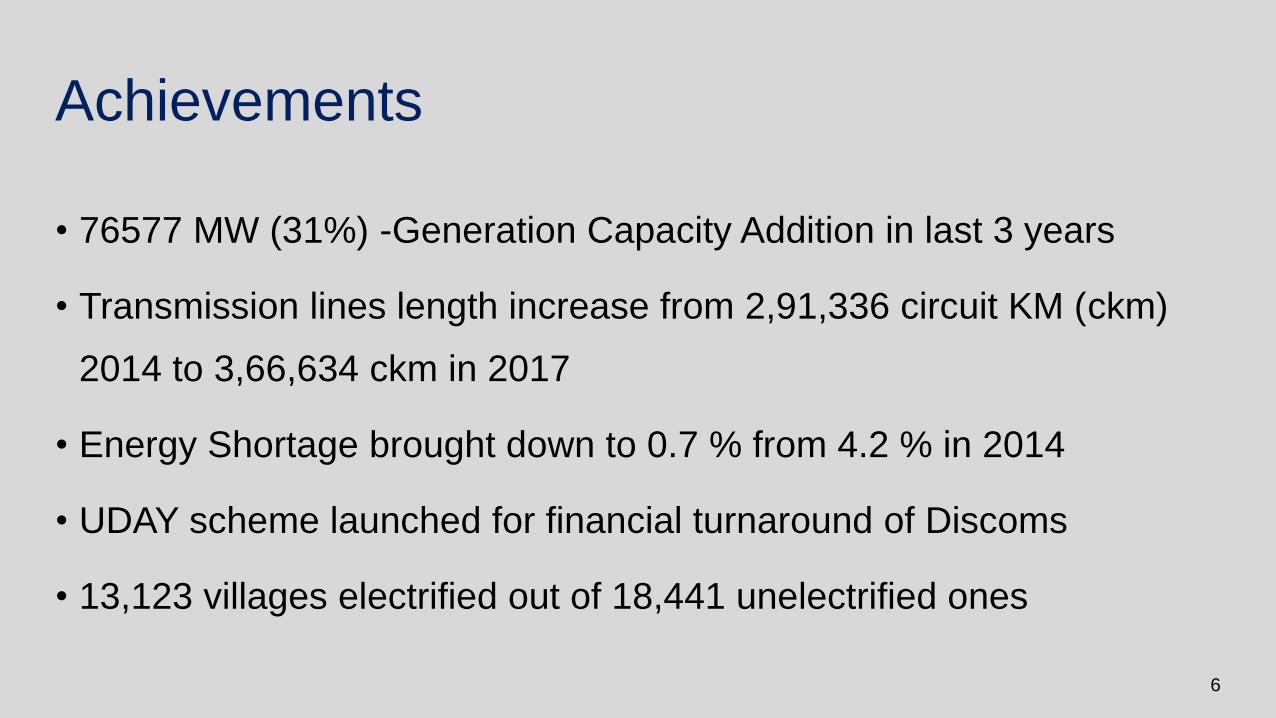

Achievements

• 76577 MW (31%) -Generation Capacity Addition in last 3 years

• Transmission lines length increase from 2,91,336 circuit KM (ckm)

2014 to 3,66,634 ckm in 2017

• Energy Shortage brought down to 0.7 % from 4.2 % in 2014

• UDAY scheme launched for financial turnaround of Discoms

• 13,123 villages electrified out of 18,441 unelectrified ones

7

Section 1Power

8

Overview

• Interesting facts

• Power Sector Structure

• Contracts Structure

• Challenges

• UDAY

9

Some Interesting Facts• India is the world's third largest electricity producer (1368 BU*)– After China

(5682 BU) and USA (4324 BU)

• India is also the fourth largest consumer of electricity – 1135 BU

• Per capita electricity consumption is low despite cheap electricity tariffs- 1010

kWh vs 12973 kWh for USA

• India accounts for over 300 million of the world’s total 1.4 billion people with

no access to electricity

*BU = Billion Units 1 Unit = 1 kWh

Sources: Central Electricity Authority (CEA), USA Energy Information Administration (EIA)

10

Electricity Generation Capacity addition at a CAGR of 8.7% since 1947

Source: CEA Website

0

50

100

150

200

250

300

350

0

200

400

600

800

1000

12001

947

1950

1956

1961

1966

19

69

1974

1979

1980

1985

1990

1992

19

97

2002

2007

2012

2013

2014

2015

20

16

Insta

lled C

ap

acity (

‘000 M

W)

Per

Capita C

onsum

ption (

kW

h)

Installed Capacity (MW) Per Capita Consumption (kWh)

11

Electricity Access: India still far behind its BRICS peers

0

10

20

30

40

50

60

70

80

90

100T

ZA

KE

N

MM

R

NG

A

BG

D

IND

SA

S

NP

L

ZA

F

LK

A

IDN

PA

K

ME

X

IRN

BR

A

EG

Y

BT

N

CH

N

RU

S

Perc

ent

of P

opula

tion

Source: WDI database

12

Low Electricity Access levels in Poor States

0

10

20

30

40

50

60

70

80

90

100D

L

GA

CH

PB

AP

TN

KL

WB

HP

GJ

MZ

UK

KA

MH

CG

HR JK

RJ

TR

MP

OD

AS

UP

BR

JH

Perc

ent

Households having electricity (%) 2017 India Average (2017)

Source: Uday Website, Ministry of Power

13

T&D* Losses-Far away from BRICS peers

0

5

10

15

20

25

30

35

40

45

CHN ZAF IDN RUS EGY BGD LKA BRA NGA PAK KEN TZA IND MMR NPL

Perc

ent

2000 2014

* Transmission and Distribution Losses. They are a measure of the technical efficiency and losses due to

electricity theft

14

AT&C* losses for 2014-15- Still very high in poorer states

0

10

20

30

40

50

60

AP DL TL HP GJ PB KL KA UK MH TN AS CG RJ MP HR UP WB OR BR JH JK

Percent

• Aggregate Technical and Commercial Losses. They include technical losses, theft and commercial losses due

to non-payment of electricity bills by consumers

• Source: Ministry of Power

15

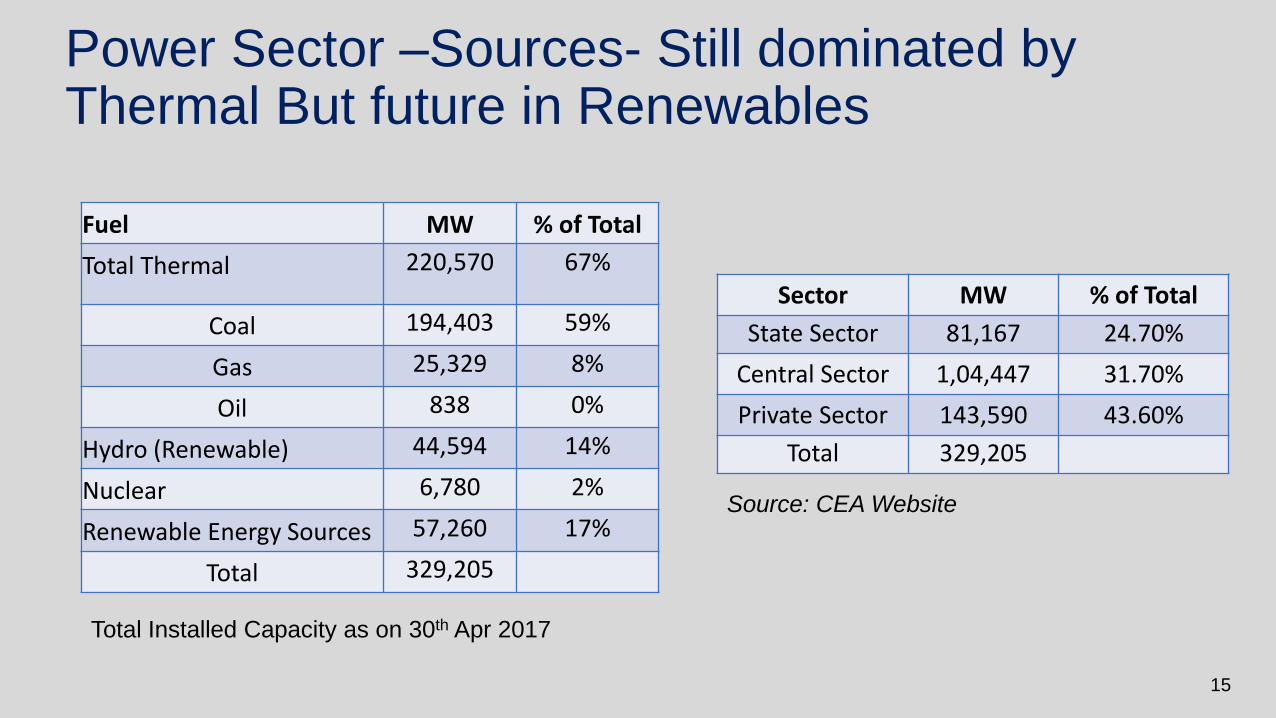

Power Sector –Sources- Still dominated by Thermal But future in Renewables

Fuel MW % of Total

Total Thermal 220,570 67%

Coal 194,403 59%

Gas 25,329 8%

Oil 838 0%

Hydro (Renewable) 44,594 14%

Nuclear 6,780 2%

Renewable Energy Sources 57,260 17%

Total 329,205

Total Installed Capacity as on 30th Apr 2017

Source: CEA Website

Sector MW % of Total

State Sector 81,167 24.70%

Central Sector 1,04,447 31.70%

Private Sector 143,590 43.60%

Total 329,205

16

Transmission lines 230-500 kV

r

Generator

Transmission subs

66-115 kV lines

Distribution subs

Distribution lines

Electricity Supply Segments: Generation, Transmission, Distribution

17

G

T

D/R

Consumers

No Competition

• No Choice

• Government makes decisions

G

D/R

Consumers

G G G EG

T/MO

Wholesale Competition

• Distribution/retail companies have choice

G

Consumers

G G G EG

D/R

T/MO

Retail Competition

• Consumers have choice

Evolving Industry Structure- Last Mile Still Left!

MO = Market Operator

EG = Embedded Generator/Captive

= Who has choice

Before Electricity Act 2003 After Electricity Act 2003 Future

Natural Monopolies

D = Distribution Network Owner

T = Transmission Network Owner

R = Retailer

G = Generator

18

Institutional Structure- Both Centre and State involved

in governance

State Gencos STUs

Generation

CPSU (NTPC) CTU

(POWERGRID)

IPPs(Tata)

Private

Licensees

(Delhi &

Mumbai)

Agricultural

Domestic

Commercial

Industrial

Others

Captive Plants

(Essar)Captive

Transmission Distribution Consumption

Power Trading

Companies and Power

Exchanges

Open Access

State DISCOMS

19

Contracts Structure- Dominated by long term Power Purchase Agreements (PPAs)

• Specific Seller and Buyer

• Pricing based on cost of asset and socialized over all beneficiaries

Long Term –12 - 25 years

• Specific Seller and Buyer set

• Pricing arrived at as a percentage of long term transmission pricing

• Earnings used to reduce cost of asset for long term consumers

Short Term –Up to 3 months

• Access for trades through Power Exchanges - Collective transactions

• Charges regulated by the Commission

Day Ahead Market– For the next day

only

Contract Type Share (in percent)

Long Term Contracts 91

Short Term Contracts 5

Day Ahead Market 4

Source: CEA website

20

Challenges

21

1. Complex tariff schedules; One price for petroleum but 100 prices for power

Consumer Category

Energy

Charge

(Rs /Unit)

Consumer Category

Energy

Charge

(Rs /Unit)

Consumer Category

Energy

Charge

(Rs /Unit)

LT-I:DOMESTIC (Telescopic) LT-V:AGRICULTURE ** SEASONAL INDUSTRIES (off season Tariff)

LT I(A):Upto 50 Units/Month 1.45 LT-V(A):AGRICULTURE WITH DSM

MEASURES

11 kV 7.25

LT I(B):>50 and upto 100 Units/Month Corporate Farmers & IT Assesses 2.50 33 kV 6.59

First 50 Units 1.45 Wet Land Farmers (Holdings >2.5 acre) 0.50 132 kV & Above 6.33

51-100 Units 2.60 Dry Land Farmers (Connections > 3 nos.) 0.50 TIME OF DAY TARIFFS (6 PM to 10 PM)

LT I(C):>100 and upto 200 Units/Month Wet Land Farmers (Holdings ≤ 2.5 acre) 0.00 11 kV 7.07

First 50 2.60 Dry Land Farmers (Connections ≤ 3 nos.) 0.00 33 kV 6.62

51-100 2.60 LT-V(B):AGRICULTURE WITHOUT DSM

MEASURES

132 kV & Above 6.20

101-150 3.60 Corporate Farmers & IT Assesses 3.50 HT-I(B):FERRO ALLOY UNITS

151-200 3.60 Wet Land Farmers (Holdings >2.5 acre) 1.00 11 kV 5.68

LT I(D):Above 20 0 Units/Month Dry Land Farmers (Connections > 3 nos.) 1.00 33 kV 5.23

First 50 2.60 Wet Land Farmers (Holdings ≤ 2.5 acre) 0.50 132 kV & Above 4.81

51-100 3.25 Dry Land Farmers (Connections ≤ 3 nos.) 0.50 HT-II:OTHERS

101-150 4.88 LT-V(C):OTHERS 11 kV 7.25

151-200 5.63 Salt farming units upto 15HP 3.70 33 kV 6.59

201-250 6.70 Rural Horticulture Nurseries upto 15HP 3.70 132 kV & Above 6.33

251-300 7.22 LT-VI:STREET LIGHTING AND PWS TIME OF DAY TARIFFS (6 PM to 10 PM)

301-400 7.75 LT-VI(A):STREET LIGHTING 11 kV 8.30

401-500 8.27 Panchayats 5.64 33 kV 7.64

Above 500 8.80 Municipalities 6.16 132 kV & Above 7.38

LT-II:NON DOMESTIC/COMMERCIAL Municipal Corporations 6.69 HT-III:AIRPORTS,BUS STATIONS AND RAILWAY

STATIONSLT II(A):Upto 50 Units/Month 5.40 LT-VI(B):PWS SCHEMES 11 kV 6.91

LT II(B):Above 50 Units/Month Panchayats 4.59 33 kV 6.31

First 50 6.63 Municipalities 5.64 132 kV & Above 6.01

51-100 7.38 Municipal Corporations 6.16 TIME OF DAY TARIFFS (6 PM to 10 PM)

101-300 8.54 LT-VI(C):NTR Sujala Padhakam 4.00 11 kV 7.96

301-500 9.06 LT-VII:GENERAL 33 kV 7.36

Above 500 9.59 LT-VII(A):GENERAL PURPOSE 6.86 132 kV & Above 7.06

LT II(C):ADVERTISEMENT HOARDINGS 11.58 LT-VII(B):RELIGIOUS PLACES (CL ≤ 2 KW) 4.70 HT-IV: Govt., LIFT IRRIGATION, AGRICULTURE

AND CPWSLT-III:INDUSTRY LT-VIII: TEMPORARY SUPPLY 9.90 Govt. Lift Irrigation & Agriculture 5.64

Industry (General) 6.38 HT-I:INDUSTRY Composite Water Supply Schemes 4.61

Seasonal Industries (off season) 7.09 HT-I(A): INDUSTRY GENERAL HT-V:RAILWAY TRACTION 6.68

Pisciculture/Prawn culture 4.63 11 kV 6.02 HT-VI:TOWNSHIPS AND RESIDENTIAL COLONIES 5.96

Sugarcane crushing 4.63 33 kV 5.57 HT-VII:GREEN POWER 11.32

Poultry farms 5.63 132 kV & Above 5.15 HT-VIII:TEMPORARY

Mushroom & Rabbit Farms 5.63 INDUSTRIAL COLONIES RURAL ELECTRIC CO-OPERATIVES

Floriculture in Green House 5.63 11 kV 5.96 Kuppam 0.24

LT-IV:COTTAGE INDUSTRIES & OTHERS 33 kV 5.96 Anakapally 1.38

a) Cottage Industries upto 10 HP 3.75 132 kV & Above 5.96 Chipurupally 0.22

b) Agro Based Activity upto 10 HP 3.75

Source: Andhra Pradesh Tariff order

22

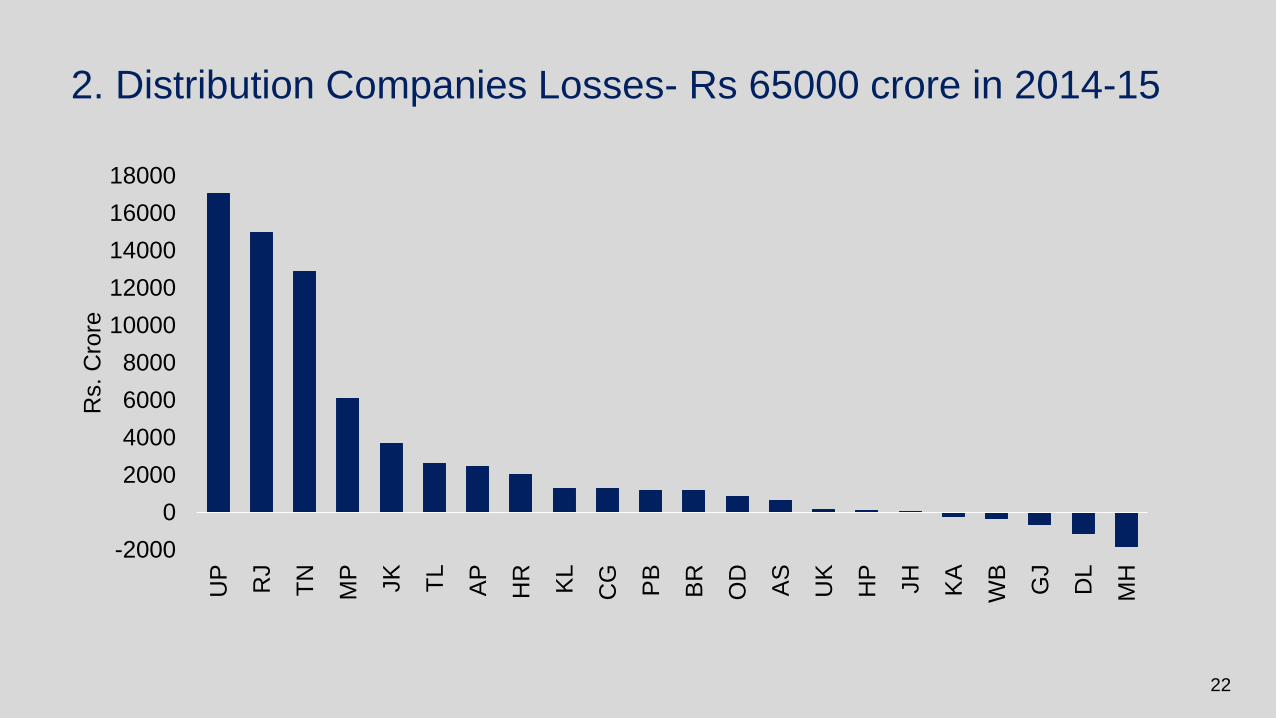

2. Distribution Companies Losses- Rs 65000 crore in 2014-15

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

UP

RJ

TN

MP

JK

TL

AP

HR

KL

CG

PB

BR

OD

AS

UK

HP

JH

KA

WB

GJ

DL

MH

Rs.

Cro

re

23

Tariffs per unit: 2013-14Subsidies

3. Cross-Subsidies hurting Make in India

0

5

10

15

20

25

30

35

40

45

5020

12

-13

2013-1

4

2014-1

5

Rs

(thousands o

f cro

res)

0

1

2

3

4

5

6

7

8

Ag

ricu

ltu

re

Do

mestic

Indu

str

ial

Railw

ays

Com

merc

ial

Rupees

Sources: PFC Status of Power Utilities Report & Planning Commission State Discoms Report

24

3. Expensive and Low quality electricity supply to Industry

AustraliaAustria

Bangladesh

Belgium

Chile

Czech Republic

Denmark

France

Hungary

India

Indonesia

ItalyJapan

Luxembourg

Mexico

PortugalSlovenia

South Africa

Switzerland

Turkey

USA

Australia

Austria

Bangladesh

Belgium

Chile

Czech Republic

Denmark

France

Hungary

India

Indonesia

ItalyJapan

Luxembourg

Mexico

Portugal Slovenia

South Africa

Switzerland

Turkey

USA

(300) (200) (100) 0 100 200 300 400

Pe

r C

ap

ita

GD

P

PPP Exchange RatesMarket Exchange Rates

More Expensive More Expensive

Colours represent the quality of electricity supply (on a scale of 1 to 7)

Source: World Economic Forum-Global Competitiveness Report 2015-16

(score >6)

(4< score <6)

(score <4)

25

3. Cross-Subsidies and Poor quality of electricity supply affect Make in India

APBR

CH

DLGJ

HP

HRJH

JK

KA

KL

MH

MP

OR

PBRJ TN

UP

UT

WB

IND

60

70

80

90

100

110

120

130

Industr

ial Tariff (

US

D/M

Wh)

Per Capita GSDP

(response <10%)

(10%< response <20%)

(response >20%)

Colours highlight the share of firms (in %) identifying electricity as a major constraint in their state

Source: World Bank’s Enterprise Survey of Industries (2013-14). Industrial tariffs are from the Planning

Commission/Niti Aayog

26

0

0.5

1

1.5

2

2.5

3

3.5

TN AP WB HR MP DL GJ TL MH OR KA PB CH BR UT JH UP HP RJ KL JK

Rs/k

Wh

4. India still not one market for power: States impose exorbitant taxes on purchase from other states

Cross Subsidy Surcharge imposed by states for purchasing

electricity from power exchange, 2015-16

27

5. New Challenge: Declining Renewable Energy Prices But threat to Thermal Power

0

2

4

6

8

10

12

14

16

18

20

201

1

201

1

2012

201

2

201

2

201

3

201

3

201

3

201

4

201

4

201

4

2015

201

5

201

5

201

5

201

7

201

7

Rs/k

Wh

State Rate (Rs /kWh)

Andhra

Pradesh

4.84

Gujarat 4.19

Karnataka 4.5

Madhya

Pradesh

4.78

Maharashtra 3.82-5.56

Rajasthan 5.76-6.04

Tamil Nadu 4.16

Feb 2017 Bid 3.46

SOLAR WIND

Sources: MNRE

28

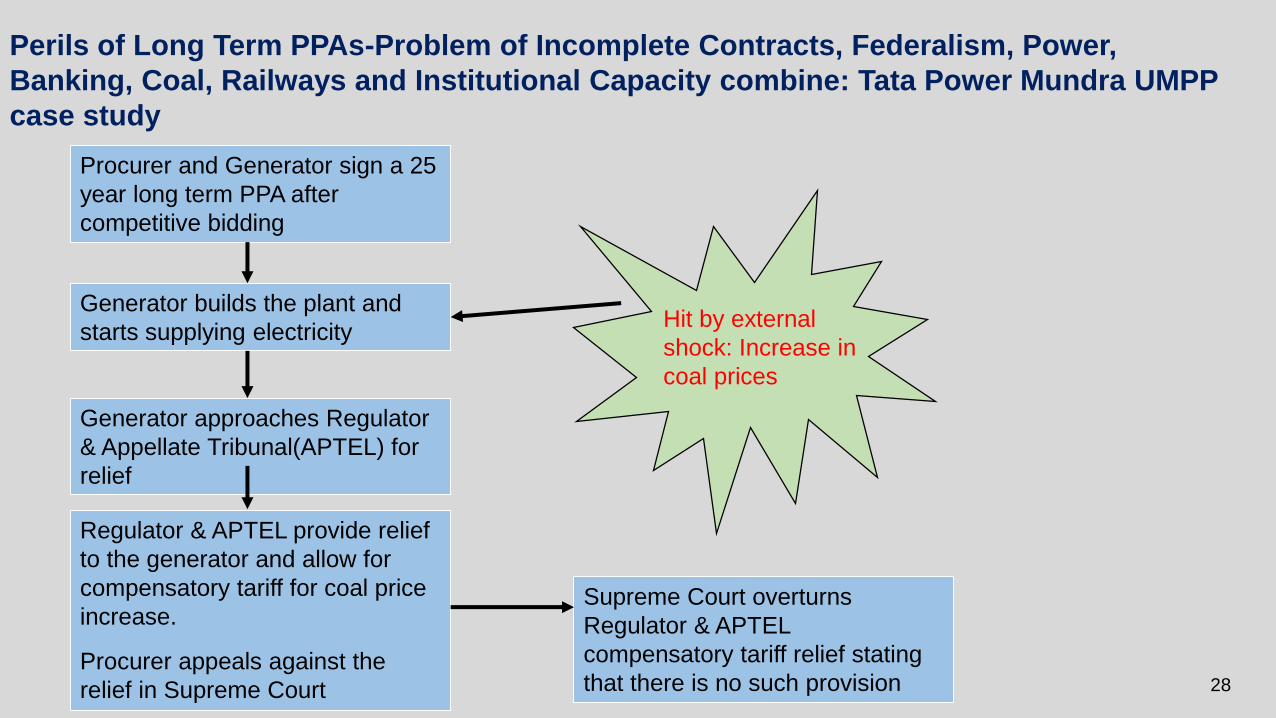

Perils of Long Term PPAs-Problem of Incomplete Contracts, Federalism, Power,

Banking, Coal, Railways and Institutional Capacity combine: Tata Power Mundra UMPP

case study

Procurer and Generator sign a 25

year long term PPA after

competitive bidding

Generator builds the plant and

starts supplying electricityHit by external

shock: Increase in

coal prices

Generator approaches Regulator

& Appellate Tribunal(APTEL) for

relief

Regulator & APTEL provide relief

to the generator and allow for

compensatory tariff for coal price

increase.

Procurer appeals against the

relief in Supreme Court

Supreme Court overturns

Regulator & APTEL

compensatory tariff relief stating

that there is no such provision

29

5. New challenge: Power Generators’ Viability Threatened

Given large cost over-runs, break even tariff is well above current merchant rates*

*: Tariffs are in Rs./kWh and on shown in RHS. Costs are in Rs. Million.

0

1

2

3

4

5

6

7

8

9

0

20

40

60

80

100

120

140

160G

VK

- A

lakna

nda

Unlis

ted C

om

p

GM

R -

Raik

hed

a

GV

K -

Go

ind

wal S

ah

ib

Ja

ype

e -

Nig

rie

Lan

co

- A

ma

rkan

tak

Lan

co

- B

aba

ndh

Lan

co

- V

ida

rbh

a

Ja

ype

e -

Ba

ra I

Unlis

ted C

om

p

Relia

nce -

Sasa

n

Re

lian

ce -

Butib

ori

JS

W -

Raj W

est

GM

R -

Ka

mala

ng

a -

I

Original Cost per MW (Rs mn) Cost overrun per MW (Rs mn)

Required Tariff (Rs/KwH) (RHS) Current Merchant tariff (Rs/KwH) (RHS)

Sources: Credit Suisse Report

30

6. Excess Demand and Excess Supply at the same time

0

10

20

30

40

50

60

70

80

90

100

DL

GA

CH

PB

AP

TN

KL

WB

HP

GJ

MZ

UK

KA

MH

CG

HR JK

RJ

TR

MP

OD

AS

UP

BR

JH

Pe

rce

nt

Households having electricity (%) 2017 India Average (2017)

0

10

20

30

40

50

60

70

80

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

Pe

rce

nt

Plant Load Factors

31

• Financial Assistance to States…

• States will take over 75% of the DISCOM debt as on Sept 30, 2015

• 50% in FY 2015-16 and 25% in FY 2016-17

• But conditional on Reforms by Discoms

• Reduce AT&C losses to 15 % by 2019

• Eliminate financial losses by 2019

• Feeder and Distribution Transformer metering by 2017

• Smart metering for Consumers

UDAY-Government Response

32

33

Overview

• History

• Interesting facts

• Jaitley-Prabhu Dilemma

• Subsidies

• Costs

• Way Forward

34

Indian Railways network- 1860 to 1930 to Present

Source: Dave Donaldson, 2010, “Railroads of the Raj: Estimating the Impact of Transportation Infrastructure”

35

Social Engineering by Railways: The Freight Equalization Scheme

• Subsidized long-distance transport of key inputs (iron, steel, fertilizers, cement, and petroleum) to achieve geographical spread of industrialization

• States closer to natural resources (Eastern states) experienced slower growth of manufacturing than distant states (Punjab-- distant from markets and inputs--even had a steel plant!)

(Firth and Liu (2017), forthcoming)

36

Indian Railways Today: Facts

More than 13000 passenger trains and 9000 goods trains run

daily

4th largest rail network in the world (after US,

China and Russia).

3rd largest under single management.

Carried 8.1 billion passengers and 11.1

billion tones of freight in 2015-16.

Employee count- 14 lakh. 8th biggest

employer in the world and largest in India.

37

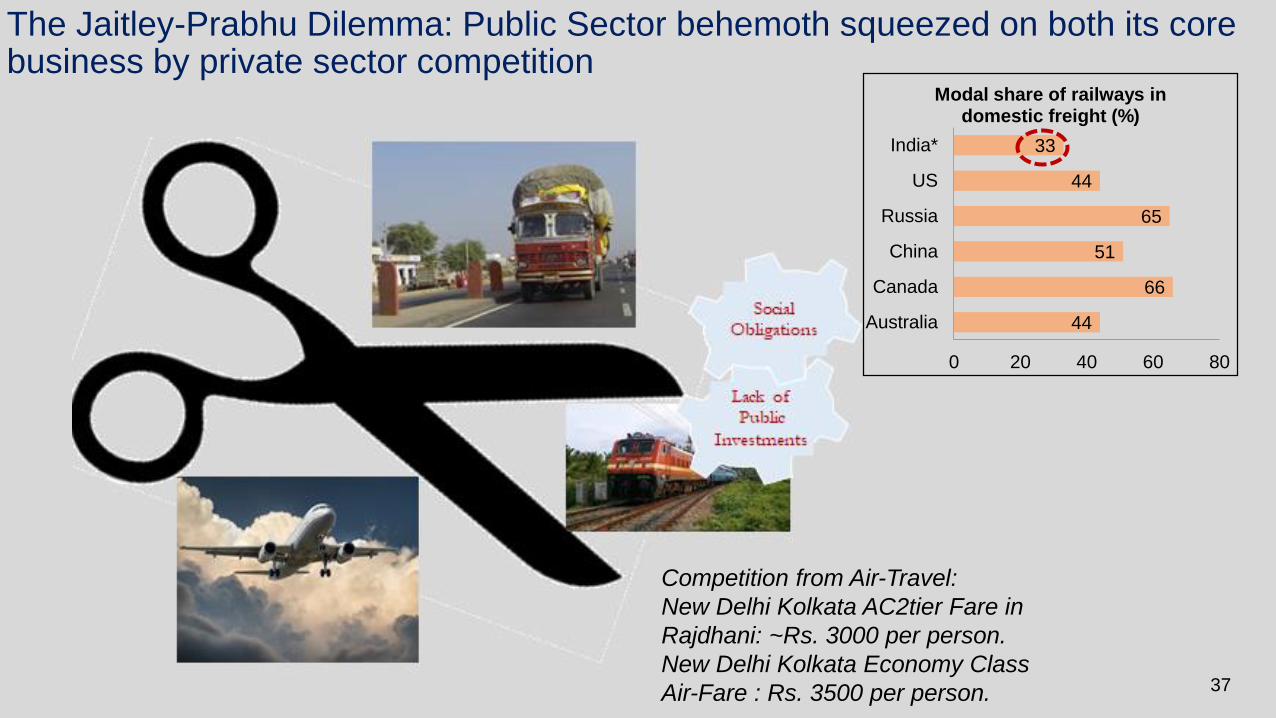

The Jaitley-Prabhu Dilemma: Public Sector behemoth squeezed on both its core business by private sector competition

44

66

51

65

44

33

0 20 40 60 80

Australia

Canada

China

Russia

US

India*

Modal share of railways in domestic freight (%)

Competition from Air-Travel:

New Delhi Kolkata AC2tier Fare in

Rajdhani: ~Rs. 3000 per person.

New Delhi Kolkata Economy Class

Air-Fare : Rs. 3500 per person.

38

Complex Bureaucratic Structure Total 10 Grade A

Services

39

Chronic Under investment in Railways

0

2

4

6

8

10

12

14

16

18

Up to 5thPlan

6th Plan 7th Plan 8th Plan 9th Plan 10th Plan11th Plan12th Plan

Pe

rce

nt o

f To

tal P

lan

Resource Allocation in Transport Sector and Railways

Transport sector as percentage of total plan Railways as percentage of total plan

Share of IR in total

plan outlay only 5.5

per cent vis-à-vis

about 11 per cent

for the other

transport sectors

• Share of IR in overall development expenditure low, at below 2 percent over the past decade.

40

Low Investment leading to lack of Capacity Addition

90

110

130

150

170

190

210

230

250

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

roadindex railindex

‘Railindex’ is an index of running track kilometers over the

period 1991 to 2012 with base 1991. ‘Roadindex’ is an

index of length of roads in kilometers inclusive of national

& state highways, urban & rural roads.

55

65

75

85

95

105

115

125

1990 1995 2000 2005 2010 2012 2013 2014 2015

China

India

Addition to capacity measured by addition of RKM in

000’s.

41

Consequence: High CongestionOn HDN routes over 65% of sections operating at > 100% capacity

42

Shouldering the Social Responsibility: Cross subsidy from freight to passengers

50

100

150

200

250

300

350

400

450

500

19

93

-94

19

94

-95

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

2003-0

4

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

Ind

ex

Consumer Prices and Passenger Rates

Passenger Rate Index CPI(IW)

50

100

150

200

250

300

350

400

450

500

19

93

-94

1994-9

5

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

2002-0

3

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

Ind

ex

Wholesale Prices and Freight Rates

Freight Rate Index WPI

The price indices and those of passenger and freight rates are constructed with 1993-94 as

base.

43

Subsidies (2014-15)

Category Subsidies

(in crore)

All AC Categories 1,115

Sleeper Class Category

(mail and executive class)9,002

44

Costs of Under-Provided Railways Services

• Large opportunity cost as railways has strong linkages. The railways multiplier effect is around 5 or more: a Re. 1 increase in railways investment would increase economy-wide output by about 5 rupees.

• Environmental Damage :

• Rail transport emits 17 gram CO2 equivalent per PKM as compared to 84 gram per PKM in case of road transport.

• Rail transport emits 28 gram CO2 equivalent per NTKM as compared to 64 gram per NTKM in case of road transport. (Source: NTDPC Report 2013).

45

Way Forward• Dedicated Freight Corridors to ease congestion

• Independent Rail regulator to facilitate private

investment, corporatization & reforms viz. tariff

revisions

• Debroy Committee recommendations:

• Accounting reforms

• HR reforms- Rationalisation of the large number of

Railway services to one or two services

• Current Government undertaking many

efficiency-enhancing reforms:

• Merging of Rail Budget to Union Budget will facilitate

multi-modal transport planning

• Steps to ensure passenger safety and capital

investments

46

Recommended Material

• Economic Survey 2015-16, Chapter 11, Powering One India

• Katiyabaaz/Powerless (2013) – Movie on Electricity Supply Situation

in Kanpur City of Uttar Pradesh

• Economic survey 2014-15, Chapter 6, Putting Public Investment on

Track: The Rail Route to Higher Growth

• Bibek Debroy Committee Report on Mobilization of Resources for

Major Railway Projects and Restructuring of Railway Ministry and

Railway Board

• National Transport Development Policy Committee (NTDPC) Report

![Diagnostic Laboratory [Rs. 5.63 million, Apr-2020]](https://static.fdocuments.us/doc/165x107/6182d8b8c457b372562f2d61/diagnostic-laboratory-rs-563-million-apr-2020.jpg)

![Untitled-1 []/media/resources... · 114.3 80 5.63 80 5.63 80 5.63 80 5.63 80 ... by bs&b as part of the safety head assembly ... 812.8 23/8 60.3 31/8 37/8 98.4 43/4 120.7](https://static.fdocuments.us/doc/165x107/5a9ecee77f8b9a8e178be350/untitled-1-mediaresources1143-80-563-80-563-80-563-80-563-80-by.jpg)