PROSPECTUS CONTINUOUS OFFERING … · PROSPECTUS CONTINUOUS OFFERING December ... Covington is a...

84

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. PROSPECTUS CONTINUOUS OFFERING December 28, 2009 COVINGTON FUND II INC. CLASS A SHARES AND COVINGTON STRATEGIC CAPITAL FUND INC. CLASS A SHARES, SERIES I AND CLASS A SHARES, SERIES II Covington Fund II Inc. (“Covington Fund II”) and Covington Strategic Capital Fund Inc. (“Covington Strategic Capital Fund”) (Covington Fund II and Covington Strategic Capital Fund are individually referred to as a “Fund” and collectively referred to as the “Funds”) are each registered as a labour sponsored investment fund corporation under the Community Small Business Investment Funds Act (Ontario) (the “Ontario Act”) and are each a prescribed labour-sponsored venture capital corporation under the Income Tax Act (Canada), as amended (the “Federal Tax Act”). Class A Shares of Covington Fund II and Class A Shares, Series I (“Series I Shares”) and Class A Shares, Series II (“Series II Shares”) of Covington Strategic Capital Fund are being offered separately hereunder. During the period of distribution, prices may vary from purchaser to purchaser. Unless the context provides otherwise, references to “Class A Shares” in this prospectus are to the Class A Shares of both Funds. Covington Fund II Investment Objective and Strategy: Covington Fund II will make investments in eligible businesses as defined in the Ontario Act. In general terms, eligible businesses are public or private companies carrying on business in Ontario with less than 500 employees and less than $50 million of total assets. The objective of Covington Fund II is to earn long-term capital appreciation on part of its investment portfolio and current yield and early return of capital on the remainder of its investment portfolio. In order to achieve this objective, the investment strategy of Covington Fund II is to invest in two different types of situations. The first is in companies with significant growth potential in early stage or expanding markets. The second is in more established, steady growth companies which will often provide current yield and early return of capital to Covington Fund II. See “Investment Objective” and “Investment Strategies”. Investment Advisor and Fund Advisor: The investment advisor of Covington Fund II is Covington Capital Corporation (“Covington”). As investment advisor, Covington provides advice and analysis to Covington Fund II in respect of Covington Fund II’s investments in eligible businesses. Covington is a wholly-owned subsidiary of RC Capital Management Inc. (“RC Capital”) which purchased Covington from AMG Canada Corp. on July 2, 2009. Mr. Scott D. Clark is the President, Chief Executive Officer and Chief Compliance Officer of Covington and Mr. Philip R. Reddon is the Managing Director of Covington (collectively, the “Principals”). The Principals, supported by a senior investment team, have significant experience as investors in, or advisors to, middle market Canadian companies. The fund advisor for Covington Fund II is also Covington. As fund advisor, Covington is responsible for providing marketing and investor relations services to Covington Fund II. See “Organization and Management Details of the Funds”. Covington Strategic Capital Fund Investment Objective and Strategy: Covington Strategic Capital Fund will make investments in eligible businesses as defined in the Ontario Act. The objective of Covington Strategic Capital Fund is to realize long-term capital appreciation on part of its investment portfolio and current yield and early return of capital on the remainder of its investment portfolio. Covington Strategic Capital Fund will invest primarily in Canadian independent software vendors that develop software applications to run on one or more software operating systems, and intends

Transcript of PROSPECTUS CONTINUOUS OFFERING … · PROSPECTUS CONTINUOUS OFFERING December ... Covington is a...

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise.

PROSPECTUS

CONTINUOUS OFFERING

December 28, 2009

COVINGTON FUND II INC. CLASS A SHARES

AND

COVINGTON STRATEGIC CAPITAL FUND INC. CLASS A SHARES, SERIES I AND CLASS A SHARES, SERIES II

Covington Fund II Inc. (“Covington Fund II”) and Covington Strategic Capital Fund Inc. (“Covington Strategic Capital Fund”) (Covington Fund II and Covington Strategic Capital Fund are individually referred to as a “Fund” and collectively referred to as the “Funds”) are each registered as a labour sponsored investment fund corporation under the Community Small Business Investment Funds Act (Ontario) (the “Ontario Act”) and are each a prescribed labour-sponsored venture capital corporation under the Income Tax Act (Canada), as amended (the “Federal Tax Act”). Class A Shares of Covington Fund II and Class A Shares, Series I (“Series I Shares”) and Class A Shares, Series II (“Series II Shares”) of Covington Strategic Capital Fund are being offered separately hereunder. During the period of distribution, prices may vary from purchaser to purchaser. Unless the context provides otherwise, references to “Class A Shares” in this prospectus are to the Class A Shares of both Funds.

Covington Fund II

Investment Objective and Strategy: Covington Fund II will make investments in eligible businesses as defined in the Ontario Act. In general terms, eligible businesses are public or private companies carrying on business in Ontario with less than 500 employees and less than $50 million of total assets. The objective of Covington Fund II is to earn long-term capital appreciation on part of its investment portfolio and current yield and early return of capital on the remainder of its investment portfolio. In order to achieve this objective, the investment strategy of Covington Fund II is to invest in two different types of situations. The first is in companies with significant growth potential in early stage or expanding markets. The second is in more established, steady growth companies which will often provide current yield and early return of capital to Covington Fund II. See “Investment Objective” and “Investment Strategies”.

Investment Advisor and Fund Advisor: The investment advisor of Covington Fund II is Covington Capital Corporation (“Covington”). As investment advisor, Covington provides advice and analysis to Covington Fund II in respect of Covington Fund II’s investments in eligible businesses. Covington is a wholly-owned subsidiary of RC Capital Management Inc. (“RC Capital”) which purchased Covington from AMG Canada Corp. on July 2, 2009. Mr. Scott D. Clark is the President, Chief Executive Officer and Chief Compliance Officer of Covington and Mr. Philip R. Reddon is the Managing Director of Covington (collectively, the “Principals”). The Principals, supported by a senior investment team, have significant experience as investors in, or advisors to, middle market Canadian companies. The fund advisor for Covington Fund II is also Covington. As fund advisor, Covington is responsible for providing marketing and investor relations services to Covington Fund II. See “Organization and Management Details of the Funds”.

Covington Strategic Capital Fund

Investment Objective and Strategy: Covington Strategic Capital Fund will make investments in eligible businesses as defined in the Ontario Act. The objective of Covington Strategic Capital Fund is to realize long-term capital appreciation on part of its investment portfolio and current yield and early return of capital on the remainder of its investment portfolio. Covington Strategic Capital Fund will invest primarily in Canadian independent software vendors that develop software applications to run on one or more software operating systems, and intends

- 2 -

to develop and grow investee businesses in cooperation with strategic partners. See “Investment Objective” and “Investment Strategies”.

The Manager and Fund Advisor: The manager of Covington Strategic Capital Fund is Covington. As manager, Covington performs Covington Strategic Capital Fund’s daily administrative operations and engages and supervises service providers to Covington Strategic Capital Fund and provides advice and analysis to Covington Strategic Capital Fund in respect of Covington Strategic Capital Fund’s investments in eligible businesses. The fund advisor for Covington Strategic Capital Fund is also Covington. As fund advisor, Covington is responsible for providing marketing and investor relations services to Covington Strategic Capital Fund. See “Organization and Management Details of the Funds - CSCF Fund Advisor Agreement”.

Covington Fund II and Covington Strategic Capital Fund

The Sponsor: The sponsor of each of the Funds is the Canadian Police Association (the “Sponsor”). Prior to August 2003, the Sponsor was the Canadian Police Association Incorporated, which merged with the National Professional Police Association in August 2003 to form the Canadian Police Association. See “Organization and Management Details of the Funds – The Sponsor of the Funds”.

The Fund Administrator: The fund administrator for each of the Funds is CI Investments Inc. (formerly called “CI Mutual Funds Inc.”) (“CI”). CI is responsible for providing administration and client services, shareholder reporting and transfer agency services to the Funds. See “Organization and Management Details of the Funds – The Fund Administrator of the Funds”.

Tax Benefits

Federal Tax Credits: Individuals resident in Canada who are first purchasers of Class A Shares of a Fund issued under this prospectus will be eligible for a 15% federal tax credit to a maximum credit of $750 for the year (for investments of $5,000 or more). See “Canadian Federal Income Tax Considerations – Federal Tax Credit Available to First Purchasers”.

Ontario Tax Credits: Pursuant to the Ontario Tax Act (Ontario Tax Act means the Taxation Act, 2007 (Ontario), as amended, with respect to the 2009 and subsequent taxation years in force on the date of this prospectus), individuals resident in Ontario who purchase Class A Shares issued under this Prospectus by March 1, 2010, will be eligible for a provincial tax credit equal to 15% of the purchase price of Class A Shares to a maximum credit of $1,125 for the 2009 taxation year based on an investment of $7,500. The provincial tax credit will be reduced for the 2010 and 2011 taxation years and eliminated for the 2012 and subsequent taxation years. See the “Prospectus Summary – Tax Benefits” and “Ontario Income Tax Considerations – Ontario Tax Credits Available to First Purchasers”.

An individual may generally claim federal and Ontario tax credits for investments in Class A Shares made by the individual’s registered retirement savings plan (“RRSP”) and an individual or his or her spouse or common-law partner may generally claim the tax credits for investments in Class A Shares made by a spousal RRSP.

Eligible investors who purchase Class A Shares after December 31, 2009, but on or before March 1, 2010 (the last day on which Class A Shares may be acquired by an eligible investor to claim federal and provincial tax credits for 2009) may elect to have their Ontario tax credit and their federal tax credit apply in respect of the 2009 taxation year instead of the 2010 taxation year.

The above maximum Ontario and federal tax credits for a taxation year apply in respect of an eligible investor’s aggregate purchases in respect of that year of shares issued by labour sponsored investment fund corporations, in the case of the Ontario tax credit, or labour-sponsored venture capital corporations, in the case of the federal tax credit.

The Offering:

Continuous Offering Price for Covington Fund II: net asset value per Class A Share Continuous Offering Price for Covington Strategic Capital Fund: net asset value per Class A Share, Series I or

Class A Share, Series II Minimum Initial Subscription: $500 Minimum Subsequent Subscription: $25 For Pre-Authorized Chequing Plan, Minimum Subscription: $25

- 3 -

Covington Fund II. Covington Fund II pays to the selling registered dealers a commission of 6% of the offering price in respect of the sale of Class A Shares. Covington Fund II also pays to registered dealers a service fee equal to 0.5% annually of the average total net asset value of the Class A Shares held by the clients of the sales representatives of the dealers, calculated and paid monthly. See “Plan of Distribution”. Sales commissions incurred prior to January 1, 2004 have been capitalized as deferred charges and amortized on a straight line basis over eight years, consistent with Covington Fund II’s past practice. Sales commissions incurred on and after January 1, 2004 are charged to retained earnings (deficit) in accordance with generally accepted accounting principles. See “Fees and Expenses”.

Class A Shares of Covington Fund II are offered on a continuous basis (the “Continuous Offering”) at the net asset value per Class A Share. See “Calculation of Net Asset Value”. Covington Fund II may suspend offering Class A Shares and recommence offering Class A Shares at any time Covington Fund II, in its discretion, deems appropriate. Class A Shares subscribed for during the Continuous Offering will be issued as of the first business day following the date of subscription for a purchase price equal to the net asset value per Class A Share at the close of business on the business day on which the subscription is received. During the period of distribution, prices may vary from purchaser to purchaser. See “Purchases of Securities”.

Covington Strategic Capital Fund. Covington Strategic Capital Fund distributes Class A Shares through registered dealers and Covington manages the relationship with such registered dealers. Covington is paid a fee for providing distribution and capital retention services. Investors who purchase Class A Shares will not pay any sales commissions directly. Covington pays to registered dealers a commission of 10% of the offering price in respect of the sale of Series I Shares. In addition, after a period of eight years, Covington Strategic Capital Fund will pay to each registered dealer having clients holding Series I Shares a servicing commission equal to 0.5% annually of the net asset value of the Series I Shares held by those clients. Covington pays to registered dealers a commission of 6% of the offering price in respect of the sale of Series II Shares. In addition, Covington Strategic Capital Fund pays to each registered dealer having clients holding Series II Shares a servicing commission equal to 0.5% annually of the net asset value of the Series II Shares held by those clients. See “Purchases of Securities”.

Class A Shares of Covington Strategic Capital Fund are offered on a continuous basis (the “Continuous Offering”) at the net asset value per Class A Share for the applicable series of Class A Shares. See “Calculation of Net Asset Value”. Covington Strategic Capital Fund may suspend offering Class A Shares or any series thereof and recommence offering Class A Shares or any series thereof at any time that Covington Strategic Capital Fund, in its discretion, deems appropriate. Class A Shares subscribed for during the Continuous Offering will be issued as of the first business day following the date of subscription for a purchase price equal to the net asset value per Class A Share for the applicable series of Class A Shares at the close of business on the business day on which the subscription is received. During the period of distribution, prices may vary from purchaser to purchaser. See “Purchases of Securities”.

Additional information about the Funds is available in the following documents:

� the most recently filed annual financial statements;

� any interim financial statements filed after those annual financial statements;

� the most recently filed annual management report of fund performance; and

� any interim management report of fund performance filed after that annual management report of fund performance.

These documents are incorporated by reference into this prospectus which means that they legally form part of this prospectus. Please see the “Documents Incorporated by Reference” section for further details.

Investors should read the prospectus and review the financial statements and management reports of fund performance carefully before making an investment decision. Careful consideration should be given to the risk factors associated with making an investment in the Fund. See “Risk Factors”. Investors should also consult with their professional advisors prior to making an investment in the Fund.

The Class A Shares of each Fund are highly speculative in nature. An investment in a Fund is appropriate only for investors who are prepared to retain their money in that Fund for a long period of time and who

- 4 -

have the capacity to absorb a loss of some or all of their investment. There is no guarantee that an investment in a Fund will earn a regular rate of return. Although the Funds are mutual funds, some of the rules designed to protect investors who purchase securities of mutual funds sold in Ontario do not apply to the Funds. In particular, rules directed at ensuring liquidity and diversification of investments and certain other investment restrictions and practices normally applicable to mutual funds do not apply to the Funds. See “Risk Factors”.

Mutual funds generally value their investments at the closing market price at which they can be bought and sold. Each Fund is required, by applicable securities legislation, to obtain on an annual basis, a valuation by an independent qualified person of the net asset value of the Fund and the net asset value per Share. The Fund satisfies this requirement by engaging Ernst & Young LLP, the Fund’s independent auditors, to perform certain procedures on the value of the Fund’s investments for which no public markets exist as at August 31 of each year as part of Ernst & Young LLP’s audit of the Fund’s annual financial statements.The Funds and Covington are responsible for valuations of the Class A Shares for purposes of sales and redemptions. The existence of a daily valuation is designed to give investors flexibility in the timing of purchases and redemptions of Class A Shares but in no way modifies the restrictions on the transfer or redemption of Class A Shares. The valuations carried out by the Funds, Covington or an independent qualified person may not reflect the prices at which the investments of the Funds can actually be sold, particularly after taking into account associated selling costs such as sales commissions and legal fees. See “Calculation of Net Asset Value”.

The Funds may have liability for the repayment of tax credits in certain circumstances. Investors may be required to repay any tax credit received as a result of their investment if their Class A Shares are redeemed within eight years of purchase. Also, in most cases, investors must pay redemption fees to the Funds if their Class A Shares are redeemed within eight years of purchase. Furthermore, the Funds are prohibited by law from making redemptions in certain circumstances, may suspend redemptions for substantial periods of time in certain circumstances and, in any financial year, a Fund will not be required to redeem Class A Shares having an aggregate redemption price exceeding 20% of the net asset value of that Fund as of the last day of the preceding financial year. Investors may not be able to dispose of their Class A Shares other than by way of redemption, as there is no formal market, such as a stock exchange, through which Class A Shares may be sold. In addition, there are restrictions on the voting and transfer of Class A Shares. See “Canadian Federal Income Tax Considerations”, “Ontario Income Tax Considerations” and “Attributes of the Securities”.

Subscriptions will be received subject to rejection or allotment in whole or in part. The Class A Shares are offered for sale only through registered dealers. The Funds will not accept a purchase order placed directly by an investor. See “Purchases of Securities”.

- 5 -

TABLE OF CONTENTS

ELIGIBILITY FOR INVESTMENT............................................................................................................................. 6 PROSPECTUS SUMMARY......................................................................................................................................... 7 OVERVIEW OF THE LEGAL STRUCTURE OF THE FUNDS ................................................................................ 24 INVESTMENT OBJECTIVE ....................................................................................................................................... 24 INVESTMENT STRATEGIES..................................................................................................................................... 25 OVERVIEW OF THE SECTORS THAT THE FUNDS INVEST IN .......................................................................... 29 INVESTMENT RESTRICTIONS................................................................................................................................. 36 FEES AND EXPENSES ............................................................................................................................................... 37 ANNUAL RETURNS AND MANAGEMENT EXPENSE RATIO ............................................................................ 42 RISK FACTORS ........................................................................................................................................................... 43 DISTRIBUTION POLICY............................................................................................................................................ 46 PURCHASES OF SECURITIES .................................................................................................................................. 47 REDEMPTION OF SECURITIES................................................................................................................................ 48 CANADIAN FEDERAL INCOME TAX CONSIDERATIONS.................................................................................. 49 ONTARIO INCOME TAX CONSIDERATIONS........................................................................................................ 53 ORGANIZATION AND MANAGEMENT DETAILS OF THE FUNDS ................................................................... 56 CALCULATION OF NET ASSET VALUE ................................................................................................................ 67 ATTRIBUTES OF THE SECURITIES ........................................................................................................................ 70 SECURITYHOLDER MATTERS................................................................................................................................ 74 TERMINATION OF THE FUND................................................................................................................................. 75 PLAN OF DISTRIBUTION.......................................................................................................................................... 76 PRINCIPAL HOLDERS OF SECURITIES OF THE FUNDS..................................................................................... 77 INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS............................................. 77 PROXY VOTING DISCLOSURE FOR PORTFOLIO SECURITIES HELD ............................................................. 77 MATERIAL CONTRACTS.......................................................................................................................................... 78 LEGAL AND ADMINISTRATIVE PROCEEDINGS ................................................................................................. 79 EXPERTS...................................................................................................................................................................... 79 EXEMPTIONS AND APPROVALS ............................................................................................................................ 79 PURCHASERS’ STATUTORY RIGHTS OF WITHDRAWAL AND RESCISSION................................................ 80 DOCUMENTS INCORPORATED BY REFERENCE ................................................................................................ 80 AUDITORS’ CONSENT .............................................................................................................................................. 81 CERTIFICATE.............................................................................................................................................................. C-1 CERTIFICATE.............................................................................................................................................................. C-1

- 6 -

ELIGIBILITY FOR INVESTMENT

In the opinion of Gowling Lafleur Henderson LLP, so long as a Fund is registered as a labour sponsored investment fund corporation under the Ontario Act and is a prescribed labour-sponsored venture capital corporation under the Federal Tax Act, Class A Shares of that Fund will be qualified investments for trusts governed by a registered retirement savings plan (“RRSP”) and a registered retirement income fund (“RRIF”) (each a “Registered Plan”) at a particular time if: (i) the annuitant is not at that time a designated shareholder of that Fund and (ii) it cannot reasonably be considered that any amount received in respect of the Class A Shares is on account of payment for services provided by the annuitant of the Registered Plan to that Fund or a person related to that Fund. In general, a designated shareholder is a person who is, or is related to, a person who, alone or together with non-arm’s length persons, owns directly or indirectly not less than 10% of the issued shares of any class or series of the capital stock of the applicable Fund, or any other corporation related to the applicable Fund. However, an annuitant will not be considered to be a designated shareholder if the cost to the annuitant, and persons not dealing at arm’s length with the annuitant, of shares in the applicable Fund, or any other corporation related to the applicable Fund, is less than $25,000, and the annuitant deals at arm’s length with the applicable Fund.

Alternatively, the Class A Shares will be qualified investments for such trust at any time if: (i) immediately after the time the Class A Shares were acquired by the Registered Plan, the annuitant was not a connected shareholder of the applicable Fund; and (ii) the Registered Plan does not receive an amount in respect of the Class A Shares which may reasonably be considered to be on account of payment for services to or for the applicable Fund or a person related to the applicable Fund or in respect of the acquisition of goods or services from the applicable Fund or person related to the applicable Fund. In general, a connected shareholder is a person who, alone or together with non-arm’s length persons, owns directly or indirectly not less than 10% of the issued shares of any class or series of the capital stock of the applicable Fund, or any other corporation related to the applicable Fund. However, an annuitant will not be considered to be a connected shareholder if the annuitant deals at arm’s length with the applicable Fund and the cost to the annuitant, and persons not dealing at arm’s length with the annuitant, of shares in the applicable Fund, or any other corporation related to the applicable Fund, is less than $25,000. See “Canadian Federal Income Tax Considerations” and “Ontario Income Tax Considerations”.

Although, as described above, Class A Shares will generally be qualified investments for RRIFs, a RRIF is not permitted to subscribe directly for Class A Shares.

- 7 -

PROSPECTUS SUMMARY

The following is a summary of the principal features of this distribution and should be read together with the more detailed information and financial data and statements contained elsewhere in this prospectus or incorporated by reference in this prospectus.

Covington Fund II

Covington Fund II is a corporation incorporated under the laws of Ontario. Covington Fund II is registered as a labour sponsored investment fund corporation under the Ontario Act and qualifies as a prescribed labour-sponsored venture capital corporation under the Income Tax Act (Canada) (the “Federal Tax Act”).

Covington Fund II makes investments in eligible businesses as defined in the Ontario Act. In general terms, eligible businesses are public or private companies carrying on business in Ontario with less than 500 employees and less than $50 million of total assets. The objective of Covington Fund II is to earn long-term capital appreciation on part of its investment portfolio and current yield and early return of capital on the remainder of its investment portfolio. In order to achieve this objective, the investment strategy of Covington Fund II is to invest in two different types of situations. The first is in companies with significant growth potential in early stage or expanding markets. The second is in more established, steady growth companies, which will often provide current yield and early return of capital to Covington Fund II. Pending such investments, Covington Fund II will invest in high quality, short-term government and public company debt obligations.

Covington Strategic Capital Fund

Covington Strategic Capital Fund is a corporation incorporated under the laws of Ontario. Covington Strategic Capital Fund is registered as a labour sponsored investment fund corporation under the Ontario Act and qualifies as a prescribed labour-sponsored venture capital corporation under the Federal Tax Act.

Covington Strategic Capital Fund makes investments in eligible businesses as defined in the Ontario Act. The objective of Covington Strategic Capital Fund is to realize long-term capital appreciation on part of its investment portfolio and current yield and early return of capital on the remainder of its investment portfolio. Covington Strategic Capital Fund will invest primarily in Canadian independent software vendors that develop software applications that may run on one or more software operating system platforms, and intends to develop and grow investee businesses in cooperation with strategic partners.

Covington has considerable experience in investing in this industry sector with approximately one-third of its managed portfolio companies being software companies. It has been Covington’s experience that limitations on a software company’s revenue growth are attributable largely to a lack of relationships and the inability to establish the necessary channel partners for product distribution in these various sectors. Although obtaining sufficient capital is a part of solving these shortcomings, software companies must also forge relationships with key industry partners so that the capital investment can be efficiently leveraged through collaboration with established, successful and strategic partners. Covington believes that involving strategic partners in Covington Strategic Capital Fund’s investment process can greatly assist investee companies in establishing necessary relationships. The appropriate candidates will be early to expansion stage software companies that would benefit from the services of strategic partners in addition to the financing to be provided by Covington Strategic Capital Fund. Covington expects that strategic partners will assist in establishing appropriate sales channels while providing equally important product and market credibility to prospective customers of the investee company.

Covington Strategic Capital Fund seeks to establish both formal and informal relationships with strategic partners that can assist Covington Strategic Capital Fund in achieving its objectives. Strategic partners with which Covington Strategic Capital Fund establishes relationships are expected to be a source of qualified investment referrals to Covington and, where appropriate, they will provide resources to assist in due diligence evaluations. Although reference is made in this prospectus to the term “strategic partners”, the relationship of Covington Strategic Capital Fund and Covington with such parties is not and is not expected to be in the form of a legal partnership and in many cases will be strictly informal.

- 8 -

Investment Restrictions

Covington Fund II and Covington Strategic Capital Fund are subject to certain investment restrictions under the Ontario Act. In addition, the Funds have adopted certain other investment policies and guidelines. Potential investments of a Fund will be evaluated according to, among other things: stage of development; size of company; quality of management; the market potential of the products or services sold or distributed; the profit potential of the company; and the opportunity for realization by the Fund of its investments. See “Investment Objective” and “Investment Strategies”.

Risk Factors

These securities are highly speculative in nature and suitable only for investors able to make a long-term investment and who have the capacity to lose some or all of their investment. Many of the companies in which the Funds will invest are developing products, technologies or services for which markets are not yet established and may never be established. It is possible that some of the Funds’ investments will not mature and generate expected returns. There is no assurance that suitable investments in eligible businesses will be found. Early stage investment funds are usually considered more risky than funds that invest in companies at varying stages of development. The Funds’ early stage investments will typically take longer to mature and present opportunities than other venture capital investments. Venture capital investment in eligible businesses according to the investment restrictions and policies applicable to the Funds requires a greater commitment to investment analysis than investments in most other securities. Investors in Class A Shares of a Fund will be relying on the business judgment, expertise and integrity of the board of directors and management of the applicable Fund and of Covington. Many of the rules normally applicable to mutual funds do not apply to the Funds. In particular, rules directed at ensuring liquidity and diversification of investments and certain other investment restrictions and practices normally applicable to mutual funds do not apply. The Funds may take positions in small and medium-sized businesses that represent a larger percentage of the equity than a mutual fund would be permitted to take, and this may increase the risk per investment. The values that the Funds put on their investments may not reflect the amounts for which they can actually be sold. The transfer of Class A Shares of each Fund is restricted. There is no formal market, such as a stock exchange, through which Class A Shares may be sold, and none is expected to develop. The Funds will generally be required to withhold certain amounts on the redemption of their Class A Shares before the eighth anniversary of the issue date for the particular share. There are certain restrictions on the voting and redemption of Class A Shares. The Funds may be subject to certain penalty taxes or lose their registration if they fail to meet the investment requirements of the Ontario Act. If a Fund’s registration under the Ontario Act is revoked, investors in that Fund may be ineligible for federal and provincial tax credits. There is no assurance that changes will not be introduced to federal or provincial legislation or regulations which, if unfavourable, could impair the Funds’ investment performance and their ability to attract future investment capital. Investors should consult with a professional advisor. See “Risk Factors”. The reduction of Ontario tax credits for the 2010 and 2011 taxation years and the elimination of the Ontario provincial tax credit for 2012 and subsequent years are likely to materially reduce future sales of Class A Shares of the Fund. The availability of funds for investment by the Funds in the future will be reduced and the Funds may be adversely impacted. Investors should consult with a professional advisor. See “Risk Factors”.

Tax Benefits

Federal Tax Credits: Individuals resident in Canada who are first purchasers of Class A Shares of the Funds issued under this prospectus will be eligible for a 15% federal tax credit to a maximum credit of $750 for the year (based on an investment of $5,000). Proposed amendments to the Federal Tax Act, applicable to acquisitions of Class A Shares after 2003, provide that a federal tax credit is only available for a Class A share of a prescribed labour-sponsored venture capital corporation that is not federally registered if a provincial tax credit is also available in respect of the Class A Share. See “Canadian Federal Income Tax Considerations – Federal Tax Credit Available to First Purchasers”.

Ontario Tax Credits: Individuals resident in Ontario who purchase Class A Shares issued under this Prospectus by March 1, 2010 will be eligible for a provincial tax credit equal to 15% of the purchase price of Class A Shares to a maximum credit of $1,125 for the 2009 taxation year based on an investment of $7,500. The provincial tax credit

- 9 -

will be reduced for the 2010 and 2011 taxation years and eliminated for the 2012 and subsequent taxation years. See “Ontario Income Tax Considerations – Ontario Tax Credits Available to First Purchasers”.

Investors who purchase Class A Shares of a Fund after December 31, 2009, but on or before March 1, 2010 (the last day on which Class A Shares may be acquired by an eligible investor to claim federal and provincial tax credits for 2009) may elect to have their Ontario tax credit and their federal tax credit apply in respect of the 2009 taxation year instead of the 2010 taxation year.

The above maximum Ontario and federal tax credits apply in respect of an eligible investor’s aggregate purchases in respect of the year of shares issued by labour sponsored investment fund corporations, in the case of the Ontario tax credit, or prescribed labour-sponsored venture capital corporations, in the case of the federal tax credit.

Subject to the qualification discussed above under the heading “Eligibility for Investment”, the Class A Shares of the Funds are qualified investments for RRSPs and RRIFs. An individual who purchases Class A Shares and elects to transfer such Class A Shares to an RRSP under which the individual or his or her spouse or common-law partner is the annuitant is entitled to treat such transfer as a deductible contribution to the RRSP, subject to the contribution limits in the Federal Tax Act. This deduction from income is in addition to the federal and provincial tax credits referred to above. In addition, Class A Shares may be purchased by certain RRSPs. In such a case, the individual who contributed to the RRSP generally is entitled to claim the federal tax credit and the provincial tax credit. See “Eligibility for Investment”, “Canadian Federal Income Tax Considerations” and “Ontario Income Tax Considerations”.

The Offering

Offering: Class A Shares of Covington Fund II.

Series I Shares and Series II Shares of Covington Strategic Capital Fund. The difference between the Series I Shares and the Series II Shares is the sales commission structure and corresponding redemption structure associated with each such series, and the difference in the time over which and corresponding net asset value upon which such fees are calculated. See “Purchases of Securities”.

Offering Price: Class A Shares of Covington Fund II are offered on a continuous basis at the net asset value per Class A Share at the close of business on the date on which the subscription for Class A Shares is received.

Class A Shares of Covington Strategic Capital Fund are offered on a continuous basis at the net asset value per Class A Share for the applicable series of Class A Shares at the close of business on the date on which the subscription for Class A Shares is received.

Purchasers: The Class A Shares of each Fund may be issued only to individuals and RRSPs. See “Attributes of the Securities — Class A Shares — Issue”.

Minimum Investment for each Fund:

Minimum initial subscription: $500. Minimum subsequent subscription: $25. For pre-authorized chequing plan, the minimum subscription is $25.

- 10 -

Voting Rights: Each Class A Share entitles the holder to one vote per share at all general meetings of shareholders of the applicable Fund. Holders of Class A Shares of Covington Fund II are currently entitled to elect two directors of the Covington Fund II. Holders of Class A Shares of Covington Strategic Capital Fund are currently entitled to elect one director of the Covington Strategic Capital Fund. See “Attributes of the Securities” and “Organization and Management Details of the Funds - The Sponsor of the Funds”.

Transfer: The transfer of Class A Shares of a Fund is restricted except in circumstances similar to those described below with respect to the redemption of Class A Shares. See “Attributes of the Securities – Class A Shares - Redemption”.

Redemption

A holder of Class A Shares of a Fund may require that Fund to redeem his or her Class A Shares on or after the eighth anniversary of the date of issue of the Class A Shares. Class A Shares may also be redeemed at any time prior to the expiry of the eight year period if a special tax determined by formula for recovery of an amount in respect of the tax credits on such shares is withheld from the redemption proceeds and paid to the Receiver General for Canada and an amount equal to 15% of the original issue price or the redemption price, whichever is less, is withheld and paid to the Minister of Revenue (Ontario).

A holder of Class A Shares of a Fund may also require that Fund to redeem his or her Class A Shares prior to expiry of the eight year period without withholding of the tax credit or other amount referred to above in the event of any of the following: (i) the holder has requested the applicable Fund to redeem the Class A Shares within 60 days after the day on which the Class A Shares were issued to the original purchaser and the tax credit certificate issued under the Ontario Act has been returned to the applicable Fund; (ii) the original purchaser of the Class A Shares, as defined in the Ontario Act, has become disabled and permanently unfit for work or becomes terminally ill, (iii) the Class A Shares or the beneficial interest therein has devolved upon the holder as a consequence of the death of the original purchaser; or (iv) the applicable Fund publicly announces that it proposes to dissolve or wind-up and the redemption, acquisition or cancellation of the Class A Shares is part of the dissolution or wind-up of the applicable Fund, and occurs within a reasonable time before the applicable Fund surrenders its registration.

In determining whether the redemption of a Class A Share is prior to eight years from the date of issue, under the Ontario Act, a Class A Share issued in February or March that is redeemed in February or on March 1 is deemed to be redeemed on March 31. Under the Federal Tax Act, if a Class A Share is redeemed in February or on March 1 of a calendar year and that day is no more than 31 days before the day that is eight years after the day on which the Class A Share was issued, then there will be no requirement to withhold the federal special tax.

Subject to the withholding of any amount required to be withheld as described above and the deduction of the applicable redemption fees described below, Class A Shares will be redeemed at the net asset value per Class A Share as of the close of business on the date on which the applicable Fund receives the duly completed request for redemption.

In any financial year, a Fund will not be required to redeem Class A Shares having an aggregate redemption price exceeding 20% of the net asset value of that Fund as of the last day of the preceding financial year. Each Fund intends to maintain sufficient liquid investments to enable it to honour requests for redemptions however Covington Fund II may subject itself to an annual cap on redemptions as part of its strategy to ensure sufficient liquidity to honour redemptions. See “Redemption of Securities”, “Attributes of the Securities — Class A Shares” and “Risk Factors – Redemption”.

- 11 -

Redemption Fee

Covington Fund II:

A redemption fee of up to 6% of the offering price of the Class A Shares will be charged to investors and calculated as 0.75% of the offering price of the Class A Shares multiplied by the number of years or partial years remaining until the eighth anniversary of the date of issue of such Class A Shares. After the eighth anniversary of the date of issue of the Class A Shares, there will be no redemption fee. The redemption fee will be deducted from the redemption amount otherwise payable and will be paid to Covington Fund II. See “Redemption of Securities” and “Attributes of the Securities — Class A Shares”.

Covington Strategic Capital Fund:

Series I Shares: A redemption fee of up to 10% of the offering price of the Series I Shares will be charged to investors and calculated as 1.25% of the offering price of the Series I Shares multiplied by the number of years or partial years remaining until the eighth anniversary of the date of issue of such Series I Shares. After the eighth anniversary of the date of issue of the Series I Shares, there will be no redemption fee. The redemption fee will be deducted from the redemption amount otherwise payable and will be paid to Covington. See “Redemption of Securities” and “Attributes of the Securities — Class A Shares”.

Series II Shares: A redemption fee of up to 6% of the offering price of the Series II Shares will be charged to investors and calculated as 0.75% of the offering price of the Series II Shares multiplied by the number of years or partial years remaining until the eighth anniversary of the date of issue of such Series II Shares. After the eighth anniversary of the date of issue of the Series II Shares, there will be no redemption fee. The redemption fee will be deducted from the redemption amount otherwise payable and will be paid to Covington. See “Redemption of Securities” and “Attributes of the Securities — Class A Shares”.

Valuation Dates

In order to establish the net asset value per Class A Share for purposes of issuing and redeeming Class A Shares, valuations of each Fund’s assets are carried out on a daily basis. The net asset value per Class A Share is determined as at the end of each business day. The Fund is required, by applicable securities legislation, to obtain on an annual basis, a valuation by an independent qualified person of the net asset value of the Fund and the net asset value per Share. The Fund satisfies this requirement by engaging Ernst & Young LLP, the Fund’s independent auditors, to perform certain procedures on the value of the Fund’s investments for which no public markets exist as at August 31 of each year as part of Ernst & Young LLP’s audit of the Fund’s annual financial statements. See “Calculation of Net Asset Value”.

Dividends

Holders of Class A Shares of a Fund are entitled to receive dividends at the discretion of the board of directors of the applicable Fund. The dividend policy of each Fund is, under normal circumstances, not to pay any cash dividends. However, earnings and realized capital gains of a Fund may be capitalized each year thereby entitling the applicable Fund to certain tax refunds. See “Distribution Policy – Dividends”. See “Canadian Federal Income Tax Considerations” and “Ontario Income Tax Considerations”.

Termination

Either Fund may be dissolved by special resolution of its shareholders. See “Termination of the Fund” and “Attributes of the Securities – Class A Shares – Dissolution” for information about the entitlements of Class A shareholders on a dissolution.

- 12 -

Organization and Management of Covington Fund II Inc. and Covington Strategic Capital Fund Inc.

Covington Capital Corporation: Covington is the investment advisor of Covington Fund II and the manager of Covington Strategic Capital Fund. Covington sources and manages eligible investments for each Fund.

Covington is responsible for identifying investment opportunities, investigating, structuring and negotiating prospective investments, making recommendations and providing certain administrative services. However, the Investment Committee of each Fund is responsible for final approval of all investment decisions. Subject to independent valuation as required under the Ontario Act and approval of the applicable Fund’s Valuation Committee in specified circumstances, Covington is responsible for evaluating and reporting on the performance of portfolio companies on an ongoing basis and assisting the management of portfolio companies where appropriate. Finally, Covington is responsible for the determination and execution of the appropriate timing, terms and methods of liquidating investments in portfolio companies. See “Investment Strategies”.

Covington is a wholly-owned subsidiary of RC Capital which purchased Covington from AMG Canada Corp. on July 2, 2009. RC Capital is owned equally by two trusts of which the Principals are the sole trustees. Mr. Scott D. Clark is the President, Chief Executive Officer and Chief Compliance Officer of Covington and Mr. Philip R. Reddon is the Managing Director of Covington. The Principals, supported by an investment team, have significant experience as investors in, or advisors to, middle market Canadian companies. The Principals have networks of contacts through which to source potential investments and have the capability and experience to undertake financial and business analysis, investment structuring, credit evaluation, business valuation, investment monitoring and control, financial and corporate restructuring, and exit management. See “Organization and Management Details of the Funds – Investment Advisor”.

Covington also provides investment advisory services to certain other labour sponsored investment funds. See “Organization and Management Details of the Funds - Conflicts of Interest”.

The head office and principal place of business of Covington is 200 Front Street West, Suite 3003, Toronto, Ontario M5V 3K2.

The Fund Advisor:

Covington is the fund advisor for the Funds. As fund advisor, Covington provides marketing and investor relations services to the Funds. See “Organization and Management Details of the Funds - CFII Fund Promoter Agreement” and “Organization and Management Details of the Funds - CSCF Fund Advisor Agreement”.

The Fund Administrator:

The Fund Administrator for the Funds is CI, which provides administration and client services, shareholder reporting and transfer agency services to each of the Funds from Toronto, Ontario. See “Organization and Management Details of the Funds - The Fund Administrator of the Funds”.

The Sponsor: The sponsor of each of the Funds is the Canadian Police Association (the “Sponsor”) which is based in Ottawa, Ontario. Prior to August 2003, the Sponsor was the Canadian Police Association Incorporated, which merged with the National Professional Police Association in August 2003 to form the Canadian Police Association. See “Organization and Management Details of

- 13 -

the Funds – The Sponsor of the Funds”.

The Sponsor is entitled to elect that number of directors representing the total number of directors less the number of directors that the holders of the Class A Shares are entitled to elect. Therefore, the Sponsor is currently entitled to elect four out of the six members of the board of directors of Covington Fund II. The Sponsor owns all of the issued and outstanding Class B Shares of Covington Fund II, which entitle holders to one vote per share at general meetings of shareholders of Covington Fund II but do not entitle the holders to any dividends. See “Attributes of the Securities — Sponsor’s Shares (Class B Shares)”.

The Sponsor is entitled to elect that number of directors representing the total number of directors less the number of directors that the holders of the Class A Shares are entitled to elect. Therefore, the Sponsor is currently entitled to elect five of the six members of the board of directors of Covington Strategic Capital Fund. The Sponsor owns all of the issued and outstanding Class B Shares of Covington Strategic Capital Fund, which entitle holders to one vote per share at general meetings of shareholders of Covington Strategic Capital Fund but do not entitle holders to any dividends. See “Attributes of the Securities — Sponsor’s Shares (Class B Shares)”.

While members of the Sponsor may subscribe for Class A Shares of the Funds, neither the Sponsor nor its members are required to make any investment in Class A Shares of the Funds. Individuals investing in Class A Shares need not be members of or have any connection with the Sponsor.

- 14 -

The Registrar and Transfer Agent:

Each of Covington Fund II and Covington Strategic Capital Fund has retained CI to provide registrar, transfer agency, shareholder reporting, customer support and various other administration services. In addition to providing the registrar, transfer agency and other shareholder administration services to Covington Fund II and Covington Strategic Capital Fund, the Registrar and Transfer Agent performs similar services for outside clients including other labour sponsored investment funds. See “Organization and Management Details of the Funds – The Registrar and Transfer Agent”.

The Custodian:

Each of Covington Fund II and Covington Strategic Capital Fund has retained RBC Dexia Investor Services Trust to act as custodian of the Class A Share Investment Portfolios and the reserve portfolio. The Custodian also performs certain valuation and fund accounting services for the Funds. The Custodian provides services to each of Covington Fund II and Covington Strategic Capital Fund in Toronto, Ontario. See “Calculation of Net Asset Value” and “Securityholder Matters – Reporting to Shareholders”.

The Auditor:

Each of Covington Fund II and Covington Strategic Capital Fund has retained Ernst & Young LLP, Ontario to act as the auditor of the Funds. The Auditor provides services to the Funds in Toronto, Ontario. See “Organization and Management Details of the Funds – The Auditor”.

- 15 -

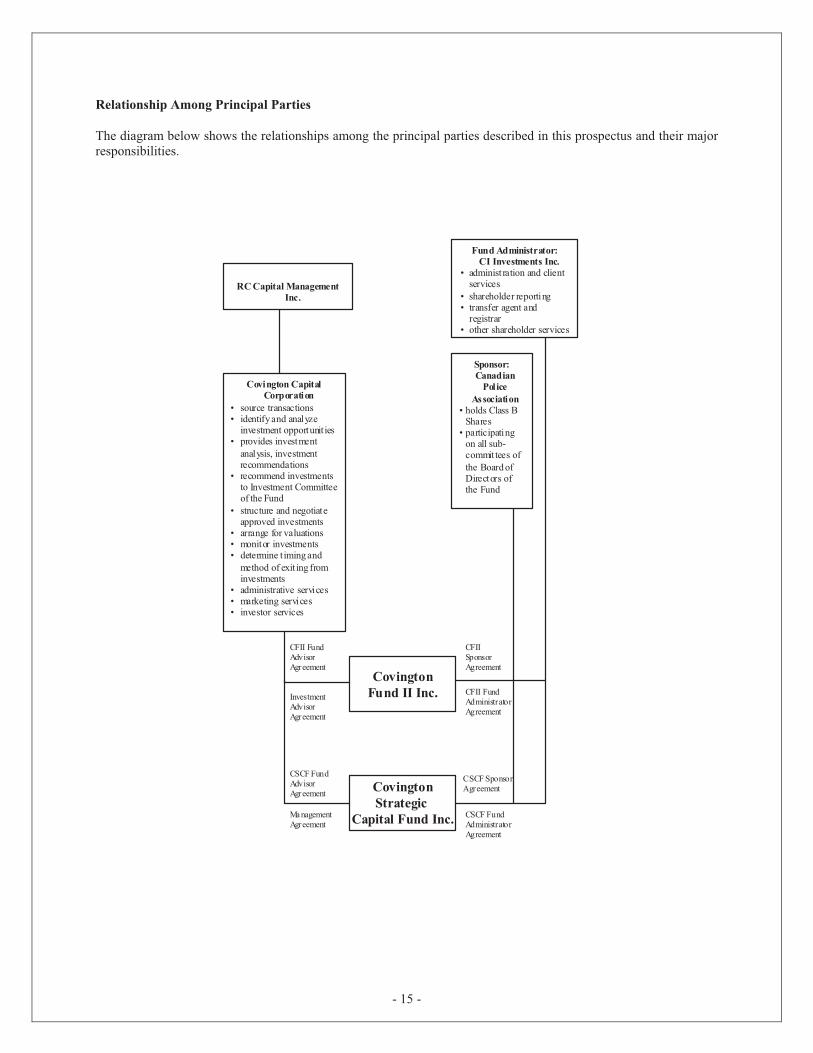

Relationship Among Principal Parties

The diagram below shows the relationships among the principal parties described in this prospectus and their major responsibilities.

RC Capital Management Inc.

Fund Administrator:CI Investments Inc.

• administ ration and client services

• shareholder reporting• transfer agent and

registrar• other shareholder services

Sponsor:Canadian

PoliceAssociation

• holds Class B Shares

• participating on all sub-commit tees of the Board of Directors of the Fund

CFIISponsorAgreement

CFII FundAdministratorAgreement

Covington CapitalCorporation

• source transactions• identify and analyze

investment opportunit ies• provides investment

analysis, investment recommendations

• recommend investments to Investment Committee of the Fund

• structure and negotiate approved investments

• arrange for valuations• monitor investments• determine t iming and

method of exit ing from investments

• administrative services• marketing services• investor services

InvestmentAdvisorAgreement

CFII FundAdvisorAgreement

CovingtonStrategic

Capital Fund Inc.

CSCF Sponsor Agreement

CSCF FundAdministratorAgreement

CSCF FundAdvisorAgreement

Ma nagementAgreement

CovingtonFund II Inc.

- 16 -

Summary of Fees and Expenses

This table lists the fees and expenses that you have to pay if you invest in Covington Fund II Inc. and/or Covington Strategic Capital Fund Inc. You may have to pay some of these fees and expenses directly. The Fund may have to pay some of these fees and expenses, which will reduce the value of your investments in the Fund.

Summary of Distribution Expenses Payable by Covington Fund II

Sales Commissions and Service Fees:

6% of offering price plus an annual service fee of 0.5% of net asset value of Class A Shares.(*)

Investors who purchase Class A Shares will not pay any sales commissions directly.

Covington Fund II pays to the selling registered dealer a commission of 6% of the offering price in respect of the sale of Class A Shares. Covington Fund II also pays to registered dealers a service fee equal to 0.5% annually of the average total net asset value of the Class A Shares held by the clients of the sales representatives of the dealers, calculated and paid monthly. See “Purchases of Securities”.

Marketing Services Fee:

0.5% of offering price of Class A Shares.(*)

Covington Fund II pays to Covington a marketing services fee of 0.5% of the offering price of Class A Shares. See “Purchases of Securities”.

Summary of Distribution Expenses Payable by Covington Strategic Capital Fund

Sales Commissions and Service Fees:

Series I Shares: 10% of offering price plus, after eight years, an annual service fee equal to 0.5% of the net asset value of the Series I Shares.(*)

Investors who purchase Class A Shares will not pay any sales commissions directly.

Series I Shares: Covington pays to the selling registered dealer a commission of 10% of the offering price in respect of the sale of Series I Shares. This commission consists of a 6% commission plus an additional 4% commission of the offering price of the Series I Shares. The 4% commission is paid in lieu of any service fees payable before the eighth anniversary of the date of issue of such Series I Shares. In addition, after a period of eight years, Covington Strategic Capital Fund will pay to registered dealers a service fee equal to 0.5% annually of the net asset value of the Series I Shares held by clients of the sales representatives of such registered dealers, calculated and paid monthly. See “Purchases of Securities”.

Series II Shares: 6% of offering price plus an annual service fee equal to 0.5% of the net asset value of the Series II Shares.(*)

Series II Shares: Covington pays to the selling registered dealer a commission of 6% of the offering price in respect of the sale of Series II Shares. In addition, Covington Strategic Capital Fund pays to registered dealers a service fee equal to 0.5% annually of the net asset value of the Series II Shares held by clients of the sales representatives of such registered dealers, calculated and paid monthly. See “Purchases of Securities”.

Although investors who purchase Class A Shares will not pay any sales commissions directly, they indirectly support the payment of sales commissions by Covington Strategic Capital Fund and Covington as Covington Strategic Capital Fund pays services fees to registered dealers whose sales representatives’ clients hold Class A Shares and Covington Strategic Capital Fund compensates Covington for the payment of sales commissions through a monthly distribution fee and the provision of various

- 17 -

other services discussed in this prospectus through the fees paid in respect of investment advisory services and management services. See “Fees and Expenses” and “Purchases of Securities”.

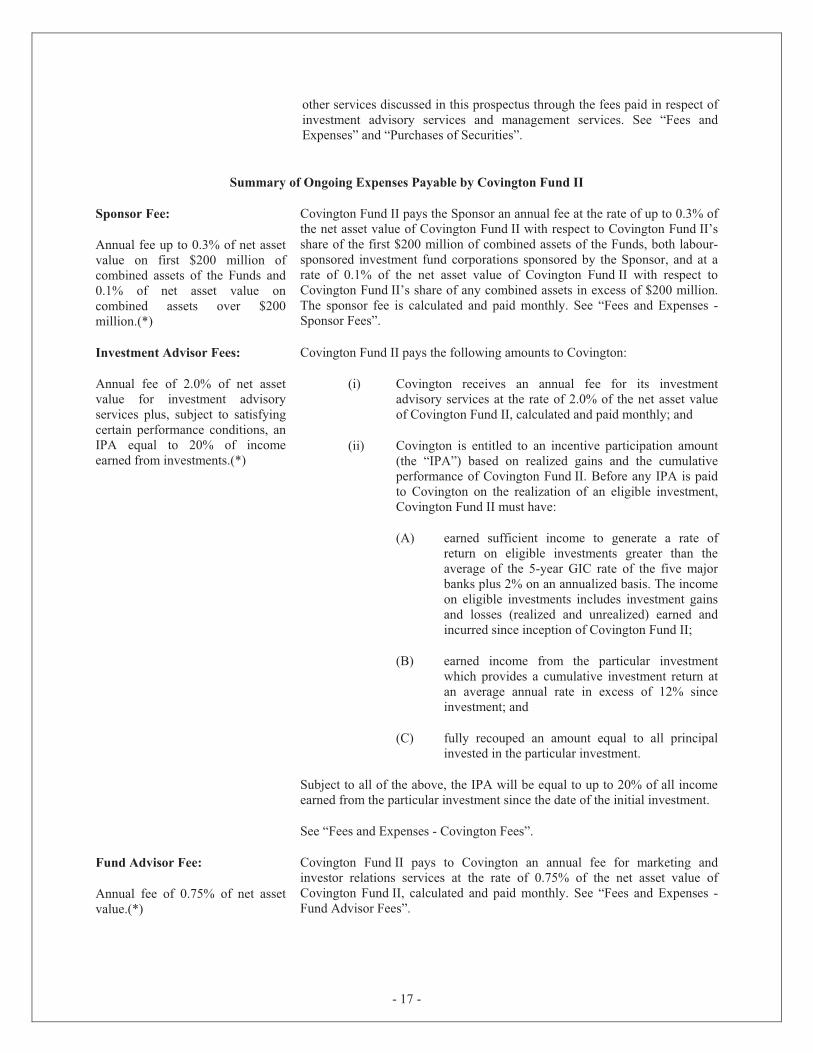

Summary of Ongoing Expenses Payable by Covington Fund II

Sponsor Fee:

Annual fee up to 0.3% of net asset value on first $200 million of combined assets of the Funds and 0.1% of net asset value on combined assets over $200 million.(*)

Covington Fund II pays the Sponsor an annual fee at the rate of up to 0.3% of the net asset value of Covington Fund II with respect to Covington Fund II’s share of the first $200 million of combined assets of the Funds, both labour-sponsored investment fund corporations sponsored by the Sponsor, and at a rate of 0.1% of the net asset value of Covington Fund II with respect to Covington Fund II’s share of any combined assets in excess of $200 million. The sponsor fee is calculated and paid monthly. See “Fees and Expenses - Sponsor Fees”.

Investment Advisor Fees: Covington Fund II pays the following amounts to Covington:

(i) Covington receives an annual fee for its investment advisory services at the rate of 2.0% of the net asset value of Covington Fund II, calculated and paid monthly; and

Annual fee of 2.0% of net asset value for investment advisory services plus, subject to satisfying certain performance conditions, an IPA equal to 20% of income earned from investments.(*)

(ii) Covington is entitled to an incentive participation amount (the “IPA”) based on realized gains and the cumulative performance of Covington Fund II. Before any IPA is paid to Covington on the realization of an eligible investment, Covington Fund II must have:

(A) earned sufficient income to generate a rate of return on eligible investments greater than the average of the 5-year GIC rate of the five major banks plus 2% on an annualized basis. The income on eligible investments includes investment gains and losses (realized and unrealized) earned and incurred since inception of Covington Fund II;

(B) earned income from the particular investment which provides a cumulative investment return at an average annual rate in excess of 12% since investment; and

(C) fully recouped an amount equal to all principal invested in the particular investment.

Subject to all of the above, the IPA will be equal to up to 20% of all income earned from the particular investment since the date of the initial investment.

See “Fees and Expenses - Covington Fees”.

Fund Advisor Fee:

Annual fee of 0.75% of net asset value.(*)

Covington Fund II pays to Covington an annual fee for marketing and investor relations services at the rate of 0.75% of the net asset value of Covington Fund II, calculated and paid monthly. See “Fees and Expenses - Fund Advisor Fees”.

- 18 -

Fund Administrator Fee:

Annual fee of 0.60% of net asset value.(*)

Covington Fund II pays to the Fund Administrator an annual fee for administration and client services, shareholder reporting and transfer agency services at the rate of 0.60% of the net asset value of Covington Fund II per annum. See “Fees and Expenses - Fund Administrator Fees”.

Operating Expenses:

As incurred.(*)

Other Covington Fund II expenses include administrative and operating expenses including expenses relating to portfolio transactions, taxes, legal, audit, custodial and fund accounting fees, costs of qualifying the Class A Shares for distribution, marketing, security realization and directors’ fees (including fees paid to directors who are members of the Audit Committee, Investment Committee or the Valuation Committee). These operating expenses will be higher than those of other mutual funds and pooled investment vehicles. See “Fees and Expenses - Operating Expenses”. All the fees and expenses payable in connection with the establishment and maintenance of the Independent Review Committee will be paid by Covington Fund II. See “Organization and Management Details of the Funds - Independent Review Committee of the Funds”.

Summary of Ongoing Expenses Payable by Covington Strategic Capital Fund

Sponsor Fee:

Annual fee up to 0.3% of average net asset value on the first $200 million of combined assets of the Funds and 0.1% of average net asset value on combined assets over $200 million.(*)

Covington Strategic Capital Fund pays the Sponsor an annual fee at the rate of up to 0.3% of the average net asset value of Covington Strategic Capital Fund with respect to Covington Strategic Capital Fund’s share of the first $200 million of combined assets of Covington Strategic Capital Fund and Covington Fund II Inc., both labour sponsored investment fund corporations sponsored by the Sponsor, and at a rate of 0.1% of the average net asset value of Covington Strategic Capital Fund with respect to the Covington Strategic Capital Fund’s share of any combined assets in excess of $200 million, provided that all of the assets of Covington Fund II are included in the first $200 million of combined assets. The sponsor fee is calculated and paid monthly. See “Fees and Expenses – Sponsor Fees”.

Management Fees:

Annual fee of 1.5% of average net asset value for investment advisory services, plus annual fee of 0.525% of the average net asset value for management services plus, subject to satisfying certain performance conditions, an IPA equal to 20% of income earned from investments.(*)

Covington Strategic Capital Fund pays the following amounts to Covington:

(a) Covington receives an annual fee for its investment advisory services at the rate of 1.5% of the average net asset value of Covington Strategic Capital Fund, calculated and paid monthly;

(b) Covington is entitled to an incentive participation amount (the “IPA”) based on realized gains and the cumulative performance of the Fund. Before any IPA is paid to Covington on the realization of an eligible investment, Covington Strategic Capital Fund must have:

(i) earned sufficient income to generate a rate of return on eligible investments greater than the average of the 5-year GIC rate of the five major Canadian banks plus 2% on an annualized basis. The income on eligible investments includes investment gains and losses (realized and unrealized) earned and incurred since inception of Covington Strategic Capital Fund;

(ii) earned income from the particular investment which provides a cumulative return at an average annual rate in

- 19 -

excess of 8% since investment; and

(iii) fully recouped an amount equal to all principal invested in the particular investment.

Subject to all of the above, the IPA will be equal to up to 20% of all income earned from the particular investment since the date of the initial investment, provided that Covington Strategic Capital Fund will not pay the IPA on any partial disposition of an eligible investment unless and until Covington Strategic Capital Fund receives (from all dispositions of that investment on a cumulative basis) an amount equal to at least the full amount of the principal invested in the eligible investment; and

(c) Covington receives an annual fee for management services at the rate of 0.525% of the average net asset value of Covington Strategic Capital Fund, calculated and paid monthly.

See “Fees and Expenses - Operating Expenses – Manager Fees”.

Fund Advisor Fee:

Monthly fee equal to 1/12 of 0.975% of the net asset value per year.(*)

Covington Strategic Capital Fund pays to Covington a monthly fee for marketing and investor relations services at the rate of 1/12 of 0.975% of the average net asset value of Covington Strategic Capital Fund calculated and paid monthly. See “Fees and Expenses - Operating Expenses – Fund Advisor Fee”.

Fund Administrator Fee:

Annual fee of 0.60% of net asset value(*)

Covington Strategic Capital Fund pays to the Fund Administrator an annual fee for administration and client services, shareholder reporting and transfer agency services at the rate of 0.60% of the net asset value of Covington Strategic Capital Fund per annum. See “Fees and Expenses - Operating Expenses — Fund Administrator Fee”.

Distribution and Services Costs: Covington is responsible for managing the relationship with registered dealers selling the Class A Shares of Covington Strategic Capital Fund and will pay the sales commission to such dealers in respect of sales of the Class A Shares. Such sales commissions will not be charged to nor amortized by Covington Strategic Capital Fund.

Series I Shares: monthly fee equal to 0.160% of the offering price of unredeemed Series I Shares plus, after eight years, Covington Strategic Capital Fund will pay registered dealers having clients holding Series I Shares a commission equal to 0.5% annually of the net asset value of the Series I Shares held by clients of the sales representatives of such registered dealers.(*)

Series I Shares: Covington Strategic Capital Fund pays Covington a monthly distribution services fee in respect of such distribution related services equal to 0.160% of the offering price of the issued and unredeemed Series I Shares, equivalent to an annual distribution services fee of 1.92% of such offering price. The monthly distribution services fee is intended to reimburse Covington for financing costs incurred to fund the payment of the commissions, including an amount for interest and a one-time financing commitment fee payable in connection with such financing. In addition, after a period of eight years, Covington Strategic Capital Fund pays to each registered dealer having clients holding Series I Shares a servicing commission equal to 0.5% annually of the net asset value of the Series I Shares held by clients of the sales representatives of such registered dealers, calculated and paid monthly. See “Purchases of Securities”.

- 20 -

Series II Shares: monthly fee equal to 0.096% of original issue price of unredeemed Series II Shares plus Covington Strategic Capital Fund will pay registered dealers having clients holding Series II Shares a commission equal to 0.5% annually of the net asset value of the Series II Shares held by clients of the sales representatives of such registered dealers.(*)

Series II Shares: Covington Strategic Capital Fund pays Covington a monthly distribution services fee in respect of such distribution related services equal to 0.096% of the offering price of the issued and unredeemed Series II Shares, equivalent to an annual distribution services fee of 1.152% of such offering price. The monthly distribution services fee is intended to reimburse Covington for financing costs incurred to fund the payment of the commissions, including an amount for interest and a one-time financing commitment fee payable in connection with such financing. In addition, Covington Strategic Capital Fund pays to each registered dealer having clients holding Series II Shares a servicing commission equal to 0.5% annually of the net asset value of the Series II Shares held by clients of the sales representatives of such registered dealers, calculated and paid monthly. See “Purchases of Securities”.

Operating Expenses:

As incurred.(*)

Other Covington Strategic Capital Fund expenses include administrative expenses and operating expenses including expenses relating to portfolio transactions, taxes, legal, audit, custodial and fund accounting fees, costs of qualifying the Class A Shares for distribution, marketing, security realization and directors’ fees (including fees paid to directors who are members of the Audit Committee, Investment Committee or the Valuation Committee). These operating expenses will be higher than those of other mutual funds and pooled investment vehicles. See “Fees and Expenses - Operating Expenses”. All the fees and expenses payable in connection with the establishment and maintenance of the Independent Review Committee will be paid by Covington Strategic Capital Fund. See “Organization and Management Details of the Funds - Independent Review Committee of the Funds”.

Summary of Investor Expenses for Covington Fund II

Sales Charge: Nil.

Transfer Fee: Nil.

RRSP/RRIF Fee: Nil. See “Purchase of Class A Shares — RRSPs and RRIFs”.

Redemption Fee:

Up to 6% of the offering price, reduced by 0.75% of the offering price for each year or partial year elapsed since issuance.(*)

A redemption fee of up to 6% of the offering price of the Class A Shares will be charged to investors and calculated as 0.75% of the offering price of the Class A Shares multiplied by the number of years or partial years remaining until the eighth anniversary of the date of issue of such Class A Shares. After the eighth anniversary of the date of issue of the Class A Shares, there will be no redemption fee. The redemption fee will be deducted from the redemption amount otherwise payable and will be paid to Covington Fund II. See “Redemption of Securities” and “Attributes of the Securities — Class A Shares — Redemption”.

Summary of Investor Expenses for Covington Strategic Capital Fund

Sales Charge: Nil.

Transfer Fee: Nil.

RRSP/RRIF Fee: Nil. See “Purchases of Securities - RRSPs and RRIFs”.

- 21 -

Redemption Fee:

Series I Shares: up to 10% of offering price, reduced by 1.25% of the offering price for each year or partial year elapsed since issuance.(*)

Series I Shares: A redemption fee of up to 10% of the offering price of the Series I Shares will be charged to investors and calculated as 1.25% of the offering price of the Series I Shares multiplied by the number of years or partial years remaining until the eighth anniversary of the date of issue of such Series I Shares. After the eighth anniversary of the date of issue of the Series I Shares, there will be no redemption fee. The redemption fee will be deducted from the redemption amount otherwise payable and will be paid to Covington. See “Redemption of Securities” and “Attributes of the Securities — Class A Shares — Redemption”.

Series II Shares: up to 6% of offering price, reduced by 0.75% of the offering price for each year or partial year elapsed since issuance.(*)

Series II Shares: A redemption fee of up to 6% of the offering price of the Series II Shares will be charged to investors and calculated as 0.75% of the offering price of the Series II Shares multiplied by the number of years or partial years remaining until the eighth anniversary of the date of issue of such Series II Shares. After the eighth anniversary of the date of issue of the Series II Shares, there will be no redemption fee. The redemption fee will be deducted from the redemption amount otherwise payable and will be paid to Covington Strategic Capital Fund who will in turn pay it to Covington. See “Redemption of Securities” and “Attributes of the Securities — Class A Shares — Redemption”.

Summary of Dealer Compensation for the Funds

Sales Commissions: See “Summary of Distribution Expenses Payable by Covington Fund II ___ Sales Commissions and Service Fees” and “Summary of Distribution Expenses Payable by Covington Strategic Capital Fund — Sales Commissions and Service Fees”.

Service Fee: See “Summary of Ongoing Expenses Payable by Covington Fund II — Sales Commissions and Service Fees” and “Summary of Ongoing Expenses Payable by Covington Strategic Capital Fund – Sales Commissions and Service Fees”.

Notes:

(*) This is only a summary and should be read together with the detailed information appearing elsewhere in this prospectus

- 22 -

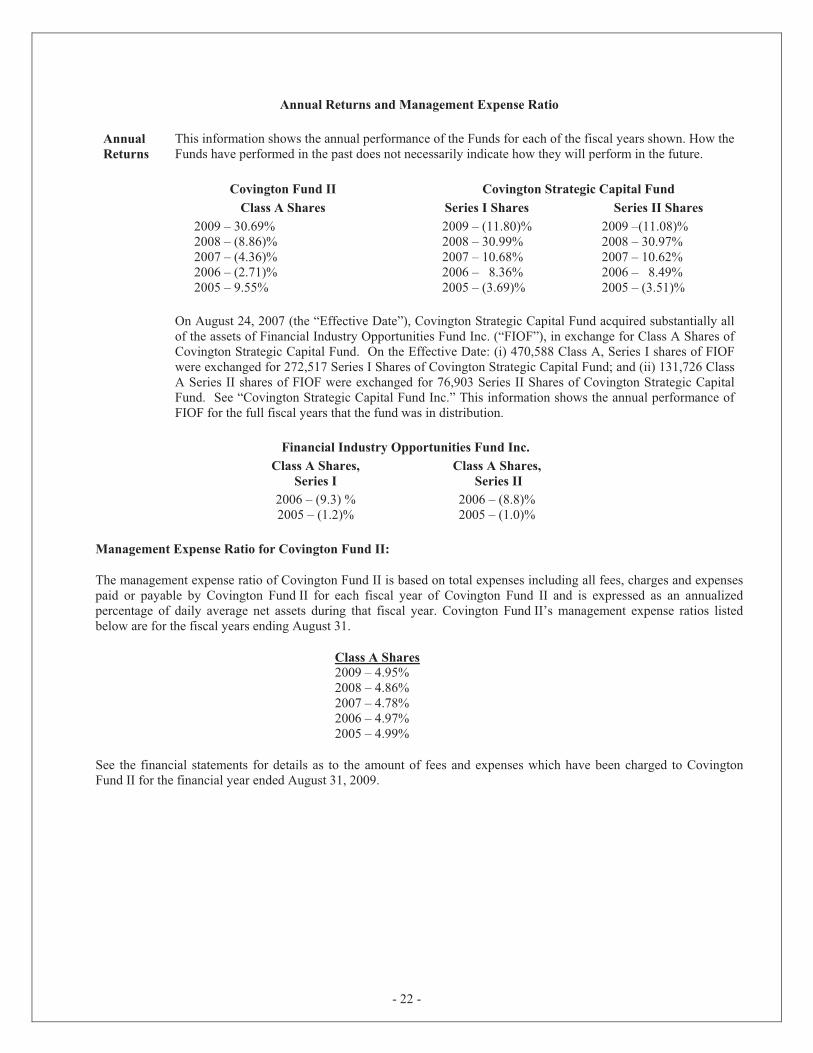

Annual Returns and Management Expense Ratio

Annual Returns

This information shows the annual performance of the Funds for each of the fiscal years shown. How the Funds have performed in the past does not necessarily indicate how they will perform in the future.

Covington Fund II Covington Strategic Capital Fund Class A Shares Series I Shares Series II Shares

2009 – 30.69% 2008 – (8.86)% 2007 – (4.36)% 2006 – (2.71)% 2005 – 9.55%

2009 – (11.80)% 2008 – 30.99% 2007 – 10.68% 2006 – 8.36% 2005 – (3.69)%

2009 –(11.08)% 2008 – 30.97% 2007 – 10.62% 2006 – 8.49% 2005 – (3.51)%

On August 24, 2007 (the “Effective Date”), Covington Strategic Capital Fund acquired substantially all of the assets of Financial Industry Opportunities Fund Inc. (“FIOF”), in exchange for Class A Shares of Covington Strategic Capital Fund. On the Effective Date: (i) 470,588 Class A, Series I shares of FIOF were exchanged for 272,517 Series I Shares of Covington Strategic Capital Fund; and (ii) 131,726 Class A Series II shares of FIOF were exchanged for 76,903 Series II Shares of Covington Strategic Capital Fund. See “Covington Strategic Capital Fund Inc.” This information shows the annual performance of FIOF for the full fiscal years that the fund was in distribution.

Financial Industry Opportunities Fund Inc.

Class A Shares, Series I Class A Shares,

Series II

2006 – (9.3) % 2005 – (1.2)%

2006 – (8.8)% 2005 – (1.0)%

Management Expense Ratio for Covington Fund II:

The management expense ratio of Covington Fund II is based on total expenses including all fees, charges and expenses paid or payable by Covington Fund II for each fiscal year of Covington Fund II and is expressed as an annualized percentage of daily average net assets during that fiscal year. Covington Fund II’s management expense ratios listed below are for the fiscal years ending August 31.

Class A Shares 2009 – 4.95% 2008 – 4.86% 2007 – 4.78% 2006 – 4.97% 2005 – 4.99%

See the financial statements for details as to the amount of fees and expenses which have been charged to Covington Fund II for the financial year ended August 31, 2009.

- 23 -

Management Expense Ratio for Covington Strategic Capital Fund:

The management expense ratio of Covington Strategic Capital Fund is based on total expenses including all fees, charges and expenses paid or payable by Covington Strategic Capital Fund for each fiscal year of Covington Strategic Capital Fund and is expressed as an annualized percentage of daily average net assets during that fiscal year. Covington Strategic Capital Fund’s management expense ratios listed below are for the fiscal years ending August 31.

Series I Shares Series II Shares

2009 – 8.57%* 2009 – 8.44%* 2008 – 15.81%* 2008 – 15.56%* 2007 – 12.28%* 2007 – 10.72%* 2006 – 4.78% 2006 – 4.49% 2005 – 7.40% 2005 – 7.12%