Projected Retirement Income: What’s the Future Hold for...

19

Projected Retirement Income: What’s the Future Hold for Employees Findings from Retirement Income Adequacy at Large Companies, an Aon Hewitt Study Retirement Income Industry Association May 16, 2013

Transcript of Projected Retirement Income: What’s the Future Hold for...

Projected Retirement Income: What’s the Future Hold for Employees

Findings from Retirement Income Adequacy at Large Companies, an Aon Hewitt Study

Retirement Income Industry AssociationMay 16, 2013

Today’s Speakers

Rob Reiskytl, FSA Partner, National Leader of Retirement Plan Strategy and DesignAon Hewitt

Barbara Hogg, FSAPartner, Retirement Communication LeaderAon Hewitt

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013 1

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013 2

Why Talk About Retirement Income Adequacy?

Employers want to: Maximize value

of plansEnhance employee

appreciationHelp attract, retain, and

engage employeesFacilitate orderly

retirement patterns

It naturally matters to individuals……but it also matters to employers

Employers seek: Efficiency Adequacy

3

Aon Hewitt’s Study: The Real Deal

About the study: Projected retirement income – Resources– Needs

2.2 million employees78 companiesFocus on “full-career contributors”– Hired by age 35– Allows for measurement across

potentially full career

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Study: 2012 Retirement Income Adequacyat Large Companies

4

Defining Retirement Income Adequacy

Retirement Resources Consider key sources of retirement income:

Defined Contribution– Actual balances,

contribution elections, and current plan provisions

Defined BenefitSocial Security

Retirement NeedsCalculate amount needed tosustain preretirement standard ofliving

Start with pay at retirementAdjust for: – Retirement savings stop– Taxes decrease– Expenditures change– Medical costs increase

Reflect postretirement inflation and medical trend

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

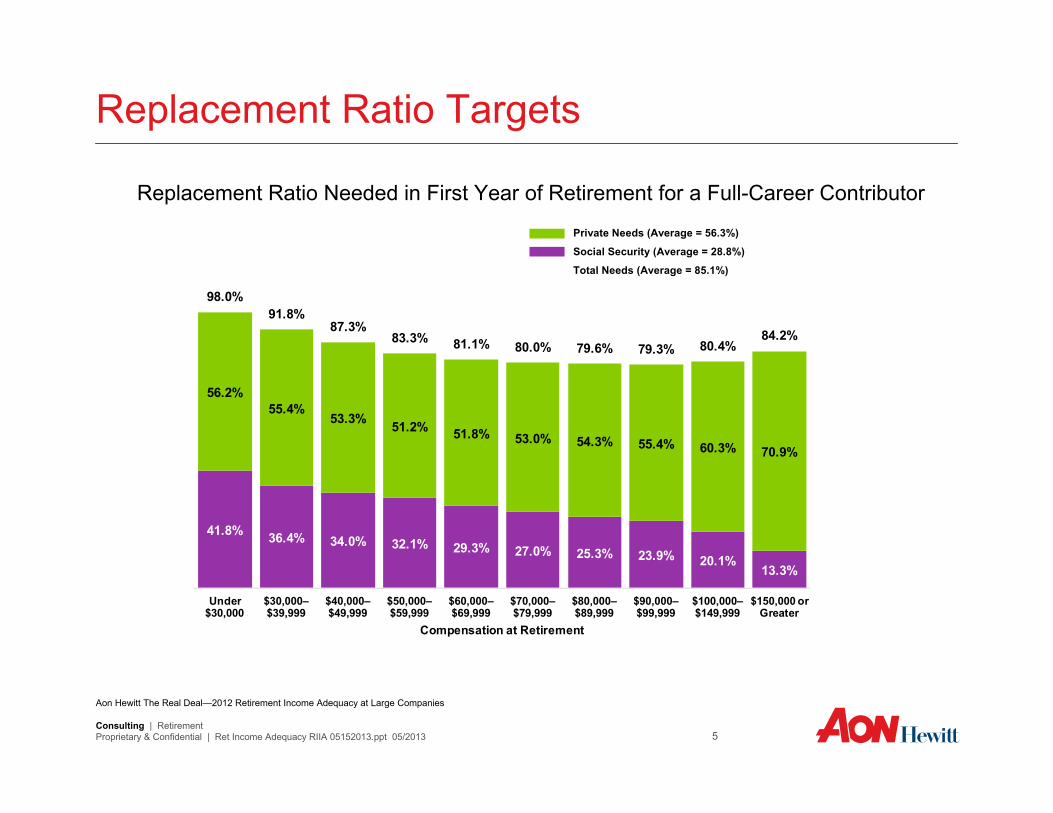

41.8% 36.4% 34.0% 32.1% 29.3% 27.0% 25.3% 23.9% 20.1%13.3%

56.2%55.4%

53.3% 51.2% 51.8% 53.0% 54.3% 55.4% 60.3% 70.9%

98.0%91.8%

87.3%83.3% 81.1% 80.0% 79.6% 79.3% 80.4%

84.2%

Under $30,000

$30,000–$39,999

$40,000–$49,999

$50,000–$59,999

$60,000–$69,999

$70,000–$79,999

$80,000–$89,999

$90,000–$99,999

$100,000–$149,999

$150,000 or Greater

Compensation at Retirement

5

Replacement Ratio Targets

Replacement Ratio Needed in First Year of Retirement for a Full-Career Contributor

Private Needs (Average = 56.3%)

Social Security (Average = 28.8%)

Total Needs (Average = 85.1%)

Aon Hewitt The Real Deal—2012 Retirement Income Adequacy at Large Companies

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

6

2.1

2.6

4.1

2.2

11.0

4.9

15.9

8.8

Private Resources

Shortfall Private Needs

Social Security

Total Needs

Full-Career Contributors

Projected Results at Age 65

2.2 times pay shortfall, down from 2.4 times pay in 2010– Strong market returns during

2009 and 2010– Continued participant

contributions– More participants in automatic

contribution escalation

Defined Contribution Plan—Employee Portion

Defined Contribution Plan—Employer Portion

Defined Benefit Plan

Shortfall

Private Needs

Social Security

Total Needs

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

7

Percent of Pay(to retirement)

Multiples of Pay (through

retirement)

85% Total Income Need 15.9 times pay

(29%) Expected from Social Security (4.9 times pay)

56% Other (employer/personal/etc.) 11.0 times pay

How much money do I need to support all my years of retirement?

How much retirement income

do I need when I retire?

Aon Hewitt The Real Deal—2012 Retirement Income Adequacy at Large Companies

Perspectives on Retirement Income Needs

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

8

9.0%

11.8%

16.4%

18.0%

15.7%

11.8%

17.3%

Less than (8)

(8) - (6.1)

(6) - (4.1)

(4) - (2.1)

(2) - (0.1)

0 - 1.9

2 or Greater

Baseline Average = (2.2)

Surplus/(Shortfall) at Age 65

On Track

Relatively even distribution among full-career contributing employees

Nearly 30% are “on track”Another 16% have a relatively small predicted shortfallMore than 20% have projected shortfalls of greater than six times pay

Aon Hewitt The Real Deal—2012 Retirement Income Adequacy at Large Companies

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Tracking Toward Adequate Retirement Income

Total contribution rate (assuming only eligible for a defined contribution plan) required based on age savings start– All contributions (employee and employer) – Percent of each year’s pay

Average percentage shown; approx 3% range around average allows for changing assumptions. Calculations assume consistent savings rate every year during working career until retirement at age 65 (or 67) with targeted retirement resources of 11 times pay at 65 or 9.4 times pay at 67, 7% annual return on DC assets during accumulation, 4% annual pay increases, and unsubsidized future retiree medical coverage

Start at 25 Start at 30 Start at 35

24% (age 65)18% (age 67)15% (age 65)

12% (age 67)

19% (age 65)15% (age 67)

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013 9

10

How can individuals quickly see if they are on track based on how much they have accumulated?

0.00x1.75x

4.00x

7.00x

11.00x

25 35 45 55 65

Aon Hewitt The Real Deal—2012 Retirement Income Adequacy at Large Companies

Tracking Toward Adequate Retirement Income

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Multiples of Pay Milestones

Age

11

Results for DC-Only Employers

3.4

2.3

3.2

3.9

4.4

1.1 3.89.6

7.6

10.7 11.4

Private Resources

Shortfall Private Needs

Private Resources

Shortfall Private Needs

DB & DC Employees DC Only Employees

DC-only employees are projected to have a larger shortfall, on

average, due to lower total

employer-provided benefits

Average:Employees With DB

and DC PlansEmployees With DC

Plans Only

Participation rate 78% 69%

Savings rate 7.8% 6.7%

Age 65 projected savings rate 8.8% 9.4%

Account balance to date $120,000 $67,000

Age 41 35

Service 15 9

Pay $83,000 $68,000

Defined Contribution Plan—Employee Portion

Defined Contribution Plan—Employer Portion

Defined Benefit Plan

Shortfall

Private Needs

Social Security

Total Needs

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

12

Impact of Gender

2.6 1.98.6 8.9

11.2 10.8

Private Resources

Shortfall Private Needs

Private Resources

Shortfall Private Needs

Females Males

Average: Females Males

Participation rate 73% 74%

Savings rate 6.9% 7.8%

Account balance to date $75,000 $118,000

Life expectancy age 88 87

Age 39 39

Service 13 13

Pay $66,000 $87,000

Females are more at risk of inadequate retirement

income because they save less than males and

are expected to live longer

Private Resources

Shortfall

Private Needs

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

13

How Can We Improve Results?

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Employer actionsExpand automation

Offer array of investment advisory

servicesDesign plans thoughtfully

Employee actionsRetire laterSave more

Invest better Understand and

use lifetime income solutions

GamificationModeling Tools

Driving Behaviors and Outcomes

Are you on track to retire?

• How old are you? • How much do you earn?

Personalized Communication Benefits Hubs Flash/Video

Attitudinal Segmentation

14Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

15

Taking Action

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Identify andManage Risk• Adequacy

modeling• Workforce

analysis

Communicatewith Employees• Education /

awareness• Personalized

communication • Online modeling

tools • Professional help

Consider LongevitySolutions• Education on

alternatives • Cost/benefit

analysis • Choosing

providers

1 2 3

Large Consumer Products CompanyProblem: Organization seeks to embrace DC Plan Sponsorship, differences from DBAnalysis: Measure theoretical potential, followed by Real Deal study of actual results

1. Measure theoretical retirement income potential of new DC plans versus prior DB plans

2. Analyze actual Real Deal resultsNew hires DC-OnlyGrandfathered with pensionChoice with partial pension

3. FindingsFemales tend to have smaller balances and live longer, but they also save at stronger rates than malesKeep automation, with increased escalation defaultsConsider financial advice and lifetime income solutionsClarify messages and communicate

4. Next steps—consider: Race/ethnicitySensitivity to future inflationImpact of changing health careImpact of changing tax rates

Retiree Medical Subsidy

DC Plan—Employee Portion

DC Plan—Employer Portion

Defined Benefit Plan

Social Security

Shortfall

Retirement Needs

All results expressed as multiples of payAll results expressed as multiples of pay

4.4

2.11.2

2.73.7

2.4 1.0

3.8 4.7

4.7

0.113.3

14.115.115.7

Resources Shortfall Needs Resources Shortfall Needs

Real Deal Study Land O'LakesABC CompanyReal Deal Study Including Key Scenarios

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

65 70 75 80 85 90 95 100

DB Benefit Social Security Total DC Balance Total Need

Retirement Adequacy Modeling

16Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Technology CompanyProblem: Client needs to improve awareness of retirement income targets and promote actionSolutions: Use personalized employee education and online modeling tools

1. Educate through personalized communication and messaging

2. Offer Retirement Readiness Calculator

3. Promote financial education and planning resources (telephone-based personal financial planning)

Retirement Readiness Modeler

17Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013

Questions

Consulting | RetirementProprietary & Confidential | Ret Income Adequacy RIIA 05152013.ppt 05/2013 18

![Anti-Windup Implementation of Projected Dynamics · dynamical systems that encompasses projected gradient ow [17], projected New-ton ow [16], subgradient ow [9] and projected saddle-ows](https://static.fdocuments.us/doc/165x107/60294d1aac77a707331df610/anti-windup-implementation-of-projected-dynamics-dynamical-systems-that-encompasses.jpg)