PUBLIC HEALTH - MADISON AND DANE COUNTY...supplement the basic financial statements. Such...

58

PUBLIC HEALTH - MADISON AND DANE COUNTY Madison, Wisconsin FINANCIAL STATEMENTS Including Independent Auditors' Report As of and for the Year Ended December 31, 2013

Transcript of PUBLIC HEALTH - MADISON AND DANE COUNTY...supplement the basic financial statements. Such...

PUBLIC HEALTH - MADISON AND DANE COUNTY

Madison, Wisconsin

FINANCIAL STATEMENTS

Including Independent Auditors' Report

As of and for the Year Ended December 31, 2013

PUBLIC HEALTH - MADISON AND DANE COUNTY

TABLE OF CONTENTSAs of and for the Year Ended December 31, 2013

Page(s)

Independent Auditors' Report i - iii

Management's Discussion and Analysis iv - xi

Basic Financial Statements

Government-Wide Financial Statements

Statement of Net Position 1

Statement of Activities 2

Fund Financial Statements

Balance Sheet - Governmental Funds 3

Reconciliation of the Balance Sheet of Governmental Funds to the Statement ofNet Position 4

Statement of Revenues, Expenditures and Changes in Fund Balances -Governmental Funds 5

Reconciliation of the Statement of Revenues, Expenditures and Changes inFund Balances of Governmental Funds to the Statement of Activities 6

Index to Notes to Financial Statements 7

Notes to Financial Statements 8 - 22

Required Supplementary Information

General Fund

Detailed Schedule of Revenues, Expenditures and Changes in Fund Balance -Budget and Actual - General Fund 23

Notes to Required Supplementary Information 24

Single Audit Section

Schedule of Expenditures of Federal and State Awards 25 - 27

Notes to the Schedule of Expenditures of Federal and State Awards 28

Report on Internal Control Over Financial Reporting and on Compliance and OtherMatters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 29 - 30

Report on Compliance for Each Major Federal and Major State Program andReport on Internal Control Over Compliance Required by OMB Circular A-133and the State Single Audit Guidelines 31 - 32

Schedule of Findings and Questioned Costs 33 - 37

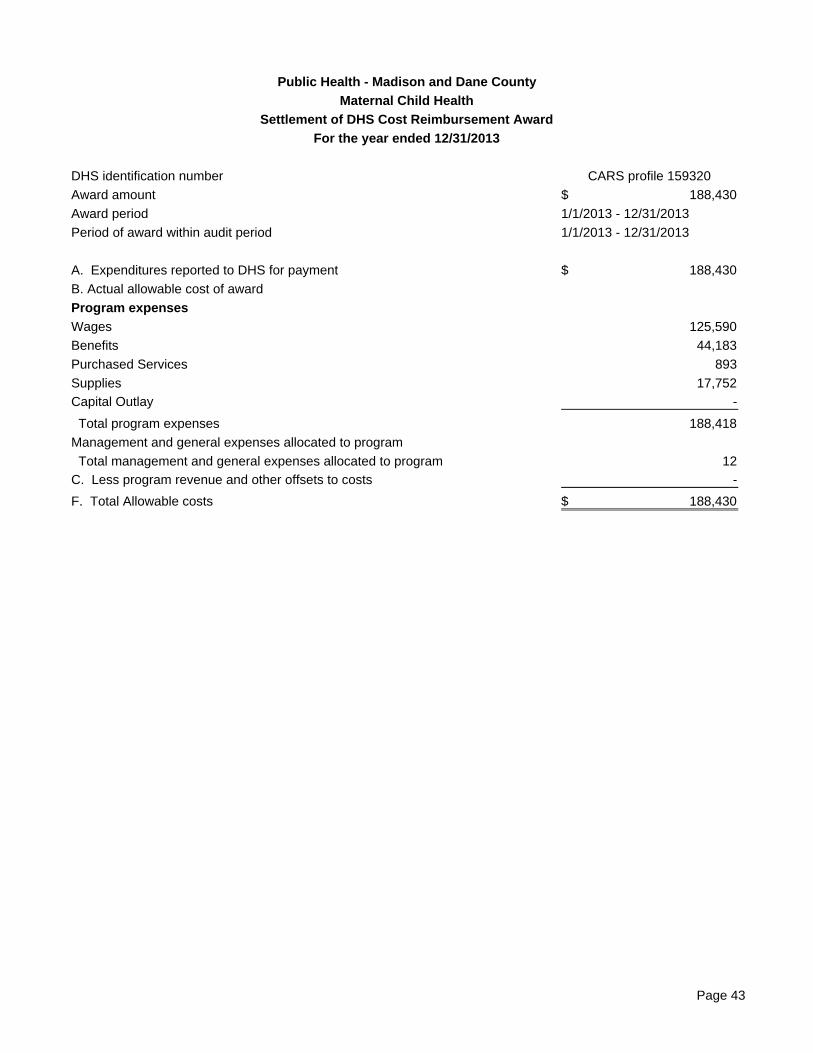

Settlement of DHS Cost Reimbursement Award Schedules 38 - 43

To the Board of Health for Madison and Dane CountyPublic Health - Madison and Dane County

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respectivefinancial position of the governmental activities and major fund of Public Health - Madison and Dane County asof December 31, 2013 and the respective changes in financial position for the year then ended in accordancewith accounting principles generally accepted in the United States of America.

Emphasis of a Matter

As discussed in Note I, the Public Health - Madison and Dane County adopted the provisions of GASBStatement No. 65, Items Previously Reported as Assets and Liabilities, effective January 1, 2013. Our opinionsare not modified with respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’sdiscussion and analysis and budgetary comparison information as listed in the table of contents be presented tosupplement the basic financial statements. Such information, although not a part of the basic financialstatements, is required by the Governmental Accounting Standards Board who considers it to be an essentialpart of financial reporting for placing the basic financial statements in an appropriate operational, economic, orhistorical context. We have applied certain limited procedures to the required supplementary information inaccordance with auditing standards generally accepted in the United States of America, which consisted ofinquiries of management about the methods of preparing the information and comparing the information forconsistency with management’s responses to our inquiries, the basic financial statements, and other knowledgewe obtained during our audit of the basic financial statements. We do not express an opinion or provide anyassurance on the information because the limited procedures do not provide us with sufficient evidence toexpress an opinion or provide any assurance.

Supplementary Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the department’s basic financial statements. The accompanying schedule of expenditures of federaland state awards and settlement of DHS cost reimbursement award schedules as required by the Office ofManagement and Budget Circular A-133, Audits of States, Local Governments and Non-Profit Organizations andthe State Single Audit Guidelines as listed in the table of contents are presented for purposes of additionalanalysis and are not a required part of the basic financial statements. Such information is the responsibility ofmanagement and was derived from and relates directly to the underlying accounting and other records used toprepare the basic financial statements. The information has been subjected to the auditing procedures applied inthe audit of the basic financial statements and certain additional procedures, including comparing and reconcilingsuch information directly to the underlying accounting and other records used to prepare the basic financialstatements or to the basic financial statements themselves, and other additional procedures in accordance withauditing standards generally accepted in the United States of America. In our opinion, the accompanyingschedule of expenditures of federal and state awards and settlement of DHS cost reimbursement awardschedules as required by the Office of Management and Budget Circular A-133, Audits of States, LocalGovernments and Non-Profit Organizaitons and the State Single Audit Guidelines are fairly stated in all materialrespects, in relation to the basic financial statements as a whole.

Page ii

Public Health—Madison and Dane County Management Discussion and Analysis

iv

Public Health—Madison and Dane County

MANAGEMENT DISCUSSION AND ANALYSIS (UNAUDITED) For the year ending December 31, 2013 Public Health‐‐Madison & Dane County (PHMDC) serves almost 500,000 people who live in Madison and Dane County and the 1,200 square miles of urban, suburban, small town and rural environments they live in. The basic mission is to join with partners in the community to promote wellness, prevent disease and help ensure a healthy environment. PHMDC is committed to addressing the root causes of socioeconomic and racial injustices that lead to health inequities. We will accomplish this through:

dissemination of the latest science to increase understanding of health equity and dispel common misconceptions;

increasing capacity and leadership of residents and community organizations;

facilitating institutional, environmental, and policy change to support access to resources and opportunities for all with the end result of improving health status;

strengthening existing social, political, educational, and economic structures. Public Health—Madison and Dane County (PHMDC) is a merged City‐County local health department (WI Statutes 251.02 (1m)) created in January 2008. The governing body is the Board of Health for Madison and Dane County, which has eight members—four appointed by Dane County and four by the City of Madison. The Intergovernmental Agreement (IGA) that created PHMDC made the City of Madison the fiscal agent. Consequently the department uses the city’s accounting and purchasing procedures and follows the city’s processes for their budget and annual audit.

Public Health—Madison and Dane County Management Discussion and Analysis

v ANNUAL OVERVIEW Tobacco Free Columbia‐Dane County Coalition (TFCDC) has been working with property owners and managers in to educate them about the benefits of implementing smoke‐free policies in their rental units. About 72% of Wisconsin renters prefer to live in a smoke‐free environment, whether they smoke or not. Since beginning this effort in 2012, TFCDC has helped implement 15 smoke‐free policies, covering over 2,000 units—this exceeds what the state as a whole, set as a goal. Because of these efforts, about 4,740 Dane County residents will no longer be exposed to secondhand smoke in their home. The number of participants in the Women, Infants and Children (WIC) supplemental nutrition program has been declining for several years—this is part of a national trend. One of the reasons given for the caseload reduction is the increased availability of Supplemental Nutrition Assistance Program (SNAP) benefits which are targeted at low‐income individuals and families. In November 2013 there was a reduction in SNAP benefits and in each month since then there has been a slow increase in the WIC caseload. PHMDC is committed to addressing the root causes of socioeconomic and racial injustices that lead to disparate health outcomes. We are re‐organizing our department to develop and support (via partnership) the creation of an environment where the primary determinate of a resident’s health status is not their zip code, a proxy for socioeconomic status and often a result of long‐standing institutional and structural racism associated with traditional governmental and private sector practices. With all of the other work that is mandated of Public Health, it has been difficult to find the staff resources to move forward. In 2013 the department was able to hire two Health Equity Coordinators to begin to work at the policy and systems level. While PHMDC will be at this work for years to come, this has been an encouraging first step forward. The goals of these positions are to work on developing department capacity and external partners’ capacity to understand the impacts of inequity on health and the social determinants of health. Internally, a health equity training and technical assistance strategy is being developed to create understanding and capacity throughout the agency in understanding the social determinants of health and strategies to intervene upon them. Working with the City’s Department of Civil Rights, PHMDC has taken the lead in incorporating the concept of equity into the way the City does business by establishing the Racial Equity and Social Justice Initiative. Through this initiative, all departments will

Public Health—Madison and Dane County Management Discussion and Analysis

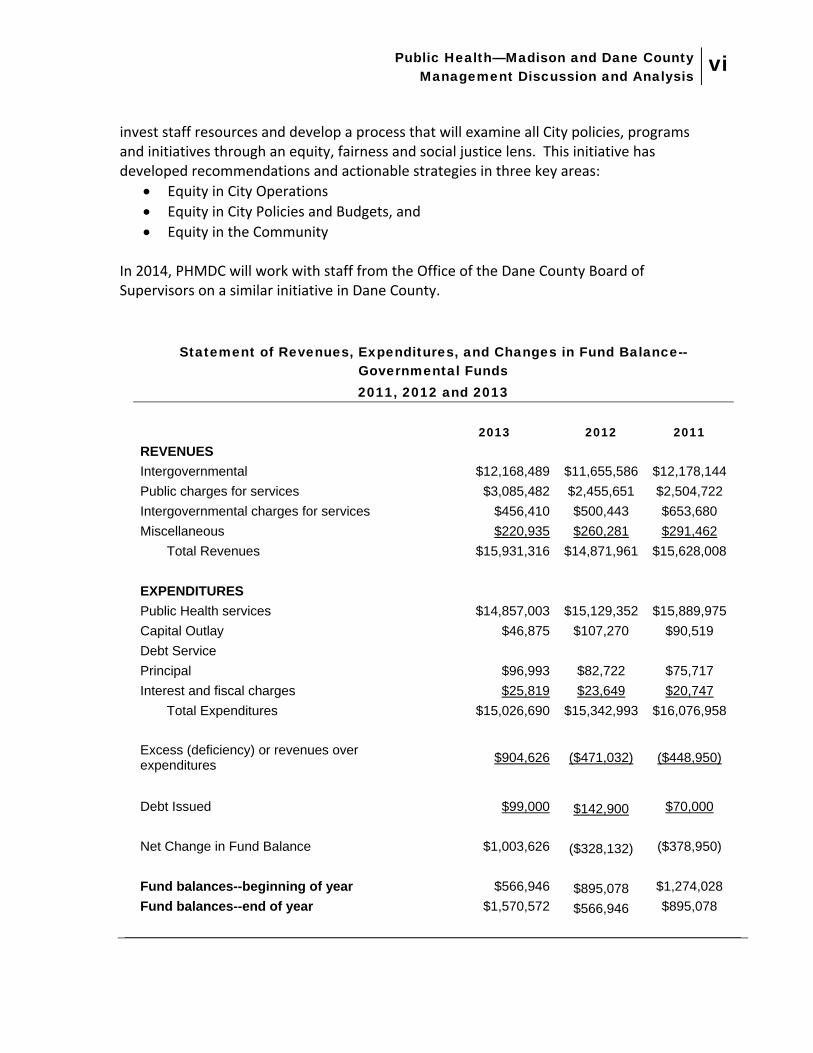

vi invest staff resources and develop a process that will examine all City policies, programs and initiatives through an equity, fairness and social justice lens. This initiative has developed recommendations and actionable strategies in three key areas:

Equity in City Operations

Equity in City Policies and Budgets, and

Equity in the Community In 2014, PHMDC will work with staff from the Office of the Dane County Board of Supervisors on a similar initiative in Dane County.

Statement of Revenues, Expenditures, and Changes in Fund Balance--

Governmental Funds 2011, 2012 and 2013

2013 2012 2011

REVENUES

Intergovernmental $12,168,489 $11,655,586 $12,178,144

Public charges for services $3,085,482 $2,455,651 $2,504,722

Intergovernmental charges for services $456,410 $500,443 $653,680

Miscellaneous $220,935 $260,281 $291,462

Total Revenues $15,931,316 $14,871,961 $15,628,008

EXPENDITURES

Public Health services $14,857,003 $15,129,352 $15,889,975

Capital Outlay $46,875 $107,270 $90,519

Debt Service

Principal $96,993 $82,722 $75,717

Interest and fiscal charges $25,819 $23,649 $20,747

Total Expenditures $15,026,690 $15,342,993 $16,076,958

Excess (deficiency) or revenues over expenditures

$904,626 ($471,032) ($448,950)

Debt Issued $99,000 $142,900 $70,000

Net Change in Fund Balance $1,003,626 ($328,132) ($378,950)

Fund balances--beginning of year $566,946 $895,078 $1,274,028

Fund balances--end of year $1,570,572 $566,946 $895,078

Public Health—Madison and Dane County Management Discussion and Analysis

vii

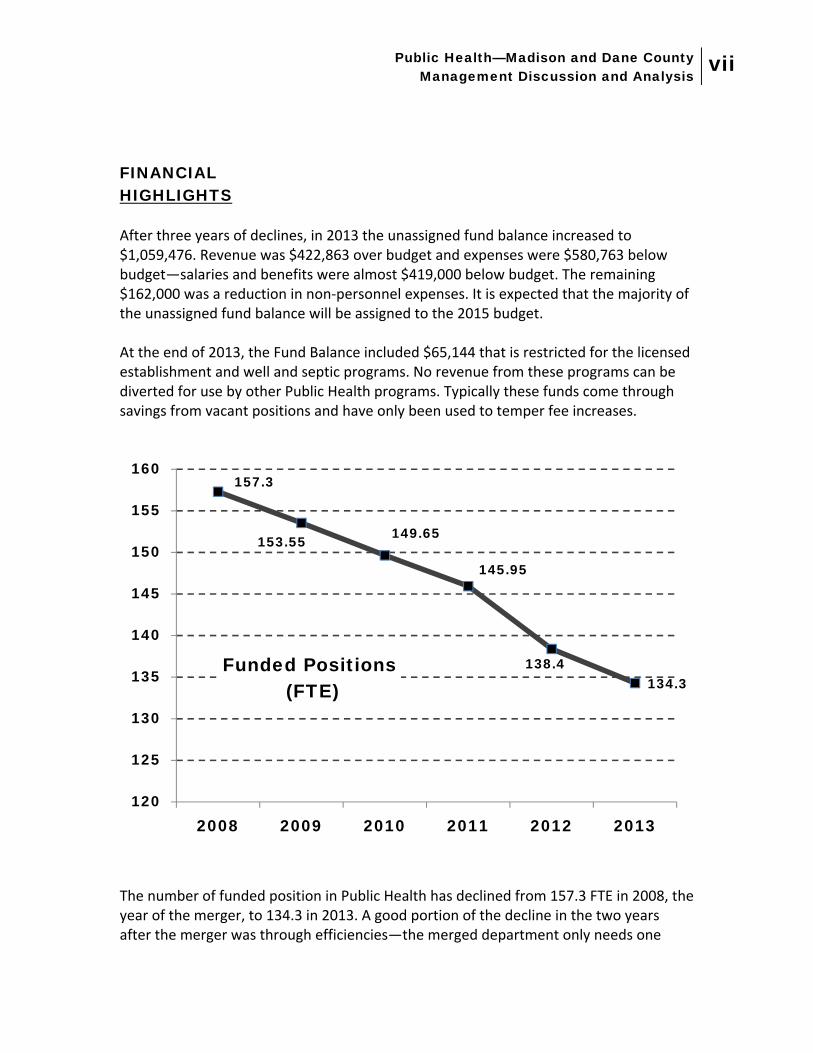

FINANCIAL HIGHLIGHTS After three years of declines, in 2013 the unassigned fund balance increased to $1,059,476. Revenue was $422,863 over budget and expenses were $580,763 below budget—salaries and benefits were almost $419,000 below budget. The remaining $162,000 was a reduction in non‐personnel expenses. It is expected that the majority of the unassigned fund balance will be assigned to the 2015 budget.

At the end of 2013, the Fund Balance included $65,144 that is restricted for the licensed establishment and well and septic programs. No revenue from these programs can be diverted for use by other Public Health programs. Typically these funds come through savings from vacant positions and have only been used to temper fee increases.

The number of funded position in Public Health has declined from 157.3 FTE in 2008, the year of the merger, to 134.3 in 2013. A good portion of the decline in the two years after the merger was through efficiencies—the merged department only needs one

157.3

153.55 149.65

145.95

138.4134.3

120

125

130

135

140

145

150

155

160

2008 2009 2010 2011 2012 2013

Funded Positions(FTE)

Public Health—Madison and Dane County Management Discussion and Analysis

viii Director, one payroll clerk, one management team. The declines since 2010 have been dictated more by the availability of funding. Per capita support of Public Health in Wisconsin from federal sources is among the lowest in the nation (47 out of 50 states); per capita support from state sources is not much higher (46 out of 50 states). Consequently, there is a much greater reliance on local tax levy support for public health than in most other areas of the country. Tax levy support for PHMDC is divided based upon equalized valuation (WI Statutes 251.11)—in 2013 Dane County provided 55.291% and the City of Madison provided the remaining 44.709%. The City of Madison provides additional funding for community agency contracts, which PHMDC monitors. Tax levy support in 2013 was only 5.6 percent higher than it was in 2008, an average increase of only 1.1% per year since the merger in 2008. The liability for compensated absences (unused sick time) has grown in the last five years. At the end of December 2013, the department’s liabilities included $4,607,262 for compensated absences. The growth in the liability for compensated absences is of concern because PHMDC is the oldest department in both the City and County—almost 40% of Public Health staff is 55 years or older. The department has added funds to its operating budget to cover payouts as staff retire.

Public Health—Madison and Dane County Management Discussion and Analysis

ix

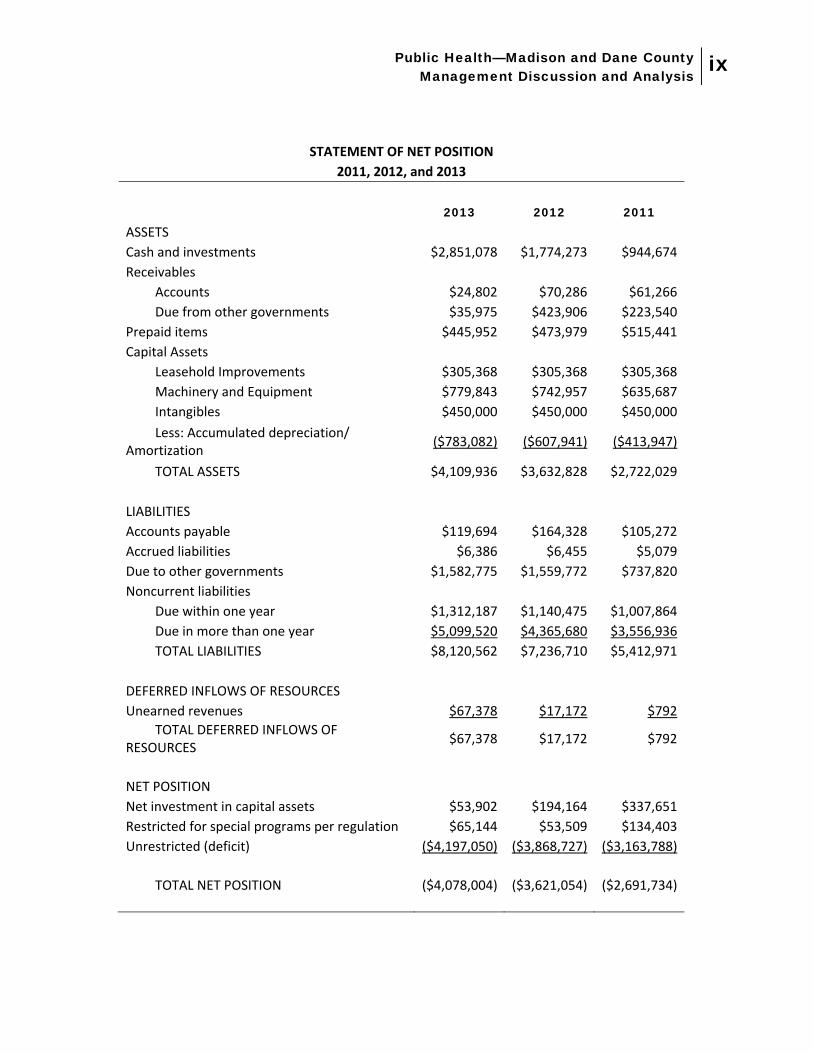

STATEMENT OF NET POSITION

2011, 2012, and 2013

2013 2012 2011 ASSETS

Cash and investments $2,851,078 $1,774,273 $944,674

Receivables

Accounts $24,802 $70,286 $61,266

Due from other governments $35,975 $423,906 $223,540

Prepaid items $445,952 $473,979 $515,441

Capital Assets

Leasehold Improvements $305,368 $305,368 $305,368

Machinery and Equipment $779,843 $742,957 $635,687

Intangibles $450,000 $450,000 $450,000

Less: Accumulated depreciation/ Amortization

($783,082) ($607,941) ($413,947)

TOTAL ASSETS $4,109,936 $3,632,828 $2,722,029

LIABILITIES

Accounts payable $119,694 $164,328 $105,272

Accrued liabilities $6,386 $6,455 $5,079

Due to other governments $1,582,775 $1,559,772 $737,820

Noncurrent liabilities

Due within one year $1,312,187 $1,140,475 $1,007,864

Due in more than one year $5,099,520 $4,365,680 $3,556,936

TOTAL LIABILITIES $8,120,562 $7,236,710 $5,412,971

DEFERRED INFLOWS OF RESOURCES

Unearned revenues $67,378 $17,172 $792

TOTAL DEFERRED INFLOWS OF RESOURCES

$67,378 $17,172 $792

NET POSITION

Net investment in capital assets $53,902 $194,164 $337,651

Restricted for special programs per regulation $65,144 $53,509 $134,403

Unrestricted (deficit) ($4,197,050) ($3,868,727) ($3,163,788)

TOTAL NET POSITION

($4,078,004) ($3,621,054) ($2,691,734)

Public Health—Madison and Dane County Management Discussion and Analysis

x SIGNIFICANT EFFECTS Dane County is the fastest growing county in Wisconsin, with some strong demographic shifts. The fastest growing age group is seniors, a trend that is expected to continue for at least the next two decades. The growth in the Hispanic/Latino, African American, and Asian communities has been dramatic. In the 2000 Census, 89% of county residents were non‐Hispanic whites. In the 2010 census this dropped to 84% and 2018 projections are that this will drop to about 80%. While the number of residents who do not speak English well was only 5% in the 2010 census, this was 50% higher than the 2000 census. People of color are disproportionately represented below the poverty level. These trends are expected to have an impact on the shape of public health services in the coming years. The Affordable Care Act is also reshaping public health services. While it is still too early to predict the full impact, the intent of the Affordable Care Act is to increase the number of people who have medical coverage. The positive news is that more people will be able to secure medical coverage for their families and themselves. The PHMDC program where this seems to be having the greatest impact is immunizations, as clients are able to shift to private providers. But the hard reality is that some people will not qualify for coverage if only because they lack documentation. One of the promising components of the Affordable Care Act is its emphasis on home visitation for at‐risk pregnant women. A primary goal of PHMDC is to improve birth outcomes, and when possible, improve parenting in early childhood. The Department of Children and Families administers most of these funds and made a decision to provide only minimal support for nurse‐based programs such as PHMDC’s Nurse Family Partnership program. PHMDC has a long‐term strategy of working with other counties in the region to create a larger pool to advocate for state support. In the last year, NFP expanded into Adams, Juneau and Sauk Counties. The state is launching a pilot project in Dane and Rock counties to minimally reimburse health plans for births under Medicaid managed care (‘BadgerCare’). This will require the health plans to conduct one or more home visits to high‐risk pregnant women. None of the health plans in Dane County currently provide this type of service and are looking at PHMDC for assistance in these efforts. PHMDC is working with our healthcare partners to develop strategies on how to best coordinate these visits to create the least amount of confusion and the best health outcomes for these women. Local health departments are responsible for providing ten essential services in three priority areas: assessment (assessing, investigating and evidence‐based practice),

Public Health—Madison and Dane County Management Discussion and Analysis

xi assurance (enforcing laws and regulations that protect health and ensure safety, link people to needed personal health services, ensure health care services are available when they are otherwise unavailable, assure a competent public and personal health care workforce, research to reveal new insights and innovate solutions to health problems) and policy development (identify policies and systems that promote good health outcomes; inform, educate, and empower the community; and mobilize community partnerships) Planning began in mid‐2013, but it was with the 2014 adopted operating budget that PHMDC was able to create the Division of Policy, Planning and Evaluation (PPE). The goal of the PPE Division is to build capacity so that we can have a broader impact in these ten essential services. For example, PHMDC is hiring staff with skills in economic, housing, and social policy analysis to work with staff who are content experts in pre‐natal case management, epidemiologists and health educators to paint a robust picture with data, policy and lived experiences of the factors that influence poor (or good) health outcomes and strategies to improve (or maintain) them. PHMDC is confident that these changes will support our ability to make the City of Madison and Dane County a place where all our residents have the same opportunities to achieve good health regardless of their zip code, income, race, ethnicity, gender or sexual orientation. Following this discussion, there are a series of financial statements and notes. It is our fervent hope that these statements will provide further insight into the finances of PHMDC.

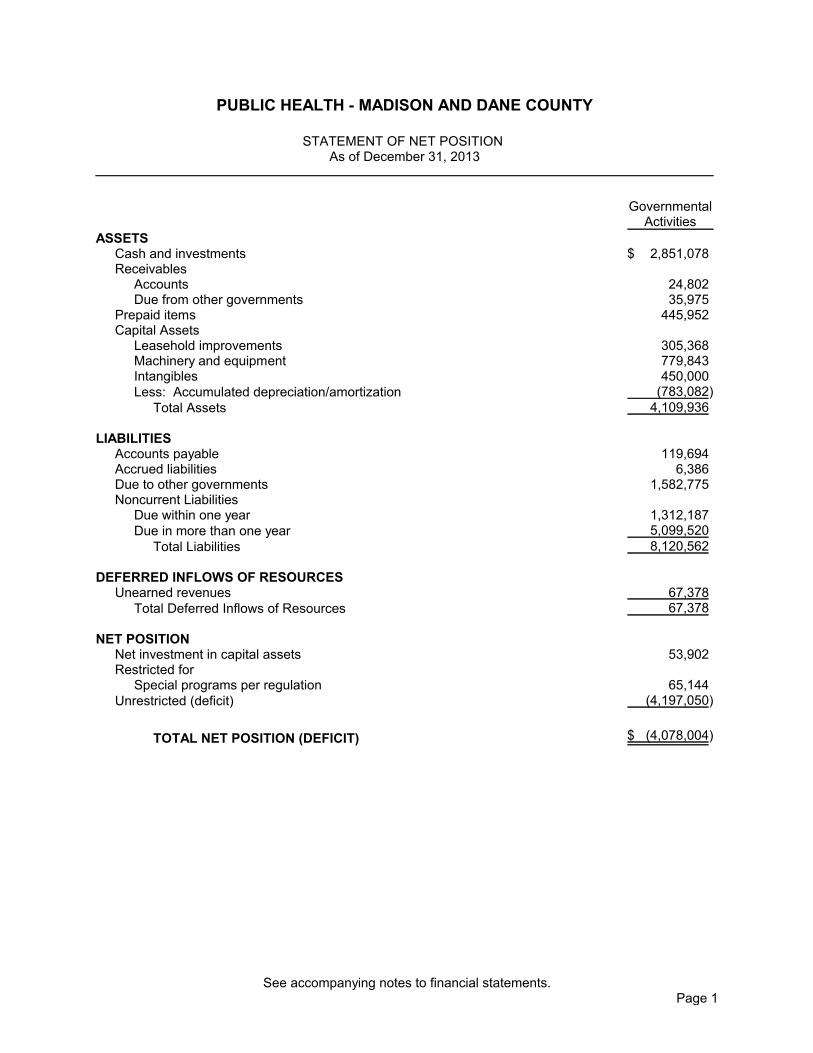

PUBLIC HEALTH - MADISON AND DANE COUNTY

STATEMENT OF NET POSITIONAs of December 31, 2013

GovernmentalActivities

ASSETSCash and investments $ 2,851,078Receivables

Accounts 24,802Due from other governments 35,975

Prepaid items 445,952Capital Assets

Leasehold improvements 305,368Machinery and equipment 779,843Intangibles 450,000Less: Accumulated depreciation/amortization (783,082)

Total Assets 4,109,936

LIABILITIESAccounts payable 119,694Accrued liabilities 6,386Due to other governments 1,582,775Noncurrent Liabilities

Due within one year 1,312,187Due in more than one year 5,099,520

Total Liabilities 8,120,562

DEFERRED INFLOWS OF RESOURCESUnearned revenues 67,378

Total Deferred Inflows of Resources 67,378

NET POSITIONNet investment in capital assets 53,902Restricted for

Special programs per regulation 65,144Unrestricted (deficit) (4,197,050)

TOTAL NET POSITION (DEFICIT) $ (4,078,004)

See accompanying notes to financial statements.Page 1

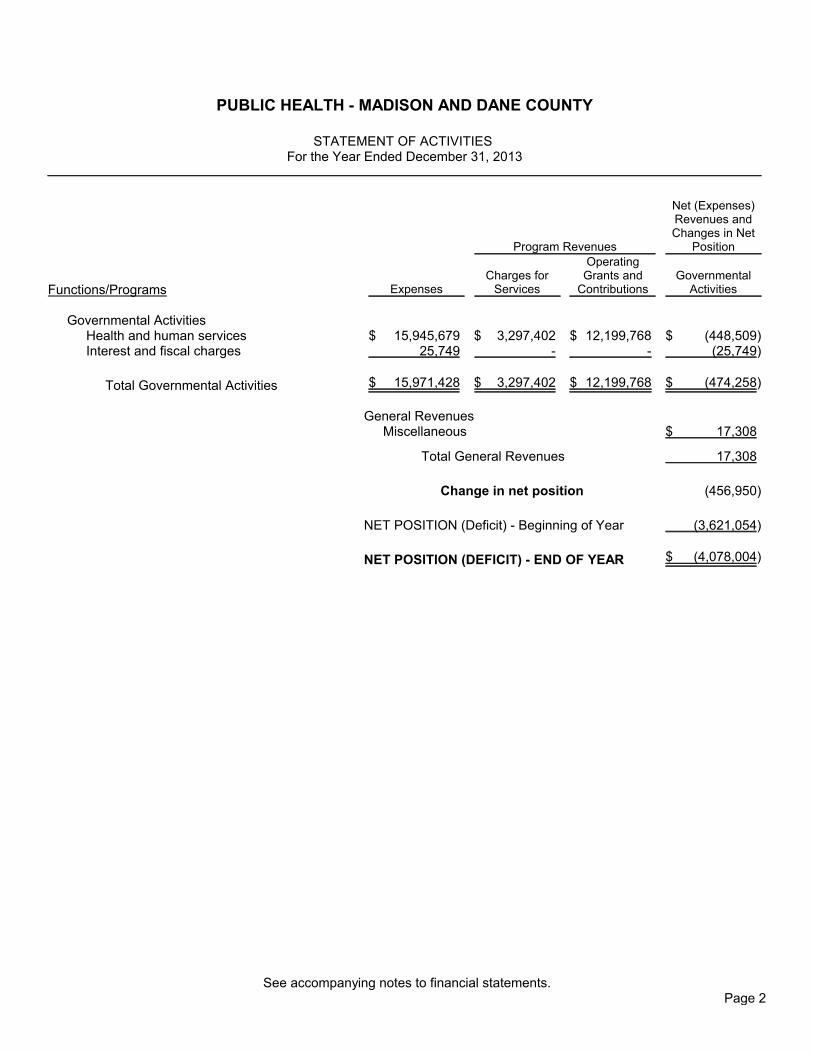

PUBLIC HEALTH - MADISON AND DANE COUNTY

STATEMENT OF ACTIVITIESFor the Year Ended December 31, 2013

Program Revenues

Net (Expenses)Revenues andChanges in Net

Position

Functions/Programs ExpensesCharges for

Services

OperatingGrants and

ContributionsGovernmental

Activities

Governmental ActivitiesHealth and human services $ 15,945,679 $ 3,297,402 $ 12,199,768 $ (448,509)Interest and fiscal charges 25,749 - - (25,749)

Total Governmental Activities $ 15,971,428 $ 3,297,402 $ 12,199,768 $ (474,258)

General RevenuesMiscellaneous $ 17,308

Total General Revenues 17,308

Change in net position (456,950)

NET POSITION (Deficit) - Beginning of Year (3,621,054)

NET POSITION (DEFICIT) - END OF YEAR $ (4,078,004)

See accompanying notes to financial statements.Page 2

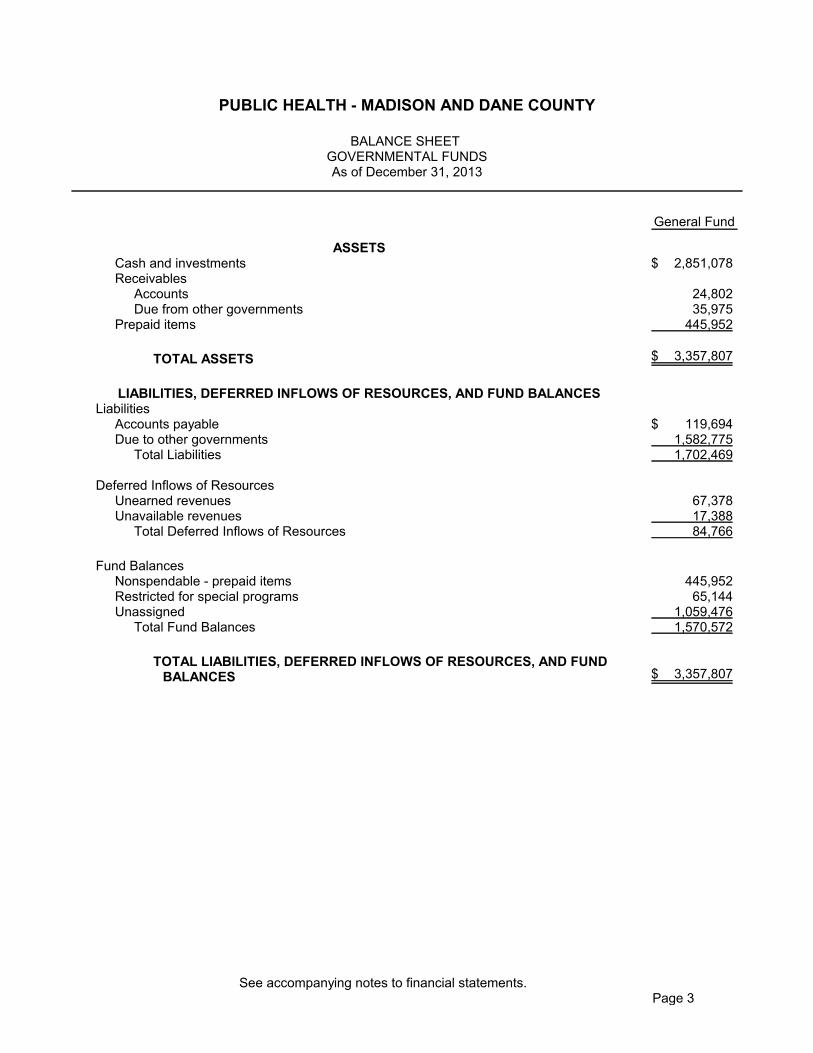

PUBLIC HEALTH - MADISON AND DANE COUNTY

BALANCE SHEETGOVERNMENTAL FUNDSAs of December 31, 2013

General Fund

ASSETSCash and investments $ 2,851,078Receivables

Accounts 24,802Due from other governments 35,975

Prepaid items 445,952

TOTAL ASSETS $ 3,357,807

LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND FUND BALANCESLiabilities

Accounts payable $ 119,694Due to other governments 1,582,775

Total Liabilities 1,702,469

Deferred Inflows of ResourcesUnearned revenues 67,378Unavailable revenues 17,388

Total Deferred Inflows of Resources 84,766

Fund BalancesNonspendable - prepaid items 445,952Restricted for special programs 65,144Unassigned 1,059,476

Total Fund Balances 1,570,572

TOTAL LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND FUNDBALANCES $ 3,357,807

See accompanying notes to financial statements.Page 3

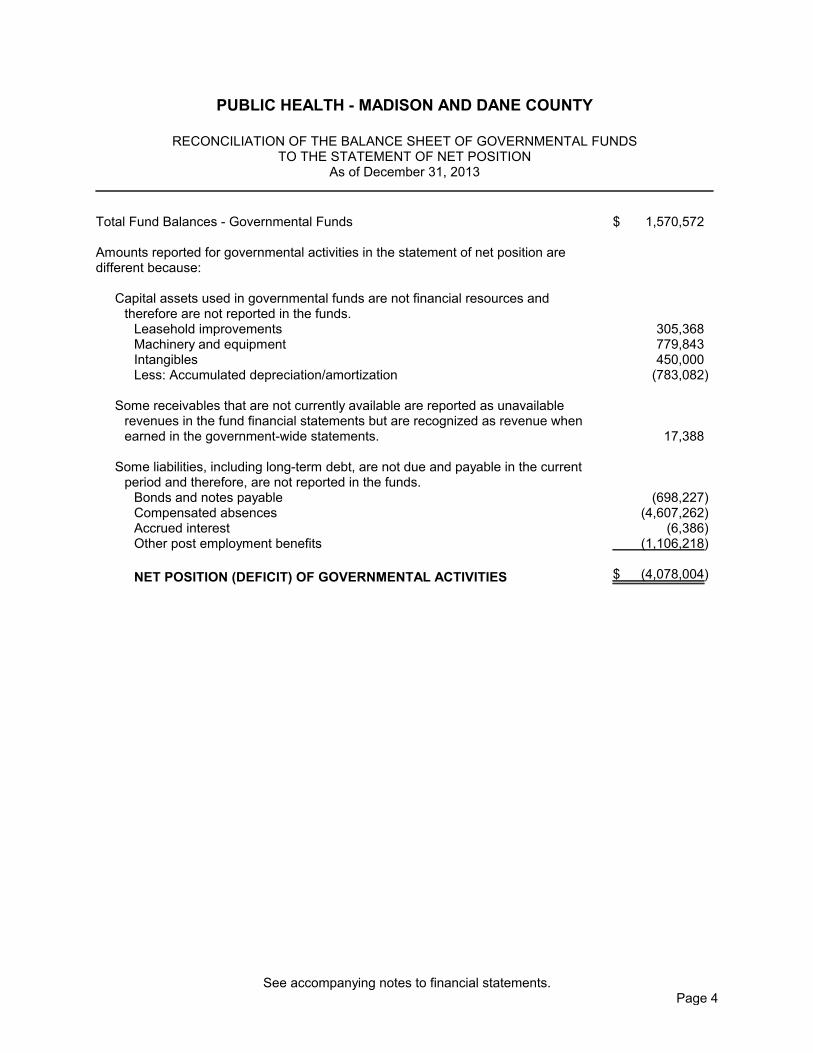

PUBLIC HEALTH - MADISON AND DANE COUNTY

RECONCILIATION OF THE BALANCE SHEET OF GOVERNMENTAL FUNDSTO THE STATEMENT OF NET POSITION

As of December 31, 2013

Total Fund Balances - Governmental Funds $ 1,570,572

Amounts reported for governmental activities in the statement of net position aredifferent because:

Capital assets used in governmental funds are not financial resources andtherefore are not reported in the funds.

Leasehold improvements 305,368Machinery and equipment 779,843Intangibles 450,000Less: Accumulated depreciation/amortization (783,082)

Some receivables that are not currently available are reported as unavailablerevenues in the fund financial statements but are recognized as revenue whenearned in the government-wide statements. 17,388

Some liabilities, including long-term debt, are not due and payable in the currentperiod and therefore, are not reported in the funds.

Bonds and notes payable (698,227)Compensated absences (4,607,262)Accrued interest (6,386)Other post employment benefits (1,106,218)

NET POSITION (DEFICIT) OF GOVERNMENTAL ACTIVITIES $ (4,078,004)

See accompanying notes to financial statements.Page 4

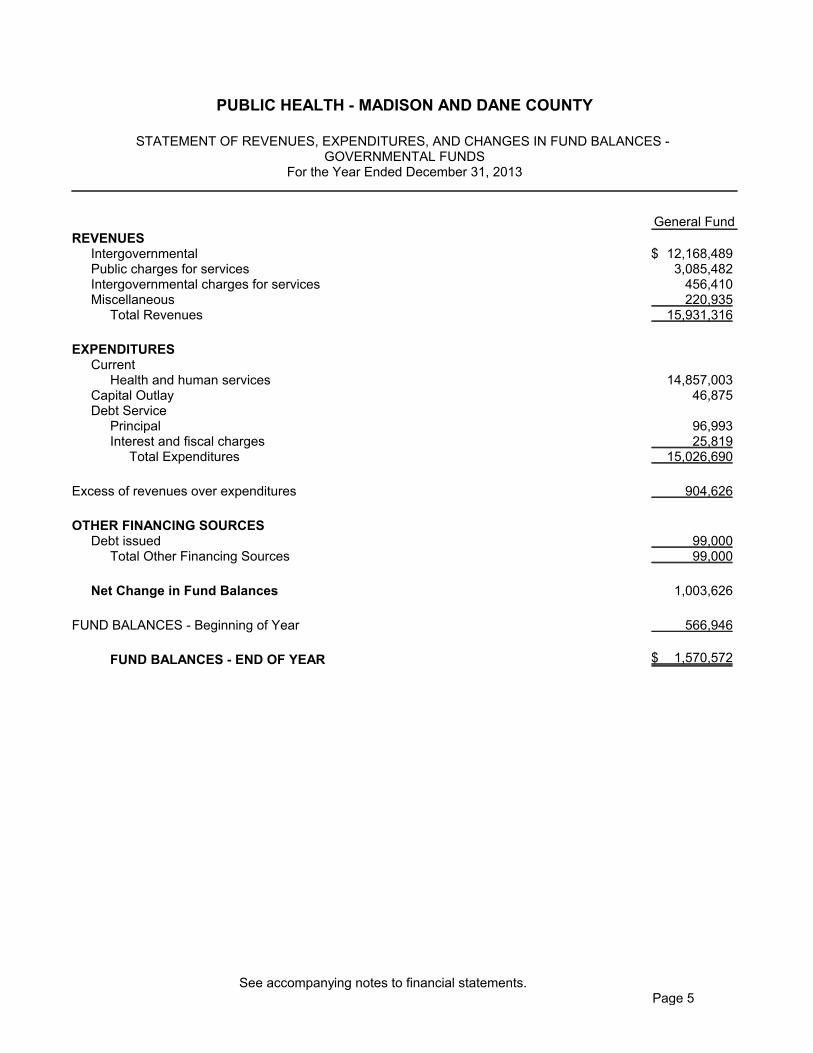

PUBLIC HEALTH - MADISON AND DANE COUNTY

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES -GOVERNMENTAL FUNDS

For the Year Ended December 31, 2013

General Fund

REVENUESIntergovernmental $ 12,168,489Public charges for services 3,085,482Intergovernmental charges for services 456,410Miscellaneous 220,935

Total Revenues 15,931,316

EXPENDITURESCurrent

Health and human services 14,857,003Capital Outlay 46,875Debt Service

Principal 96,993Interest and fiscal charges 25,819

Total Expenditures 15,026,690

Excess of revenues over expenditures 904,626

OTHER FINANCING SOURCESDebt issued 99,000

Total Other Financing Sources 99,000

Net Change in Fund Balances 1,003,626

FUND BALANCES - Beginning of Year 566,946

FUND BALANCES - END OF YEAR $ 1,570,572

See accompanying notes to financial statements.Page 5

PUBLIC HEALTH - MADISON AND DANE COUNTY

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS

TO THE STATEMENT OF ACTIVITIESFor the Year Ended December 31, 2013

Net change in fund balances - total governmental funds $ 1,003,626 Amounts reported for governmental activities in the statement of net position are differentbecause:

Governmental funds report capital outlays as expenditures. However, in the statement ofnet position the cost of these assets is capitalized and they are depreciated over theirestimated useful lives and reported as depreciation expense in the statement of activities.

Capital outlay is reported as an expenditure in the fund financial statements but iscapitalized in the government-wide financial statements 46,875

Depreciation is reported in the government-wide financial statements (178,137)Net book value of assets retired (6,993)

Receivables not currently available are reported as revenue when collected or currentlyavailable in the fund financial statements but are recognized as revenue when earned inthe government-wide financial statements. (416,838)

Debt issued provides current financial resources to governmental funds, but issuing debtincreases long-term liabilities in the statement of net position. Repayment of debt principalis an expenditure in the governmental funds, but the repayment reduces long-termliabilities in the statement of net position.

Debt issued (99,000)Principal repaid 96,993

Some expenses in the statement of activities do not require the use of current financialresources and, therefore, are not reported as expenditures in the governmental funds.

Compensated absences (605,431)Other postemployment benefits (298,115)Accrued interest on debt 70

CHANGE IN NET POSITION OF GOVERNMENTAL ACTIVITIES $ (456,950)

See accompanying notes to financial statements.Page 6

PUBLIC HEALTH - MADISON AND DANE COUNTY

INDEX TO NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE Page

I Summary of Significant Accounting Policies 8A. Reporting Entity 8B. Government-Wide and Fund Financial Statements 8C. Measurement Focus, Basis of Accounting, and Financial Statement

Presentation 9D. Assets, Liabilities, Deferred Inflows of Resources, and Net Position or Equity 10

1. Deposits and Investments 102. Prepaid Items 123. Capital Assets 124. Compensated Absences 135. Long-Term Obligations 136. Deferred Inflows of Resources7. Equity Classifications 13

II Detailed Notes on All Funds 15A. Deposits and Investments 15B. Receivables 16C. Capital Assets 17D. Long-Term Obligations 17E. Lease Disclosures 19F. Net Position/Fund Balances 19

III Other Information 20A. Employees' Retirement System 20B. Risk Management 21C. Commitments and Contingencies 21D. Other Postemployment Benefits 21E. Effect of New Accounting Standards on Current-Period Financial Statements 22

Page 7

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting policies of the Public Health - Madison and Dane County, Wisconsin conform toaccounting principles generally accepted in the United States of America as applicable to governmentalunits. The accepted standard-setting body for establishing governmental accounting and financialreporting principles is the Governmental Accounting Standards Board (GASB).

A. REPORTING ENTITY

The Board of Health of Madison & Dane County governs Public Health - Madison & Dane County,provides supervision to the Director, and assures the enforcement of state and local public health lawsand regulations. Subject to approval of the Madison City Council and the Dane County Board ofSupervisors, it may adopt rules necessary to protect and improve public health, determine servicepriorities and assign funding levels to those priorities, and enter into contracts for the provision of publichealth services.

B. GOVERNMENT-WIDE AND FUND FINANCIAL STATEMENTS

In March 2012, the GASB issued statement No. 65 - Items Previously Reported as Assets and Liabilities.This statement establishes accounting and financial reporting standards that reclassify, as deferredoutflows of resources or deferred inflows of resources, certain items that were previously reported asassets and liabilities and recognizes, as outflows of resources or inflows of resources, certain items thatwere previously reported as assets and liabilities. This standard was effective January 1, 2013.

Government-Wide Financial Statements

The statement of net position and statement of activities display information about the reportinggovernment as a whole. They include all funds of the reporting entity. Governmental activities generallyare financed through taxes, intergovernmental revenues, and other nonexchange revenues.

The statement of activities demonstrates the degree to which the direct expenses of a given function orsegment are offset by program revenues. Direct expenses are those that are clearly identifiable with aspecific function or segment. The department does not allocate indirect expenses to functions in thestatement of activities. Program revenues include 1) charges to customers or applicants who purchase,use or directly benefit from goods, services, or privileges provided by a given function or segment, and 2)grants and contributions that are restricted to meeting the operational or capital requirements of aparticular function or segment. Taxes and other items not included among program revenues are reportedas general revenues. Internally dedicated resources are reported as general revenues rather than asprogram revenues.

Fund Financial Statements

Financial statements of the reporting entity are organized into funds, each of which is considered to be aseparate accounting entity. Each fund is accounted for by providing a separate set of self-balancingaccounts, which constitute its assets, deferred outflows of resources, liabilities, deferred inflows ofresources, net position/fund equity, revenues, and expenditures/expenses.

Page 8

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

B. GOVERNMENT-WIDE AND FUND FINANCIAL STATEMENTS (cont.)

Fund Financial Statements (cont.)

The department reports the following major governmental fund:

General Fund - accounts for the department's operating activities.

C. MEASUREMENT FOCUS, BASIS OF ACCOUNTING, AND FINANCIAL STATEMENT PRESENTATION

Government-Wide Financial Statements

The government-wide statement of net position and statement of activities are reported using theeconomic resources measurement focus and the accrual basis of accounting. Under the accrual basis ofaccounting, revenues are recognized when earned and expenses are recorded when the liability isincurred or economic asset used. Revenues, expenses, gains, losses, assets, and liabilities resulting fromexchange and exchange-like transactions are recognized when the exchange takes place. Grants andsimilar items are recognized as revenue as soon as all eligibility requirements imposed by the provider aremet.

Fund Financial Statements

Governmental fund financial statements are reported using the current financial resources measurementfocus and the modified accrual basis of accounting. Revenues are recorded when they are bothmeasurable and available. Available means collectible within the current period or soon enough thereafterto be used to pay liabilities of the current period. For this purpose, the department considers revenues tobe available if they are collected within 60 days of the end of the current fiscal period. Expenditures arerecorded when the related fund liability is incurred, except for unmatured interest on long-term debt,claims, judgments, compensated absences, and pension expenditures, which are recorded as a fundliability when expected to be paid with expendable available financial resources.

Intergovernmental aids and grants are recognized as revenues in the period the department is entitled theresources and the amounts are available. Amounts owed to the department which are not available arerecorded as receivables and unavailable revenues. Amounts received before eligibility requirements(excluding time) are met are recorded as liabilities. Amounts received in advance of meeting timerequirements are recorded as deferred inflows.

Revenues susceptible to accrual include public charges for services and interest. Other general revenuessuch as fines and forfeitures, inspection fees, and miscellaneous revenues are recognized when receivedin cash or when measurable and available under the criteria described above.

Page 9

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

C. MEASUREMENT FOCUS, BASIS OF ACCOUNTING, AND FINANCIAL STATEMENT PRESENTATION (cont.)

All Financial Statements

The preparation of financial statements in conformity with generally accepted accounting principlesrequires management to make estimates and assumptions that affect the reported amounts of assets andliabilities and disclosure of contingent assets and liabilities at the date of the financial statements and thereported amounts of revenues and expenditures/expenses during the reporting period. Actual resultscould differ from those estimates.

D. ASSETS, LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND NET POSITION OR EQUITY

1. Deposits and Investments

Investment of department funds is restricted by Wisconsin state statutes. Available investments arelimited to:

a. Time deposits in any credit union, bank, savings bank or trust company maturing in three years orless.

b. Bonds or securities of any county, city, drainage district, technical college district, village, town, orschool district of the state. Also, bonds issued by a local exposition district, a local professionalbaseball park district, a local professional football stadium district, a local cultural arts district, theUniversity of Wisconsin Hospitals and Clinics Authority, or the Wisconsin Aerospace Authority.

c. Bonds or securities issued or guaranteed by the federal government.

d. The local government investment pool.

e. Any security maturing in seven years or less and having the highest or second highest ratingcategory of a nationally recognized rating agency.

f. Securities of an open-end management investment company or investment trust, subject tovarious conditions and investment options.

g. Repurchase agreements with public depositories, with certain conditions.

The City of Madison has adopted an investment policy. That policy contains the following guidelines forallowable investments: obligations of the U.S. Government; obligations of U.S. Government agencies;time deposits (defined as savings accounts or certificates of deposits); and repurchase agreements with apublic depository, if the agreement is secured by bonds or securities issued or guaranteed as to principaland interest by the U.S. Government.

Page 10

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

D. ASSETS, LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND NET POSITION OR EQUITY (cont.)

1. Deposits and Investments (cont.)

Interest Rate Risk

The city will minimize interest rate risk, which is the risk that the market value of securities in the portfoliowill fall due to the changes in merit interest rates by:

Structuring the investment portfolio so that the securities mature to meet cash requirements for

ongoing operations, thereby avoiding the need to sell securities on the open market prior to

maturity.

Investing operating funds primarily in short-term securities, money market mutual funds, or

similar investment pools and limiting the average maturity of the portfolio in accordance with this

policy.

Credit Risk

The city will minimize credit risk which is the risk of loss due to the failure o the security issuer to backerby:

Limiting investments to the types of securities listed elsewhere in this Investment Policy.

Pre-qualifying the financial institutions, broker/dealers, intermediaries, and advisors with which

the City of Madison will do business in accordance with Section V.

Diversifying the investment portfolio so that the impact of potential losses from any one type of

security or from any one individual issuer will be minimized.

Concentration of Credit Risk

The policy also states that the city shall not invest more than 25% of the funds in certificates of depositswith any one financial institution.

Custodial Credit Risk

The city's investment policy states that funds in excess of insured or guaranteed limits be secured bysome form of collateral. The fair market value of all collateral pledged will not be less than 110% of theamount of public funds to be secured at each institution.

Page 11

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

D. ASSETS, LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND NET POSITION OR EQUITY (cont.)

1. Deposits and Investments (cont.)

Investments are stated at fair value, which is the amount at which an investment could be exchanged in acurrent transaction between willing parties. Fair values are based on quoted market prices. Noinvestments are reported at amortized cost. Adjustments necessary to record investments at fair value arerecorded in the operating statement as increases or decreases in investment income. The differencebetween the bank statement balance and carrying value is due to outstanding checks and/or deposits intransit.

See Note II. A. for further information.

2. Prepaid Items

Certain payments to vendors reflect costs applicable to future accounting periods and are recorded asprepaid items in both government-wide and fund financial statements.

3. Capital Assets

Government-Wide Statements

Capital assets, which include property, plant and equipment, are reported in the government-wide financialstatements. Capital assets are defined by the government as assets with an initial cost of more than$5,000 for general capital assets and an estimated useful life in excess of one year. All capital assets arevalued at historical cost, or estimated historical cost if actual amounts are unavailable. Donated capitalassets are recorded at their estimated fair value at the date of donation.

Depreciation and amortization of all exhaustible capital assets is recorded as an allocated expense in thestatement of activities, with accumulated depreciation and amortization reflected in the statement of netposition. Depreciation and amortization is provided over the assets' estimated useful lives using thestraight-line method. The range of estimated useful lives by type of asset is as follows:

Leasehold improvements 20 YearsMachinery and Equipment 10 YearsIntangibles 5 Years

Fund Financial Statements

In the fund financial statements, capital assets used in governmental fund operations are accounted for ascapital outlay expenditures of the governmental fund upon acquisition.

Page 12

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

D. ASSETS, LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND NET POSITION OR EQUITY (cont.)

4. Compensated Absences

Under terms of employment, employees are granted sick leave and vacations in varying amounts. Onlybenefits considered to be vested are disclosed in these statements. Vested vacation pay and comp timeare also recorded as a liability.

All vested vacation and sick leave pay is accrued when incurred in the government-wide financialstatements. A liability for these amounts is reported in governmental funds only if they have matured, forexample, as a result of employee resignations and retirements, and are payable with expendable availableresources.

Payments for vacation and sick leave will be made at rates in effect when the benefits are used.Accumulated vacation and sick leave liabilities at December 31, 2013, are determined on the basis ofcurrent salary rates and include salary related payments.

5. Long-Term Obligations

All long-term obligations to be repaid from governmental resources are reported as liabilities in thegovernment-wide statements. The long-term obligations consist primarily of notes payable, accruedcompensated absences, and other post employment benefits.

Long-term obligations for governmental funds are not reported as liabilities in the fund financialstatements. The face value of debts (plus any premiums) are reported as other financing sources andpayments of principal and interest are reported as expenditures.

6. Deferred Inflows of Resources

A deferred inflow of resources represents an acquisition of net position that applies to a future period andtherefore will not be recognized as an inflow of resources (revenue) until that future time.

7. Equity Classifications

Government-Wide Statements

Equity is classified as net position and displayed in three components:

a. Net investment in capital assets - Consists of capital assets including restricted capital assets,net of accumulated depreciation and reduced by the outstanding balances (excluding unspentdebt proceeds) of any bonds, mortgages, notes, or other borrowings that are attributable to theacquisition, construction, or improvement of those assets.

b. Restricted net position - Consists of net position with constraints placed on their use either by 1)external groups such as creditors, grantors, contributors, or laws or regulations of other

Page 13

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

D. ASSETS, LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND NET POSITION OR EQUITY (cont.)

7. Equity Classifications (cont.)

Government-Wide Statements (cont.)governments or, 2) law through constitutional provisions or enabling legislation.

c. Unrestricted net position - All other net positions that do not meet the definitions of "restricted" or"net investment in capital assets."

When both restricted and unrestricted resources are available for use, it is the department's policy to userestricted resources first, then unrestricted resources as they are needed.

Fund Statements

Governmental fund equity is classified as fund balance and displayed as follows:

a. Nonspendable - Includes fund balance amounts that cannot be spent either because they arenot in spendable form or because legal or contractual requirements require them to bemaintained intact.

b. Restricted - Consists of fund balances with constraints placed on their use either by 1) externalgroups such as creditors, grantors, contributors, or laws or regulations of other governments or2) law through constitutional provisions or enabling legislation.

c. Committed - Includes fund balance amounts that are constrained for specific purposes that areinternally imposed by the government through formal action of the highest level of decisionmaking authority. Fund balance amounts are committed through a formal action (resolution) ofthe department. This formal action must occur prior to the end of the reporting period, but theamount of the commitment, which will be subject to the constraints, may be determined in thesubsequent period. Any changes to the constraints imposed require the same formal action ofthe department that originally created the commitment.

d. Assigned - Includes spendable fund balance amounts that are intended to be used for specificpurposes that are not considered restricted or committed. Fund balance may be assignedthrough the following; 1) The department has not adopted specific financial policies regardingassigned fund balances, however, financial managers have authority to assign fund balances forspecific purposes. 2) All remaining positive spendable amounts in governmental funds, otherthan the general fund, that are neither restricted nor committed. Assignments may take placeafter the end of the reporting period.

e. Unassigned - Includes residual positive fund balance within the general fund which has not beenclassified within the other above mentioned categories. Unassigned fund balance may alsoinclude negative balances for any governmental fund if expenditures exceed amounts restricted,committed, or assigned for those purposes.

Page 14

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE I - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

D. ASSETS, LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND NET POSITION OR EQUITY (cont.)

7. Equity Classifications (cont.)

Fund Statements (cont.)

The department considers restricted amounts to be spent first when both restricted and unrestricted fundbalance is available unless there are legal documents/contracts that prohibit doing this, such as in grantagreements requiring dollar for dollar spending. Additionally, the department would first use committed,then assigned and lastly unassigned amounts of unrestricted fund balance when expenditures are made.

See Note II. F. for further information.

NOTE II - DETAILED NOTES ON ALL FUNDS

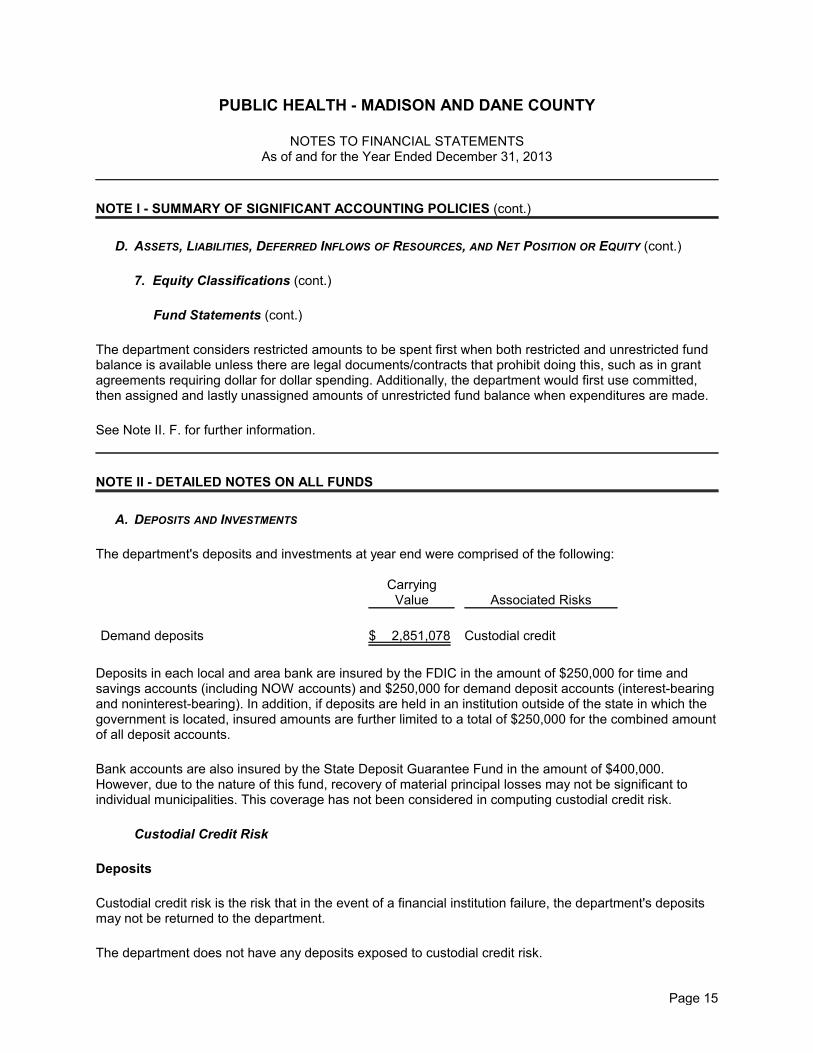

A. DEPOSITS AND INVESTMENTS

The department's deposits and investments at year end were comprised of the following:

CarryingValue Associated Risks

Demand deposits $ 2,851,078 Custodial credit

Deposits in each local and area bank are insured by the FDIC in the amount of $250,000 for time andsavings accounts (including NOW accounts) and $250,000 for demand deposit accounts (interest-bearingand noninterest-bearing). In addition, if deposits are held in an institution outside of the state in which thegovernment is located, insured amounts are further limited to a total of $250,000 for the combined amountof all deposit accounts.

Bank accounts are also insured by the State Deposit Guarantee Fund in the amount of $400,000.However, due to the nature of this fund, recovery of material principal losses may not be significant toindividual municipalities. This coverage has not been considered in computing custodial credit risk.

Custodial Credit Risk

Deposits

Custodial credit risk is the risk that in the event of a financial institution failure, the department's depositsmay not be returned to the department.

The department does not have any deposits exposed to custodial credit risk.

Page 15

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE II - DETAILED NOTES ON ALL FUNDS (cont.)

A. DEPOSITS AND INVESTMENTS (cont.)

See Note I.D.1. for further information on deposit and investment policies.

B. RECEIVABLES

All of the receivables on the balance sheet are expected to be collected within one year.

Governmental funds report unavailable or unearned revenue in connection with receivables for revenuesthat are not considered to be available to liquidate liabilities of the current period. Property taxes levied forthe subsequent year are not earned and cannot be used to liquidate liabilities of the current period.Governmental funds also defer revenue recognition in connection with resources that have been received,but not yet earned. At the end of the current fiscal year, the various components of unavailable revenueand unearned revenue reported in the governmental funds were as follows:

Unearned Unavailable

Grant drawdowns prior to meeting all eligibilityrequirements $ 67,378 $ -

Unavailable intergovernmental payments thatwere received after the availability period - 17,388

Total Unearned/Unavailable Revenue forGovernmental Funds $ 67,378 $ 17,388

Page 16

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE II - DETAILED NOTES ON ALL FUNDS (cont.)

C. CAPITAL ASSETS

Capital asset activity for the year ended December 31, 2013, was as follows:

BeginningBalance Additions Deletions

EndingBalance

Governmental ActivitiesCapital assets being

depreciated/amortizedLeasehold improvements $ 305,368 $ - $ - $ 305,368Machinery and equipment 742,957 46,875 9,989 779,843Intangibles 450,000 - - 450,000

Total Capital Assets BeingDepreciated/Amortized 1,498,325 46,875 9,989 1,535,211

Less: Accumulateddepreciation/amortization forLeasehold improvements (102,052) (20,592) - (122,644)Machinery and equipment (370,889) (67,545) 2,996 (435,438)Intangibles (135,000) (90,000) - (225,000)

Total AccumulatedDepreciation/Amortization (607,941) (178,137) 2,996 (783,082)

Total GovernmentalActivities Capital Assets,Net of AccumulatedDepreciation/Amortization $ 890,384 $ (131,262) $ 6,993 $ 752,129

D. LONG-TERM OBLIGATIONS

Long-term obligations activity for the year ended December 31, 2013, was as follows:

BeginningBalance Increases Decreases

EndingBalance

Amounts DueWithin One

Year

Governmental ActivitiesBonds and Notes Payable

Other long-term liabilities $ 696,220 $ 99,000 $ 96,993 $ 698,227 $ 106,882

Other LiabilitiesVested compensated

absences 4,001,831 1,648,913 1,043,482 4,607,262 1,205,305Other post-employment

benefits 808,103 298,115 - 1,106,218 -

Total Other Liabilities 4,809,934 1,947,028 1,043,482 5,713,480 1,205,305

Total GovernmentalActivities Long-TermLiabilities $ 5,506,154 $ 2,046,028 $ 1,140,475 $ 6,411,707 $ 1,312,187

Page 17

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE II - DETAILED NOTES ON ALL FUNDS (cont.)

D. LONG-TERM OBLIGATIONS (cont.)

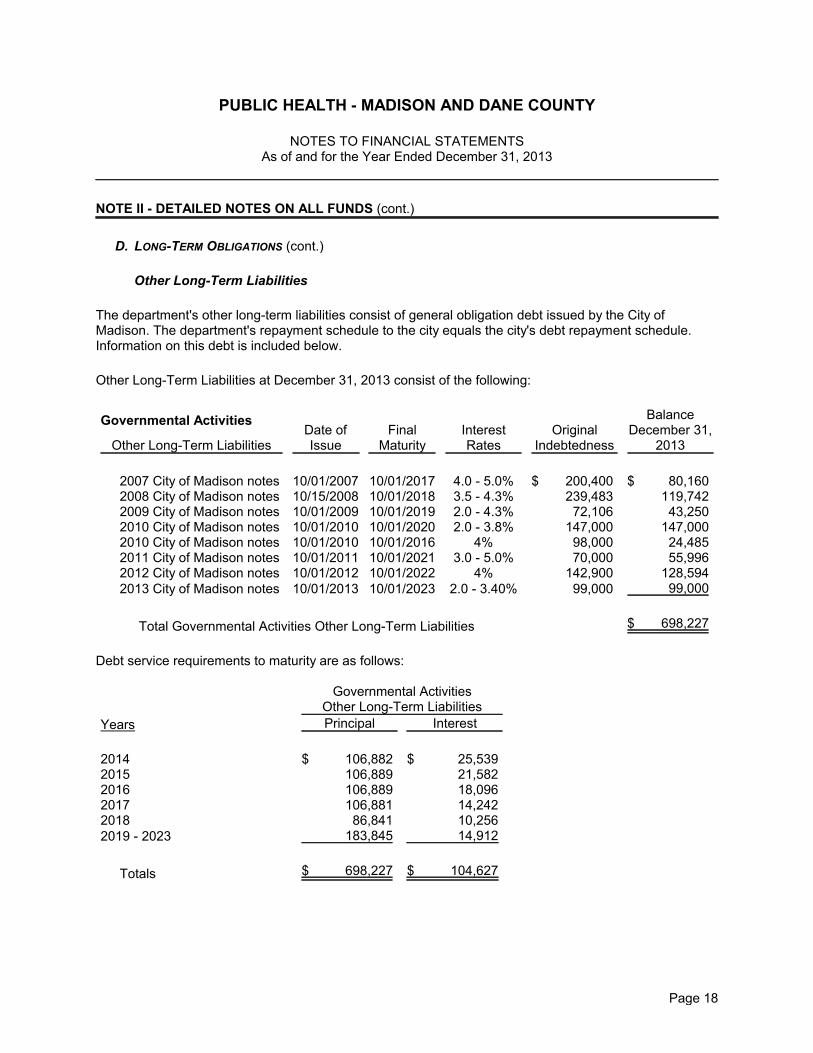

Other Long-Term Liabilities

The department's other long-term liabilities consist of general obligation debt issued by the City ofMadison. The department's repayment schedule to the city equals the city's debt repayment schedule.Information on this debt is included below.

Other Long-Term Liabilities at December 31, 2013 consist of the following:

Governmental Activities

Other Long-Term LiabilitiesDate ofIssue

FinalMaturity

InterestRates

OriginalIndebtedness

BalanceDecember 31,

2013

2007 City of Madison notes 10/01/2007 10/01/2017 4.0 - 5.0% $ 200,400 $ 80,1602008 City of Madison notes 10/15/2008 10/01/2018 3.5 - 4.3% 239,483 119,7422009 City of Madison notes 10/01/2009 10/01/2019 2.0 - 4.3% 72,106 43,2502010 City of Madison notes 10/01/2010 10/01/2020 2.0 - 3.8% 147,000 147,0002010 City of Madison notes 10/01/2010 10/01/2016 4% 98,000 24,4852011 City of Madison notes 10/01/2011 10/01/2021 3.0 - 5.0% 70,000 55,9962012 City of Madison notes 10/01/2012 10/01/2022 4% 142,900 128,5942013 City of Madison notes 10/01/2013 10/01/2023 2.0 - 3.40% 99,000 99,000

Total Governmental Activities Other Long-Term Liabilities $ 698,227

Debt service requirements to maturity are as follows:

Governmental ActivitiesOther Long-Term Liabilities

Years Principal Interest

2014 $ 106,882 $ 25,5392015 106,889 21,5822016 106,889 18,0962017 106,881 14,2422018 86,841 10,2562019 - 2023 183,845 14,912

Totals $ 698,227 $ 104,627

Page 18

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE II - DETAILED NOTES ON ALL FUNDS (cont.)

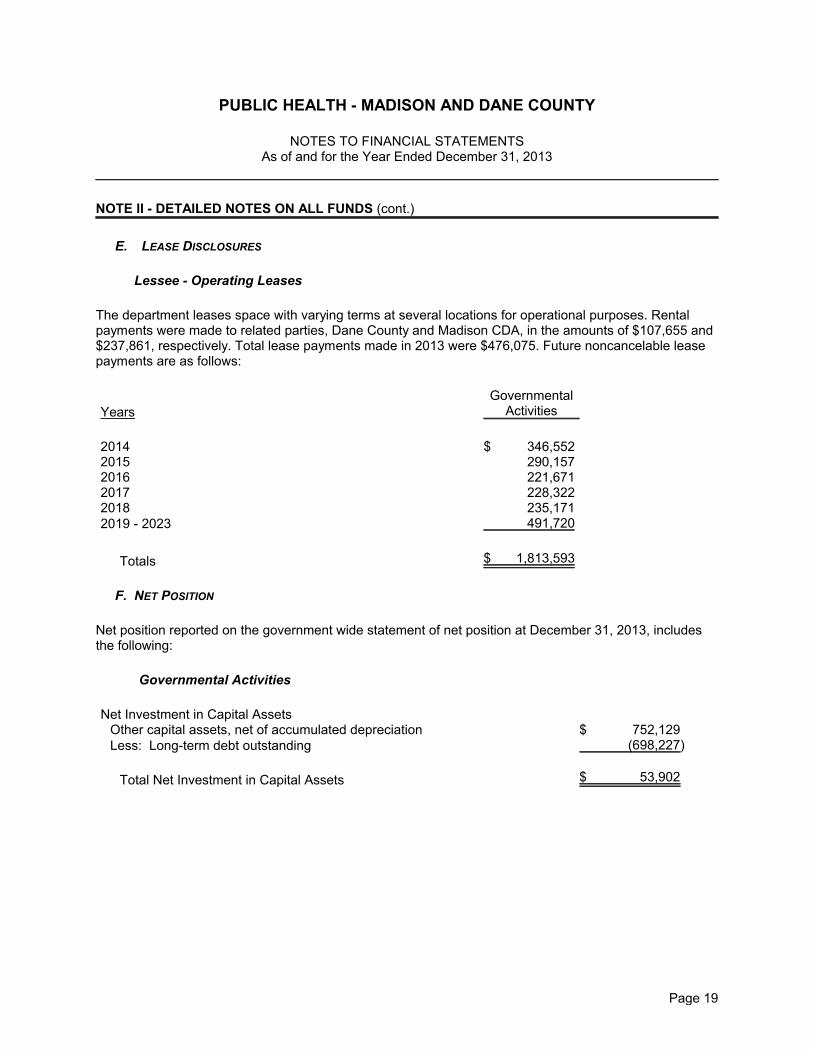

E. LEASE DISCLOSURES

Lessee - Operating Leases

The department leases space with varying terms at several locations for operational purposes. Rentalpayments were made to related parties, Dane County and Madison CDA, in the amounts of $107,655 and$237,861, respectively. Total lease payments made in 2013 were $476,075. Future noncancelable leasepayments are as follows:

Years

GovernmentalActivities

2014 $ 346,5522015 290,1572016 221,6712017 228,3222018 235,1712019 - 2023 491,720

Totals $ 1,813,593

F. NET POSITION

Net position reported on the government wide statement of net position at December 31, 2013, includesthe following:

Governmental Activities

Net Investment in Capital AssetsOther capital assets, net of accumulated depreciation $ 752,129Less: Long-term debt outstanding (698,227)

Total Net Investment in Capital Assets $ 53,902

Page 19

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE III - OTHER INFORMATION

A. EMPLOYEES' RETIREMENT SYSTEM

All eligible department employees participate in the Wisconsin Retirement System (WRS), a cost-sharing,multiple-employer, defined benefit, public employee retirement system. All employees, initially employedby a participating WRS employer prior to July 1, 2011, expected to work over 600 hours a year andexpected to be employed for at least one year from employee's date of hire are eligible to participate in theWRS. All employees, initially employed by a participating WRS employer on or after July 1, 2011, andexpected to work at least 1,200 hours a year and expected to be employed for at least one year fromemployee's date of hire are eligible to participate in the WRS.

Effective the first day of the first pay period on or after June 29, 2011 the employee required contributionwas change to one-half of the actuarially determined contribution rate for General category employees,and Executives and Elected Officials. Required contributions for protective employees are the same asgeneral employees. Employers are required to contribute the remainder of the actuarially determinedcontribution rate. The employer may not pay the employee required contribution unless provided for by anexisting collective bargaining agreement. Contribution rates for December 31, 2013 are:

Employee Employer

General 6.65% 6.65%Executives and Elected Officials 7.00% 7.00%Protective with Social Security 6.65% 9.75%Protective without Social Security 6.65% 12.35%

The payroll for department employees covered by the WRS for the year ended December 31, 2013 was$8,845,758; the employer's total payroll was $8,845,758. The total required contribution for the year endedDecember 31, 2013 was $933,971 or 10.6% of covered payroll. Of this amount, 100% was contributed forthe current year. Total contributions for the years ended 2012 and 2011 were $1,059,760 and $1,116,432,respectively, equal to the required contributions for each year.

Employees who retire at or after age 65 (62 for elected officials and 54 for protective occupationemployees with less than 25 years of service, 53 for protective occupation employees with more than 25years of service) are entitled to receive a retirement benefit. Employees may retire at age 55 (50 forprotective occupation employees) and receive actuarially reduced benefits. The factors influencing thebenefit are: (1) final average earnings, (2) years of creditable service, and (3) a formula factor. A finalaverage earnings is the average of the employee's three highest years' earnings. Employees terminatingcovered employment and submitting application before becoming eligible for a retirement benefit maywithdraw their contributions and, by doing so, forfeit all rights to any subsequent benefit. For employeesbeginning participation on or after January 1, 1990, and no longer actively employed on or after April 24,1998, creditable service in each of five years is required for eligibility for a retirement annuity. Participantsemployed prior to 1990 and on or after April 24, 1998 and prior to July 1, 2011 are immediately vested.Participants who initially became WRS eligible on or after July 1, 2011 must have five years of creditableservice to be vested.

The WRS also provides death and disability benefits for employees. Eligibility and the amount of allbenefits are determined under Chapter 40 of Wisconsin Statutes.

Page 20

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE III - OTHER INFORMATION (cont.)

A. EMPLOYEES' RETIREMENT SYSTEM (cont.)

The WRS issues an annual financial report which may be obtained by writing to the Department ofEmployee Trust Funds, P.O. Box 7931, Madison, WI 53707-7931.

As of December 31, 2013 there was no pension related debt for the department.

B. RISK MANAGEMENT

The department is covered by the City of Madison's and the County of Dane's insurance policies. Refer tothe City's and County's financial statements for more information.

C. COMMITMENTS AND CONTINGENCIES

Claims and judgments are recorded as liabilities if all the conditions of Governmental AccountingStandards Board pronouncements are met. The liability and expenditure for claims and judgments areonly reported in governmental funds if it has matured. Claims and judgments are recorded in thegovernment-wide statements and proprietary funds as expenses when the related liabilities are incurred.

From time to time, the department is party to various pending claims and legal proceedings. Although theoutcome of such matters cannot be forecasted with certainty, it is the opinion of management and thedepartment attorney that the likelihood is remote that any such claims or proceedings will have a materialadverse effect on the department's financial position or results of operations.

The department has received federal and state grants for specific purposes that are subject to review andaudit by the grantor agencies. Such audits could lead to requests for reimbursements to the grantoragency for expenditures disallowed under terms of the grants. Management believes such disallowances,if any, would be immaterial.

D. OTHER POSTEMPLOYMENT BENEFITS

Employees of the department are employed by the County of Dane. Refer to the financial statements ofthe county for details on other postemployment benefits.

Page 21

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2013

NOTE III - OTHER INFORMATION (cont.)

E. EFFECT OF NEW ACCOUNTING STANDARDS ON CURRENT-PERIOD FINANCIAL STATEMENTS

The Governmental Accounting Standards Board (GASB) has approved the following:

Statement No. 67, Financial Reporting for Pension Plans - an amendment of GASB Statement

No. 25

Statement No. 68, Accounting and Financial Reporting for Pensions - an amendment of GASB

Statement No. 27

Statement No. 69, Government Combinations and Disposals of Government Operations

Statement No. 70, Accounting and Financial Reporting for Nonexchange Financial Guarantees

When they become effective, application of these standards may restate portions of these financialstatements.

Page 22

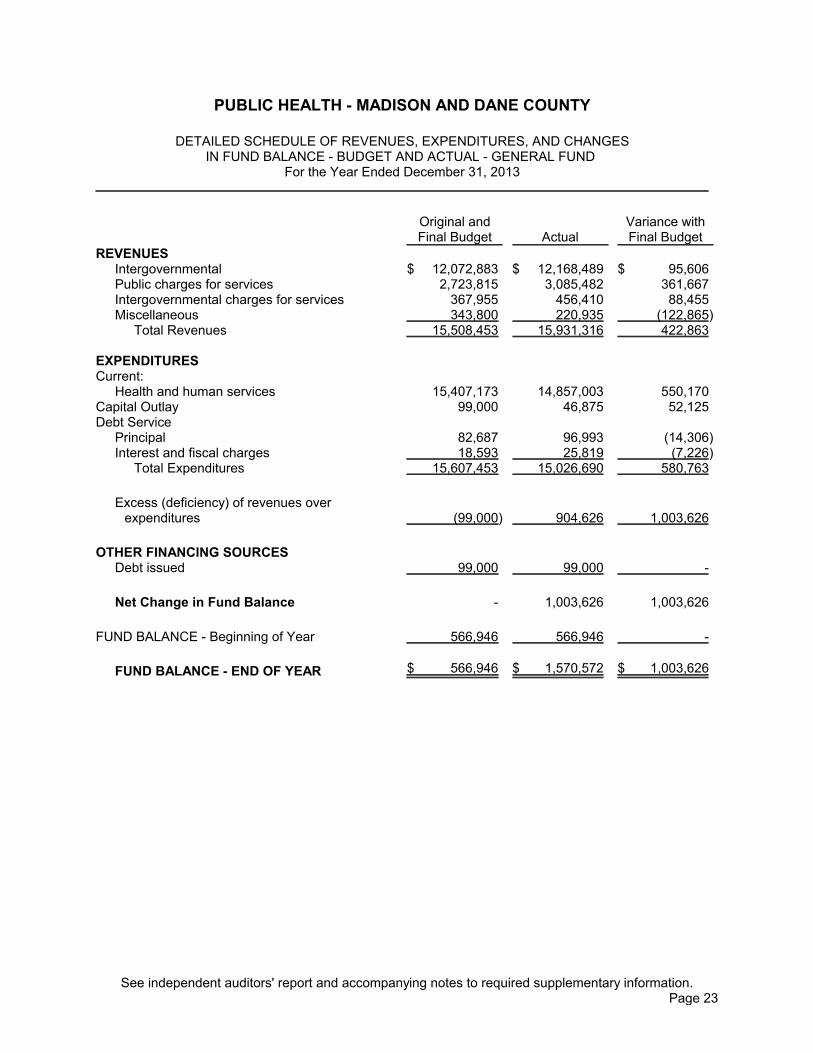

R E Q U I R E D S U P P L E M E N T A R Y I N F O R M A T I O N

PUBLIC HEALTH - MADISON AND DANE COUNTY

DETAILED SCHEDULE OF REVENUES, EXPENDITURES, AND CHANGESIN FUND BALANCE - BUDGET AND ACTUAL - GENERAL FUND

For the Year Ended December 31, 2013

Original andFinal Budget Actual

Variance withFinal Budget

REVENUESIntergovernmental $ 12,072,883 $ 12,168,489 $ 95,606Public charges for services 2,723,815 3,085,482 361,667Intergovernmental charges for services 367,955 456,410 88,455Miscellaneous 343,800 220,935 (122,865)

Total Revenues 15,508,453 15,931,316 422,863

EXPENDITURESCurrent:

Health and human services 15,407,173 14,857,003 550,170Capital Outlay 99,000 46,875 52,125Debt Service

Principal 82,687 96,993 (14,306)Interest and fiscal charges 18,593 25,819 (7,226)

Total Expenditures 15,607,453 15,026,690 580,763

Excess (deficiency) of revenues overexpenditures (99,000) 904,626 1,003,626

OTHER FINANCING SOURCESDebt issued 99,000 99,000 -

Net Change in Fund Balance - 1,003,626 1,003,626

FUND BALANCE - Beginning of Year 566,946 566,946 -

FUND BALANCE - END OF YEAR $ 566,946 $ 1,570,572 $ 1,003,626

See independent auditors' report and accompanying notes to required supplementary information.Page 23

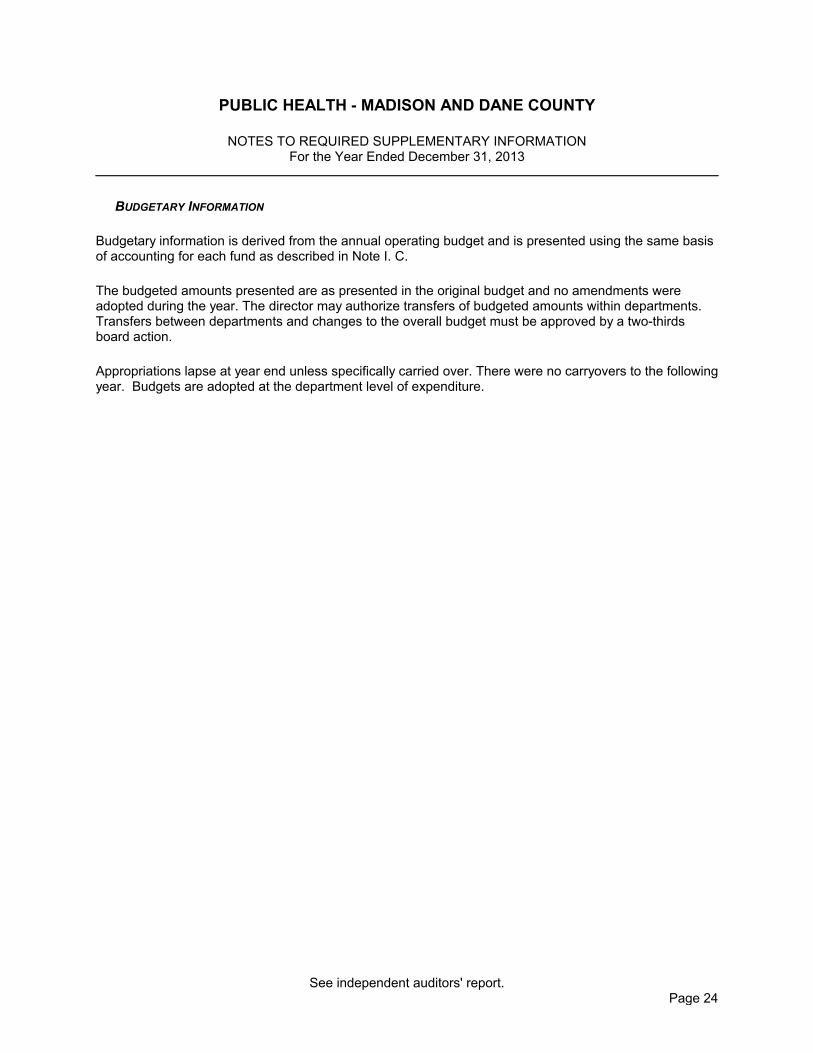

PUBLIC HEALTH - MADISON AND DANE COUNTY

NOTES TO REQUIRED SUPPLEMENTARY INFORMATIONFor the Year Ended December 31, 2013

BUDGETARY INFORMATION

Budgetary information is derived from the annual operating budget and is presented using the same basisof accounting for each fund as described in Note I. C.

The budgeted amounts presented are as presented in the original budget and no amendments wereadopted during the year. The director may authorize transfers of budgeted amounts within departments.Transfers between departments and changes to the overall budget must be approved by a two-thirdsboard action.

Appropriations lapse at year end unless specifically carried over. There were no carryovers to the followingyear. Budgets are adopted at the department level of expenditure.

See independent auditors' report.Page 24

S I N G L E A U D I T S E C T I O N

DirectGrant Number/ Accrued/ (Accrued)/

Federal Pass- Pass-Through Program (Deferred) Cash DeferredCFDA Through Grantor's or Award Beginning Received Ending

Federal Grantor/Program Title Number Agency Number Amount Balance Adjustments (Returned) Expenditures Balance

FEDERAL AWARDS

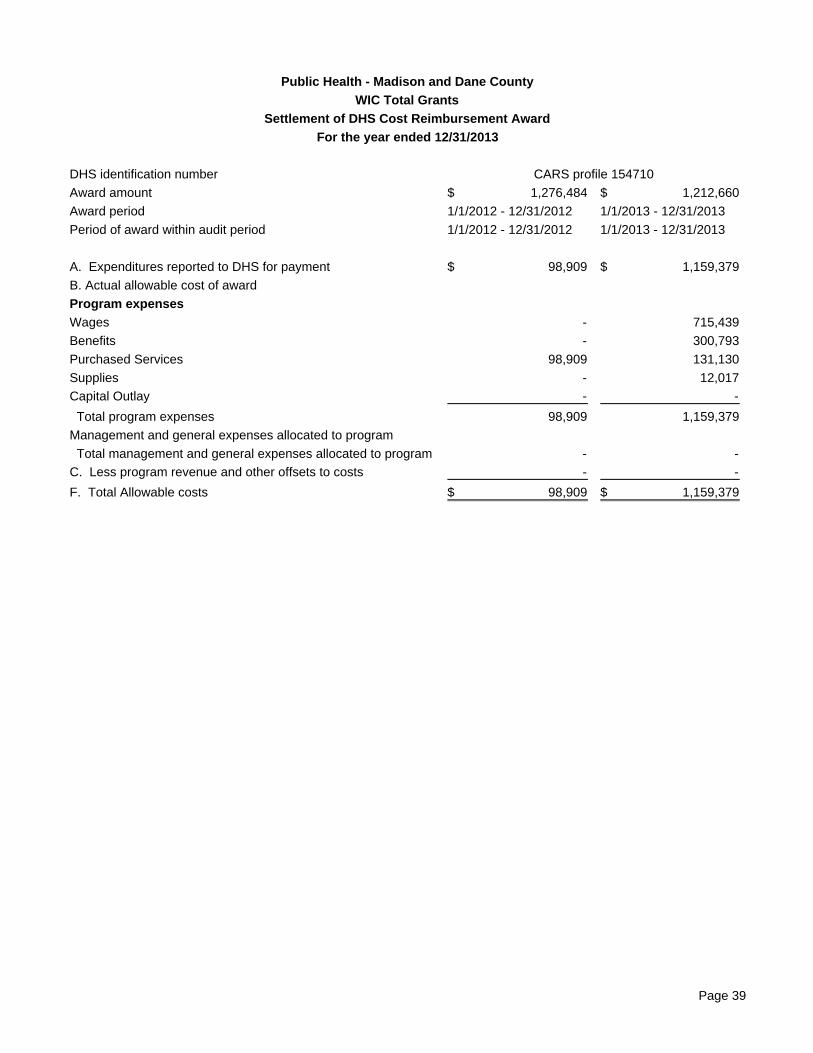

U.S. Department of Agriculture Special Supplemental Nutrition Program for Women, Infants, and Children 10.557 WIC Infrastructure WI DHS 260-154740 6,650$ (2,412)$ -$ 2,412$ -$ -$ WIC Total Grants WI DHS 260-154710 1,276,484 12,538 (11,089) 97,460 98,909 -

WIC Total Grants WI DHS 360-154710 1,212,660 - - 1,212,660 1,159,379 53,281 WIC Breastfeeding Peer Counseling WI DHS 360-154760 21,741 - - 15,773 18,371 (2,598)

10,126 (11,089) 1,328,305 1,276,659 50,683

WIC Farmers Market 10.572 WI DHS 360-154720 5,001 - - 5,001 5,001 -

Total U.S. Department of Agriculture 10,126 (11,089) 1,333,306 1,281,660 50,683

U.S. Department of Housing and Urban DevelopmentLead Hazard Reduction Demonstration Grant Program 14.905

HUD Lead Hazard Demonstration WI DHS 260-156912 15,000 136 834 (970) - -

Total U.S. Department of Housing and Urban Development 136 834 (970) - -

U.S. Environmental Protection Agency State Indoor Radon Grants 66.032

Radon Regional Information Center WI DHS 260-150321 10,998 (245) 245 - - - Radon Information Centers WI DHS 360-150321 10,998 - - 9,707 10,998 (1,291)

Total U.S. Environmental Protection Agency (245) 245 9,707 10,998 (1,291)

U.S. Department of Health and Human Services Refugee and Entrant Assistance - State Administered Programs 93.566

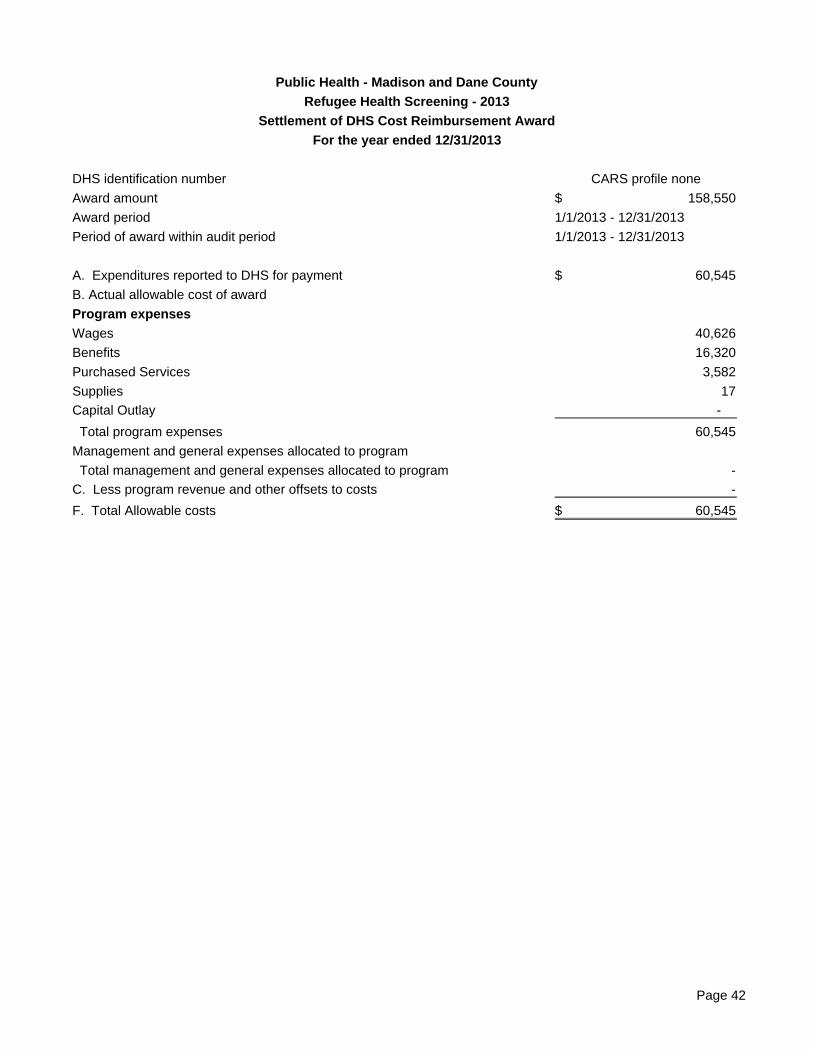

Refugee Health Screening -2013 WI DCF N/A 158,550 - - 59,995 60,545 (550)

- - 59,995 60,545 (550)

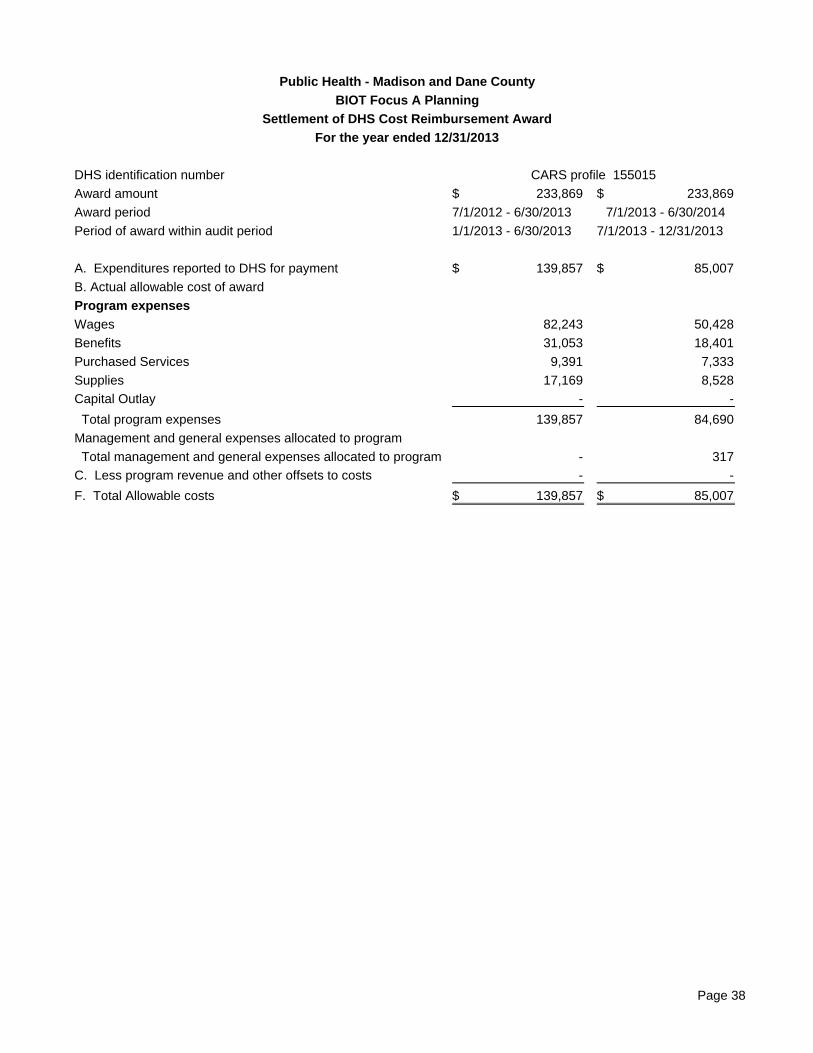

Public Health Emergency Preparedness 93.069Biot Focus A Planning WI DHS 360-155015 233,869 2,755 1 137,101 139,857 - Biot Focus A Planning WI DHS 260-155015 233,868 (17,600) 17,600 - - - Public Health Emergency Preparedness (July 1, 2013 to June 30, 2014 WI DHS 460-155015 233,869 - - 99,104 85,007 14,097

(14,845) 17,601 236,205 224,864 14,097

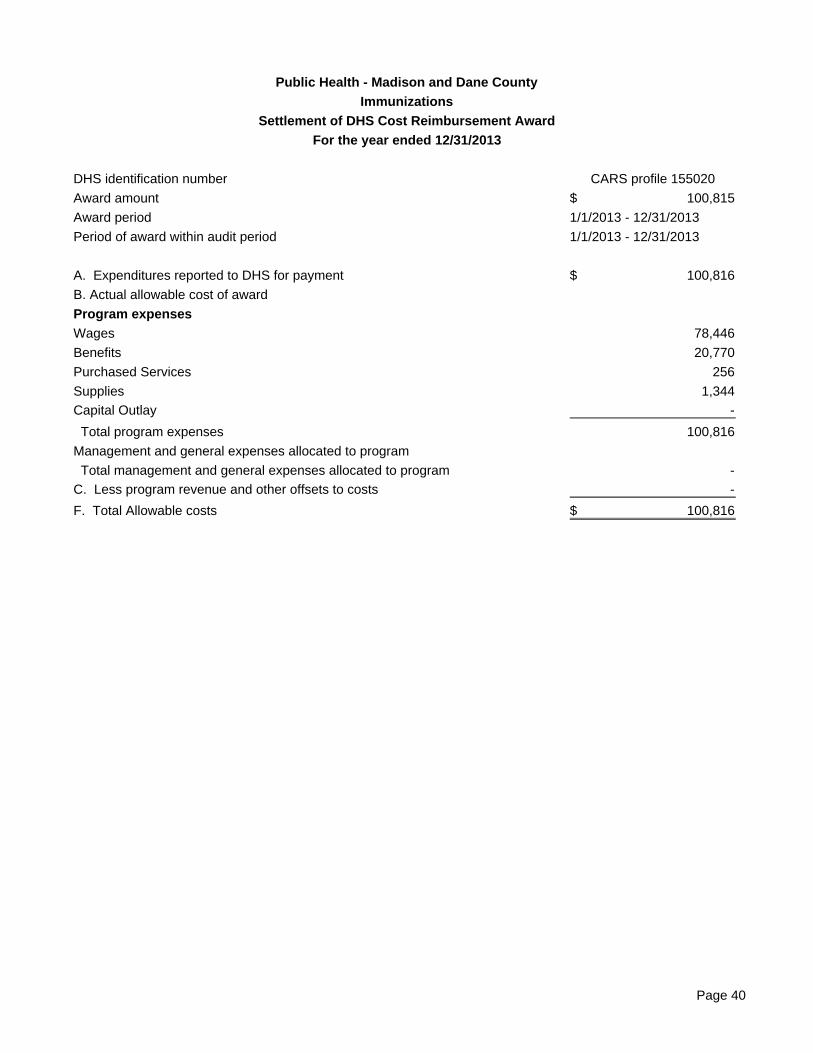

Immunization Cooperative Agreements 93.268 Cons Contracts - IMM WI DHS 260-155020 100,815 2 - (2) - - Immunization WI DHS 360-155020 100,815 - 1 100,815 100,816 -

2 1 100,813 100,816 -

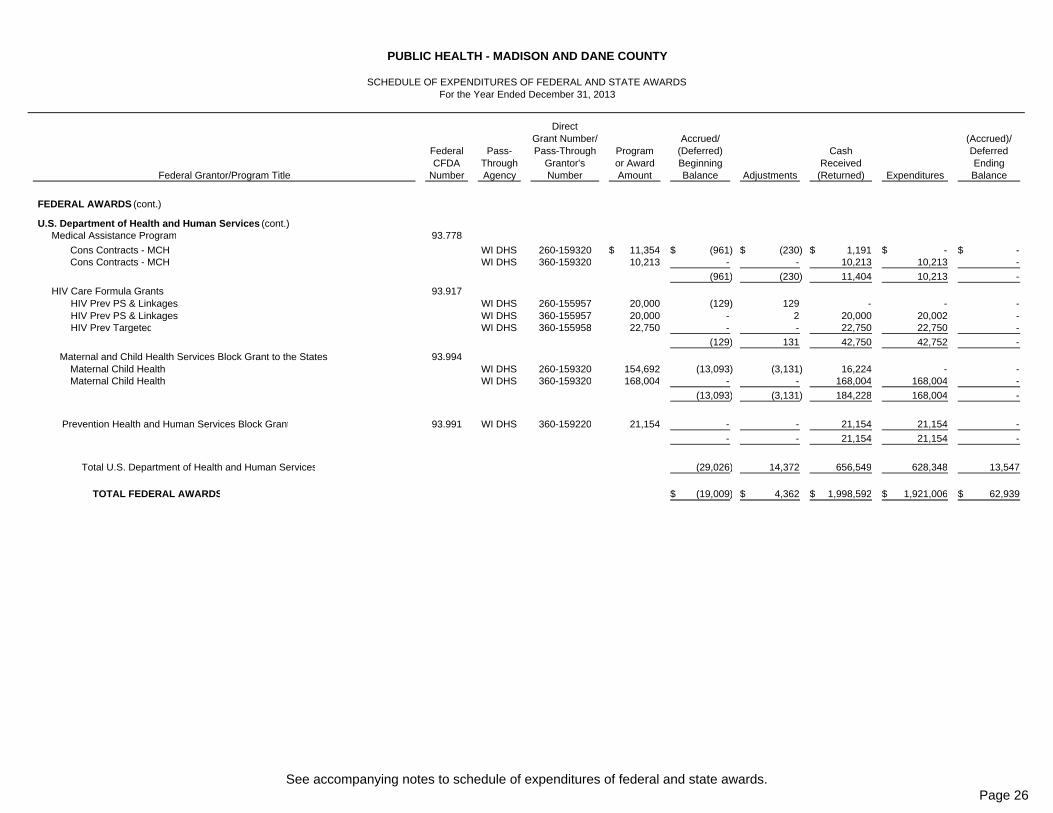

PUBLIC HEALTH - MADISON AND DANE COUNTY

SCHEDULE OF EXPENDITURES OF FEDERAL AND STATE AWARDSFor the Year Ended December 31, 2013

See accompanying notes to schedule of expenditures of federal and state awards.Page 25

DirectGrant Number/ Accrued/ (Accrued)/

Federal Pass- Pass-Through Program (Deferred) Cash DeferredCFDA Through Grantor's or Award Beginning Received Ending

Federal Grantor/Program Title Number Agency Number Amount Balance Adjustments (Returned) Expenditures Balance

PUBLIC HEALTH - MADISON AND DANE COUNTY

SCHEDULE OF EXPENDITURES OF FEDERAL AND STATE AWARDSFor the Year Ended December 31, 2013

FEDERAL AWARDS (cont.)

U.S. Department of Health and Human Services (cont.) Medical Assistance Program 93.778

Cons Contracts - MCH WI DHS 260-159320 11,354$ (961)$ (230)$ 1,191$ -$ -$ Cons Contracts - MCH WI DHS 360-159320 10,213 - - 10,213 10,213 -

(961) (230) 11,404 10,213 -

HIV Care Formula Grants 93.917 HIV Prev PS & Linkages WI DHS 260-155957 20,000 (129) 129 - - - HIV Prev PS & Linkages WI DHS 360-155957 20,000 - 2 20,000 20,002 - HIV Prev Targeted WI DHS 360-155958 22,750 - - 22,750 22,750 -

(129) 131 42,750 42,752 -

Maternal and Child Health Services Block Grant to the States 93.994Maternal Child Health WI DHS 260-159320 154,692 (13,093) (3,131) 16,224 - - Maternal Child Health WI DHS 360-159320 168,004 - - 168,004 168,004 -

(13,093) (3,131) 184,228 168,004 -

Prevention Health and Human Services Block Grant 93.991 WI DHS 360-159220 21,154 - - 21,154 21,154 -

- - 21,154 21,154 -

Total U.S. Department of Health and Human Services (29,026) 14,372 656,549 628,348 13,547

TOTAL FEDERAL AWARDS (19,009)$ 4,362$ 1,998,592$ 1,921,006$ 62,939$

See accompanying notes to schedule of expenditures of federal and state awards.Page 26

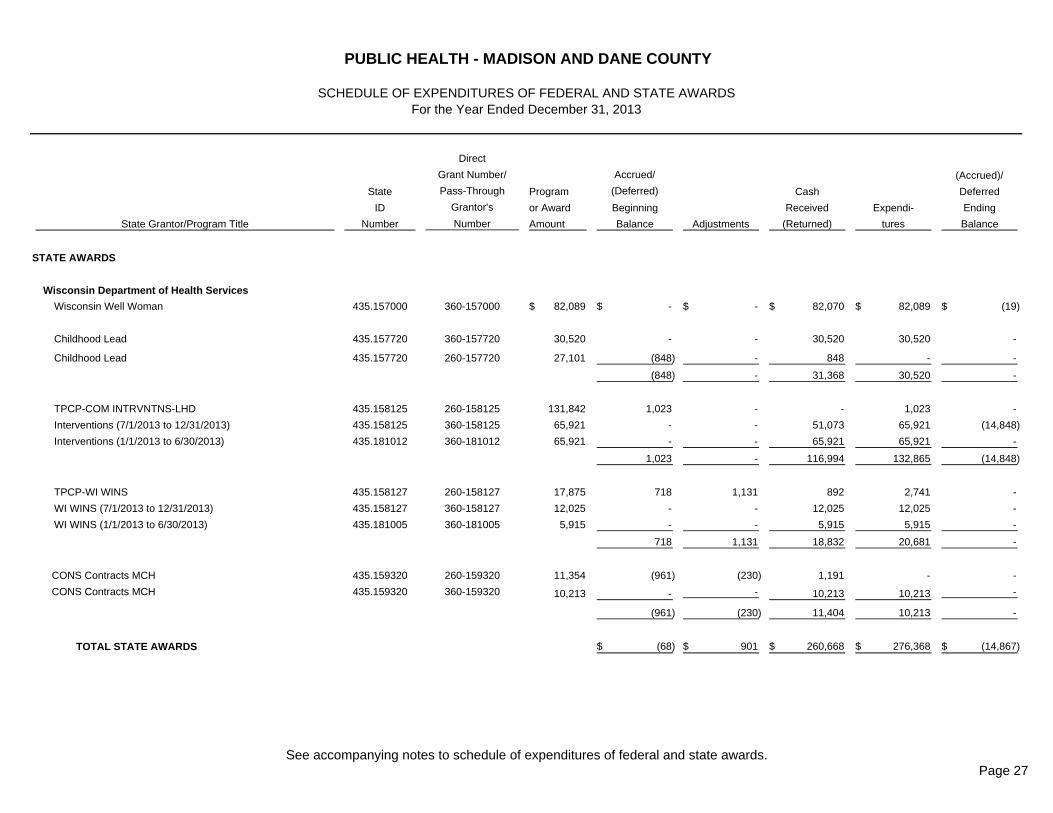

Direct

Grant Number/ Accrued/ (Accrued)/

State Pass-Through Program (Deferred) Cash Deferred

ID Grantor's or Award Beginning Received Expendi- Ending

State Grantor/Program Title Number Number Amount Balance Adjustments (Returned) tures Balance

STATE AWARDS

Wisconsin Department of Health Services

Wisconsin Well Woman 435.157000 360-157000 82,089$ -$ -$ 82,070$ 82,089$ (19)$

Childhood Lead 435.157720 360-157720 30,520 - - 30,520 30,520 -

Childhood Lead 435.157720 260-157720 27,101 (848) - 848 - -

(848) - 31,368 30,520 -

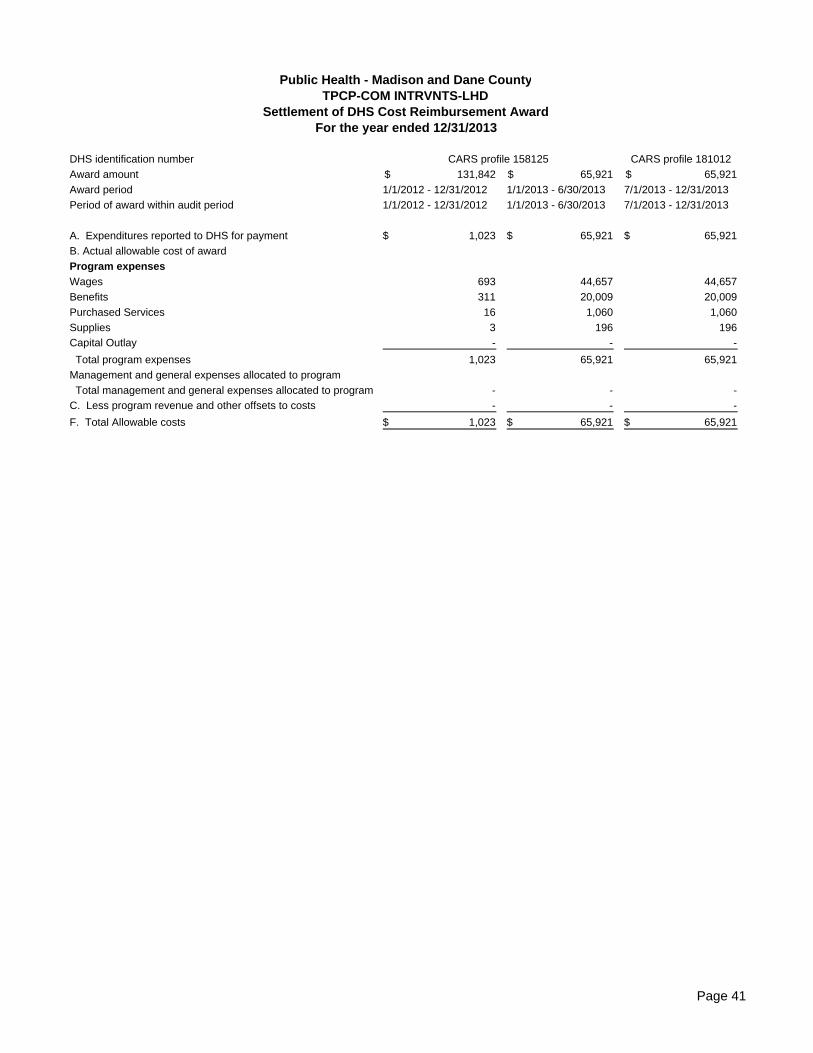

TPCP-COM INTRVNTNS-LHD 435.158125 260-158125 131,842 1,023 - - 1,023 -

Interventions (7/1/2013 to 12/31/2013) 435.158125 360-158125 65,921 - - 51,073 65,921 (14,848)

Interventions (1/1/2013 to 6/30/2013) 435.181012 360-181012 65,921 - - 65,921 65,921 -

1,023 - 116,994 132,865 (14,848)

TPCP-WI WINS 435.158127 260-158127 17,875 718 1,131 892 2,741 -

WI WINS (7/1/2013 to 12/31/2013) 435.158127 360-158127 12,025 - - 12,025 12,025 -

WI WINS (1/1/2013 to 6/30/2013) 435.181005 360-181005 5,915 - - 5,915 5,915 -

718 1,131 18,832 20,681 -

CONS Contracts MCH 435.159320 260-159320 11,354 (961) (230) 1,191 - -

CONS Contracts MCH 435.159320 360-159320 10,213 - - 10,213 10,213 -

(961) (230) 11,404 10,213 -

TOTAL STATE AWARDS (68)$ 901$ 260,668$ 276,368$ (14,867)$

PUBLIC HEALTH - MADISON AND DANE COUNTY

SCHEDULE OF EXPENDITURES OF FEDERAL AND STATE AWARDSFor the Year Ended December 31, 2013

See accompanying notes to schedule of expenditures of federal and state awards.Page 27

Page 28

PUBLIC HEALTH – MADISON AND DANE COUNTY

NOTES TO THE SCHEDULE OF EXPENDITURES OF FEDERAL AND STATE AWARDS For the Year Ended December 31, 2013

NOTE 1 – BASIS OF PRESENTATION The accompanying schedule of expenditures of federal and state awards (the “schedule”) includes the federal and state grant activity of Public Health – Madison and Dane County (“department”) under programs of the federal and state government for the year ended December 31, 2013. The information in this schedule is presented in accordance with the requirements of the Office of Management and Budget (OMB) Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and the State Single Audit Guidelines. Because the schedule presents only a selected portion of the operations of the department, it is not intended to and does not present the financial position or changes in net position of the department. NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Expenditures reported on the schedule are reported on the accrual basis of accounting. Such expenditures are recognized following the cost principles contained in OMB Circular A-87, Cost Principles for State, Local, and Indian Tribal Governments, wherein certain types of expenditures are not allowable or are limited as to reimbursement. Negative amounts shown on the schedule represent adjustments or credits made in the normal course of business to amounts reported as expenditures in prior years. Pass-through entity identifying numbers are presented where available. The underlying accounting records for grant programs are maintained on the modified accrual basis of accounting. Under the modified accrual basis, revenues are recorded when susceptible to accrual, i.e., both measurable and available. Available means collectible within the current period or soon enough thereafter to be used to pay liabilities of the current period. Expenditures are recorded when the liability is incurred. Adjustments to the schedule represent changes to the accrued or deferred balances as of the beginning of the year. NOTE 3 – CARS REPORT DATES

The Schedule of Expenditures of Federal and State Awards includes adjustments through the April 1, 2014 Community Aids Reporting System (CARS) report. NOTE 4 – PASS-THROUGH AGENCIES

Federal funds were passed through the following state agencies: WI DHS – Wisconsin Department of Health Services WI DCF – Wisconsin Department of Children and Families

Page 33

PUBLIC HEALTH – MADISON AND DANE COUNTY

SCHEDULE OF FINDINGS AND QUESTIONED COSTS For the Year Ended December 31, 2013

SECTION I – SUMMARY OF AUDITORS’ RESULTS FINANCIAL STATEMENTS

Type of auditors’ report issued: Unmodified

Internal control over financial reporting:

Material weakness(es) identified? X yes no Significant deficiency(ies) identified? X yes none reported Noncompliance material to basic financial statements noted?

yes

X

no

FEDERAL OR STATE AWARDS Internal control over major programs: Material weakness(es) identified? yes X no Significant deficiency(ies) identified? yes X none reported Type of auditor’s report issued on compliance for major programs: Unmodified Any audit findings disclosed that are required to be reported in accordance with section 510(a) of OMB Circular A-133?

yes

X

no

Federal Programs State Programs Auditee qualified as low-risk auditee? yes X no yes X no Identification of major federal programs:

CFDA Numbers Name of Federal Program

10.557 Special Supplemental Nutrition Program for Women, Infants, and Children

Federal State Dollar threshold used to distinguish between type A and type B programs:

$ 300,000

$ 100,000

Identification of major state programs:

State Number Name of State Program 435.157000 Wisconsin Well Women Program 435.158125/

435.181012 Tobacco Prevention and Control Program – Community

Interventions

Page 34

PUBLIC HEALTH – MADISON AND DANE COUNTY

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

For the Year Ended December 31, 2013 SECTION II – FINANCIAL STATEMENT FINDINGS REQUIRED TO BE REPORTED IN ACCORDANCE

WITH GOVERNMENT AUDITING STANDARDS The City of Madison has the fiduciary responsibilities over Public Health – Madison and Dane County (“department”). The financial statement findings below have been duplicated from the City of Madison’s single audit report. FINDING 2013-1: MATERIAL WEAKNESS – INTERNAL CONTROL OVER FINANCIAL REPORTING Criteria: Statement on Auditing Standards (SAS) No. 115 states that the department should have internal control procedures that enable the preparation of financial statements by department personnel that are free from material errors. Condition: Auditing standards require that we perform procedures to obtain an understanding of your government and its internal control environment as part of the annual audit. This includes an analysis of the department’s year-end financial reporting process and preparation of your financial statements. A properly designed system of internal control allows for the presentation of year-end financial data and financial statements without material errors. At this time, the department does not have internal controls in place that allow for the preparation of complete and accurate financial statements, including an independent review by someone other than the preparer. As a result, we consider this absence of controls to be a material weakness in internal control over the department’s financial reporting. Cause: Due to staffing constraints, the department relies on the auditors to prepare some financial statement disclosures. Effect: The auditors assisted with the preparation of the annual financial statements. Recommendation: The department may consider and implement additional internal control procedures in order to prepare materially correct year-end financial statements.

Management’s Response City management is aware that to avoid a material weakness related to its year-end financial reporting process, we must prepare a complete set of financial statements, conversion entries, and footnote disclosures that are free from material misstatement. Currently, City staff prepares individual fund statements, conversion entries, and some footnote disclosures. We will continue to make additional efforts to draft the government-wide statements, and to prepare additional footnote disclosures, but we expect to rely on the assistance of the external audit firm to prepare selected portions of the annual financial statements.

Page 35

PUBLIC HEALTH – MADISON AND DANE COUNTY

SCHEDULE OF FINDINGS AND QUESTIONED COSTS For the Year Ended December 31, 2013

SECTION II – FINANCIAL STATEMENT FINDINGS REQUIRED TO BE REPORTED IN ACCORDANCE

WITH GOVERNMENT AUDITING STANDARDS (cont.) FINDING 2013-2: MATERIAL WEAKNESS – INTERNAL CONTROL ENVIRONMENT Criteria: We performed our audit under Statements on Auditing Standards (SAS) Nos. 104-111, which required us to review the department’s internal controls over major accounting processes. As a result, we identified certain control deficiencies that were not in place during the year under audit. Condition: Auditing standards require that we perform procedures to obtain an understanding of your government and its internal control environment as part of the annual audit. This includes an analysis of significant transaction cycles. A properly designed system of internal control includes adequate staffing, policies, and procedures to properly segregate duties. This includes systems that are designed to limit the access or control of any one individual to your government’s assets, and to achieve a higher likelihood that errors or irregularities in your processes would be discovered by your staff. At this time, the department does not have internal controls in place to achieve adequate segregation of duties. As a result, there is a material weakness related to the department’s internal control environment. There are also other key controls related to significant transaction cycles that are important in reducing the risk of errors or irregularities. At this time, the department does not have the following controls in place:

CONTROLS OVER FINANCIAL REPORTING Account reconciliations should be performed by someone independent of the processing of

transactions in the account.

ENTITY-WIDE CONTROLS A formal fraud risk evaluation process should be in place. This is a control process that should

exist and be performed by either a newly created audit committee or a finance committee. Cause: Due to staffing constraints, some accounting activities are not able to be implemented or adequately segregated. Effect: Weaknesses in the internal controls over accounting processes increases the possibility of misstatements due to errors or fraud. Recommendation: The department may consider and implement additional internal controls over its major accounting processes to adequately segregate duties and reduce the risk of misstatements to the financial records.

Management’s Response