Psychology and Personal Finance Class 4 - Debt. Class 4 Overview Debt Options Debt Behavior Subprime...

42

Psychology and Personal Finance Class 4 - Debt

-

date post

22-Dec-2015 -

Category

Documents

-

view

221 -

download

4

Transcript of Psychology and Personal Finance Class 4 - Debt. Class 4 Overview Debt Options Debt Behavior Subprime...

Psychology and Personal Finance

Class 4 - Debt

Class 4 Overview

• Debt Options

• Debt Behavior

• Subprime Crisis and Policy Discussion

• Debt and Entrepreneurship

2

Why Debt?

• Economics Reasoning– Income smoothing (Permanent Income

Hypothesis)– Liquidity

• Behavioral Reasoning– Immediate gratification– Lack of budgeting– Innumeracy– Mental accounting

3

Debt Options

Federally Subsidized Student Loans

• Based on need, available to students

• Interest-free while in school

• Low 4 - 5% interest rate post-graduation

5

401k

• Borrowing from yourself (up to $50k)

• Loan details may vary depending on intent (general purpose vs. housing purchase, etc)

• Interest is the opportunity cost of your retirement investments

6Source: http://www.smartmoney.com/debt/calculator/index.cfm?story=borrow401k&hpadref=1

Mortgages

• Fixed / Adjustable rate mortgages

• Negative amortization – loan payment is less than interest charged over a period

• Interest rate after taxes of ~4-5%

7

Home Line of Credit

• Revolving line of credit in which the home acts as collateral

• Limited withdrawals

• Typical interest rate of prime plus 4% - can change over time

8Source: http://www.federalreserve.gov/Pubs/equity/equity_english.htm

Credit Cards

• Free if you repay regularly

• Interest rate from 0% (teaser) to 40% with a mode of 25%

9

Pawn Shops

• Use your possessions as collateral for cash

• Loan size is ~50% the value of your possession

• Typical interest rate of 25 - 60%

10Source: Caskey and Zikmund (1990)

Rent-To-Own

• Obtain goods via a regular payment plan where the goods and payments are collateral

• Typically end up paying 2-4 times the cost

• Typical interest rate of ~230%

11Source: Zikmund, et. al (1990)

Payday Loans

• Get a 1 – 2 week advance on your salary

• Typical interest rate of 391% plus fees

12Source: www.wikipedia.org

The Mob

• Use your kneecaps as collateral

• Everything is done on the mob’s terms

• Typical interest rate is what they say it is!

13

Sopranos Clip

14

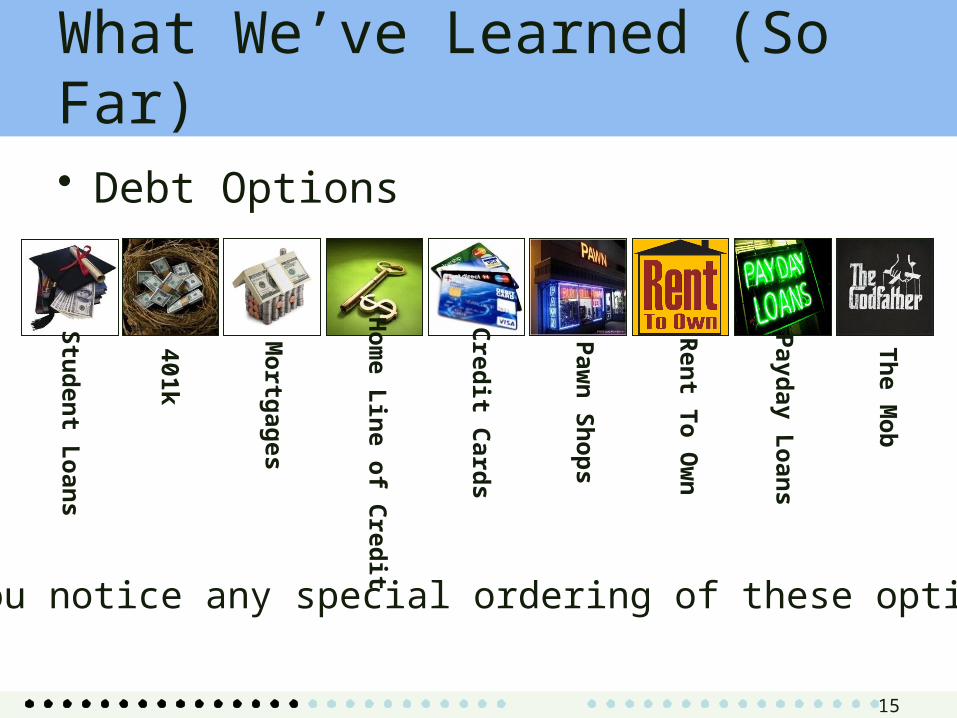

What We’ve Learned (So Far)

15

Do you notice any special ordering of these options?

• Debt Options

Student Loans

401k

Mortgages

Hom

e Line of Credit

Credit Cards

Pawn Shops

Rent To Ow

n

Payday Loans

The Mob

Debt Behavior

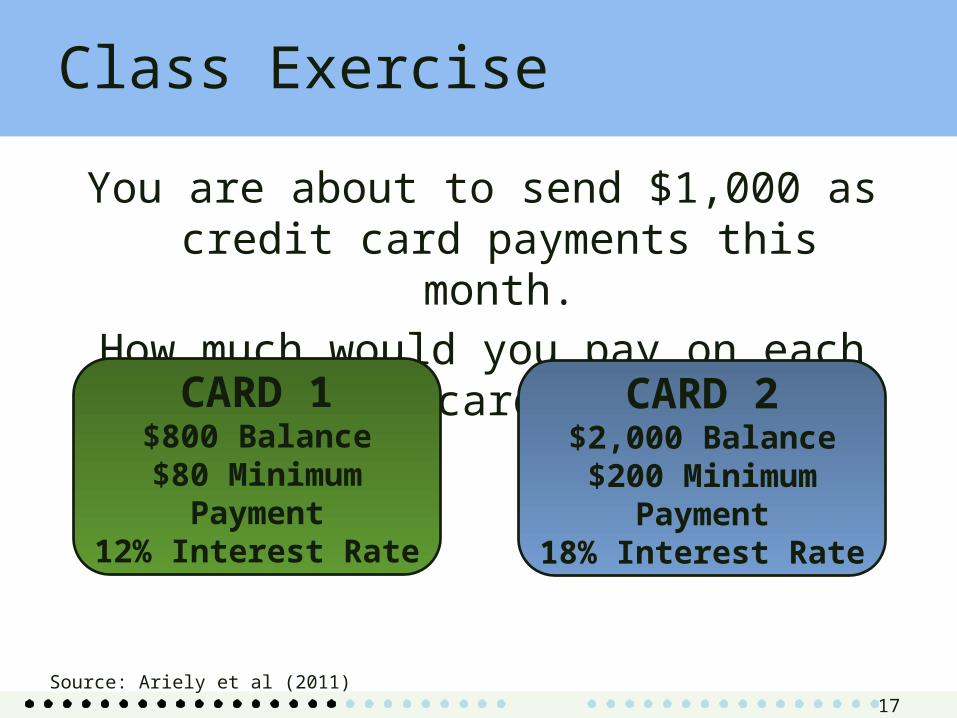

Class Exercise

You are about to send $1,000 as credit card payments this month.

How much would you pay on each card?

17

Source: Ariely et al (2011)

CARD 1$800 Balance

$80 Minimum Payment12% Interest Rate

CARD 2$2,000 Balance

$200 Minimum Payment18% Interest Rate

Debt Aversion

• Average 4 yr student loan debt is only $16,700• 26% of low income students and 31% of Asians

don’t even apply• Some people tend to pay off low rate loans

faster than required, even when there are better investment opportunities available

18Sources: Burdman (2005), Cadena, et al (2006)

Excessive Debt

• Debt / income ratio closely linked with anxiety

• Average credit card debt increased 300% (in households with at least one card) between 1990 and 2002

WHY?

19Sources: Dretna (2000), Money Central at www.msn.com

Someone Else Will Do It

• Myopia & Optimism– www.savekaryn.com – Karyn started a website in 2002 to

convince individuals to donate money to help her pay off card debt

– She did so in only 20 weeks – chances are you won’t be this lucky!

20

The Wrong Type Of Debt

• Households who shifted to 401(k) debt would save 15% on annual debt payments

• Rent-to-own is used as a budgeting mechanism for risk averse consumers

• Payday loans stem from myopia, innumeracy, self-control and budgeting

21Sources: Li and Smith (2008), Zikmund, et al (1999)

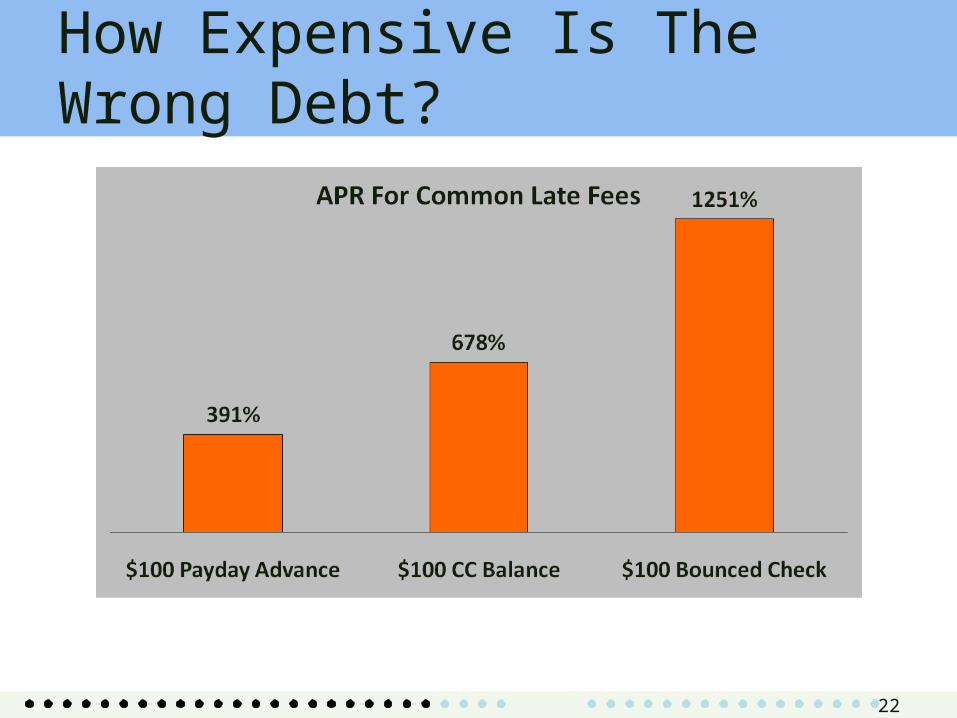

How Expensive Is The Wrong Debt?

22

Simpsons Clip

23

People Are Clueless!

24

What We’ve Learned (So Far)

• Debt Options

• Debt Behavior– Debt aversion– Excessive debt– Wrong type of debt– People are clueless

25

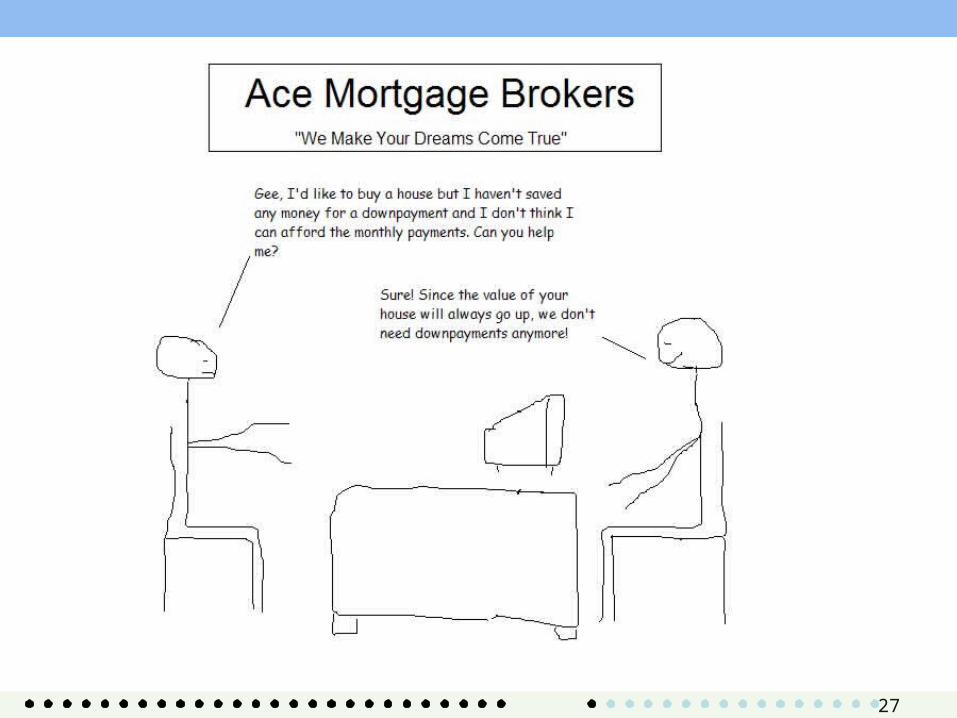

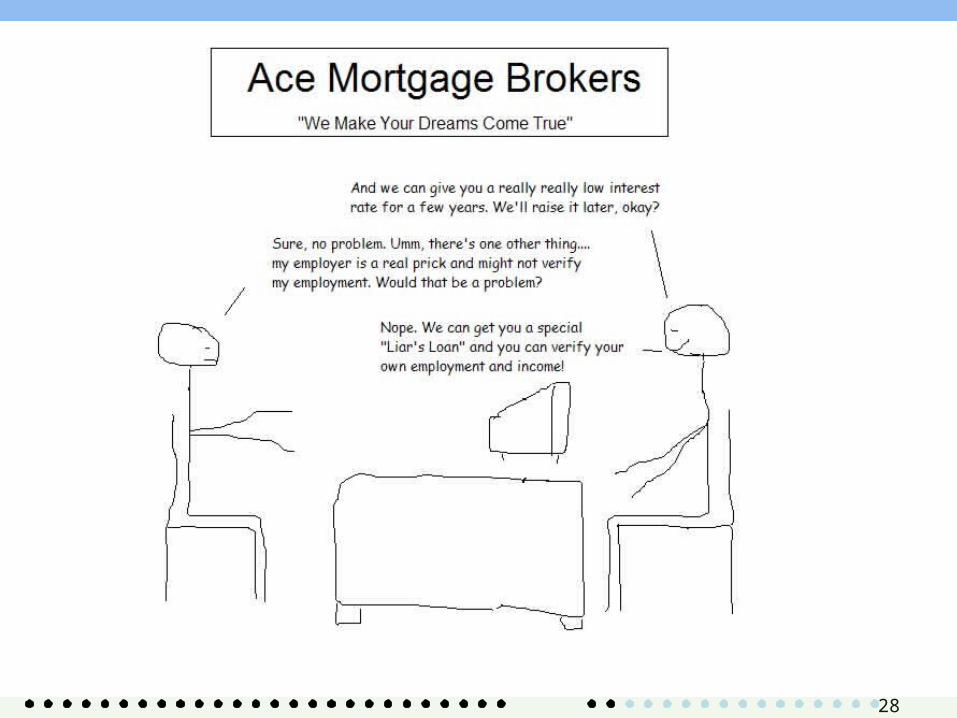

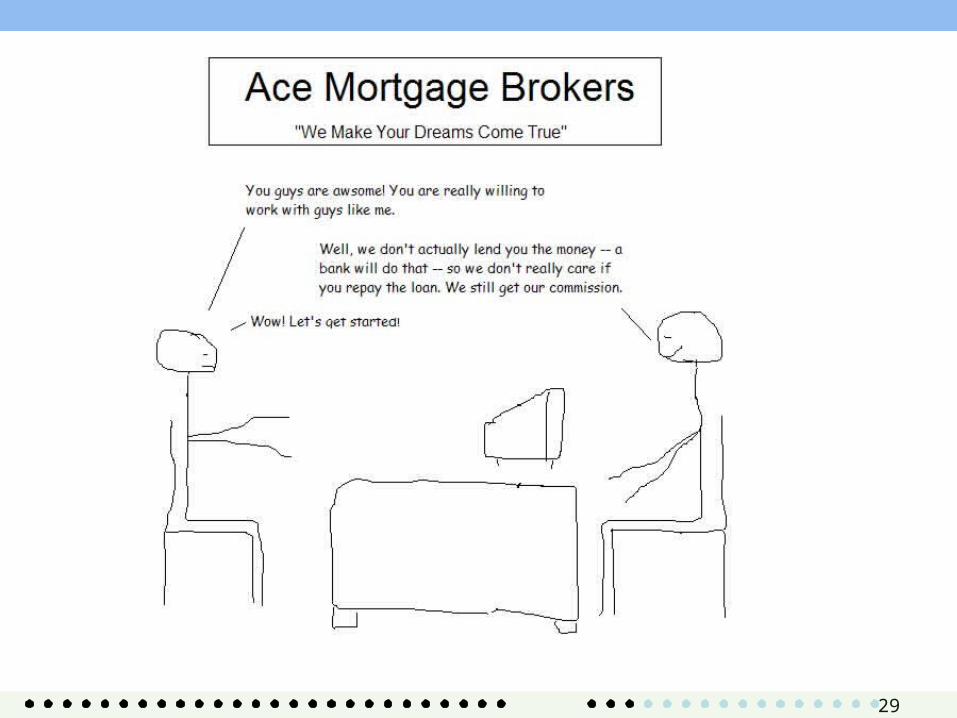

Subprime Crisis and Policy Discussion

27

28

29

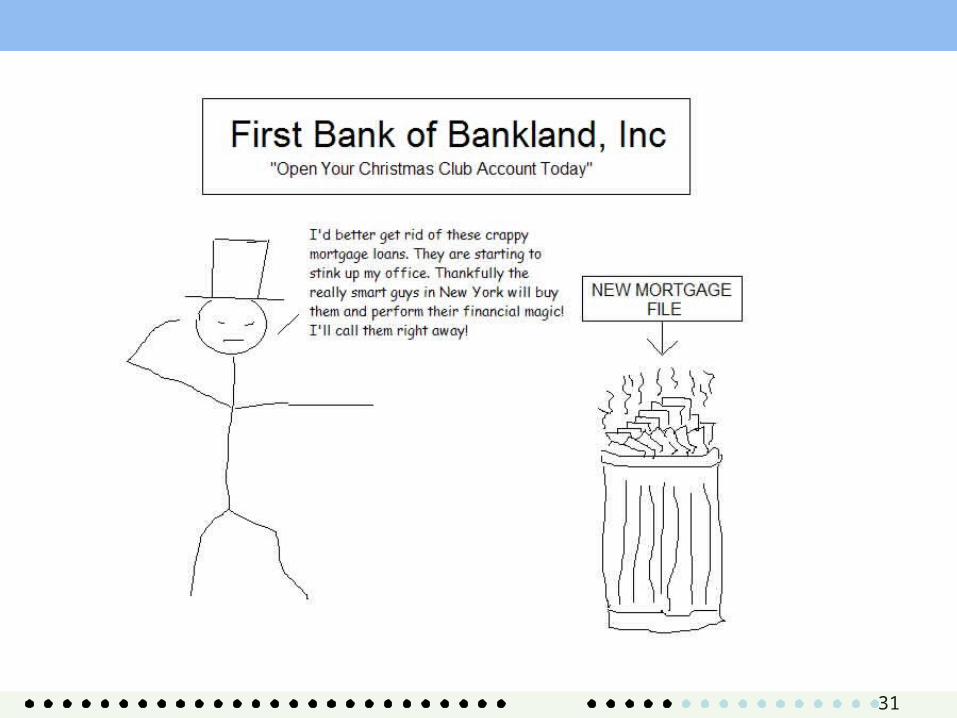

A few weeks later at the bank…

30

31

Class Discussion

Policy Discussion from Thaler & Sunstein:

Is it complexity/cheating on the part of the firm OR

Too much hope on the part of the consumer?

What should the policy be?

32

What We’ve Learned (So Far)

• Debt Options

• Debt Behavior

• Subprime Crisis and Policy Discussion

33

Debt and Entrepreneurship

Issues With Current Debt Options

• Borrowing– From banks : high rates, may not qualify, rigid

constraints

– From friends / family: uncomfortable, risk of damaging the relationship, no regulation

– From 3rd parties: transaction costs

35

Issues With Current Debt Options

• Lending– To banks: very low rates

– To friends / family: damage relationships, collection is unpleasant and not regulated

– To 3rd parties: transaction costs, legal enforcement complexities

36

Virgin Money

• Mediators for borrowing and lending money between family and friends

• The company handles legal enforcement

• Also offers real estate, personal, business and student loans

37

Prosper

• Matching service, similar to online dating

• Potential borrowers and lenders post offers

• Allows for more flexibility and smaller transaction costs

38

Zopa

• UK based matching service that obviates negotiation

• You propose a loan, they rate your risk factor– Student loan = A– Business Startup = B– Pay off credit cards = D

• Zopa sets the rate for grades and acts as the middleman

39

Class Discussion

What are the merits and issues with these services / products?

Can you think of another service / product that might be useful?

40

What We’ve Learned

• Debt options

• Debt Behavior

• Subprime Crisis and Policy Discussion

• Debt and Entrepreneurship

41

Assignment 2

Suggest how individuals could practically track their expenses for budgeting purposes.

You might find it useful to try and track your own expenses for a week or two.

Alternatively, if you feel this is impossible, then explain why.

42