Project on Corporate Loans

112

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911 EXECUTIVE SUMMARY This project was undertaken at the Union Bank of India (INDUSTRIAL FINANCE BRANCH) Office Delhi, at the Credit Department. Financial requirements for Project Finance and Working Capital purposes are taken care of at the Credit Department. Companies that intend to seek credit facilities approach the bank. Primarily, credit is required for following purposes: a. Working capital finance b. Term loans for corporate projects Project Financing discipline includes understanding the rationale for project financing, how to prepare the financial plan, assess the risks, design the financing mix, and raise the funds. In addition, one must understand some project financing plans have succeeded while others have failed. A knowledge-base is required regarding the design of contractual arrangements to support project financing; issues for the host government legislative provisions, public/private infrastructure partnerships, public/private financing structures; credit requirements of lenders, and how to determine the project's borrowing capacity; how to analyze cash flow projections and use them to measure expected rates of GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 1

-

Upload

rahul-gupta -

Category

Documents

-

view

7 -

download

0

description

report on corporate loans in union bank

Transcript of Project on Corporate Loans

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

EXECUTIVE SUMMARY

This project was undertaken at the Union Bank of India (INDUSTRIAL FINANCE

BRANCH) Office Delhi, at the Credit Department. Financial requirements for Project

Finance and Working Capital purposes are taken care of at the Credit Department.

Companies that intend to seek credit facilities approach the bank. Primarily, credit is

required for following purposes:

a. Working capital finance

b. Term loans for corporate projects

Project Financing discipline includes understanding the rationale for project

financing, how to prepare the financial plan, assess the risks, design the financing

mix, and raise the funds. In addition, one must understand some project financing

plans have succeeded while others have failed. A knowledge-base is required

regarding the design of contractual arrangements to support project financing; issues

for the host government legislative provisions, public/private infrastructure

partnerships, public/private financing structures; credit requirements of lenders, and

how to determine the project's borrowing capacity; how to analyze cash flow

projections and use them to measure expected rates of return; tax and accounting

considerations; and analytical techniques to validate the project's feasibility

The purpose of this project is to explain, in a brief and general way, the manner in

which risks are approached by financiers in a project finance transaction. Such risk

minimization lies at the heart of project finance. Efficient management of credit

portfolio is of utmost importance as it has a tremendous impact on the Banks’ assets

quality & profitability. The concept of Credit Management is undergoing radical

changes. Credit Risk in all exposures calls for precise measuring and monitoring for

taking considered credit decisions with suitable risk factor, risk premium, etc. Credit

portfolio should be well diversified in various promising sectors with a cautious

approach to be adopted in risky segments.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 1

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

CHAPTER 1

INTRODUCTION

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 2

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

INTRODUCTION TO THE PROJECT

The project undertaken is credit appraisal of industrial finance for corporate loans..

The credit appraisal for corporate projects starts with understanding the need of loan

to the borrower i.e. for which purpose the loan is required. After this next step is to

analyse the financial statement of the company to whom the loan is to be sanctioned.

The main things which are taken into consideration while analyzing the financial

statement are type of statement, nature of activity ,accounting policy, qualities of

assets and liabilities , unit wise performance result of the company & director’s

report. After analyzing the financial statement the second step is to study the principle

given by Basel committee on banking supervision which basically Indian banks have

to be followed as per the order by Reserve Bank of India. The third step is to analyse

the key financial ratios of the company such as: Leverage ratio, liquidity ratio,

profitability ratio, turnover ratio, inventory norms., credit rating methodology differ

from bank to bank in term of the weight age given to the parameters but the parameter

used by the banks to assess credit worthiness are almost same to all company.

The report is divided into different parts that includes-

Chapter1- Introduction contains the background, achievements, objectives,

developments & financial profile, and SWOT analysis of the Union Bank of India.

Chapter 2- Theoretical framework of the study contains concepts of Working Capital

and criteria for credit rating.

Chapter 3- Research methodology and design contains type of the data collected,

design adopted, scope, objectives and limitations of the study.

Chapter 4- Data analysis & Interpretation contains the analysis and interpretation of

the financial balance sheets and its financial indicators to evaluate credit rating.

Chapter 5- Major findings & Discussions contains examination of the working capital

and ratios interpreted.

Chapter 6- Recommendations and Conclusions contains the suggestions for the

company’s improvements in the fields where needed.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 3

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

INDUSTRY PROFILE

The last decade has seen many positive developments in the Indian banking sector.

The growth in the Indian Banking Industry has been more qualitative than quantitative

and it is expected to remain the same in the coming years. Based on the projections

made in the "India Vision 2020" prepared by the Planning Commission, the report

forecasts that the pace of expansion in the balance-sheets of banks is likely to

decelerate. The total assets of all scheduled commercial banks by end-March 2010 is

estimated at Rs 40,90,000 crores. That will comprise about 65 per cent of GDP at

current market prices as compared to 67 per cent in 2002-03. Bank assets are expected

to grow at an annual composite rate of 13.4 per cent during the rest of the decade as

against the growth rate of 16.7 per cent that existed between 1994-95 and 2002-03. It

is expected that there will be large additions to the capital base and reserves on the

liability side.

The Indian Banking Industry can be categorized into non-scheduled banks and

scheduled banks. Scheduled banks constitute of commercial banks and co-operative

banks. There are about 67,000 branches of Scheduled banks spread across India. As

far as the present scenario is concerned the Banking Industry in India is going through

a transitional phase.

The Public Sector Banks (PSBs), which are the base of the Banking sector in India

account for more than 78 per cent of the total banking industry assets. Unfortunately

they are burdened with excessive Non Performing assets (NPAs), massive manpower

and lack of modern technology. On the other hand the Private Sector Banks are

making tremendous progress. They are leaders in Internet banking, mobile banking,

phone banking, ATMs. As far as foreign banks are concerned they are likely to

succeed in the Indian Banking Industry.

Currently, banking in India is generally fairly mature in terms of supply, product

range and reach-even though reaching rural India still remains a challenge for the

private sector and foreign banks. In terms of quality of assets and capital adequacy,

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 4

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Indian banks are considered to have clean, strong and transparent balance sheets

relative to other banks in comparable economies in its region. The Reserve Bank of

India is an autonomous body, with minimal pressure from the government. The stated

policy of the Bank on the Indian Rupee is to manage volatility but without any fixed

exchange rate-and this has mostly been true.

With the growth in the Indian economy expected to be strong for quite some time-

especially in its services sector-the demand for banking services, especially retail

banking, mortgages and investment services are expected to be strong. One may also

expect Mergers &Acquisitions, takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its

stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the first time an

investor has been allowed to hold more than 5% in a private sector bank since the RBI

announced norms in 2005 that any stake exceeding 5% in the private sector banks

would need to be vetted by them.

Currently, India has 88 scheduled commercial banks (SCBs) - 28 public sector banks

(that is with the Government of India holding a stake), 29 private banks (these do not

have government stake; they may be publicly listed and traded on stock exchanges)

and 31 foreign banks. They have a combined network of over 53,000 branches and

17,000 ATMs. According to a report by ICRA Limited, a rating agency, the public

sector banks hold over 75 percent of total assets of the banking industry, with the

private and foreign banks holding 18.2% and 6.5% respectively.

The policy makers, which comprise the Reserve Bank of India (RBI), Ministry of

Finance and related government and financial sector regulatory entities, have made

several notable efforts to improve regulation in the sector. The sector now compares

favorably with banking sectors in the region on metrics like growth, profitability and

non-performing assets (NPAs). Indian banks have compared favorably on growth,

asset quality and profitability with other regional banks over the last few years.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 5

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

The banking index has grown at a compounded annual rate of over 51 per cent since

April 2001 as compared to a 27 per cent growth in the market index for the same

period. The interplay between policy and regulatory interventions and management

strategies will determine the performance of Indian banking over the next few years.

Management success will be determined on three fronts:

i. Fundamentally upgrading organizational capability to stay in tune with the

changing market

ii. Adopting value-creating M&A as an avenue for growth

iii. Continually innovating to develop new business models to access untapped

opportunities

Opportunities and Challenges for the Players

The bar for what it means to be a successful player in the sector has been raised. Four

challenges must be addressed before success can be achieved.

i. The market is seeing discontinuous growth driven by new products and

services that include opportunities in credit cards, consumer finance and

wealth management on the retail side, and in fee-based income and investment

banking on the wholesale banking side. These require new skills in sales &

marketing, credit and operations

ii. Banks will no longer enjoy windfall treasury gains that the decade-long

secular decline in interest rates provided

iii. With increased interest in India, competition from foreign banks will only

intensify

iv. Given the demographic shifts resulting from changes in age profile and

household income, consumers will increasingly demand enhanced institutional

capabilities and service levels from banks

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 6

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

COMPANY PROFILE

Union Bank of India, a public sector bank was incorporated in 1919.After the

inauguration by father of the nation “Mahatma Gandhi” bank has travelled a long

successful journey of 88 yrs of banking. Union Bank of India is committed to

maintain its identity as a leading innovative commercial Bank, alive to the changing

needs of the society. Union Bank has offered vast and varied services to its clientele

taking care of their needs. Today, with its efficient customer service, consistent

profitability & growth, adoption of new technologies and value added services, Union

Bank truly lives up to the image of, “GOOD PEOPLE TO BANK WITH”.

The key business areas of the bank are retail banking, international banking, corporate

banking & treasury. As Retail banking is growing very fast in Indian banking industry

union bank of India is also showing strong growth in this sector. The bank provide

housing, retailing trade, automobile, consumer, education and other personal loans

and deposits services such as fixed, saving and demand deposits for the valuable

clients. The bank has increased foreign exchange turnover from 361.02 bn in 2004-05

to408.94 bn in 2006-07 with annual growth rate of 13.27%. The corporate banking

sector offers various loan and free based products and services to its small and

medium enterprises, agriculture sector.

To boost SME Segment the bank has set up separate SME cells .the total employee

strength of bank are 25,421.Union bank of India is targeting a 25% growth in its SME

portfolio. The bank SME portfolio in 2005-06 was 6,839 crore and its target in 2006-

07 is 8,540 crore. Union bank of India has made an agreement with SIDBI to provide

loan to SMEs. The bank is converting 32 small scale industry branches to SME

branches. Union bank of India and SIDBI are also in the process of putting up

marketing teams in 15 centers for identifying and appraising SMEs units and lending

them. Union bank of India has a network of more than 2200 branches all over India.

The Bank came out with its Initial Public Offer (IPO) in August 20, 2002 and

government of India holds 55.4% of the bank followed by FII 19.9% & Indian public

hold14.8% of the bank.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 7

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

At the end of September 2011 the Bank achieved total business level of Rs.3,42,856

crore (Rupees Three Lakh Forty two thousand Eight hundred fifty six crore)

The Bank has over the years earned the reputation of being a techno-savvy Bank and

is one of the front runners amongst public sector bank in the field of technology. It is

one of the pioneer public sector banks, which launched Core Banking Solution in

2002. Online Tele banking facility is available to all its Core Banking customers. The

multi facility versatile Internet Banking Solution provides extensive information in

addition to the on line transaction facility to both individuals and corporate banking

with the Core Banking branches of the Bank. In addition to regular banking facilities,

today customer can also avail variety of value added services like cash management

service, insurance, mutual funds, Demat from the Bank.

The Vision Statement

To become the bank of first choice in our chosen area by building beneficial and

lasting relationship with the customers through a process of continuous process.

The Mission Statement

A logical extension of the Vision Statement is the Mission of the Bank, which is

to gain market recognition in the chosen areas.

To build a sizeable market shares in each of the chosen areas of business through

effective strategies in terms of pricing, product packaging and promoting the

product in the market.

To facilitate a process of restructuring of branches to support a greater efficiency

in the retail banking field.

To sustain the mission objective through harnessing technology driven banking

and delivery channels.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 8

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

To promote confidence and commitment among the staff members, to address the

expectations of the customers efficiently and handle technology banking with

ease.

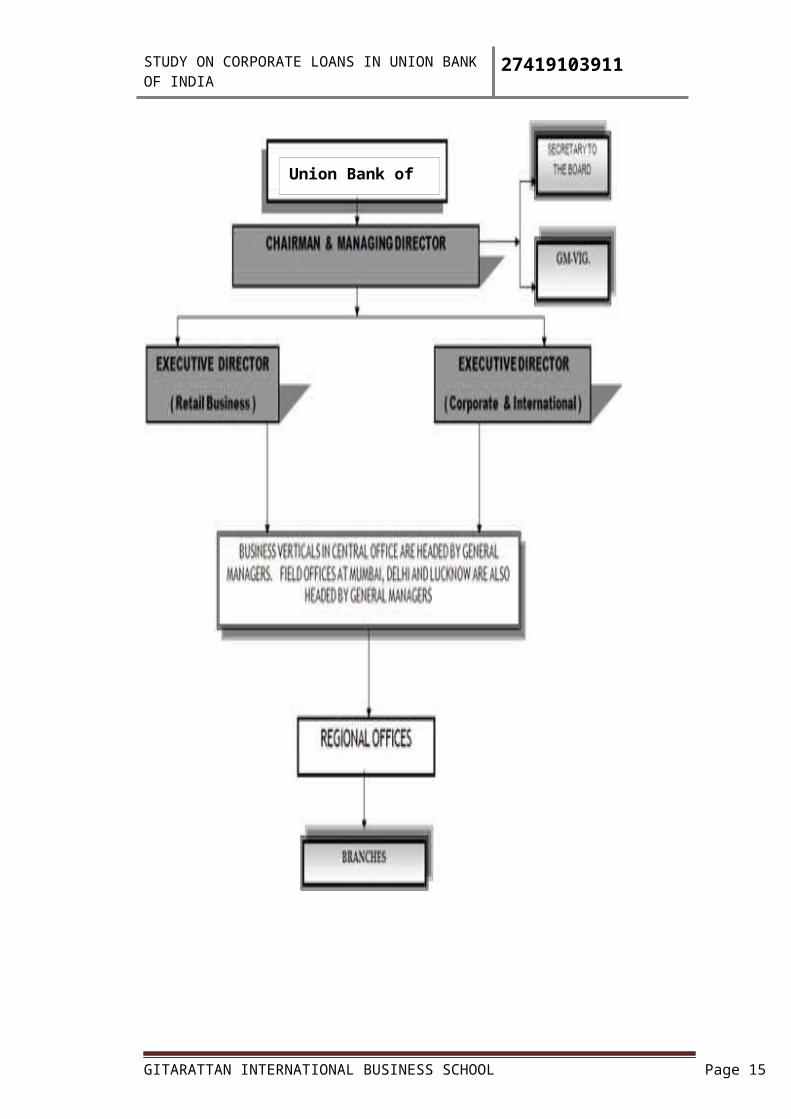

ORGANISATIONAL STRUCTURE OF UBI

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 9

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 10

Union Bank of India

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

CHAPTER 2

THEORITICAL FRAMEWORK

ASSESSMENT OF FUNDS

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 11

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

I. WORKING CAPITAL AND ITS ASSESSMENT

The objective of running any industry is earning profits. An industry will require

funds to acquire “fixed assets” like land and building, plant and machinery,

equipments, vehicles etc… and also to run the business i.e. its day to day operations.

Working capital is defined, as the funds required for carrying the required levels of

current assets to enable the unit to carry on its operations at the expected levels

uninterruptedly. Thus working capital required (WCR) is dependent on

i. The volume of activity (viz. level of operations i.e. Production and Sales)

ii. The activity carried on viz. manufacturing process, product, production

programmed, and the materials and marketing mix.

The purpose of assessing the WC requirement of the industry is to determine how the

total requirements of funds will be met. The two sources for meeting these

requirements are the unit’s long-term sources (like capital and long term borrowings)

and the short-term borrowings from banks. The long-term resources available to the

unit are called the liquid surplus or Net Working Capital (NWC).

It can be explained by visualizing the process of setting up of industry. The unit’s

starts with a certain amount of capital, which will not normally be sufficient, even to

meet the cost of fixed assets. The unit, therefore, arranges for a long-term loan from a

financial institution or a bank towards a part of the cost of fixed assets. From these

two sources after meeting the cost of fixed assets some funds remain to be used for

working capital. This amount is the Net Working Capital or Liquid Surplus and will

be one of the sources of meeting the working capital requirements.

The remaining funds for working capital have to be raised from banks; banks

normally provide working capital finance by way of advantage against stocks and

sundry debtors. Banks, however, do not finance the full amount of funds required for

carrying inventories and receivables: and normally insist on the stake of the enterprise

at every stage, by way of margins.

Bank finance is normally restricted to the amount of funds locked up less a certain

percentage of margins. Margins are imposed with a view to have adequate stake of the

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 12

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

promoter in the business both to ensure his adequate interest in the business and to act

as a protection against any shocks that the business may sustain. The margins

stipulated will depend on various factors like salability, quality, durability, price

fluctuations in the market for the commodity etc. taking into account the total working

capital requirements as assessed earlier, the permissible limit, up to which the bank

finance cab be granted is arrived. While granting working capital advances to a unit, it

will be necessary to ensure that a reasonable proportion of the working capital is met

from the long-term sources viz. liquid surplus. Normally, liquid surplus or net

working capital be at least 25% of the working capital requirement (corresponding to

the benchmark current ratio of 1.33), though this may vary depending on the nature of

industry/ trade and business conditions.

Various methods for assessment of Working Capital are discussed in detail:

1. Operating cycle method :

Any manufacturing activity is characterized by a cycle of operations consisting of

purchase of raw materials for cash, converting them into finished goods and realizing

cash by sale of these finished goods. The time that lapses between cash outlay and

cash realization by sale of finished goods and realization of sundry debtors is known

as length of operating cycle. That is, the operating cycle consists of:

i. Time taken to acquire raw materials and average period for which they

are in store.

ii. Conversion process time

iii. Average period for which finished goods are in store and

iv. Average collection period of receivables (sundry debtors).

Operating Cycle is also called cash-to-cash and indicates how cash is converted into

raw materials, stocks in process, finished goods, bills (receivables) and finally backs

to cash. Working capital is the total cash that is circulating in this cycle. Therefore,

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 13

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

working capital can be turned over or deployed after completing the cycle. Factors,

which influence working capital requirement, are Level of operating expenses and

Length of operating cycle.

Any reduction in either of the both will mean reduction in working capital

requirement or indicate an efficient working capital management.

It can thus be concluded that by improving that by improving the working capital

turnover ratio (i.e. by reducing the length of operating cycle) a better management

(utilization) of working capital results. It is obvious that any reduction in the length of

the operating cycle can be achieved only by better management only by better

management of one or more of the individual phases of the operating cycle period for

which raw materials are in store, conversion process time, period for which finished

goods are in store and collection period of receivables. Looking at whole problem

from another angle, we find that we can set up extremely clear guidelines for working

capital management viz. examining the length of each of the phases of the operating

cycle to assess the scope for reduction in one or more of these phases.

The length of the operating cycle is different from industry to industry and from one

firm to another within the same industry. For instance, the operating cycle of a

pharmaceutical unit would be quite different from one engaged in the manufacture of

machine tools. The operating cycle concept enables to assess working capital need of

each enterprise keeping in view the peculiarities of the industry it is engaged in and its

scale of operations. Operating cycle is an important management tool in decision –

making.

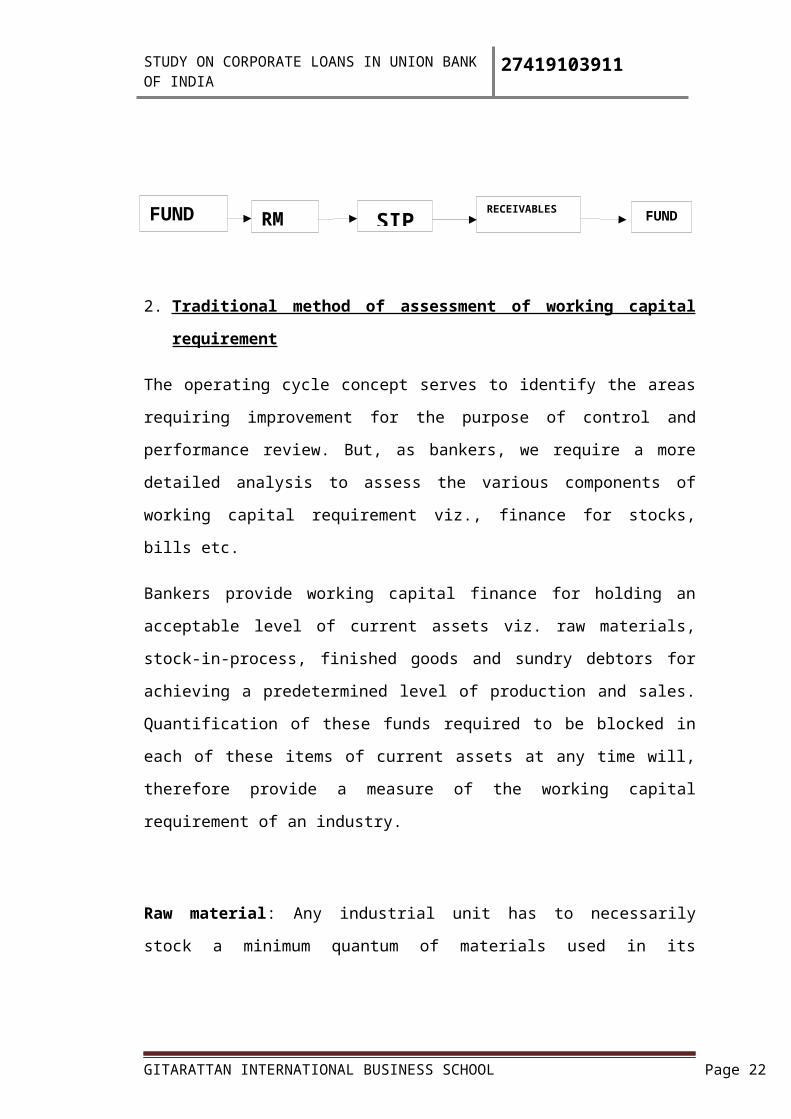

2. Traditional method of assessment of working capital requirement

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 14

RM SIPRECEIVABLES

FUNDFUND

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

The operating cycle concept serves to identify the areas requiring improvement for the

purpose of control and performance review. But, as bankers, we require a more

detailed analysis to assess the various components of working capital requirement

viz., finance for stocks, bills etc.

Bankers provide working capital finance for holding an acceptable level of current

assets viz. raw materials, stock-in-process, finished goods and sundry debtors for

achieving a predetermined level of production and sales. Quantification of these funds

required to be blocked in each of these items of current assets at any time will,

therefore provide a measure of the working capital requirement of an industry.

Raw material: Any industrial unit has to necessarily stock a minimum quantum of

materials used in its production to ensure uninterrupted production. Factors, which

affect or influence the funds requirement for holding raw material, are:

i. Average consumption of raw materials.

ii. Their availability – locally or form places outside, easy availability /

scarcity, number of sources of supply

iii. Time taken to procure raw materials (procurement time or lead time)

iv. Imported or indigenous.

v. Minimum quantity supplied by the market (Minimum Order Quantity

(MOQ)).

vi. Cost of holding stocks (e.g. insurance, storage, interest)

vii. Criticality of the item.

viii. Transport and other charges (Economic Order Quantity (EOQ)).

ix. Availability on credit or against advance payment in cash.

x. Seasonality of the materials.

Stock in process: Barring a few exceptional types of industries, when the raw

material get converted into finished products within few hours, there is normally a

time lag or delay or period of processing only after which the raw materials get

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 15

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

converted into finished product. During this period of processing, the raw materials

get converted into finished goods and expenses are being incurred.

The period of processing may vary from a few hours to a number of months and unit

will be blocked working funds in the stock-in-process during this period. Such funds

blocked in SIP depend on:

i.The processing time

ii.Number of products handled at a time in the process

iii.Average quantities of each product, processed at each time (batch

quantity)

iv.The process technology

v.Number of shifts.

Finished goods: All products manufactured by an industry are not sold immediately.

It will be necessary to stock certain amount of goods pending sale. This stock depends

on:

i. Whether the manufacture is against firm order or against anticipated

order

ii. Supply terms

iii. Minimum quantity that can be dispatched

iv. Transport availability and transport cost

v. Pre-dispatch inspection

vi. Seasonality of goods

vii. Variation in demand

viii. Peak level/ low level of operations

ix. Marketing arrangement- e.g. direct sale to consumers or through

dealers/ wholesalers.

Sundry debtors (receivables): Sales may be affected under three different methods:

i. Against advance payment

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 16

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

ii. Against cash

iii. On credit

iv.

A unit grants trade credit because it expects this investment to be profitable. It would

be in the form of sales expansion and fresh customers or it could be in the form of

retention of existing customers. The extent of credit given by the industry normally

depends upon:

i. Trade practices

ii. Market conditions

iii. Whether it is bulky by the buyer

iv. Seasonality

v. Price advantage

Even in cases where no credit is extended to buyers, the transit time for the goods to

reach the buyer may take some time and till the cash is received back, the unit will

have to be cut out of funds. The period from the time of sale to receipt of funds will

have to be reckoned for the purpose of quantifying the funds blocked in sundry

debtors. Even though the amount of sundry debtors according to the unit’s books will

be on the basis of Sale Price, the actual amount blocked will be only the cost of

production of the materials against which credit has been extended- the difference

being the unit’s profit margin- (which the unit does not obviously have to spend). The

working capital requirement against Sundry Debtors will therefore be computed on

the basis of cost of production (whereas the permissible bank finance will be

computed on basis of sale value since profit margin varies from product to product

and buyer to buyer and cannot be uniformly segregated from the sale value).The

working capital requirement is expressed as so many months’ cost of production.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 17

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Expenses: It is customary in assessing the working capital requirement of industries,

to provide for 1 month’s expenses also. A question might be raised as to why

expenses should be taken separately, whereas at every stage the funds required to be

blocked had been taken into account. This amount is provided merely as a cushion, to

take care of temporary bottlenecks and to enable the unit to meet expenses when they

fall due. Normally 1-month total expenses, direct and indirect, salaries etc. are taken

into account. While computing the working capital requirements of a unit, it will be

necessary to take into account 2 other factors,

i. Is the credit received on purchases- trade credit is a normal practice in

trading circles. The period of such credit received varies from place to

place, material to material and person to person. The amount of credit

received on purchases reduces the working capital funds required by

the unit.

ii. Industries often receive advance against orders placed for their

products. The buyers, in certain cases, have to necessarily give advance

to producers e.g. custom made machinery. Such funds are used for the

working capital of an industry. It can be thus summarized as follows:

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 18

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

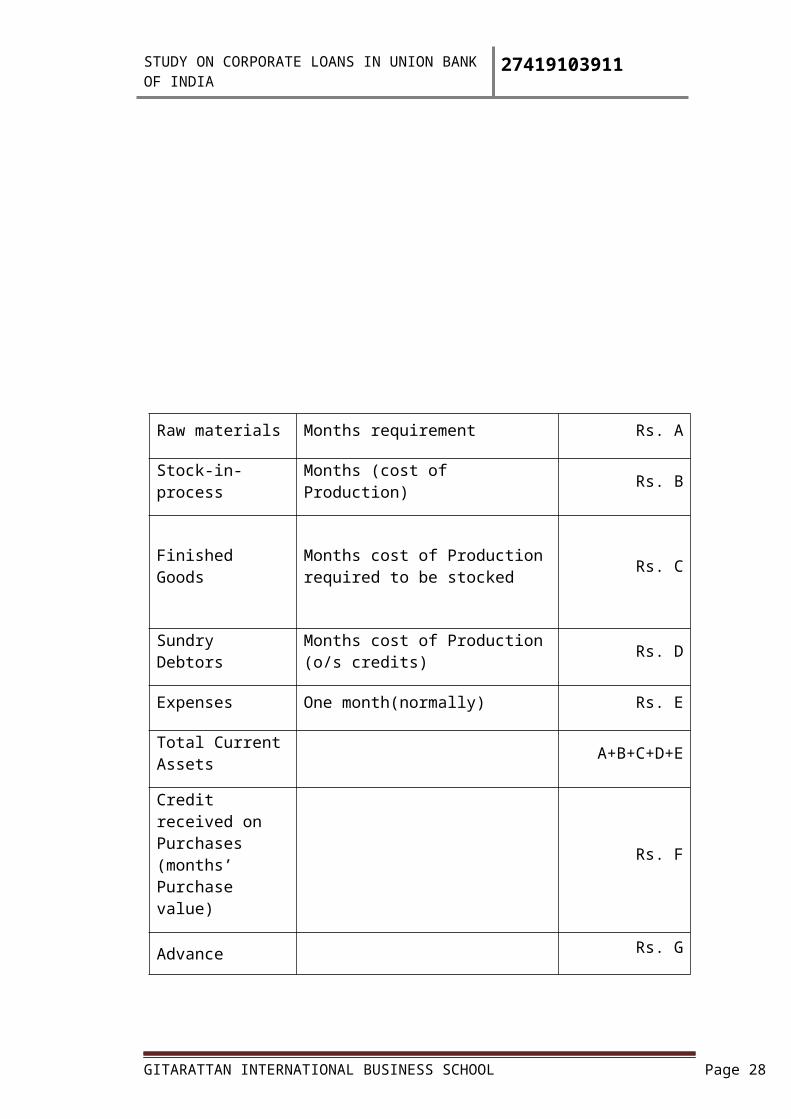

Raw materials Months requirement Rs. A

Stock-in-process Months (cost of Production) Rs. B

Finished GoodsMonths cost of Production required to be stocked

Rs. C

Sundry DebtorsMonths cost of Production (o/s credits)

Rs. D

Expenses One month(normally) Rs. E

Total Current Assets A+B+C+D+E

Credit received on Purchases (months’ Purchase value)

Rs. F

Advance payment on order received

Rs. G

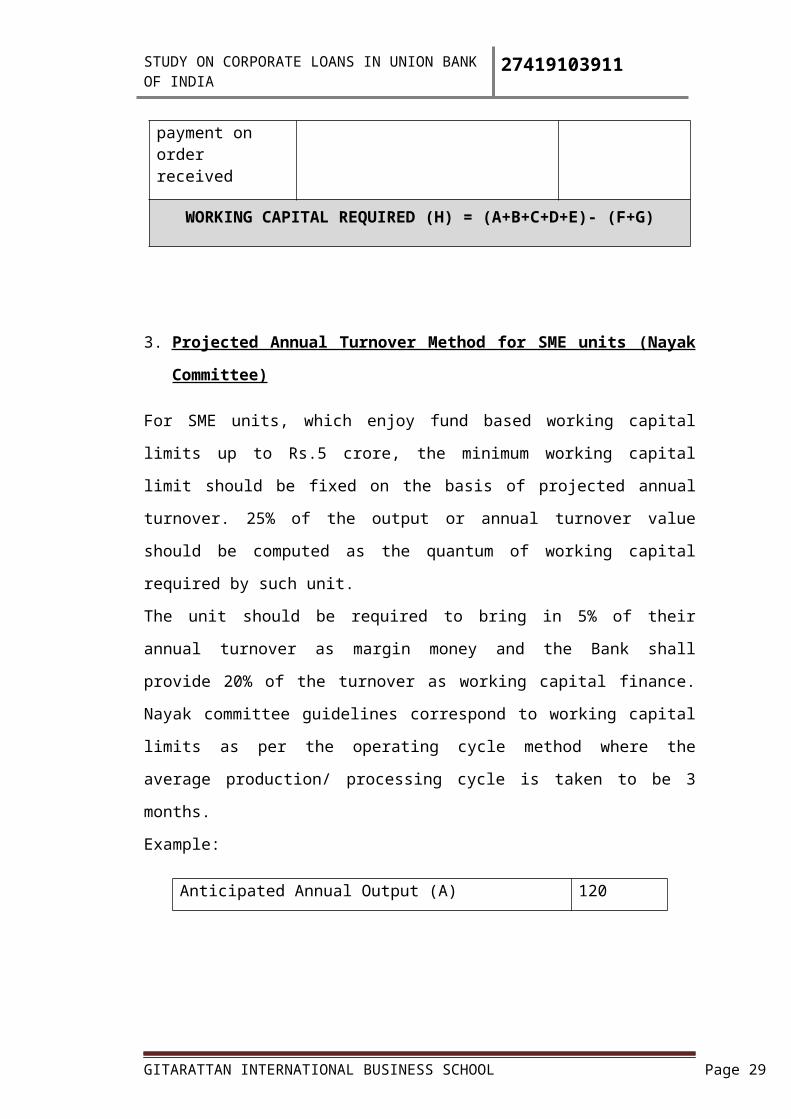

WORKING CAPITAL REQUIRED (H) = (A+B+C+D+E)- (F+G)

3. Projected Annual Turnover Method for SME units (Nayak Committee)

For SME units, which enjoy fund based working capital limits up to Rs.5 crore, the

minimum working capital limit should be fixed on the basis of projected annual

turnover. 25% of the output or annual turnover value should be computed as the

quantum of working capital required by such unit.

The unit should be required to bring in 5% of their annual turnover as margin money

and the Bank shall provide 20% of the turnover as working capital finance. Nayak

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 19

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

committee guidelines correspond to working capital limits as per the operating cycle

method where the average production/ processing cycle is taken to be 3 months.

Example:

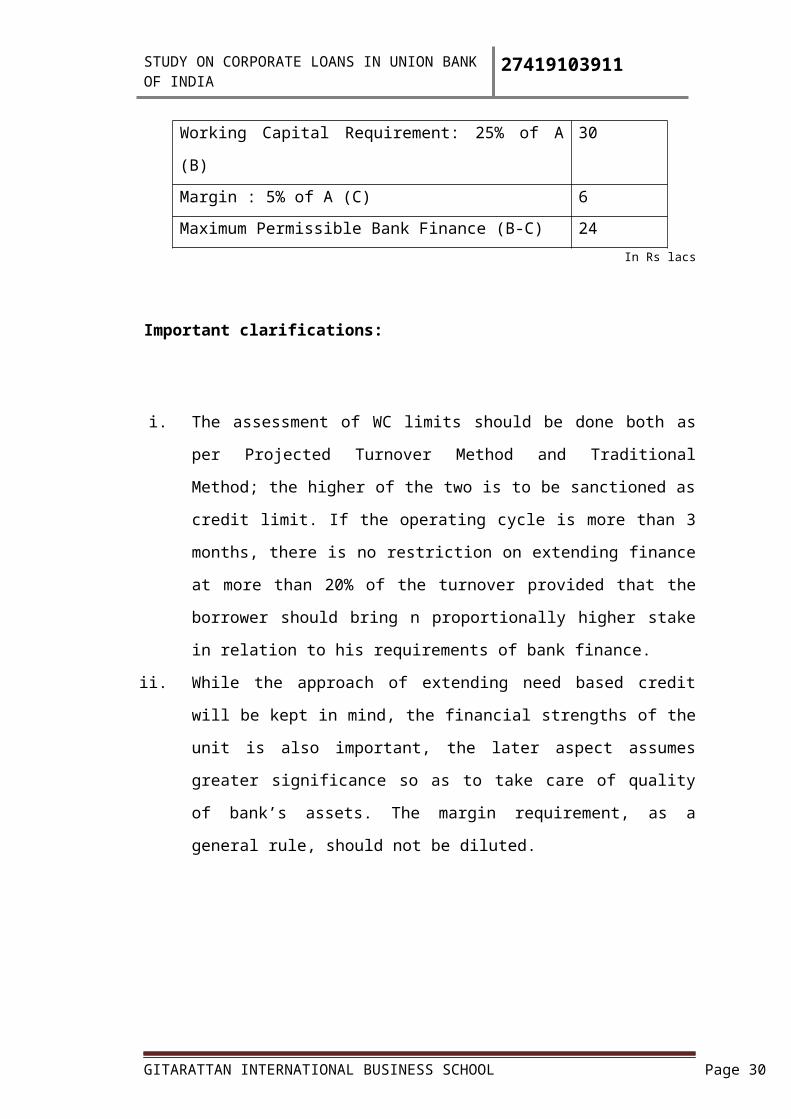

Anticipated Annual Output (A) 120

Working Capital Requirement: 25% of A (B) 30

Margin : 5% of A (C) 6

Maximum Permissible Bank Finance (B-C) 24

In Rs lacs

Important clarifications:

i. The assessment of WC limits should be done both as per Projected Turnover

Method and Traditional Method; the higher of the two is to be sanctioned as

credit limit. If the operating cycle is more than 3 months, there is no restriction

on extending finance at more than 20% of the turnover provided that the

borrower should bring n proportionally higher stake in relation to his

requirements of bank finance.

ii. While the approach of extending need based credit will be kept in mind, the

financial strengths of the unit is also important, the later aspect assumes

greater significance so as to take care of quality of bank’s assets. The margin

requirement, as a general rule, should not be diluted.

4. MPBF Method (Tandon and Chore Committee Recommendations)

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 20

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

The Tandon Committee was appointed to suggest a method for assessing the working

capital requirements and the quantum of bank finance. Since at that time, there was

scarcity of bank’s resources, the Committee was also asked to suggest norms for

carrying current assets in different industries so that bank finance was not drawn more

than the minimum required level. The Committee was also asked to devise an

information system that would provide, periodically, operational data, business

forecasts, production plan and resultant credit needs of units. Chore Committee,

which was appointed later, further refined the approach to working capital

assessment. The MPBF method is the fall out of the recommendations made by

Tandon and Chore Committee. Regarding approach to lending: the committee

suggested three methods for assessment of working capital requirements.

i. First Method of lending: According to this method, Banks would finance up to a

max. of 75% of the working capital gap (WCG= the total current assets - current

liabilities other than bank borrowing) and the balance 25 % of the WCG considered

as margin is to come out of long term source i.e. owned funds and term borrowings.

This will give rise to a minimum current ratio of 1.17:1. The difference of (1.17-1)

represents the borrower’s margin which is popularly known as Net Working Capital

(NWC) of the unit

ii. Second Method of lending: As per the 2nd method Bank will finance maximum up to

75% of total current assets (TCA) & Borrowers has to provide a minimum of 25% of

total current assets as the margin out of long term sources. This will give a minimum

current ratio of 1.33:1

iii. Third Method of lending: Same as 2nd method, but excluding core current assets

from total assets and the core current assets is financed out of long term funds. The

term ‘core current assets’ refers to the absolute minimum level of investment in

current assets, which is required at all times to carry out minimum level of business

activity. The current ratio is further improved i.e. 1.79: 1

Example:

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 21

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

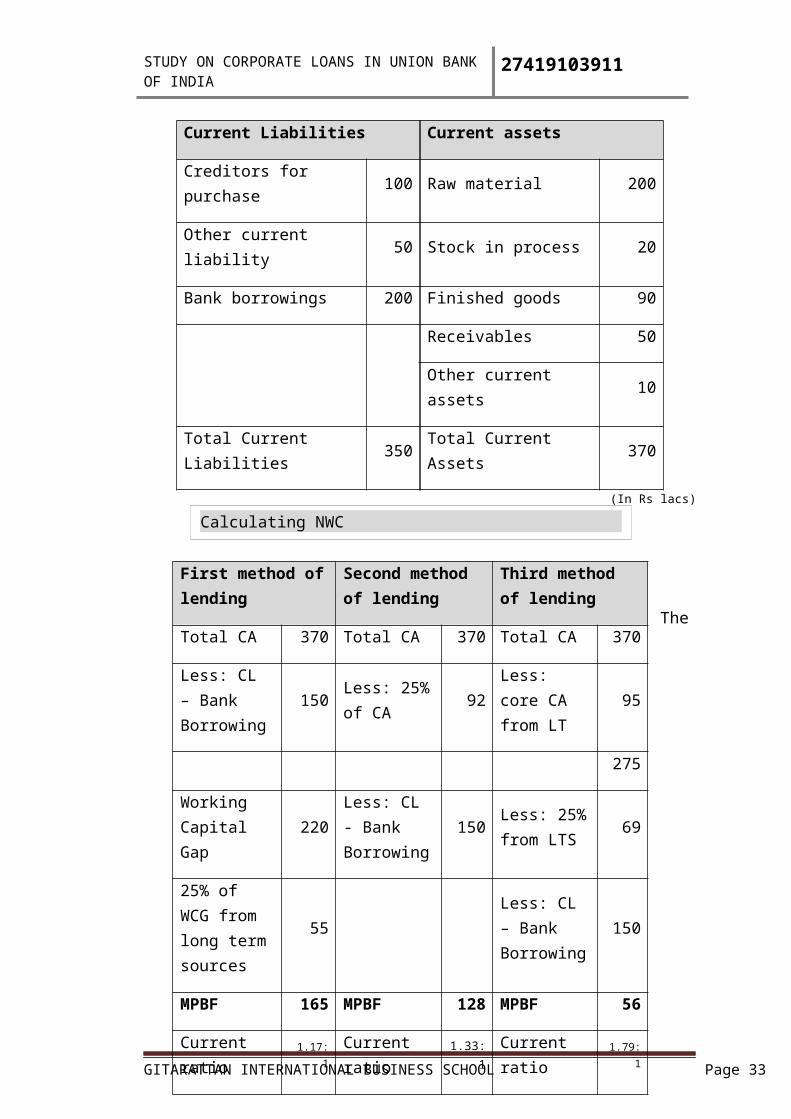

Current Liabilities Current assets

Creditors for purchase 100 Raw material 200

Other current liability 50 Stock in process 20

Bank borrowings 200 Finished goods 90

Receivables 50

Other current assets 10

Total Current Liabilities 350 Total Current Assets 370

(In Rs lacs)

The above example shows that the contribution of margin by the borrower increases

when financing is shifted from First method to Second method which is known to be

stringent from borrower point of view (Third method was not accepted by RBI).

5. Projected Balance Sheet Method (PBS)

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 22

Calculating NWC

First method of lending

Second method of lending

Third method of lending

Total CA 370 Total CA 370 Total CA 370

Less: CL – Bank Borrowing

150Less: 25% of CA

92Less: core CA from LT

95

275

Working Capital Gap

220Less: CL - Bank Borrowing

150Less: 25% from LTS

69

25% of WCG from long term sources

55Less: CL – Bank Borrowing

150

MPBF 165 MPBF 128 MPBF 56

Current ratio 1.17: 1 Current ratio 1.33: 1 Current ratio 1.79: 1

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

The PBS method of assessment will be applicable to all borrowers who are engaged in

manufacturing, services and trading activities who require fund based working capital

finance of Rs. 25 lacs and above. In case of SSI borrowers, who require working

capital credit limit up to Rs. 5 cr, the limit shall be computed on the basis of Nayak

Committee formula as well as that based on production and operating cycle of the unit

and the higher of the two may be sanctioned.. The assessment will be based on the

borrower’s projected balance sheet, the funds flow planned for current/ next year and

examination of the profitability, financial parameters etc. unlike the MPBF method, it

will not be necessary in this method to fix or compute the working capital finance on

the basis of a stipulated minimum level of liquidity (Current Ratio). The working

capital requirement worked out is based on the following:

i. CMA assessment method is continued with certain modifications.

ii. Analysis of the Profit and Loss account, Balance Sheet, Funds flow etc.

for the past periods is done to examine the profitability, financial position,

and financial management etc of the business.

iii. Scrutiny and validation of the projected income and expenses in the

business and projected changes in the financial position (sources and uses

of funds). This is carried out to examine whether these parameters are

acceptable from the angle of liquidity, overall gearing, efficiency of

operations etc. In the PBS method, the borrower’s total business

operations, financial position, management capabilities etc. are analysed

in detail to assess the working capital finance required and to evaluate the

overall risk. The assessment procedure is as follows:

i. Collection of financial information from the borrower

ii. Classification of current assets / current liabilities

iii. Verification of projected levels of inventory/ receivables/ sundry creditors

iv. Evaluation of liquidity in the business operation

v. Validation of bank finance sought

II. ASSESSMENT OF TERM LOANS

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 23

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Term Loans are generally granted to finance capital expenditure, i.e. for acquisition of

land, building and plant and machinery, required for setting up a new industrial

undertaking or expansion/diversification of an existing one and also for acquisition of

movable fixed assets. Term Loans are also given for modernization, renovation, etc.

to improve the product quality or increase the productivity and profitability.

The basic difference between short-term facilities and term loans is that short-term

facilities are granted to meet the gap in the working capital and are intended to be

liquidated by realization of assets, whereas term loans are given for acquisition of

fixed assets and have to be liquidated from the surplus cash generated out of earnings.

They are not intended to be paid out of the sale of the fixed assets given as security

for the loan. This makes it necessary to adopt a different approach in examining the

application of the borrowers for term credits.For the assessment to Term Loan Techno

Economic Feasibility Study is done. The success of a feasibility study is based on the

careful identification and assessment of all of the important issues for business

success. A detailed Project Report is submitted by an entrepreneur, prepared by a

approved agency or a consultancy organization. Such report provides in-depth details

of the project requesting finance. It includes the technical aspects, Managerial Aspect,

the Market Condition and Projected performance of the company. It is necessary for

the appraising officer to cross check the information provided in the report for

determining the worthiness of the project. The feasibility study is a part of Credit

Appraisal process and the same is discussed in the later chapter.

BASEL ACCORD & RISK MANAGEMENT

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 24

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

The Basel accord/accords refer to the banking supervision accords namely Basel I and

Basel II issued by the Basel Committee on Banking Supervision (BCBS).

BASEL I ACCORD

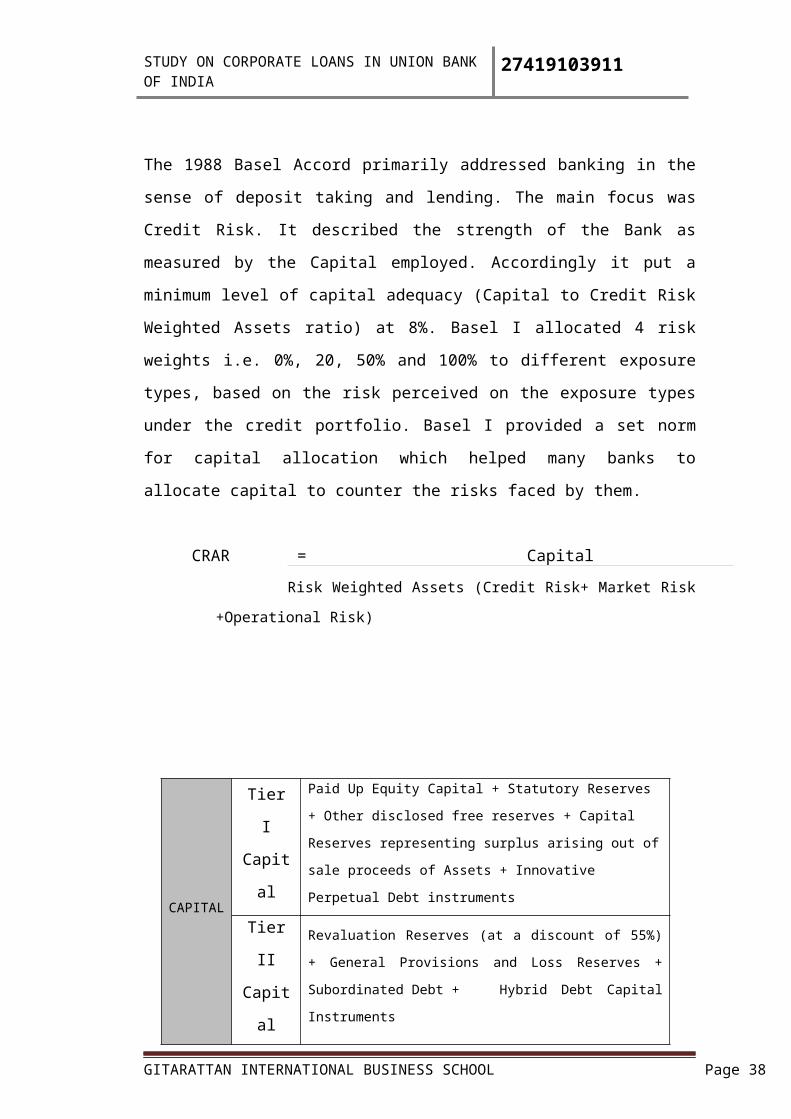

The 1988 Basel Accord primarily addressed banking in the sense of deposit taking

and lending. The main focus was Credit Risk. It described the strength of the Bank as

measured by the Capital employed. Accordingly it put a minimum level of capital

adequacy (Capital to Credit Risk Weighted Assets ratio) at 8%. Basel I allocated 4

risk weights i.e. 0%, 20, 50% and 100% to different exposure types, based on the risk

perceived on the exposure types under the credit portfolio. Basel I provided a set

norm for capital allocation which helped many banks to allocate capital to counter the

risks faced by them.

CRAR = Capital

Risk Weighted Assets (Credit Risk+ Market Risk +Operational Risk)

Risk Weighted Assets

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 25

CAPITAL

Tier I

Capital

Paid Up Equity Capital + Statutory Reserves + Other disclosed

free reserves + Capital Reserves representing surplus arising out

of sale proceeds of Assets + Innovative Perpetual Debt

instruments

Tier II

Capital

Revaluation Reserves (at a discount of 55%) + General Provisions

and Loss Reserves + Subordinated Debt + Hybrid Debt Capital

Instruments

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Basel I introduced the concept of Risk Weighted Assets (RWA). All the assets of a

bank (advances, investments, fixed assets etc.) carry certain amount of risk. In

proportion to the quantum of this risk, bank must maintain capital. Quantification of

risk is done in percentage (0%, 20%, 50% etc.). Exposure when multiplied with these

percentages gives risk based value of assets. These assets are also called Risk

Weighted Assets (RWA).

BASEL II ACCORD

Banking has changed dramatically since the Basel I document of 1988. Advances in

risk management and the increasing complexity of financial activities / instruments

prompted international supervisors to review the appropriateness of regulatory capital

standards under Basel I. To meet this requirement, the Basel I accord was amended

and refined which came out as the Basel II document. The Basel II document is

structured into three parts. Each part is called as a pillar. Thus these three parts

constitute three pillars of Basel II.

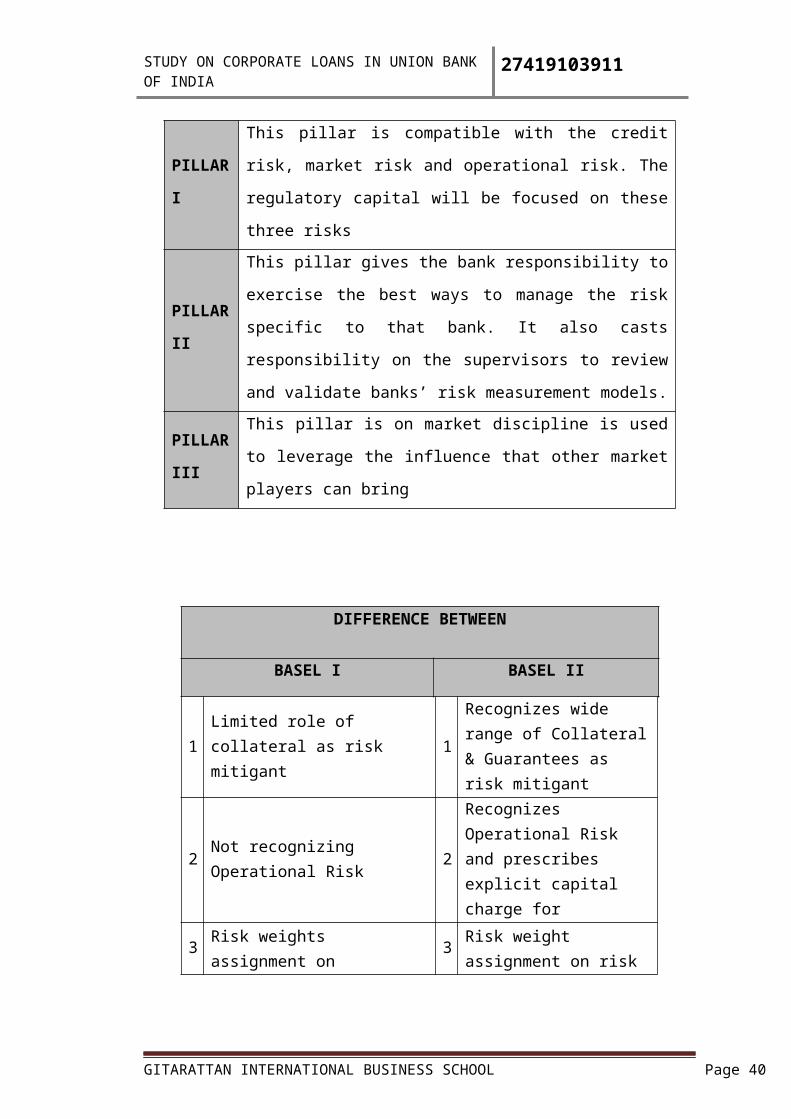

PILLA

R I

This pillar is compatible with the credit risk, market risk and

operational risk. The regulatory capital will be focused on these

three risks

PILLA

R II

This pillar gives the bank responsibility to exercise the best ways

to manage the risk specific to that bank. It also casts

responsibility on the supervisors to review and validate banks’

risk measurement models.

PILLA

R III

This pillar is on market discipline is used to leverage the

influence that other market players can bring

DIFFERENCE BETWEEN

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 26

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

BASEL I BASEL II

1Limited role of collateral as risk mitigant

1Recognizes wide range of Collateral & Guarantees as risk mitigant

2 Not recognizing Operational Risk 2Recognizes Operational Risk and prescribes explicit capital charge for

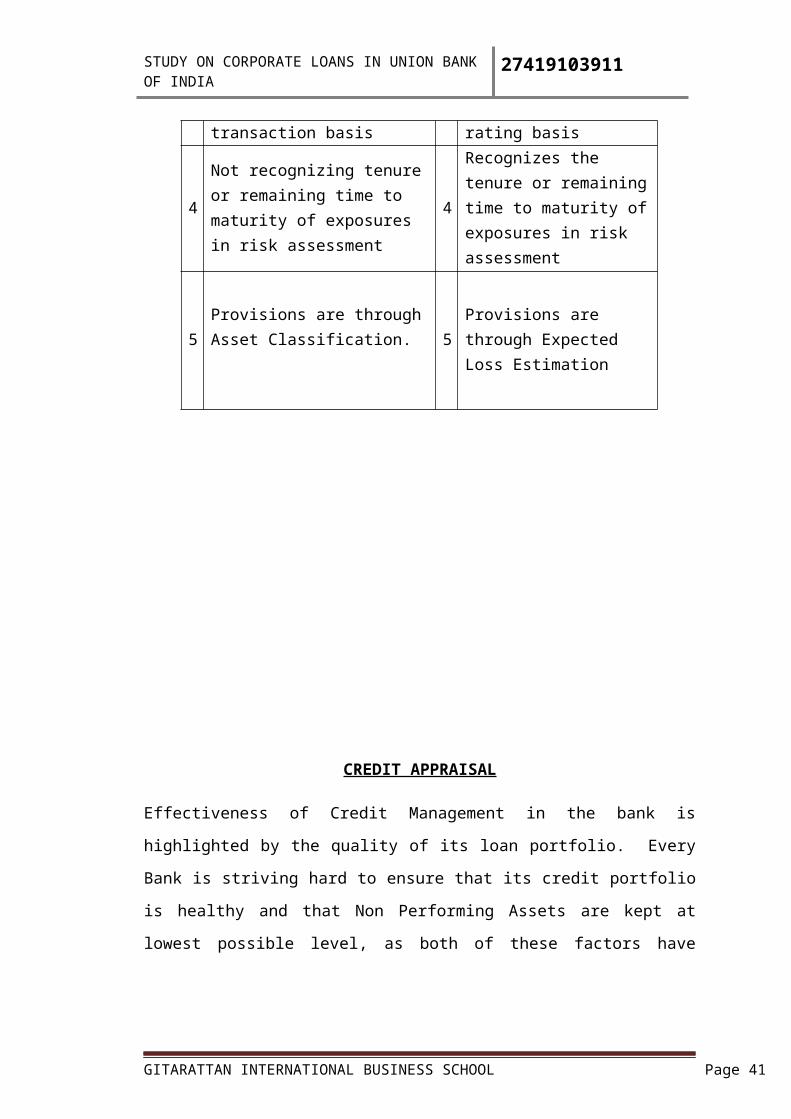

3Risk weights assignment on transaction basis

3Risk weight assignment on risk rating basis

4Not recognizing tenure or remaining time to maturity of exposures in risk assessment

4

Recognizes the tenure or remaining time to maturity of exposures in risk assessment

5Provisions are through Asset Classification. 5

Provisions are through Expected Loss Estimation

CREDIT APPRAISAL

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 27

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Effectiveness of Credit Management in the bank is highlighted by the quality of its

loan portfolio. Every Bank is striving hard to ensure that its credit portfolio is healthy

and that Non Performing Assets are kept at lowest possible level, as both of these

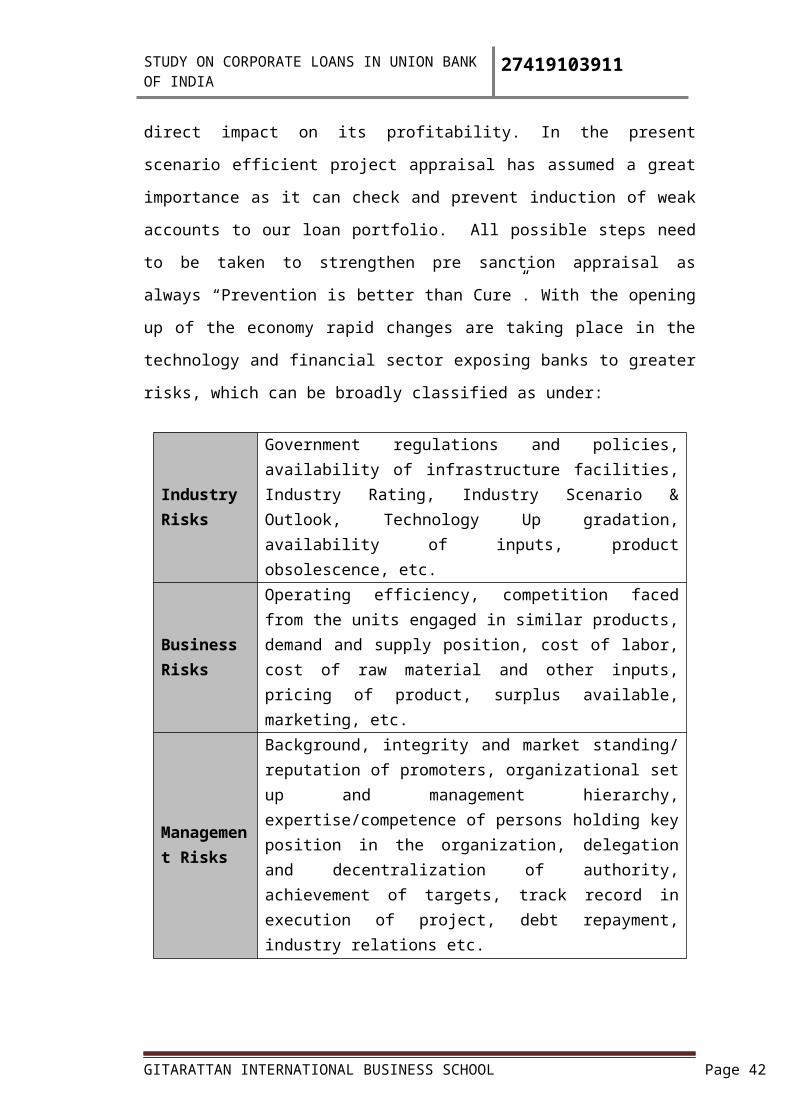

factors have direct impact on its profitability. In the present scenario efficient project

appraisal has assumed a great importance as it can check and prevent induction of

weak accounts to our loan portfolio. All possible steps need to be taken to strengthen

pre sanction appraisal as always “Prevention is better than Cure”. With the opening up

of the economy rapid changes are taking place in the technology and financial sector

exposing banks to greater risks, which can be broadly classified as under:

Industry Risks

Government regulations and policies, availability of infrastructure facilities, Industry Rating, Industry Scenario & Outlook, Technology Up gradation, availability of inputs, product obsolescence, etc.

Business Risks

Operating efficiency, competition faced from the units engaged in similar products, demand and supply position, cost of labor, cost of raw material and other inputs, pricing of product, surplus available, marketing, etc.

Management Risks

Background, integrity and market standing/ reputation of promoters, organizational set up and management hierarchy, expertise/competence of persons holding key position in the organization, delegation and decentralization of authority, achievement of targets, track record in execution of project, debt repayment, industry relations etc.

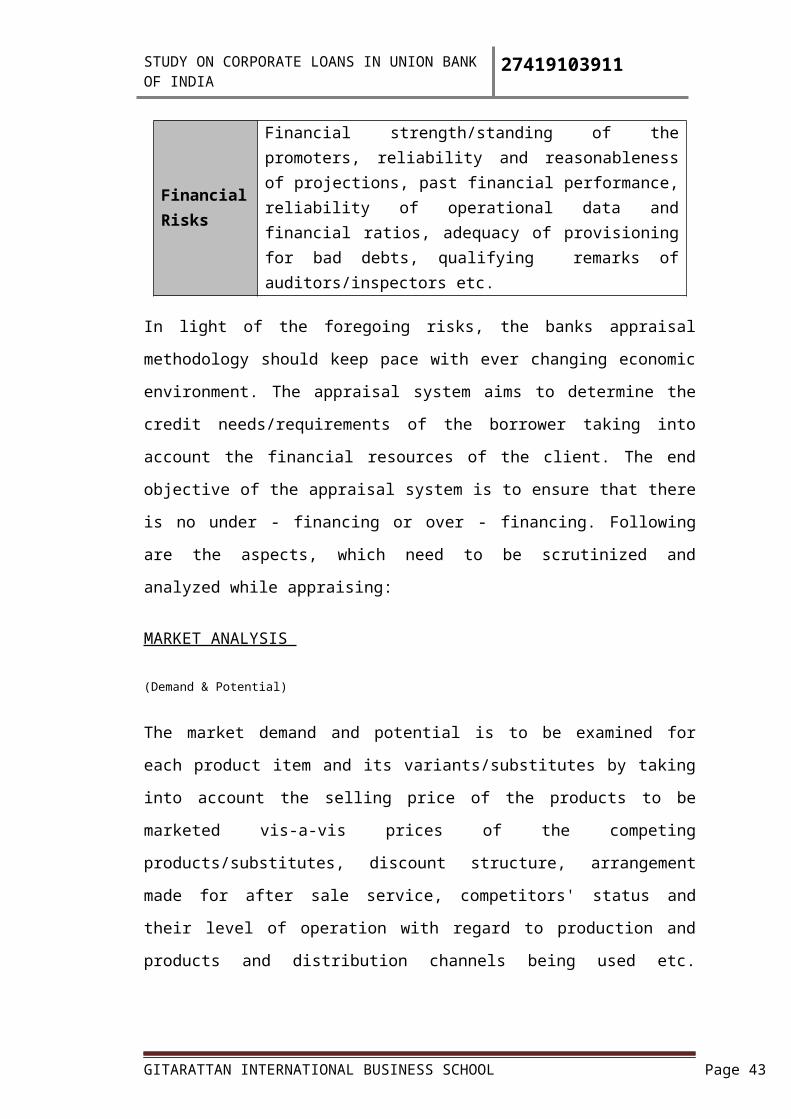

Financial Risks

Financial strength/standing of the promoters, reliability and reasonableness of projections, past financial performance, reliability of operational data and financial ratios, adequacy of provisioning for bad debts, qualifying remarks of auditors/inspectors etc.

In light of the foregoing risks, the banks appraisal methodology should keep pace with

ever changing economic environment. The appraisal system aims to determine the

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 28

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

credit needs/requirements of the borrower taking into account the financial resources

of the client. The end objective of the appraisal system is to ensure that there is no

under - financing or over - financing. Following are the aspects, which need to be

scrutinized and analyzed while appraising:

MARKET ANALYSIS

(Demand & Potential)

The market demand and potential is to be examined for each product item and its

variants/substitutes by taking into account the selling price of the products to be

marketed vis-a-vis prices of the competing products/substitutes, discount structure,

arrangement made for after sale service, competitors' status and their level of

operation with regard to production and products and distribution channels being used

etc. Critical analysis is required regarding size of the market for the product(s) both

local and export, based on the present and expected future demand in relation to

supply position of similar products and availability of the other substitutes as also

consumer preferences, practices, attitudes, requirements etc. Further, the buy-back

arrangements under the foreign collaboration, if any, and influence of Government

policies also needs to be considered for projecting the demand. Competition from

imported goods, Government Import Policy and Import duty structure also need to be

evaluated.

TECHNICAL ANALYSIS

In a dynamic market, the product, its variants and the product-mix proposed to be

manufactured in terms of its quality, quantity, value, application and current

taste/trend requires thorough investigation.

Location and Site

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 29

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Based on the assessment of factors of production, markets, Govt. policies and other

factors, Location (which means the broad area) and Site (which signifies specific plot

of land) selected for the Unit with its advantages and disadvantages, if any, should be

such that overall cost is minimized. It is to be seen that site selected has adequate

availability of infrastructure facilities viz. Power, Water, Transport, Communication,

state of information technology etc. and is in agreement with the Govt. policies.

The adequacy of size of land and building for carrying out its present/proposed

activity with enough scope for accommodating future expansion needs to be judged.

Raw Material

The cost of essential/major raw materials and consumables required their past and

future price trends, quality/properties, their availability on a regular basis,

transportation charges, Govt. policies regarding regulation of supplies and prices

require to be examined in detail. Further, cost of indigenous and imported raw

material, firm arrangements for procurement of the same etc. need to be assessed.

Plant & Machinery, Plant Capacity and Manufacturing Process

The selection of Plant and Machinery proposed to be acquired whether indigenous or

imported has to be in agreement with required plant capacity, principal inputs,

investment outlay and production cost as also with the machinery and equipment

already installed in an existing unit, while for the new unit it is to be examined

whether these are of proven technology as to its performance. The technology used

should be latest and cost effective enabling the unit to compete in the market.

Purchase of reconditioned/old machinery is to be dealt in terms of laid down

guidelines. Compatibility of plant and machinery, particularly, in respect of imported

technology with quality of raw material is to be kept in view. Also plant and

machinery and other equipments needed for various utility services, their supply

position, specification, price and performance as also suppliers' credentials, and in

case of collaboration, collaborators' present and future support requires critical

analysis. Plant capacity and the concept of economic size has a major bearing on the

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 30

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

present and future plans of the entrepreneur(s) and should be related to the availability

of raw material, product demand, product price and technology.

The selected process of manufacturing indicating the adequacy, availability and

suitability of technology to be used along with plant capacity, manufacturing process

needs to studied in detail with capacities at various stages of production being such

that it facilitates optimum utilization and ensures future expansion/ debottlenecking,

as and when required. It is also to be ensured that arrangements are made for

inspection at intermediate/final stages of production for ensuring quality of goods on

successful commencement of production and completion, wherever required.

FINANCIAL ANALYSIS

The aspects which need to be analyzed under this head should include cost of project,

means of financing, cost of production, break-even analysis, financial statements as

also profitability/funds flow projections, financial ratios, sensitivity analysis which

are discussed as under:

Cost of Project & Means of Financing

a. The major cost components of any project are land and building including

transfer, registration and development charges as also plant and machinery,

equipment for auxiliary services, including transportation, insurance, duty,

clearing, loading and unloading charges etc. It also involves consultancy and

know-how expenses which are payable to foreign collaborators or consultants

who are imparting the technical know-how. Recurring annual royalty payment is

not reflected under this head but is accounted for under the profitability

statements. Further, preliminary expenses, such as, cost of incorporation of the

Company, its registration, preparation of feasibility report, market surveys, pre-

operative expenses like salary, travelling, start up expenses, mortgage expenses

incurred before commencement of commercial production also form part of cost

of project. Also included in it are capital issue expenses which can be in the form

of brokerage, commission, advertisement, printing, stationery etc. Finally,

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 31

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

provisions for contingencies to meet any unforeseen expenses, such as, price

escalation or any other expense which have been inadvertently omitted like

margin for working capital requirements required to complete the production

cycle, interest during construction period, etc. are also part of capital cost of

project. It is to be ensured while appraising the project that cost and various

estimates given are realistic and there is no under/over estimation.

b. Besides Bank’s loan, the project cost is normally financed by bringing capital by

the promoters and shareholders in the form of equity, debentures, unsecured long

term loans and deposits raised from friends and relatives which are not repayable

till repayment of Bank's loan. Resources are raised for financing project by

raising term loans from Institutions/Banks which are repayable over a period of

time, deferred term credits secured from suppliers of machinery which are

repayable in installments over a period of time. The above is an illustrative list,

as the promoters have now started raising funds through Euro-issues, Foreign

Currency loans, premium on capital issues, etc. which are sometimes

comparatively cheap means of finance. Subsidies and development loans

provided by the Central/State Government in notified backward districts to attract

entrepreneurs are also means of financing a project. It is to be ascertained that

requirement of finance has been properly tied-up for unhindered implementation

of a project. The financing structure accepted must be in consonance with

generally accepted levels along with adequate Promoters' stake. The

resourcefulness, willingness and capacity of promoter to contribute the same have

also to be investigated. In case of project finance, the promoter/borrower may

bring in upfront his contribution (other than funds to be provided through internal

generation) and the branches should commence its disbursement after the

stipulated funds are brought in by the promoter/borrower. A condition to this

effect should be stipulated by the sanctioning authority in case of project finance,

on case to case basis depending upon the resourcefulness and capacity of the

promoter to contribute the same. It should be ensured that at any point of time,

the promoter’s contribution should not be less than the proportionate share.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 32

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Profitability Statement

The profitability statement which is also known as `Income and Expenditure

Statement' is prepared after considering the net sales figure and details of direct

costs/expenses relating to raw material, wages, power, fuel, consumable stores/spares

and other manufacturing expenses to arrive at a figure of gross profit. Thereafter, all

other expenses like salaries, office expenses, packing, selling/distribution, interest,

depreciation and any other overhead expenses and taxes are taken into account to

arrive at the figure of net profit. The projections of profit/loss are prepared for a

period covering the repayment of term loans. The economic appraisal includes

scrutinizing all the items of cost, and examining the assumptions, if any, to ensure that

these are realistic and achievable. There should not be any optimism or pessimism in

working out profitability projections since even a little change in the product-mix

from non-remunerative to remunerative or vice-versa can distort the picture. While

preparing profitability projections, the past trends of performance in an industry and

other environmental factors influencing the cost and revenue items should also be

considered objectively.

Generally speaking, a unit may be considered as financially viable, progressive and

efficient if it is able to earn enough profits not only to service its debts timely but also

for future development/growth.

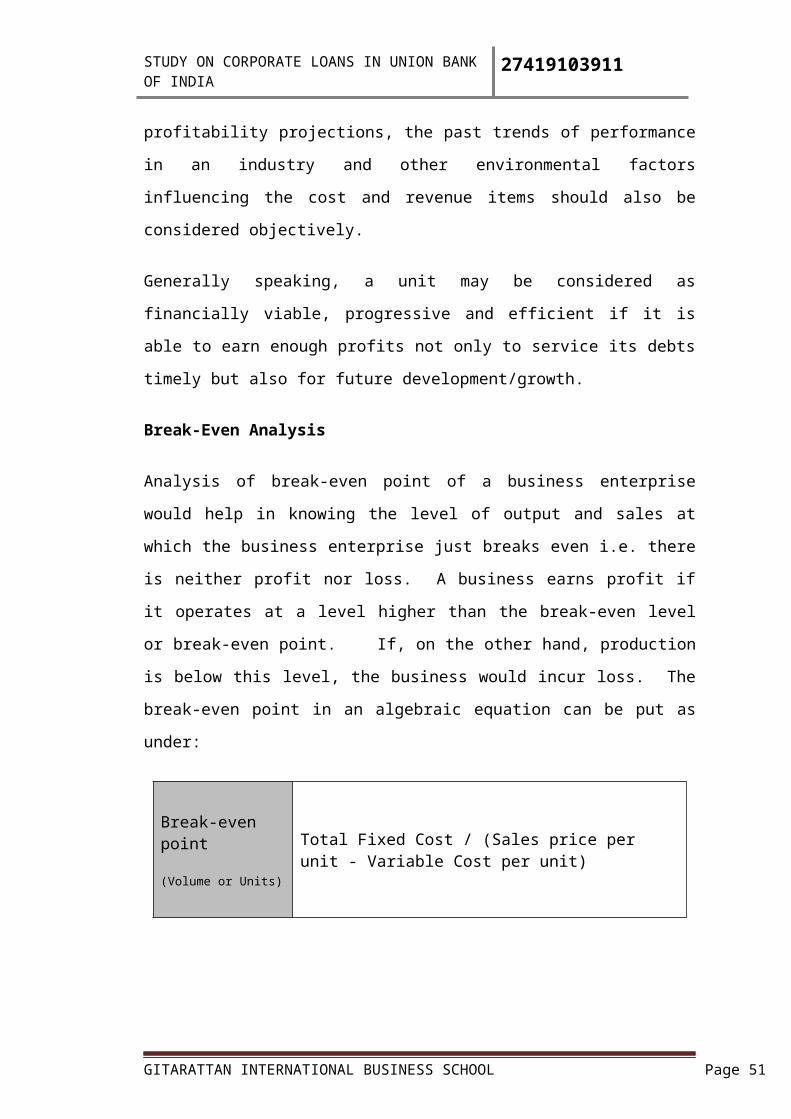

Break-Even Analysis

Analysis of break-even point of a business enterprise would help in knowing the level

of output and sales at which the business enterprise just breaks even i.e. there is

neither profit nor loss. A business earns profit if it operates at a level higher than the

break-even level or break-even point. If, on the other hand, production is below this

level, the business would incur loss. The break-even point in an algebraic equation

can be put as under:

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 33

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

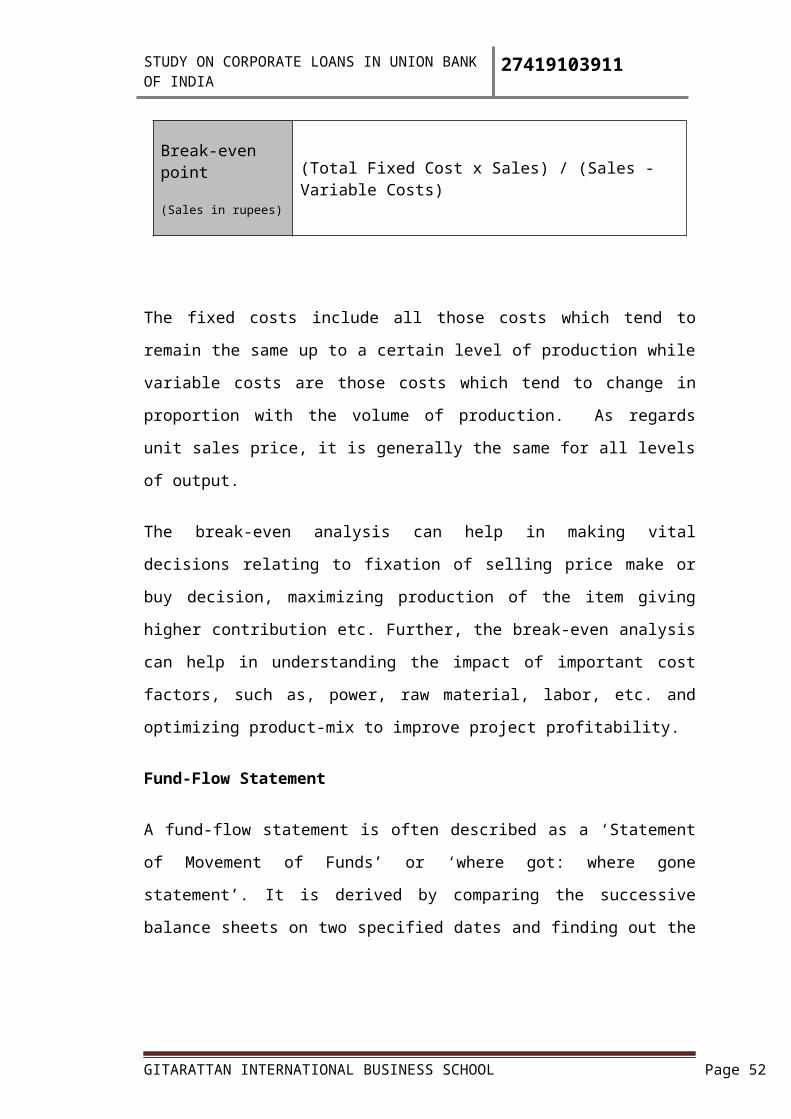

Break-even point

(Volume or Units)

Total Fixed Cost / (Sales price per unit - Variable Cost per unit)

Break-even point

(Sales in rupees)

(Total Fixed Cost x Sales) / (Sales - Variable Costs)

The fixed costs include all those costs which tend to remain the same up to a certain

level of production while variable costs are those costs which tend to change in

proportion with the volume of production. As regards unit sales price, it is generally

the same for all levels of output.

The break-even analysis can help in making vital decisions relating to fixation of

selling price make or buy decision, maximizing production of the item giving higher

contribution etc. Further, the break-even analysis can help in understanding the

impact of important cost factors, such as, power, raw material, labor, etc. and

optimizing product-mix to improve project profitability.

Fund-Flow Statement

A fund-flow statement is often described as a ‘Statement of Movement of Funds’ or

‘where got: where gone statement’. It is derived by comparing the successive balance

sheets on two specified dates and finding out the net changes in the various items

appearing in the balance sheets.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 34

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

A critical analysis of the statement shows the various changes in sources and

applications (uses) of funds to ultimately give the position of net funds available with

the business for repayment of the loans. A projected Fund Flow Statement helps in

answering the under mentioned points.

How much funds will be generated by internal operations/external sources?

How the funds during the period are proposed to be deployed?

Is the business likely to face liquidity problems?

Balance Sheet Projections

The financial appraisal also includes study of projected balance sheet which gives the

position of assets and liabilities of a unit at a particular future date. In other words,

the statement helps to analyze as to what an enterprise owns and what it owes at a

particular point of time. An appraisal of the projected balance sheet data of the unit

would be concerned with whether the projections are realistic looking to various

aspects relating to the same industry.

Financial Ratios

While analyzing the financial aspects of project, it would be advisable to analyze the

important financial ratios over a period of time as it may tell us a lot about a unit's

liquidity position, managements' stake in the business, capacity to service the debts

etc. The financial ratios which are considered important are discussed as under:

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 35

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

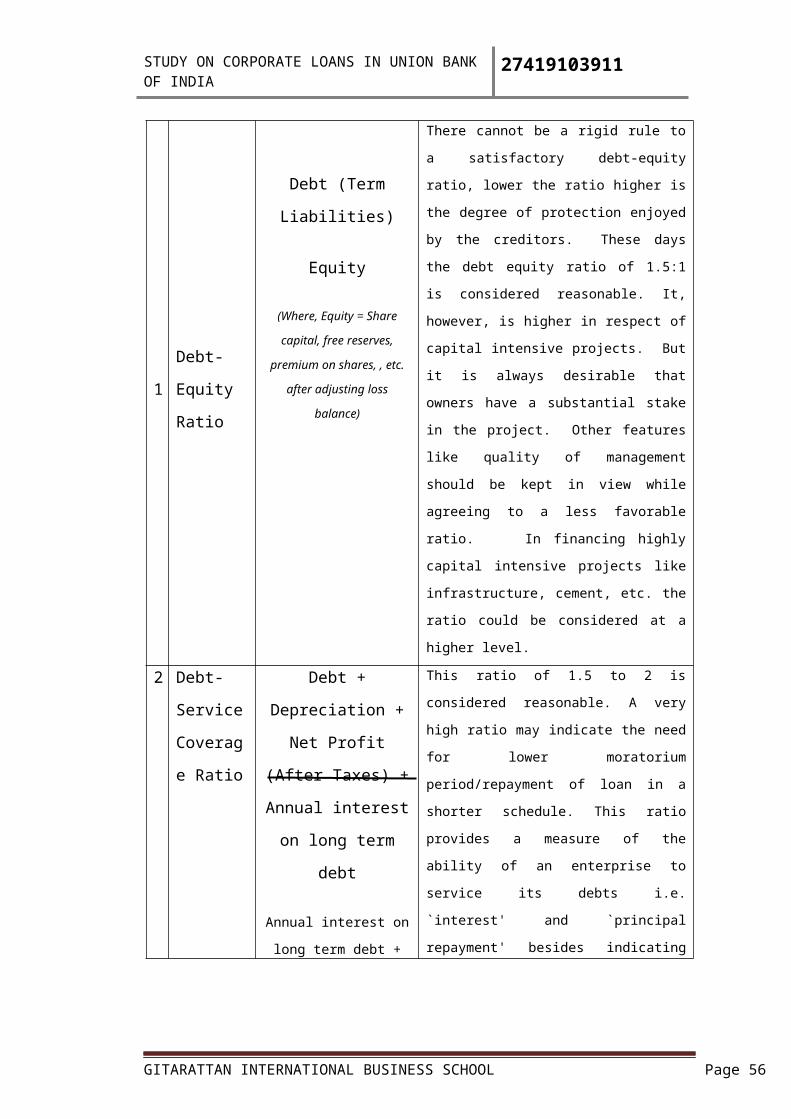

Ratio Formula Remarks

1

Debt-

Equity

Ratio

Debt (Term Liabilities)

Equity

(Where, Equity = Share

capital, free reserves, premium

on shares, , etc. after adjusting

loss balance)

There cannot be a rigid rule to a satisfactory

debt-equity ratio, lower the ratio higher is the

degree of protection enjoyed by the creditors.

These days the debt equity ratio of 1.5:1 is

considered reasonable. It, however, is higher in

respect of capital intensive projects. But it is

always desirable that owners have a substantial

stake in the project. Other features like quality

of management should be kept in view while

agreeing to a less favorable ratio. In financing

highly capital intensive projects like

infrastructure, cement, etc. the ratio could be

considered at a higher level.

2

Debt-

Service

Coverage

Ratio

Debt + Depreciation +

Net Profit (After

Taxes) + Annual

interest on long term

debt

Annual interest on long

term debt + Repayment of

debt

This ratio of 1.5 to 2 is considered reasonable. A

very high ratio may indicate the need for lower

moratorium period/repayment of loan in a

shorter schedule. This ratio provides a measure

of the ability of an enterprise to service its debts

i.e. `interest' and `principal repayment' besides

indicating the margin of safety. The ratio may

vary from industry to industry but has to be

viewed with circumspection when it is less than

1.5.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 36

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

3 TOL /

TNW

Ratio

Tangible Net Worth

(Paid up Capital +

Reserves and Surplus -

Intangible Assets)

Total outside

Liabilities (Total

Liability - Net Worth)

This ratio gives a view of borrower's

capital structure. If the ratio shows a

decreasing trend, it indicates that the

borrower is relying more on his own

funds and less on outside funds and vice

versa

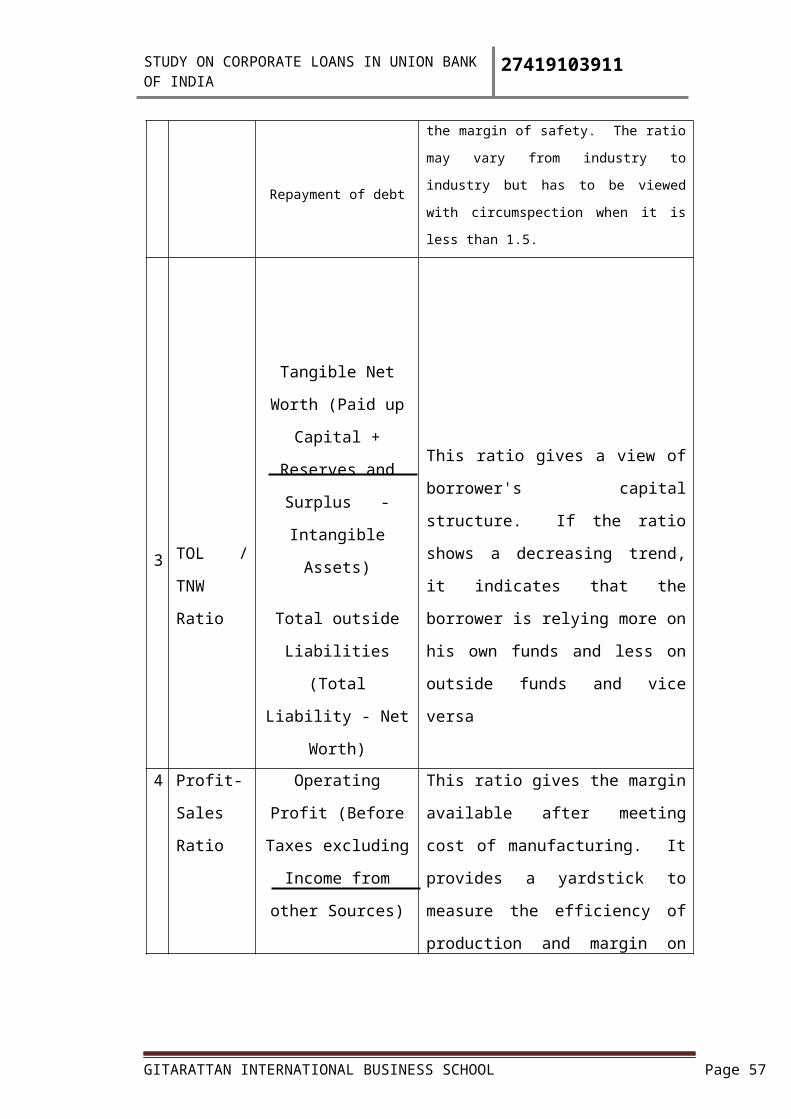

4Profit-

Sales Ratio

Operating Profit

(Before Taxes

excluding Income

from other Sources)

Sales

This ratio gives the margin available

after meeting cost of manufacturing. It

provides a yardstick to measure the

efficiency of production and margin on

sales price i.e. the pricing structure

5

Sales-

Tangible

Assets

Ratio

Sales

Total Assets -

Intangible Assets

This ratio is of a primary importance to

see how best the assets are used. A

rising trend of the ratio reveals that

borrower has been making efficient

utilization of his assets. However,

caution needs to be exercised when

fixed assets are old and depreciated, as

in such cases the ratio tends to be high

because the value of the denominator of

the ratio is very low.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 37

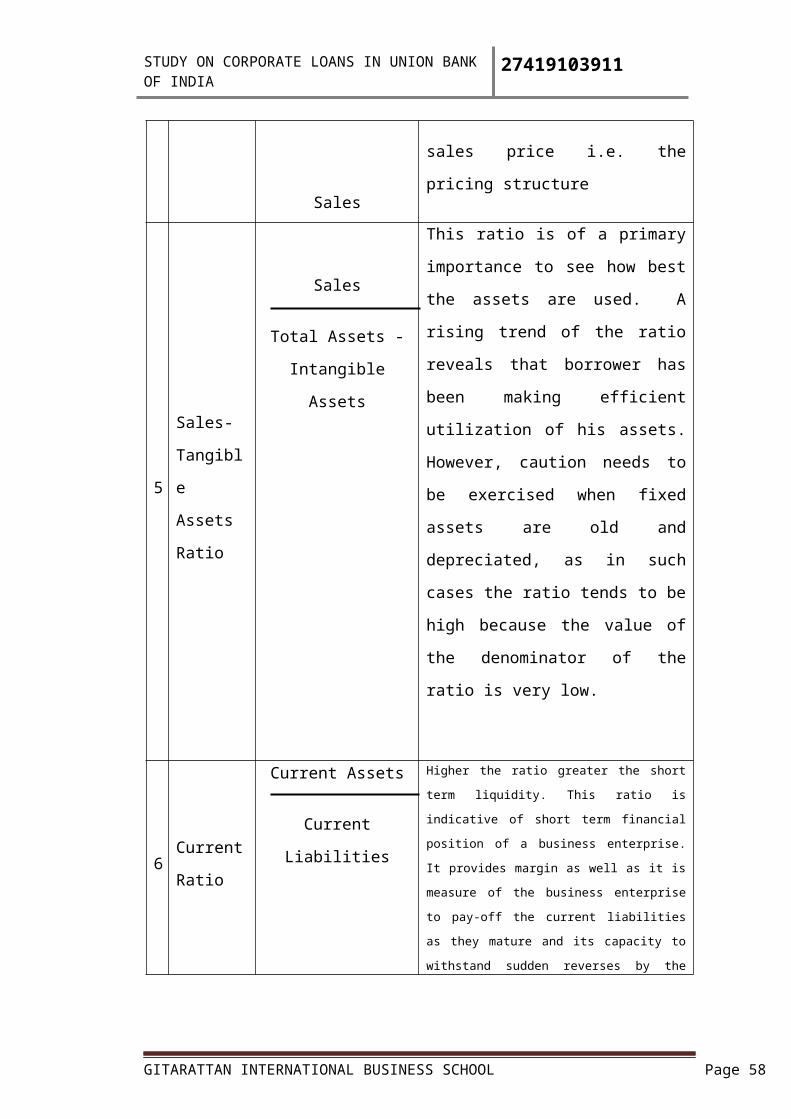

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

6Current

Ratio

Current Assets

Current Liabilities Higher the ratio greater the short term liquidity. This

ratio is indicative of short term financial position of a

business enterprise. It provides margin as well as it is

measure of the business enterprise to pay-off the

current liabilities as they mature and its capacity to

withstand sudden reverses by the strength of its liquid

position. Ratio analysis gives indications; to be made

with reference to overall tendencies and parameters in

relation to the project.

7

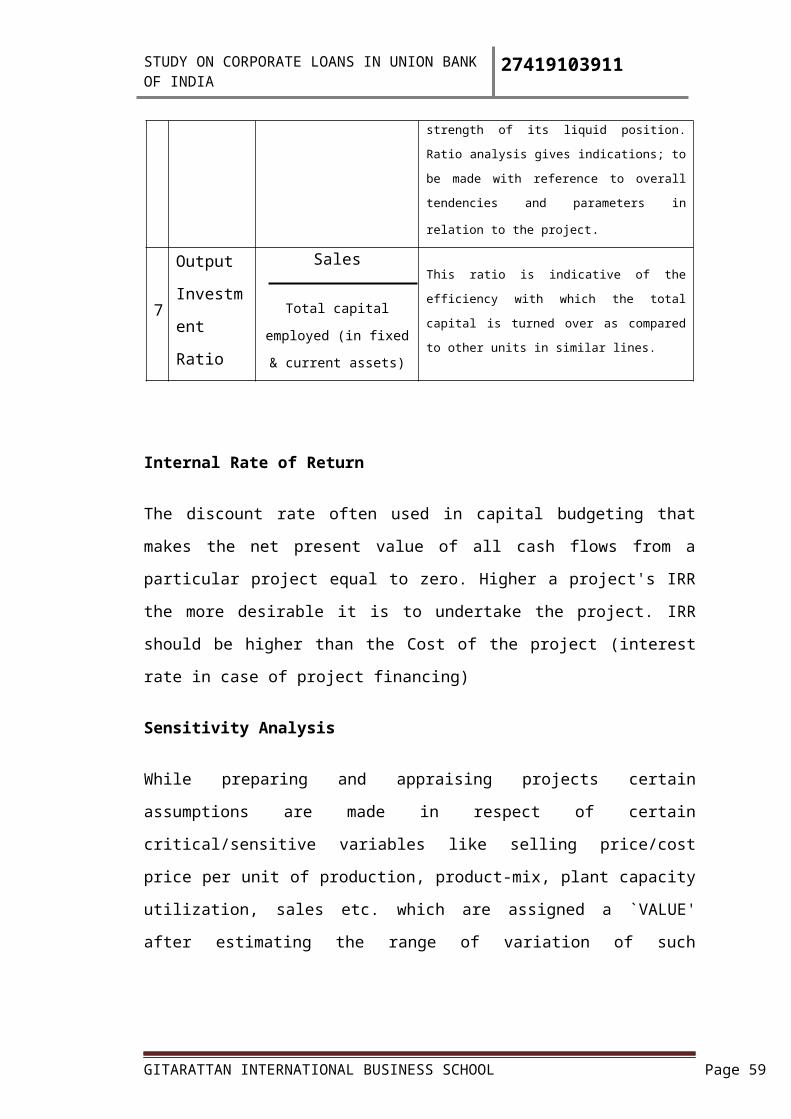

Output

Investment

Ratio

Sales

Total capital employed (in

fixed & current assets)

This ratio is indicative of the efficiency with which

the total capital is turned over as compared to other

units in similar lines.

Internal Rate of Return

The discount rate often used in capital budgeting that makes the net present value of

all cash flows from a particular project equal to zero. Higher a project's IRR the more

desirable it is to undertake the project. IRR should be higher than the Cost of the

project (interest rate in case of project financing)

Sensitivity Analysis

While preparing and appraising projects certain assumptions are made in respect of

certain critical/sensitive variables like selling price/cost price per unit of production,

product-mix, plant capacity utilization, sales etc. which are assigned a `VALUE' after

estimating the range of variation of such variables. The `VALUE' so assumed and

taken into consideration for arriving at the profitability projections is the `MOST

LIKELY VALUE'. Sensitivity Analysis is a systematic approach to reduce the

uncertainties caused by such assumptions made.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 38

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

The Sensitivity Analysis helps in arriving at profitability of the project wherein

critical or sensitive elements are identified which are assigned different values and the

values assigned are both optimistic and pessimistic such as increasing or reducing the

sale price/sale volume, increasing or reducing the cost of inputs etc. and then the

project viability is ascertained. The critical variables can then be thoroughly examined

by generally selecting the pessimistic options so as to make possible improvements in

the project and make it operational on viable lines even in the adverse circumstances.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 39

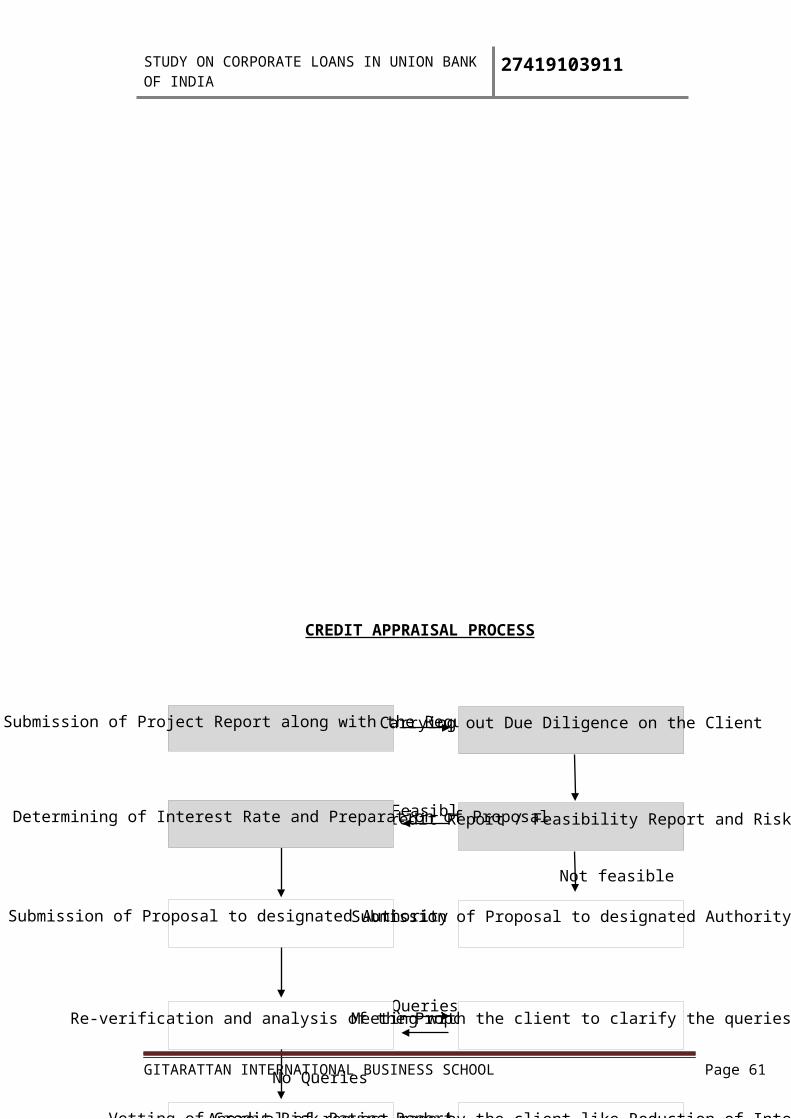

Not feasible

No Queries

Queries

Feasible

Submission of Project Report along with the Request LetterCarrying out Due Diligence on the Client

Submission of Proposal to designated Authority (Circle office)

Re-verification and analysis of the Proposal

Submission of Proposal to designated Authority

Preparing Credit Report / Feasibility Report and Risk RatingDetermining of Interest Rate and Preparation of Proposal

Meeting with the client to clarify the queries

Vetting of Credit Risk Rating ReportApproval of request made by the client like Reduction of Interest Rates etc

Sanction of Proposal on various Terms & Conditions Acknowledgement of Sanction Terms & Condition by the client

Application to comply with Sanction T&C. Execution of Loan DocumentsDisbursement of Sanctioned Amount from the branch office

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

CREDIT APPRAISAL PROCESS

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 40

Procedures at Branch Office Level

Procedures at Circle Office Level

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

LOAN POLICY OF BANK

UBI’s LOAN POLICY

The Credit Management & Risk Policy of the bank at the macro level is an

embodiment of the Bank’s approach to understand, measure and manage the credit

risk and aims at ensuring sustained growth of healthy loan portfolio while dispensing

the credit and managing the risk. This would entail reducing exposures in high risk

areas, emphasizing more on the promising industries / productive sectors/ segments of

the economy, optimizing the return by striking balance between the risk and the return

on assets and striving towards maintaining/improving market share.

BASIC OF THE POLICY

All loan facilities considered only after obtaining loan application from the

borrower and compilation of Confidential Report on them and the guarantor. The

borrowers should have the desired background, experience/expertise to run their

business successfully

Project for which the finance is granted should be technically feasible and

economically/commercially viable i.e. it should be able to generate enough

surplus so as to service the debts within a reasonable period of time.

Cost of the project and means of financing the same should be properly assessed

and tied up. Both, under-financing and over- financing can have an adverse impact

on the successful implementation of the project.

Borrowers should be financially sound, enjoy good market reputation and must

have their stake in the business i.e. they should possess adequate liquid resources

to contribute to the margin requirements.

Loans should be sanctioned by the competent sanctioning authority as per the

delegated loaning powers and should be disbursed only after execution of all the

required documents.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 41

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Projects financed must be closely monitored during implementation stage to avoid

time and cost overruns and thereafter till the adjustment of the bank's loan.

The policy sets out minimum or benchmark lending rate, BPLR = 11 %

The policy lays down norms for takeover of advances from other banks/ financial

institutions

As a matter of policy the bank does not take over any Non-performing Asset

(NPA) from other banks

METHODS OF LENDING

For Working Capital

i. Simplified method linked with turnover

Simplified method based on turnover for assessing working capital finance up to

Rs.2 crore (upto Rs. 5 crore in case of SSI units)

ii. MPBF System

Existing MPBF system with flexible approach shall be followed for units

requiring working capital finance exceeding the above-mentioned amount

iii. Cash Budget System

Cash Budget System shall be followed in Sugar, Tea, Service Sector and Film

Production accounts. It will be our endeavor to introduce the same selectively in

other areas also

For Term Loan

In case of infrastructure/mega projects, proper appraisal will be made by utilizing

the services of specialized / Technical officers.

The term loans with remaining maturity period of above 5 years shall not exceed

50% of the term deposits with remaining maturity period of above 5 years after

taking into account the renewal of term deposits as per the past trend.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 42

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

TYPES OF LENDING ARRANGEMENTS

Business entities can have various types of borrowings arrangements. They are:

One borrower – one bank

One borrower – several banks

One borrower – several banks (with consortium arrangements)

One borrower – several banks ( without consortium arrangements- multiple

banking )

One borrower – several banks (loan syndication)

One Bank

The most familiar amongst the above for smaller loans is the one borrower – one bank

arrangement. Here the borrower confines all his financial dealings with only one

bank. Sometimes, units would prefer to have banking arrangements with more than

one bank on account of the large financial requirement or the resource constraint of

his own banker or due to varying terms & conditions offered by different banks or for

sheer administrative/consortium arrangement are that exposure to an individual

customer is limited & risk is proportionate. The bank is also able to spread his

portfolio. In case of borrowing business entity, it is able to meet its fund requirement

without being constrained by the limited resource of its own banker. Besides this,

consortium arrangement enables participating banks to save manpower & resources

through common appraisal & inspection & sharing credit information.

Consortium lending

When borrowers avails loans from several banks under an arrangement among all the

lending bankers, this lends to a consortium banking lending arrangements. In

consortium lending, several banks pool banking resources & expertise in credit

management together & finance a single borrower with a common appraisal, common

documentation & joint supervision & follow up. The bank taking the highest share of

credits will usually be the leader of consortium. There is no ceiling of banks in a

consortium.

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 43

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Multiple Banking Arrangement

Multiple banking arrangement is one where rules of consortium do not apply & no

inter agreement among banks exists. The borrower avails credit facility from various

banks providing separate securities on different terms & conditions. There is no such

arrangement called ‘multiple banking arrangements’& term is used only to donate the

existence of banking arrangement with more than one bank.

Credit Syndication

A syndicated loan or credit is the arrangement between two or more lending

institutions to provide a borrower a credit facility using common loan documentation.

It is a convenient mode of raising long term funds. The borrowers mandate a lead

manager of his choice to arrange a loan for him. The mandate spells out the terms of

the loan & the mandated bank’s rights & responsibilities. The mandated banker – the

lead manager – prepares an information memorandum & circulates among

prospective lender banks soliciting their participation in the loan. On the basis of the

memorandum & on their own independent evaluation the leading banks take a view

on the proposal. The mandated bank convenes the meeting to discuss the syndicated

strategy relating to coordination, communication & control within the syndication

process & finalizes deal timing, management fees, cost of credit etc. The loan

agreement is signed by all the participating banks. The borrower is required to give

prior notice to the lead manager about loan drawl to enable him to tie up

disbursements with other lending banks.

FEATURES OF SYNDICATED LOANS

Arrangements brings together group of banks

Borrower is not requires to have interface with participating banks, thus easy

& hassle free

Large loans can be raised through syndication by accessing global markets

For the borrower, the competition among the lenders leads to finer terms

Small banks can also have access to large ticket loans & top class credit

appraisal & management

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 44

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

CREDIT RISK RATING

CREDIT RISK

Credit risk means the possibility of loss associated with diminution in the credit

quality of borrowers. In a bank’s portfolio, losses stem from outright default due to

inability or unwillingness of a customer or counter party to meet, commitments in

relation to lending, trading, settlement and other financial transactions.

CREDIT RISK MANAGEMENT SYSTEM IN UBI

A comprehensive credit risk management system, which is in place in the bank,

encompasses the following processes:

Identification of Credit Risk

Measurement of Credit Risk

Grading of Credit Risk

Reporting and analysis of rating related data

Control of Credit Risk

CREDIT RISK IDENTIFICATION

In order to take informed credit decisions, it is necessary to identify the areas of credit

risk in each borrower as well as each industry. Risk Management Division HO, in

coordination with other HO divisions involved in disbursal of credit and also the risk

management departments of various zonal offices identifies these risks areas and

develops necessary tools and processes to measure and monitor the risk.

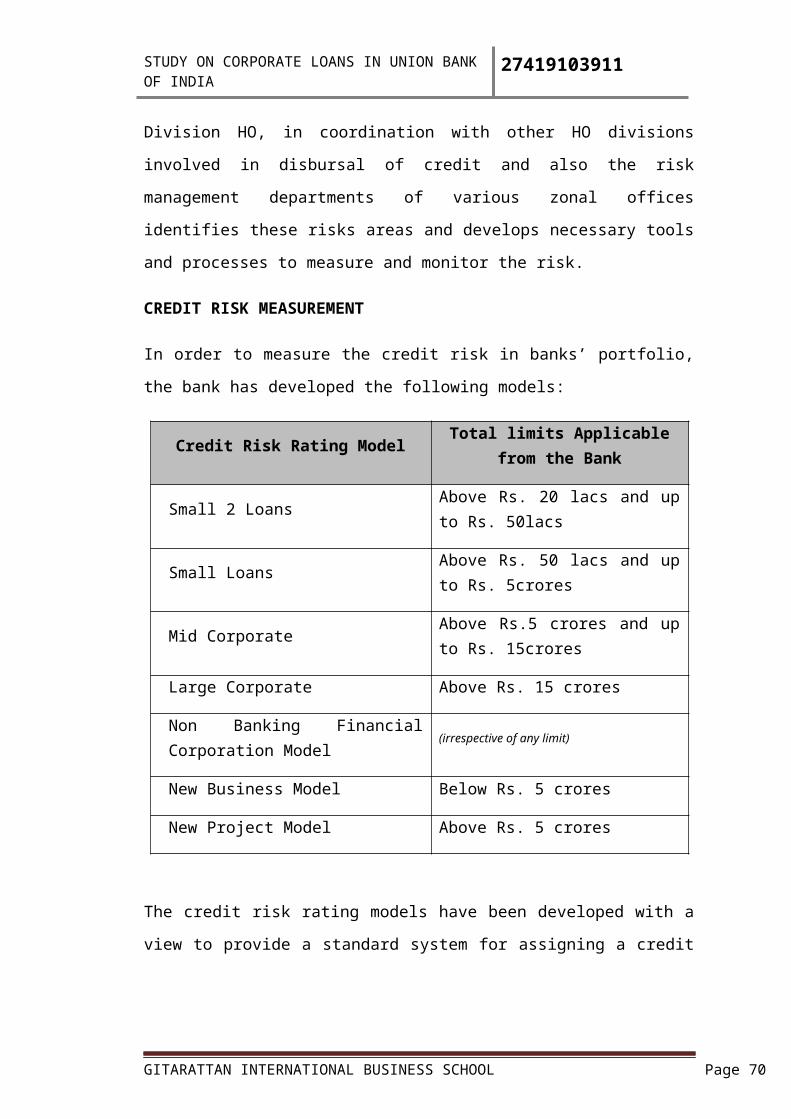

CREDIT RISK MEASUREMENT

In order to measure the credit risk in banks’ portfolio, the bank has developed the

following models:

Credit Risk Rating Model Total limits Applicable from the

GITARATTAN INTERNATIONAL BUSINESS SCHOOL Page 45

STUDY ON CORPORATE LOANS IN UNION BANK OF INDIA 27419103911

Bank

Small 2 LoansAbove Rs. 20 lacs and up to Rs. 50lacs

Small LoansAbove Rs. 50 lacs and up to Rs. 5crores

Mid CorporateAbove Rs.5 crores and up to Rs. 15crores

Large Corporate Above Rs. 15 crores

Non Banking Financial Corporation Model

(irrespective of any limit)