PROPERTY MAH SING GROUP - AmeSecurities Sing Group 1208… · PROPERTY MAH SING GROUP (MSGB MK,...

11

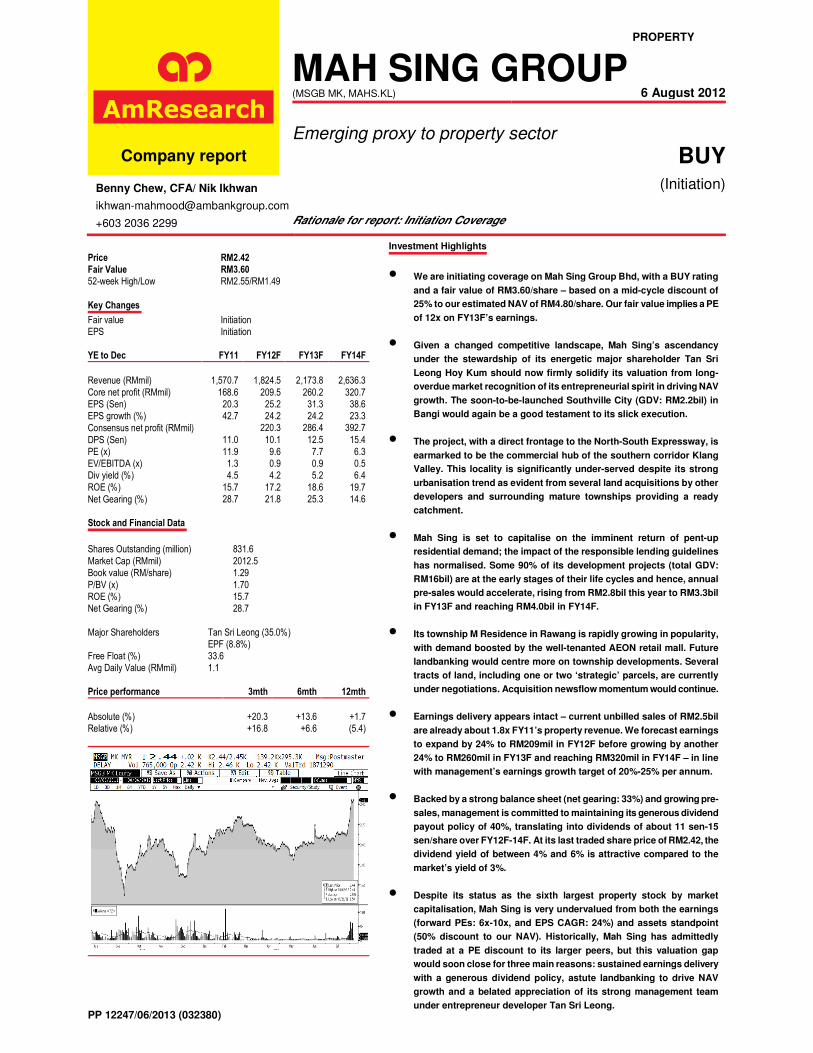

PROPERTY MAH SING GROUP (MSGB MK, MAHS.KL) 6 August 2012 Emerging proxy to property sector Company report BUY Benny Chew, CFA/ Nik Ikhwan [email protected] +603 2036 2299 (Initiation) Rationale for report: Initiation Coverage Price RM2.42 Fair Value RM3.60 52-week High/Low RM2.55/RM1.49 Key Changes Fair value Initiation EPS Initiation YE to Dec FY11 FY12F FY13F FY14F Revenue (RMmil) 1,570.7 1,824.5 2,173.8 2,636.3 Core net profit (RMmil) 168.6 209.5 260.2 320.7 EPS (Sen) 20.3 25.2 31.3 38.6 EPS growth (%) 42.7 24.2 24.2 23.3 Consensus net profit (RMmil) 220.3 286.4 392.7 DPS (Sen) 11.0 10.1 12.5 15.4 PE (x) 11.9 9.6 7.7 6.3 EV/EBITDA (x) 1.3 0.9 0.9 0.5 Div yield (%) 4.5 4.2 5.2 6.4 ROE (%) 15.7 17.2 18.6 19.7 Net Gearing (%) 28.7 21.8 25.3 14.6 Stock and Financial Data Shares Outstanding (million) 831.6 Market Cap (RMmil) 2012.5 Book value (RM/share) 1.29 P/BV (x) 1.70 ROE (%) 15.7 Net Gearing (%) 28.7 Major Shareholders Tan Sri Leong (35.0%) EPF (8.8%) Free Float (%) 33.6 Avg Daily Value (RMmil) 1.1 Price performance 3mth 6mth 12mth Absolute (%) +20.3 +13.6 +1.7 Relative (%) +16.8 +6.6 (5.4) PP 12247/06/2013 (032380) Investment Highlights • We are initiating coverage on Mah Sing Group Bhd, with a BUY rating and a fair value of RM3.60/share – based on a mid-cycle discount of 25% to our estimated NAV of RM4.80/share. Our fair value implies a PE of 12x on FY13F’s earnings. • Given a changed competitive landscape, Mah Sing’s ascendancy under the stewardship of its energetic major shareholder Tan Sri Leong Hoy Kum should now firmly solidify its valuation from long- overdue market recognition of its entrepreneurial spirit in driving NAV growth. The soon-to-be-launched Southville City (GDV: RM2.2bil) in Bangi would again be a good testament to its slick execution. • The project, with a direct frontage to the North-South Expressway, is earmarked to be the commercial hub of the southern corridor Klang Valley. This locality is significantly under-served despite its strong urbanisation trend as evident from several land acquisitions by other developers and surrounding mature townships providing a ready catchment. • Mah Sing is set to capitalise on the imminent return of pent-up residential demand; the impact of the responsible lending guidelines has normalised. Some 90% of its development projects (total GDV: RM16bil) are at the early stages of their life cycles and hence, annual pre-sales would accelerate, rising from RM2.8bil this year to RM3.3bil in FY13F and reaching RM4.0bil in FY14F. • Its township M Residence in Rawang is rapidly growing in popularity, with demand boosted by the well-tenanted AEON retail mall. Future landbanking would centre more on township developments. Several tracts of land, including one or two ‘strategic’ parcels, are currently under negotiations. Acquisition newsflow momentum would continue. • Earnings delivery appears intact – current unbilled sales of RM2.5bil are already about 1.8x FY11’s property revenue. We forecast earnings to expand by 24% to RM209mil in FY12F before growing by another 24% to RM260mil in FY13F and reaching RM320mil in FY14F – in line with management’s earnings growth target of 20%-25% per annum. • Backed by a strong balance sheet (net gearing: 33%) and growing pre- sales, management is committed to maintaining its generous dividend payout policy of 40%, translating into dividends of about 11 sen-15 sen/share over FY12F-14F. At its last traded share price of RM2.42, the dividend yield of between 4% and 6% is attractive compared to the market’s yield of 3%. • Despite its status as the sixth largest property stock by market capitalisation, Mah Sing is very undervalued from both the earnings (forward PEs: 6x-10x, and EPS CAGR: 24%) and assets standpoint (50% discount to our NAV). Historically, Mah Sing has admittedly traded at a PE discount to its larger peers, but this valuation gap would soon close for three main reasons: sustained earnings delivery with a generous dividend policy, astute landbanking to drive NAV growth and a belated appreciation of its strong management team under entrepreneur developer Tan Sri Leong.

-

Upload

hoangnguyet -

Category

Documents

-

view

213 -

download

0

Transcript of PROPERTY MAH SING GROUP - AmeSecurities Sing Group 1208… · PROPERTY MAH SING GROUP (MSGB MK,...

PROPERTY

MAH SING GROUP (MSGB MK, MAHS.KL) 6 August 2012

Emerging proxy to property sector

Company report BUY

Benny Chew, CFA/ Nik Ikhwan

+603 2036 2299

(Initiation)

Rationale for report: Initiation Coverage

Price RM2.42

Fair Value RM3.60

52-week High/Low RM2.55/RM1.49

Key Changes

Fair value Initiation

EPS Initiation

YE to Dec FY11 FY12F FY13F FY14F

Revenue (RMmil) 1,570.7 1,824.5 2,173.8 2,636.3

Core net profit (RMmil) 168.6 209.5 260.2 320.7

EPS (Sen) 20.3 25.2 31.3 38.6

EPS growth (%) 42.7 24.2 24.2 23.3

Consensus net profit (RMmil) 220.3 286.4 392.7

DPS (Sen) 11.0 10.1 12.5 15.4

PE (x) 11.9 9.6 7.7 6.3

EV/EBITDA (x) 1.3 0.9 0.9 0.5

Div yield (%) 4.5 4.2 5.2 6.4

ROE (%) 15.7 17.2 18.6 19.7

Net Gearing (%) 28.7 21.8 25.3 14.6

Stock and Financial Data

Shares Outstanding (million) 831.6

Market Cap (RMmil) 2012.5

Book value (RM/share) 1.29

P/BV (x) 1.70

ROE (%) 15.7

Net Gearing (%) 28.7

Major Shareholders Tan Sri Leong (35.0%)

EPF (8.8%)

Free Float (%) 33.6

Avg Daily Value (RMmil) 1.1

Price performance 3mth 6mth 12mth

Absolute (%) +20.3 +13.6 +1.7

Relative (%) +16.8 +6.6 (5.4)

PP 12247/06/2013 (032380)

Investment Highlights

• We are initiating coverage on Mah Sing Group Bhd, with a BUY rating

and a fair value of RM3.60/share – based on a mid-cycle discount of

25% to our estimated NAV of RM4.80/share. Our fair value implies a PE

of 12x on FY13F’s earnings.

• Given a changed competitive landscape, Mah Sing’s ascendancy

under the stewardship of its energetic major shareholder Tan Sri

Leong Hoy Kum should now firmly solidify its valuation from long-

overdue market recognition of its entrepreneurial spirit in driving NAV

growth. The soon-to-be-launched Southville City (GDV: RM2.2bil) in

Bangi would again be a good testament to its slick execution.

• The project, with a direct frontage to the North-South Expressway, is

earmarked to be the commercial hub of the southern corridor Klang

Valley. This locality is significantly under-served despite its strong

urbanisation trend as evident from several land acquisitions by other

developers and surrounding mature townships providing a ready

catchment.

• Mah Sing is set to capitalise on the imminent return of pent-up

residential demand; the impact of the responsible lending guidelines

has normalised. Some 90% of its development projects (total GDV:

RM16bil) are at the early stages of their life cycles and hence, annual

pre-sales would accelerate, rising from RM2.8bil this year to RM3.3bil

in FY13F and reaching RM4.0bil in FY14F.

• Its township M Residence in Rawang is rapidly growing in popularity,

with demand boosted by the well-tenanted AEON retail mall. Future

landbanking would centre more on township developments. Several

tracts of land, including one or two ‘strategic’ parcels, are currently

under negotiations. Acquisition newsflow momentum would continue.

• Earnings delivery appears intact – current unbilled sales of RM2.5bil

are already about 1.8x FY11’s property revenue. We forecast earnings

to expand by 24% to RM209mil in FY12F before growing by another

24% to RM260mil in FY13F and reaching RM320mil in FY14F – in line

with management’s earnings growth target of 20%-25% per annum.

• Backed by a strong balance sheet (net gearing: 33%) and growing pre-

sales, management is committed to maintaining its generous dividend

payout policy of 40%, translating into dividends of about 11 sen-15

sen/share over FY12F-14F. At its last traded share price of RM2.42, the

dividend yield of between 4% and 6% is attractive compared to the

market’s yield of 3%.

• Despite its status as the sixth largest property stock by market

capitalisation, Mah Sing is very undervalued from both the earnings

(forward PEs: 6x-10x, and EPS CAGR: 24%) and assets standpoint

(50% discount to our NAV). Historically, Mah Sing has admittedly

traded at a PE discount to its larger peers, but this valuation gap

would soon close for three main reasons: sustained earnings delivery

with a generous dividend policy, astute landbanking to drive NAV

growth and a belated appreciation of its strong management team

under entrepreneur developer Tan Sri Leong.

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 2

INITIATE WITH A BUY

� Tan Sri Leong’s stewardship drives Mah Sing

We are initiating coverage on Mah Sing Group Bhd,

with a BUY rating and a fair value of RM3.60/share –

based on a mid-cycle discount of 25% to our

estimated NAV of RM4.80/share. Our fair value

implies a PE of 12x on FY13F’s earnings.

Given a changed competitive landscape, Mah Sing’s

ascendancy under the stewardship of its energetic

major shareholder Tan Sri Leong Hoy Kum should

now firmly solidify its valuation from long-overdue

market recognition of its entrepreneurial spirit in

driving NAV growth. The soon-to-be-launched

Southville City (GDV: RM2.2bil) in Bangi would again

be a good testament to its slick execution.

Mah Sing is set to capitalise on the imminent return

of pent-up residential demand; the impact of the

responsible lending guidelines has normalised.

Some 90% of its development projects (total GDV:

RM16bil) are at the early stages of their life cycles

and hence, annual pre-sales would accelerate, rising

from RM2.8bil this year to RM3.3bil in FY13F, and

reaching RM4.0bil in FY14F.

Earnings delivery appears intact; current unbilled

sales of RM2.5bil are already about 1.8x FY11’s

revenue. We forecast earnings to expand by 24% to

RM209mil in FY12F before growing by another 24% to

RM260mil in FY13F and reaching RM320mil in FY14F

– in line with management’s earnings growth target

of 20%-25% pa.

Despite its status as the sixth largest property stock

by market capitalisation, Mah Sing is far

undervalued from both the earnings (forward PEs:

6x-10x, and EPS CAGR: 24%) and assets standpoint

(50% discount to our NAV).

Historically, Mah Sing has admittedly traded at a PE

discount to its larger peers, but this valuation gap

would soon close for three reasons: sustained

earnings delivery with a generous dividend policy,

astute landbanking to drive NAV growth and a

belated appreciation of its strong management team

under entrepreneur developer Tan Sri Leong.

� Fast turnaround model

Mah Sing started as a plastic manufacturer, but gradually

ventured into property development. The development of

an integrated industrial park in 1994 marked Mah Sing’s

foray into property development. The company then

made a rapid expansion into the Klang Valley from 2000

to 2006. Key developments included Aman Perdana,

Perdana Residence, One Legenda, Kemuning Residence

and Damansara Legenda.

Mah Sing is well known for its small, niche fast-

turnaround developments, as the group does not own a

single parcel of land bigger than 400 acres until the

recent acquisition of the Bangi land.

Evidently, this has worked very well whereby holding

costs are minimised and return on equity maximised.

Despite Mah Sing’s focus on landed residential

developments on bigger parcels of land, it would adopt a

similar concept whereby the objective is to quickly reach

a stage where its projects are self-financing.

� Property sector outlook

We have a contrarian OVERWEIGHT stance on the

property sector as we advocate investors to focus more on

cyclicals. Property companies are trading at steep 40%-

50% discounts to NAVs which are at trough levels and

property stocks are laggards.

We expect a return of pent-up demand to take place given

the normalisation of the impact of responsible lending

guidelines, continued urbanisation and several prolific

projects, including IJM Land’s Bandar Rimbayu, to kick-

start buying momentum.

Mah Sing is set to capitalise on the imminent return of

pent-up residential demand. Some 90% of its

development projects (total GDV: RM16bil) are at the

early stages of their life cycles and hence, annual pre-

sales would accelerate, rising from RM2.8bil this year

to RM3.3bil in FY13F, and reaching RM4.0bil in FY14F.

CHART 1: REMAINING GDV & UNBILLED SALES BY

GEOGRAPHY

RM 12,507 mil

69%

RM 1,308 mil

7%

RM 3,514 mil

19%

RM 830 mil

5%

Klang Valley (28 projects)

Johor (5 projects)

Penang (5 projects)

Sabah (1 project)

Source: Company / AmResearch

CHART 2: REMAINING GDV & UNBILLED SALES BY TYPE

RM 6,977 mil

38%

RM 692 mil

4%RM 403mil

2%

RM 4,398 mil

24%

RM 1,762 mil

10%

RM 3,927 mil

22%Commercial

Industrial

Legenda

Residence

Perdana

High-rise

Source: Company / AmResearch

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 3

ON TRACK TO ACHIEVE RM2.5BIL SALES

� Secures RM1bil in new sales up to Mid-May

Mah Sing has achieved RM1bil in new sales up to the

middle of May 2012, or accounting for 40% of its sales

target of RM2.5bil. In 1QFY12 alone, it sold RM676mil

worth of properties, or a 21% growth YoY. Key contributors

include: (1) Kinrara Residence, (2) M City, and (3) M

Residence 1

We believe Mah Sing is very much on track to meet its new

sales target of RM2.5bil this year. Together with the

already strong sales generated in the first five months,

Mah Sing has a slew of exciting launches in the pipeline

for the rest of the year.

Key launches and previews for 2HFY12F include: (1)

Southbay Plaza retail lots, (2) Feringghi Residence, (3)

iParc@PTP, (4) ongoing launches at

MResidence@Rawang, Icon City, Kinrara Residence,

MCity, Clover@ Garden Residence, and Garden Plaza, as

well as its bread-and-butter projects in Johor.

TO CONTINUE FOCUS ON AFFORDABLE

LANDED RESIDENTIAL PROPERTIES

Mah Sing is a market-driven developer and would

continue to focus on the mass market segment, i.e.

quality houses in a gated-and-guarded (G&G)

concept priced below RM1mil. The recent acquisition

of the sizeable tract of land in Bangi strengthens Mah

Sing’s position in this segment. Management has

guided that similar acquisitions could be in the

offing.

Including the other ongoing landed residential

projects, Mah Sing has in excess of RM2bil worth of

properties in this segment in the pipeline in the near

to medium term.

� Product segmentation heavy on commercial and high-rise, but Mah Sing is focusing more on landed products now

Mah Sing has an estimated remaining GDV of about

RM16bil – excluding its unbilled sales of RM2.5bil – which

is mostly made up of commercial projects within integrated

developments, accounting for 38% or about RM7bil. Key

developments include Icon City, Southbay City, Star

PICTURE 1: M RESIDENCE 1 & 2

Source: Company/ Google Maps

TABLE 1: LAUNCHES & PREVIEWS FROM 2HFY12F ONWARDS GDV

(RM mil)

iParc@Iskandar Johor 206 627 3Q12

Feringghi Residence Penang 61 800 3Q12

Southville City Greater KL 412 2,152 Register interest by 4Q12

M Residence 2 Greater KL 157 650 Early 2013

Sutera Avenue Sabah 8.7* *830 1H13

Icon Georgetown Penang 3 280 2013

Total 847.7 5,339

*Kindly note that the GDV figure is for the whole project, and launch will be in phases.

Project Name Location Size (acre) Preview / Launch Date

Source: Company

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 4

Avenue and Sutera Avenue.

Likewise about 22% of its future launches are high-rise

developments with a value of about RM3.9bil. Combining

these two product types, Mah Sing’s exposure is quite

significant at 60%.

Given this figure, we are not surprised that the

management does not intend to increase its exposure in

this type of development in the near to medium term.

Rather, focus will be on churning out landed residential

products priced within RM500k-RM700k, with M Residence

and Southville City as anchor projects.

Management has been proactive and sensitive to market

demand, focusing its property launches this year on

residential properties – 43% and 26% of its planned

launches will consist of landed and high-rise properties,

respectively. In fact, management has guided that similar

acquisitions to that of the Southville City land could be in

the offing in the Klang Valley, Penang and Johor Bahru.

ROLLING OUT WHAT THE MARKET WANTS

Its township M Residence in Rawang is rapidly

growing in popularity with demand boosted by the

well-tenanted AEON retail mall. Future landbanking

would centre more on township developments.

Several tracts of land, including one or two ‘strategic’

parcels, are currently under negotiations. Acquisition

newsflow momentum would continue.

� M Residence 1

This development sits on a 226-acre of freehold land, just

next to AP Land’s Tasik Puteri township. Phase 1 & 2A

comprises 282 units of double-storey link (214) and

double-storey superlink houses (68) with built-ups ranging

between1,650sf and 2,380sf.

The starting prices for the double-storey units are at

RM380k-RM420k per unit, while the superlink units are

tagged at an average RM500k.

Recall that Guocoland’s Emerald development – just about

8km away from the site – was selling similar units at

RM300k about a year ago.

So far, Mah Sing has launched about RM106mil worth of

properties comprising three phases, with RM81mill sales

having been achieved or at an average price of RM220psf.

We are not surprised that this development has been well

received, given that houses are priced within RM400k-

RM500k per unit for G&G concept.

This indicates that quality houses priced within affordable

price brackets would see solid demand, despite the

tightening in lending by financial institutions.

Secondly, there are a few key selling points that would

make Rawang a more vibrant area – especially with the

widening of the Batu Arang road, the opening of the 2nd

biggest Jusco retail mall in Malaysia (just 3km from

MResidence), while accessibility has improved due to the

recently-opened Latar Highway.

Buoyed by the strong demand, the group is now testing the

market with a preview of its semi-D units with a 40x80 land

area and a built-up of 3,000sf. From our ground checks,

there will be 68 units on offer and they would be selling

starting at RM918k each. Interests have been decent with

18% registrants and some of the units are now being sold

at as high as RM970k.

� M Residence 2@ Rawang

Mah Sing will introduce the sequel to M Residence to the

market by 1H2013F although the details – number of units,

GDV and pricing - have yet to be finalised. Recall this

PICTURE 2: LOCATION OF SOUTHVILLE CITY

Source: Company / Google Maps

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 5

development would have a GDV of RM650mil in total.

Judging by the success of M Residence 1, we are

expecting end-demand to continue to be strong for M

Residence 2, despite having a leasehold status. As we

have highlighted above, there are a few catalysts to make

Rawang a more vibrant place.

SOUTHVILLE CITY

Given a changed competitive landscape, Mah Sing’s

ascendancy under the stewardship of its energetic

major shareholder Tan Sri Leong should now firmly

solidify its valuation from long-overdue market

recognition of its entrepreneurial spirit in driving

NAV growth. The soon-to-be-launched Southville City

(GDV: RM2.2bil) in Bangi would again be a good

testament to its slick execution.

The said project, with direct frontage to the North-

South Expressway, is earmarked to be the

commercial hub of the southern corridor Klang

Valley.

This locality is significantly under-served despite its

strong urbanisation trend as evident from several

land acquisitions by other developers and

surrounding mature townships providing a ready

catchment.

� Replicating M Residence in Bangi

Encouraged by the strong demand for landed residential

properties, the group plans to replicate its M Residence

G&G scheme in Bangi with a starting price of

RM500K/unit. The first phase is slated for launch by

1HFY13F.

The site is located along the North South Highway within

Mukim of Kajang and Dengkil, or to be more exact, in

between Bandar Baru Bangi and Bandar Seri Putra – the

two nearest residential areas with about 20,000 to 30,000

residents each.

Over the years, Bangi has become one of the new

hotspots for residential enclaves and is maturing well –

aided by the emergence of several universities and rapid

urbanisation.

Bangi is also just a 30minutes’ drive from Kuala Lumpur,

served by several highways, namely North-South Highway

and the Kajang-Seremban Highway (LEKAS).

In fact, Mah Sing plans to build a new interchange at the

North South Highway – just 2.5km from the Bangi

interchange - which would allow direct access into the

township.

� Southville City to change Bangi

Southville City would largely comprise landed residential

units including linkhouses – with 30% of the GDV to be

allocated for units priced at below RM1mil - and semi-Ds

with 30% of the landbank to be allocated for commercial

properties i.e. cluster shop offices, boutique corporate

offices and a lifestyle mall.

The group is targeting the upgraders and new buyers from

Bangi and surrounding townships of Kajang, Putrajaya,

Cyberjaya, Nilai and Seremban, which boast a population

catchment of 1.2 million people.

We understand that the group plans to develop a retail

mall with a GFA of 350,000sf to 500,000sf within Southville

City, tapping on the under-served market within the area.

To recap, the few prominent shopping malls within the

area are the Alamanda Mall in Putrajaya and the Mines

Shopping Centre – both about 15 minutes’ drive away. We

expect Mah Sing to monetise the retail mall once it has

reached maturity stage, for which interest in well-located

malls continue to be strong especially with the growing

number of retail REITs listed on Bursa Malaysia.

On the flipside, based on our estimates, Mah Sing would

be able to yield 18% to 26% margins from this

development. This is based on a plot ratio of 4x, efficiency

ratio of 70%, construction cost of RM150psf and an

average selling price of RM270psf to RM300psf.

We forecast sales from this development to grow from

RM60mil in the first year to RM118mil in the second year

and on average at RM280mil per annum in sales for the

remaining useful life of the landbank.

AGGRESSIVE IN LANDBANKING

� Has reached 73% of its RM5bil GDV renewal target for FY2012F

Mah Sing has been one of the most active property

developers in land acquisitions, given over RM1bil worth of

land bought over the past four years with circa RM11bil in

GDV. (See Table above)

This year is no different. The group has secured three

parcels of land, which will yield a total GDV of RM3.63bil or

accounting for 73% of its 2012 GDV replenishment target

of RM5bil.

CHART 3: AGGRESSIVE LANDBANKING BY MAH SING

0

1000

2000

3000

4000

5000

6000

0

100

200

300

400

500

600

700

800

2000 2003 2004 2005 2006 2007 2008 2009 2010 2011 May-12

Cost (RM mil) - LHS

GDV (RM mil) - RHS

Source: Company / AmResearch

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 6

� Sutera Avenue

Mah Sing kicked off the year with the acquisition of a 4.26

acre-piece of commercial land along the coastal highway

in Kota Kinabalu for RM39mil or RM210psf.

Mah Sing is also entitled to exercise an option for another

4.41 acres of an adjacent site at an entitlement price of

RM216psf or circa RM41.5mil within six months of this

agreement.

A leasehold land with a tenure of 99 years, the land would

be jointly developed with the vendor, Paduan Hebat, with a

GDV of RM830mil –RM360mil for the first 4.26 acres and

RM470mil for the second piece of land.

The site is located diagonally opposite the 5-star Sutera

Harbour Resort and KK Times Square, and has direct road

frontage to the Coastal Highway. The land is also situated

close to the Ming Garden Hotel and Asia City.

We understand the development concept would be similar

to Icon City’s 30 Jewels and Gourmet Street Shops. The

development would comprise multi-storey shop offices and

complemented by street mall retail lots as well as serviced

apartments.

� M Residence 2@ Rawang

Mah Sing announced in March that it was acquiring two

parcels of land in Rawang measuring about 157acres for

RM40.9mil or RM6psf. This development would have a

GDV of RM650mil comprising landed residential

properties.

The land cost is cheaper by 33% – on a psf basis – despite

being located just 1km south of Mah Sing’s maiden project

in Rawang, i.e. M Residence given that the former has a

leasehold tenure.

Judging by the success of the phase 1, we are expecting

end-demand to continue to be strong. As we have

highlighted, there are a few catalysts to make Rawang a

more vibrant area.

These include the widening of the Batu Arang road, the

opening of the 2nd

biggest Jusco retail mall in Malaysia

(just 3km from MResidence), while accessibility has

improved due to the recently-opened Latar Highway.

� Southville City

Mah Sing acquired a 412-acre piece of mostly freehold

land in Bangi for RM333.2mil or RM18.55psf in 2Q2012,

which would be for the biggest township development so

far for the company.

Encouraged by the strong demand for landed residential

properties, the group plans to replicate its M Residence

scheme in Bangi with a starting price of RM500k/unit.

This development would have a GDV of RM2.15bil and the

first phase is slated for launch by 1QFY13F.

CONCERNS OVER ICON CITY MAY BE

OVERPLAYED

� Icon City is the new Icon for PJ

One of the key projects for Mah Sing is The Icon City,

located on a 20-acre leasehold site at the junction of the

Federal Highway and the Damansara-Puchong Highway

(LDP).

This project has a GDV of RM3.5bil over a seven-year

development period. In line with market trend, Icon City is

planned to be an integrated commercial development

comprising:- (i) Lifestyle shop offices, (ii) SOVO units, (iii)

1-2 storey retail shops, and (iv) serviced apartments.

Given the concerns about heavy traffic, Mah Sing will be

building ramps and underpasses as part of Icon City’s

infrastructure development.

� But largely commercial

Concerns over take-ups for Icon City began to emerge

once the 70% LTV ruling was introduced into the market.

This was particularly so given that the commercial property

segment is dominated by investors and speculators. As a

whole, take-up has been decent; out of the RM795mil

launched, Mah Sing has sold RM532mil worth of

properties or at a take-up rate of 67%.

While the bigger units or the lifestyle shop offices have

been largely sold (96% sold), reception for the remaining

retail shops units has been mixed, where retail shops has

a take-up of 50% (of value terms). Meanwhile the SOVO

units and serviced apartments have seen 70% take-up

rates.

Following the cancellation of a proposed partnership with a

Thai company, Mah Sing is not in a hurry to look for a new

partner in the development and the management of a retail

mall in Icon City.

� But continued subdued take-up for Icon Residence, Mon’t Kiara is expected

Given the demand saturation for high-rise residential units

in Mon’t Kiara, and exacerbated by the steep pricing of

RM1,000psf-RM1,200psf, we are not surprised that

response for Icon Residence (GDV:RM471mil) has been

rather lacklustre. We understand Tower 1 has seen a 65%

take-up rate, while Tower 2 has only seen 20% of the units

sold.

On top of that, Mah Sing has recently terminated a

RM220mil enbloc sale, comprising 96 units, to a Chinese

party. This is the result of default in payments to

subcontractors by the Chinese party.

As a consequence of this, the group has decided to re-look

its plans for the third tower.

� M City is well located, hence selling well

M City (GDV: RM1.4bil) is an integrated commercial

development, located in Ampang, not too far from

embassy row.

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 7

Mah Sing is expecting over RM418mil sales from this

development alone for FY12F. The group is well on track,

having achieved 61% or RM253mil of its sales target as

at the middle of May.

The group has so far launched only four blocks, out of five.

Response has been encouraging, with 302 units having

been sold out of 380 units on offer, or at a 79% take-up

overall.

FINANCIALS

We estimate Mah Sing’s earnings to rise from

RM169mil in FY11 to RM209mil in FY12F, RM260mil in

FY13F and RM320mil in FY14F, with a three-year

earnings CAGR of 24% anchored by in-demand

landed residential developments – M Residence 1 & 2

and Southville City.

The group’s earnings are very much secured with

current unbilled sales of RM2.5bil (1.8x FY11

turnover). Annual pre-sales are expected to rise to

RM3.5bil in FY13F and to RM4bil in FY14F. Net

gearing is expected to rise to 0.5x with one or two

more land acquisitions by the end of the year, but

this is still within a comfortable level and should be

pared down by its solid cashflows.

Mah Sing has a dividend payout policy of 40%. We

estimate Mah Sing to pay 11.0 sen/share-15sen/share

for FY12F-FY14F translating to decent yields of 4%-

6%.

TABLE 2: MAH SING AT EARLY GROWTH STAGE

Current Classification of Life Cycle Stage Remaining GDV + Unbilled Sales (RM mil) As a % of remaining GDV and unbilled sales

Matured 81-100% of GDV billed 296 2%

Growth 11-80% of GDV billed 2243 12%

Infant Ready to launch to 10% of GDV billed 5644 31%

Planning Acquisition date to ready to launch 9976 55%

18,159 100%

Source: Company / AmResearch

CHART 4: DIVIDEND PAYOUT

69

25 26

42

46

4143

40 41

0

5

10

15

20

25

30

35

40

45

50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Dividend Payout Ratio (%)

Source: Company / AmResearch

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 8

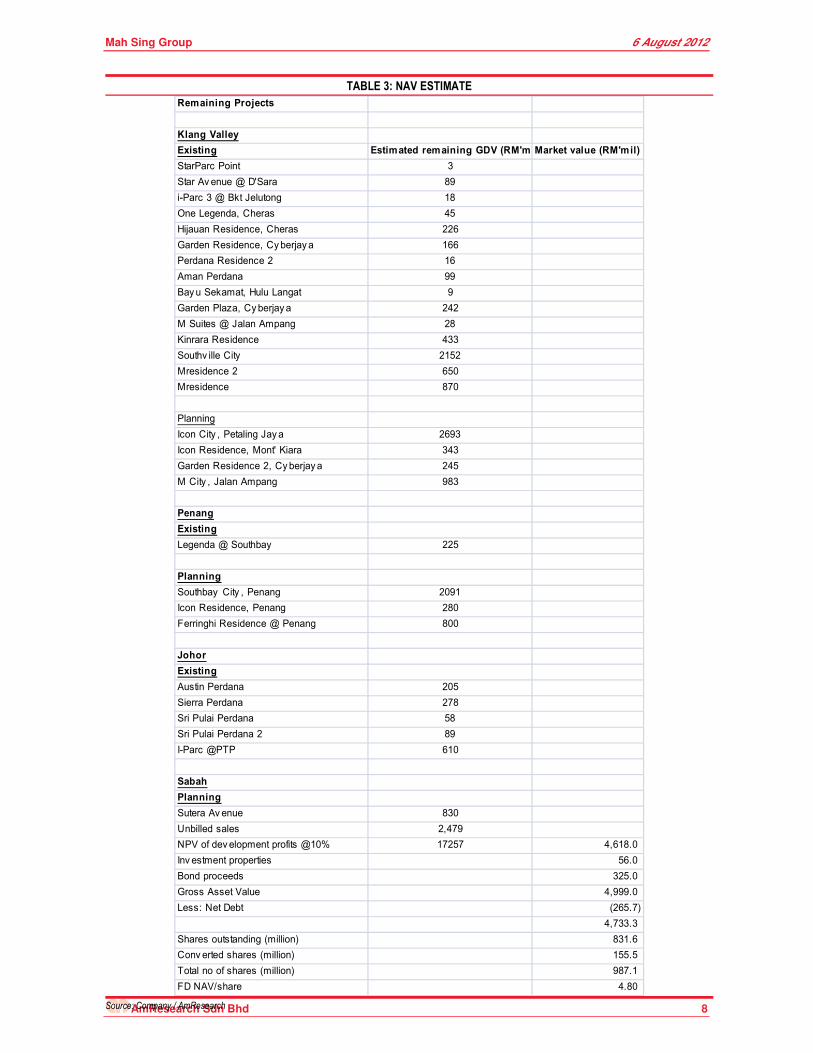

TABLE 3: NAV ESTIMATE

Remaining Projects

Klang Valley

Existing Estimated remaining GDV (RM'mil)Market value (RM'mil)

StarParc Point 3

Star Av enue @ D'Sara 89

i-Parc 3 @ Bkt Jelutong 18

One Legenda, Cheras 45

Hijauan Residence, Cheras 226

Garden Residence, Cyberjay a 166

Perdana Residence 2 16

Aman Perdana 99

Bayu Sekamat, Hulu Langat 9

Garden Plaza, Cyberjay a 242

M Suites @ Jalan Ampang 28

Kinrara Residence 433

Southv ille City 2152

Mresidence 2 650

Mresidence 870

Planning

Icon City , Petaling Jay a 2693

Icon Residence, Mont' Kiara 343

Garden Residence 2, Cyberjay a 245

M City , Jalan Ampang 983

Penang

Existing

Legenda @ Southbay 225

Planning

Southbay City , Penang 2091

Icon Residence, Penang 280

Ferringhi Residence @ Penang 800

Johor

Existing

Austin Perdana 205

Sierra Perdana 278

Sri Pulai Perdana 58

Sri Pulai Perdana 2 89

I-Parc @PTP 610

Sabah

Planning

Sutera Av enue 830

Unbilled sales 2,479

NPV of dev elopment profits @10% 17257 4,618.0

Inv estment properties 56.0

Bond proceeds 325.0

Gross Asset Value 4,999.0

Less: Net Debt (265.7)

4,733.3

Shares outstanding (million) 831.6

Conv erted shares (million) 155.5

Total no of shares (million) 987.1

FD NAV/share 4.80

Source: Company / AmResearch

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 9

TABLE 4: MAH SING AT EARLY GROWTH STAGE

Price Market Capitalisation Estimated Remaining GDV P/E (x)

Developer (RM/share) (RM'mil) (RM'mil) FY12F FY13F

UEM Land 1.95 8439.0 40000 24.4 21.7

SP Setia 3.59 7207.6 78000 15.4 12.8

KLCC Property 5.48 5118.9 n/a 18.9 16.6

IGB Corporation 2.72 4053.9 3200 18.3 17.4

IJM Land 2.45 3432.2 20000 14.3 10.2

Mah Sing 2.42 2012.5 17000 9.6 7.7 Source: Company / AmResearch

TABLE 5: PROPERTY SNAPSHOT

Stock Rating Price Fair value EPS (sen) PE (x) Yield (%) NAV/share Premium/

(RM/share) (RM/share) FY12F FY12F FY12F (RM) (discount) to NAV

IJM Land* BUY 2.45 3.80 17.1 14.3 1.4 4.20 (41.7)

SP Setia HOLD 3.59 3.95 23.3 15.4 4.7 5.41 (33.6)

IGB Corp BUY 2.72 3.50 13.4 20.3 2.8 4.54 (40.1)

Mah Sing BUY 2.42 3.60 25.2 9.6 4.2 4.80 (49.6)

BRDB HOLD 2.66 2.30 12.7 20.9 1.2 3.70 (28.1)

Sunway Bhd HOLD 2.30 2.60 26.6 8.6 2.3 3.50 (34.3)

CMMT HOLD 1.73 1.68 8.7 19.9 4.9 1.11 55.9

Pav ilion REIT HOLD 1.34 1.33 6.2 21.6 4.9 0.96 39.6

Al Aqar HOLD 1.44 1.39 11.2 12.9 5.4 1.26 14.3

*EPS, PE & Yield are for FY13F -35.6

Source: Company / AmResearch

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 10

TABLE 6: FINANCIAL DATA

Income Statement (RMmil, YE 31 Dec) FY10 FY11 FY12F FY13F FY14F

Revenue 1,110.1 1,570.7 1,824.5 2,173.8 2,636.3

EBITDA 188.1 244.7 308.4 382.7 472.5

Depreciation (11.4) (11.4) (15.6) (19.5) (23.0)

Operating income (EBIT) 176.4 231.5 291.1 361.4 447.7

Other income & associates 0.0 0.0 0.0 0.0 0.0

Net interest (2.6) (3.0) (3.5) (3.0) (3.7)

Exceptional items 2.0 3.0 4.0 5.0 6.0

Pretax profit 177.9 238.6 296.5 368.3 453.9

Taxation (49.5) (70.0) (87.0) (108.0) (133.1)

Minorities/pref dividends (10.3) (0.1) (0.1) (0.1) (0.1)

Net profit 118.1 168.6 209.5 260.2 320.7

Core net profit 118.1 168.6 209.5 260.2 320.7

Balance Sheet (RMmil, YE 31 Dec) FY10 FY11 FY12F FY13F FY14F

Fixed assets 66.1 85.3 119.8 150.2 177.2

Intangible assets 0.0 0.0 0.0 0.0 0.0

Other long-term assets 72.9 102.2 116.6 129.5 149.4

Total non-current assets 139.0 187.5 236.3 279.8 326.6

Cash & equivalent 308.6 665.7 598.3 659.8 665.7

Stock 33.2 43.8 41.5 49.1 59.3

Trade debtors 426.1 355.6 400.2 431.8 465.4

Other current assets 1,200.2 1,541.6 2,079.3 2,597.7 3,116.1

Total current assets 1,968.1 2,606.7 3,119.3 3,738.4 4,306.5

Trade creditors 670.9 736.2 954.1 1,127.1 1,361.7

Short-term borrowings 134.8 39.2 29.2 79.2 69.2

Other current liabilities 21.1 32.4 260.1 180.3 550.2

Total current liabilities 826.7 807.8 1,243.4 1,386.6 1,981.1

Long-term borrowings 368.5 934.8 834.8 934.8 834.8

Other long-term liabilities 6.0 19.3 104.1 347.3 250.0

Total long-term liabilities 374.6 954.1 938.9 1,282.1 1,084.8

Shareholders’ funds 918.9 1,073.2 1,219.8 1,402.0 1,626.5

Minority interests 17.6 15.3 15.3 15.3 15.3

BV/share (RM) 1.1 1.3 1.5 1.7 2.0

Cash Flow (RMmil, YE 31 Dec) FY10 FY11 FY12F FY13F FY14F

Pretax profit 177.9 238.6 296.5 368.3 453.9

Depreciation 11.4 11.4 15.6 19.5 23.0

Net change in working capital (431.9) (218.0) (175.4) (133.9) (190.8)

Others (59.9) (69.4) (117.7) (92.7) (178.6)

Cash flow from operations (302.5) (37.4) 19.0 161.3 107.6

Capital expenditure (18.1) (41.5) (50.0) (50.0) (50.0)

Net investments & sale of fixed assets 0.1 0.8 0.8 0.8 0.8

Others (1.4) (7.4) (5.0) (5.2) (5.3)

Cash flow from investing (19.3) (48.1) (54.2) (54.4) (54.5)

Debt raised/(repaid) 286.1 197.3 50.0 50.0 50.0

Equity raised/(repaid) 0.0 290.0 0.0 0.0 0.0

Dividends paid (40.5) (50.1) (65.7) (70.4) (87.1)

Others (23.1) 28.0 15.0 (25.0) (10.0)

Cash flow from financing 222.5 465.2 (0.7) (45.4) (47.1)

Net cash flow (99.3) 379.7 (35.9) 61.5 6.0

Net cash/(debt) b/f 356.6 246.5 634.2 598.3 659.8

Net cash/(debt) c/f 246.5 634.2 598.3 659.8 665.7

Key Ratios (YE 31 Dec) FY10 FY11 FY12F FY13F FY14F

Revenue growth (%) 58.2 41.5 16.2 19.1 21.3

EBITDA growth (%) 20.1 30.1 26.0 24.1 23.5

Pretax margins (%) 16.0 15.2 16.3 16.9 17.2

Net profit margins (%) 10.6 10.7 11.5 12.0 12.2

Interest cover (x) 67.0 76.2 82.5 121.4 120.1

Effective tax rate (%) 27.8 29.3 29.3 29.3 29.3

Net dividend payout (%) 40.0 41.0 40.0 40.0 40.0

Debtors turnover (days) 120 105 90 80 70

Stock turnover (days) 12 11 10 10 10

Creditors turnover (days) 502 657 580 580 580

Source: Company, AmResearch estimates

Mah Sing Group 6 August 2012

AmResearch Sdn Bhd 11

Anchor point for disclaimer text box

Published by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

Printed by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

The information and opinions in this report were prepared by AmResearch Sdn Bhd. The investments discussed or recommended in this report may not be suitable for all investors. This report has been prepared for information purposes only and is not an offer to sell or a solicitation to buy any securities. The directors and employees of AmResearch Sdn Bhd may from time to time have a position in or with the securities mentioned herein. Members of the AmInvestment Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein. The information herein was obtained or derived from sources that we believe are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. No liability can be accepted for any loss that may arise from the use of this report. All opinions and estimates included in this report constitute our judgement as of this date and are subject to change without notice.

For AmResearch Sdn Bhd

Benny Chew Managing Director