Cost Report Workshops and OMB Uniform Guidance Cost Principles

Upload

lamont-fullingtonCategory

view

217download

3

Proposed OMB Uniform Guidance: Cost

Principles, Audit, and Administrative

Requirements for Federal Awards

National Association for State Community Services Programs

Kevin C. Myren, C.P.A.

Overall Themes

Major Changes

Impact on our Work

What’s Next

Questions and Answers

AGENDA

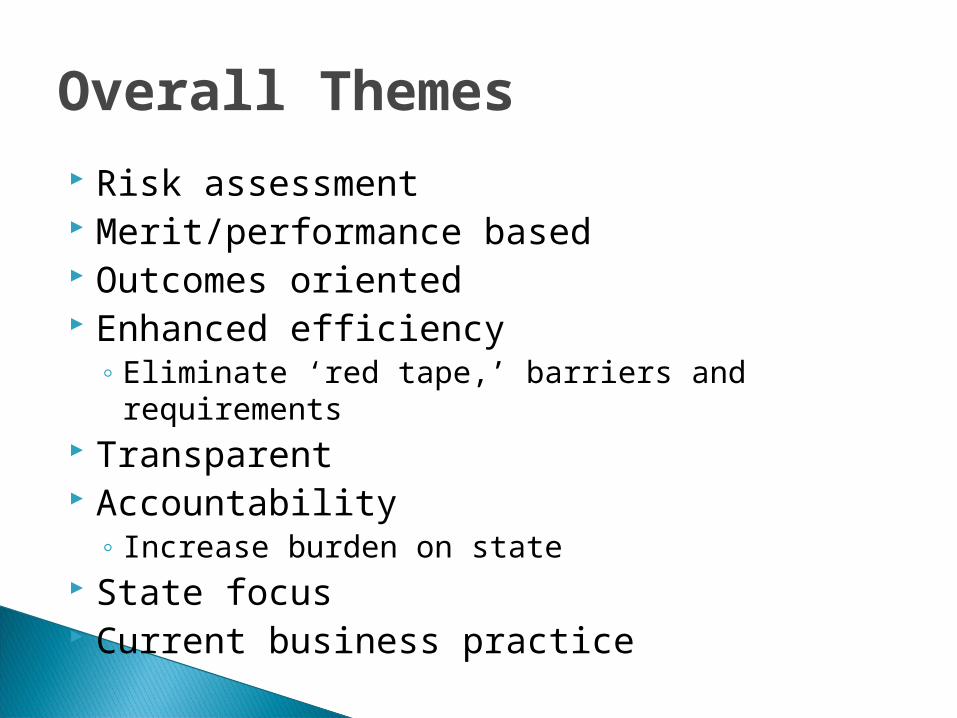

Overall Themes

Risk assessment Merit/performance based Outcomes oriented Enhanced efficiency

◦ Eliminate ‘red tape,’ barriers and requirements Transparent Accountability

◦ Increase burden on state State focus Current business practice

Overall Themes

Major Changes

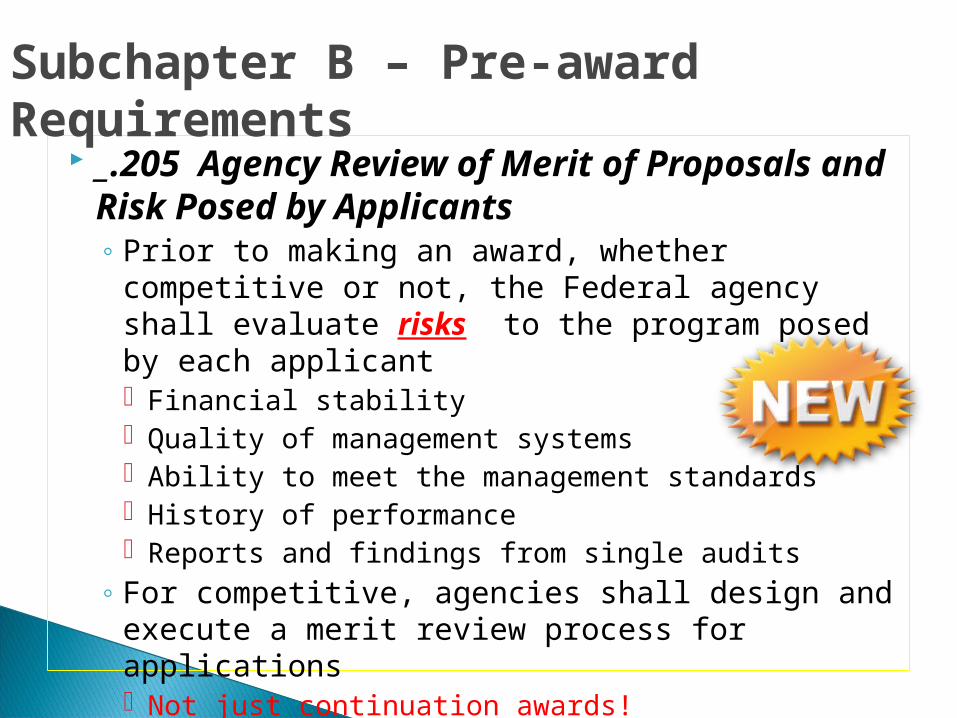

_.205 Agency Review of Merit of Proposals and Risk Posed by Applicants◦ Prior to making an award, whether competitive or

not, the Federal agency shall evaluate risks to the program posed by each applicant Financial stability Quality of management systems Ability to meet the management standards History of performance Reports and findings from single audits

◦ For competitive, agencies shall design and execute a merit review process for applications Not just continuation awards!

Subchapter B – Pre-award Requirements

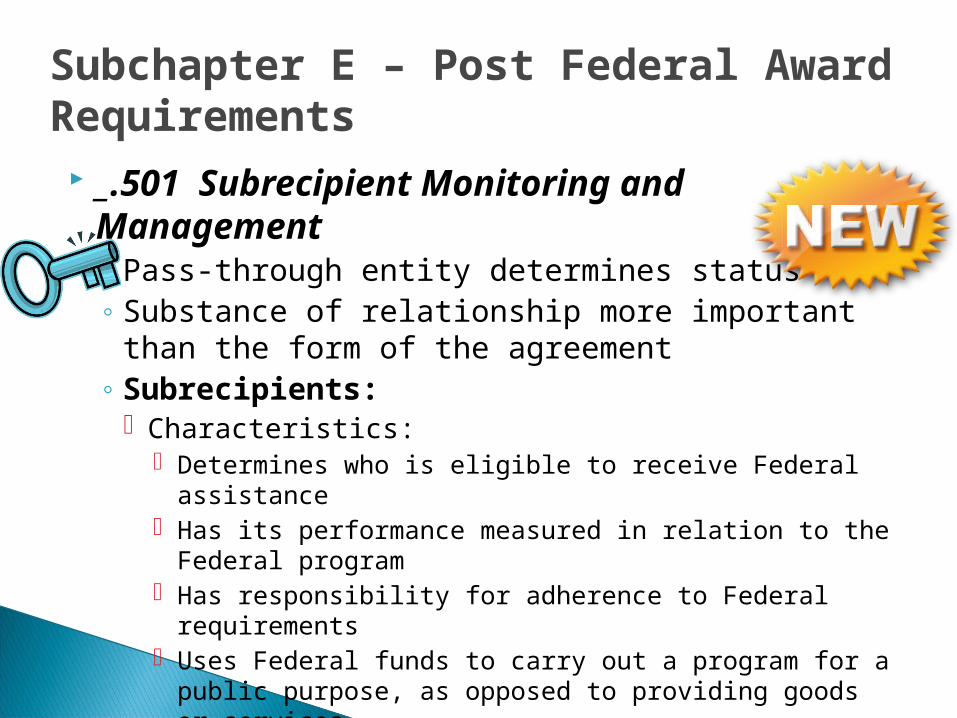

_.501 Subrecipient Monitoring and Management ◦ Pass-through entity determines status◦ Substance of relationship more important than

the form of the agreement◦ Subrecipients:

Characteristics: Determines who is eligible to receive Federal assistance Has its performance measured in relation to the Federal

program Has responsibility for adherence to Federal requirements Uses Federal funds to carry out a program for a public

purpose, as opposed to providing goods or services

Subchapter E – Post Federal Award Requirements

_.501 Subrecipient Monitoring and Management, continued◦ Contractors:

Characteristics: Provides goods or services within normal business

operations Provides similar goods or services to many different

purchasers Normally operates in a competitive environment Provides goods or services that are ancillary to the

operation of the Federal program Is NOT subject to compliance requirements

Subchapter E – Post Federal Award Requirements

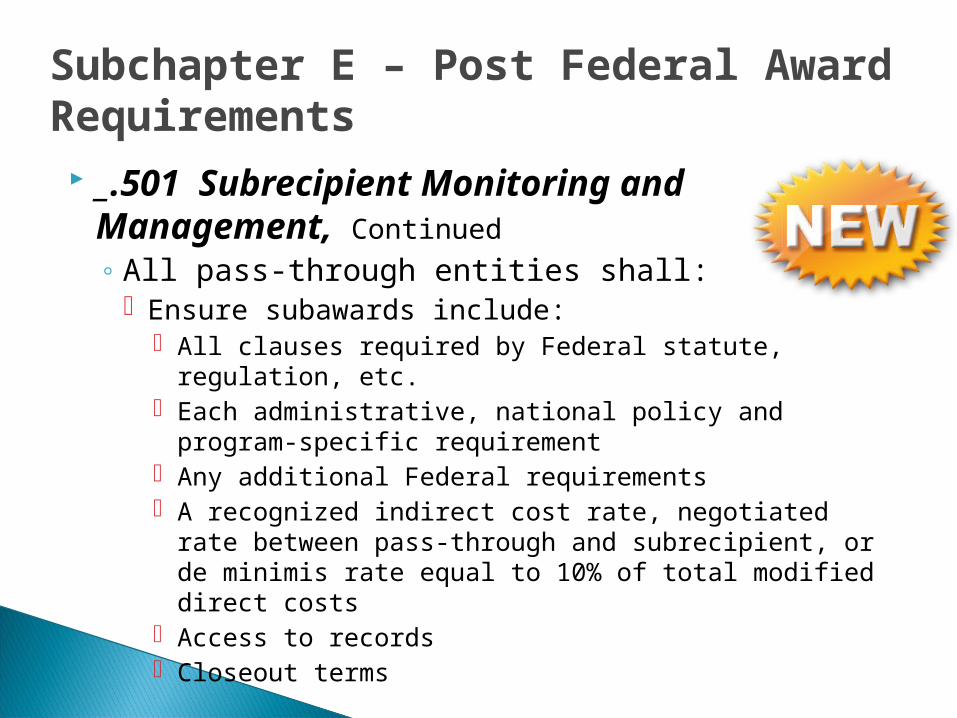

_.501 Subrecipient Monitoring and Management, Continued◦ All pass-through entities shall:

Ensure subawards include: All clauses required by Federal statute, regulation, etc. Each administrative, national policy and program-

specific requirement Any additional Federal requirements A recognized indirect cost rate, negotiated rate between

pass-through and subrecipient, or de minimis rate equal to 10% of total modified direct costs

Access to records Closeout terms

Subchapter E – Post Federal Award Requirements

_.501 Subrecipient Monitoring and Management, Continued◦ All pass-through entities shall, Continued

Inform the subrecipient of the CFFA title and number Ensure subrecipients are aware of requirements

imposed upon them by Federal laws, regulations, and provisions of subawards

Monitor the activities as necessary to ensure Federal awards are used for authorized purpose, in compliance with laws, regulations and provisions of subawards Analyze financial and programmatic reports of subs Follow-up and ensure subs take timely and appropriate

action on all deficiencies from audits and on-site reviews Issue a management decision for audit findings

Subchapter E – Post Federal Award Requirements

_.501 Subrecipient Monitoring and Management, Continued◦ All pass-through entities shall, Continued◦ Depending upon pass-through entity’s assessment of risk posed

by the subrecipient, the following monitoring tools may be used to ensure proper accountability and compliance with program requirements and achievement of performance goals” Performing on-site reviews of operations Providing training and technical assistance Arranging for agreed-upon-procedures engagements

◦ Ensure every sub is audited◦ Consider whether adjustments are needed on pass

through books◦ Consider taking enforcement

action

Subchapter E – Post Federal Award Requirements

_.502 Standards for Financial and Program Management, continued◦ Period of availability◦ Internal Controls

Recipient shall identify Federal awards received and expended

Must maintain internal control over Federal programs that provides reasonable assurance that awards are managed in compliance with laws, regulations, terms and conditions of awards that could have a material effect on each program

Comply with laws, regulations, and the terms and conditions of Federal awards for each of its programs

Subchapter E – Post Federal Award Requirements

_.503 Property Standards, continued

◦ Equipment Title vests upon acquisition in the recipient or sub States will use, manage and dispose of equipment

acquired under an award in accordance with state laws and procedures

Use: Equipment shall be used for purpose as long as needed When no longer needed, may be used in other activities

supported by a Federal agency (includes IT systems) May use for a few, but may not compete unfairly with

private companies that provide equivalent services May trade-in or use sales proceeds to offset cost of

replacement equipment, subject to Federal approval

Subchapter E – Post Federal Award Requirements

_.504 Procurement Standards◦ States will follow state policies and procedures◦ Requirements:

Recipients use their own procurement procedures Maintain a contract administration system Written standards of real or apparent conflict of

interest Review proposed procurements to avoid unnecessary

or duplicative acquisitions Encouraged to use

State and local intergovernmental agreements Federal excess and surplus property Value engineering

Consider contractor integrity, compliance, past performance and technical and financial resources

Subchapter E – Post Federal Award Requirements

_.504 Procurement Standards, continued◦ Competition

Full and open competition Contractors that develop specs, ect are prohibited from

proposing Situations considered restrictive of competition

Unreasonable requirements on firms to qualify Unnecessary experience and excessive bonding Specifying a “brand name”

Written selection procedures Must have a written procurement protest procedure

Subchapter E – Post Federal Award Requirements

_.504 Procurement Standards, continued◦ Methods of procurement:

Some form of cost or price analysis required for all Small purchases

$150,000 or less Price or rate quotations shall be obtained from an

adequate number of qualified sources Sealed bids

Preferred method for procuring construction Invitation for bids will be publicly advertised Bids will be publicly opened Awarded to lowest responsive and responsible bidder

Subchapter E – Post Federal Award Requirements

_.504 Procurement Standards, continued◦ Methods of procurement, continued

Competitive proposals Requests for proposals will be publicized Solicited from an adequate number of qualified sources Written method for conducting technical evaluation Awarded to firm whose proposal is most advantageous to

the program, with price and other factors considered Noncompetitive proposals

Available only from a single source

Subchapter E – Post Federal Award Requirements

_.504 Procurement Standards, continued◦ Small, minority, women and labor surplus area

firms Affirmative steps:

Placing firms on solicitation lists Solicited whenever they are potential sources Dividing total requirements into smaller tasks Requiring prime contractor to subcontract

Subchapter E – Post Federal Award Requirements

_.505 Performance and financial Monitoring and Reporting◦ Collect reports electronically◦ Shall only solicit OMB-approved data elements for

financial reporting◦ Monitoring by recipients must cover each

program, function or activity◦ Performance reports must include:

Comparison of actual accomplishments to award Reason for slippage, if any Explanation of any cost overruns or high unit cost

Subchapter E – Post Federal Award Requirements

_.616 Indirect (F & A) Costs, Continued

◦ Negotiate Indirect Cost Rates Negotiated rates shall be accepted by all Federal agencies Any entity that has never received or does not currently

have a negotiated indirect cost rate is eligible for a de minimis indirect cost rate of 10% of modified total direct costs (MTDC) May be utilized for an initial period of up to 4 years MTDC = salaries, wages, fringe benefits, materials and

supplies, services, travel and subgrants up to the first $25,000 of each

Excluded from MTDC = equipment, capital expenditures, rent, participant costs

All entities may apply for a one-time extension of a current negotiated indirect cost rate for a period of up to 4 years

Subchapter F – Cost PrinciplesSubtitle III – Direct and Indirect Costs

_.621 Selected Items of Cost, Continued

◦ C – 10 Compensation – Personal Services Reasonable – consistent with that paid for similar work Consistent – must follow organization-wide

policies/practices Incentive compensation

Overall compensation must be reasonable Paid or accrued pursuant to an agreement entered into in good

faith before services were rendered

Subchapter F – Cost PrinciplesSubtitle VI – General Provisions for Selected

Items of Cost

_.621 Selected Items of Cost, Continued

◦ C – 10 Compensation – Personal Services Standards for Documentation of Personnel Expenses

Based on documented payrolls approved by a responsible official

No documentation outside payroll system required for employee who works in a single indirect activity

Where employee works solely on a single Federal award, charges will be supported by periodic certification Certification prepared at least semi-annually AND signed by

employee or a responsible supervisory official Reports may be integrated into payroll distribution system

No duplication necessary Reports must be after-the-fact certification

Subchapter F – Cost PrinciplesSubtitle VI – General Provisions for Selected

Items of Cost

_.621 Selected Items of Cost, Continued

◦ C – 10 Compensation – Personal Services Standards for Documentation of Personnel Expenses

Nonprofessional employees’ compensation must supported by records indicating total hours worked

Salaries/wages for matching/cost sharing must be supported in the same manner

Substitute system for allocating salaries/wages may be used, if approved by the cognizant agency Random moment sampling, “rolling” time studies, case counts, or

other quantifiable measures of employee effort After the fact certification is still required

Subchapter F – Cost PrinciplesSubtitle VI – General Provisions for Selected

Items of Cost

_.621 Selected Items of Cost, Continued

◦ C – 11 Compensation – Fringe Benefits Costs of leaves, employee insurances, pensions Must be reasonable and required by law, entity-employee

agreement or an established policy Leaves

Under written leave policies Equitably allocated to all related activities Determined by GAAP, when leave is earned

Lesser of the amount accrued or funded Insurances and pensions must be granted under a written

policy May be assigned to cost objectives by indentifying specific

benefits to individual employees or by allocating on the basis of entity-wide salaries and wages

Subchapter F – Cost PrinciplesSubtitle VI – General Provisions for Selected

Items of Cost

_.621 Selected Items of Cost, Continued

◦ C – 11 Compensation – Fringe Benefits Insurance

Reserves under a self-insurance program for unemployment compensation or workers’ comp are allowable If provisions represent reasonable estimates of liabilities However, provisions for self-insured liabilities which do not

become payable for more than one year after the provision is made shall not exceed the present value of the liability

Automobiles That portion of automobile costs furnished by the entity that

relates to personal use by employees is unallowable regardless of whether the cost is reported as taxable income to the employee

Subchapter F – Cost PrinciplesSubtitle VI – General Provisions for Selected

Items of Cost

_.621 Selected Items of Cost, Continued

◦ C – 11 Compensation – Fringe Benefits Pension

Costs for a fiscal year must be funded within 6 months of fiscal year end

Post Retirement Health Pay-as-you-go…actual payments to beneficiaries are allowable Actuarial cost…GAAP expense allowed, if funded in 6 months

Severance Pay Allowable if required by law, employer-employee agreement,

or established policy

Subchapter F – Cost PrinciplesSubtitle VI – General Provisions for Selected

Items of Cost

_.701 Audit Requirements◦ Required for non-Federal entities that expend $750,000

or more in Federal awards in a year Single audit unless eligible and elect program-specific

audit Program-specific audit allowable if entity has only one

Federal program When a subrecipient and a contractor – Recipient and sub

subject to audit requirements; contractor would not Contractor – Federal compliance conditions do NOT pass

down For-profit subrecipients, pass through entity shall establish

requirements

Subchapter G – Audit RequirementsSubtitle II – Audits

_.708 Auditee responsibilities◦ The auditee shall:

Prepare appropriate financial statements Procure or otherwise arrange for the audit Follow up and take corrective action on audit findings Provide the auditor with access

_.709 Auditor Selection◦ Factors to considered in evaluating proposals for audit

services: responsiveness; relevant experience; availability of staff with professional qualifications; technical abilities; peer review; and, price

◦ Preparer of indirect cost proposal or cost allocation plan can NOT perform the audit

Subchapter G – Audit RequirementsSubtitle III – Auditees

_.710 Financial Statements◦ Auditee shall prepare:

Statement of Financial Position Statement of Activities (results of operations/changes in

NA) Statement of Cash Flows Schedule of expenditures of Federal Awards

_.711 Audit Findings Follow-Up◦ Auditee shall prepare schedule of prior audit findings◦ Auditee shall prepare Corrective Action Plan, for

current year findings

Subchapter G – Audit RequirementsSubtitle III – Auditees

_.714 Management Decision◦ Federal agency or pass-through entity shall make

management decision on audit findings◦ Federal agency is responsibility for coordinating a

management decision for a program◦ Pass-through entity shall make management decision

on findings of subrecipients◦ Management decision shall be made within 6 months

of acceptance of the audit report by the Federal Clearinghouse

Subchapter G – Audit RequirementsSubtitle IV – Federal Agencies

_.717 Audit Findings◦ Significant deficiencies and material weaknesses in

internal control over major programs◦ Material noncompliance with the provisions of laws,

regulations or terms/conditions of awards over a major◦ Known questioned costs that are greater than $25,000

Auditor should project potential error◦ Known or likely fraud

Subchapter G – Audit RequirementsSubtitle V – Auditors

_.717 Audit Findings, Continued

◦ Elements of a finding Federal program and Federal award identification CFFA number and title Criteria upon which the audit finding is based (citation) Condition found (facts that support the deficiency) Statement of effect Identification of questioned cost and how computed Information on prevalence (# of findings from # in

universe) Whether a repeat finding from a previous audit Recommendation to prevent future occurrences View of responsible official of the auditee

Subchapter G – Audit RequirementsSubtitle V – Auditors

_.718 Audit Documentation◦ Must be sufficiently detailed to enable someone having

no previous connection to the audit to understand Nature, timing and extent of audit procedures Results of audit procedures performed and evidence

obtained Conclusions reached on significant matters Extent of agreement between accounting records and

audited financial statement◦ Auditor shall retain audit documentation for 3 years

after date of issuance of the auditor’s report

Subchapter G – Audit RequirementsSubtitle V – Auditors

Audit Requirements Streamlining the types of compliance

requirements.◦ Focus on areas of higher risk◦ In:

A. Activities Allowed/Unallowed and B. Allowable Costs/Cost Principles (combined)

C. Cash Management E. Eligibility L. Reporting M. Subrecipient Monitoring N. Special Tests and Provisions

Audit Requirements Out:

◦ D. Davis-Bacon◦ F. Equipment and Real property Management◦ G. Matching, Level of Effort and Earmarking◦ H. Period of Availability of Federal Funds◦ I. Procurement and Suspension and Debarment◦ J. Program Income◦ K. Real Property Acquisition and Relocation

Assistance

Impact on our Work

Potential Impact on Our Work Some agencies may no longer be audited

◦ $500,001 - $750,000 Some programs may not be audited

◦ Major program definition changes Amount of dollars audited will decrease Auditors will no longer review certain compliance

elements Emphasis on RISK analysis MERIT, not just continuation Subchapter E.501 – Monitoring responsibilities

more detailed (greater emphasis)◦ Need to use single audits

Indirect cost rates – what’s next? Internal control section is new, what’s it mean?

Responding to the Change Educating our recipients

◦ Communicating changes Training

◦ Update policies and procedures Procurement Payroll systems

Modifying our monitoring practices Sharing Best Practices

What’s Next

What Next…… Comments through June 2, 2013 OMB will ‘FINAL’ the document

◦ Perhaps as early as end of the year??????? Then agencies have one year to codify

◦ Put in the CFR Then put it in the grants

Over 300 comments received by OMB Mostly from Colleges/Universities & Native

American Tribes General Themes:

◦ Lack of Privacy (Tribal Governments)◦ Time and effort reporting◦ Deadlines for reporting◦ Monitoring requirements are too burdensome◦ Indirect Cost Rates

Comments

Full text of Proposed OMB Uniform Guidance for Federal Financial Assistance◦ http://www.regulations.gov/#!documentDetail;D=

OMB-2013-0001-0002

CROSSWALKS from existing to proposed guidance◦ http://www.regulations.gov/#!docketBrowser;rpp=

25;po=0;dct=SR%252BO;D=OMB-2013-0001

Resources

Questions………………………….