Protecting and growing a portfolio with convertible bonds

9

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010 Protect and Grow Wealth with Convertible Bonds A Way to Improve Yields with Lower Risks in Any Investor’s Portfolio Prepared by: Steve Stanganelli, CFP ® , CRPC ® CERTIFIED FINANCIAL PLANNER (TM) Professional Clear View Wealth Advisors, LLC, a Registered Investment Adviser Amesbury, MA Wilmington, MA Office: 978-388-0020 or 617-398-7494 CELL: 978-621-8268 [email protected] Fee-Only * Five-Star Rating * Board-Certified

-

Upload

steve-stanganelli -

Category

Economy & Finance

-

view

674 -

download

5

description

Convertible Bonds are an overlooked asset class that may help an investor increase portfolio income while protecting against the volatility of individual stocks. An important tool to help reduce risk and improve portfolio returns for retirement income portfolios.

Transcript of Protecting and growing a portfolio with convertible bonds

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

Protect and Grow Wealth with Convertible BondsA Way to Improve Yields with Lower Risks in Any Investor’s Portfolio

Prepared by:

Steve Stanganelli, CFP®, CRPC®

CERTIFIED FINANCIAL PLANNER (TM) Professional

Clear View Wealth Advisors, LLC, a Registered Investment AdviserAmesbury, MA Wilmington, MA

Office: 978-388-0020 or 617-398-7494CELL: 978-621-8268

Fee-Only * Five-Star Rating * Board-Certified

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

Convertible Bonds: An Overlooked Asset Class

“If you stay out of stocks, you might miss the rally. If you buy stocks, you might get

creamed in another slump. But convertible(s)…let you have it both ways.”

From Forbes Magazine

Convertible Bonds may be unfamiliar to most investors but they are a great tool for helping to

minimize certain risks in almost any investment portfolio.

Convertible Bonds can be an important part of any portfolio and can be structured to

accommodate any investor risk profile.

For an investor who is seeking an income-producing portfolio, they can provide an

enhancement to a traditional fixed-income portfolio. For a more growth-oriented portfolio, using

Convertible Bonds helps provide upside potential while receiving some income return. And in

uncertain times of higher volatility or sideways markets, including this asset class helps

investors protect their core holdings.

Whether an investor is concerned with stock market volatility or a market environment with

higher interest rates or inflation, Convertible Bonds provide an attractive alternative to traditional

stocks or bonds.

Convertible Securities: A Hybrid Investment

Convertible securities include both convertible bonds and convertible preferred stocks.

Convertible Bonds are hybrid investment vehicles that offer the best of both worlds — income

now like a bond and the potential to capture appreciation later like a stock.

Convertible Bonds – A Bond with an Option

The basic feature of any convertible security is its ability to be converted. Like a chameleon

changing color, the security can change from one type of investment to another. In the case of a

Convertible Bond, an investor can exercise the option to exchange the security for a

predetermined amount of shares in the common stock of the issuing company.

The bond’s issuing documents outlines this predetermined amount as a conversion ratio. For

example, if one is holding a bond with a conversion ratio of 10:1, then each bond can be

exchanged for ten shares of common stock.

The bond investor may be limited to when the exchange can be done. The issuing company

also typically reserves the right to call the bond and force a conversion.

Strengths Original investment cannot go lower than the market value of the bond;

the stock price does not matter until you exercise your option to convertinto stock.

Convertibles can be purchased through tax-deferred retirementaccounts.

Convertibles gain popularity in times of uncertainty. The best time to buya convertible is typically when interest rates are high and stock prices arelow. It is also advantageous when stock market direction is uncertain and

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

other fixed income yields are relatively low.

Weaknesses The return on the bond or preferred stock is usually quite low. "Forced conversion" can occur when the company makes you convert

your bond into stock. It is important to track when these bonds arecallable.

Three Main Uses Capital Appreciation Safe Investment Compared to Other Options Tax-Deferred Investment Shelters Income Received

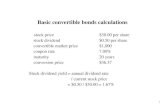

This chart illustrates the performance of a convertible bond as the stock price rises. Notice that

the price of the bond begins to rise as the stock price approaches the conversion price. At this

point your convertible performs similarly to a stock option. As the stock price moves up or

becomes extremely volatile, so does the bond.

Source: Investopedia (http://www.investopedia.com/articles/01/052301.asp)

It is important to remember that convertible bonds closely follow the underlying stock's price.

The exception occurs when the share price goes down substantially. In this case, at the time of

the bond's maturity, bond holders would receive no less than the par value, typically $1,000.

Why Companies May Issue Convertible Bonds

Convertible Bonds have evolved. In the past, many were issued by smaller companies that did

not have other means of accessing capital. Over the past 15 years, Convertible Bonds have

become more prevalent among larger brand name firms as well. Established companies have

turned to adding Convertible Bonds to their mix of financing options to lower the company’s

overall cost of capital. The coupon on a Convertible Bond is typically lower than a straight bond.

It also avoids diluting the Earnings Per Share (EPS) of common stock and may help in delaying

loss of control of a company by issuance of a new block of common stock.

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

Get Paid While You Wait

Convertible Bonds offer investors a fixed yield like any other bond. This regular income offers

better downside protection than simply holding the stock. They also have a feature that allows

the bondholder to trade in the bond for a certain amount of stock on a predetermined date. This

feature makes Convertible Bonds advantageous during inflationary times when stock prices

might be increasing and other bonds drop in value. During market corrections or bear markets,

investors receive interest while waiting for the next recovery or bull market.

Like any other bond, there is underlying credit risk of the issuer. The opportunity to convert also

means that the Convertible Bond may track the stock more closely and have higher volatility

than straight bonds. Yet the hybrid nature of this investment provides corresponding benefits.

Convertible Bond Advantages

Solid Total Returns Compared to Fixed-Income Options

As an asset class, Convertible Bonds have been around for more than 150 years. Since

December 1973 through mid-2010, the Convertible Bond index has had total returns (interest

plus appreciation) of 2736%, outpacing the government/corporate bond index by 943% and hi-

yield (aka junk) bond index of 1585% (BofA/Merrill Lynch Convertible Research, 6/30/10).

Solid Performance and Better Risk-Adjusted Returns Compared to Straight Equities

Historically, equities have offered a higher average annualized return compared to bonds. Yet

this higher potential comes with its own risks. To participate in the upside may require going

through uncertain periods subjecting a portfolio to wild fluctuations.

For those with time on their side who are able to control their emotions, a portfolio may be able

to recover. But most individual investors are too emotional when it comes to investing and not

prepared to lose. Emotion can sabotage their longer term investment plans.

Research shows and common sense supports that what matters most in investing is how much

you keep. Avoiding losses is easier than trying to make up lost ground.

Convertibles offer downside protection which may provide ballast to a portfolio and avoid the

need to “play catch-up” by taking other undue risks with a portfolio that has suffered a

drawdown caused by a market turn.

This chart shows that investing in convertibles offers an advantage that can help balance out a

portfolio especially in the recent up and down and sideways markets of this most recent decade.

Clearly relying solely on any one asset class has its risks. In this case large company equities

as represented by the familiar S&P 500 index have not offered a strong performance for the

risks associated with them over the charted period.

Through June 2010 S&P Total Return BOA/ML A0V0 Index

15 Years 6.24% 7.34%

10 Years -1.59% 2.30%

(Source: Morningstar, Inc. and Wellesley Investment Advisors, Inc)

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

Solid Returns During the “Lost Decade”

During the last decade Convertible Bonds have proven resilient and a safe harbor compared to

most other equity categories. In the ten-year stretch ending July 2010 after three major stock

busts which saw the cumulative return on the S&P 500 come in at a negative 7.37%, the Bank

of America/Merrill Lynch All Convertible index returned a total 32.64%. (Source: Financial

Advisor magazine, November 2010, “Considering Convertibles,” Kahn, p. 119). \

Asset Classes Compared

1 Year 3 Year 5 Year 10 Year

22.64% -6.79% 17.70% 22.84%

23.38% -30.78% -6.73% -27.19%

14.43% -26.62% -3.90% -14.77%

21.50% -23.65% 1.93% 34.99%

Thru 6/30/2010

Source: Wellesley Investment Advisers and BofA Merrill Lynch Convertible Dept., 6/30/10

Convertibles generally did better than their underlying stocks without the same level of exposure

to market volatility or negative returns evident in long-only stock investing.

Reasonable Holding Periods

In the past the opportunity to convert was limited or required a long holding period. Many now

offer windows to convert to stock that are relatively short: 3 to 5 years, reducing the Convertible

Bond investor’s needed holding period to cash out and get his money back with interest or a

stock gain.

Non-Correlated to the Stock Market Adding to Diversification

One goal of diversification for investors is to reduce the impact of exposure to volatile markets.

By spreading assets into different asset classes, the overall risk of the portfolio is reduced even

if the risks associated with the individual components may be high.

The challenge in a global market where more and more asset classes and economies are

becoming ever more interdependent is finding an asset class that still is non-correlated,

meaning an investment that won’t track the direction of another; one that zigs when other

investment asset classes zag.

The following chart highlights the correlation between bonds, convertibles and the broader stock

market represented by the S&P 500. Given the hybrid nature of Convertible Bonds, they show

that they are in between both stock and bond asset classes.

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

S&P 500 TR Index Barclay’s Agg Bond

Index

BofA MLV0A0 Index

S&P 500 TR Index 1 - -

Barclay’s Agg Bond

Index

0.01 1 -

BofA MLV0A0 Index 0.67 .01 1

Source: Morningstar, Inc.

Performance During Rising Interest Rate Environment

During Fed tightening, Convertible Bonds have performed well. It is inevitable that interest rates

will rise from their historically low rates with or without inflation. While the value of other

government and high-quality corporate bonds will suffer when interest rates rise, Convertible

Bonds will likely hold their value, continue to pay out interest and offer the potential of greater

return when converted to stock compared to only holding long equities or other types of bonds.

During two of the last 4 major Fed tightening cycles over the past 22 years, the returns on the

Convertible Bonds index (Merrill Lynch V0A0) have shown clear advantages in two periods,

competitive returns in a third and a loss in only one.

Fed Policy Rate S&P 500

Merrill Lynch

V0A0 Index

Start

Date

End

Date

Duration

(months)

Start

Value End Value

Interest

Rate

Increase Change (%) Change (%)

03/29/88 02/24/89 11 6.50 9.75 3.25% 10.38% 11.20%

02/04/94 02/01/95 12 3.00 6.00 3.00% 0.13% -8.46%

06/30/99 05/16/00 11 4.75 6.50 1.75% 6.80% 26.47%

06/30/04 06/29/06 24 1.00 5.25 4.25% 11.58% 8.67%

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

Convertible Bond Risks

No investment is perfect and convertibles are no different.

As with any bond there is the underlying credit risk of the issuer. In the event of a company

default, there is the risk of losing one’s investment. A mitigating factor is that bondholders are

first in line to receive proceeds from a company liquidation which is not an option for

stockholders.

As noted earlier there is the risk that the issuing company may force a conversion by calling the

bond. This may occur at an inopportune time for an investor who was relying upon the income

stream generated by the bond. And the conversion to the underlying stock may not be

appropriate for an individual investor’s risk profile which may require selling the stock and result

in an unexpected capital gain if the bond was not previously held in a tax-deferred account.

The market float for Convertible Bonds is small compared to the value of equities and other

bonds. According to BIS (2004) reports, the total float of issues was under $400 billion. While

ideal for a niche investing strategy, the limited size of the market can make it susceptible to

freeze-ups in the market. This has happened in 1998 and 2005 and more dramatically in 2008.

Convertible Bonds have been a favorite of hedge fund traders. By 2008, nearly 75% of all

issuance was held by hedge funds. As liquidity and investor appetite for risk dried up in late

2008, this lead to highly leveraged hedge funds in need of cash and liquidity to dump their

holdings at steep price declines and even losses resulting in a 35% fall in the Barclays Capital

US Convertible Bond Index for 2008.

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

An Illustration of a Convertible Bond Strategy in Action

Fundamental analysis is key to implementing a Convertible Bond strategy.

Because this is a niche area it lends itself to highly specialized investment managers who have

the research bench and resources to execute a strategy over entire business cycles. This is

more of a hands-on approach rather than an index approach.

Some of the key elements to this approach are:

Focusing on “investment grade” stocks

Find convertibles with attractive provisions: short time period until call, put or maturity

Identifying companies with profits growing 10% + per year and strong corporate balance

sheets with a ten year history of stability or strengthening

Analysis of the macroeconomic conditions and how they may impact the bond being

issued

An Example of What Can Happen When a Stock Appreciates: The Home Run *

Home Depot (HD), 3.25% coupon convertible bond

Convertible Bond Stock

November 25, 1996

Purchased Home Depot

3.25% convertible bond

Due 10/1/01 – Convertible to

43.402 shares HD

$995.00

Price Paid Per

Bond

$51.88

before split

$17.29

after 3:2 and 2:1

splits

October 1, 1999

Sold Home Depot convertible

bond before Call Date

Callable 10/2/99

$3,011.95

Per bond

$69.79

Including dividends

of $0.23

GAIN (LOSS)

Interest Income

202.71%

9.25% 303.64%

In hindsight, a stockholder would have received a higher return compared to buying the

convertible and converting. While the convertible provides a cap on the upside, it offered

income and downside protection.

© Steve Stanganelli, CFP®, CRPC® and Clear View Wealth Advisors, LLC 2010

An Example of What Can Happen When a Stock Depreciates: The Strike Out *

AOL Time Warner, 0% convertible bond

Convertible Bond Stock

November 30, 2000

Purchased AOL 0%

convertible bond

Due 12/6/2019 – Convertible

to 5.834 shares of AOL

(Put on 12/6/2004 at $639.76

per bond)

$501.25

Price Paid Per

Bond

$40.61

Per share

March 28, 2002

Sold AOL 0%

convertible bond

$548.75

Per bond

$23.65

Per share

GAIN (LOSS) 9.47% - 47.16%

* Source: Wellesley Investment Advisers

Holding the stock would have resulted in a significant loss in value. Hedging strategies could

have been employed which would increase the cost of holding. Opting for the convertible bond

provided income and an opportunity to exercise the “put” by converting to the stock. The

convertible provides a floor under the stock which reduces the investor’s risk.

Conclusions

Convertible Bonds provide opportunities to build and protect wealth in uncertain times. They

offer investors compelling reasons to add them to their portfolio mix:

1. Higher yield than most equities (presently > 3.5%)

2. Potential to capture appreciation

3. Enhanced diversification and lower potential risk resulting from low correlation with stocks

and bonds

4. Track record of preserving capital

5. Unlike other bonds, Convertible Bonds have generally performed well during periods of

increasing interest rates or inflationary periods.