PT ASTRA INTERNATIONAL TBK - astra.co.id Mar 2017/AI Business Update 2016... · Astra does not...

36

Full Year 2016 – Results Presentation PT ASTRA INTERNATIONAL TBK

Transcript of PT ASTRA INTERNATIONAL TBK - astra.co.id Mar 2017/AI Business Update 2016... · Astra does not...

Full Year 2016 – Results Presentation

PT ASTRA INTERNATIONAL TBK

The materials in this presentation have been prepared by PT Astra International Tbk (Astra) and are generalbackground information about Astra Group business performances current as at the date of this presentation andare subject to change without prior notice.

This information is given in summary form and does not purport to be complete. Information in this presentation,including forecast financial information, should not be considered as advice or a recommendation to investors orpotential investors in relation to holding, purchasing or selling securities or other financial products or instrumentsand does not take into account their particular investment objectives, financial situation or needs. Before acting onany information, readers should consider the appropriateness of the information having regard to these matters,any relevant offer document and in particular, readers should seek independent financial advice.

This presentation may contain forward looking statements including statements regarding our intent, belief orcurrent expectations with respect to Astra businesses and operations, market conditions, results of operation andfinancial condition, capital adequacy, specific provisions and risk management practices. Readers are cautioned notto place undue reliance on these forward looking statements; past performance is not a reliable indication offuture performance. Astra does not undertake any obligation to publicly release the result of any revisions to theseforward looking statements to reflect events or circumstances after the date hereof to reflect the occurrence ofunanticipated events.

We disclaim any responsibility or liability whatsoever arising which may be brought or suffered by any person as aresult of acting in reliance upon the whole or any part of the contents of this report and neither Astra and/or itsaffiliated companies and/or their respective employees and/or agents accepts liability for any errors, omissions,negligent or otherwise, in this report and any inaccuracy herein or omission here from which might otherwisearise.

Disclaimer

1

2

For the years ended 31st December 2016

2016 2015 Change

Net revenue (Rp bn) 181,084 184,196 (2%)

Net income (Rp bn)* 15,156 14,464 5%

Net earnings per share (Rp) 374 357 5%

As at 31st

December 2016As at 31st

December 2015Change

Shareholders’ funds (Rp bn)** 111,951 102,043 10%

Net asset value per share (Rp)** 2,765 2,521 10%

* Net income is profit attributable to owners of the parent, i.e. Astra International shareholders.** Shareholders' funds and net asset value per share are based on equity attributable to owners of the parent.The financial results for the year ended 31st December 2016 and 2015 as well as the financial position as at 31st December 2016 and2015 have been prepared in accordance with Indonesian Financial Accounting Standards and are audited in accordance with theauditing standards established by the Indonesian Institute of Certified Public Accountants.

Higher Result in heavy equipment and

mining as well as agribusiness

Significant increase in loan loss provisions

reported by Permata Bank

Highlights

Net earnings per shareRp374

5% 56% 74%

Auto Market Share

Business Structure

Automobile• Toyota• Daihatsu• Isuzu• BMW• Peugeot• UD Trucks

Other

Motorcycle•Honda

Component•Astra

Otoparts

Others•AstraWorld

Automobile•Astra Credit

Companies•Toyota Astra

Finance

Motorcycle• Federal

InternationalFinance

Heavy Equipment • SAN Finance• Komatsu Astra

Finance

Banking• Bank Permata

Insurance• Asuransi Astra

Buana• Astralife

Construction Machinery• United Tractors• Traktor Nusantara

Mining Contracting• Pamapersada Nusantara

Coal Mining • Tuah Turangga Agung

Construction Industry• Acset Indonusa

Palm Oil Plantation• Astra Agro Lestari

Olein Refinery• Tanjung Sarana Lestari

• Kreasijaya Adhikarya

Commodity Trading• Astra-KLK Pte.Ltd

Cattle in Palm Oil Plantation• Agro Menara Rahmat

Toll Road• MMS• MHI• MTN• TMJ• TBS• LMS

Logistics• SERA / TRAC• Mobil88 • SELOG• TFSI

Water Utility• Palyja

Sea Port• Eastkal

Document Solution•Astra Graphia

IT Solution• Astra Graphia

Information Technology

Office Services• Astragraphia Xprins

Indonesia

• Menara Astra• Brahmayasa Bahtera• Samadista Karya• Astra Land Indonesia• Astra Modern Land

3

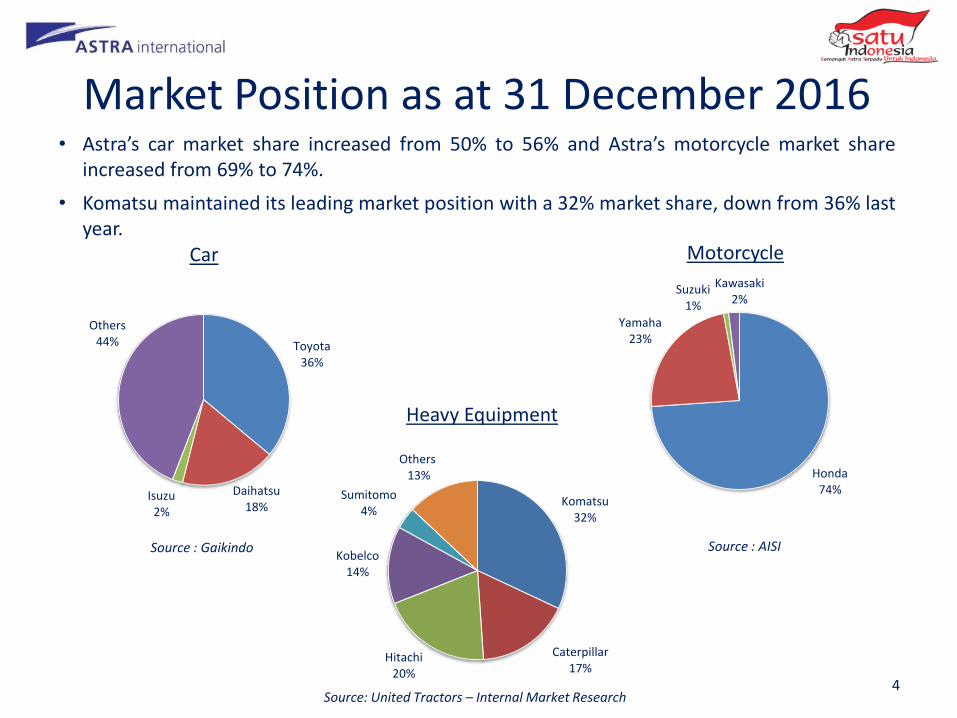

Toyota36%

Daihatsu 18%

Isuzu2%

Others44%

Car

• Astra’s car market share increased from 50% to 56% and Astra’s motorcycle market shareincreased from 69% to 74%.

• Komatsu maintained its leading market position with a 32% market share, down from 36% lastyear.

Source : Gaikindo

Honda74%

Yamaha23%

Suzuki1%

Kawasaki2%

Motorcycle

Source : AISI

Source: United Tractors – Internal Market Research

Heavy Equipment

Market Position as at 31 December 2016

4

Komatsu 32%

Caterpillar17%

Hitachi 20%

Kobelco14%

Sumitomo 4%

Others13%

5

Corporate Actions

Jun ‘16 • Permata Bank completed a rights issue which raised Rp5.5 trillion in order tostrengthen its capital base.

• General contractor Acset Indonusa, a 50.1% subsidiary of United Tractors,completed a rights issue raising Rp600 billion to support its business growth.

• Astra Agro Lestari completed a Rp4.0 trillion rights issue to strengthen itsbalance sheet.

Jul ‘16

Apr ‘16 • Astratel Nusantara acquired 25% stakes in PT Trans Bumi Serbaraja, a companythat operates 30km long Serpong Balaraja Toll Road.

• United Tractors, through PT Karya Supra Perkasa, established PT SupraAlphaplus Handal, a synergy in its construction business in manufacturing anddistributing concrete products.

6

Corporate Actions

Oct ‘16 • PT Astra Land Indonesia, owned 50% by Astra and 50% by Hongkong Land,signed an agreement with a subsidiary of PT Modernland Realty Tbk to acquireand jointly develop a 67-hectare site in Cakung, East Jakarta.

• UT, through PT Tuah Turangga Agung, signed a Conditional Shares and PurchaseAgreement (CSPA) to acquire coal mining company (coking coal) in CentralKalimantan, PT Suprabari Mapindo Mineral.

Dec‘16 • AAL and its subsidiary, PT Eka Dura Perdana, acquired all stakes in PT MitraBarito Gemilang, a rubber plantation company, rising AAL’s total rubberplantation land to 1,700 hectare.

Financial Performances

7

In Billion Rupiah 2016 2015 Change

IDR / USD, average 13,330 13,458 (1%)

Net Revenue 181,084 184,196 (2%)

Gross Profit 36,432 36,710 (1%)

Selling, General and Administrative Expenses

(18,898) (19,498) (3%)

Impairment Losses Related to MiningProperties

- (5,255) (100%)

Other Income 1,370 3,206 (57%)

Shares of Results of Joint Ventures andAssociates

3,349 4,467 (25%)

Income Tax Expenses (3,951) (4,017) (2%)

Non-controlling Interests (3,146) (1,149) 174%

Net Income 15,156 14,464 5%

“The Group’s underlying trading results for the year were satisfactory with steadyprogress seen in a number of areas. The outlook for 2017 appears positive with improvingeconomic conditions and the benefit of higher coal prices.”

- Prijono Sugiarto, President Director -

Consolidated Income Statement

8

2001 2014 2015 2016

Auto (Incl. autorelated Financial Services)

89% 63% 76% 85%

Non-Auto 11% 37% 24% 15%

Share of Net Income (%) Ownership %2016 2015

Auto Non-Auto Auto Non-Auto4W Automotive

SO – Toyota, Daihatsu, IsuzuToyota Astra MotorAstra Daihatsu MotorIsuzu Astra Motor Indonesia

100513250

34 31

2W AutomotiveAstra Honda MotorHonda SO

50100

24 19

ComponentAstra Otoparts 80 2 2

Financial ServicesAstra Sedaya FinanceFederal International FinanceToyota Astra Financial ServicesKomatsu Astra FinanceSAN FinanceAsuransi Astra BuanaPermata BankAstra Life

86100505060964550

25 (20)* 24 1

Heavy Equipment & MiningUnited TractorsPamapersada NusantaraTuah Turangga AgungAcset IndonusaTraktor Nusantara

6060603050

20 16

AgribusinessAstra Agro Lestari 80 11 3

Infrastructure, Logistics, IT & PropertyMarga MandalasaktiSERAPalyjaAstra GraphiaMenara AstraBrahmayasa BahteraSamadista Karya

791004977

10060

100

4 4

Astra Portfolio as at 31 December 2016

9* Permata Bank reported a loss of Rp6.5 trillion in 2016. (2015: Permata Bank net income of Rp247 billion).

• Astra’s net asset value per share of Rp2,765 at 31 December 2016 was 10% higher than at the end of2015.

• Net cash, excluding the Group’s financial services subsidiaries, was Rp6.2 trillion at 31st December2016, compared to net cash of Rp1.0 trillion at the end of 2015. The Group’s financial servicessubsidiaries had net debt of Rp47.7 trillion, compared to Rp44.6 trillion at the end of 2015.

In Billion Rupiah 31-Dec-16 31-Dec-15 Change

Cash and Cash Equivalents 29,357 27,102 8%

Trade Receivables 19,426 18,088 7%

Inventories 17,771 18,337 (3%)

Financing Receivables 64,639 60,105 8%

Investment in Joint Ventures and Associates 33,987 29,640 15%Fixed Assets 43,237 41,702 4%

Other Assets 53,438 50,461 6%

Total Assets 261,855 245,435 7%

Short-term Borrowings 18,764 11,975 57%

Trade Payables 22,489 20,557 9%

Long-term Debt 52,146 58,674 (11%)

Other Liabilities 28,550 27,696 3%

Total Liabilities 121,949 118,902 3%

Equity Attributable to the Owners of The Parent 111,951 102,043 10%

Non – controlling Interest 27,955 24,490 14%

Total Equity 139,906 126,533 11%

Net Debt 41,553 43,547 (5%)

Net Cash (Excl. Financial Services) (6,193) (1,034) 499%

Consolidated Balance Sheet

10

In Billion Rupiah 2016 2015 Change

Cash generated from operations 22,734 31,117 (8,383)

Tax Payments (4,706) (6,498) 1,792

Interest Received 1,379 1,280 99

Dividend Received 3,820 3,554 266

Net Cash flow provided from Operating Activities 23,227 29,453 (6,226)

Net Capex (8,368) (7,499) (869)

Net Investment (6,263) (2,251) (4,012)

Other Investing 13 (954) 967

Net Cash flow used in Investing Activities (14,618) (10,704) (3,914)

Net Proceeds / (Repayments) of Debt 2,685 (2,120) 4,805

Finance Costs Paid (2,042) (718) (1,324)

Dividend Payments (8,140) (10,585) 2,445

Other Financing 1,609 16 1,593

Net Cash flow used in Financing Activities (5,888) (13,407) 7,519

Increase in Cash 2,721 5,342 (2,621)

Opening Cash Balance (incl. Bank Overdraft) 27,072 20,728 6,344

Exchange Rate Adjustment (437) 1,002 (1,439)

Closing Cash Balance (incl. Bank Overdraft) 29,356 27,072 2,284

Consolidated Cash FlowAs at 31 December 2016, Astra’s ending consolidated cash balance (incl. Bank Overdraft)was Rp29.4 trillion.

11

Business Updates

12

Segment 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sedan 6% 6% 5% 4% 3% 3% 3% 2% 2% 1%

4x2 & 4x4 66% 64% 69% 67% 64% 67% 65% 57% 54% 58%

Commercial 28% 30% 26% 29% 33% 30% 28% 27% 28% 19%

LCGC 0% 0% 0% 0% 0% 0% 4% 14% 16% 22%

223318 281

427 483605 655 614

510 591211

290205

338411

511575 594

503471

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Astra Others

Lehman Crisis(↓20%)

LTV Policy(↑25%)

Historical Domestic Car Sales

In thousand units

In 2016, car sales grew due to many new products introduction, mostly coming from Astra’sbrand.

13

1,116

894

765

486

608

434

Source: Gaikindo

1,230 1,208

1,013

Weak GDP of 4.79% (↓16%)

1,062

Astra’s car sales were 10% higher at 421,000 units, resulting in an increase in market sharefrom 50% to 54%.

Automotive – Wholesale Car Market

Astra590,982 / 55.7% Astra

510,224 / 50.4%

Others470,877 / 44.3% Others

503,067 / 49.6%

4x2 & 4x4 612,835 / 57.7% 4x2 & 4x4

553,808 / 54.7%

Commercial200,530 / 18.9%

Commercial,276,627 / 27.3%

LCGC 235,171 / 22.1%

LCGC165,434 / 16.3%

Toyota382,610 / 36% Toyota

322,466 / 31.8%

Daihatsu 189,683 / 17.9% Daihatsu

167,808 / 16.6%

Isuzu, 16,848 / 1.6%

Isuzu, 19,350 / 1.9%

Other Brands470,877 / 44.3% Other Brands

503,067 / 49.6%

M/S2016

Market Segment Brand M/S2015

Market Segment Brand

Sedan17,422 / 1.7%

Sedan13,323 / 1.3%

2016 2015

1,013,2911,061,859

Astra’s car sales were 16% higher at 591,000 units, resulting in an increase in market sharefrom 50% to 56%.

5%

Source: Gaikindo14

Isuzu FVR 34 P HDOctober 2016

BMW i8August 2016

Toyota All New FortunerJanuary 2016

Daihatsu Hi-Max November 2016

In 2016, Astra has launched 14 new models and 9 revamped models.

Automotive – Car Product Launches

Astra Daihatsu SigraAugust 2016

Toyota SientaJuly 2016

15

2,141 2,875 2,701

3,416 4,274 4,089 4,697 5,051 4,454 4,381

2,547

3,341 3,151

3,957 3,739

2,975 3,047 2,816

2,026 1,550

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Astra OthersIn thousand units

Segment 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Cub 73% 63% 52% 45% 37% 26% 19% 16% 12% 9%

Scooter 18% 26% 39% 46% 52% 60% 63% 68% 75% 79%

Sport 9% 11% 9% 9% 11% 14% 18% 16% 13% 12%

Historical Domestic Motorcycle SalesWholesale market for motorcycles decreased by 8% to 5.9 million units in 2016.

Scooter matic segment continues to dominate the motorcycle market.

16

4,688

7,373

5,8526,216

8,013

7,064

Lehman Crisis(↓6%)

Source: AISI

7,8677,744

LTV Policy(↓12%)

6,480

Weak GDP of 4.79% (↓16%)

5,931

•

•

Honda4,380,888

73.9%

Honda 4,453,888

68.7%

Yamaha1,394,078

23.5%

Yamaha1,798,630

27.8%

Kawasaki 1.6%Suzuki 1.7%

Kawasaki 1.8%

Cub363,906

8.3%

Cub404,872

9.1%

Scooter3,661,284

83.6%

Scooter3,750,803

84.2%

Sport/Others8.1%

Sport/Others6.7%

Cub363,90669.7%

Cub404,87255.4%

Scooter3,661,284

78.1%

Scooter3,750,803

76.9%

Sport/Others49.3%

Sport/Others34.2%

Cub522,082

8.8%

Cub522,08211.3%

Scooter4,688,004

79%

Scooter4,688,004

75.3%

Sport/Others12.2%

Sport/Others13.4%

Brand2016

Honda Segment Honda Product M/S

Segment Brand2015

Honda Segment Honda Product M/S

Segment

Source: AISI

2016 2015

6,480,1555,931,285

Astra Honda Motor’s domestic sales were 2% lower at 4.4 million units; however, its marketshare increasing from 69% to 74%.

Automotive – Wholesale Motorcycle Market

8%

17

Suzuki 1%

Honda CBR150RFebruary 2016

Honda Vario 150 eSPFebruary 2016

Honda Supra GTR 150May 2016

Automotive – Motorcycle Product LaunchesIn 2016, Astra Honda Motor has launched 7 new models and 8 revamped models.

Honda BeAT Sporty EspAugust 2016

Honda CB 150 Street fireAugust 2016

Honda CBR 250 RRJuly 2016

18

188

287

230 31

Shares of Results of Joint Ventures & AssociatesConsolidated Income

48% 48%

42%41%

10%11%

Export After Market OEM

Net Income (IDR billion)

319

Revenue (IDR billion)

9%

2016 2015 2016 2015

11,72412,807

418

Net income at Astra Otoparts, the Group’s component business, increased 31% to Rp418billion, with higher revenue from its OEM and aftermarket segments combined with higherearnings contribution from its associated companies.

Automotive – Components

31%

19

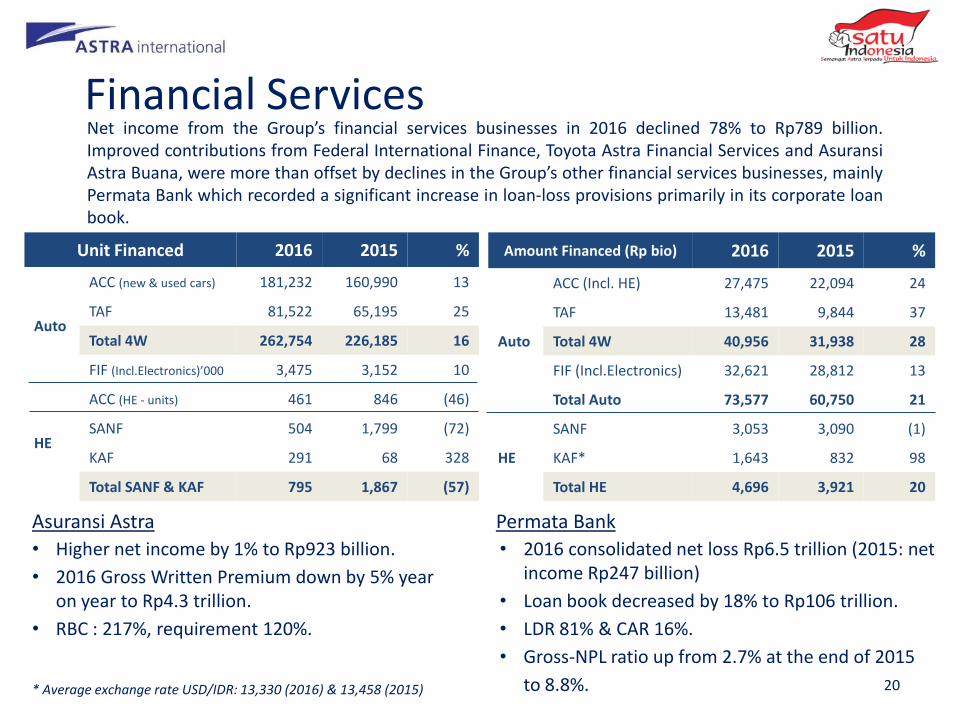

Net income from the Group’s financial services businesses in 2016 declined 78% to Rp789 billion.Improved contributions from Federal International Finance, Toyota Astra Financial Services and AsuransiAstra Buana, were more than offset by declines in the Group’s other financial services businesses, mainlyPermata Bank which recorded a significant increase in loan-loss provisions primarily in its corporate loanbook.

Amount Financed (Rp bio) 2016 2015 %

Auto

ACC (Incl. HE) 27,475 22,094 24

TAF 13,481 9,844 37

Total 4W 40,956 31,938 28

FIF (Incl.Electronics) 32,621 28,812 13

Total Auto 73,577 60,750 21

HE

SANF 3,053 3,090 (1)

KAF* 1,643 832 98

Total HE 4,696 3,921 20

• 2016 consolidated net loss Rp6.5 trillion (2015: net income Rp247 billion)

• Loan book decreased by 18% to Rp106 trillion.

• LDR 81% & CAR 16%.

• Gross-NPL ratio up from 2.7% at the end of 2015

to 8.8%.

Asuransi Astra

• Higher net income by 1% to Rp923 billion.

• 2016 Gross Written Premium down by 5% year on year to Rp4.3 trillion.

• RBC : 217%, requirement 120%.

Permata Bank

Unit Financed 2016 2015 %

Auto

ACC (new & used cars) 181,232 160,990 13

TAF 81,522 65,195 25

Total 4W 262,754 226,185 16

FIF (Incl.Electronics)’000 3,475 3,152 10

HE

ACC (HE - units) 461 846 (46)

SANF 504 1,799 (72)

KAF 291 68 328

Total SANF & KAF 795 1,867 (57)

Financial Services

* Average exchange rate USD/IDR: 13,330 (2016) & 13,458 (2015) 20

Historical Heavy Equipment Market

3,454 4,345 3,111

5,404

8,467 6,202

4,203 3,513 2,124 2,181

3,584

5,339

3,533

6,377

8,893

8,219

6,049 5,354

3,788 4,663

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Others Komatsu

6,8447,038

9,684

6,644

11,781

17,360

14,421

Market Share 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Komatsu 49% 45% 47% 46% 49% 43% 41% 40% 36% 32%

Caterpillar 22% 23% 21% 16% 18% 19% 19% 18% 22% 17%

Hitachi 16% 17% 18% 19% 15% 21% 21% 20% 18% 20%

Others 13% 15% 14% 19% 18% 17% 19% 22% 24% 31%

21

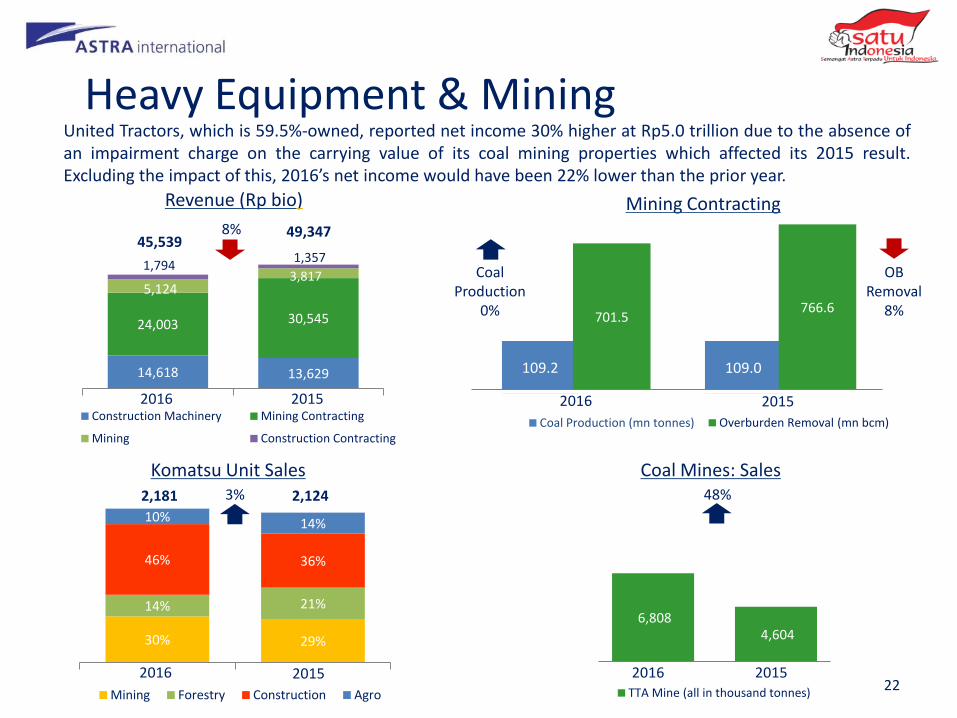

Heavy equipment market in 2016 slightly improved due to better coal price index in thefinal quarter of the year.

In Units

Source: UT’s internal research

10,2528,867

5,912

•

22

6,808 4,604

TTA Mine (all in thousand tonnes)

109.2 109.0

Coal Production (mn tonnes)

701.5 766.6

Overburden Removal (mn bcm)

14,618 13,629

24,003 30,545

5,124 3,817

1,794 1,357

Construction Machinery Mining Contracting

Mining Construction Contracting

30% 29%

14% 21%

46% 36%

10% 14%

Mining Forestry Construction Agro

Mining Contracting

Coal Mines: SalesKomatsu Unit Sales2,124

Revenue (Rp bio)

2016 2015 2016 2015

2016 2015 2016 2015

8%

Coal Production

0%

OB Removal

8%

48%3%

United Tractors, which is 59.5%-owned, reported net income 30% higher at Rp5.0 trillion due to the absence ofan impairment charge on the carrying value of its coal mining properties which affected its 2015 result.Excluding the impact of this, 2016’s net income would have been 22% lower than the prior year.

Heavy Equipment & Mining

45,53949,347

2,181

17.3 19.4 21.0 22.1 24.3 26.9 28.5

31.3 33.4 31.8

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

In million tonnes

Historical Palm Oil Production

23

Palm Oil Area 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Mature (Million hectare)

4.54 4.95 5.37 5.74 6.08 6.65 7.72 8.15 8.63 9.13

Yields (T/Ha) 3.80 3.92 3.91 3.85 4.00 4.05 3.69 3.84 3.61 3.22

The growth of Indonesia’s CPO production is mainly due to the added planted areas by the palmoil producers in Indonesia during commodities boom in 2010.

Source : Oil World (as of 16 December 2016)

•

24

266 258

31 39

Immature

Mature1,554 1,737

1,014 1,042

320 412

Production Sales Olein Sales

3.84 4.68

9,422 8,693

4,700 4,366

Export

Local

Area Maturity (‘K Ha)*

Revenue (Rp bio)

CPO Production & Sales (‘K tonnes)297 298

* Incl. plasma plantation

CPO Yield (tonne/Ha)

13,059

2016 2015

8% 18%

CPO Production

11%

14,122

2016 2015

2016 2015 2016 2015

CPO Sales 3%

Astra Agro Lestari, which is 79.7%-owned, reported net income of Rp2.0 trillion, up from Rp619 billion,due to improved revenue from higher crude palm oil prices and the benefit of the stronger rupiah on thetranslation of its US dollar monetary liabilities.

Agribusiness

23,853 24,573

SERA Unit in Contract (unit)

47,829 46,475

MMS Vehicle Traffic Volume (‘K unit)

2016 2015

2016 2015

3%

3%

The 72.5km Tangerang-Merak toll road, operated by79.3%-owned Marga Mandalasakti, saw trafficvolume increase by 3% to 48 million vehicles.

Serasi Autoraya’s net income increased by 96% toRp100 billion, due to higher net margins in its carleasing and rental, used vehicle sales and logisticsbusinesses, despite a 3% decline in contracted vehiclesin its car leasing and rental business.

Infrastructure & Logistics

25

59% 61%

41% 39%

Astragraphia Revenue (Rp bio)

2016 2015

AGDS

1%

2,713 2,655

Information Technology

AGIT

7%

255 265

Astragraphia Net Income (Rp bio)

2016 2015

4%

Astra Graphia, which is 76.9%-owned, reported a 4% decline in net income to Rp255 billion, despite an increase in revenue mainly due to lower net margins.

26

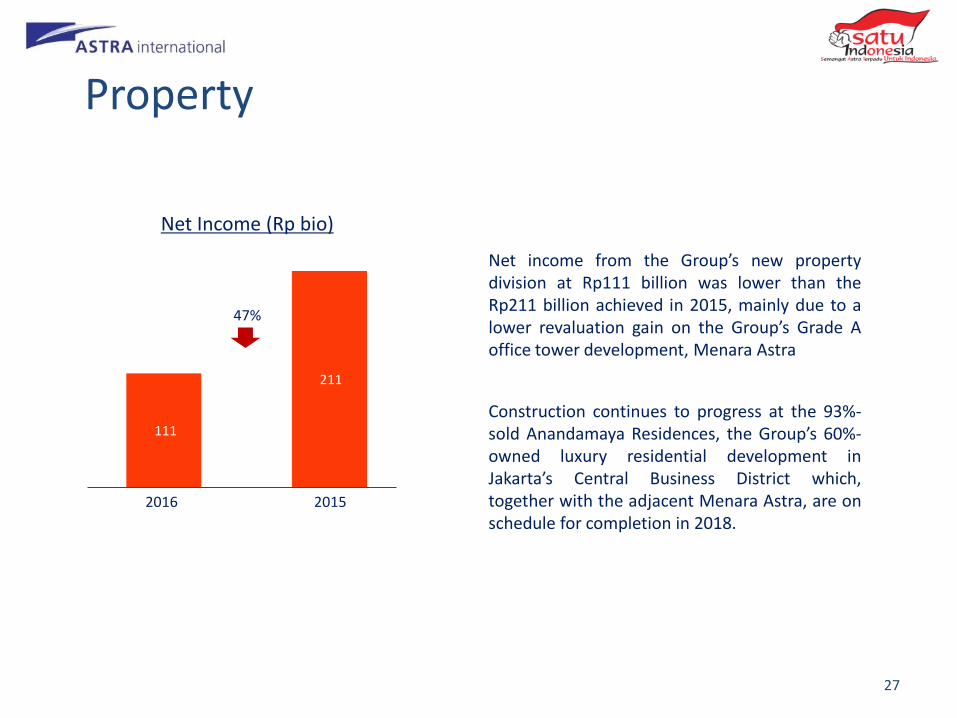

111

211

Net Income (Rp bio)

2016 2015

Property

Construction continues to progress at the 93%-sold Anandamaya Residences, the Group’s 60%-owned luxury residential development inJakarta’s Central Business District which,together with the adjacent Menara Astra, are onschedule for completion in 2018.

47%

Net income from the Group’s new propertydivision at Rp111 billion was lower than theRp211 billion achieved in 2015, mainly due to alower revaluation gain on the Group’s Grade Aoffice tower development, Menara Astra

27

Appendices

28

In Billion Rupiah 2016 2015 Change

Automotive 94,440 95,434 (1%)

Financial Services 17,762 17,074 4%

Heavy Equipment & Mining 45,112 49,209 (8%)

Agribusiness 14,121 13,059 8%

Infrastructure & Logistics 7,189 6,935 4%

Information Technology 2,451 2,474 (1%)

Property 9 11 (18%)

Total 181,084 184,196 (2%)

Divisional Net Income

In Billion Rupiah 2016 2015 Change

Automotive 9,166 7,464 23%

Financial Services 789 3,555 (78%)

Heavy Equipment & Mining 3,032 2,342 30%

Agribusiness 1,599 493 224%

Infrastructure & Logistics 263 195 35%

Information Technology 196 204 (4%)

Property 111 211 (47%)

Total 15,156 14,464 5%

Divisional Net Revenue and Net IncomeDivisional Net Revenue

29

Models Launched Launching Period Engine Capacity Prices (Rp mio)

Toyota All New Fortuner Jan’16 2,400cc-2,700cc 442-631.5

Daihatsu Sirion Sport Jan’16 1,300cc 168.3-179.3

Toyota Rush Feb’16 1,500cc 237.8-262.5

Daihatsu Terios Feb’16 1,500cc 228.1-242.2

Lexus GSF Mar’16 2,000cc 1,245

Lexus GS Mar’16 2,000cc 1,185

Lexus LX Mar’16 5,700cc 3,015

BMW M2 Apr’16 3,000cc 1,349*

Isuzu NMR 71T May’16 4,500cc 387.5-302.5

BMW X1 18i May’16 1,500cc 619*

BMW X1 18i xLine May’16 1,500cc 659*

Toyota Sienta Jul’16 1,500cc 230-295

BMW i8 Aug’16 1,500cc 3,499*

Astra Daihatsu Sigra Aug’16 1,000cc-1,200cc 106.6-147.4

Astra Toyota Calya Aug’16 1,200cc 132.5-150

Isuzu MU-X 2.5 VGS Aug’16 2,500cc 448-478

Isuzu D-MAX 2.5 VGS Aug’16 2,500cc 341-514.5

Car Products Launched in 2016

*off the road price

30

Models Launched Launching Period Engine Capacity Prices (Rp mio)

Isuzu FTR 90 T Oct’16 5,193cc 515

Isuzu FVR 34 P HD Oct’16 7,790cc 604.5

Isuzu LT1 34 (Big Bus) Oct’16 7,790cc 700

Toyota Vios Oct’16 1,500cc 272.4-323.8

Toyota Yaris Nov’16 1,500cc 228.3-277.3

Daihatsu Hi-Max Nov’16 1,000cc 95.3-103.3

Car Products Launched in 2016

31

Models Launched Launching Period Engine Capacity Prices (Rp mio)

Honda BeAT POP eSP Jan’16 110cc 14.3-15

Honda CBR 150 R Feb’16 150cc 32.5-33.3

Honda CBR 500 R Feb’16 500cc 144

Honda PCX 150 Feb’16 150cc 39.8

Honda Vario 150 eSP Feb’16 150cc 20.7

Honda Vario 125 eSP Feb’16 125cc 17.7-18.3

Honda CB 500 F Feb’16 500cc 133-139

Honda CB 500 X Feb’16 500cc 147

Honda CB 650 F Feb’16 650cc 235

Honda Supra GTR 150 May’16 150cc 21.3-21.5

Honda CBR 250 RR Jul’16 250cc 47.8-56.2

Honda BeAT Sporty eSP Aug’16 110cc 14.7-15.4

Honda CB 150 R Street Fire Aug’16 150cc 25.6-26.6

Honda Sonic 150R Aug’16 150cc 21.4-22

Honda BeAT Street eSP CBS Oct’16 110cc 15.4

Motorcycle Products Launched in 2016

32

National Market Data2016 2015

Major BrandsWholesale Astra Wholesale Astra

Car

Non LCGC 826,564 51.7% 847,857 49.2%Toyota – Avanza, Innova, Fortuner; Honda – HR-V, Mobilio, BR-V, Daihatsu – Xenia, Terios, Gran Max

LCGC 235,171 69.4% 165,434 56.1%Astra Toyota – Calya, Agya; Astra Daihatsu – Sigra, Ayla; Honda - Brio Satya; Datsun - GO Panca; Suzuki - Karimun Wagon R

Total 1,061,735 55.7% 1,013,291 50.4%

Mo

torc

ycle

Cub 522,082 69.7% 731,166 55.4%Honda - Supra Series, Revo Series, Blade; Yamaha –Jupiter MX King, Jupiter ZX, Vega Force; Suzuki –Smash; Kawasaki - ZX130, Edge

Scooter 4,688,004 78.1% 4,877,725 76.9%Honda - BeAT, Vario, Scoopy; Yamaha - Mio, N-Max,Fino; Suzuki – Address, Nex

Sport & Others 721,199 49.3% 871,264 34.2%Honda - CB 150 R Street Fire, Verza, CBR 150R, Sonic 150R; Yamaha - V-ixion R - 15, Xabre, Byson; Suzuki - Satria F 150; Kawasaki – Ninja

Total 5,931,285 73.9% 6,480,155 68.7%

33

No Brokerage Analyst Email

1 Bahana Securities Leonardo Henry Gavaza [email protected] 2 BCA Sekuritas Darmawan Halim [email protected] CIMB Securities Indonesia Erindra Krisnawan [email protected]

4 Ciptadana Securities Arief Budiman [email protected]

5 Citigroup Investment Research Ferry Wong [email protected] 6 CLSA Indonesia Sarina Lesmina [email protected] 7 Credit Suisse Securities Indonesia Jahanzeb Naseer [email protected]

8 Danareksa Sekuritas Stefanus Darmagiri [email protected]

9 DBS Vickers Maynard Priajaya Arif [email protected]

10 Deutsche Verdhana Securities Reggy Susanto [email protected]

11 Goldman Sachs Pramod Kumar [email protected]

12 HSBC Tarun Bhatnagar [email protected]

13 IndoPremier Securities Chandra Pasaribu [email protected]

14 J.P. Morgan Aditya Srinath [email protected]

15 Mandiri Sekuritas Ariyanto Kurniawan [email protected]

16 Macquarie Capital Securities Jayden Vantarakis [email protected]

17 Maybank Kim Eng Securities Isnaputra Iskandar [email protected]

18 Merrill Lynch Swati Chopra [email protected] MNC Securities Edwin Sebayang [email protected]

20 Morgan Stanley Andri Ngaserin [email protected]

21 Nomura Indonesia Elvira Tjandrawinata [email protected]

22 Onix Capital Bagus Hananto [email protected]

23 Reliance Securities Robertus Yanuar Hardi [email protected]

24 RHB OSK Securities Indonesia Andrey Wijaya [email protected] 25 Samuel Sekuritas Akhmad Nurcahyadi [email protected]

26 Trimegah Securities Frederick Daniel [email protected]

27 UBS Securities Indonesia Ronald Liem [email protected]

28 UOB Kay Hian Securities Stevanus Juanda [email protected] Valbury Asia Securities Budi Rustanto [email protected] Yuanta Securities Indonesia Kim Kwi Sjamsudin [email protected]

Equity Research Contact Details

34

For further information please contact:

PT Astra International Tbk

Corporate Investor Relations

P: (+62 21) 652 2555

F: (+62 21) 6530 4953

35