Validation of a Process-Based Agro-Ecosystem Model (Agro ...

Upload

cathleen-petersCategory

view

217download

1

Prospects for world supply & demand of vegetable oils - global challenges and implications for theoil palm agro-industry

Peter Thoenes Trade and Markets Division Food and Agriculture Organization of the U.N.

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es

Overview

1. Medium-term outlook for the global oilcrop market2. Global food demand, food security, resource issues and

climate change3. The case of oil palm

4. Emerging recommendations

2

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es 1. Medium-term outlook for the global oilcrop market

a) Price projectionsb) Supply projectionsc) Demand projections (incl. biofuel)d) Trade Projectionse) Sources of uncertainty

• model-based projections generated by OECD-FAO• entire agricultural sector, including biofuel• only four main oilcrops & products covered• 10-year horizon 2009-2018

focus on vegoils ... palm oil3

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

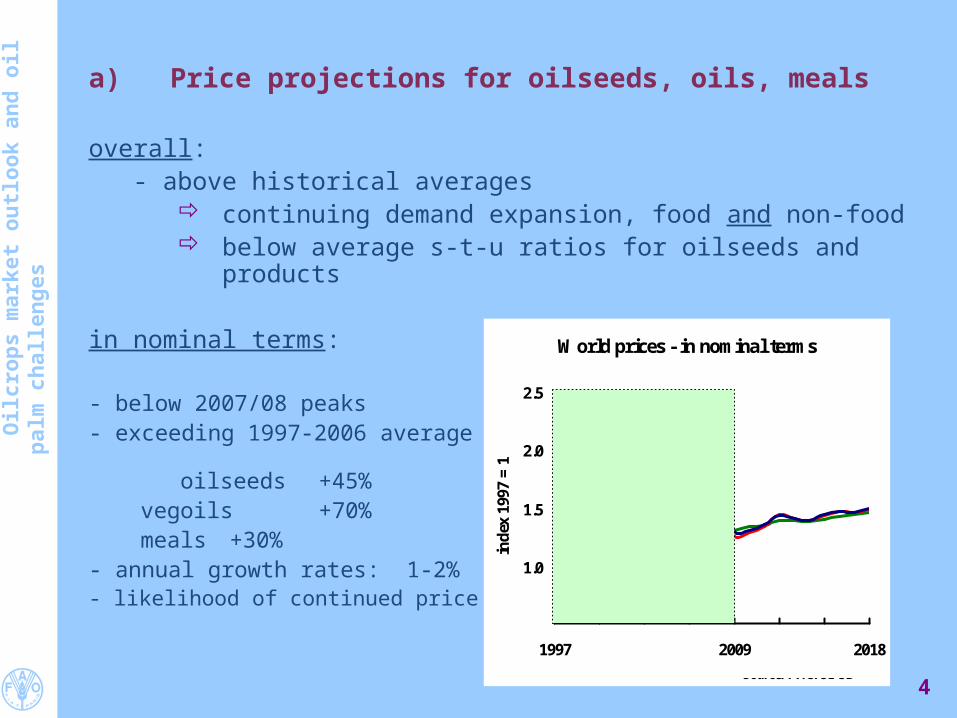

es a) Price projections for oilseeds, oils, meals

overall:- above historical averages

continuing demand expansion, food and non-food below average s-t-u ratios for oilseeds and products

in nominal terms:

- below 2007/08 peaks- exceeding 1997-2006 average

oilseeds +45%vegoils +70%meals +30%

- annual growth rates: 1-2%- likelihood of continued price volatility

4

World prices - in nominal terms

0.5

1.0

1.5

2.0

2.5

1997 2000 2003 2006 2009 2012 2015 2018

ind

ex 1

997

= 1

Vegetable Oils

Oilseeds

Oilseed meals

Source: FAO/OECD

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

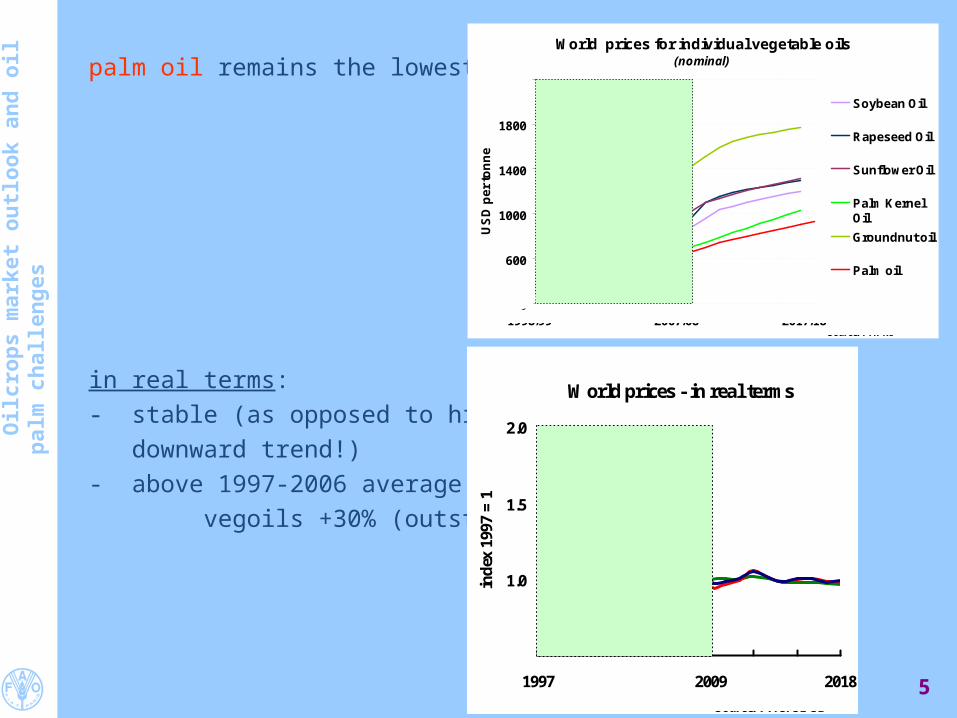

es palm oil remains the lowest-priced oil

in real terms:- stable (as opposed to historical downward trend!)- above 1997-2006 average: vegoils +30% (outstanding!)

5

World prices for individual vegetable oils(nominal)

200

600

1000

1400

1800

2200

US

D p

er

ton

ne

Soybean Oil

Rapeseed Oil

Sunflower Oil

Palm KernelOil

Groundnut oil

Palm oil

1998/99 2007/08 2017/18Source: FAPRI

World prices - in real terms

0.5

1.0

1.5

2.0

1997 2000 2003 2006 2009 2012 2015 2018

ind

ex 1

997

= 1

Vegetable Oils

Oilseeds

Oilseed meals

Source: FAO/OECD

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

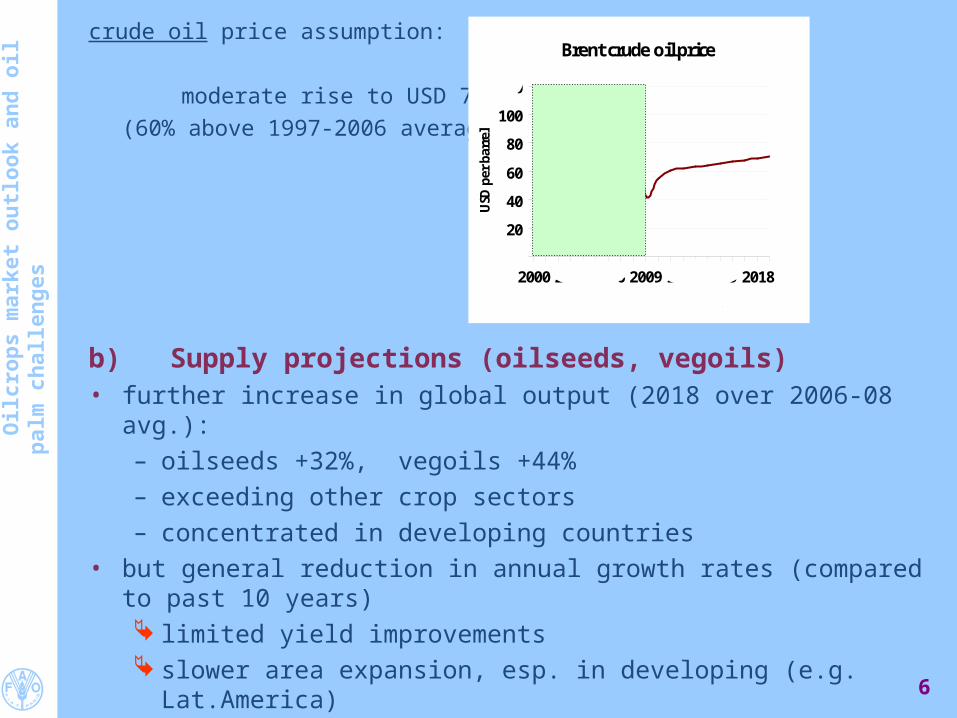

escrude oil price assumption:

moderate rise to USD 70 in 2018(60% above 1997-2006 average)

b) Supply projections (oilseeds, vegoils)• further increase in global output (2018 over 2006-08 avg.):

– oilseeds +32%, vegoils +44% – exceeding other crop sectors– concentrated in developing countries

• but general reduction in annual growth rates (compared to past 10 years) limited yield improvements slower area expansion, esp. in developing (e.g. Lat.America)

6

Brent crude oil price

0

20

40

60

80

100

120

2000 2003 2006 2009 2012 2015 2018

USD

per

bar

rel

Source: USEIA, OECD

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es• EU vegoil production continues to expand: +26% (from domestic and imported seed)• palm oil:

– fastest expanding vegoil (ahead of soy oil)– driven by food and industrial demand– main factor in Indonesia: area; in Malaysia: yield – share in total vegoil output: grows to 30%

c) Demand projections for vegoils

• further expansion: +44%• commodity group with fastest growing consumption: 3% p.a.• but growth slowdown

reduced population growth + saturation effects firm prices

• developing countries contribute most (esp. in Asia) population growth, income growth, low per caput consumption level

• largest expansion: palm oil, followed by soyoil• EU and China account for 28% and 16% of global expansion

7

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

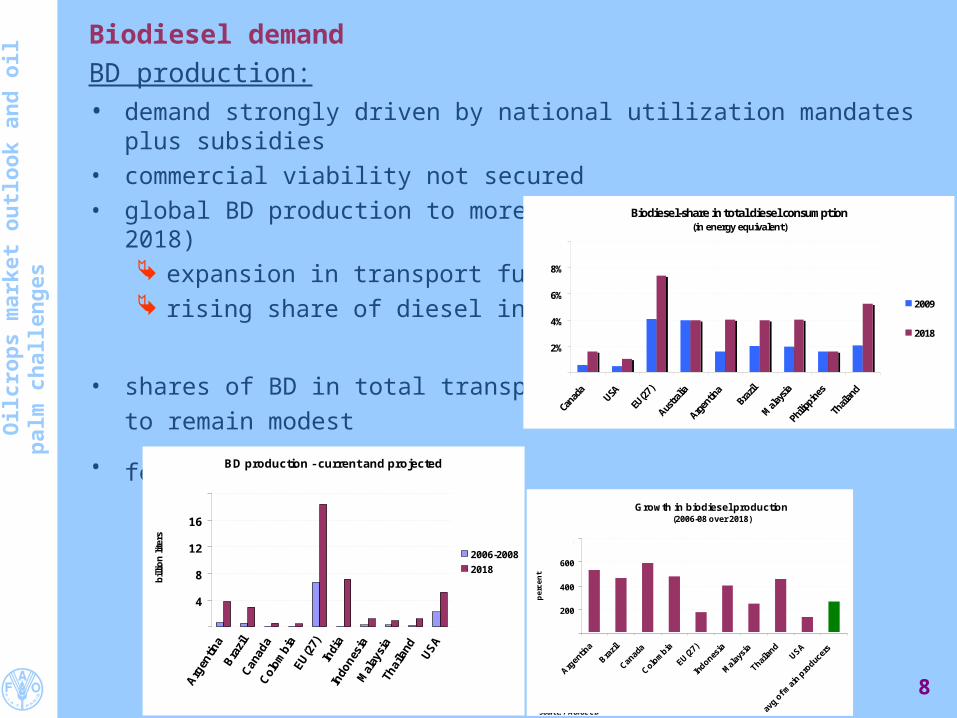

esBiodiesel demandBD production:• demand strongly driven by national utilization mandates plus subsidies• commercial viability not secured• global BD production to more than double: +127% (2009-2018)

expansion in transport fuel rising share of diesel in transp. fuel

• shares of BD in total transport fuelto remain modest

• few important players:

8

BD production - current and projected

0

4

8

12

16

20

Arg

entin

a

Bra

zil

Can

ada

Col

ombi

a

EU(2

7)

Indi

a

Indo

nesi

a

Mal

aysi

a

T

haila

nd

US

A

bill

ion

lite

rs

2006-2008

2018

Source: FAO/OECD

Growth in biodiesel production(2006-08 over 2018)

0

200

400

600

800

Arg

entin

a

Bra

zil

Canad

a

Col

ombia

EU(27)

Indones

ia

Mal

aysi

a

Thai

land

USA

avg o

f mai

n pro

ducer

s

pe

rce

nt

Source: FAO/OECD

.

Biodiesel-share in total diesel consumption(in energy equivalent)

0%

2%

4%

6%

8%

10%

2009

2018

Source: FAO/OECD

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

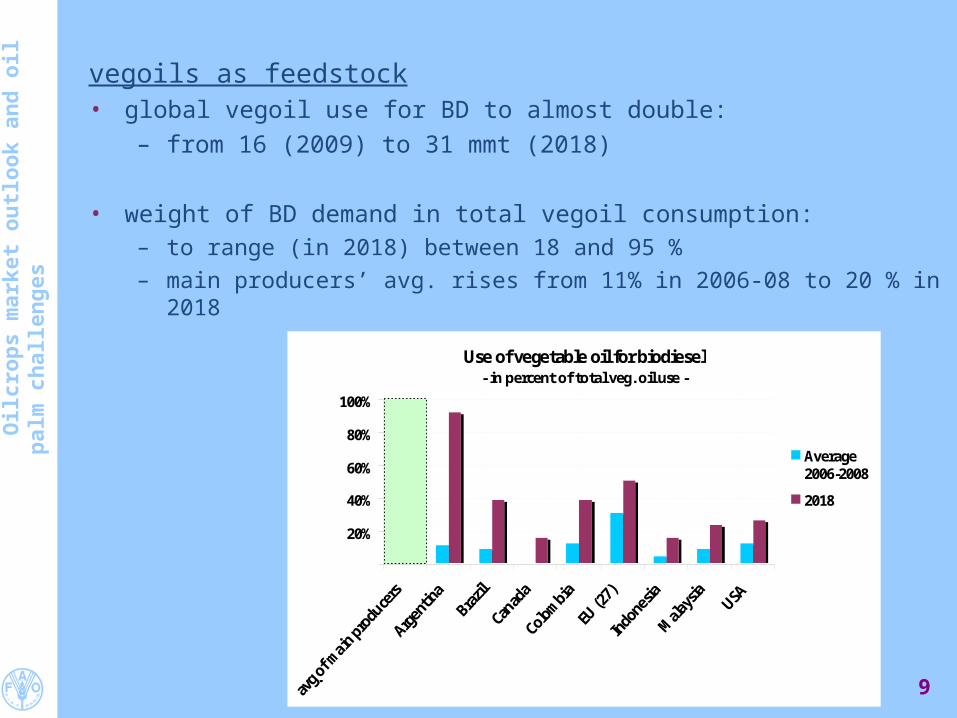

es vegoils as feedstock• global vegoil use for BD to almost double:

– from 16 (2009) to 31 mmt (2018)

• weight of BD demand in total vegoil consumption:– to range (in 2018) between 18 and 95 %– main producers’ avg. rises from 11% in 2006-08 to 20 % in 2018

9

Use of vegetable oil for biodiesel- in percent of total veg. oil use -

0%

20%

40%

60%

80%

100%

avg of m

ain produce

rsArge

ntina

Brazil

Canad

aColombia

EU (2

7)IndonesiaM

alays

ia

USA

Average2006-2008

2018

Source: FAO/OECD.

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

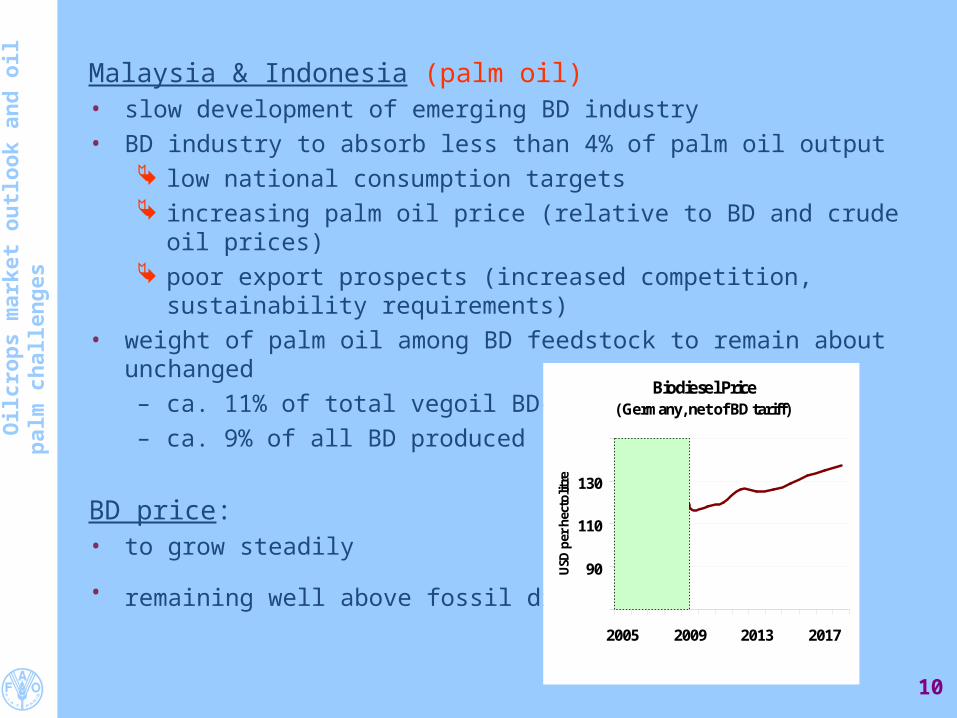

es Malaysia & Indonesia (palm oil)• slow development of emerging BD industry• BD industry to absorb less than 4% of palm oil output

low national consumption targets increasing palm oil price (relative to BD and crude oil prices) poor export prospects (increased competition, sustainability requirements)

• weight of palm oil among BD feedstock to remain about unchanged– ca. 11% of total vegoil BD-use– ca. 9% of all BD produced

BD price:• to grow steadily

• remaining well above fossil diesel prices

10

Biodiesel Price( Germany, net of BD tariff)

70

90

110

130

150

2005 2009 2013 2017

USD

per

hec

tolit

re

Source: FAO/OECD

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

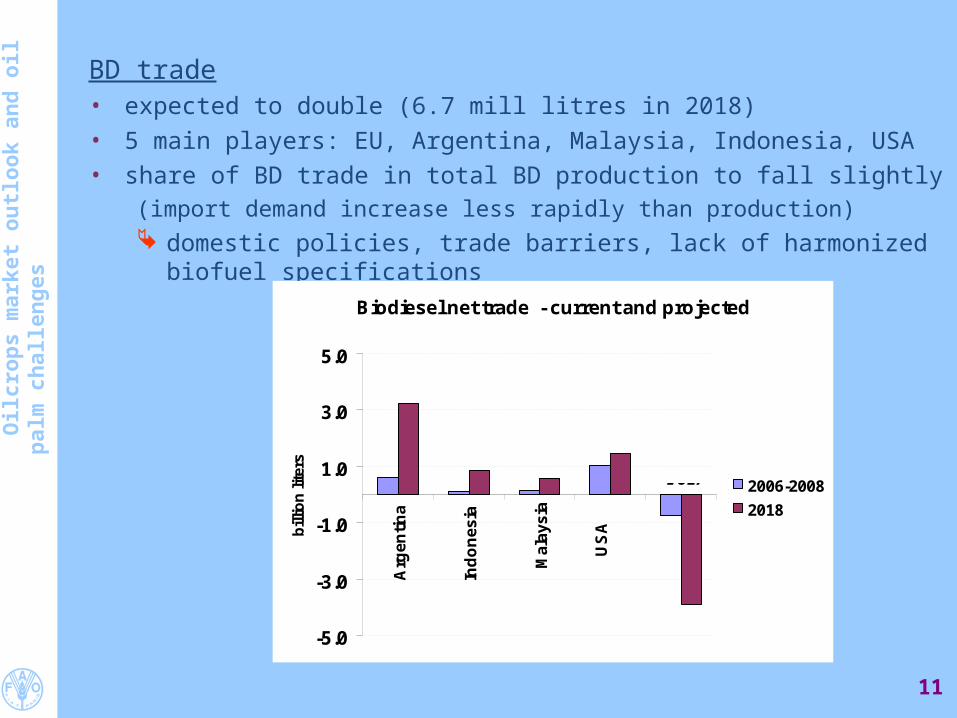

es BD trade• expected to double (6.7 mill litres in 2018)• 5 main players: EU, Argentina, Malaysia, Indonesia, USA• share of BD trade in total BD production to fall slightly

(import demand increase less rapidly than production) domestic policies, trade barriers, lack of harmonized biofuel specifications

11

Biodiesel net trade - current and projected

-5.0

-3.0

-1.0

1.0

3.0

5.0

A

rge

nti

na

Ind

on

es

ia

Ma

lay

sia

US

A

bill

ion

lite

rs

2006-2008

2018

EU27

Source: FAO/OECD

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

esd) Trade projections (major vegoils)

• 50% expansion– production in main comsumption regions not keeping up with demand– fastest growing commodity– BF production triggers additional import demand

• lead of developing countries • continued expansion in South-South trade• palm oil: remains most traded vegoil

Export market:• 3 countries to supply 75%: Indonesia, Malaysia, Argentina • Indonesia & Malaysia (palm oil)

– 4-5% annual growth– 80-90% of domestic production exported

• Argentina & Brazil (soy oil)– moderate growth

• other sources of growth: Canada, USA, CIS nations 12

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

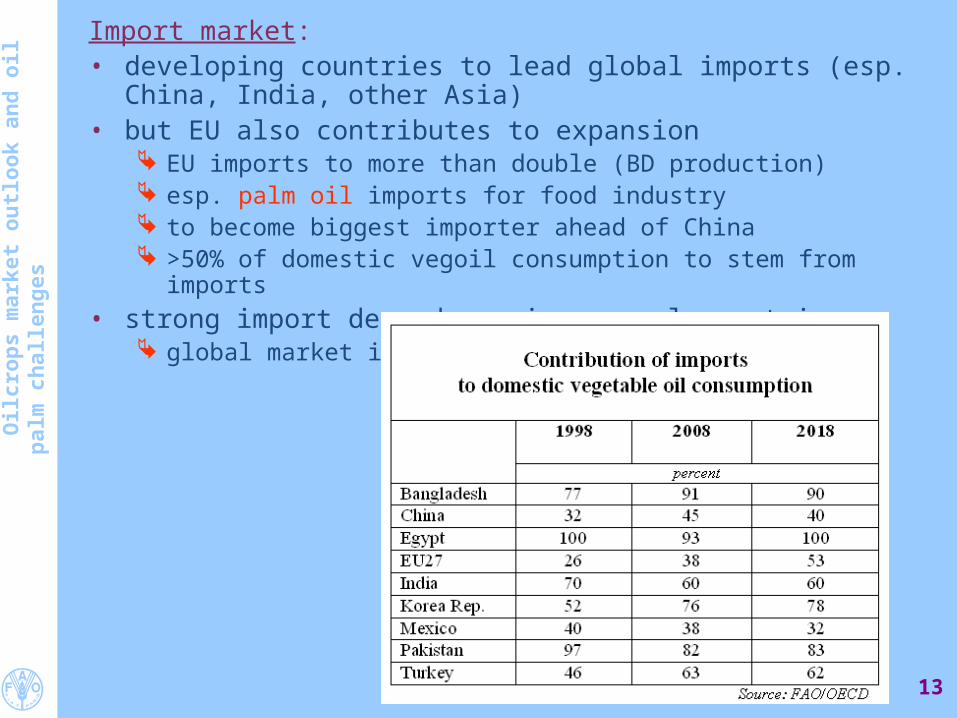

esImport market:• developing countries to lead global imports (esp. China, India, other Asia)• but EU also contributes to expansion

EU imports to more than double (BD production) esp. palm oil imports for food industry to become biggest importer ahead of China >50% of domestic vegoil consumption to stem from imports

• strong import dependence in several countries global market instability

13

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es e) Sources of uncertainty

• resumption of global economic growth: 2010 or later?• policy responses to global price volatility• high market concentration increases market instability • continued consumer concerns about environmental risks as well as GM

products• exposure to developments in the energy market:

higher crude oil priceslower crop production (via rising production costs)reduce food consumption (via higher crop prices)increase BD production

• land reallocations triggered by food/fuel competition

14

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es 2. Global food demand, food security, resource issues and climate change

a) Food securityb) Global food demand, resource issues, climate change

15

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

esa) Food security

• good medium- and longer-term market prospects– stable/slightly rising commodity prices– demand growth matched by production increase– developing nations participating in expansion of production, consumption and

trade• deterioration in world hunger and food security

– rise in number of people living below the hunger threshold– rising food prices

contributing factors:– temporary supply and demand imbalances– increased market instability– national interventions in markets– direct linkage energy & food prices– food/fuel competition– falling international investment flows– budgetary pressure on development aid– global economic slowdown

16

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

esb) Global food demand, resource issues, climate change

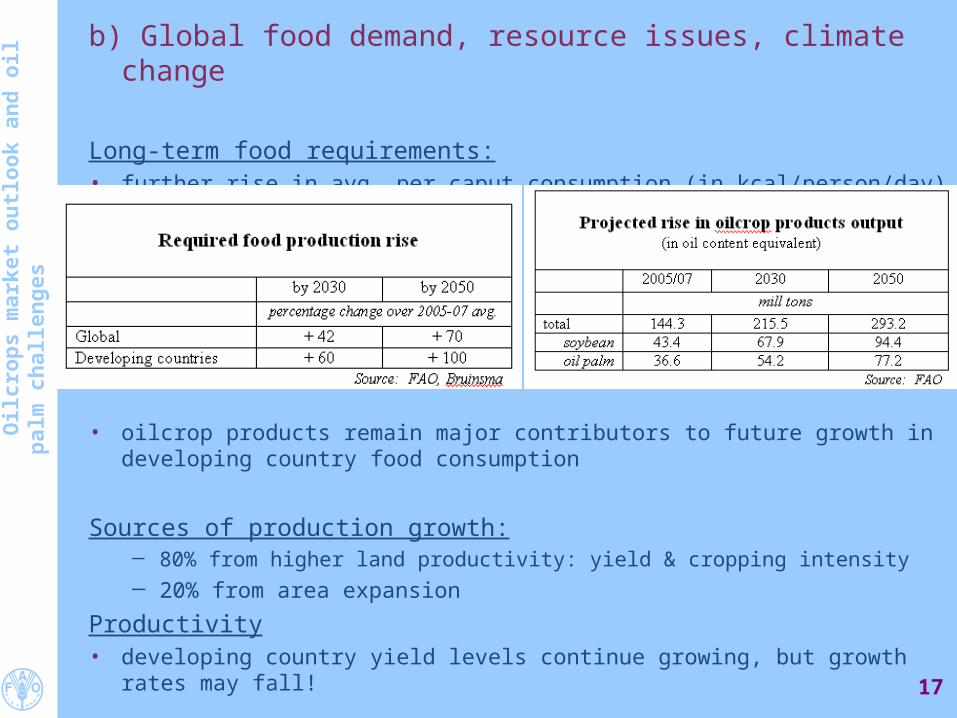

Long-term food requirements:• further rise in avg. per caput consumption (in kcal/person/day)

• oilcrop products remain major contributors to future growth in developing country food consumption

Sources of production growth:─ 80% from higher land productivity: yield & cropping intensity─ 20% from area expansion

Productivity• developing country yield levels continue growing, but growth rates may fall!

17

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

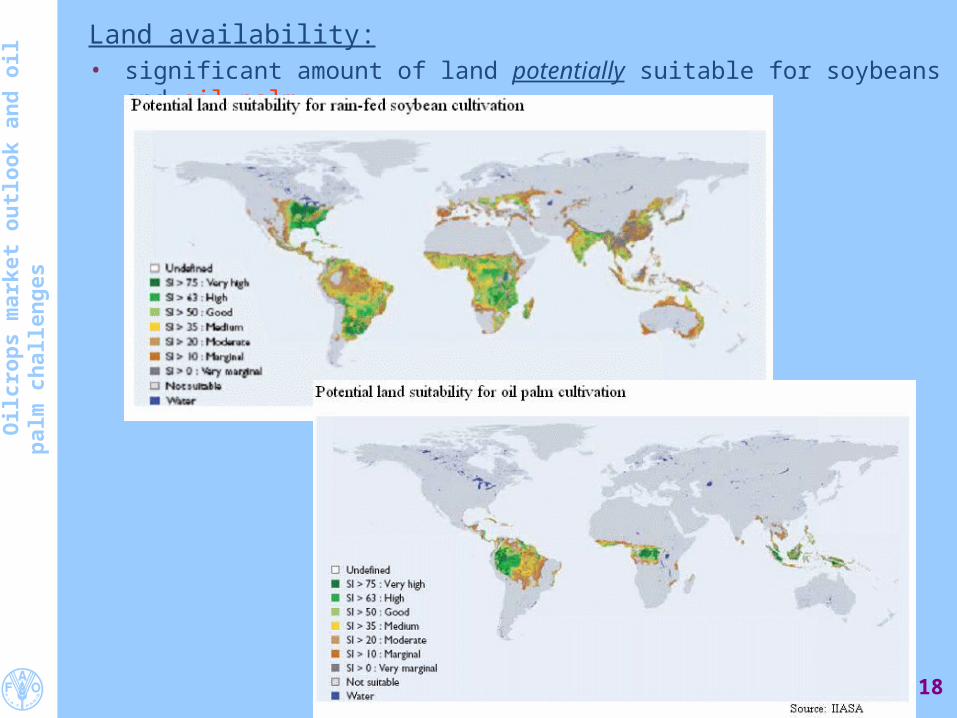

esLand availability:• significant amount of land potentially suitable for soybeans and oil palm

18

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es

• actual land availability is limited competition among food crops, pasture uses, wood uses and other, new uses

(energy crops, crops with low carbon footprint) growing urban, industrial, infrastructural uses only part of the land has high or at least good yield potential considerable part of land consists of forest - conversion carries significant

social/environmental costs

Climate change:

• no consensus on ultimate net global impact on agric. production• global warming and changing rainfall patterns potentially

beneficial in high latitude regions damaging in low latitude tropical areas

• uncertainty regarding the effects of higher atmospheric CO2 concentration (carbon fertilization)

• consensus: – food security to be affected– considerable scope to improve resilience via adaptation – until 2050: increased risk of water stress; rising incidence of extreme weather

events– after 2050: significant impact on agr productivity (shifts in production frontiers)

and on the global food system19

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es 3. The case of oil palm

a) Growth factors: productivity and areab) Area expansion issuesc) Productivity improvementd) Socio-economic dimensione) Palm oil as BD feedstock

20

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

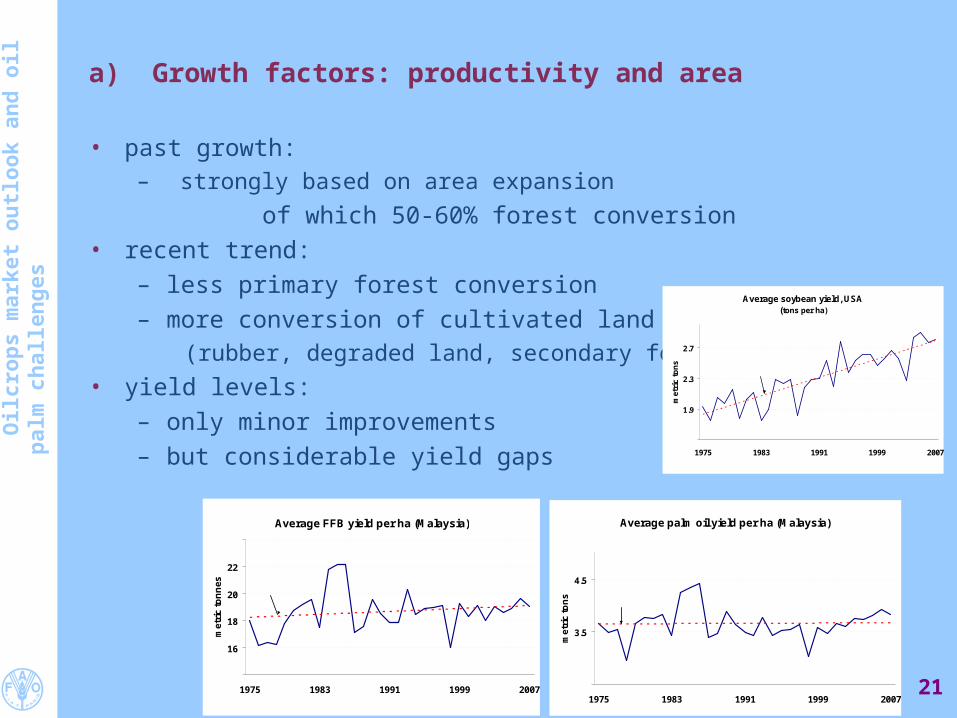

es a) Growth factors: productivity and area

• past growth:– strongly based on area expansion

of which 50-60% forest conversion• recent trend:

– less primary forest conversion– more conversion of cultivated land

(rubber, degraded land, secondary forests)• yield levels:

– only minor improvements – but considerable yield gaps

21

Average FFB yield per ha (Malaysia)

14

16

18

20

22

24

1975 1983 1991 1999 2007

me

tric

to

nn

es

linear trend

Source : MPOB

Average palm oil yield per ha (Malaysia)

2.5

3.5

4.5

1975 1983 1991 1999 2007

me

tric

to

ns

linear trend

Source : MPOB

Average soybean yield, USA(tons per ha)

1.5

1.9

2.3

2.7

1975 1983 1991 1999 2007

met

ric

ton

s

linear trend

Source : FAO

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

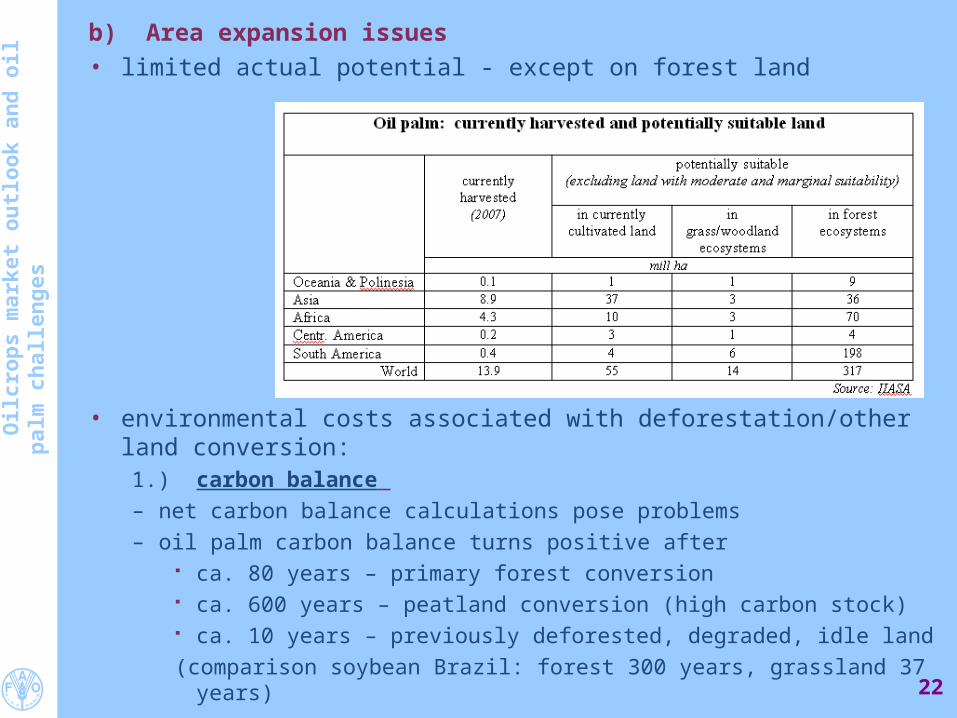

esb) Area expansion issues• limited actual potential - except on forest land

• environmental costs associated with deforestation/other land conversion:1.) carbon balance – net carbon balance calculations pose problems– oil palm carbon balance turns positive after

ca. 80 years – primary forest conversion ca. 600 years – peatland conversion (high carbon stock) ca. 10 years – previously deforested, degraded, idle land(comparison soybean Brazil: forest 300 years, grassland 37 years)

22

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es 2.) reduction in biodiversity─ highest in forest conversion─ some improvement when degraded land is reclaimed

3.) additional problems associated with deforestation─ land fragmentation─ loss of forest habitats─ land clearing through fire (traditional method, cost effective, common

among smallholders)

c) Productivity improvement

1.) improved management practices─ esp. in smallholder oil palm cultivation (closing the yield gap)

typically using less productive land limited access to capital and labour limited access to technical/managerial know-how

23

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es

2.) improved planting material─ smallholder access (closing yield gap) ─ traditional selection and breeding methods

19-year selection cycle limited supplies of improved material

─ genetic modification 2008 breakthrough: sequencing of oil palm genome much shorter selection cycle risk: GM opposition by end-consumers

d) Socio-economic aspects

• important benefits– employment and income generation– improved access to health care, education and other social services– attractive for smallholders (good return-to-input ratio)

• dangers associated with deforestation– erosion of traditional culture, income sources, self-sufficiency– conflicts over land tenure right

• workforce issues– labourers’ rights not respected– ethnic conflicts in case of migrant labourers

• smallholder dependence on large mills (setting the FFB price) 24

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es e) Palm oil as BD feedstock

• lowest-priced feedstock with good energy efficiency

• competition from vegoils that enjoy direct policy support

• all vegoil feedstock (as well as ethanol feedstock) achieve limited net carbon savings compared to fossil fuels

esp. when counting direct/indirect land use changes• all food-crop based BF production affects food supply and food prices

rising market instabilitynegative repercussions on food security

• investment uncertainties:– further changes in policy interventions

(food security, environmental & budgetary considerations, standards)– future crude oil-vegoil price ratio

– advent of (replacement by) 2nd generation feedstock & technologies

25

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es4. Emerging recommendations

a) National priorities

oil palm cultivation• minimize conversion of primary forests• encourage use of idle, degraded and other marginal land• promote best management practices in production & processing

– sustainable yield improvement– reduced land degradation, pollution etc.– biodiversity preservation , cover crops, IPM etc.

• support smallholder involvement– improve access to high-yielding varieties– promote improved plantation management– encourage establishment of smallholder cooperatives– retain diversification – promote development of small-scale mills

• secure funding for R&D and infrastructural works• enforce (and monitor adherence to) regulations

– environmental protection– land tenure guarantees, labour rights etc.– product quality (sustainability standards)

26

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es Palm oil-based biodiesel production• favour production on land not suitable for food production• allow gradual expansion of BF industry; put in place entire commodity chain;

provide appropriate regulatory framework • favour production for domestic market

general support to rural development and overall economic growth meeting fuel needs in areas where feedstock is grown, esp. less accessible areas

• production for export offers limited scope main consumers rely on domestic sources (except EU) various barriers to trade remain (lack of harmonized specifications,

sustainability certification, tariff protection)

27

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es a) International priorities

Food security• coordinate national policies and market interventions to reduce food security risks• encourage establishment of social safety net schemes• accelerate multilateral trade liberalization

Biofuel sector • improve policy planning and coordination• harmonization of trade regulations, sustainability standards• promote transition to 2nd generation technologies and feedstock

Climate change• coordinate national policies• foster analysis of impact on global agric. & food systems• coordinate research & investment into adaptation measures

28

Oilc

rop

s m

arke

t o

utl

oo

k an

d o

il p

alm

ch

alle

ng

es Oil palm• promote schemes that reward reduced deforestation and forest degradation

(e.g. REDD) and other control measures• support voluntary, private sector initiatives on standards for sustainable production

and processing (e.g. RSPO)─ application is demanding and costly; economic return is uncertain─ adaptation to smallholder environment needed─ supporting legal/policy reforms required at national level

• coordinate investment into agric. R&D (productivity enhancement) and facilitate technology transfer

29