Public & Government Affairs Overview - Dipartimento di ... intervento Ing... · • Conoscere...

65

This presentation includes forward-looking statements. Actual future conditions (including economic conditions, energy demand, and energy supply) could differ materially due to changes in technology, the development of new supply sources, political events, demographic changes, and other factors discussed herein (and in Item 1A of ExxonMobil’s latest report on Form 10-K or information set forth under "factors affecting future results" on the "investors" page of our website at www.exxonmobil.com). This material is not to be reproduced without the permission of Exxon Mobil Corporation. Public & Government Affairs Overview Rome – April 21, 2017 Proprietary

Transcript of Public & Government Affairs Overview - Dipartimento di ... intervento Ing... · • Conoscere...

This presentation includes forward-looking statements. Actual future conditions (including economic conditions, energy demand, and energy supply) could differ materially due to changes in technology, the development of new supply sources, political events, demographic changes, and other factors discussed herein (and in Item 1A of ExxonMobil’s latest report on Form 10-K or information set forth under "factors affecting future results" on the "investors" page of our website at www.exxonmobil.com). This material is not to be reproduced without the permission of Exxon Mobil Corporation.

Public & Government Affairs Overview

Rome – April 21, 2017

Proprietary

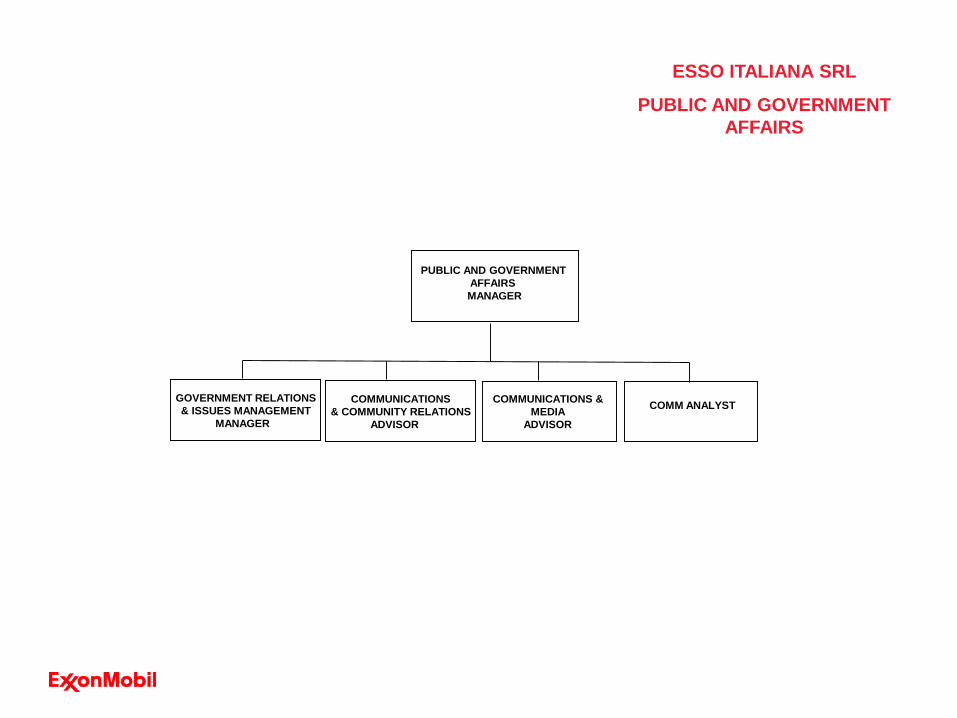

ESSO ITALIANA SRL

PUBLIC AND GOVERNMENT AFFAIRS

PUBLIC AND GOVERNMENT AFFAIRS MANAGER

COMMUNICATIONS& COMMUNITY RELATIONS

ADVISOR

COMMUNICATIONS & MEDIA

ADVISOR

COMM ANALYSTGOVERNMENT RELATIONS& ISSUES MANAGEMENT

MANAGER

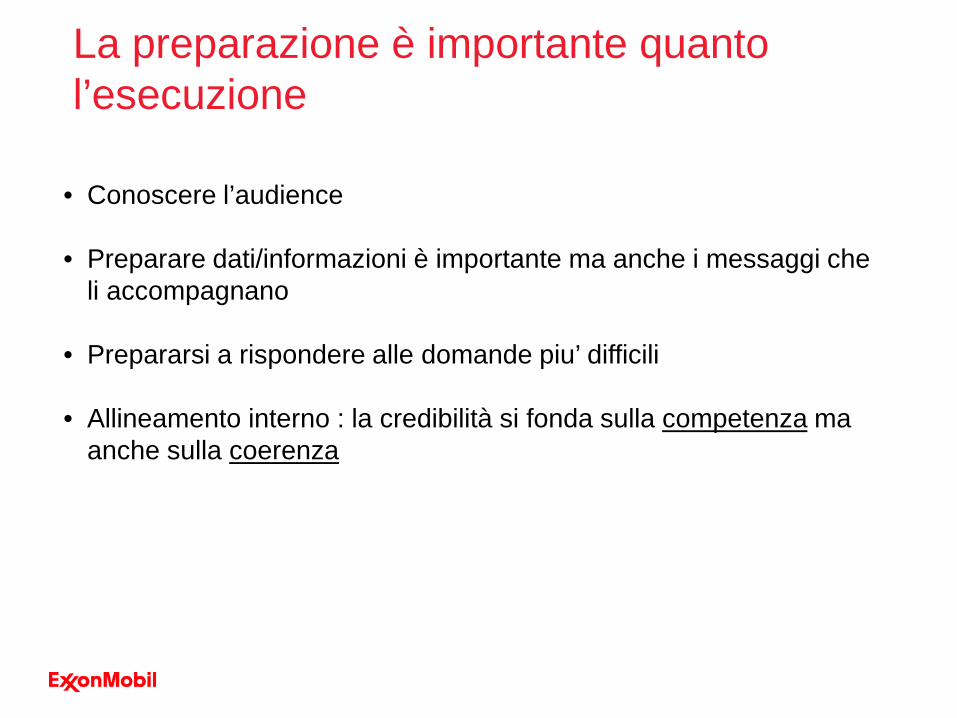

• Conoscere l’audience

• Preparare dati/informazioni è importante ma anche i messaggi che li accompagnano

• Prepararsi a rispondere alle domande piu’ difficili

• Allineamento interno : la credibilità si fonda sulla competenza ma anche sulla coerenza

La preparazione è importante quanto l’esecuzione

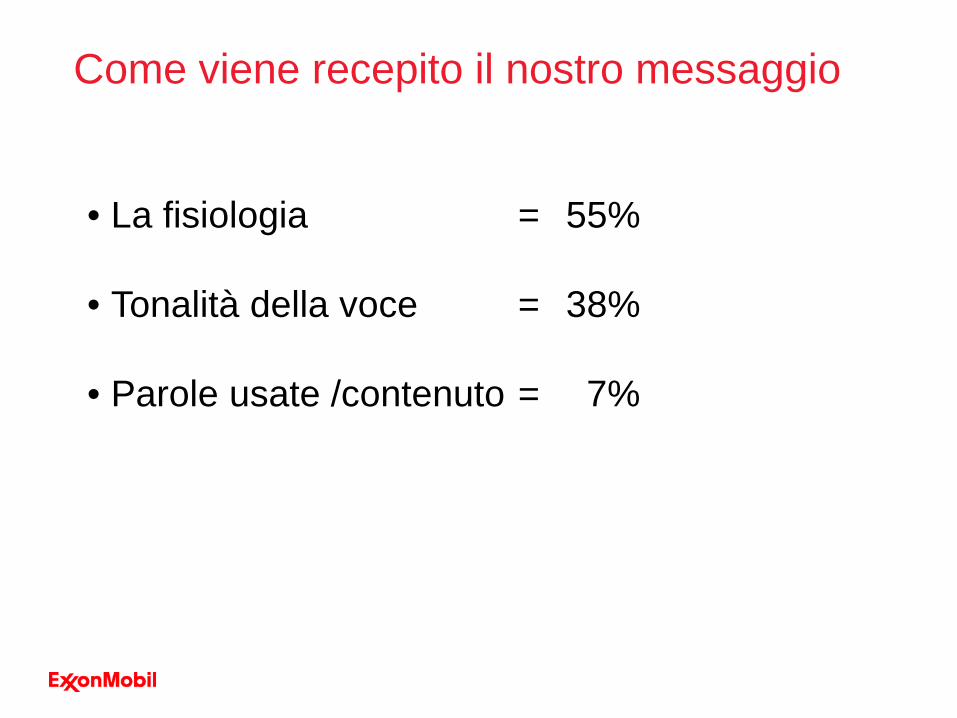

• La fisiologia = 55%

• Tonalità della voce = 38%

• Parole usate /contenuto = 7%

Come viene recepito il nostro messaggio

L’evoluzione del messaggio è difficile da controllare

Il messaggio viaggia....e si modifica

Abbiamo avuto il numero record di segnalazioni di Near Miss (quasi incidenti) nell’ultimo mese!

• Audience interna

• Audience esterna

Capire le diverse prospettive

DOMANDE?

The Outlook for Energy includes Exxon Mobil Corporation’s internal estimates and forecasts of energy demand, supply, and trends through 2040 based upon internal data and analyses as well as publicly available information from external sources including the International Energy Agency. Work on the report was conducted throughout 2016. This presentation includes forward looking statements. Actual future conditions and results (including energy demand, energy supply, the relative mix of energy across sources, economic sectors and geographic regions, imports and exports of energy) could differ materially due to changes in economic conditions, technology, the development of new supply sources, political events, demographic changes, and other factors discussed herein and under the heading “Factors Affecting Future Results” in the Investors section of our website at www.exxonmobil.com. This material is not to be used or reproduced without the permission of Exxon Mobil Corporation. All rights reserved.

2017 Outlook for Energy: A View to 2040

0%

25%

50%

75%

100%

125%

2015 2040

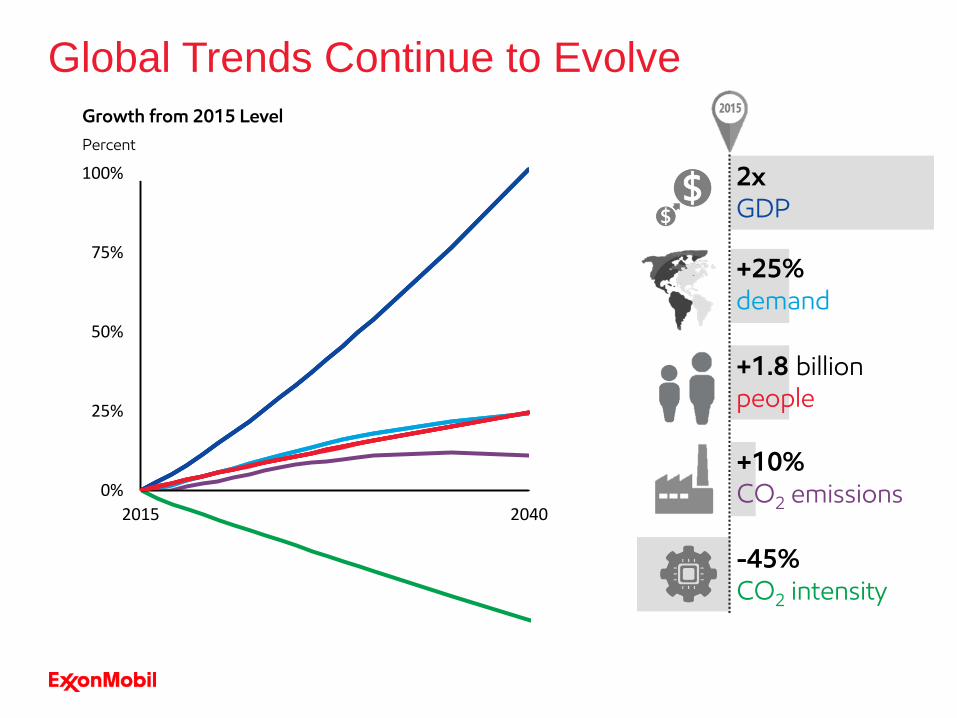

Global Trends Continue to Evolve

+1.8 billionpeople

2xGDP

+25%demand

+10%CO2 emissions

-45%CO2 intensity

Percent

Growth from 2015 Level

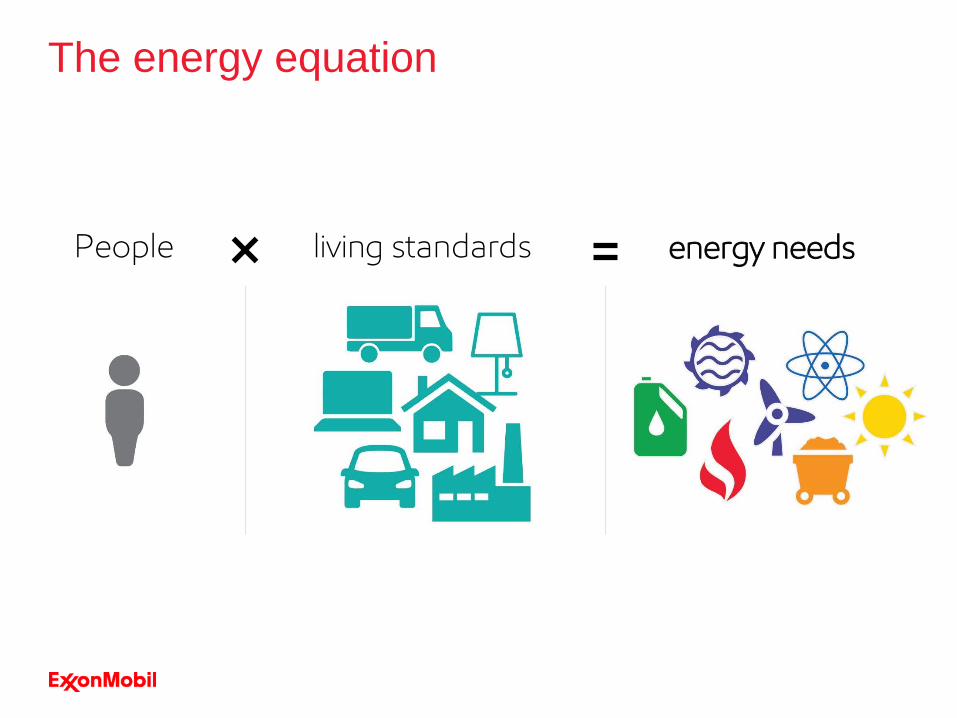

The energy equation

living standardsPeople energy needs

0

2

4

6

8

10

1950 1995 20400

2

4

6

8

10

1950 1995 2040

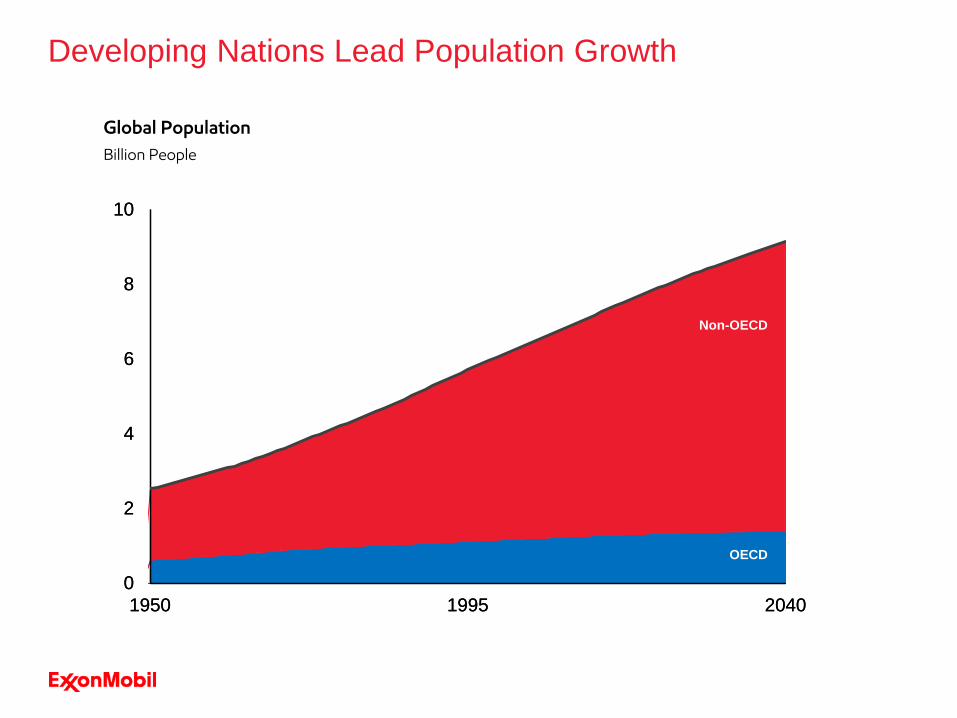

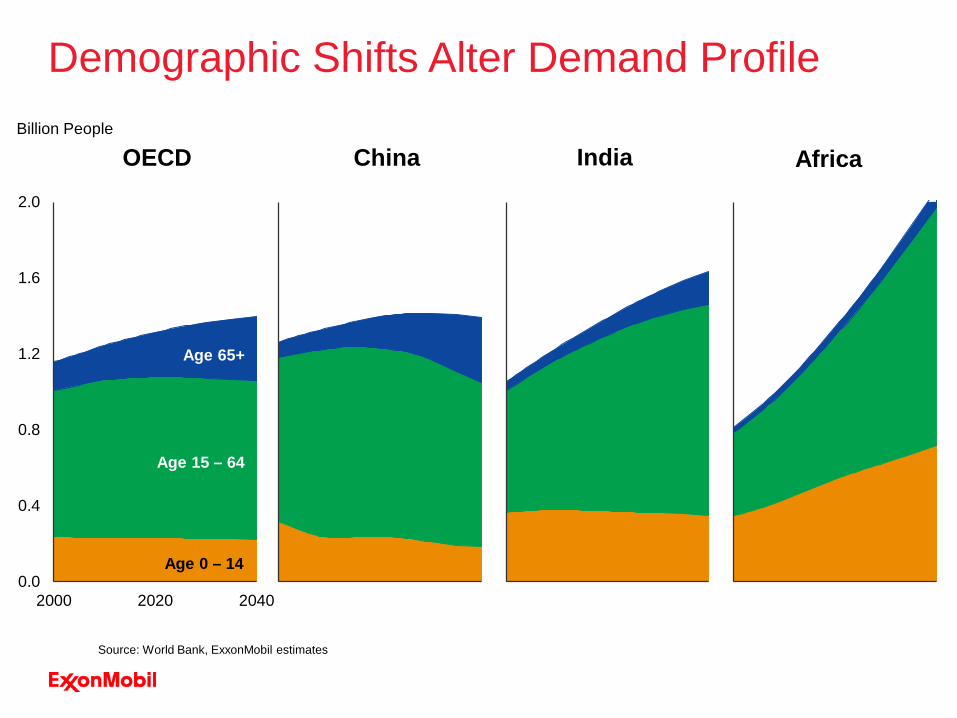

Developing Nations Lead Population Growth

Global PopulationBillion People

OECD

Non-OECD

0.0

0.4

0.8

1.2

1.6

2.0

2000 2020 20400.0

0.4

0.8

1.2

1.6

2.0

2000 2020 20400.0

0.4

0.8

1.2

1.6

2.0

2000 2020 20400.0

0.4

0.8

1.2

1.6

2.0

2000 2020 2040

Demographic Shifts Alter Demand ProfileBillion People

OECD China India Africa

Source: World Bank, ExxonMobil estimates

Age 0 – 14

Age 15 – 64

Age 65+

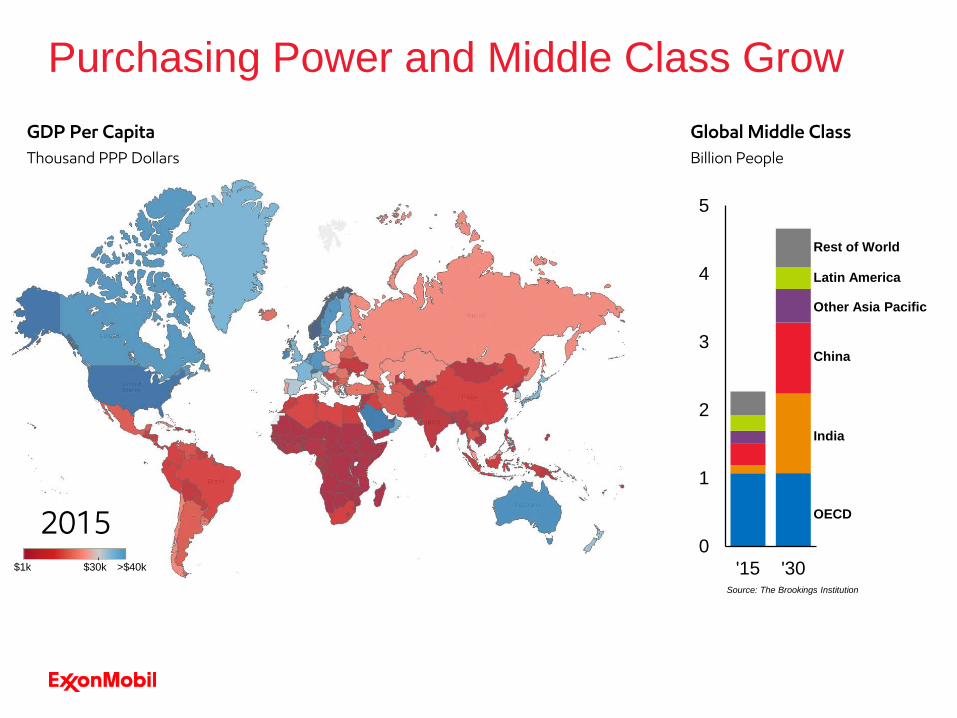

Purchasing Power and Middle Class GrowGDP Per CapitaThousand PPP Dollars

$1k $30k >$40k

China

India

Other Asia Pacific

Rest of World

OECD

Source: The Brookings Institution

0

1

2

3

4

5

'15 '30

Latin America

Global Middle ClassBillion People

20402015

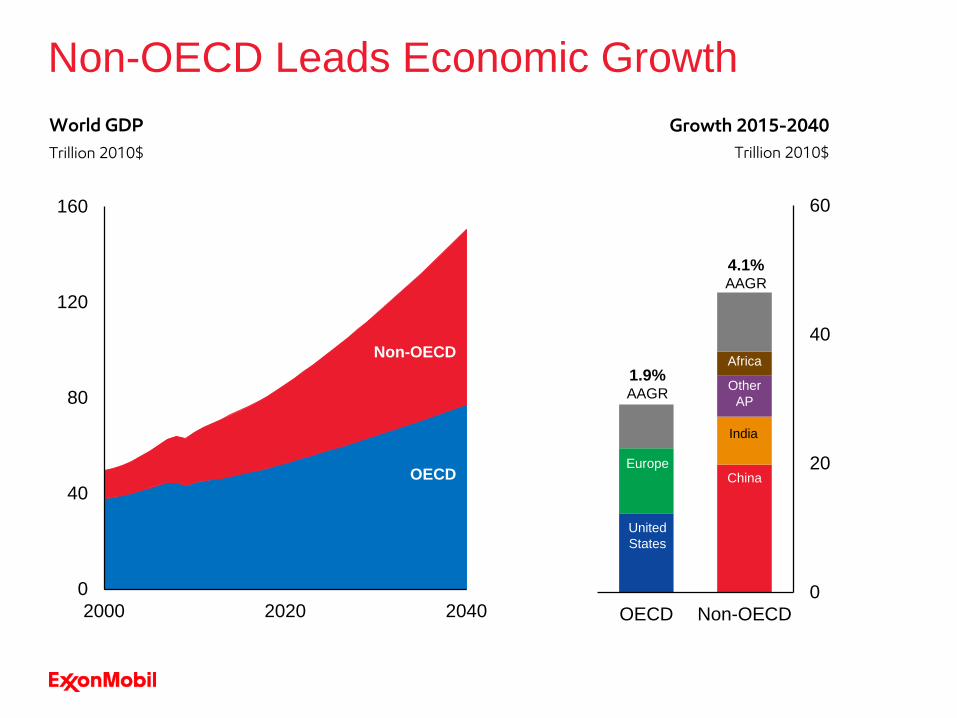

Non-OECD Leads Economic GrowthWorld GDPTrillion 2010$

0

40

80

120

160

2000 2020 2040

Non-OECD

OECD

OECD Non-OECD0

20

40

60

Growth 2015-2040Trillion 2010$

United States

China

India

1.9%AAGR

4.1%AAGR

Other AP

Africa

Europe

0

200

400

600

800

1000

1200

2000 2020 20400

200

400

600

800

1000

1200

2000 2020 20400

200

400

600

800

1000

1200

2000 2020 2040

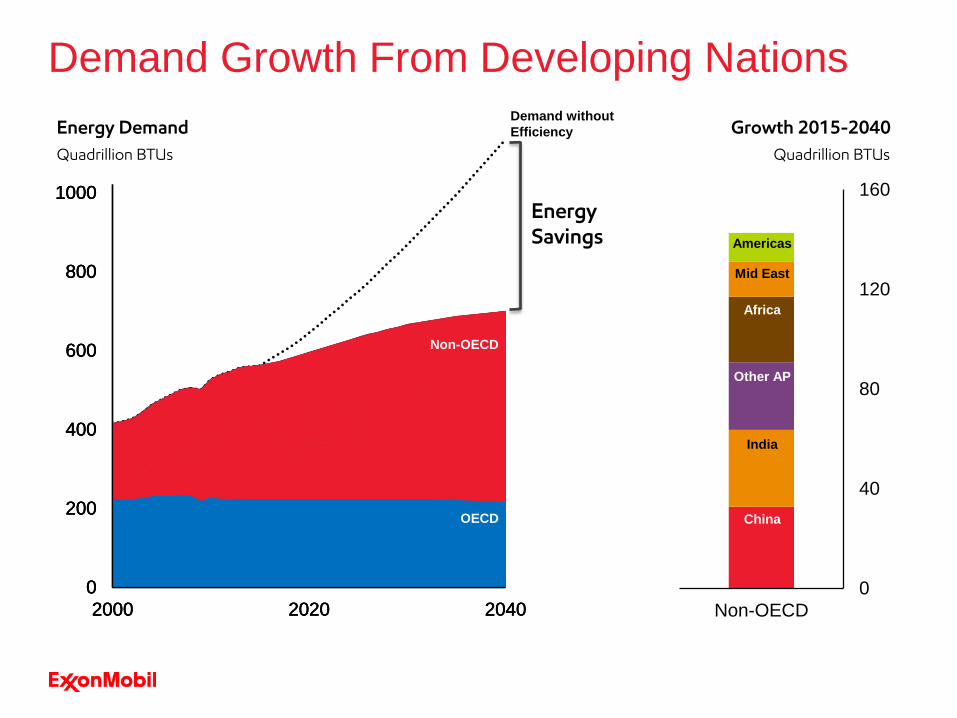

Demand

Demand Growth From Developing NationsDemand without Efficiency

Energy Savings

Energy DemandQuadrillion BTUs

OECD

Non-OECD

Non-OECD0

40

80

120

160

China

India

Other AP

Africa

Mid East

Americas

Growth 2015-2040Quadrillion BTUs

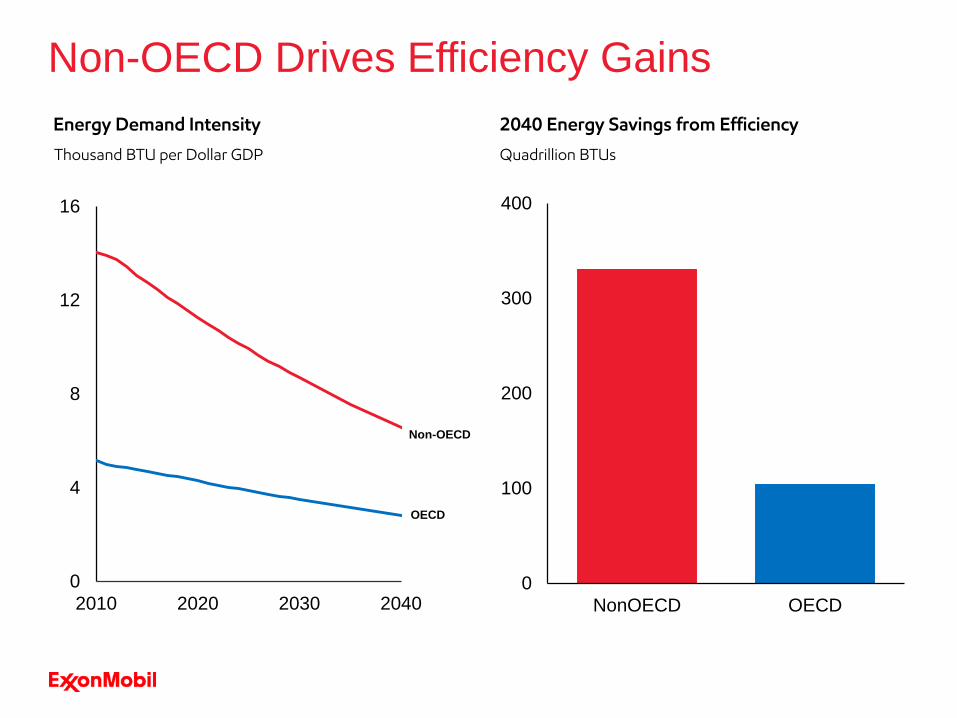

Non-OECD Drives Efficiency Gains2040 Energy Savings from Efficiency

Quadrillion BTUs

0

100

200

300

400

NonOECD OECD0

4

8

12

16

2010 2020 2030 2040

Energy Demand Intensity

Thousand BTU per Dollar GDP

OECD

Non-OECD

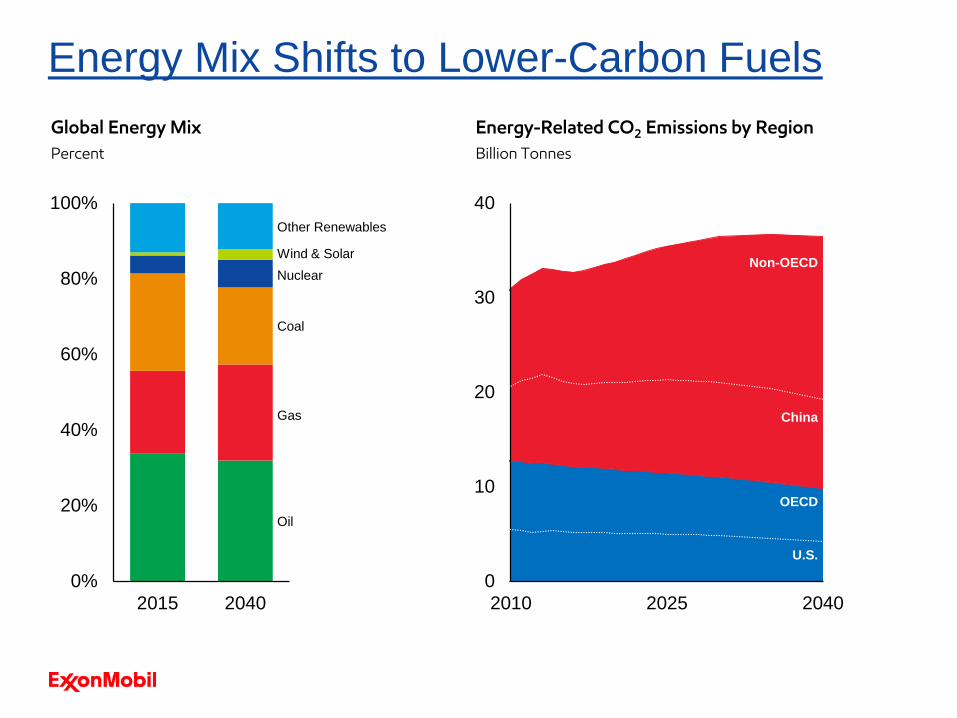

Economics and policies impact the energy mix.

Energy-Related CO2 Emissions by RegionBillion Tonnes

CO2 Emissions PlateauEnergy Mix Shifts to Lower-Carbon FuelsGlobal Energy MixPercent

0%

20%

40%

60%

80%

100%

2015 2040

Oil

Gas

Coal

NuclearWind & Solar

Other Renewables

0

10

20

30

40

2010 2025 2040

U.S.

OECD

China

Non-OECD

0.0

1.0

2.0

3.0

4.0

5.0

2000 2020 20400.0

1.0

2.0

3.0

4.0

5.0

2000 2020 2040

Billion Tonnes

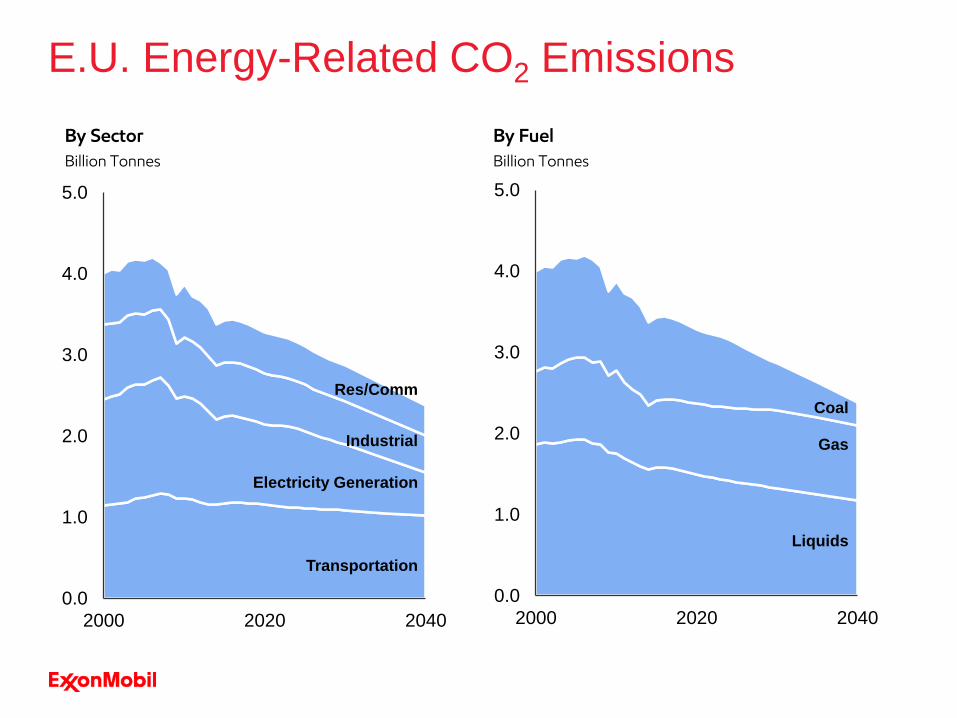

E.U. Energy-Related CO2 Emissions

Liquids

Gas

Coal

Transportation

Electricity Generation

Industrial

Res/Comm

By Sector By FuelBillion Tonnes

Oil remains the world’s primary fuel through 2040.

0

25

50

75

Transportation Industrial Res/Comm ElectricityGeneration

Transportation and Chemicals Drive Growth

0

25

50

75

Transportation Industrial Res/Comm ElectricityGeneration

Liquids Demand by Sector

MBDOE

Chem

‘15‘25

‘40

LightDuty

0

40

80

120

2000 2020 2040

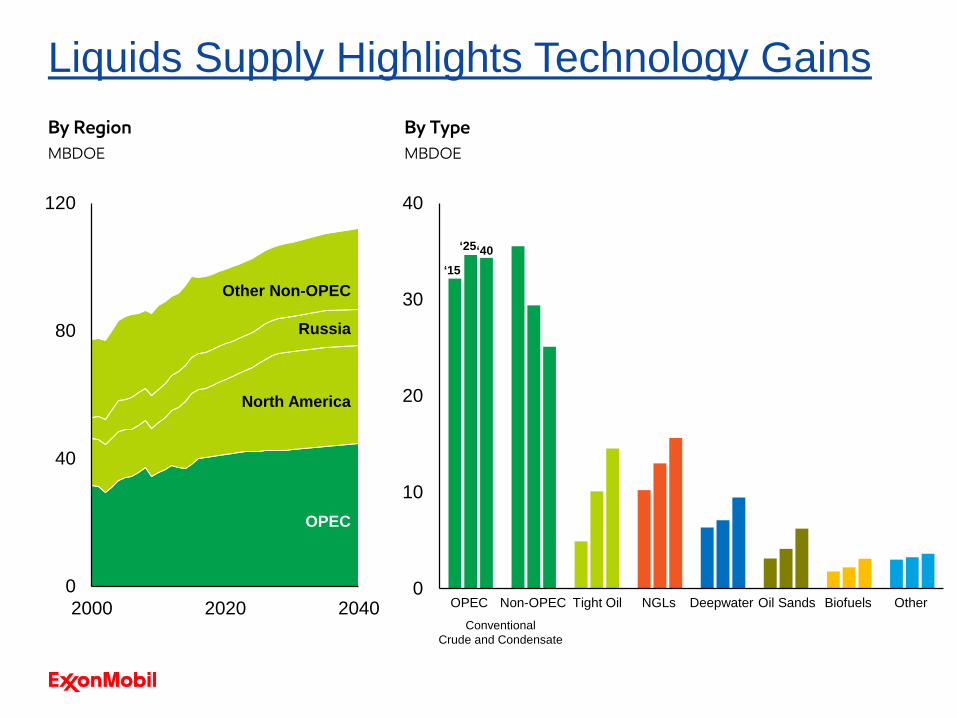

Liquids Supply Highlights Technology GainsBy RegionMBDOE

Other Non-OPEC

North America

Russia

By TypeMBDOE

OPEC

Conventional Crude and Condensate

0

10

20

30

40

OPEC Non-OPEC Tight Oil NGLs Deepwater Oil Sands Biofuels Other

‘25‘40‘15

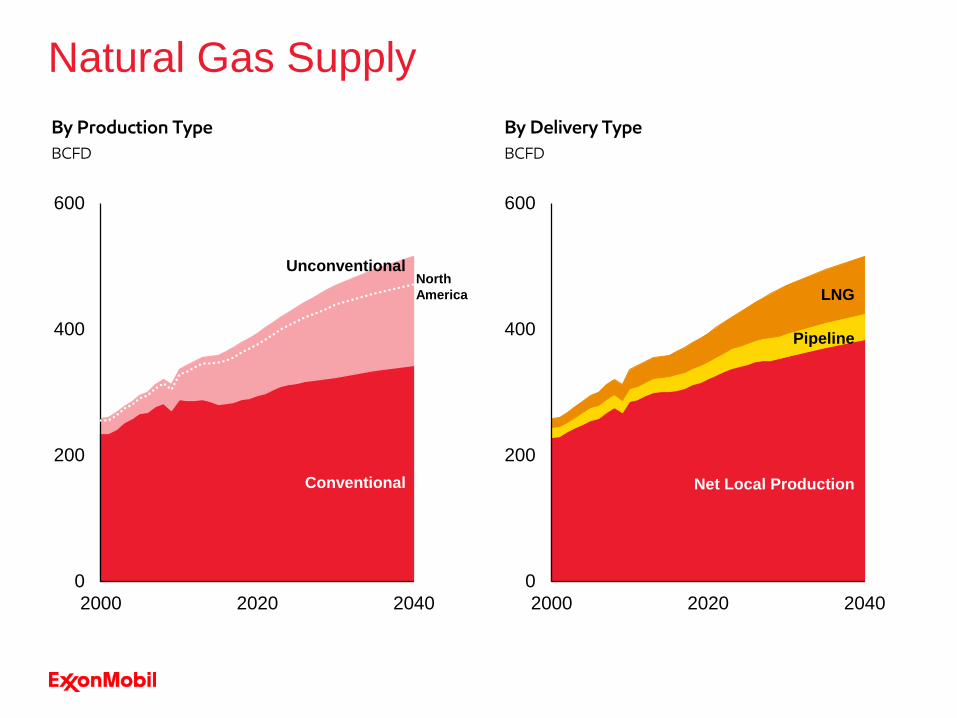

Natural gas growsmore than any otherenergy source.

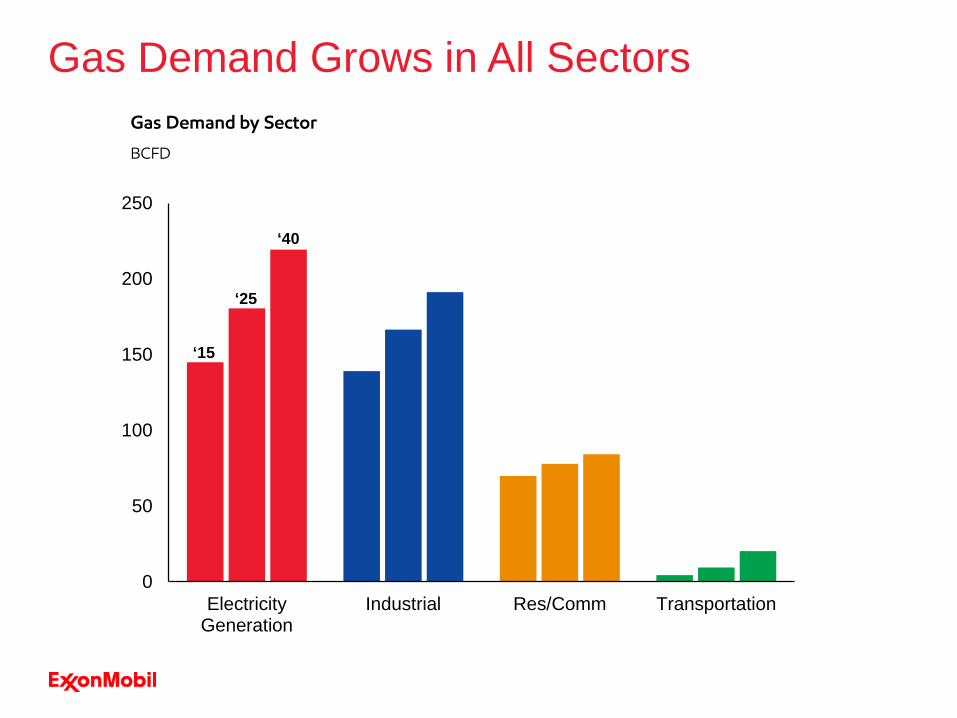

Gas Demand Grows in All Sectors

0

50

100

150

200

250

ElectricityGeneration

Industrial Res/Comm Transportation

Gas Demand by Sector

BCFD

‘15

‘25

‘40

0

2

4

6

8

10

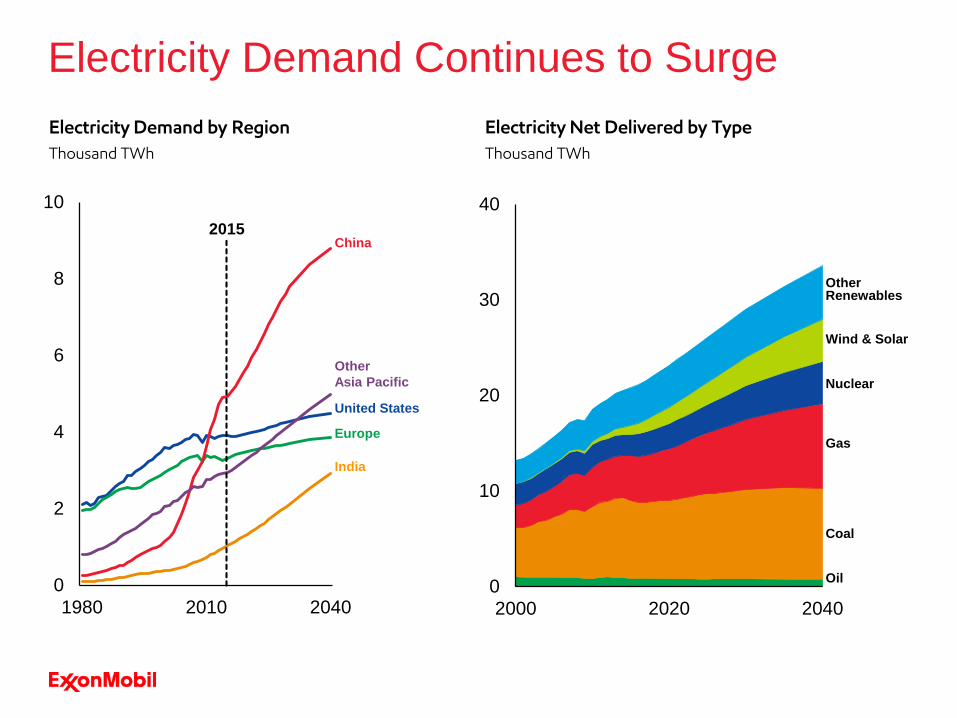

1980 2010 2040

Electricity Demand by RegionThousand TWh

United States

India

Europe

China

OtherAsia Pacific

2015

Electricity Demand Continues to Surge Electricity Net Delivered by TypeThousand TWh

0

10

20

30

40

2000 2020 2040

Oil

Coal

Nuclear

OtherRenewables

Gas

Wind & Solar

0

200

400

600

2000 2020 2040

Natural Gas Supply

0

200

400

600

2000 2020 2040

By Delivery TypeBCFD

Unconventional

Conventional

By Production TypeBCFD

Pipeline

Net Local Production

LNGNorthAmerica

Transportation

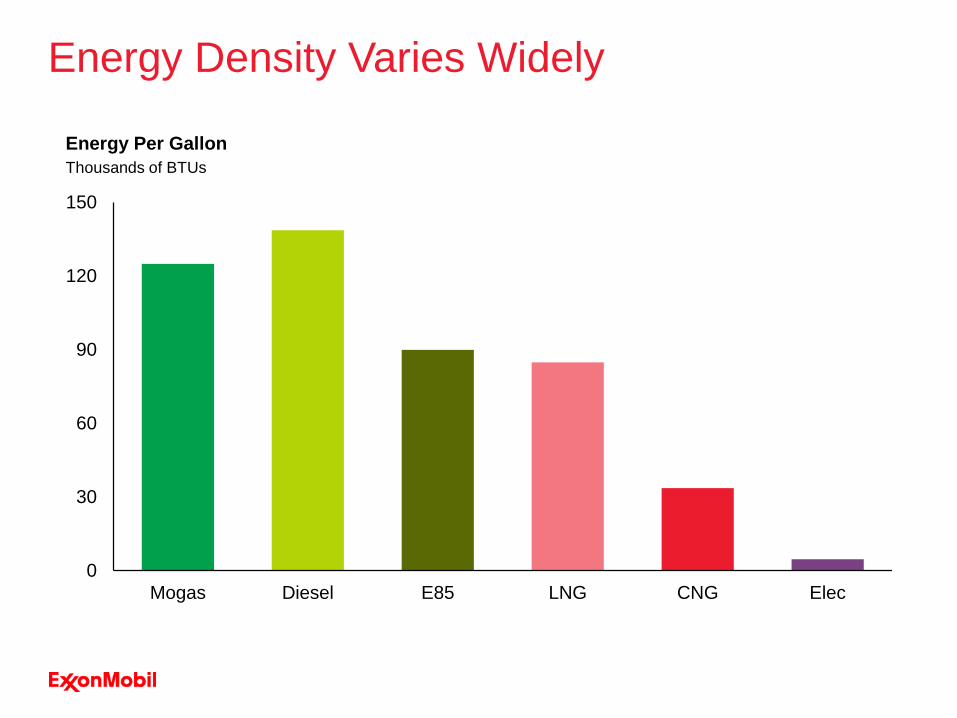

Energy Density Varies Widely

0

30

60

90

120

150

Mogas Diesel E85 LNG CNG Elec

Thousands of BTUsEnergy Per Gallon

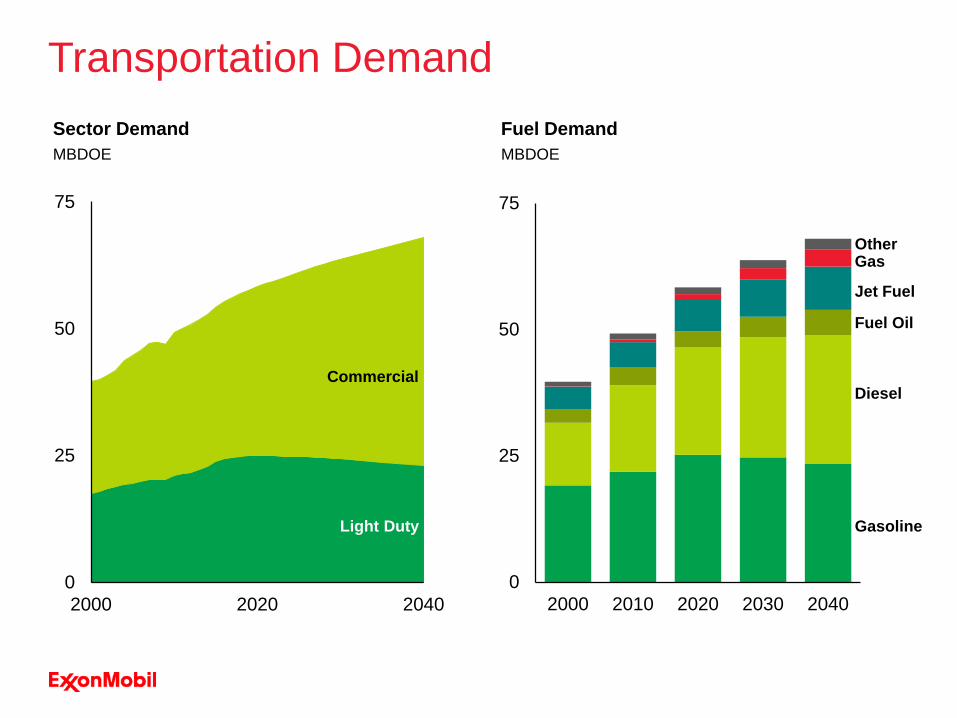

Sector DemandMBDOE

Transportation Demand

0

25

50

75

2000 2020 2040

Light Duty

Commercial

0

25

50

75

2000 2010 2020 2030 2040

Gasoline

Diesel

Fuel Oil

Jet Fuel

GasOther

Fuel DemandMBDOE

0

10

20

30

2000 2020 20400

10

20

30

2000 2020 20400

10

20

30

2000 2020 2040

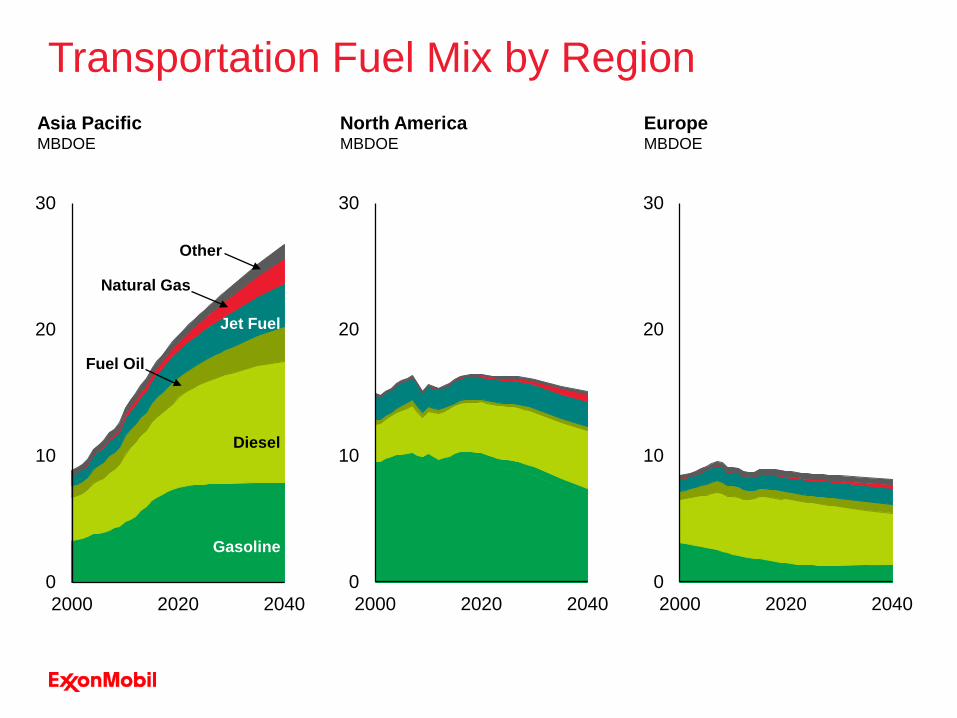

Transportation Fuel Mix by RegionAsia PacificMBDOE

Diesel

Gasoline

Jet Fuel

Fuel Oil

Other

Natural Gas

North AmericaMBDOE

EuropeMBDOE

0

5

10

15

20

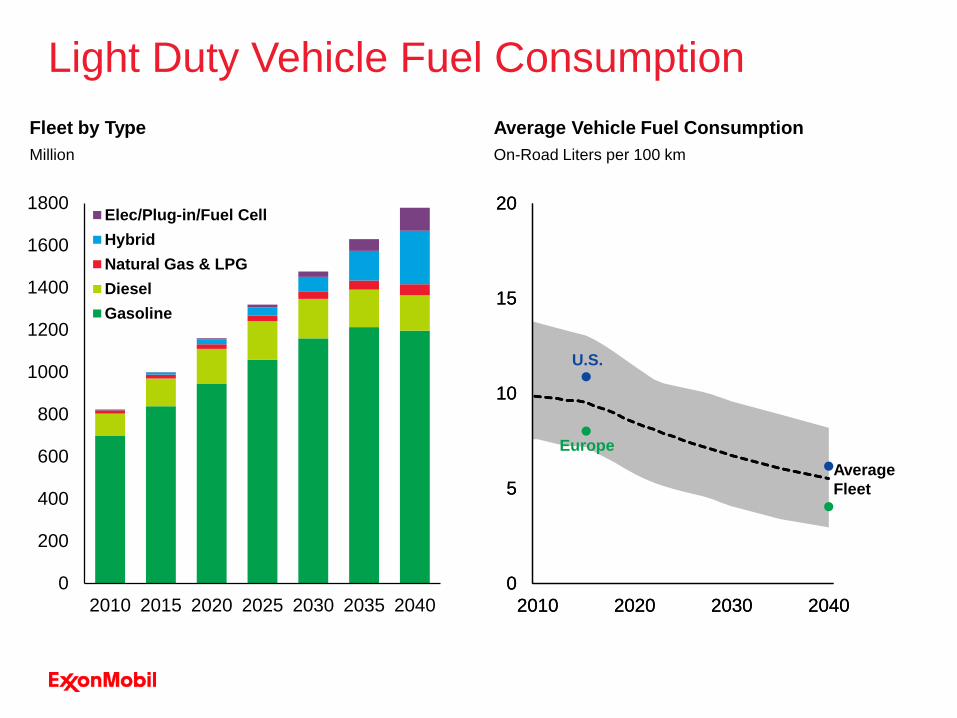

2010 2020 2030 2040

Average Vehicle Fuel ConsumptionOn-Road Liters per 100 km

Average Fleet

Light Duty Vehicle Fuel ConsumptionFleet by TypeMillion

0

5

10

15

20

2010 2020 2030 2040

U.S.

Europe

0

200

400

600

800

1000

1200

1400

1600

1800

2010 2015 2020 2025 2030 2035 2040

Elec/Plug-in/Fuel CellHybridNatural Gas & LPGDieselGasoline

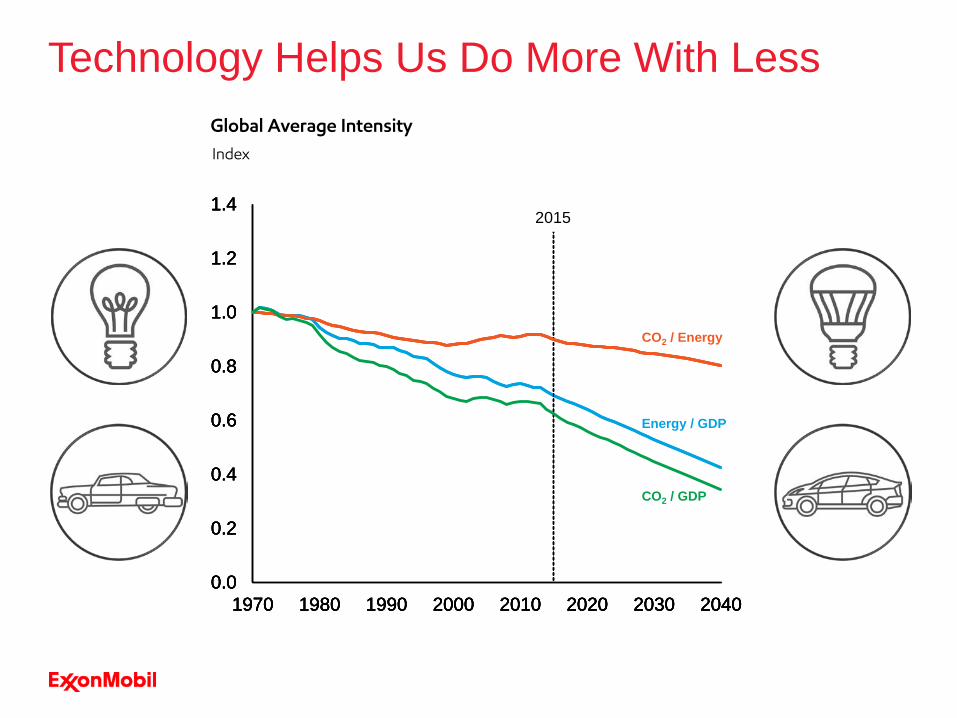

Technology has thehighest potential and greatest uncertainty.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1970 1980 1990 2000 2010 2020 2030 20400.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1970 1980 1990 2000 2010 2020 2030 20400.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1970 1980 1990 2000 2010 2020 2030 20400.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1970 1980 1990 2000 2010 2020 2030 2040

Technology Helps Us Do More With LessGlobal Average IntensityIndex

2015

Energy / GDP

CO2 / Energy

CO2 / GDP

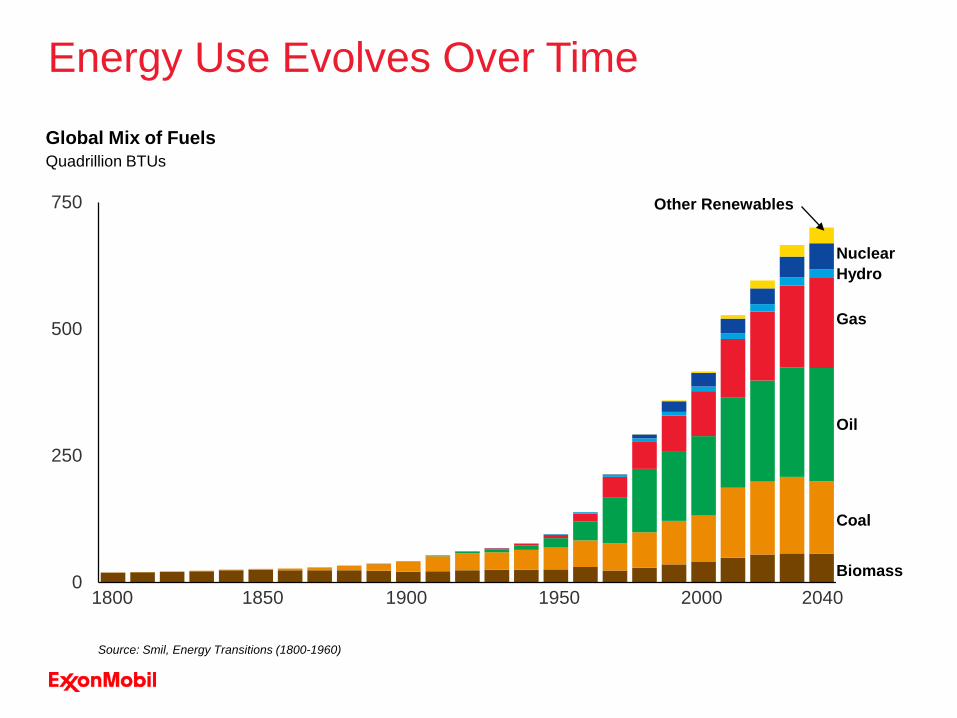

0

250

500

750

Energy Use Evolves Over Time

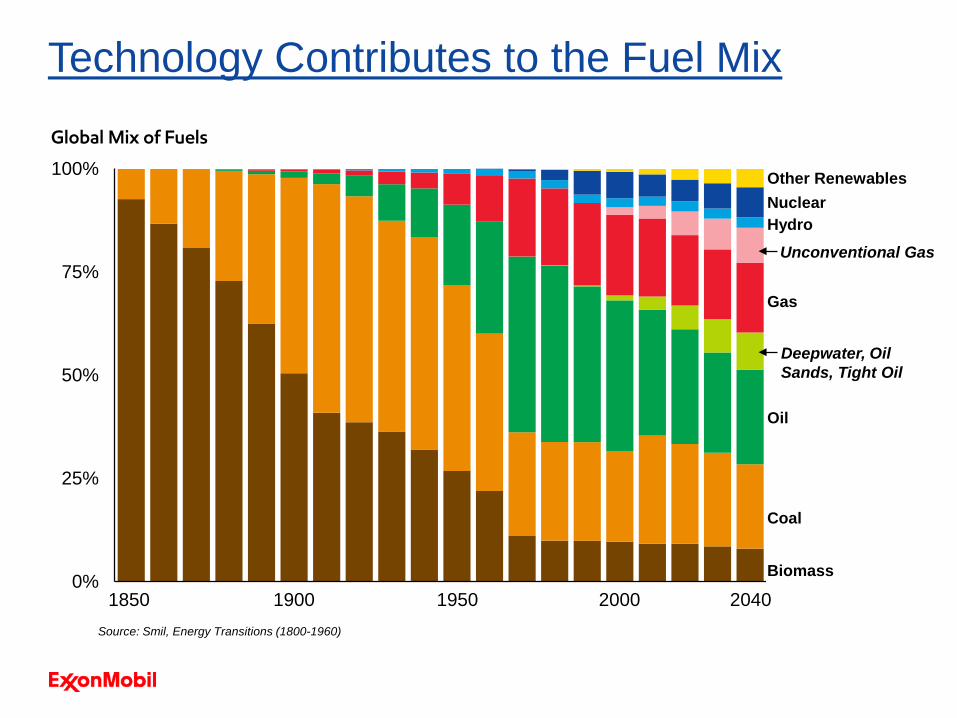

Quadrillion BTUsGlobal Mix of Fuels

1800 1900 20001850 1950Biomass

Coal

Oil

Gas

HydroNuclear

Other Renewables

2040

Source: Smil, Energy Transitions (1800-1960)

0%

25%

50%

75%

100%

Technology Contributes to the Fuel MixGlobal Mix of Fuels

1850 1900 20001950Biomass

Coal

Oil

Gas

HydroNuclearOther Renewables

2040Source: Smil, Energy Transitions (1800-1960)

Unconventional Gas

Deepwater, Oil Sands, Tight Oil

For more information, visit exxonmobil.com/energyoutlookor download the ExxonMobil app

DOMANDE?

What Public and Government Affairs(P&GA) is about

• Support Sr. Management and Business Lines in dealing with/managing increasingly complex relations with the external world• Governments • Institutions (National / International)• Opinion Leaders/Makers• Media• Public Opinion• Communities• Employees• Clients• Shareholders

P&GA main roles

• Issues Mgmt/Advocacy and Government Relations to promote and protect business interests• Company P&GA Mgr, Washington & Brussels Offices, International

Government Relations, Issues Mgmt & Advocacy COE

• Communications (including Media Relations, Corporate Advertising, Branding, Corporate Citizenship, Opinion Leaders Relations) to promote and protect corporate values and reputation• Corporate P&GA COE

• Community Investments to promote and protect “licence to operate” in areas where we have or plan to have operations• ExxonMobil Foundation

• Consequential impact on ExxonMobil and either

Major political (legislative or regulatory) dimensionor

Publicly controversial problem or solution• Issues not meeting these criteria (e.g. permitting) may be worked directly by businesses

What is a Public Policy Issue?

• Ensure timely issues identification• Prioritize & Resource issues appropriately • Speak with a single voice within an approved strategy • Assure alignment across the functions • Steward results

Purpose of Issue Management Process

• Public & Government Affairs (Corporate, Functional, Country):− Process managers and “secretariat” − Responsible for development and dissemination of best practices

• Issue ownership is primarily a line responsibility to ensure alignment with business needs− Other departments may, by exception, own issues with cross-functional dimensions

• Issue lists are the primary means of tracking and prioritizing issues• Regulatory Development monitored by dedicated Steering Committee process (RDSC)

Principles

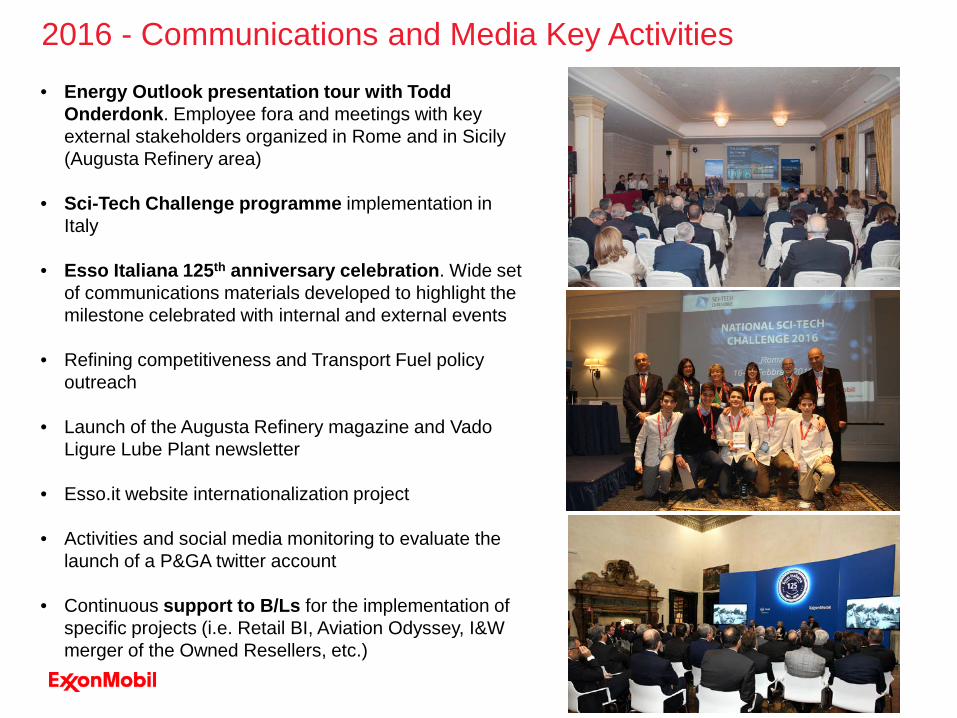

• Energy Outlook presentation tour with Todd Onderdonk. Employee fora and meetings with key external stakeholders organized in Rome and in Sicily (Augusta Refinery area)

• Sci-Tech Challenge programme implementation in Italy

• Esso Italiana 125th anniversary celebration. Wide set of communications materials developed to highlight the milestone celebrated with internal and external events

• Refining competitiveness and Transport Fuel policy outreach

• Launch of the Augusta Refinery magazine and VadoLigure Lube Plant newsletter

• Esso.it website internationalization project

• Activities and social media monitoring to evaluate the launch of a P&GA twitter account

• Continuous support to B/Ls for the implementation of specific projects (i.e. Retail BI, Aviation Odyssey, I&W merger of the Owned Resellers, etc.)

Proprietary

2016 - Communications and Media Key Activities

2016 – Key external events

• February 16-17 – National Sci-Tech Challenge

• April 20-22 – Energy Outlook presentation tour (Rome, Augusta)

• September 13/14 – VGR conference on Industrial Risks (Rome)

• September 27 - ATI conference on High Efficiency Low Emissions (Milan)

• October 05 - Round table on Transport Policy in cooperation with AREL (Rome)

• October 20 - RCS Corriere Innovazione Energy event (Venice)

• November 8 - IBL annual dinner (Milan)

• November 30 - 1st AIEE Energy Symposium on Current and Future Challenges to Energy

Security (Milan, 30 November-2 December)

• November 23 – Esso Italiana 125 Years Anniversary - (Rome)

• Several lectures at key Universities and post-graduate masters

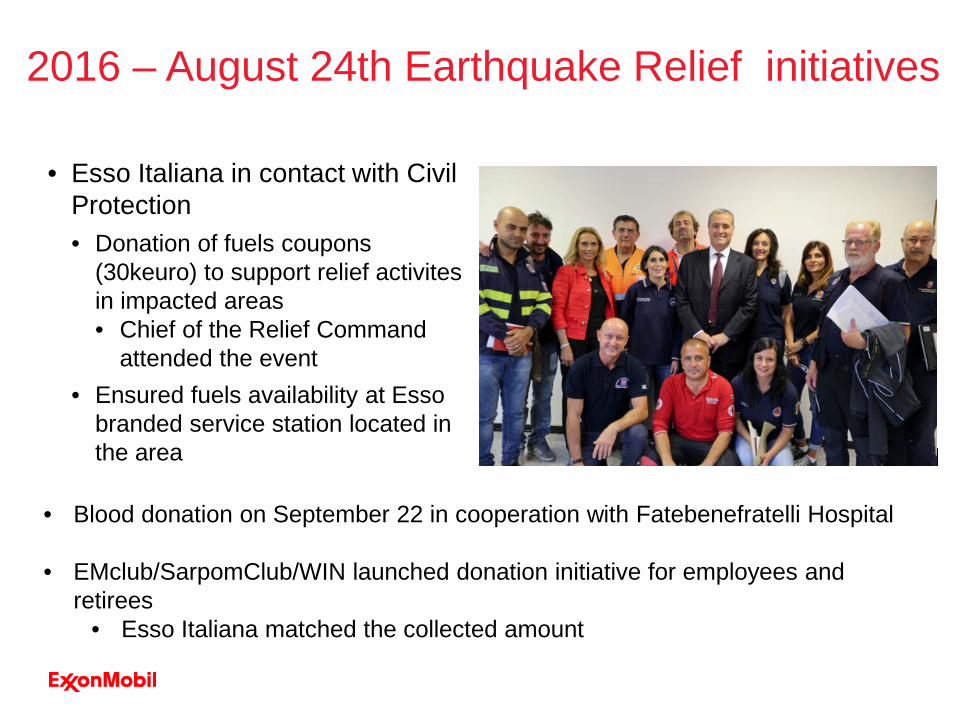

• Esso Italiana in contact with Civil Protection • Donation of fuels coupons

(30keuro) to support relief activites in impacted areas• Chief of the Relief Command

attended the event • Ensured fuels availability at Esso

branded service station located in the area

2016 – August 24th Earthquake Relief initiatives

• Blood donation on September 22 in cooperation with Fatebenefratelli Hospital

• EMclub/SarpomClub/WIN launched donation initiative for employees and retirees

• Esso Italiana matched the collected amount

• Sci-Tech Challenge 2016-2017 cycle• ~ 950 students of 10 schools from Naples, Novara, Savona, Siracuse and Rome involved• 18 classroom visits held by company volunteers from Augusta, Vado Ligure, Naples, Rome and

SARPOM Refinery. • Several B/Ls involved: R&S, Midstream, Retail, P&GA• 50 students to participated in the National Challenge (Rome, February 20-21, 2017)• Integrated communication strategy with JA include traditional and digital media, internal comms

• Energy Outlook roll-out in April – Todd Onderdonk tour. Engagements under consideration:• Employee forum at Rome HQ• External event with key stakeholders• Face to face meeting with Ministry of Economic Development representatives

• Speakers Coalition• 16 in-country trained and active members• Continuous identification of speaking opportunities: average of 20/25 speeches/educational

lectures per year given; focus on Energy Outlook, ExxonMobil in Italy, Refining Competitiveness, Transport Fuel policies

• Crisis Communications Media Training• Yearly session for supervisors/middle management

2017 – Communications and Media Key Activities

• Refining competitiveness outreach plan update and integration with initiatives topromote EM view on low-emission mobility

• Ongoing support to BLs for proactive/reactive communication needs related to the implementation of their business projects

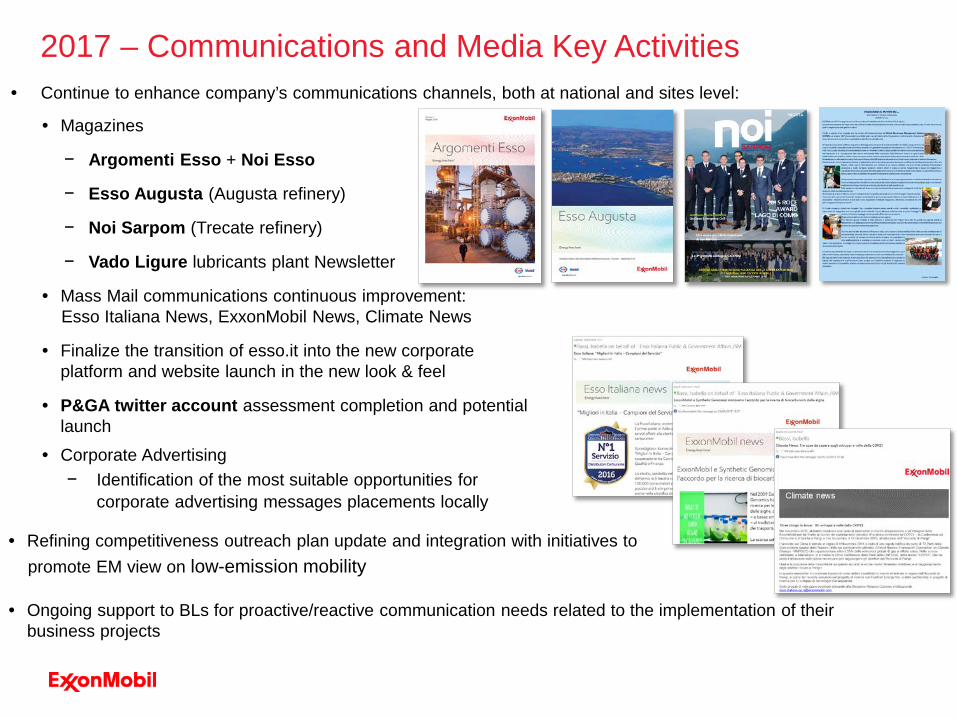

• Magazines

− Argomenti Esso + Noi Esso

− Esso Augusta (Augusta refinery)

− Noi Sarpom (Trecate refinery)

− Vado Ligure lubricants plant Newsletter

• Mass Mail communications continuous improvement: Esso Italiana News, ExxonMobil News, Climate News

• Finalize the transition of esso.it into the new corporate platform and website launch in the new look & feel

• P&GA twitter account assessment completion and potentiallaunch

• Corporate Advertising− Identification of the most suitable opportunities for

corporate advertising messages placements locally

2017 – Communications and Media Key Activities• Continue to enhance company’s communications channels, both at national and sites level:

Best Practices in External Affairs (BPEA)

Community Engagement: A Global Best Practices Model

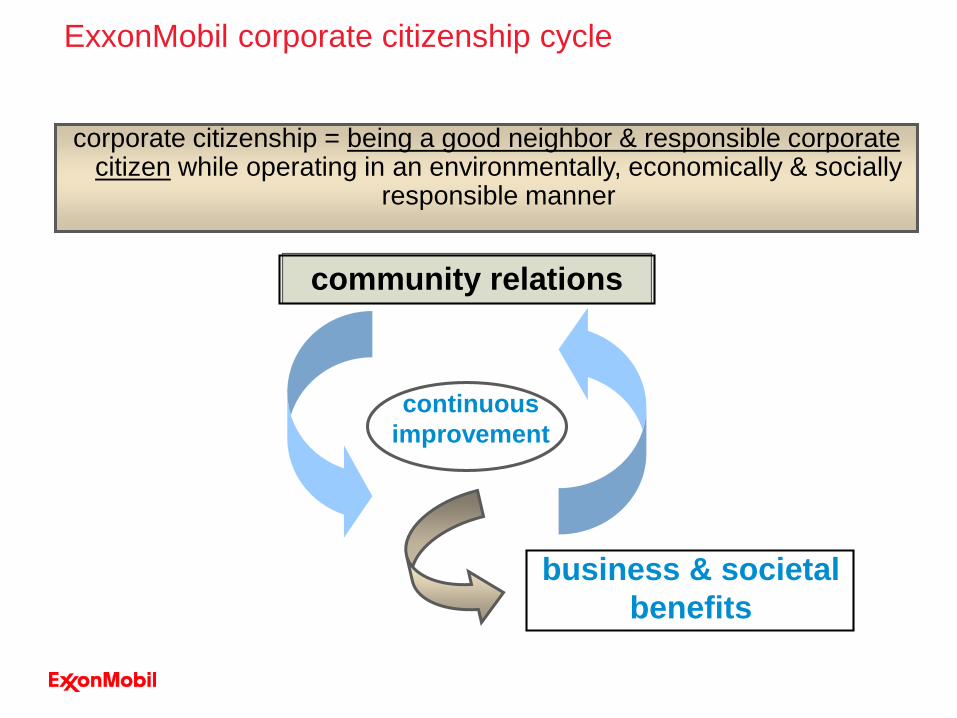

ExxonMobil corporate citizenship cycle

corporate citizenship = being a good neighbor & responsible corporate citizen while operating in an environmentally, economically & socially

responsible manner

continuous improvement

business & societal benefits

community relations

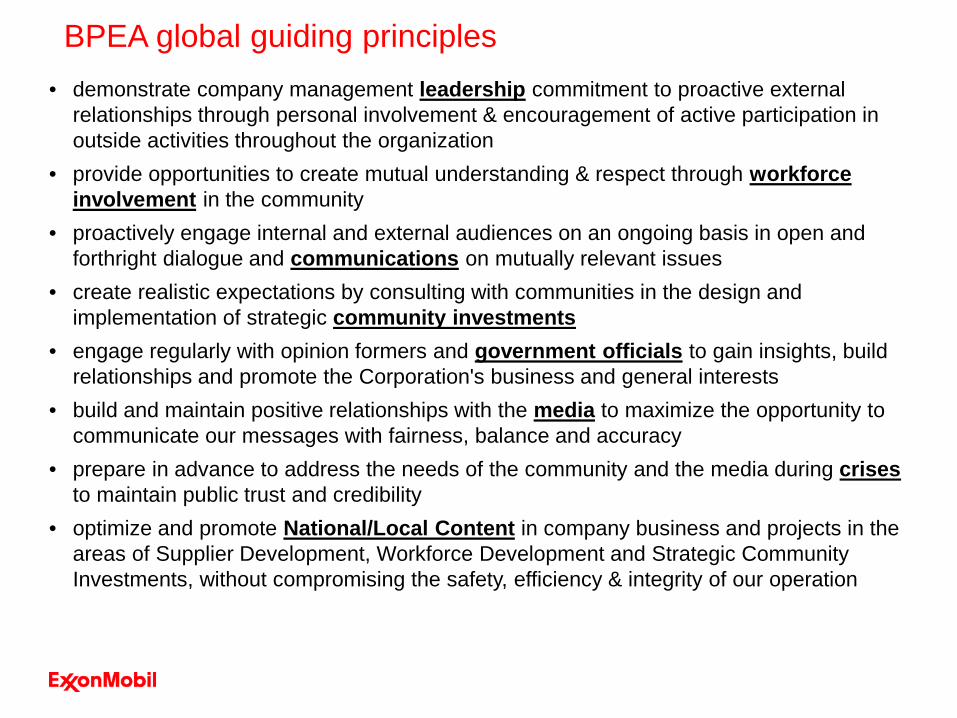

BPEA global guiding principles• demonstrate company management leadership commitment to proactive external

relationships through personal involvement & encouragement of active participation in outside activities throughout the organization

• provide opportunities to create mutual understanding & respect through workforce involvement in the community

• proactively engage internal and external audiences on an ongoing basis in open and forthright dialogue and communications on mutually relevant issues

• create realistic expectations by consulting with communities in the design and implementation of strategic community investments

• engage regularly with opinion formers and government officials to gain insights, build relationships and promote the Corporation's business and general interests

• build and maintain positive relationships with the media to maximize the opportunity to communicate our messages with fairness, balance and accuracy

• prepare in advance to address the needs of the community and the media during crisesto maintain public trust and credibility

• optimize and promote National/Local Content in company business and projects in the areas of Supplier Development, Workforce Development and Strategic Community Investments, without compromising the safety, efficiency & integrity of our operation

Assessment result: workforce involvement

A = Leadership support & involvementB = Employees as community ambassadorsC = Focus on areas of importance to the communityD = Community awareness of volunteer activitiesE = Employee morale, loyalty & teamwork

0123

4A

B

CD

E

Current

Desired

Guiding Principle & Action Plans Add’l Budget

($k)

Add’l Staff Effort FTE

(wks)

Who When

WORKFORCE INVOLVEMENT: Provide opportunities to create mutualunderstanding & respect through workforce volunteer involvement in the community.

Enhance communication to LMT about initiatives towards community to foster workforce involvement.

Continue encouraging employees speeches on key Company messages to schools and local communities providing background material

Evaluate initiatives to allow/facilitate employees ambassador program

BPEA assessment process

Initiate a Feedback MechanismMaintain & optimize operations

Institute Verification & Measurement of Action Plan activities & results

Develop & implement a BPEA or External Affairs Plan based on Guiding Principle Action Plans

Assess Current & Desired levels of performance for each Guiding Principle & identify any gaps

Determine business needs, incorporating relevant & practicable community needs & expectations

Community Needs Assessment

Metrics assessments, spider charts, Action Plans & Gap Prioritization

Business Needs Assessment

BPEA or External Affairs Plan with incremental costs, Roles & Responsibilities & timing for gap closure

Documented results (Community Needs Survey, Media Trend Analysis, Program Evaluations)

BPEA or External Affairs PlanRepeat full BPEA cycle every year

Steps OutputsConsult with our primary external stakeholders to

understand their needs & expectations

BACK_UP

Adriatic LNG

80

Overview

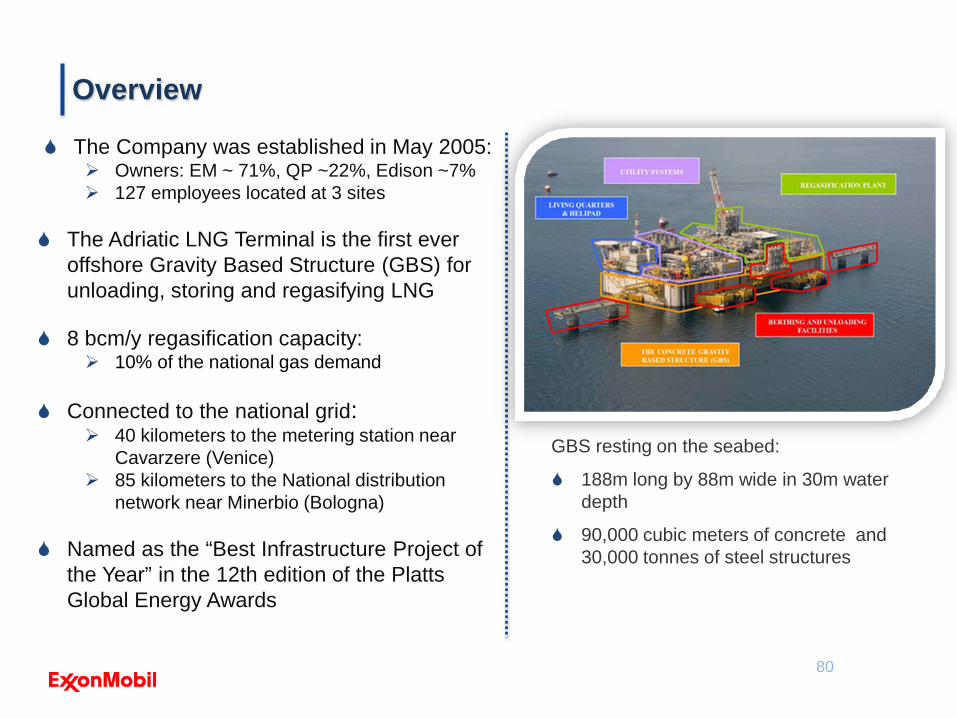

The Company was established in May 2005: Owners: EM ~ 71%, QP ~22%, Edison ~7% 127 employees located at 3 sites

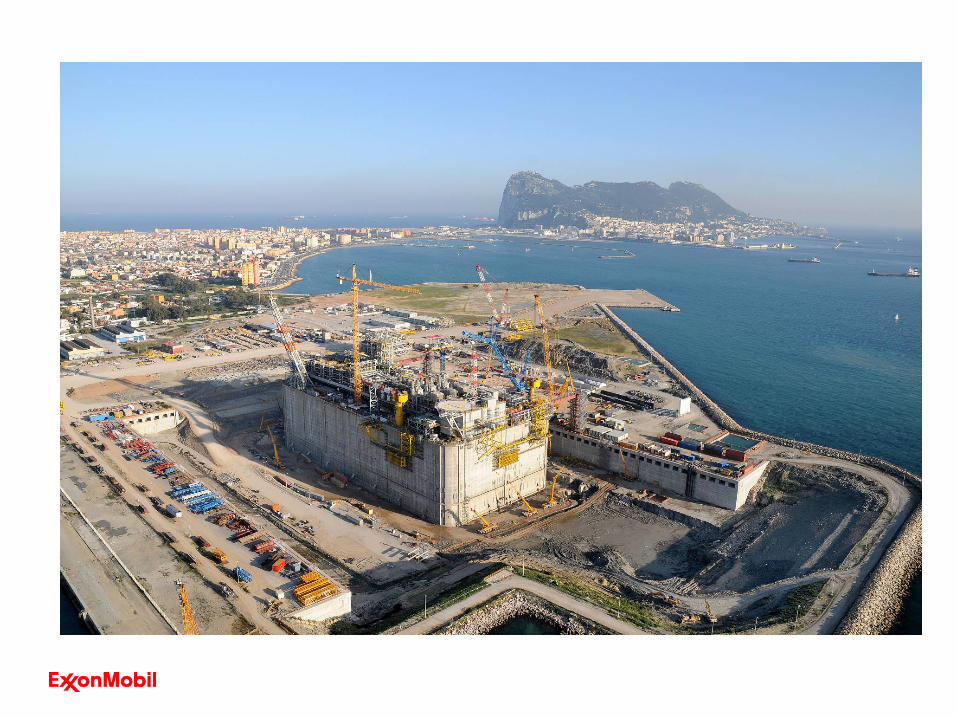

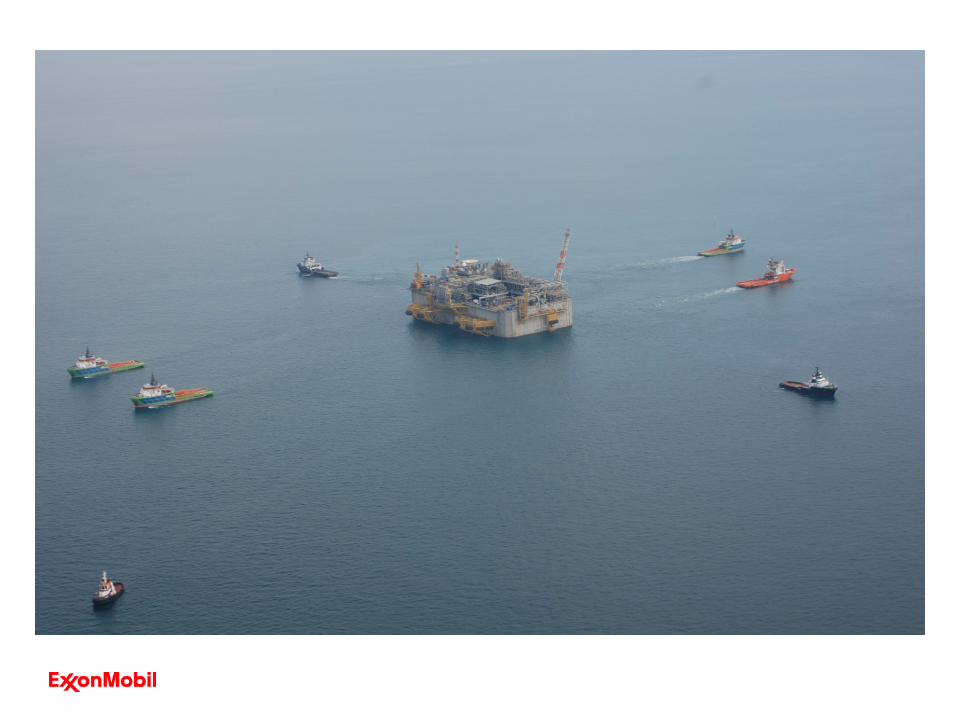

The Adriatic LNG Terminal is the first ever offshore Gravity Based Structure (GBS) for unloading, storing and regasifying LNG

8 bcm/y regasification capacity: 10% of the national gas demand

Connected to the national grid: 40 kilometers to the metering station near

Cavarzere (Venice) 85 kilometers to the National distribution

network near Minerbio (Bologna)

Named as the “Best Infrastructure Project of the Year” in the 12th edition of the PlattsGlobal Energy Awards

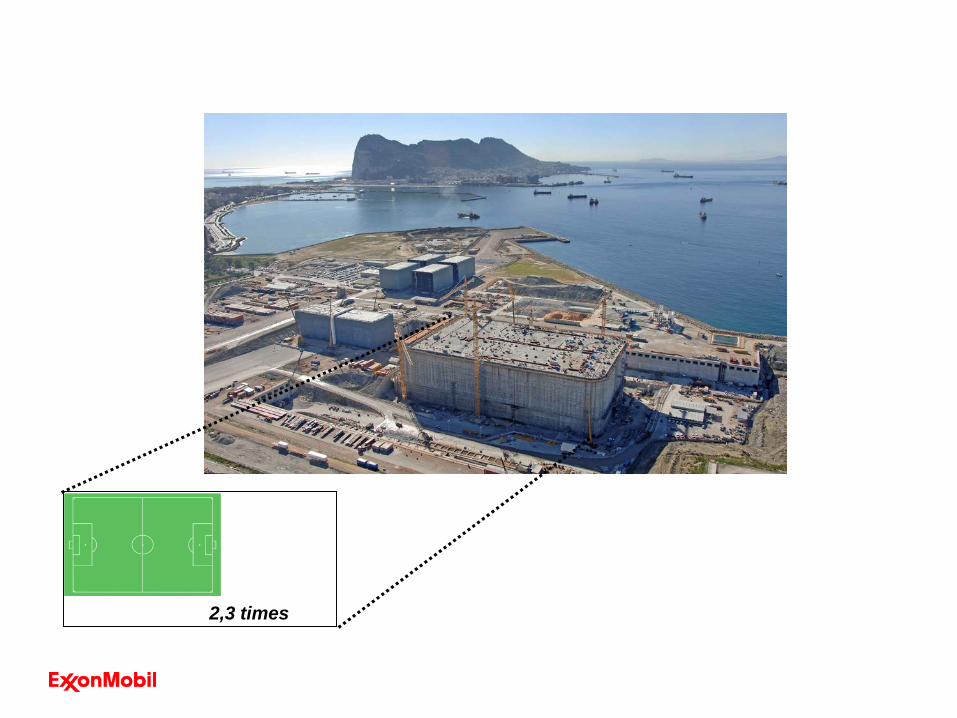

GBS resting on the seabed:

188m long by 88m wide in 30m water depth

90,000 cubic meters of concrete and 30,000 tonnes of steel structures

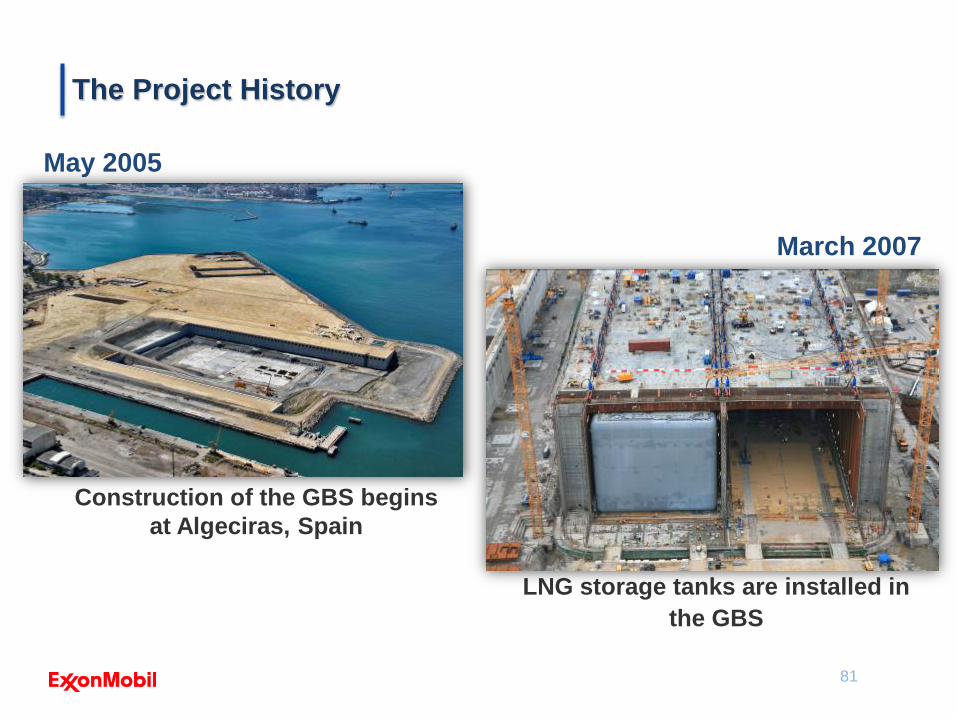

May 2005

March 2007

Construction of the GBS begins at Algeciras, Spain

LNG storage tanks are installed in the GBS

The Project History

81

2,3 times

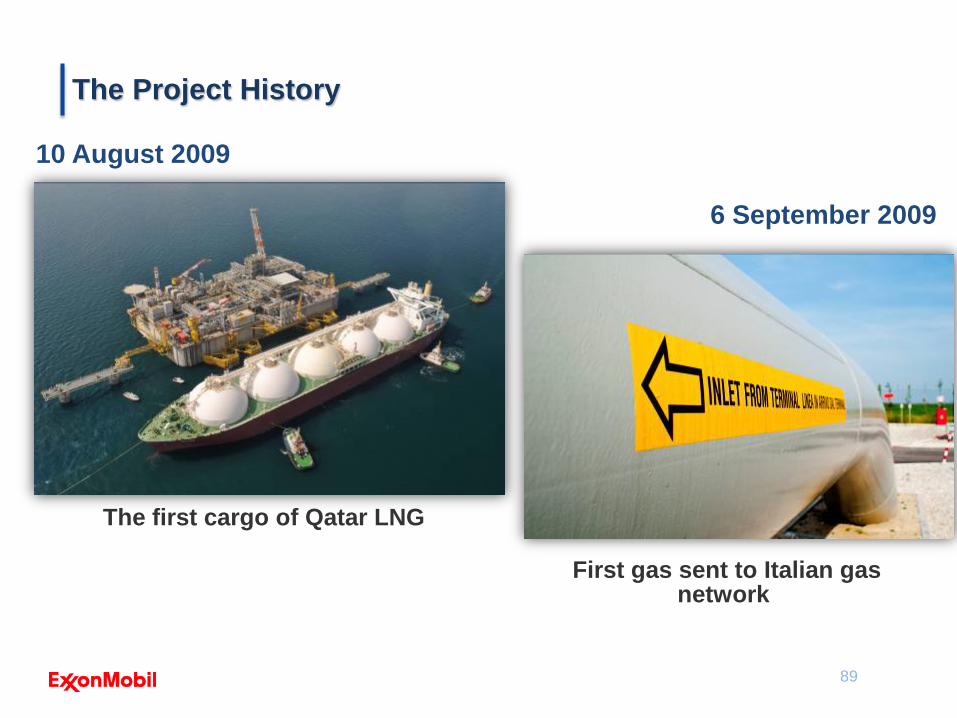

The first cargo of Qatar LNG

10 August 2009

6 September 2009

First gas sent to Italian gas network

89

The Project History

Global Project

Project activity in over seventeen locations in twelve countries

GBS Construction SiteAlgeciras, Spain

LNG TanksUS, Canada, UK, South Korea

Mooring DolphinsVenice, Italy

VaporizerJapan

TopsidesSpain

Loading ArmsFranceLiving Quarters

Sweden

GBS & Mooring StructureNorway

90

81

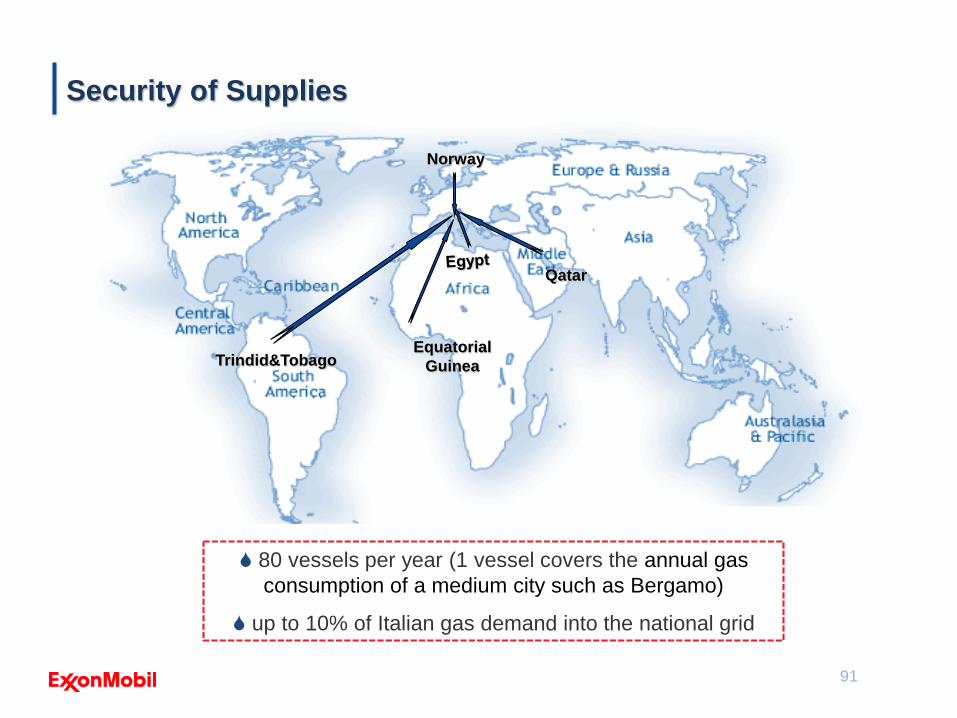

Norway

Qatar

Equatorial GuineaTrindid&Tobago

91

Norway

80 vessels per year (1 vessel covers the annual gas consumption of a medium city such as Bergamo)

up to 10% of Italian gas demand into the national grid

Security of Supplies