Public Disclosure Authorized EAST ASIA - World Bank

249

Editors Kathie Krumm and Homi Kharas EAST ASIA Integrates A TRADE POLICY AGENDA FOR SHARED GROWTH

Transcript of Public Disclosure Authorized EAST ASIA - World Bank

T R A D E A N D D E V E L O P M E N T S E R I E S

ISBN 0-8213-5514-7

A Trad

e Policy A

gen

da fo

r Shared

Gro

wth

THE WORLD BANK

Emerging East Asian economies have seen their share of world exports more thantriple during the past quarter-century, and intraregional trade has driven thisgrowth. Broad measures of development in East Asia have improved at the same

headlong pace. Why push further integration now? Two economic events of historicproportions provide the context: strategic rethinking of development in the region followingthe East Asian financial crisis of 1997–98 and the accession of China to the World TradeOrganization. Policymakers interested in a stable, prosperous region are concerned bymildly rising inequality within countries and a widening income gap between richereconomies and the poorest economies. Increasingly, the development agenda in theregion—with its focus on growth, jobs, and social stability—and the trade policy agen-da—with its focus on market access and competitiveness—have become intertwined.

East Asian policymakers seek to develop a coherent set of economic policies that candeliver stability, growth, and regional integration. Without attempting to be compre-hensive, East Asia Integrates offers fundamental strategies that promote cross-borderflows of trade, globally and regionally, along with domestic policies on logistics, tradefacilitation, standards, and institutions to maximize the impact of these flows on devel-opment and to distribute the gains from trade widely.

As the authors demonstrate, multilateral and regional trade initiatives must provide acompelling vision of how integration can deliver broadly shared growth and prosperityif they are to succeed. In addition, they must use the momentum offered by tradeagreements to address the links between trade on the one hand, and social stability,poverty reduction, and growth on the other.

EditorsKathie Krumm and Homi Kharas

EAST ASIAIntegrates

A TRADE POLICY AGENDA FOR SHARED GROWTH

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Administrator

28041

east Asia integratesA Trade Policy Agenda for Shared Growth

east Asia integratesA Trade Policy Agenda for Shared Growth

Kathie Krumm and Homi Kharas, Editors

A copublication of the World Bank and Oxford University Press

© 2004 The International Bank for Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC 20433Telephone 202-473-1000Internet www.worldbank.orgE-mail [email protected]

All rights reserved.

1 2 3 4 06 05 04

A co-publication of the World Bank and Oxford University Press.

The findings, interpretations, and conclusions expressed here are those of the author(s) and do notnecessarily reflect the views of the Board of Executive Directors of the World Bank or the governmentsthey represent.

The World Bank cannot guarantee the accuracy of the data included in this work. The boundaries,colors, denominations, and other information shown on any map in this work do not imply on the part ofthe World Bank any judgment of the legal status of any territory or the endorsement or acceptance ofsuch boundaries.

Rights and PermissionsThe material in this work is copyrighted. No part of this work may be reproduced or transmitted in

any form or by any means, electronic or mechanical, including photocopying, recording, or inclusion inany information storage and retrieval system, without the prior written permission of the World Bank.The World Bank encourages dissemination of its work and will normally grant permission promptly.

For permission to photocopy or reprint, please send a request with complete information to the Copy-right Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA, telephone 978-750-8400, fax978-750-4470, www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Officeof the Publisher, World Bank, 1818 H Street NW, Washington, DC 20433, fax 202-522-2422, e-mail [email protected].

ISBN 0-8213-5514-7

Cover photo: World Bank

Library of Congress Cataloguing-in-Publication data has been applied for.

Foreword xi

Acknowledgments xiii

Overview xvKathie Krumm Homi Kharas

PART I WIDENING OPPORTUNITIES IN TRADE ARRANGEMENTS 1

1. China’s Accession to the WTO: Impacts on China 3William J. MartinDeepak BhattasaliShantong Li

2. Regional Impact of China’s Accession to the WTO 21Elena Ianchovichina Sethaput Suthiwart-Narueput Min Zhao

CONTENTS

vi East Asia Integrates

3. New Regionalism: Options for East Asia 39Mari Pangestu Sudarshan Gooptu

4. Market Access Barriers and Poverty in Developing East Asia 59Bijit Bora with additional material by Paul Brenton and Takako Ikezuki

PART II DEVELOPMENT ORIENTATION FOR A BEHIND-THE-BORDER AGENDA 75

5. Trade and Logistics: An East Asian Perspective 77Robin Carruthers Jitendra N. Bajpai David Hummels

6. Protecting Industrial Inventions, Authors’ Rights, and Traditional Knowledge:Relevance, Lessons, and Unresolved Issues 95Manjula Luthria Keith E. Maskus

7. Trade and Competitiveness Aspects of Environmental and Labor Standards in East Asia 115Keith E. Maskus

PART III REINFORCING SOCIAL STABILITY THROUGHBROAD SHARING OF BENEFITS 135

8. Household Welfare Impacts of China’s Accession to the WTO 137Shaohua Chen Martin Ravallion

9. Trade in Sectors Important to the Poor: Rice in Cambodia and Vietnam and Cashmere in Mongolia 149Jehan Arulpragasam Francesco Goletti Tamar Manuelyan Atinc Vera Songwe

10. Trade and Labor Market Vulnerability in Indonesia,Republic of Korea, and Thailand 171François BourguignonChor-ching Goh

Authors and Their Affiliations 189

Index 191

FIGURESFigure 1 Trends in Regional Trade xviiiFigure 2 Intraregional Trade xixFigure 3 China’s Trade in Third-Country Markets xxFigure 4 Reduced Agricultural Protection in China xxiFigure 5 Chinese Imports, 1995 and 2005 xxiiFigure 6 Regional Trade Arrangements xxviFigure 7 Inland Transport Costs for Remote Regions xxixFigure 8 Expanded Exports to APEC from Improvements in Trade Facilitation xxxFigure 9 Costs of Producer Services xxxFigure 10 Regulatory and Competitive Reforms, Selected Countries xxxiiFigure 11 Geographic Distribution of Bilateral Trade Treaties xxxiiiFigure 12 Environmental and Labor Standards, East Asia xxxivFigure 13 Poverty and Inequality xxxviFigure 14 Effects of China’s Accession to WTO on Household Incomes xxxviiFigure 15 Trade and Stability in Labor Markets, Republic of Korea xxxixFigure 2.1 Exports to China from East Asia Compared with Exports to

Other Partners 22Figure 2.2 China’s Imports, 1995 and 2005 23Figure 2.3 China’s Growing Role in Production Networks 24Figure 2.4 Impact of China’s WTO Accession on Japan and East Asia’s NIEs, 2001–10 26Figure 2.5 Impact of China’s WTO Accession on Developing Economies of

East Asia, 2001–10 27Figure 4.1 Real Income Gains in Developing East Asia from Agricultural Liberalization 60Figure 5.1 Potential Contribution of Transport to Economic Growth in East Asia 79Figure 5.2 Poverty and Accessibility in Lao PDR 82Figure 6.1 Comparison of Patenting Trends, Republic of Korea and Major

Developing Countries, 1978–99 97Figure 6.2 Comparison of Korean Semiconductor Patents with Worldwide

Semiconductor Patents, 1976–99 98Figure 6.3 Comparison of Korean Semiconductor Patents with Semiconductor

Patents of Major Advanced Countries, 1976–99 98Figure 6.4 Citations of Korean Patents as a Proportion of Total Patent Citations,

by Types of Patent Applicants, 1986–99 101Figure 6.5 Self-Citation Rates of Korean Private Corporations, 1980–99 102Figure 6.6 Korean Patents Granted in the United States, Selected Industries, 1981–99 102Figure 8.1 Poverty Incidence Curves: Rural 141Figure 8.2 Poverty Incidence Curves: Urban 142Figure 8.3 Mean Gains by Provinces: Absolute Gains in Yuan Per Capita 143Figure 8.4 Mean Gains by Provinces: Proportionate Gains in Percent 143Figure 8.5 Mean Gains by Provinces: Percentage of Gainers 144Figure 8.6 Mean Gains in Yuan, by Income Percentile 144Figure 8.7 Mean Percentage Gain, by Income Percentile 145Figure 8.8 Percentage of Gainers, by Income Percentile 145Figure 9.1 Profit Shares for Rice Value Chain, Cambodia and Vietnam 155Figure 9.2 Profit Structure of Rice Value Chain, Cambodia and Vietnam 161Figure 9.3 Share of Cashmere Products in Mongolia’s Total Cashmere Exports,

1993–2001 166

Contents vii

Figure 10.1 Decade Averages of Import Tariffs for Manufacturing Industries:Indonesia, Republic of Korea, and Thailand, 1980s and 1990s 174

Figure 10.2 Average Log of Real Wages of Males by Broad Sectors (Manufacturing,Services and Construction, and Others) and by Trade Exposure (Low, Medium, and High): Republic of Korea, 1976–2000 177

Figure 10.3 Average Log of Real Wages of Males by Broad Sectors (Manufacturing and Services) and by Trade Exposure (Low, Medium, and High):Thailand, 1991–2000 178

Figure 10.4 Average Log of Real Wages of Males by Broad Sectors (Manufacturing and Services): Indonesia, 1986–1999 178

Figure 10.5 Standard Deviation of Log of Real Wages of a Male Cohort in Low,Medium, and High Trade Exposure Industries: Republic of Korea,1976–2000 179

Figure 10.7 Average Monthly Hours Worked of a Male Cohort in Manufacturing and Services: Thailand, 1991–2000 180

Figure 10.6 Distribution of Employment Status and Employment Sectors ofa Male Cohort: Republic of Korea, 1985–2000 180

Figure 10.8 Estimated ρ by Birth Year Cohort: Republic of Korea, 1929–69 183Figure 10.9 Vulnerability by Sectors and Trade Exposure Groups: Republic of Korea,

1976–2000 184Figure 10.10 Vulnerability by Gender and Educational Attainment: Thailand, 1991–2000 185

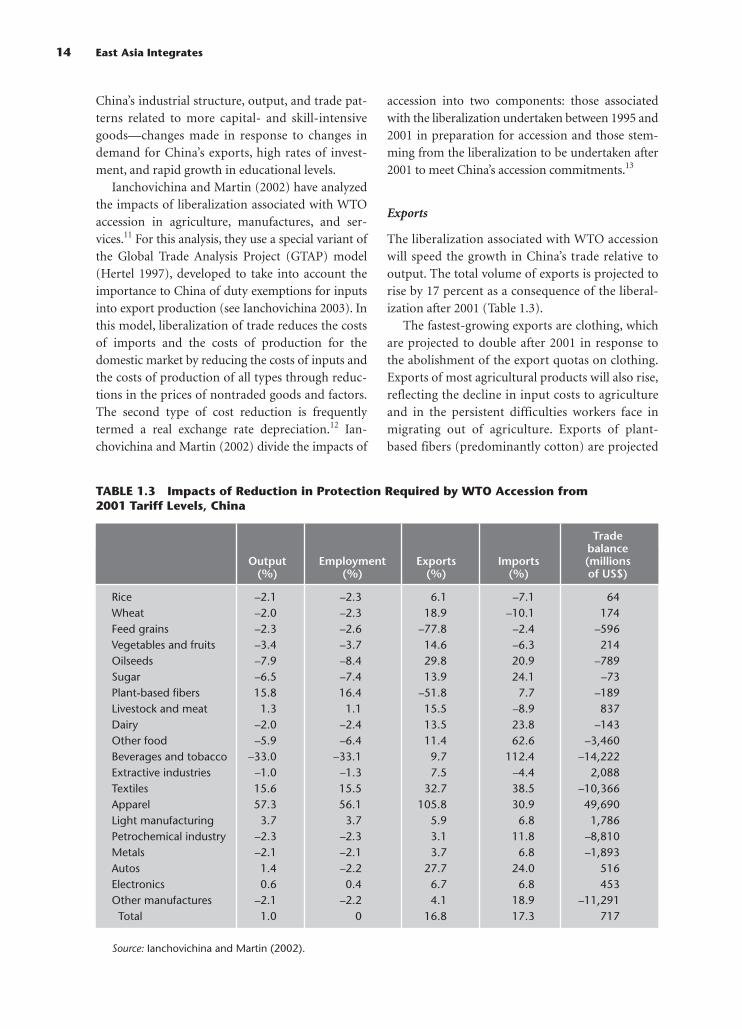

TABLESTable 1 Effects on Economic Welfare of Various Regional Trade Proposals xxivTable 2 Structure of Manufactured Exports by Country, 1985 and 1996 xxixTable 1.1 Some Measures of Import Protection in China’s Agriculture 8Table 1.2 Protection of Industrial Sectors in China 10Table 1.3 Impacts of Reduction in Protection Required by WTO Accession from

2001 Tariff Levels, China 14Table 2.1 Weighted Average Tariffs Facing Exports to China: Indonesia and

Thailand, 2001–08 28Table 2.2 Shares of Exports to China Affected by Lifting of Quantitative

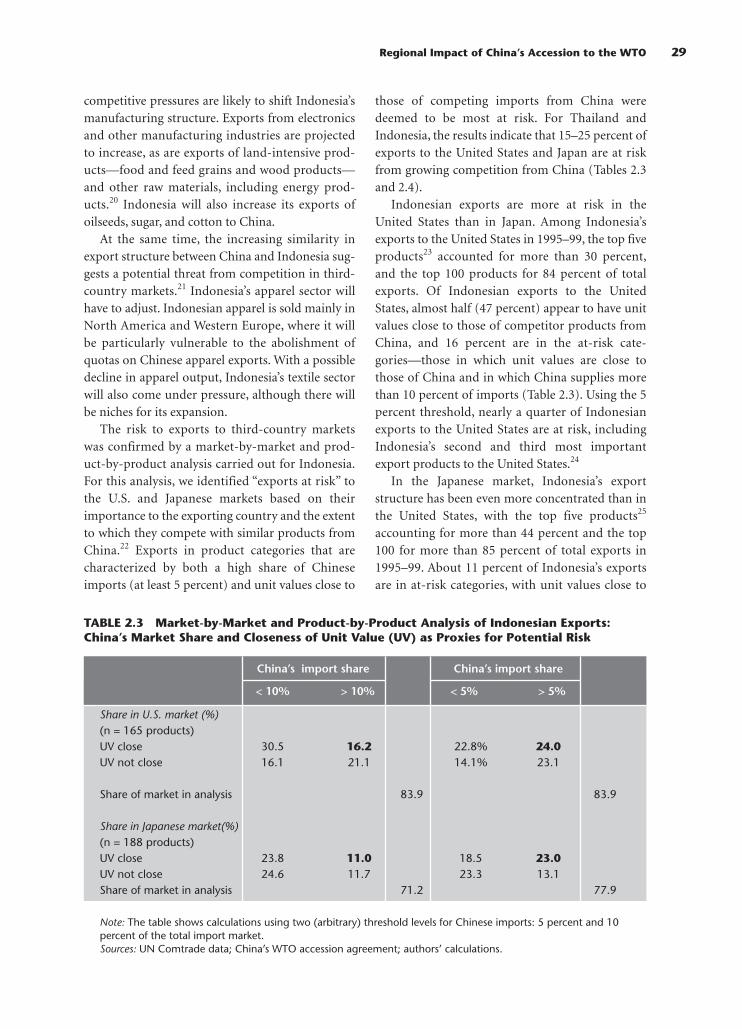

Restrictions (QRs): Indonesia and Thailand 28Table 2.3 Market-by-Market and Product-by-Product Analysis of Indonesian Exports:

China’s Market Share and Closeness of Unit Value (UV) as Proxies for Potential Risk 29

Table 2.4 Market-by-Market and Product-by-Product Analysis of Thai Exports:China’s Market Share and Closeness of Unit Value (UV) as Proxies for Potential Risk 30

Table 2.5 Share of Exports to China Affected by Lifting of Quantitative Restrictions (QRs): Cambodia and Lao PDR 33

Table 2.6 Market-by-Market and Product-by-Product Analysis ofCambodian Exports: China Market Share and Closeness of Unit Value (UV) as Proxies for Potential Risk 34

Table 2.7 Market-by-Market and Product-by-Product Analysis of Lao PDR’s Exports: China Market Share and Closeness of Unit Value (UV) as Proxies for Potential Risk 35

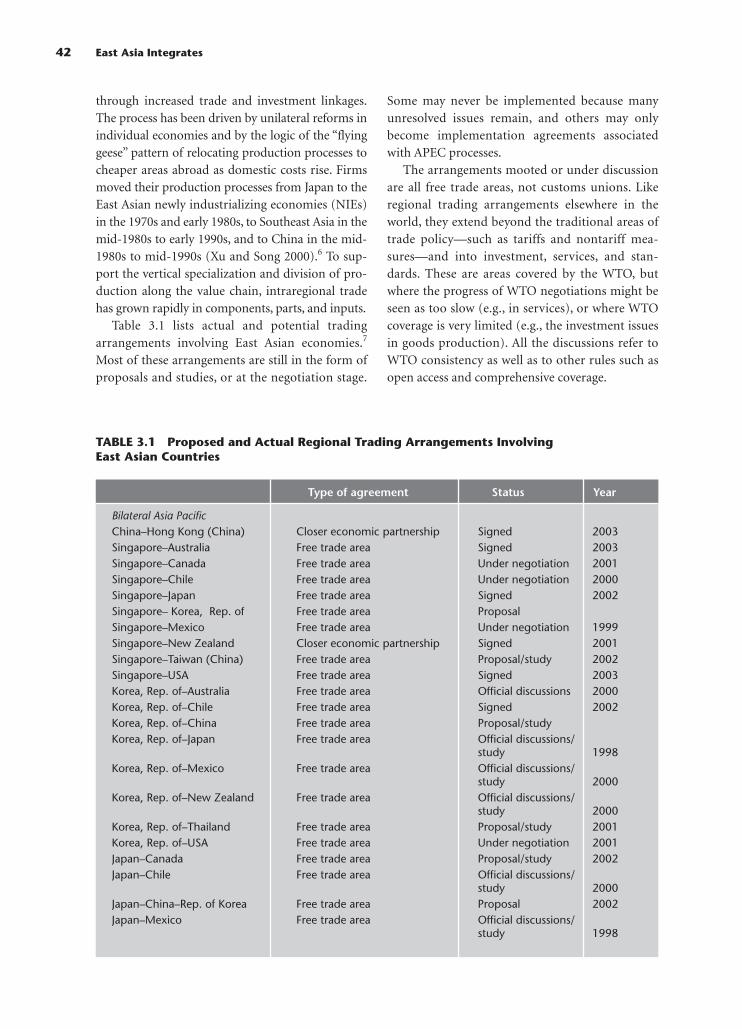

Table 3.1 Proposed and Actual Regional Trading Arrangements Involving East Asian Countries 42

viii East Asia Integrates

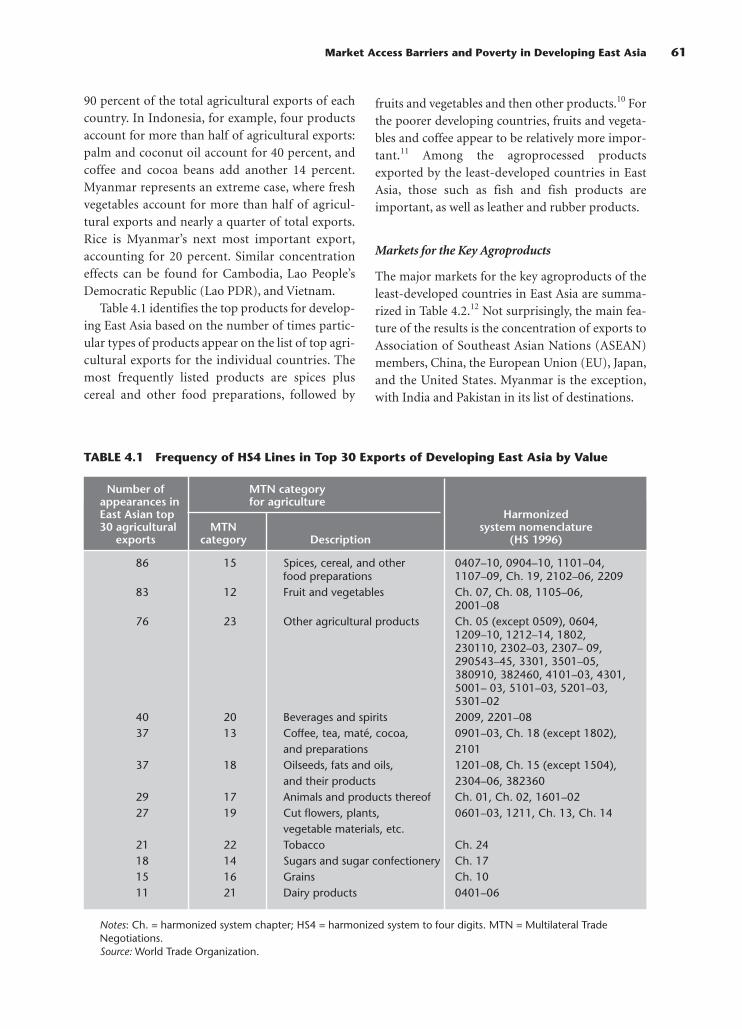

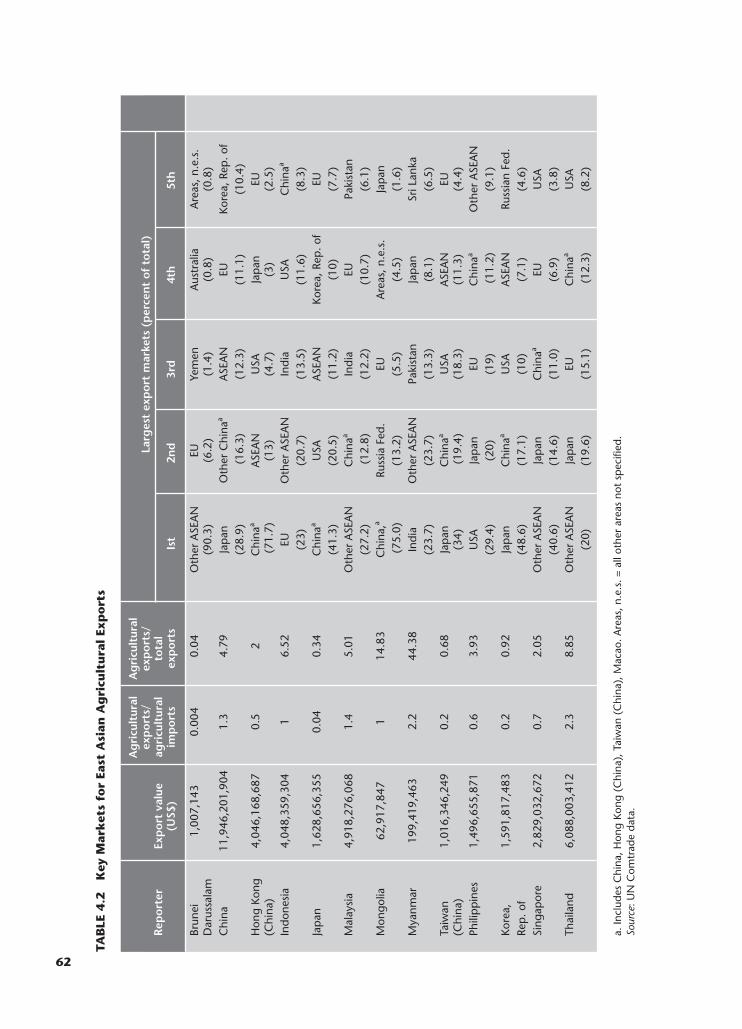

Table 4.1 Frequency of HS4 Lines in Top 30 Exports of Developing East Asia by Value 61Table 4.2 Key Markets for East Asian Agricultural Exports 62Table 4.3 Commitments and Average Direct Domestic Support Levels, 1995–98 64Table 4.4 Simple Average MFN Applied Tariff Rates by MTN Category,

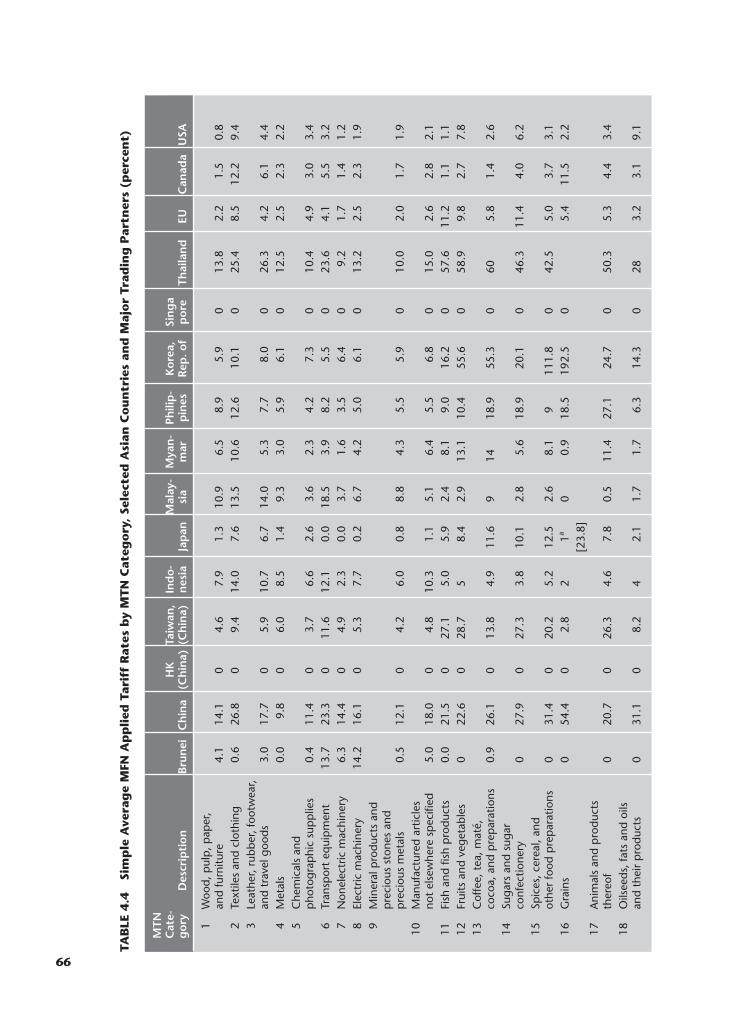

Selected Asian Countries and Major Trading Partners 66Table 4.5 Trade Policy Structure of European Union, Japan, and United States

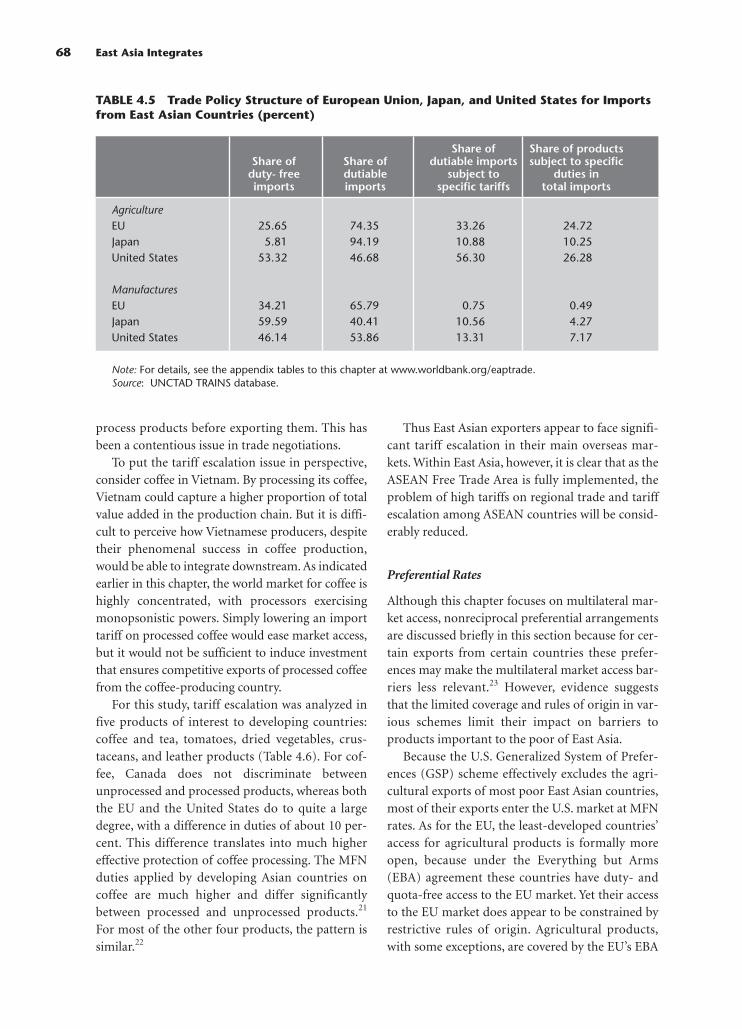

for Imports from East Asian Countries 68Table 4.6 Tariff Escalation for Selected Products in Selected Markets

and ASEAN Free Trade Area 69Table 4.7 Nontariff Measures Affecting Products of Interest to Developing

East Asia Economies 71Table 5.1 Availability of Transport Infrastructure 79Table 5.2 Composition of Logistics Costs of Container Transport from Inland China

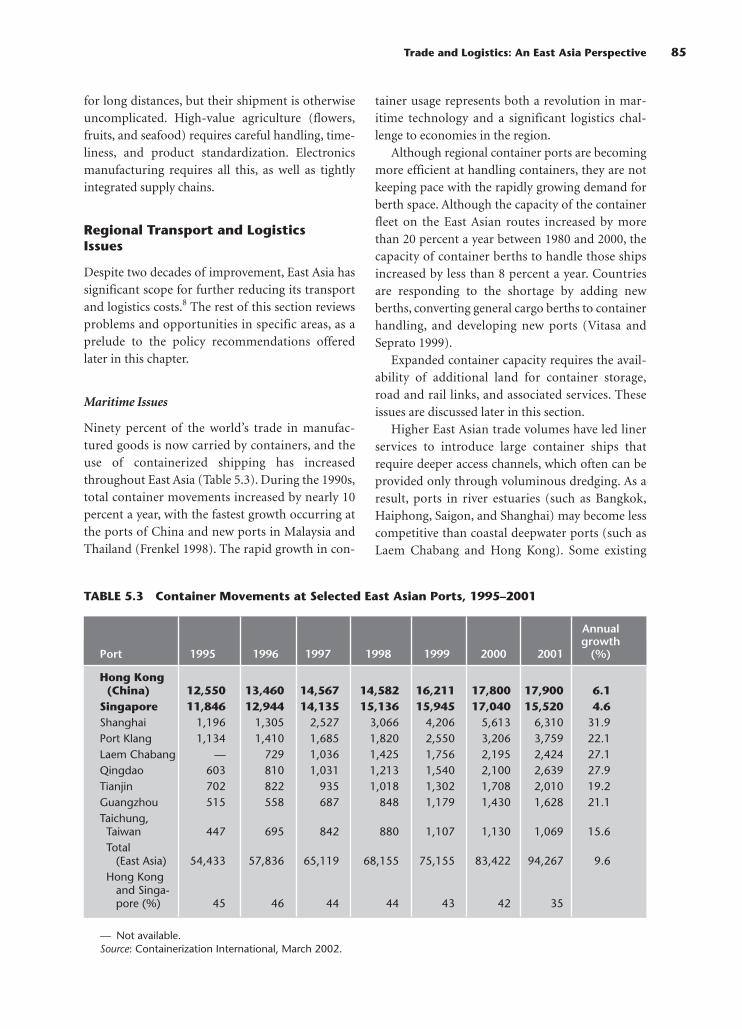

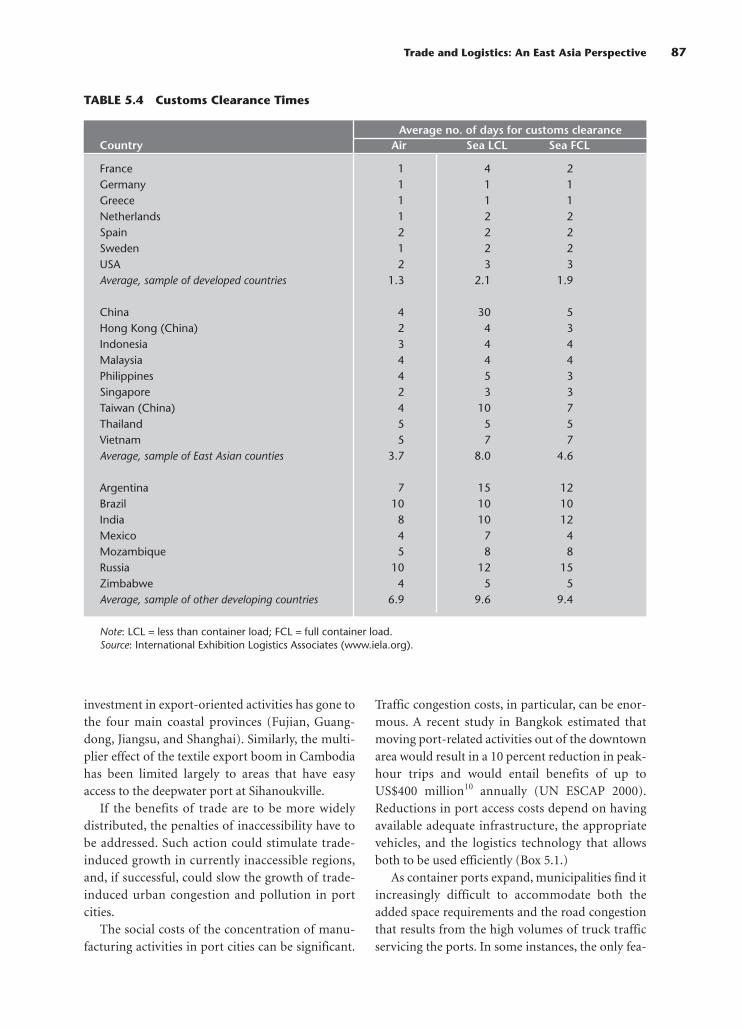

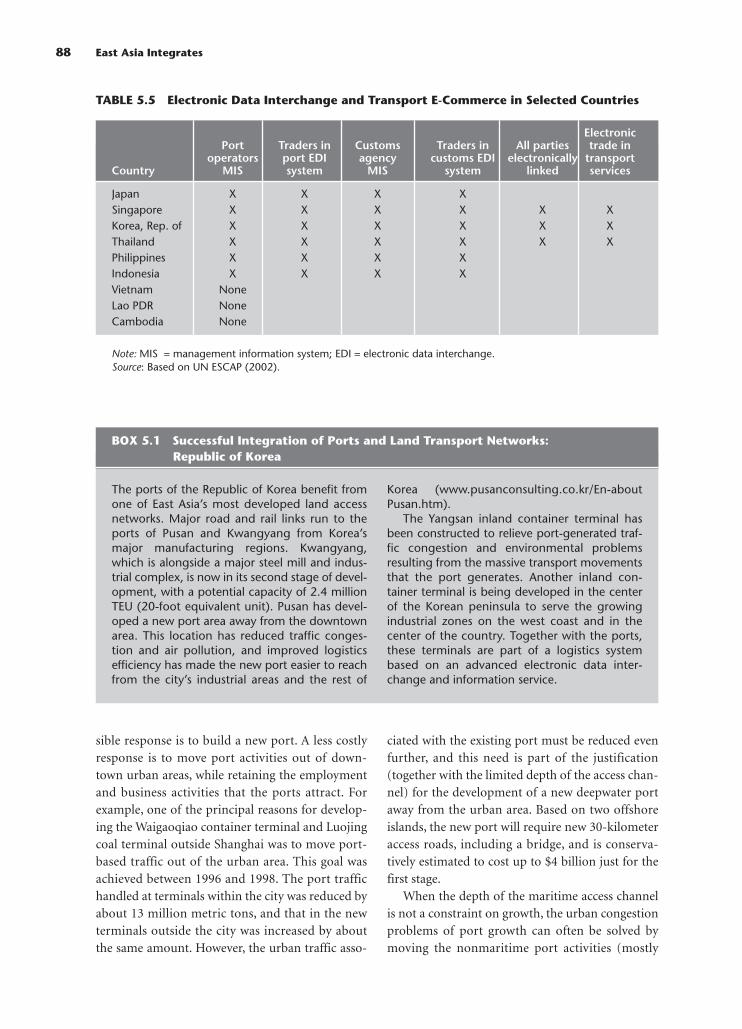

(Chongqing) to U.S. West Coast 84Table 5.3 Container Movements at Selected East Asian Ports, 1995–2001 85Table 5.4 Customs Clearance Times 87Table 5.5 Electronic Data Interchange and Transport E-Commerce in

Selected Countries 88Table 5.6 Ranking of Major Freight Airports in East Asia, 2001 89Table 6.1 Research Productivity of Selected Countries 100Table 7.1 Ratifications of Fundamental ILO Conventions Covering Worker Rights,

Selected East Asian Countries 117Table 7.2 Overall Ranking of Labor Standards 119Table 7.3 Impacts of Labor Standards on Labor–Intensive Exports from

Developing Countries 122Table 7.4 Environmental Policy Indexes 127Table 7.5 Impacts of Environmental Standards on Pollution-Intensive Exports

from Developing Countries 128Table 8.1 Predicted Aggregate Impacts on Welfare of Rural and Urban Households 141Table 9.1 Rice in Cambodia and Vietnam 153Table 9.2 Land Size and Rice Profit, Cambodia and Vietnam 154Table 9.3 Rice and Income of the Poor, Cambodia and Vietnam 154Table 9.4 Strategic Options for Rice, Cambodia and Vietnam 158Table 9.5 Effects of Various Policy Options on Rice Production, Income,

and Exports: Cambodia and Vietnam 159Table 9.6 Qualitative Analysis of Strategic Options, Cambodia 159Table 9.7 Marketing Costs and Margins for Rice in Cambodia, 2002 160Table 9.8 Marketing Costs and Margins for Export Rice in Vietnam, 2002 160Table 9.9 Marketing Margins of Farmers in Cambodia, Vietnam, Thailand,

and United States 161Table 9.10 Cashmere in Mongolia 162Table 10.1 Average Import Tariffs (Applied Duty Rates) and Percentage Change

in Tariffs of Indonesia, Republic of Korea, and Thailand between 1980s and 1990s 173

Table 10.2 Core Nontariff Barrier Measures: Indonesia, Republic of Korea,and Thailand, 1989–99 175

Table 10.3 Decade Average Shares of Import Tax Revenue in Total Government Revenue and Total Trading: Indonesia, Republic of Korea, and Thailand,1980–2000 175

Contents ix

Table 10.4 Volatility of Annual Growth Rates in GDP and Value Added in Manufacturing, Measured by Coefficient of Variation: Indonesia,Republic of Korea, and Thailand, 1970–96 176

Table 10.5 Level and Fluctuation of Wage Growth Rates (Males) by Trade Exposure Groups: Republic of Korea, 1976–1997 176

Table 10.6 Estimated ρ2 Correlation of Variance of Residual Earnings by Education,Gender, and Sector: Indonesia 183

Table 10.7 Vulnerability by Education, Gender, and Sector: Indonesia, 2001 184

BOXESBox 3.1 Forms of Regional Preferential Trading Arrangements 40Box 3.2 “Early Harvest” 52Box 4.1 Global Trade in Rice 65Box 5.1 Successful Integration of Ports and Land Transport Networks:

Republic of Korea 88Box 6.1 Protection of Indigenous Knowledge in the Philippines 111Box 9.1 Value Added from Value Chains 152

x East Asia Integrates

This collection of studies focuses on one of themost important economic issues facing East Asianand Pacific nations today. We have titled this collec-tion East Asia Integrates: A Trade Policy Agenda forShared Growth to capture three forces operating inthe region.

• First, a strong force for policy integration issweeping through the region, and it has gath-ered strength since the 1997–98 Asian financialcrisis. This new regionalism in East Asia is basedon a strategic re-rethinking of what needs to bedone to bolster growth and stability across theregion.

• Second, trade policy has gained prominence as acentral force, in part because trade within theregion has been one of the dynamos of growthin recent years, accounting for almost 90 percentof East Asian export growth in 2002, and in partbecause of the historic accession of China to theWorld Trade Organization in November 2001.Other countries in the region will have to adapttheir own national development strategies asChina adjusts to its new commitments.

• The third force is the determination that EastAsia should develop strategies to narrow the gapbetween richer and poorer countries andbetween urban and rural households to promoteregional stability and reduce poverty.

This is a very broad agenda, and, of course, nosingle volume can tackle all the problems in depth.But in launching this work we felt it was importantto broaden the approach beyond the technical per-spective of trade policy to emphasize developmentoutcomes and the links to social stability. Increas-ingly, the development agenda in the region—withits focus on growth, jobs, and social stability—andthe trade policy agenda—with its focus on marketaccess and competitiveness—have become inter-twined. Economic integration is a growing force,and we want to ensure it is managed carefully sothat its benefits can be shared broadly by poorercountries and the poor within countries.

To be sure, East Asia is a very diverse region, andour analysis shows that there is no one-size-fits-allapproach. Yet the studies included here suggestseveral policy priorities for East Asia as well as

xi

FOREWORD

directions for further empirical analysis that wouldcarry policymaking to a conclusive stage. It isimperative that all countries have the capacity toundertake detailed analysis on these priorityissues, because today there is an urgency to thepolicymaking process. Negotiating positions arenow being developed for an array of regional andbilateral agreements and for the Doha Develop-ment Agenda after Cancun. The stakes are high, sowe must move from debate and academic discus-sions to the real world of negotiations and concretepolicies.

The World Bank has a long and proud traditionof supporting the expansion of trade in East Asiaand around the world as a crucial tool in promot-ing growth and development. But this support doesnot mean a blind adherence to lower tariffs andreduced nontariff barriers. It does mean support-ing measures to ensure that the opportunitiesafforded by trade are available to everyone and ben-

efit everyone. Thus this volume contains studies onagriculture, market access for the goods producedby the poor, logistics to connect far-flung producerswith markets, environmental and labor standards,income and employment vulnerability, and theeffects on households of opening trade. A compre-hensive approach is needed to link trade to devel-opment and poverty reduction, and we urge policy-makers to develop such a comprehensive approachin their national development strategies, in theirregional and bilateral agreements, and in theirglobal negotiating positions.

We hope you, the reader, will find the studies inthis volume interesting and that in turn you willcontribute your voice to this critical debate.

Jemal-ed-din KassumVice President

East Asia and Pacific RegionWorld Bank

xii East Asia Integrates

ACKNOWLEDGMENTS

We have benefited from the input and guidance ofnumerous colleagues and officials who have supportedthe analysis underpinning this volume. We would liketo express our particular appreciation to the authors ofthe chapters and the background papers. Earlier draftsof the chapters and the main findings were presentedat seminars and workshops throughout East Asia,including Bangkok, Beijing, Hanoi, Jakarta, PhnomPenh, Seoul, Singapore, Tokyo, Ulaanbaatar, and Vien-tiane. We would like to thank the organizers, includingthe Institute for Southeast Asian Studies at theNational University of Singapore, the DevelopmentResearch Center and Tsinghua University in China, theThailand Development and Research Institute, and theWorld Bank Institute, as well as the staff of the countryoffices of the World Bank. We also benefited frominteraction with scholars and policymakers at theFourth Asia Development Forum on Trade andPoverty held in Seoul and organized jointly with theKorean Institute for International Economic Policy, theKorea Development Institute, and the Asia Develop-ment Bank. Valuable comments and contributionswere provided, and we would like to thank all of thosewho participated in these seminars as moderators, dis-cussants, and presenters. Special thanks go to

Narongchai Akrasanee, Ataman Aksoy, Myrna Austria,Choong Yong Ahn, Florian Alburo, Kanemi Ban, Dou-glas Brooks, Siow Yue Chia, Lu Ding, Carsten Fink,Yujiro Hajami, Masahiro Kawai, Jeffrey Lewis, Mai Lu,Aaditya Matoo, Deunden Nikomborirak, Hadi Soesas-tro, Jomo Sundaram, Somkiat Tangkitvanich, JoseTongzan, Shujiro Urata, Dominique Van der Mens-brugghe, Sangui Wang, John Wilson, Lan Xue, andIppei Yamazawa.

The views expressed in this book are those of theauthors and should not be attributed to any particularinstitution, including institutions with which individ-ual authors may be associated, including the WorldBank and the World Trade Organization.

Emerging East Asian economies1 have seen theirshare of world exports more than triple during thepast quarter-century, from 5.4 percent in 1975 to19.8 percent in 2002. Their trade with one anotherhas grown faster than their trade with any othermarket and now makes up 7.2 percent of globaltrade.2 Broad measures of development in East Asiahave improved at the same headlong pace; since1990 more than 300 million people have seen theirincomes rise above a poverty threshold of US$2.00a day.3

But performance has varied sharply over timeand across the region. Most recent trends showmildly rising inequality within countries, includingChina, Vietnam, and the Philippines, and a widen-ing income gap between richer economies such asSingapore and Hong Kong (China) and the poor-est, Lao People’s Democratic Republic (Lao PDR)and Cambodia.4 Both trends are of concern to pol-icymakers interested in a stable, prosperous region,and both trends have been linked with economicliberalization.

Against this background, some analysts estimatethat East Asia would still benefit more than anyother region from global liberalization (WorldBank 2002c)—because of the potential shown byits dynamic exporters—and that it could achievemuch of the benefits of liberalization throughregional integration—because of the wide scope ofintraregional trade among what are very diverseeconomies. The potential gains to the region fromglobal liberalization are estimated at hundreds ofbillions of U.S. dollars by 2015. Increasingly, thedevelopment agenda in the region, with its focus ongrowth, jobs, and social stability, and the trade pol-icy agenda, with its focus on market access andcompetitiveness, have become intertwined.

Pursuit of a “trade for development” strategy inEast Asia will not be easy. It involves economicchange at a time when policymakers are trying tomanage major financial and corporate restructur-ing, repair overstretched social safety nets, respondto the challenges posed by China, listen to thegreater plurality of voices and interest groups com-

xv

OverviewKathie Krumm

Homi Kharas

peting for political power, and adapt to sometimesvicious global economic cycles. Given that stabilityis seen as a key to investor confidence and a returnto high growth, it is not surprising that there isresistance to still further change.

Why Push Integration Now?

Two economic events of historic proportions pro-vide the context for East Asian development today.

The first event, the currency and financial crisisof 1997–98, still affects every aspect of economicpolicymaking. The crisis shattered a deeply heldand broadly shared view of the policy keys to devel-opment success, and called for a review of whatnow needs to be done to build on the basic tenets ofmacroeconomic stability, high savings and invest-ment, rapid expansion of education, and a strongexport orientation.5 Many in the region considerthe crisis to have been a “defining moment” (WorldBank 2002b).

The second major event was China’s accession tothe World Trade Organization (WTO) in November2001—the culmination of a 15-year-long bid formembership. China’s economy is already one of thelargest in the world, and China’s prominence as aneconomic force in the region has clearly risen sincethe crisis.6 China’s strong currency and stronggrowth, set against the weakening currencies andweak growth of other developing countries in theregion, have meant that China’s gross domesticproduct (GDP) now surpasses that of the rest ofemerging East Asia combined.7 China was theworld’s largest recipient of foreign direct investmentin 2002. Moreover, with its trade growing rapidly,China has become an important destination forexports from the rest of the region, and it is a fiercecompetitor in third-country markets.8 Because of itssize and diversity, China resists easy definitions of itscomparative advantage in terms of high-tech or low-wage manufacturing, and now that it has acceded tothe WTO its comparative advantage may changeappreciably. Thus it is no surprise that many policy-makers in the region feel the need to understand thetrends at work in China before they can formulatetheir own development strategies (World Bank2002b). Typically, too, they recognize that overcom-ing the formidable challenges of implementingChina’s WTO commitments will be as important forthe rest of East Asia as it is for China itself.

The region is now shaping its responses to thesetwo events. The financial crisis has forced policy-makers to rethink the financial, trade, and invest-ment linkages that connect regional economies. Atthe same time, it has given new impetus to ideas forregional institutions to help shape commonresponses. East Asian countries had historicallypursued unilateral and nonpreferential approachesto liberalization, sealed through commitmentsmade under WTO agreements. Indeed, through thecrisis market access was largely preserved. Butequally, significant gaps in the international archi-tecture were exposed, in finance, investment flows,and macroeconomic (especially exchange rate)coordination.

On the financial front of this new regionalism,the Chiang Mai initiative has created a web of swapagreements between regional central banks to bedeployed in case of future liquidity problems. TheAsian Bond Fund concept has been endorsed byseveral countries. Informal economic cooperationforums have discussed regional currency coopera-tion and a host of other economic and noneco-nomic issues.

In this context, the trade policy agenda for inte-gration—the subject of this volume—is only oneelement of a broader set of policy and institutionalchanges taking place in the region. Althoughregional trade negotiations have not advanced as faras those governing financial arrangements, manyanalysts consider them to be more fundamental andthe foundation for regional economic cooperation.Success will ultimately depend on the consistency ofapproaches among all elements of integration. Toachieve such consistency, the scope of discussionmust be broadened. To this end, the integrationagenda discussed in this volume covers three areas:

1. Widening opportunities, globally and regionally,in trade arrangements

2. A behind-the-border agenda to maximize thedevelopment impact of international commit-ments

3. Broad sharing of benefits to reinforce social sta-bility and a long-term political commitment tofurther reforms.

These areas are discussed in sections of thisoverview, and the concluding section outlines pri-ority areas for action.

xvi East Asia Integrates

Context: Recent Trends in Trade

Rapid and sustained growth in international tradehas long been a hallmark of successful growth anddevelopment strategies in East Asia. Some successstories are well known: those of the newly industri-alizing economies (NIEs) such as the Republic ofKorea, as well as middle-income economies such asMalaysia and the transition economy of China.More recent entrants to world markets that haveseen rapid export growth include low-incomeeconomies such as Cambodia and Vietnam. Tradehas been an important factor in growth in theregion, enabling progress in poverty reduction.Although the 1997–98 financial crisis interruptedthis progress, recovery since then has broughtpoverty rates in every emerging economy in theregion to record lows, and in economies like that ofVietnam, trade growth has brought with it a rapidreduction in poverty.

Intraregional trade in East Asia has grown fasterthan trade with any other market, and while thelargest economies account for the bulk of thistrade, the regional trade of most smaller economieshas also grown. Trade integration has been market-led, stemming from a combination of unilateralreforms, fulfillment of multilateral commitments,and a pattern of relocation of production processes(see Kawai and Urata 2002). Intraregional trade hasbeen driven not only by growing demand butincreasingly by improved competitiveness inregional markets, as reflected in increased marketshares (Figure 1). China has been particularlydynamic, but almost all countries increased theircompetitiveness in regional markets during1995–2001.9 This increase was accomplished with-out loss of competitiveness in other markets; EastAsia continued to expand its market shares in theEuropean Union (EU) and North American FreeTrade Agreement (NAFTA) markets in the sameperiod.

The product composition of intraregional tradehas become highly concentrated. The top 30exports now account for more than half of totaltrade, with 38 percent in just four subsectors: officemachinery, telecommunications equipment, elec-tronics, and textiles and clothing (Figure 2).

One of the major factors in the concentration ofintraregional trade has been the remarkableincrease in international production networks, as

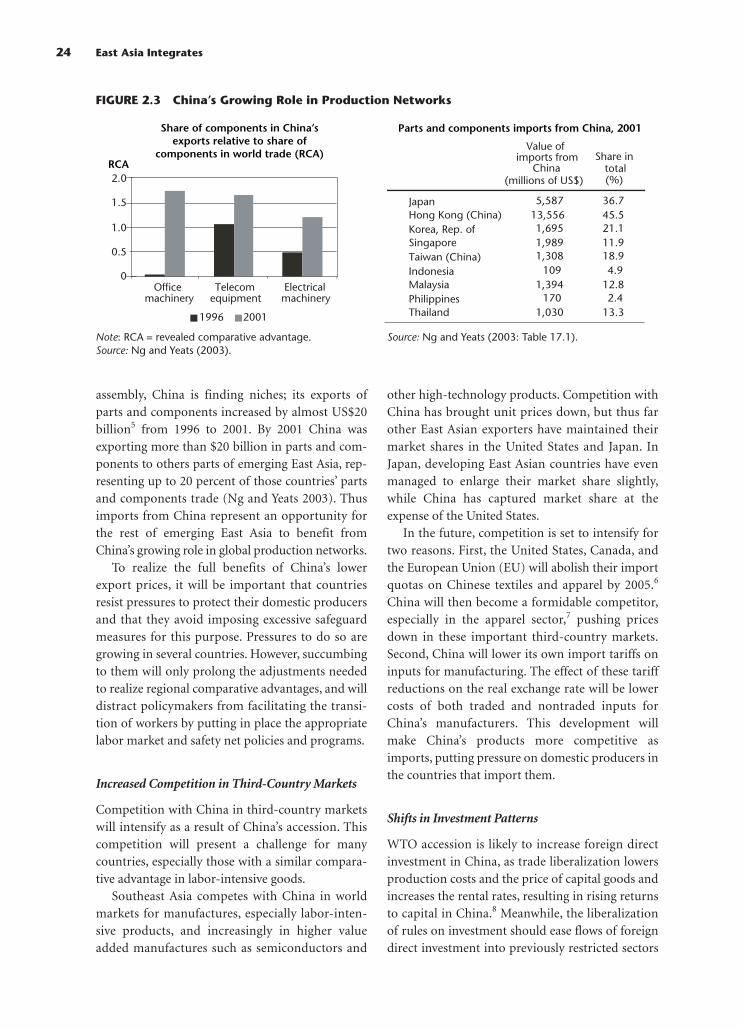

reflected in the growth of trade in components orpartly assembled goods. China is increasingly acentral player in such production networks, both asa final assembler of products and as an efficientprovider of components. Although Japan remainsan important center of production-sharing opera-tions in East Asia and is the origin of about one-third of all regional exports of components forassembly, China is finding niches; its exports ofparts and components grew by almost $20 billionduring 1996–2001. At the same time, other EastAsian economies have been finding their ownniches within China’s markets and increasing theirshares of China’s imports.

Meanwhile, East Asian trade profiles havebecome more mutually complementary, and thedegree of complementarity for emerging East Asiais now comparable to that of the EU and NAFTA.10

The exceptions are low-income countries suchas Cambodia, Lao PDR, and, to a lesser extent, Viet-nam. This finding is perhaps not surprising, giventhat a country’s trade structure becomes more likethe world’s trade structure as the country’s incomerises. The wide gap between rich and poor coun-tries in East Asia is also largely responsible for a risein regional income inequality (see Milanovic 2003and the discussion later in this chapter). Policiesand institutions that contribute to fuller integra-tion of the low-income countries and regions ofEast Asia will be critical to addressing incomeinequality in East Asia and contributing to a stableregion.

Widening Opportunities in TradeArrangements

Today, the region’s policymakers see trade andinvestment integration as key elements of strategy.Although a few trade barriers were erected inresponse to the Asian economic crisis, they wereminor and temporary.11 Indeed, instead of moreprotection, the crisis produced a new impetus foropenness. A multitrack approach is being followed,with support for a new global round of trade nego-tiations as well as for regional and bilateral arrange-ments.

Liberalization of trade and investment policies isrecognized as a way to spur gains in efficiency. Assuch, it fits well with the new emphasis in Asia oninnovation in firms and on economy-wide produc-

Overview xvii

tivity growth to replace the old model of growththrough physical and human capital accumulation(Yusuf and others 2003). There is ample evidencethat export-oriented firms and those with foreignequity participation are far more productive than

domestic-oriented firms, with productivity differ-entials of 40 percent in Indonesia and the Philip-pines and 15–20 percent in Thailand and Korea(Hallward-Driemeier, Iarossi, and Sokoloff 2002).Moreover, China’s restructuring provides an impe-

xviii East Asia Integrates

Emerging East Asia: share of world trade

0

5

10

15

20Percent

Percent

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Emerging East Asia intraregional trade

Intraregional trade: share of export change accounted for by competitiveness

and demand changes

0

20

40

60

80

100

85–9

5

95–0

1

85–9

5

95–0

1

85–9

5

95–0

1

Competitive factora Demand factorb

With emergingEast Asia

Within emerging East Asia

Emerging EastAsia—Japan

0

5

1015

20

25

30

35

40Percent Percent

United StatesJapan

China Other East Asia

East Asia NIEs: export markets(as % of total exports)

Developing East Asia: export markets(as % of total exports)

05

10

15

2025

30

3540

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

United StatesJapan

China Other East Asia

FIGURE 1 Trends in Regional Trade

Note: Emerging East Asia is ASEAN plus other newlyindustrializing economies plus China plus Mongolia.Source: IMF, Direction of Trade Statistics (various years);data reported from exporter country accounts.

Note: East Asia NIEs refers to Hong Kong (China), Repub-lic of Korea, Singapore, Taiwan (China).Sources: IMF, Direction of Trade Statistics (various years);data reported from exporter country accounts.

Note: Developing East Asia refers to Indonesia, Malaysia,Philippines, Thailand, Cambodia, Lao PDR, Mongolia,Myanmar, Vietnam.Sources: IMF, Direction of Trade Statistics (various years);data reported from exporter country accounts.

Note: Diversification, or change in exports due to newproducts, accounts for a small share.a. Competitive factor = change in market share.b. Demand factor = change in market size.Source: Ng and Yeats (2003: Table 9.1).

Emerging East Asia economies’ share of world exportsgrew…and trade among these economies grew evenfaster.

Intraregional trade is driven increasingly by competitiveness and growing market share.

Exports to China are particularly dynamic, with East Asia finding niches in China’s markets.

tus for establishing new regional production net-works, initially in electronics, that would promotehighly productive firms. For now, these productionnetworks are oriented toward exports to developedcountries, but the growing markets within East Asiaprovide a potential complementary source ofdemand.12

Policies can support these natural economicforces, and the drive to liberalize is shaping new

institutional arrangements. The willingness of theworld’s richer countries to target the needs ofdeveloping countries in the context of the DohaDevelopment Agenda is helpful, but the outcome ofthese negotiations is still uncertain. And regionaland bilateral agreements fit in well with other polit-ical aims of East Asian countries, giving theseagreements a momentum that the global discus-sions have yet to achieve. ASEAN has moved to a

Overview xix

Telecom equipment

5%

Electrical machinery21%

Textiles and clothing6%

Other top 30

13%

Others49%

Office machinery

.6%

Others72%

Parts andcomponents in top 30

28%

Share of 2001 five-digit SITC parts andcomponents in top 30 exports

Share of 2001 intraregional trade accounted forby 30 largest four-digit SITC exports

FIGURE 2 Intraregional Trade

Note: SITC = Standard International Trade Classification.Source: Ng and Yeats (2003: Table 12.1).

Note: Revealed comparative advantage (RCA) measures a country’s relative export performance in a good j. It is definedas the country’s share of world exports of good j (xij/xwj) divided by its share of total world exports (Xi/Xw), where xij andxwj represent the value of good j exported by country i and the world, respectively, and Xi and Xw are country i’s andthe world’s total exports, respectively. If the value of the index exceeds unity, the country is said to have a comparativeadvantage in the production of good j.Source: Ng and Yeats (2003).

Note: In addition, parts and components in the non–top30 exports account for an additional US$8.3 billion or 4percent of total non–top 30 exports.Source: Ng and Yeats (2003: Table 17.1).

Intraregional trade is increasingly concentrated…and production sharing is a major determinant.

China is an increasingly central player in production networks.

0.5

1.0

1.5

2.0

2.5

RCA RCA

Officemachinery

Telecomequipment

Electricalmachinery

Officemachinery

Telecomequipment

Electricalmachinery

0

0.5

1.0

1.5

2.0

1996 2001

Share of components in China's importsrelative to share of components in world trade

Share of components in China's exportsrelative to share of components in world trade

two-tier system to permit its more advanced mem-bers to accelerate trade reform, while launchingnew initiatives to integrate its less-developed mem-bers—Cambodia, Lao PDR, Myanmar, and Viet-nam. At the same time, the speed with which theASEAN-China Framework Agreement has beenlaunched and the ideas for a new ASEAN-Japan arecreating new alliances in favor of liberalizationwithin the region. As Philippines president GloriaArroyo noted in a speech of May 2002, combiningthe Association of Southeast Asian Nations(ASEAN) and Chinese economies “would givebirth to a market of 1.8 billion consumers or almostone third of humanity.”

China’s Role in the Region

In line with its own reforms, China has been agrowing economic force in East Asia. Exports toChina have been dynamic over the last decade, par-ticularly for the newly industrializing economiesbut also for the rest of developing East Asia (Figure1), while shares to the United States and Japan havebeen flat or declining. China’s trade with majormarkets also has been expanding, but not at theexpense of developing East Asia (Figure 3).

Membership in the WTO and the reforms asso-ciated with membership give China an opportunityto play an even larger and growing role in the worldeconomy, and in the regional economy, amplifyingpreexisting trends.

What WTO Accession Means for China: SectoralShifts. As explained in Chapter 1, assessing theimplications of major economy-wide reform suchas that involved in China’s WTO accession is inher-ently difficult. Much of the impact will consist ofreinforcing the structural changes already underway. The experience with other trade events such asthe formation of NAFTA suggests that the actualoverall impact will be much greater than suggestedby ex ante modeling, largely as a result of produc-tivity and other changes that are hard for models tocapture.

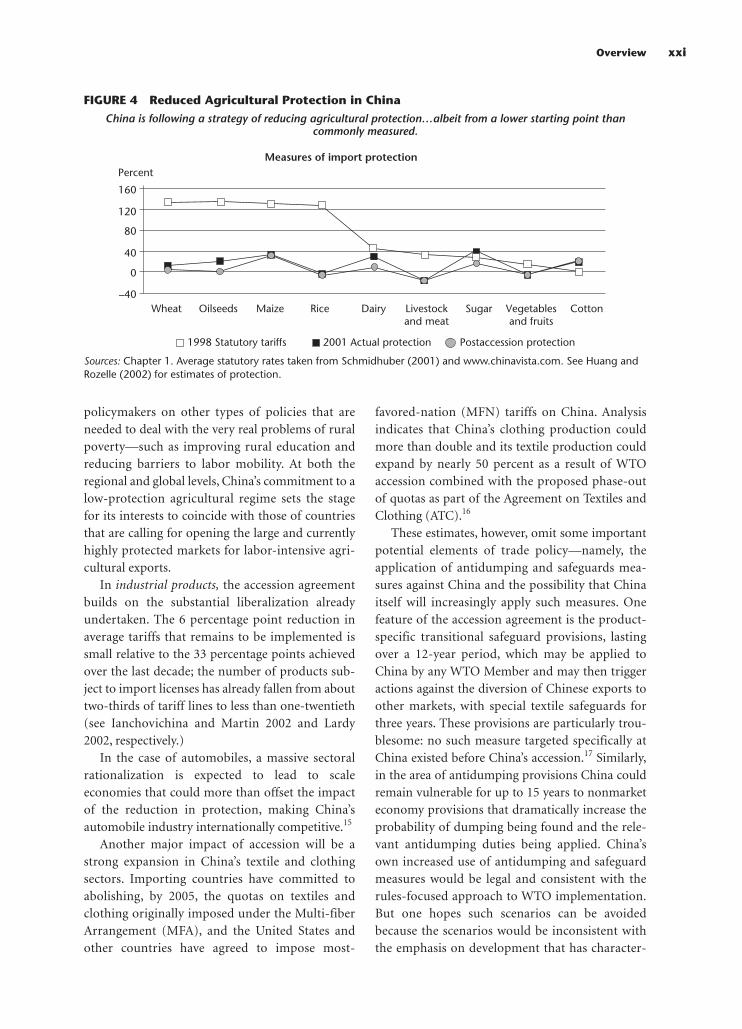

In agriculture, the initial levels of effective pro-tection are in fact likely to be far lower than othershave estimated, implying that sectoral shifts arelikely to be less dramatic than others are predict-ing.13 Nonetheless, China’s agricultural trade liber-alization plan is the expected source of about halfof the efficiency gains from the WTO accessionpackage. Reduced protection and greater scope forimports are likely in a range of products, includingoilseeds, sugar, and dairy products (where the prin-cipal form of protection has been tariffs, which arebeing reduced substantially) and cotton (whereexport subsidies are now ruled out) (Figure 4). Anddemand will sharply increase for other raw materi-als and natural resources such as wood and energyproducts.

China’s decision to contain agricultural protec-tion has more far-reaching implications.14 This useof WTO rules as a commitment device will focus

xx East Asia Integrates

Share of U.S. imports

0

5

10

Percent Percent

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

Share of Japanese imports

0

5

10

15

20

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

China

Other developing East Asia

FIGURE 3 China’s Trade in Third-Country Markets

Source: IMF, Direction of Trade Statistics (various years.)

This trade is expanding…but not at East Asia’s expense.

policymakers on other types of policies that areneeded to deal with the very real problems of ruralpoverty—such as improving rural education andreducing barriers to labor mobility. At both theregional and global levels, China’s commitment to alow-protection agricultural regime sets the stagefor its interests to coincide with those of countriesthat are calling for opening the large and currentlyhighly protected markets for labor-intensive agri-cultural exports.

In industrial products, the accession agreementbuilds on the substantial liberalization alreadyundertaken. The 6 percentage point reduction inaverage tariffs that remains to be implemented issmall relative to the 33 percentage points achievedover the last decade; the number of products sub-ject to import licenses has already fallen from abouttwo-thirds of tariff lines to less than one-twentieth(see Ianchovichina and Martin 2002 and Lardy2002, respectively.)

In the case of automobiles, a massive sectoralrationalization is expected to lead to scaleeconomies that could more than offset the impactof the reduction in protection, making China’sautomobile industry internationally competitive.15

Another major impact of accession will be astrong expansion in China’s textile and clothingsectors. Importing countries have committed toabolishing, by 2005, the quotas on textiles andclothing originally imposed under the Multi-fiberArrangement (MFA), and the United States andother countries have agreed to impose most-

favored-nation (MFN) tariffs on China. Analysisindicates that China’s clothing production couldmore than double and its textile production couldexpand by nearly 50 percent as a result of WTOaccession combined with the proposed phase-outof quotas as part of the Agreement on Textiles andClothing (ATC).16

These estimates, however, omit some importantpotential elements of trade policy—namely, theapplication of antidumping and safeguards mea-sures against China and the possibility that Chinaitself will increasingly apply such measures. Onefeature of the accession agreement is the product-specific transitional safeguard provisions, lastingover a 12-year period, which may be applied toChina by any WTO Member and may then triggeractions against the diversion of Chinese exports toother markets, with special textile safeguards forthree years. These provisions are particularly trou-blesome: no such measure targeted specifically atChina existed before China’s accession.17 Similarly,in the area of antidumping provisions China couldremain vulnerable for up to 15 years to nonmarketeconomy provisions that dramatically increase theprobability of dumping being found and the rele-vant antidumping duties being applied. China’sown increased use of antidumping and safeguardmeasures would be legal and consistent with therules-focused approach to WTO implementation.But one hopes such scenarios can be avoidedbecause the scenarios would be inconsistent withthe emphasis on development that has character-

Overview xxi

–40

40

0

80

120

160

PercentMeasures of import protection

1998 Statutory tariffs 2001 Actual protection Postaccession protection

Wheat Oilseeds Maize Rice Dairy Livestockand meat

Sugar Vegetablesand fruits

Cotton

FIGURE 4 Reduced Agricultural Protection in China

Sources: Chapter 1. Average statutory rates taken from Schmidhuber (2001) and www.chinavista.com. See Huang andRozelle (2002) for estimates of protection.

China is following a strategy of reducing agricultural protection…albeit from a lower starting point than commonly measured.

ized China’s trade reform agenda since the begin-ning of the reform era.

China’s trade in services was the subject of one ofthe most radical services reforms ever negotiated inthe WTO. The potential for rapidly increasing tradein services is significant. The important feature ofChina’s commitments is that they focus on marketaccess and do not discriminate between domesticand foreign suppliers. With China expected to bethe largest market for telecommunications in theworld by 2010, its commitments in that sector areprofound in that they allow foreign entry for a widerange of activities. One area of services with animportant bearing on trade is the activities thatmake up the logistical chain. China’s WTO com-mitments promise increased competition andreduced costs in several areas, including throughthe development of third-party logistical firms. Yetrestrictions remain in place on the form of estab-lishments, such as requirements for joint ventures,and on geographic scope.18

What WTO Accession Means for China: Ways ofDoing Business. The implications for China ofaccession to the WTO go beyond the specific com-mitments in its accession package. Changes in theways of doing business—elimination of dual pric-ing, phasing out of restrictions on trading, moreuniform administrative arrangements, and judicialreview—are likely to result in dynamic gains thatwill outweigh those based on comparative-staticestimates of efficiency gains. Every 1 percent gain in

productivity in the services sector from expandedcompetition and foreign entry, for example, implieswelfare gains of $10 billion and a real GDP increaseof 2.2 percent, equivalent to the total estimatedstatic gain from China’s accession to the WTO (Ian-chovichina and Walmsley 2002).

What WTO Accession Means for the Rest of EastAsia: On Balance, More Opportunity. The fore-most opportunity for the rest of East Asia arisingfrom China’s WTO accession lies in expandingexports to China’s growing and more open mar-kets; China’s imports are expected to grow from 3percent of global GDP in 2000 to more than 6 per-cent by 2005 across an array of commodities (Fig-ure 5). China receives 55 percent of its importsfrom East Asia and 37 percent from emerging EastAsia. All groups of countries in East Asia will bene-fit from China’s more open markets, but evidencesuggests the scope is especially large for China’smajor trading partners of Japan and the newlyindustrializing economies, but will still be signifi-cant for the middle-income countries and thelowest-income countries, as explained in Chapter 2.

Indeed, the sectoral landscape just describedsuggests significant export opportunities for devel-oping East Asian economies. For countries such asIndonesia and Thailand, the weighted average tariffon their top 100 export products falls by a half asthe result of China’s accession, and some of theirtop agricultural and raw material exports—rubber,sugar, urea, and to a lesser extent rice—will benefit

xxii East Asia Integrates

China: Percent Change in Imports Between 1995 and 2005

0 100 200 300 400 500 600 700

Other manufacturesElectronics

MetalsWood and paper

Wearing apparel, netTextiles

Extractive industriesBeverages/tobacco

Other foodDairy

Meat and livestockOilseeds

FeedgrainsFoodgrains

Without accession With accession

Percent

times 10

FIGURE 5 Chinese Imports, 1995 and 2005

Source: Ianchovichina and Martin (2001).

What will China import more of?

from a reduction in nontariff barriers. These coun-tries also may see increased interindustry trade andproduction sharing as China’s electronics and othermanufacturing industries, for example, grow.

For the lowest-income countries such as Cam-bodia and Lao PDR, there also will be opportuni-ties. The decline in these countries’ weighted aver-age tariff for the top 100 exports to China is quitesmall (from 4.3 to 2.6 percent for Cambodia andfrom 7.3 to 6.0 percent for Lao PDR), and onlyabout 10 percent of Cambodia’s exports and lessthan 1 percent of Lao PDR’s exports, includingwood and rubber, will face fewer quantitativerestrictions. However, given the trade intensity withChina, they will benefit from China as a powerfulsource of external demand.19

China’s accession also offers the rest of theregion the opportunity to import cheaper pro-duced goods. Most obviously, consumers of Chi-nese finished good imports will benefit. But manyproducers will also gain by access to cheaper inter-mediate inputs into production processes. Forexample, chemicals already represent nearly 10 per-cent of imports from China in Indonesia and Thai-land. By 2001 China was exporting more than $20billion in parts and components to other parts ofemerging East Asia, representing up to 20 percentof those countries’ parts and components trade.Continued growth in imports of parts and compo-nents from China will represent an opportunity forthe rest of emerging East Asia to develop competi-tive firms.

To benefit from these opportunities, it will beimportant that East Asian countries resist the grow-ing protectionist pressures for imposition of exces-sive safeguard measures in a futile effort to protectall domestic producers. In Thailand, local manufac-turers are complaining about low-cost imports ofelectrical appliances and motorbikes from China.In 2002 Indonesia imposed temporary safeguardmeasures for garment imports, and Vietnam did sofor motorbikes. Such decisions can only prolongthe shifts in production that are necessary to realizeregional comparative advantages, and distract poli-cymakers from facilitating the adjustment of work-ers through appropriate labor market and safetynet policies and programs.

China’s WTO entry also implies increased com-petition in third-country markets. If recent Chi-nese export performance (Figure 3) is an indicator,

the expansion of China’s presence in major mar-kets will not necessarily crowd out other develop-ing East Asian exports, although it may constraintheir growth prospects to levels below those of thelate 1980s.

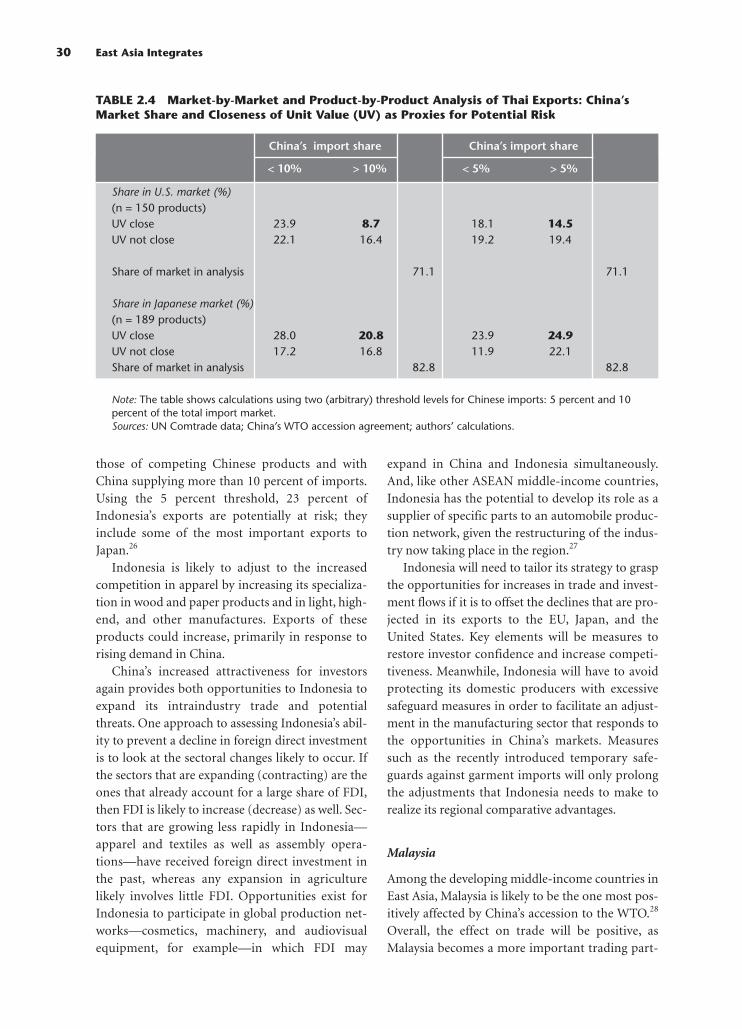

Nonetheless, certain exports appear at risk.Clearly, the apparel and textile sectors in other EastAsian countries will face additional competition inmarkets that are currently constrained by quotarestrictions. The market-by-market and product-by-product analysis in Chapter 2 indicates that for Thai-land, for example, only about 15 percent of exportsto the United States are at risk from increased com-petition from China, but that 25 percent of exportsto Japan are at risk. For Indonesia, the second andthird most important exports to the United States—footwear and video-recording and -reproducingapparatuses—face direct competition with China, asdo about a quarter of exports to Japan.

Among lower-income countries, Cambodia isparticularly vulnerable because its exports arehighly concentrated in apparel. Roughly 30 percentof Cambodia’s exports to the United States haveunit values similar to those of Chinese exports,indicating direct competition, or are in categoriesin which China is currently quota-constrained,indicating that competition from China is likely toincrease. This prospect highlights the need forurgency; such countries must speed up their gover-nance and other reforms to ensure the develop-ment of alternative products.

Nonetheless, on balance, China represents moreof an opportunity than a threat to the rest of EastAsia. Certain challenges will need to be met, andadjustments made. However, the scope for gainsfrom a dynamic China is large across the range ofcountries in East Asia.

Regional Interdependence

Recent trends in the magnitude and composition ofintra–East Asian trade bode well for further inte-gration (also see Ng and Yeats 2003). Comparisonsshow that conditions within East Asia are now verysimilar to those in countries that were previouslyable to implement such successful regionalarrangements as the European Union and NAFTA.

East Asia has achieved a high degree of market-driven regional integration, but regionalism—moreformal economic cooperation and economic inte-

Overview xxiii

gration arrangements and agreements betweencountries—has traditionally been quite limited, asexplained in Chapter 3.20 The major exceptions havebeen the ASEAN Free Trade Area (AFTA), estab-lished in 1993, and dialogue under the Asia-PacificEconomic Cooperation (APEC) forum. However,the past several years have seen a plethora of pro-posals for new bilateral and regional trade arrange-ments: the Framework Agreement on ASEAN-China Comprehensive Economic Cooperation,signed in November 2002; an East Asia–wide freetrade agreement; a more recent proposal by Japanfor an ASEAN-plus-Japan free trade agreement; andbilateral agreements under negotiation, in particu-lar by Japan, Singapore, Korea, and Thailand.

Scope for Gains from Regionalism. Addressingintraregional barriers can ensure continueddynamism in regional trade and investmentflows—including in response to China’s growingrole. The stated motivation of several initiatives,including the ASEAN-China Framework Agree-ment, is to take advantage of complementaritiesand build on existing strengths in order to make theregion collectively more efficient and competitiveand thereby attract investment. The regional agree-ments under consideration are increasingly com-prehensive in scope, going beyond the removal oftariffs and nontariff barriers on trade in goods to

include trade facilitation measures, such as con-formity of standards and procedures acrossnational boundaries, and trade in services. TheNew-Age Partnership between Singapore and Japanannounced in January 2002 is notable in thisregard.

The countries in the region could reap worth-while economic benefits from increased regional-ism aimed at removing border barriers, accordingto analysis using the standard models for evaluatingbenefits from regional trading arrangements (Table1). As is typical in these models, the gains areshown to be greater the wider the country coverageand the wider the sectoral coverage of the regionalarrangements. Notably, the gains for ASEAN coun-tries are shown to be greater than those for theother countries in the region. Given that the lower-and middle-income countries of ASEAN are likelyto benefit less from China’s WTO accession thanthe newly industrializing economies, greaterregionalism in East Asia can help spread the gainsacross a wider set of economies.21

One danger with the current regional arrange-ments is that they have extensive provisions forexcluding sensitive sectors. Such exclusions couldsubstantially reduce the potential for welfare gainsfrom an agreement. Within AFTA, for example, thelack of progress in agriculture and other sensitivesectors has been disappointing. To give some indi-

xxiv East Asia Integrates

TABLE 1 Effects on Economic Welfare of Various Regional Trade Proposals

% of GDP (% of GDP excluding agricultural liberalization)

Proposal ASEAN China Korea, Rep. of Japan USA

China + Korea + Japan –0.26 (–0.16) +0.1 (–0.2) +1.0 (+0.6) +0.1 (+0.2) +0.0 (+0.0)ASEAN – China +0.9 (+0.5) +0.0 (+0.1) –0.1 (–0.1) +0.0 (+0.0) +0.0 (+0.0)ASEAN – Japan +1.1 (+0.2) –0.1 (–0.1) –0.2 (–0.1) +0.0 (+0.1) +0.0 (+0.0)ASEAN + 3 +1.5 (+0.6) +0.1 (–0.2) +1.1 (+0.8) +0.2 (+0.2) –0.1 (+0.0)ASEAN + 3 + CER +1.3 (+0.6) +0.0 (–0.1) +1.1 (+0.9) +0.2 (+0.2) –0.1 (+0.0)

APEC liberalization (MFN) +0.7 +0.5 +0.7 +0.4 –0.0

APEC preferential liberalization +0.8 +0.6 +0.9 +0.4 +0.0

Note: Calculations for ASEAN include only Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Viet-nam. CER (Australia–New Zealand Closer Economics Relations Trade Agreement) includes Australia and NewZealand. Figures in parentheses refer to net welfare effects when agriculture is excluded.Sources: Scollay and Gilbert (2003) for free trade agreement proposals and Scollay and Gilbert (2001) for APECliberalization proposals.

cation of the importance of this point, some eco-nomic models suggest that if agriculture is includedin the ASEAN-China or ASEAN + 3 proposals, theestimated welfare gains for ASEAN countriesroughly doubles (Table 1).

The greatest welfare gains, however, are likely tocome from addressing the deeper integrationagenda being proposed here. In particular, the ben-efits from integrating trade in services and over-coming technical barriers to trade are likely to bemany times those from reducing border barriersalone.22 Gains from liberalizing services trade arefelt not only within the services sector itself, butalso within other sectors because services are vitalinputs in their production processes. As manufac-turing in East Asia moves into a phase where partic-ipating in global markets will become moredependent on services, it increasingly will be heldback by poor efficiency in the services sector, whichhas been protected from competition. Services lib-eralization in East Asia lags relative to that of otherregions, and action to integrate trade in servicescould help restore its global competitiveness. Simu-lation results from China, consistent with findingsfrom other parts of the world, indicate that evensmall productivity gains of 1 percent in servicesoutweigh those based on static border trade effi-ciency gains alone.23

The policy scope for enhancing efficiency inservices, as well as in other sensitive sectors such asagriculture, may well be wider initially in a regionalcontext than in a global one. In fact, expandingintegration into these sectors is one of the mainpotential advantages of regional, as opposed toglobal, liberalization. Most regional partnershipsalready in place or under discussion include theservices and agriculture sectors, whereas these sec-tors have proven much harder to tackle in globaltalks. Because the liberalization of services may benecessary for industries to benefit fully from theremoval of regional barriers to goods trade, it maybe preferable to give the services sector a high pri-ority from the start of any negotiations.

Making East Asian Arrangements a Stepping-stone to Global Integration. Liberalization goalscan be well served by moving on multiple fronts. Inthe East Asian goods trade, traditional concerns thata regional arrangement will merely divert, ratherthan create, trade are less worrisome because a rela-

tively low-tariff bloc already exists, and becausemany of the region’s economies, especially the moredeveloped, are moving toward lower average tariffs.To generate momentum, measures can be takenbefore the parties agree on formal arrangements.The “Early Harvest” aspect of the ASEAN-ChinaFramework Agreement exemplifies this approach.As part of the Early Harvest, the agreement providesaccelerated access for key products to China andASEAN markets (ahead of the MFN schedule that ispart of the WTO accession agreement). Also, Chinahas extended most-favored-nation status to the low-income non–WTO Member countries Lao PDR andCambodia.

The challenge in pursuing regional integrationarrangements will be to avoid the “spaghetti bowl”effect of different rules and regulations associatedwith different agreements, which can add unneces-sary administrative costs to firms doing businessacross the region and result in a bloc-ed up world(Figure 6). Such costs can be especially high when ahost of bilateral agreements are put in place, withlarge numbers of side agreements that each permitsome discriminatory treatment. Inconsistenciesbetween agreements with overlapping membershipalso can become a problem. The exchange of ideason a regional basis can help avoid such difficulties.While, in theory, there are some reasons to expectthat uncoordinated bilateral and regional agree-ments build in incentives toward global free trade,this outcome depends crucially on maintaining acommon set of principles for each agreement—that is, focusing on trade facilitation measures;allowing the most liberal rules of origin; and gener-ally contributing positively to multilateral trade lib-eralization. For example, allowing for accumula-tion under rules of origin will be important to thefacilitation of production networks in the region,and allowing for multiple rules for conferring ori-gin would make it easier for more firms to partici-pate in regional trade (see Brenton 2003b).

Unless countries tackle the sensitive sectors inregional trade arrangements—and ultimately at theglobal level—many of the potential economic ben-efits alluded to earlier will not be realized. China’sbinding to low tariff levels as part of its agriculturalpolicy therefore offers scope for the liberalization ofagriculture in a regional setting, which could set inplace a favorable political dynamic for more openagricultural sectors throughout East Asia.

Overview xxv

Another way to proceed would be to unbundleproposed agreements into components for deeperintegration that could realistically be agreed on andwould yield immediate results in terms of increasedefficiency and development of intraindustry tradeand production networks. In the case of China andASEAN, for example, two-way business transac-tions are already proliferating, and—long beforegovernment policymakers began to act—busi-nesses had recognized and responded to the Chinachallenge. Such transactions could be facilitatedand enhanced by an agreement that focuses ontrade and investment facilitation, such as customs.

It also would be preferable to focus attentionand the resources of policymakers on as fewregional arrangements as possible but to makethem broad in scope and country coverage, espe-cially for small economies that have limited capac-ity to evaluate the development implications ofthese arrangements.

Finally, a further benefit from stronger regionalcooperation could be to link issues of commoninterest to an effective multilateral stance, whetherin services liberalization or discipline onantidumping measures.

Expanding Market Access Globally

One of the motivating factors behind the move toregional integration in East Asia is disappointmentwith the pace of multilateral trade liberalization inproducts of most interest to developing countries.

As discussed in Chapter 4, a consensus appears tobe growing about the negative impact on develop-ing countries of trade barriers on products that areexported by the poor—particularly agriculturalproducts and labor-intensive manufactures such astextiles and clothing, which are the sectors thatconfront the greatest entry barriers in high-incomecountries. One of the disappointments of theUruguay Round was its failure to achieve greatermarket access in these products. The Doha Devel-opment Agenda launched in November 2001 hasthe potential to make the world trading systemmore conducive to development. It includes a largenumber of policy reforms that can and should beundertaken by high-income countries and that willgenerate significant benefits for ordinary people indeveloping East Asia.

Trade in Textiles and Clothing. As noted earlier,the textiles and clothing sector poses a special chal-lenge for East Asia. Many countries of the regionhave large garment export businesses employingsizable numbers of low-skilled workers, many ofwhom are female. These businesses will be threat-ened by competition from China in the form ofboth a macroeconomic threat to the balance of pay-ments (from lost exports) and a social threat of lostjobs and lower wage incomes for many poor house-holds.

Implementation of agreements for further tradeliberalization in textiles and garments is critical tosocial stability in East Asia. Under the Agreement

xxvi East Asia Integrates

Average tariff rates: comparison of MFN with preferential rates

02468

1012

AFTAMFN

AFTACEPT(2002)

GlobalLDCsMFN

GlobalINDsMFN

Number of articles of agreement: recent East Asia initiatives

0

50

100

150

200

AFTA ASEAN–China

JSEPA

FIGURE 6 Regional Trade Arrangements

Note: AFTA = ASEAN Free Trade Area; MFN = most-favored nation; CEPT = common effective preferential tar-iff; LDCs = less developed countries; INDs = industrialcountries.Source: World Bank (2001a) and www. aseansec.org.

Note: JSEPA = Japan-Singapore Economic PartnershipAgreement.Source: www. aseansec.org and www.mofa.go.jp.

Low-tariff bloc reduces trade diversion. Multidimensional nature of agreements compounds“spaghetti bowl” and impedes merging.

on Textiles and Clothing as part of the UruguayRound, quota restrictions were to be graduallyabolished over a 10-year period (that is, no laterthat January 2005) in three stages, and the remain-ing quotas were to be subject to a progressiveincrease in their rates of expansion. However,implementation to date has been disappointing.Acceleration of the quota phase-out under the ATCwould have a significant impact on poverty by sus-taining or increasing employment in these indus-tries. It would help maintain export growth in low-income East Asia, for example, permitting 20percent more exports from Vietnam. It also wouldhelp protect workers in middle-income economiessuch as Thailand, where it would affect an esti-mated 50,000 jobs for garment workers and 10,000jobs for textile workers, about 20,000 of whom arefrom poor households. Finally, acceleration wouldbenefit workers in the textile and clothing sector inChina—workers who are mainly women drawnfrom poor, remote regions—and could result in 5million fewer poor Chinese overall.24

At the same time, some economies in East Asiawill lose. Garment industries in several countrieshave depended on quotas, benefiting from some ofthe rents accruing from preferential access to EUand U.S. markets. Garment exports from higher-income economies such as Korea are likely todecline. And in Cambodia, in particular, ATCimplementation is likely to put pressure onemployment and wages in the garment sector.Cambodia will have to pursue a broader agenda toopen up other trade opportunities.

Agricultural and Rural-Based Trade. Reduction oftrade barriers in agriculture is particularly impor-tant for poverty reduction. Agriculture is the mainlivelihood for poor households: for more than 90percent in Cambodia and Vietnam, more than 75percent in Indonesia, and roughly 70 percent inThailand and the Philippines (World Bank 2002a).

Gains from agricultural liberalization by higher-income countries are estimated at more than $10billion for developing East Asia, and that figuretriples once dynamic productivity gains are takeninto account.25 In contrast to the move towardincreased transparency in trade policy for manu-facturers, agriculture remains protected in myriadways, as laid out in Chapter 4. However, the directimpact of agricultural subsidies and domestic sup-

port programs in Europe and the United States onfarmers in East Asia is limited; such domestic pro-grams are heavily concentrated on meat, dairyproducts, and cereals.26 Thus with the notableexception of rice, East Asian farmers are notdirectly engaged in these distorted world markets.But other barriers in international agriculturalmarkets are important for East Asia, and four prac-tices of the developed countries are especiallyharmful. First, their use of specific rather than advalorem tariffs often leads to very high effectiveprotection, particularly on low-quality goods pro-duced by the poorest countries. Products such aspalm oil, rice, and sugar, as well as fish, crustaceans,and fruits and vegetables are the ones mostaffected. Second, developed countries use tariffsthat cascade upward on goods such as coffee andvegetables as protective devices for their agropro-cessing industries. Third, complex rules of originmake it hard for countries to avail themselves of allthe incentives theoretically made available to them.Fourth, conformance with health and safety regula-tions, notably maximum pesticide residue levels,and difficulties with understanding and adminis-tering standards are costly for many exportingcountries.

Agricultural trade barriers are not just an issuefor developed countries; the emerging economiesof East Asia also maintain high barriers. Regionalagricultural markets already are large. China’s com-mitment to a regime of low protection in agricul-ture is fortunate for other countries that are wellplaced to supply it with imports, providing a directboost to their foreign exchange earnings and to theincomes of poor households. The ASEAN-Chinatrade agreement, with its “Early Harvest” provi-sions, provides another avenue to ensure that pooragricultural households have every opportunity tobenefit from trade opportunities in the region.There may be further scope to address the sensitivefood security and safety issues initially within thecontext of East Asian arrangements.

Development Orientation for aBehind-the-Border Agenda

As WTO director general Supachai Panitchpakdieloquently stated in November 2002, “Trade poli-cies do not stand alone. Mutually supportive com-panion policies are also necessary.” Many of the

Overview xxvii

mechanisms required to maximize the develop-mental benefits of trade and investment liberaliza-tion are “behind-the-border” institutional and reg-ulatory reforms. Each of the new regional andbilateral partnerships reflects this business reality.Technical barriers and product standards, logistics,services sectors, intellectual property rights, com-petition policy, and environmental and labor stan-dards have become as important a part of the pri-vate sector environment as trade policy itself. These“behind-the-border” issues also are featuredprominently on the Doha Development Agenda.The thrust is to place trade policy within a broaderframework of development and poverty reduction.

Technical Barriers and Standards: Balancing Tradewith Consumer Interests

As the traditional barriers to market access decline,measures aimed at trade facilitation become morecritical. Conformity with health and safety stan-dards can be one of the most decisive determinantsof access.27 Many of the standards in use representlegitimate consumer interests, but the use of tech-nical regulations, such as standards, has risen tofurther commercial policy in multilateral, regional,and global trade. An important problem forexporters is that different national governmentsoften apply different technical specifications tomeet the same goal.

For East Asian developing countries, importingcountries’ sanitary and phytosanitary (SPS) stan-dards can impose significant additional costs thatimpede exports. For example, it has been estimatedthat application of the strictest EU standard ratherthan the international Codex Alimentarius standardfor aflatoxin has cost Thailand $350 million inexport losses in cereals and dried fruit, China $380million, and Vietnam $15 million. The adoption ofa Codex standard on tetracycline could doubleThailand and China’s beef exports (Otsuki and Wil-son 2001, 2002). Exporting countries also have tocontend with importers’ use of precautionary mea-sures, such as the EU import ban on geneticallymodified organisms (GMOs), which hurts Thai-land’s tuna exports as well as exports from China,which is the third largest GMO producer in theworld. Only some of these standards may be justi-fied on grounds of consumer safety and preferences;others may simply be protectionism in disguise.

The WTO rules in this area aim at ensuring thattechnical regulations, voluntary standards, andtesting and certification of products do not consti-tute unnecessary barriers to trade. Under the Sani-tary and Phytosanitary Standards (SPS) Agree-ment, WTO Members are encouraged to adoptinternationally recognized standards, but also arefree to apply stricter ones. Although the agreementrecognizes importing countries’ right to implementSPS measures that diverge from internationalnorms, it does require them to provide scientificjustification for such measures and applies riskassessment mechanisms.

In many cases, East Asian economies will wantto adopt unilaterally the international standardsbeing set.28 China is further strengthening its foodsafety regulations and capacity to implement theseregulations as part of its WTO accession and isadopting various authentications and labeling sys-tems. Compliance with SPS in export markets caninduce changes in production systems and supplychannels, but it is likely to require modernization ofstandards infrastructure as well as information andtraining. Countries may need to seek technicalassistance and support for additional projects inthis area. A Standards and Trade DevelopmentFacility to address this need is being established, tobe administered by WTO in collaboration with theWorld Bank, the World Health Organization(WHO), the UN Food and Agriculture Organiza-tion (FAO), Codex Alimentarius, and others.

At the same time, East Asian countries can bene-fit from rationalizing standards in a regional andglobal context. Cooperation on standards is one ofthe important issues generally encompassed inregional arrangements. Recognizing that foreignstandards can achieve the same level of social orconsumer protection as domestic standards,mutual recognition agreements (MRAs) are oneoption. Such agreements have mainly been usedbetween developed countries, but ASEAN currentlyhas signed two MRAs, with plans for an additional20 products, thus avoiding duplication of testingand conformity assessment.

Transport and Logistics

The commodity mix in East Asia is changing rap-idly from resource-based commodities to low- andmedium-technology goods to high-technology

xxviii East Asia Integrates

goods (Table 2). Logistics improvements, essentialfor moving up the value chain, have very high pay-offs in East Asia, as discussed in Chapter 5. High-value agriculture (flowers, fruits, seafood) andmanufacturing (electronics) demand sophistica-tion not only in production but also in logisticshandling. Timeliness matters, and a fast, reliablesupply chain is essential.

In East Asia, the key logistical bottlenecks seemto be high internal land transport costs and portlogistics. This situation is in sharp contrast to exter-nal transport costs: with the sharp decline in trans-Pacific shipping costs over the last decade, produc-

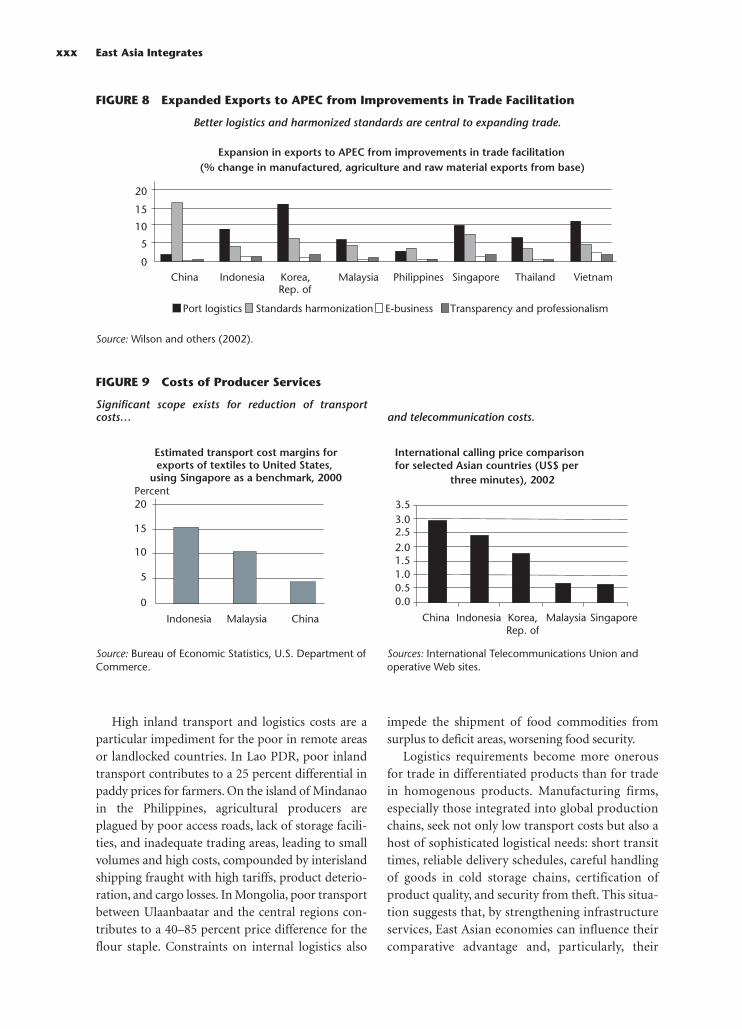

ers in many parts of East Asia can reach the U.S.market more cheaply than inland areas or neigh-boring countries. For example, the inland transportcosts of moving goods from some remote regionsof China to external markets are roughly 10 timesthe inland transport costs at the other end (Figure7). Port logistics have been identified as a high pri-ority (Figure 8). Considerable scope exists forreduction of transport cost margins (Figure 9).Modest improvements could lead to more than $50billion in additional exports from emerging EastAsia to the rest of APEC, with an even larger impacton efficiency of imports (Wilson and others 2002).

Overview xxix

TABLE 2 Structure of Manufactured Exports by Country, 1985 and 1996 (% by value)

Low-/medium- High-Resource-based technology technology

1985 1996 1985 1996 1985 1996Hong Kong (China) 2.1 4.4 78.5 66.7 19.4 28.9Singapore 42.3 12.7 25.4 21.9 32.3 65.4Korea, Rep. of 7.8 9.4 72.1 55.0 20.1 35.6Taiwan (China) 8.7 5.1 70.6 54.1 20.7 40.8Indonesia 72.2 34.9 25.1 50.4 2.7 14.7Malaysia 53.7 17.8 15.2 21.8 31.1 60.4Thailand 42.1 14.5 44.8 49.1 13.1 36.4China 11.7 9.8 78.9 69.7 9.4 20.5

Source: Lall (1998).

Logistics costs of container transport from Chongqing, Chinato the U.S. West Coast: breakdown of total cost of US$3,650 per

20-foot equivalent unit (TEU)

Maritime transport21%

Port to final destination

7%

Port handling (receiving)

4%

Land access to port63%

Port handling (sending)

5%

FIGURE 7 Inland Transport Costs for Remote Regions

Source: Carruthers and Bajpai (2002).

High inland transport and logistics costs are aparticular impediment for the poor in remote areasor landlocked countries. In Lao PDR, poor inlandtransport contributes to a 25 percent differential inpaddy prices for farmers. On the island of Mindanaoin the Philippines, agricultural producers areplagued by poor access roads, lack of storage facili-ties, and inadequate trading areas, leading to smallvolumes and high costs, compounded by interislandshipping fraught with high tariffs, product deterio-ration, and cargo losses. In Mongolia, poor transportbetween Ulaanbaatar and the central regions con-tributes to a 40–85 percent price difference for theflour staple. Constraints on internal logistics also

impede the shipment of food commodities fromsurplus to deficit areas, worsening food security.

Logistics requirements become more onerousfor trade in differentiated products than for tradein homogenous products. Manufacturing firms,especially those integrated into global productionchains, seek not only low transport costs but also ahost of sophisticated logistical needs: short transittimes, reliable delivery schedules, careful handlingof goods in cold storage chains, certification ofproduct quality, and security from theft. This situa-tion suggests that, by strengthening infrastructureservices, East Asian economies can influence theircomparative advantage and, particularly, their

xxx East Asia Integrates

Expansion in exports to APEC from improvements in trade facilitation(% change in manufactured, agriculture and raw material exports from base)

0

5

10

15

20

China Indonesia Korea,Rep. of

Malaysia Philippines Singapore Thailand Vietnam

Port logistics Standards harmonization E-business Transparency and professionalism

FIGURE 8 Expanded Exports to APEC from Improvements in Trade Facilitation

Source: Wilson and others (2002).

Better logistics and harmonized standards are central to expanding trade.