Public Financing Strategies to Leverage Private … Bartsch NALGEP tax...• Former metal scrap yard...

33

Public Financing Strategies to Leverage Private Investment in Brownfields: Focus on Tax Incentives Charlie Bartsch Senior Program Advisor for Economic Development US Environmental Protection Agency NALGEP Workshop RTM Sustainable Property Transaction Conference/Philadelphia October 8, 2014

Transcript of Public Financing Strategies to Leverage Private … Bartsch NALGEP tax...• Former metal scrap yard...

Public Financing Strategies to

Leverage Private Investment in

Brownfields: Focus on Tax

Incentives

Charlie BartschSenior Program Advisor for Economic Development

US Environmental Protection Agency

NALGEP Workshop

RTM Sustainable Property Transaction Conference/Philadelphia

October 8, 2014

• Uncle Sam’s tool box…most appropriate federal

tax incentives to link to brownfields

• Quick flavor of types of supportive state tax

incentives…what can complement, layer with

federal programs?

• Sneak peak at a key finding from a

new EPA study…with potential

impact on TIFs

• Examples along the way…

What this discussion will cover…

Increase project’s internal rate of return

Ease borrower’s cash flow by freeing up

cash ordinarily needed for tax payments

Some credits can be sold for cash, or

syndicated to attract additional capital

investment

Not subject to competitive public grant

process

Financial Advantages of Using Tax Incentives in Brownfield Projects

Credits attract different players

to the redevelopment table

Offset additional pre-development or site

preparation costs of site reuse/in-fill projects

Encourage private investment in sync with

local plans that promote brownfield

revitalization

Social/Community Advantages of Using Tax Incentives in Brownfield

Projects

• Rehabilitation tax credits

• Low income housing tax

credits

• New markets tax credits

• Energy-related tax credits

Four federal tax incentives that can be linked to brownfield projects – at little or

no cost to the project….

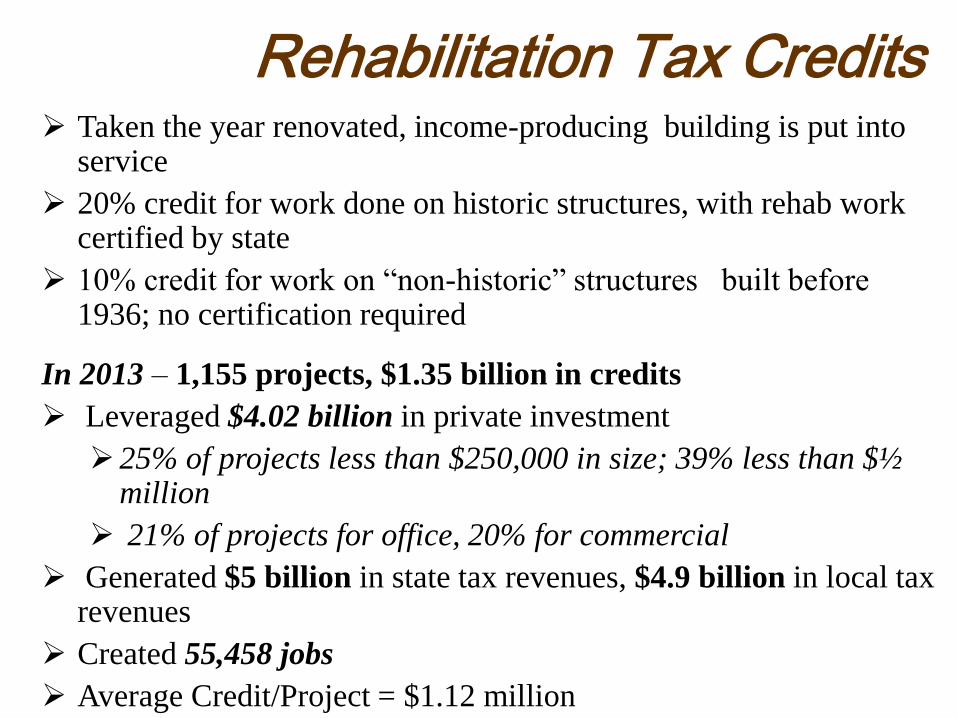

Taken the year renovated, income-producing building is put into service

20% credit for work done on historic structures, with rehab work certified by state

10% credit for work on “non-historic” structures built before 1936; no certification required

In 2013 – 1,155 projects, $1.35 billion in credits

Leveraged $4.02 billion in private investment

25% of projects less than $250,000 in size; 39% less than $½ million

21% of projects for office, 20% for commercial

Generated $5 billion in state tax revenues, $4.9 billion in local tax revenues

Created 55,458 jobs

Average Credit/Project = $1.12 million

Creative integration of energy, sustainability elements

Rehabilitation Tax Credits

Rehabilitation costs must be “substantial” –i.e., exceed minimum of $5,000 or the building’s adjusted basis

Property must be “income-producing” – multi-family rental housing can claim the 20% credit, but not the 10% credit

Rehab work must conform to state historic preservation standards – deter integration of “green” technologies

Credit is recaptured on a sliding scale (20% annually) if owner disposes of the building within five years of completing renovation

Rehabilitation Tax Credits –

caveats and “fine print”

Ford Motor Assembly Plant –Richmond CA

• Built in 1930, 520,000 sq.ft. ; closed 1953

• Original Albert Kahn “ daylight factory”

• Rehabilitation work began in 2004

– Included seismic retrofits, green

performance measures, including

solar panels on roof

• $11 million in rehab tax credits

• Today – houses several

manufacturers of sustainable

products, plus 45,000 sq ft meeting

and entertainment venue

Family Health Care – Fargo ND • Former 1920 Pence Automobile

Company renovated in 2011 to house

consolidated operations of Family

HealthCare

• $1.4 million in historic rehab tax credits

supported the $14.8 million project

• Other financing:

– $4.1 million in NMTC thru Wells

Fargo Bank

– $6.6 million HRSA facility

improvement grant

– $1.3 million from local foundations,

corporate contributors

– $2.6 million in FHC equity

Thames Street Landing – Bristol, RI• $8.3 million mixed-use redevelopment,

including housing, hotel, and offices at

a vacant downtown site

• 200-year history – buildings included

original Bank of Bristol (1797), Taylor

Store (1798) and DeWolf Warehouse

(1818); industrial uses started in 1861

• Developed in phases; banks unwilling to

provide follow-on financing until 1st

phase generated a positive cash flow

• Rehab tax credits key to generating

positive cash flow, attracting

additional private capital

• Today, project is cornerstone for historic

revitalization of Bristol waterfront

Can encourage capital investment in affordable housing on

vacant properties, brownfields, other targeted sites

Can be used to target investment to certain areas, such as

infill or distressed locations, and also to discourage sprawl

States get annual population-based allocation for

distribution to communities and non-profits – approx.

$1.75 per capita

Investors can get 9% annual credit for 10 years for qualified

new construction/rehabilitation costs (i.e. 90% of total) for

projects not financed with federal subsidy

Federal subsidy limits credit to 4%

Credits can be used for new construction, rehabilitation, or

acquisition and rehabilitation

Low-Income Housing Tax Credits

Loss of tax incentive value on secondary

market – from peak of 95 cents/$ to 75-85

cents/$ now – impacts syndication value

“Green” priority for credit allocations within states

“Difficult development areas” can get greater subsidies

Credits support a wide range of housing types/situations

Urban, suburban, rural projects

Housing for families, special needs tenants, SRO, elderly

$3.85 billion in credits issued in fiscal year 2012,

supporting 1/3 of all new construction that year

Low-Income Housing Tax Credits – fine print and caveats

Albina Corner – Portland, OR

• 3/4 acre Albina Corner is adjacent to a bus line and near a major light rail station

• Abandoned gas station, retail shop

• Small scale contaminants have deterred reuse

– Tanks, lead paint

• Site redeveloped into a mixed-use area that includes 48 units of low-income housing built over 12,000 square feet of commercial space; includes a child care center and a second floor courtyard and play lot

• LIHTCs one of 11 funding sources for the $4.4 million project

– Other include CDBG, Oregon Housing Trust, foundations

Brian J. Honan Apartments – Boston, MA

• Allston-Brighton CDC saw an

opportunity to develop former Legal

Seafoods fish processing plant into

affordable housing

• Low-income housing tax credits

key parts of financing incentive

package needed to attract capital,

convince funders that the project

would work

• Result – affordable units in a

sustainable development: green

energy, pedestrian access to

groceries, shops, transit

LIHTCs: Mifflin Mills – Lebanon, PA• Former vacant, blighted city block

near downtown

• Key concern – attracting investors to

rent-to-own project structure targeted

to moderate-income families

• Role of LIHTCs – $1.5 million in

tax credits essential to viability of

financing package

• Result – 20 units, PA’s first

affordable “rent-to-own” townhouse

community

• Energy efficient construction,

designed to blend into existing

residential neighborhood

• Gives investors federal tax credits (39% over 7 years) for equity investments in designated Community Development Entities (CDEs), for use in low-income, distressed communities

• CDEs use their allocations to make loans or investments in “qualified businesses” and development activities –

Historically, most common investments -- in for-profit, non-profit businesses and real estate

Other eligible activities include -- charter schools, homeownership projects, community facilities

All investments at preferential rates/terms

• 2014 CDE allocation applications now open

New Markets Tax Credits

$3.42 billion authorized to 87 CDEs in 32 states

Allocatees anticipate making investments in 44 states

Distribution by area type:

$2.01 billion (60%) in major urban areas

$680 million (20%) in minor urban areas

$742 million (20%) in rural areas

Planned loans to or equity investments in include:

$2.75 billion (75%) to finance/support business loans

$831 million (24%) to finance real estate projects

New Markets Tax Credits -- highlights of 2013 funding round (announced 6/5/14)

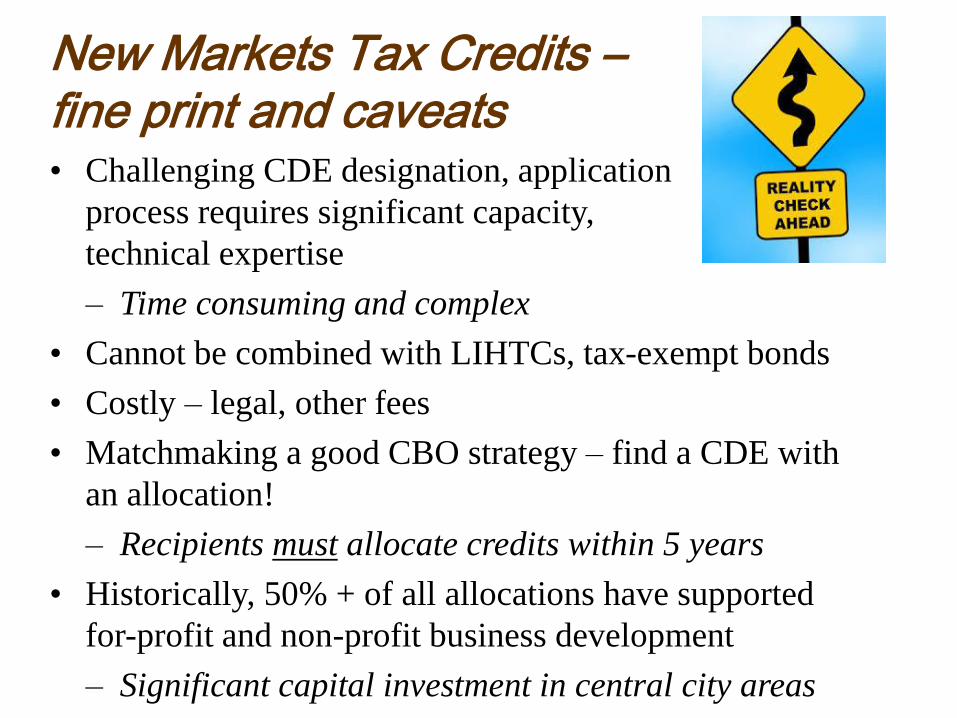

• Challenging CDE designation, application

process requires significant capacity,

technical expertise

– Time consuming and complex

• Cannot be combined with LIHTCs, tax-exempt bonds

• Costly – legal, other fees

• Matchmaking a good CBO strategy – find a CDE with

an allocation!

– Recipients must allocate credits within 5 years

• Historically, 50% + of all allocations have supported

for-profit and non-profit business development

– Significant capital investment in central city areas

New Markets Tax Credits –fine print and caveats

NMTCs : Artspace Commons North –Salt Lake City, UT • Former metal scrap yard

• Redeveloped into 102 rent-to-own units

• Includes 53,000 sq. ft. of retail

• Solar array produces 312-kilowatts from 334

rooftop solar panels and 525 solar panels on

an adjacent surface parking structure

• Key concern – financing gaps stemming

from rehab of brownfield into affordable

housing

• Role of NMTCs – $27.1 million

instrumental in attracting private capital

from US Bancorp Community Development

Corp., American Express Centurion Bank

• Significant additional private investment in

surrounding area

New Markets Tax Credits: Bethel

Center – Chicago, IL

A

f

t

e

r

• Bethel New Life, a faith-based

CDC, used $1.5 million in NMTCs

from LISC/Chicago to develop

23,000 sq.ft. Bethel Center on

brownfield site

• Center has employment, day care

services; 6 storefront businesses

• LEED gold certified

• Credit as leverage: NMTCs

attracted private capital from Bank

One and State Farm insurance

Renewable energy bonus depreciation deduction

• Solar electric, and other technologies, are classified as “5-year property” under IRS/MACRS system

– 50% “bonus” depreciation provision added in 2008: half the cost of the property can be deducted in the year placed in service, balance over 4 years

On-site renewable investment tax incentives

• 30% of costs of on-site solar, fuel cell, small wind

renewable systems, thru 12/31/16

• 10% for geothermal heat pumps, microturbines, thru 12/31/16

• 10% credit for CHP installation, thru 12/31/16, in year

it becomes operational

Energy Tax Incentives

• Grants-in-lieu incentives for renewable

have expired, continuation uncertain

• Technologies advancing

– Solar arrays becoming better suited to landfills,

northern climates

• Most energy efficiency incentives targeted to

residential uses

Energy tax incentives –fine print and caveats

Energy Credits: Bio-fuel Station – Eugene, OR• ¾ acre abandoned (since 1991) gas station,

with leaking UST systems, contaminated soil and ground water on and off-site

Energy Incentives Leveraged

• $1.2 million low-interest, redevelopment Oregon Sustainable Energy program loan

• $250,000 state energy tax credits

Results -- mixed-use bio-diesel fueling station

• 15 jobs; $4,000 in property taxes

• incorporates state-of-the art E2/P2/renewable energy techniques, including a green roof, bioswales to contain runoff

State tax

incentive

initiatives

• Site redevelopment/revitalization planning

• Infill site/vacant property acquisition

• Environmental site assessment

• Removal or remediation of contamination

• Site clearance, demolition, and debris removal

• Rehabilitation of buildings

• Construction of infrastructure, related improvements

that enhance contaminated property value

How Have State Tax Incentive Programs Been Used to Support Brownfield

Redevelopment Activities?

Tax Credits, Abatements, Incentives: What Can Support Brownfield Projects?

Examples from those in 22 states…

• deferral of increased property taxes — Connecticut

and Texas

• tax incentives for affordable housing -- Florida

• remediation tax credits – Illinois and Colorado

• cancellation of back taxes — Wisconsin and

Massachusetts

• sales tax rebates to offset cleanup costs – New Jersey

• advantageous tax treatment of brownfield property

improvements – North Carolina

• tax incentive “menu” -- Missouri

Tax policies to attract private capital

• Wisconsin allows new owners, working thru VCP, to

have back taxes waived, expedite transfer of tax

delinquent properties, to level the playing field and

attract new investors

• Gas station to coffee shop -- Milwaukee

Assignable, transferable, marketable tax credits to encourage infill and site reuse

• Massachusetts’ Brownfield Credit for Rehabilitation

of Contaminated Property; up to 50% credit against

cost of environmental response and removal; can be

combined with other state brownfield programs

• Wire fabricator to printing/graphics plant --

Dorchester

• Missouri Brownfield Redevelopment Program

– Offers range of loans, loan guarantees, for properties

abandoned or underused for at least 3 years

– Menu of jobs, investment, and property tax credits, up to

entire amount of cleanup

• Abandoned rail roundhouse complex to office park

and small business incubator

Missouri’s Incentive “Diner” – Going

a la carte for the full cleanup “meal”

Revamping traditional development entities to focus on reuse

• Michigan has created a

special category of

development authority

• Cities, towns and counties

can establish “brownfield

redevelopment authorities”

• Exercise traditional

development authority

powers: expedited title

clearance, TIF and bond

financing; eligible applicants

for other federal programs

Office of Policy Analysis impact study…

• 8,000 sites evaluated to determine impact of brownfield cleanups on property values

• About 150 with sufficient “before/after” data for detailed valuation analysis

The findings –

• Personal property values increased between 5.1% and 12.8% near

brownfield sites when cleanup is completed

• Cleaning up a brownfield can increase overall property values

within a one-mile radius – up to between $500,000 and $1.5

million

Our thinking?

• Potential impact on TIF strategies

EPA Sneak Peek – findings from OSWER/OPA Study

It’s all

creative thinking and applications…

For additional examples and information….

Contact Charlie Bartsch at

(202) 566-1054

![SUGARING THE AUTUMN. BY RUDOLF C. B. BARTSCH, · 2019. 8. 1. · 1912] Bartsch--"Sugaring" in the Autumn 195 "SUGARING" IN THE AUTUMN. BY RUDOLF C. B. BARTSCH, Roslindale, Mass. Ofthe](https://static.fdocuments.us/doc/165x107/60eafcb30f9c871c3e2acb26/sugaring-the-autumn-by-rudolf-c-b-bartsch-2019-8-1-1912-bartsch-sugaring.jpg)