Prompt Oil Price ($/bbl) $56.96 $2.55 4.7% Prompt Gas ... · leaking in early February. No...

17

1 February 25, 2019 Indicator Current Value Week's Change % Change Direction Prompt Oil Price ($/bbl) $56.96 $2.55 4.7% Prompt Gas Price ($/mmbtu) $2.70 $0.13 4.9% Wkly Trans. Value ($mm) $283 $272 nmf Wkly Trans. Count 4 3 300% US Rig Count 1,047 (4) (0.4%) US Oil Prod'n (mmbbl/d) 12.0 0.1 0.8% US Gas Prod'n (bcf/d) (1) 107.4 -- -- US Oil Storage (mmbbl) 454.5 3.7 0.8% US Gas Storage (tcf) 1.7 (0.2) (9.4%) $2.2 $8.0 $9.9 $10.7 $4.9 $15.8 $21.2 $21.9 $24.1 $17.0 $9.1 $9.2 $20.8 $8.0 $31.6 $19.2 $0.6 -- 50 100 150 200 250 300 350 400 450 500 -- $5 $10 $15 $20 $25 $30 $35 $40 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 61% 83% 74% 79% 39% 52% 62% 71% 93% 24% 68% 82% 91% 64% 46% 93% 78% Number of Transactions Transaction Value ($bn) Asset Corporate Number of Transactions % Oil Debt Markets Five issuers priced five tranches for $3.9 billion in proceeds Year-to-date U.S. volume is down 7% year-on-year U.S. high yield funds reported an inflow of $284 million ETFs reported an inflow of $55.1 million, while mutual funds reported an inflow of $228.8 million High yield index yield was 6.67%; high yield energy index yield was 7.90% Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, EIA, PLS Note: Current quarter’s data is through the week covered by this issue. 1. EIA U.S. natural gas gross withdrawals and production reported monthly as of November 2018. 2. S&P E&P = S&P Oil & Gas E&P Select Industry, SPX = S&P 500 Index. Key Industry Indicators Quarterly Deal Activity S&P E&P (2) underperformed last week 0.4% vs. SPX (2) 1.1% The major U.S. equity indexes finished higher last week. Consumer discretionary, consumer staples, financials, health care, industrials, materials, real estate, and tech finished higher. Materials performed the best, up 3.3% Equity Markets Oil ended last week up. TransCanada restarted the Nebraska-Illinois portion of Keystone that started leaking in early February. No indication yet of when full flow rates will be able to resume. Alberta announced its crude-by-rail (“CBR”) plan, whereby Alberta plans to lease 4,400 rail cars and reach 120kbpd of CBR capacity in roughly three years. Crude oil imports and exports increased. The near-term contract closed up $2.55, or 4.7%, at $56.96 Natural gas ended last week up. Western basis was extremely volatile as the market traded around recent headlines for summer maintenance on Westcoast pipeline, which drove basis higher. Additionally, warmer weather is expected in the summer for the West Coast. Weather forecasts for early March were more bullish than expectations. The near-term contract closed up $0.13, or 4.9%, at $2.70 Commodities Week in Review Covering the Week of February 15 to February 21, 2019 Mid-Con Energy Partners sold substantially all of its Texas properties for $60 million to Scout Energy Group IV Scout Energy Management sold producing properties in Caddo, Grady, and Osage counties, OK for $27.5 million to Mid-Con Energy Partners QEP Resources announced a review of strategic alternatives. BMO and Evercore are acting as financial advisors BMO is marketing Juno’s divestiture of Permian Basin assets in Crosby and Lubbock counties, TX (see page 4) BMO is also marketing Rio Oil & Gas’ divestiture of Midland Basin assets in Glasscock County, TX (see page 5) All references to last week in the comments below are through Thursday

Transcript of Prompt Oil Price ($/bbl) $56.96 $2.55 4.7% Prompt Gas ... · leaking in early February. No...

1

February 25, 2019

IndicatorCurrent

Value

Week's

Change

%

Change Direction

Prompt Oil Price ($/bbl) $56.96 $2.55 4.7%

Prompt Gas Price ($/mmbtu) $2.70 $0.13 4.9%

Wkly Trans. Value ($mm) $283 $272 nmf

Wkly Trans. Count 4 3 300%

US Rig Count 1,047 (4) (0.4%)

US Oil Prod'n (mmbbl/d) 12.0 0.1 0.8%

US Gas Prod'n (bcf/d)(1) 107.4 -- --

US Oil Storage (mmbbl) 454.5 3.7 0.8%

US Gas Storage (tcf) 1.7 (0.2) (9.4%)

$2.2

$8.0

$9.9 $10.7

$4.9

$15.8

$21.2 $21.9 $24.1

$17.0

$9.1 $9.2

$20.8

$8.0

$31.6

$19.2

$0.6

--

50

100

150

200

250

300

350

400

450

500

--

$5

$10

$15

$20

$25

$30

$35

$40

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19

61% 83% 74% 79% 39% 52% 62% 71% 93% 24% 68% 82% 91% 64% 46% 93% 78%

Nu

mb

er

of

Tra

ns

acti

on

s

Tra

ns

acti

on

Valu

e (

$b

n)

Asset Corporate Number of Transactions

% Oil

Debt

Markets

Five issuers priced five tranches for $3.9 billion in proceeds

Year-to-date U.S. volume is down 7% year-on-year

U.S. high yield funds reported an inflow of $284 million

ETFs reported an inflow of $55.1 million, while mutual funds reported an inflow of $228.8 million

High yield index yield was 6.67%; high yield energy index yield was 7.90%

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, EIA, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. EIA U.S. natural gas gross withdrawals and production reported monthly as of November 2018.

2. S&P E&P = S&P Oil & Gas E&P Select Industry, SPX = S&P 500 Index.

Key Industry Indicators

Quarterly Deal Activity

S&P E&P(2) underperformed last week 0.4% vs. SPX(2) 1.1%

The major U.S. equity indexes finished higher last week. Consumer discretionary, consumer staples,

financials, health care, industrials, materials, real estate, and tech finished higher. Materials performed

the best, up 3.3%

Equity

Markets

Oil ended last week up. TransCanada restarted the Nebraska-Illinois portion of Keystone that started

leaking in early February. No indication yet of when full flow rates will be able to resume. Alberta

announced its crude-by-rail (“CBR”) plan, whereby Alberta plans to lease 4,400 rail cars and reach

120kbpd of CBR capacity in roughly three years. Crude oil imports and exports increased. The near-term

contract closed up $2.55, or 4.7%, at $56.96

Natural gas ended last week up. Western basis was extremely volatile as the market traded around

recent headlines for summer maintenance on Westcoast pipeline, which drove basis higher. Additionally,

warmer weather is expected in the summer for the West Coast. Weather forecasts for early March were

more bullish than expectations. The near-term contract closed up $0.13, or 4.9%, at $2.70

Commodities

Week in Review

In Commodities, ECM and DCM, let’s go to journalism standards, even

though that’s not how we get the text from those groups. Main change is

that any number below 10 is spelled out (one instead of 1). This does not

apply to statistical analyses, percentages, or money, of course.

Let’s follow these guidelines when sorting articles:

• First priority: Domestic A&D, ranked by size

• Next: Domestic M&A

• Then: US companies doing international deals (like

Noble’s Tamar)

• Then: Others (Cabot’s Lackawanna)

• Then: Prices, rig count, completions, etc.

To paste the arrows with colors,

• FactSet

• Settings

• Presentation Linking and Formatting

• Import

• Colors

• Change Color Font

For the primary Commodities bullet points on oil and gas

prices, please start with “The near-term contract opened the

week at $___” and end that same bullet point with “The

near-term contract closed the week at $____, down(up)

$___, or ___%.” You don’t have to use exactly those words

as long as the opening and closing prices are included . For

example, you could write, “Opening the week at $45.21, the

near-term oil contract declined steadily based on …” – you

know, think like a journalist, be creative.

Covering the Week of February 15 to February 21, 2019

The October issue of BMO Calgary’s A&D (Canadian)

Market Monitor went live last week – read more here

[TBU]

[TBU]

[TBU]

[TBU]

[TBU] [TBU]

This is the final issue for 2018. The Market Monitor will

return on Monday, January 7th. Happy Holidays from the

BMO Capital Markets team!

Mid-Con Energy Partners sold substantially all of

its Texas properties for $60 million to Scout Energy Group IV

Scout Energy Management sold producing properties

in Caddo, Grady, and Osage counties, OK for $27.5 million to

Mid-Con Energy Partners

QEP Resources announced a review of strategic alternatives.

BMO and Evercore are acting as financial advisors

BMO is marketing Juno’s divestiture of Permian Basin assets

in Crosby and Lubbock counties, TX (see page 4)

BMO is also marketing Rio Oil & Gas’ divestiture of Midland

Basin assets in Glasscock County, TX (see page 5)

All references to last week in the comments below are through Thursday

2

February 25, 2019

Ann'd

Date Buyer Seller Area Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)

19-Feb-19 Scout Energy Partners Mid-Con Energy Partners Other North Texas assets $60 $8.22 n.a. n.a.

19-Feb-19 Mid-Con Energy Partners Scout Energy Partners Mid-Continent Caddo, Grady, and Osage cos., OK $28 n.a. $20,960 n.a.

19-Feb-19 Undisclosed Buyer Noble Energy Permian Non-core acreage in the Delaware Basin $63 n.a. n.a. n.a.

19-Feb-19 Undisclosed Buyer Noble Energy Permian 13,000 net acres in Reeves Co., TX $132 n.a. n.a. $10,154

14-Feb-19 Undisclosed Buyer Harvest Oil & Gas Corp Other Rockies San Juan Basin assets $43 $1.57 $10,835 n.a.

07-Feb-19 Kimbell Royalty Partners EnCap Investments LP Multi-Region 12,200 net royalty acres across the U.S. $151 n.a. $94,563 nmf

16-Jan-19 Talos Energy Inc Samson Energy Co LLC Gulf of Mexico Non-op Gulf of Mexico working interest $30 $13.45 $17,939 n.a.

08-Jan-19 Undisclosed Buyer MCM Energy Partners LLC Permian Midland Basin assets $20 n.a. n.a. n.a.

21-Dec-18 Pantheon Resources Plc Great Bear Petroleum LLC Alaska 250,000 leased acres in the North Slope $49 n.a. n.a. $196

19-Dec-18 Comstock Shelby Shale LLC Ark-La-Tex 6,023 net acres in Haynesville $21 n.a. n.a. $3,404

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

y = 34.083e-0.07x

R² = 0.3524

--

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

-- 5.0x 10.0x 15.0x 20.0x 25.0x 30.0x

Sale

s P

rice /

Pro

ved

R

eserv

es (

$/b

oe @

15:1

)

R / P

R / P

Sales Value /

Proved Reserves

(15:1)

(ratio) ($ / boe) ($ / mcfe)

8x $19.47 $1.30

10x $16.92 $1.13

15x $11.93 $0.80

20x $8.40 $0.56

Oil70%

Gas30%

LTM By Commodity

Permian39%

Rockies (ex. Bakken)

9%

Bakken5%

Appalachia2%

Mid-Con16%

Eagle Ford6%

Ark-La-Tex4%

Gulf of Mexico3%

Other17%

LTM By Region

Public Company

35%

PE / PE-Backed

26%

Private21%

Other18%

LTM By Buyer Type

The 10 Most Recent Asset Transactions Over $20 Million

A&D Valuation Trends(3)

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, PLS

1. Represents total enterprise value.

2. Calculated as percentage of total LTM transaction count (number of transactions, not dollar value).

3. 62 transactions from January 2015 to 2019 with transaction value >$20mm. Adjusted for changes in price outlooks. Recalculated boe reserves are on a 15:1

(gas:oil) basis. Acreage transactions excluded by using deals with PDP of >= 40% of total proved.

Asset descriptions are all hard-coded and need to be

adjusted if new deals are added

(2) (2) (2)

Confirm number of transactions weekly --->

[TBU]

[TBU]

[TBU]

3

February 25, 2019

2/21/2019

Appalachia 2

Ark-La-Tex 9

Bakken 6

Eagle Ford 5

Mid-Con 9

Other 18

Permian 22

Rockies 3

74

Select Significant Deals on the Market

Disclaimer: The foregoing links are for convenience only and relate to materials that were not prepared or reviewed by BMO Capital Markets. BMO Capital Markets takes

no responsibility for and makes no representations with respect to the contents thereof. These materials may be inconsistent with the views of BMO Capital Markets.

Source of Select Significant Deals on the Market: BMO Transaction Database

Industry Headlines

Appalachia

2 Deals

Mid-Con

9 Deals

Eagle Ford

5 Deals

Permian

22 Deals

Other

18 Deals

Rockies

3 Deals

(Click headline to link to the full article)

A&D Headlines

Bakken

6 Deals

Ark-La-Tex

9 Deals

BMO Deals (Status)

Juno Permian (In Market) – See page 4

Rio Glasscock County (In Market) – See page 5

As Westchester Clamors For Gas, ConEd Wants

Others to Cut Back

Natural Gas Moratoriums Around State Due to Lack of

Pipelines

U.S. Shale Boom Keeps Rolling Even as Wildcatters

Save Cash

California's Dirty Oil Gets Pricey Amid Venezuela

Sanctions

The OPEC+ Oil Deal Is Standing on One Wobbly Leg

Permian-Fueled Shale Boom Shows Little Sign of

Abating, Even With Capital Spending Cuts

Official Says Northern Access Pipeline Progress

Would Mean Local Jobs

Oil And Gas Investors Tell Producers to Focus on

Returns, Not Endless Growth

Mid-Con Energy Partners, LP Announces Strategic

Transaction Strengthening Balance Sheet

QEP Resources Announces Review of Strategic

Alternatives

Devon Energy Announces Final Step to Complete

Transformation to U.S. Oil Growth Company

[TBU]

[TBU] [TBU]

[TBU]

Talos Energy Announces Full Year 2019 Operating

and Financial Guidance (includes A&D

announcement)

4

February 25, 2019

Long-life, shallow decline oil assets located in the prolific Clear

Fork Trend of the Permian Basin

Largely contiguous 10,250 net acre position located in the Hoople

Field in Crosby and Lubbock counties, Texas

100% operated with high WI (100%) and NRI (>75%)

Favorable leasehold position with little-to-no drilling

obligations until 2021; >50% of acreage position under two

leases from one landowner

Current production of ~300 net bopd (100% oil) with significant

remaining drilling inventory consisting of ~200+ low-risk Clear Fork

locations

Asset provides substantial, economic running room for organic and

acquisitive growth

Existing Clear Fork acreage only ~15% developed based on

10-acre development plan

– Additional upside through 5-acre development,

secondary recovery and Glorieta development as

demonstrated in offsetting acreage; CO2 and Wolfcamp

potential

Multiple bolt-on acquisition opportunities and new leasing

opportunities

Acreage position largely delineated through existing and offset

development; full-scale development plan in place with drill-ready

infrastructure

VDR available late February

Contact Chelsea Neville at [email protected] or 713-546-

9703 for a Confidentiality Agreement, access to the VDR, and/or to

request a data room presentation

Source: Juno Permian Divestiture announcement

Substantial

Unquantified

Upside

Near-term development potential by exploiting the Glorieta across Juno’s acreage position

Acreage position on trend with offset Glorieta development

Potential development opportunity to co-mingle Clear Fork and Glorieta production, yielding twice the reserves with

little incremental D&C capex

Additional reserve recovery from waterflood operations and 5-acre development; future tertiary recovery

Offset operator testing horizontal Wolfcamp potential in the area

Large,

Contiguous

Acreage Position

in the Prolific

Clear Fork Oil

Trend

High quality anchor asset in the heart of the Midland Basin’s Eastern Shelf with multiple stacked pay potential

Acreage situated in the Hoople Field, one of the most active Clear Fork development areas with >1,000 Clear Fork

producers drilled in the last 10 years

Majority of Juno’s acreage is situated in the core of the field with vertical offset Clear Fork EURs of ~60 MBo

Primary recovery economics provide attractive IRRs with low development costs

Secondary recovery provides an incremental increase of 150% of primary EUR based on analog fields

Clear Fork A STOOIP of up to 13 mmbo per section based on core and log analysis

Increased Oil

Cuts and

Improved

Economics from

Enhanced

Completions

Targeted, optimized fracs providing robust EURs and lower WOR vs. offset results

Fracture growth limited to ~40 feet from perf

Oil cuts have improved by three-fold using selective completions

Prior generation completions took the entirety of the pay zone and pumped excessive volumes, thereby increasing

communication with higher WOR sand bodies

Asset Ready for

Full-Scale

Development

Significant inventory of 200+ economic Clear Fork locations remaining (at 10-acre spacing)

Fast cycle times (~4-5 days spud-to-spud) and favorable land position provides the ability to accelerate development within

the first year

Juno’s predecessor in the Hoople Field grew production by over 25x in less than 3 years

Inexpensive access to water sources and disposal provides for low-cost waterflood and frac’ing operations

Significant investments in infrastructure, including electrical, roads, pipelines, and facilities

No deferred maintenance or P&A issues

Currently on the Market from BMO: Juno Permian Divestiture

ASSET HIGHLIGHTS

ASSET OVERVIEW PROCESS OVERVIEW

LOCATOR MAP

5

February 25, 2019

Opportunity to acquire highly economic and

contiguous 1,064 net acre (1,645 gross acre) position

in the Midland Basin located in west-central Glasscock

County, Texas

Assets provide high degree of operational control

with 98% operated, 74% HBP, and 67% average

WI

Current net production of ~54 boe/d from ten active

vertical wells holds the majority of acreage

Proven development opportunities targeting the Lower

Spraberry, Wolfcamp A, and Wolfcamp D formations

Active development by Parsley, Oxy, Diamondback,

and others highlights robust returns and de-risked

drilling locations

Continued improvement in well performance driven by

completion optimization

VDR available late February / early March 2019

Contact Chelsea Neville ([email protected] or 713-546-

9703) for a Confidentiality Agreement, access to the VDR, and/or

to request a data room presentation

Source: Rio Oil and Gas II Glasscock County Divestiture announcement

Active

Development By

Offset Operators

Producing Robust

Returns

Outstanding position in one of the most active basins in the U.S. with 181 rigs in the Midland Basin and 14 in Glasscock

County

~3,500 feet of porous, brittle, hydrocarbon rich pay available from the top of the Spraberry to the base of the Wolfcamp

Active offsetting development in the Lower Spraberry, Wolfcamp A, Wolfcamp B, and Wolfcamp D by Parsley, OXY,

Crownquest, Cinnabar, Encana, SM, Callon, Diamondback, Hunt, and others

Parsley is actively developing with strong results its directly offsetting Calverley assets in the LS, WCA, and WCB

– Parsley brought 17 wells online in 2018; outperformed historical with peak rates up to

2,000 boepd (84% oil)

– Parsley acquired Calverley position through BTA acquisition ($40,000+/net acre)

OXY recently completed five wells (west of Rio) targeting the WCA and has two additional permits

IP and EURs continue to increase through optimization of completion techniques: predominantly slickwater fracs with

proppant loading at ~1,900 lbs/ft

Over 30 potential stacked locations with additional unquantified upside in the Wolfcamp D

Operated Asset

Set Up For

Efficient, Stacked-

Pay, Long Lateral

Development

Contiguous 1,064 net acres in west-central Glasscock County

75% effective (8/8ths) net revenue interest

74% of net acres HBP from vertical producers with remaining acreage in primary term with 2+ years remaining

Leasehold primed for efficient cube development with 100% of locations expected to support 7,500’+ laterals; 100% of

acreage owns Spraberry through WCA rights and select ownership of WCD

No long term oil and gas sales dedications offer the purchaser marketing flexibility

Full Area Exit

Full area exit for Rio

Rio’s investments have been focused on assembling the position, perfecting subsurface interpretation, and readying the

asset for full-field development

Currently on the Market from BMO: Rio Oil & Gas II Glasscock County Divestiture

ASSET HIGHLIGHTS

ASSET OVERVIEW PROCESS OVERVIEW

LOCATOR MAP

6

February 25, 2019

25%

35%

45%

55%

65%

Feb-16 Aug-16 Feb-17 Aug-17 Feb-18 Aug-18 Feb-19

% o

f W

TI

NGL as % of WTI

$1

$2

$3

$4

$5

Feb-18 Aug-18 Feb-19 Aug-19 Feb-20

($/m

mb

tu)

$20

$30

$40

$50

$60

$70

$80

Feb-18 Aug-18 Feb-19 Aug-19 Feb-20

($/b

bl)

Historical Prices as of 21-Feb-19 Close ($/gal)

NGLs Current Last Wk. 6 Mo. Ago 1 Yr. Ago

Ethane $0.31 $0.30 $0.40 $0.24

Propane $0.72 $0.66 $0.97 $0.83

Butane $0.82 $0.80 $1.02 $0.90

Iso-butane $0.91 $0.92 $1.16 $1.13

Pentane+ $1.19 $1.16 $1.49 $1.35

NYMEX Gas Futures as of 21-Feb-19 Close ($/mmbtu)

Period(1) Current Last Wk. 6 Mo. Ago 1 Yr. Ago

12 Mo. Strip $2.87 $2.78 $2.91 $2.82

2019 $2.82 $2.73 $2.83 $2.78

2020 $2.73 $2.73 $2.66 $2.78

2021 $2.63 $2.65 $2.59 $2.83

2022 $2.81 $2.84 $2.73 $2.97

2023 $2.81 $2.84 $2.73 $2.97

NYMEX WTI Futures as of 21-Feb-19 Close ($/bbl) NYMEX Gas Futures as of 21-Feb-19 Close ($/mmbtu)

Period(1) Current Last Wk. 6 Mo. Ago 1 Yr. Ago

12 Mo. Strip $58.60 $56.33 $64.67 $59.19

2019 $58.48 $56.19 $63.51 $56.31

2020 $58.31 $56.50 $60.47 $53.55

2021 $56.62 $55.12 $58.05 $51.91

2022 $55.35 $54.17 $56.46 $51.24

2023 $54.74 $53.78 $55.57 $51.13

NGL PRICING(2)

HENRY HUB NATURAL GAS (HISTORICAL / FORECAST)

Commodity Prices

Source: BMO Commodity Products Group, Bloomberg, FactSet

1. Future prices are calendar year average unless stated otherwise.

2. Assumes typical Gulf Coast barrel composition.

WTI OIL (HISTORICAL / FORECAST)

Links:

http://www.nasdaq.com/markets/crude-oil.aspx

http://www.bloomberg.com/quote/CL1:COM

http://www.nasdaq.com/markets/natural-gas.aspx

http://www.bloomberg.com/quote/NG1:COM

Link to Detailed

Futures Data

Link to Detailed

Historical Graph

Link to Detailed

Futures Data

Link to Detailed

Historical Graph

[TBU]

[TBU]

[TBU]

7

February 25, 2019

Clearbrook

Midland

Cushing

St. James

(LLS)

East Coast

U.S. (Brent)

Midland Sweet-

Sour Spread

EMS

AECO

Northern

California

Sumas

Southern

California

El Paso - SJ

Waha

HSC

Henry Hub

Panhandle

CIG Chicago

Dominion

Transco

NATURAL GAS PRICING & DIFFERENTIALS TO HENRY HUB ($ / MMBTU) – AS OF 21-FEB-19

Commodity Prices (cont’d)

OIL PRICING & DIFFERENTIALS TO CUSHING WTI ($ / BBL) – AS OF 21-FEB-19

Legend

Price

Diff.

Legend

Price

Diff.

Source: BMO Commodity Products Group, Bloomberg

Note: Prices and differentials are for prompt month futures except for Clearbrook which is based on spot prices.

MAPS IN

MASTER VIEW

TBU

[TBU]

[TBU]

$56.96

$1.33 $64.15

$7.19

$2.49

($0.21)

$2.40

($0.30)

$2.70

$2.70

--

$56.42

($0.54)

$67.07

$10.11

$56.71

($0.25)

$51.46

($5.50)

$2.49

($0.21)

$2.73

$0.03

$1.18

($1.52)

$2.28

($0.42)$2.18

($0.52)$2.88

$0.18

$1.61

($1.09)$6.30

$3.60

$3.80

$1.10

8

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 473 -- 473 Oil Differential $0.90 ($0.10) $1.000

Permitting Activity 148 (176) 324 Gas Differential ($1.47) $0.01 ($1.48)

0%

10%

20%

30%

40%

50%

--

100

200

300

400

500

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

-$4.80

-$3.20

-$1.60

$0.00

$1.60

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-$18.00

-$12.00

-$6.00

$0.00

$6.00

$ /

mm

btu

$ /

bb

l

Midland Waha

5,000

6,000

7,000

8,000

9,000

10,000

11,000

1,000

1,500

2,000

2,500

3,000

3,500

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

3,184

10,301

9901,177

1,156

1,294

1,0911,149

1,223

9931,212

1,015871

1,293

781

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)(2)

19-Feb-19 Undisclosed Buyer Noble Energy Non-core acreage in the Delaware Basin $63 n.a. n.a. n.a.

19-Feb-19 Undisclosed Buyer Noble Energy 13,000 net acres in Reeves Co., TX $132 n.a. n.a. $10,154

08-Jan-19 Undisclosed Buyer MCM Energy Partners LLC Midland Basin assets $20 n.a. n.a. n.a.

06-Nov-18 Diamondback Energy ExL Pet.; EnergyQuest 3,646 net acres in Midland Basin $313 n.a. $89,286 $85,710

05-Nov-18 Centennial Resource Dev. Undisclosed Seller 820 net acres in Delaware Basin $26 n.a. n.a. $31,707

Mean $111 n.a. $89,286 $42,524

Median $63 n.a. $89,286 $31,707

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--

$50,000

$100,000

$150,000

$200,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

1 2 6 9 5 7 11 9 9 6 1 0 7 1 5 3 0

$ /

bo

e/d

# Deals

$126,473

--$10,000$20,000$30,000$40,000$50,000$60,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

1 2 8 8 6 6 12 13 15 7 3 2 7 1 5 3 0

$ /

acre

# Deals

$28,151

GROSS PRODUCTION

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS

Permian Snapshot

RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $45,000/boepd in 2014, $30,000/boepd in 2015, $35,000/boepd in 2016 & 2017, and $40,000/boepd in 2018 & 2019.

[TBU]

[TBU]

[TBU] [TBU]

[TBU] [TBU]

[TBU]

9

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 97 (1) 98 Oil Differential $8.50 ($0.60) $9.10

Permitting Activity 56 (66) 122 Gas Differential $0.02 $0.02 $0.00

0%

5%

10%

15%

20%

--

100

200

300

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

-$0.30

-$0.20

-$0.10

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-$6.00

-$4.00

-$2.00

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$ /

mm

btu

$ /

bb

l

LLS HSC

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

10,000

10,500

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

1,452

8,328

449378

426473

436379

454

328

399342

312

399

268

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)(2)

19-Nov-18 Lonestar Resources Inc Sabine Oil & Gas Corp 2,706 net acres in Eagle Ford $39 $2.98 $48,375 $14,302

20-Sep-18 WildHorse Undisclosed Seller 20,305 net Eagle Ford/Austin Chalk acres $35 n.a. n.a. $1,743

07-Sep-18 Undisclosed Buyer Viking Minerals LLC 1,191 net royalty acres in Eagle Ford $28 n.a. n.a. nmf

31-Jul-18 EP Energy Corp Undisclosed Seller Additional working interests in Eagle Ford $31 n.a. n.a. n.a.

26-Jul-18 BP BHP Billiton Permian, Eagle Ford, and Haynesville $10,500 n.a. n.a. n.a.

Mean $2,127 $2.98 $48,375 $8,022

Median $35 $2.98 $48,375 $8,022

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--$10,000$20,000$30,000$40,000$50,000$60,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 1 2 1 2 2 0 4 2 3 1 2 4 2 1 3 0

$ /

acre

# Deals

$6,130

--

$50,000

$100,000

$150,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

1 1 3 1 2 2 2 4 4 3 1 2 7 2 0 3 0

$ /

bo

e/d

# Deals

$70,217

Eagle Ford Snapshot

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $45,000/boepd in 2014, $30,000/boepd in 2015, $35,000/boepd in 2016 & 2017, and $40,000/boepd in 2018 & 2019.

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

GROSS PRODUCTION

10

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 68 1 67 Oil Differential $8.50 ($0.60) $9.10

Permitting Activity 17 (10) 27 Gas Differential -- -- --

0%

5%

10%

15%

20%

--

20

40

60

80

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

--

$2.00

$4.00

$6.00

$8.00

$10.00

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

--

$2.00

$4.00

$6.00

$8.00

$10.00

$ /

mm

btu

$ /

bb

l

LLS Henry Hub

5,000

6,000

7,000

8,000

9,000

10,000

11,000

80

90

100

110

120

130

140

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

102

10,206

181

247

156 168 154162 165

172174

105 104 9861

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/mcfe) ($/mcfe/d) ($/acre)(2)

19-Dec-18 Comstock Shelby Shale LLC 6,023 net acres in Haynesville $21 n.a. n.a. $3,404

19-Nov-18 Aethon III QEP Resources Inc 49,700 net acres in Haynesville $735 $0.77 $2,475 $14,789

05-Sep-18 Viking Energy Group Multiple Sellers Texas and Louisiana assets $100 n.a. n.a. n.a.

05-Sep-18 Equinor Texegy LLC 60,000 net acres in Austin Chalk $75 n.a. n.a. $1,250

06-Aug-18 Mission Creek Resources Bonanza Creek Energy Inc 11,132 net acres in the Cotton Valley $117 $1.69 $6,500 $10,510

Mean $210 $1.23 $4,487 $7,488

Median $100 $1.23 $4,487 $6,957

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--$2,000$4,000$6,000$8,000

$10,000$12,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 0 5 1 1 3 2 3 0 2 2 0 1 1 2 1 0

$ /

mcfe

/d

# Deals

$5,209

--

$5,000

$10,000

$15,000

$20,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 0 3 1 1 2 1 3 0 1 2 0 1 1 1 1 0

$ /

acre

# Deals

$3,349

Ark-La-Tex Snapshot

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $3,000/mcfepd in 2014, and $2,000/mcfepd in 2015, 2016, 2017, 2018, and 2019.

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

GROSS PRODUCTION

11

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 81 1 80 Oil Differential $10.32 $0.16 $10.16

Permitting Activity 27 (41) 68 Gas Differential ($0.19) $0.01 ($0.19)

0%

5%

10%

15%

20%

--

50

100

150

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

-$3.00

-$2.00

-$1.00

$0.00

$1.00

$2.00

$3.00

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-$15.00

-$10.00

-$5.00

$0.00

$5.00

$10.00

$15.00

$ /

mm

btu

$ /

bb

l

Brent Dominion

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

50

70

90

110

130

150

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

85

26,031367

454

282328 299 269

493

373 370305 307

439

205

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/mcfe) ($/mcfe/d) ($/acre)(2)

15-Oct-18 Undisclosed Buyer Range Resources Corp Overriding royalty interests in Appalachia $300 n.a. $17,649 nmf

27-Aug-18 PennEnergy Resources Rex Energy Corp 141,026 net acres in PA and OH $601 $0.58 $2,781 $4,258

26-Jul-18 Encino Acquisition Partners Chesapeake 938,000 net acres in the Utica $1,900 $0.66 $2,960 $2,026

29-Jun-18 Ascent Resources LLC Utica Minerals; Undisclosed 35,400 acres in the Utica $700 n.a. $15,217 $19,774

29-Jun-18 Ascent Resources LLC CNX Resources; Hess 78,000 acres in the Utica $800 n.a. $4,762 $10,256

Mean $860 $0.62 $8,674 $9,079

Median $700 $0.62 $4,762 $7,257

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--$2,000$4,000$6,000$8,000

$10,000$12,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 1 0 0 1 2 2 4 2 4 1 3 1 3 2 0 0

$ /

acre

# Deals

$2,083

--$5,000

$10,000$15,000$20,000$25,000$30,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 1 0 0 1 2 2 3 2 5 1 4 3 4 3 1 0

$ /

mcfe

/d

# Deals

$4,825

Appalachia Snapshot

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $3,000/mcfepd in 2014, and $2,000/mcfepd in 2015, 2016, 2017, 2018, and 2019.

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

GROSS PRODUCTION

12

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 57 -- 57 Oil Differential ($0.25) ($0.50) $0.25

Permitting Activity 18 (19) 37 Gas Differential ($0.31) -- ($0.31)

0%

5%

10%

15%

20%

--

50

100

150

200

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

-$1.00

-$0.50

$0.00

$0.50

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-$20.00

-$10.00

$0.00

$10.00

$ /

mm

btu

$ /

bb

l

Clearbrook CIG

1,100

1,300

1,500

1,700

1,900

2,100

2,300

2,500

800

900

1,000

1,100

1,200

1,300

1,400

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

1,195

2,234

104126

108138 126

171 164

127

201

12896

133

85

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)(2)

31-Jul-18 Northern Oil and Gas W Energy Partners 10,600 net acres in Williston Basin $288 n.a. $42,708 $27,196

18-Jul-18 Northern Oil and Gas Pivotal Petroleum Partners LP Producing assets in Williston Basin $152 n.a. $37,032 n.a.

12-Jul-18 PetroShale Inc Slawson Exploration Co 1,981 net acres in Williston Basin $55 $6.04 $100,000 $27,764

06-Jul-18 Energy Resources 12 LP Bruin E&P Partners LLC 2.8% non-operated WI in Bakken assets $83 n.a. n.a. n.a.

25-Jun-18 Riverbend Oil & Gas LLC Oasis Petroleum 10,167 net acres in Williston Basin $153 n.a. $49,196 $15,049

Mean $146 $6.04 $57,234 $23,336

Median $152 $6.04 $45,952 $27,196

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--

$20,000

$40,000

$60,000

$80,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 1 1 4 0 2 3 3 0 1 3 3 0 6 3 0 0

$ /

bo

e/d

# Deals

$43,532

--

$5,000

$10,000

$15,000

$20,000

$25,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 0 1 2 0 0 2 3 1 0 3 2 0 5 2 0 0

$ /

acre

# Deals

$2,712

Bakken Snapshot

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $45,000/boepd in 2014, $30,000/boepd in 2015, $35,000/boepd in 2016 & 2017, and $40,000/boepd in 2018 & 2019.

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

GROSS PRODUCTION

13

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 82 (1) 83 Oil Differential ($0.25) ($0.50) $0.25

Permitting Activity 21 (160) 181 Gas Differential ($0.31) -- ($0.31)

0%

5%

10%

15%

20%

--

50

100

150

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)(2)

14-Feb-19 Undisclosed Buyer Harvest Oil & Gas Corp San Juan Basin assets $43 $1.57 $10,835 n.a.

01-Oct-18 DJR Energy LLC Encana 182,000 net acres in San Juan Basin $480 n.a. $88,889 $2,637

28-Aug-18 Vermilion Energy Inc Massif Oil & Gas LLC 55,000 acres in Powder River Basin $150 n.a. $56,604 $2,727

28-Aug-18 Rebellion Energy II LLC Liberty Resources II LLC 19,000 net acres in Powder River Basin $100 n.a. n.a. $5,263

09-Aug-18 Undisclosed Buyer Ultra Petroleum ~8,000 net acres in the Uinta $75 n.a. $37,500 $9,375

Mean $170 $1.57 $48,457 $5,001

Median $100 $1.57 $47,052 $3,995

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

-$1.00

-$0.50

$0.00

$0.50

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-$20.00

-$10.00

$0.00

$10.00

$ /

mm

btu

$ /

bb

l

Clearbrook CIG

11,500

12,000

12,500

13,000

13,500

14,000

400

500

600

700

800

900

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

763

12,887

460

650

327456

551666

523 510

681

824 807

346275

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

--

$5,000

$10,000

$15,000

$20,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 0 3 3 0 1 1 0 1 0 1 5 2 0 2 1 0

$ /

acre

# Deals

$4,655

--$20,000$40,000$60,000$80,000

$100,000$120,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2 0 4 4 1 6 2 0 1 6 3 9 3 1 3 1 1

$ /

bo

e/d

# Deals

$37,548

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS

Rockies (excl. Bakken) Snapshot

RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $45,000/boepd in 2014, $30,000/boepd in 2015, $35,000/boepd in 2016 & 2017, and $40,000/boepd in 2018 & 2019.

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

GROSS PRODUCTION

14

February 25, 2019

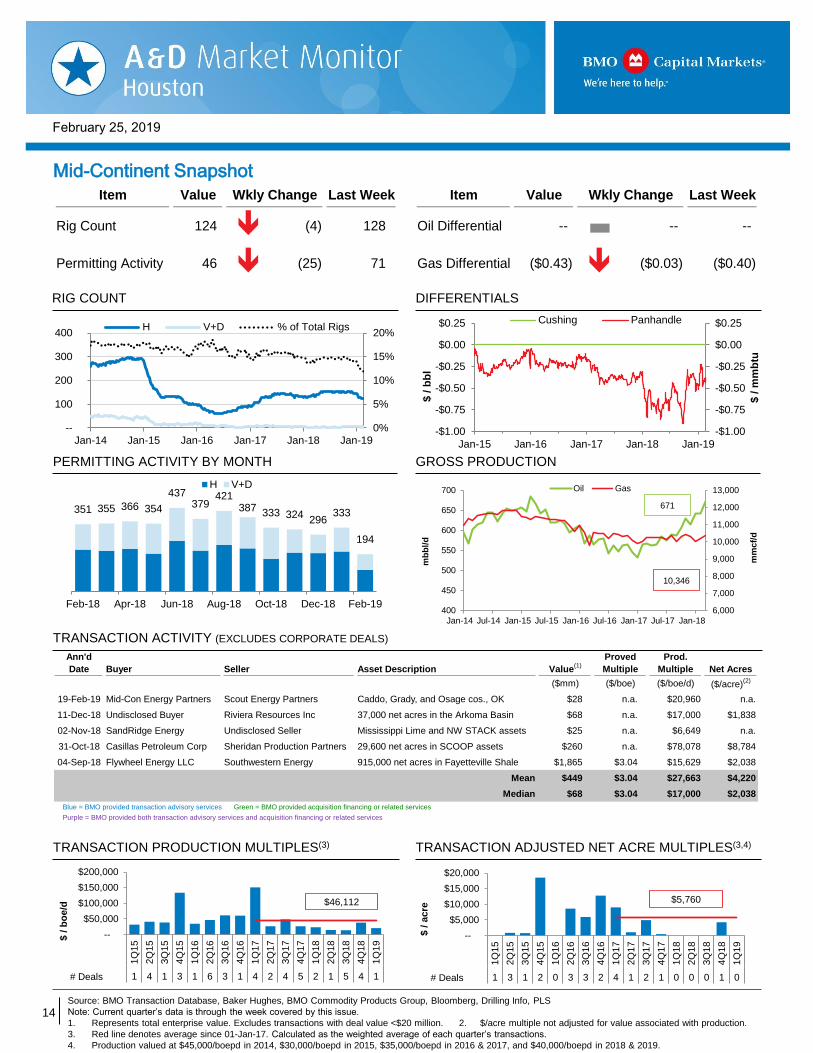

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 124 (4) 128 Oil Differential -- -- --

Permitting Activity 46 (25) 71 Gas Differential ($0.43) ($0.03) ($0.40)

0%

5%

10%

15%

20%

--

100

200

300

400

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

H V+D % of Total Rigs

-$1.00

-$0.75

-$0.50

-$0.25

$0.00

$0.25

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-$1.00

-$0.75

-$0.50

-$0.25

$0.00

$0.25

$ /

mm

btu

$ /

bb

l

Cushing Panhandle

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

400

450

500

550

600

650

700

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas

671

10,346

351 355 366 354

437379

421387 333 324

296333

194

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

H V+D

Ann'd

Date Buyer Seller Asset Description Value(1)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)(2)

19-Feb-19 Mid-Con Energy Partners Scout Energy Partners Caddo, Grady, and Osage cos., OK $28 n.a. $20,960 n.a.

11-Dec-18 Undisclosed Buyer Riviera Resources Inc 37,000 net acres in the Arkoma Basin $68 n.a. $17,000 $1,838

02-Nov-18 SandRidge Energy Undisclosed Seller Mississippi Lime and NW STACK assets $25 n.a. $6,649 n.a.

31-Oct-18 Casillas Petroleum Corp Sheridan Production Partners 29,600 net acres in SCOOP assets $260 n.a. $78,078 $8,784

04-Sep-18 Flywheel Energy LLC Southwestern Energy 915,000 net acres in Fayetteville Shale $1,865 $3.04 $15,629 $2,038

Mean $449 $3.04 $27,663 $4,220

Median $68 $3.04 $17,000 $2,038

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--

$50,000

$100,000

$150,000

$200,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

1 4 1 3 1 6 3 1 4 2 4 5 2 1 5 4 1

$ /

bo

e/d

# Deals

$46,112

--

$5,000

$10,000

$15,000

$20,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

1 3 1 2 0 3 3 2 4 1 2 1 0 0 0 1 0

$ /

acre

# Deals

$5,760

Mid-Continent Snapshot

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

PERMITTING ACTIVITY BY MONTH

DIFFERENTIALS RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Represents total enterprise value. Excludes transactions with deal value <$20 million. 2. $/acre multiple not adjusted for value associated with production.

3. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

4. Production valued at $45,000/boepd in 2014, $30,000/boepd in 2015, $35,000/boepd in 2016 & 2017, and $40,000/boepd in 2018 & 2019.

TRANSACTION PRODUCTION MULTIPLES(3) TRANSACTION ADJUSTED NET ACRE MULTIPLES(3,4)

GROSS PRODUCTION

15

February 25, 2019

Item Value Wkly Change Last Week Item Value Wkly Change Last Week

Rig Count 19 (2) 21 Oil Differential $8.50 ($0.60) $9.10

Permitting Activity 6 (1) 7 Gas Differential -- -- --

0%

5%

10%

15%

20%

--

10

20

30

40

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

Deep Water Shelf % of Total Rigs

--

$2.00

$4.00

$6.00

$8.00

$10.00

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

--

$2.00

$4.00

$6.00

$8.00

$10.00

$ /

mm

btu

$ /

bb

l

LLS Henry Hub

2,000

2,500

3,000

3,500

4,000

4,500

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

mm

cf/

d

mb

bl/

d

Oil Gas1,683

2,647

1319

2733

29 2932 33

39

3230 30

24

Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19

Ann'd

Date Buyer Seller Asset Description Value(2)

Proved

Multiple

Prod.

Multiple Net Acres

($mm) ($/boe) ($/boe/d) ($/acre)(3)

16-Jan-19 Talos Energy Inc Samson Energy Co LLC Non-op Gulf of Mexico working interest $30 $13.45 $17,939 n.a.

10-Oct-18 Murphy Petrobras Gulf of Mexico joint venture $900 $15.00 $21,951 n.a.

04-Sep-18 Talos Energy Inc Whistler Energy II LLC Leases in Green Canyon federal waters $91 n.a. $60,667 n.a.

27-Apr-18 Stone Energy Shell; ExxonMobil; Anadarko GOM Ram Powell assets $234 n.a. $38,361 n.a.

28-Mar-18 W&T Offshore Cobalt International Energy 9.375% non-op WI in the Heidelberg unit $31 $23.92 $9,345 n.a.

Mean $257 $17.46 $29,653 n.a.

Median $91 $15.00 $21,951 n.a.

Blue = BMO provided transaction advisory services Green = BMO provided acquisition financing or related services

Purple = BMO provided both transaction advisory services and acquisition financing or related services

--

$10

$20

$30

$40

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 0 1 0 0 0 2 1 0 0 0 1 2 1 0 1 1

$ /

bo

e

# Deals

$18.10

--

$15,000

$30,000

$45,000

$60,000

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

0 0 1 1 0 0 2 0 0 0 0 1 2 2 2 1 1

$ /

bo

e/d

# Deals

$32,164

Gulf of Mexico Snapshot

PERMITTING ACTIVITY BY MONTH(1)

DIFFERENTIALS RIG COUNT

Source: BMO Transaction Database, Baker Hughes, BMO Commodity Products Group, Bloomberg, Drilling Info, PLS

Note: Current quarter’s data is through the week covered by this issue.

1. Permits include directional and unidentified drilling permits. 2. Represents total enterprise value. Excludes transactions with deal value <$20 million.

3. $/acre multiple not adjusted for value associated with production.

4. Red line denotes average since 01-Jan-17. Calculated as the weighted average of each quarter’s transactions.

GROSS PRODUCTION

TRANSACTION ACTIVITY (EXCLUDES CORPORATE DEALS)

TRANSACTION PRODUCTION MULTIPLES(4) TRANSACTION PROVED RESERVE MULTIPLES(4)

16

February 25, 2019

Upcoming Industry Events

Disclaimer: The foregoing links are for convenience only and relate to materials that were not prepared or reviewed by BMO Capital Markets. BMO Capital Markets takes

no responsibility for and makes no representations with respect to the contents thereof. These materials may be inconsistent with the views of BMO Capital Markets.

Note: Event features a speaker from BMO Houston’s A&D Group.

Click event to open

July 2019 Jul 16 Houston Producers Forum Luncheon

Jul 19 ADAM-Houston Monthly Luncheon

April 2019 Apr 8-9 IPAA Oil & Gas Investment Symposium

Apr 15 DUG Sand (Fort Worth)

Apr 15 DUG Water (Fort Worth)

Apr 15-17 DUG Permian (Fort Worth)

Apr 17 176th OPEC Meeting

Apr 16 Houston Producers Forum Luncheon

Apr 19 ADAM-Houston Monthly Luncheon

ADAM-Houston Monthly Luncheon – 3rd Friday

Houston Producers Forum Luncheon – 3rd Tuesday

May 2019 May 6-9 Offshore Technology Conference

May 10 Petroleum Resources Economics Conference

May 13-17 SPE Electric Submersible Pumps Symposium

May 14-15 DUG Rockies (Denver)

May 14 Houston Producers Forum Luncheon

May 16 IADC Drilling Onshore Conference & Exhibition

May 17 ADAM-Houston Monthly Luncheon

June 2019 Jun 5-6 Midstream Texas Conference & Exhibition

Jun 18 Houston Producers Forum Luncheon

Jun 18-20 DUG East (Pittsburgh)

Jun 19-20 IADC World Drilling Conference & Exhibition

Jun 21 ADAM-Houston Monthly Luncheon

Jun 24-26 IPAA Midyear Meeting

August 2019 Aug 16 ADAM-Houston Monthly Luncheon

Aug 20 IPAA Oil & Gas Overview Course

Aug 20 Houston Producers Forum Luncheon

Aug 21-22 Summer NAPE

September 2019 Sep 17 Houston Producers Forum Luncheon

Sep 20 ADAM-Houston Monthly Luncheon

Sep 24-26 DUG Eagle Ford (San Antonio)

Sep 30-Oct 2 SPE Annual Technical Conference and Exhibition

January 2019 Jan 31 SPE A&D Symposium

October 2019 Oct 9 IPAA Leaders in Industry Luncheon

Oct 15 Houston Producers Forum Luncheon

Oct 18 ADAM-Houston Monthly Luncheon

Oct 22-23 A&D Strategies and Opportunities Conference

2020

Apr 20-22 OGIS New York

Jul 22-24 SPE Unconventional Resources Technology

Aug 11-14 Enercom Oil & Gas Conference

November 2019 Nov 4-6 Executive Oil Conference & Exhibition

Nov 15 ADAM-Houston Monthly Luncheon

Nov 19 IPAA Oil & Gas for Newcomers

Nov 19 Houston Producers Forum Luncheon

Nov 19-21 DUG Midcontinent (Oklahoma City)

December 2019 Dec 17 Houston Producers Forum Luncheon

Dec 20 ADAM-Houston Monthly Luncheon

January 2019 Jan 15 Houston Producers Forum Luncheon

Jan 25 ADAM-Houston Monthly Luncheon

Jan 24 IPAA Private Capital Conference

Jan 31 SPE A&D Symposium

March 2019

Mar 5-7 IADC/SPE Drilling Conference

Mar 15 ADAM-Houston Monthly Luncheon

Mar 19 Houston Producers Forum Luncheon

Mar 26-28 International Petroleum Technology Conference

Mar 5 Hart’s Energy Capital Conference

January 2020 Jan 23 IPAA Private Capital Conference

Jan 17 ADAM-Houston Monthly Luncheon

Jan 21 Houston Producers Forum Luncheon

February 2020 Feb 19 Houston Producers Forum Luncheon

Feb 25-26 DUG Haynesville (Shreveport)

17

February 25, 2019

SCOOP/STACK/Merge

DJ-Niobrara

Eagle Ford

Haynesville

Granite Wash

GOM

Permian

Marcellus

Utica

Williston

Gulf Coast Onshore

Piceance

Powder River Green River

Legend

Current

Change

This material is prepared by the BMO Capital Markets’ Investment and Corporate Banking Department, for distribution to BMO Capital Markets’ clientele. It is not a product of

BMO Capital Markets’ Research Department. The views of the Investment and Corporate Banking Department may differ from those of the Research Department.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal

Ireland p.l.c, and Bank of Montreal (China) Co. Ltd and the institutional broker dealer businesses of BMO Capital Markets Corp. (Member FINRA and SIPC) in the U.S., BMO Nesbitt

Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia and BMO Capital Markets Limited

(authorised and regulated by the Financial Conduct Authority) in Europe and Australia. “Nesbitt Burns” is a registered trademark of BMO Nesbitt Burns Inc., used under license. “BMO

Capital Markets” is a trademark of Bank of Montreal, used under license. "BMO (M-Bar roundel symbol)" is a registered trademark of Bank of Montreal, used under license. ® Registered

trademark of Bank of Montreal in the United States, Canada and elsewhere. ™ Trademark of Bank of Montreal in the United States and Canada.

Bank of Montreal or its subsidiaries (“BMO Financial Group”) has lending arrangements with, or provide other remunerated services to, many issuers covered by BMO Capital Markets.

The opinions, estimates and projections contained in this report are those of BMO Capital Markets as of the date of this report and are subject to change without notice. BMO Capital

Markets endeavors to ensure that the contents have been compiled or derived from sources that we believe are reliable and contain information and opinions that are accurate and

complete. However, BMO Capital Markets makes no representation or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions contained

herein and accepts no liability whatsoever for any loss arising from any use of, or reliance on, this report or its contents. Information may be available to BMO Capital Markets or its

affiliates that is not reflected in this report. The information in this report is not intended to be used as the primary basis of investment decisions, and because of individual client

objectives, should not be construed as advice designed to meet the particular investment needs of any investor. This material is for information purposes only and is not an offer to sell or

the solicitation of an offer to buy any security. BMO Capital Markets or its affiliates will buy from or sell to customers the securities of issuers mentioned in this report on a principal basis.

BMO Capital Markets or its affiliates, officers, directors or employees have a long or short position in many of the securities discussed herein, related securities or in options, futures or

other derivative instruments based thereon. BMO Capital Markets may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for

same. The reader should assume that BMO Capital Markets or its affiliates may have a conflict of interest and should not rely solely on this report in evaluating whether or not to buy or

sell securities of issuers discussed herein.

All values in this document are in US$ unless otherwise specified.

Source of rig count stats: Baker Hughes

Rig Count Summary

MAPS IN

MASTER VIEW

Contacts

Disclaimer

Geoff Roberts

MD & Co-Head of U.S. A&D

713-518-1268

Jason Martinez

MD & Co-Head of U.S. A&D

713-546-9771

Howard Barnwell

MD & Transactions Mgr.

713-546-9767

Rob Priske

MD & Transactions Mgr.

713-546-9727

Marian Yu

Associate

Aaron Moeller

Associate

Jennifer Boudreaux

Analyst

BMO uses updated basin outlines, and the resulting rig counts, to more accurately represent current basin knowledge. The data below reflect these changes

and is different than those shown by Baker Hughes. The totals are the same.

473

--

57

--

19

--

62

132

1

19

(2)

10

188

(4)

68

1

97

(1)

19

--

5

(2)

23

--19

--

[TBU]

Chelsea Neville

Transactions Coordinator

This

Week Change

Last

Week

Last

Year

Total Rigs 1,047 (4) 1,051 978

Oil 853 (4) 857 799

Gas 194 -- 194 179

Miscellaneous -- -- -- --

Directional 68 (2) 70 69

Horizontal 916 1 915 842

Vertical 63 (3) 66 67

Basin

Permian 473 -- 473 435

SCOOP/STACK/Merge 88 (4) 92 101

Granite Wash 10 1 9 18

Eagle Ford 97 (1) 98 86

Haynesville 68 1 67 59

Marcellus 62 1 61 54

Utica 19 -- 19 23

Williston 57 -- 57 50

DJ-Niobrara 32 1 31 26

Green River 19 -- 19 20

Powder River 23 -- 23 17

Piceance 5 (2) 7 7

Gulf Coast Onshore 19 -- 19 18

GOM 19 (2) 21 17

Alaska 13 1 12 9

Other 43 -- 43 38

Mid-Con 26 (1) 27 16

Rockies 3 -- 3 5

Western 12 1 11 14

Eastern 2 -- 2 3