PROJECT FINANCE and TERM LOAN ASSESSMENT Kumar Sachdev... · January 3, 2011 1 PROJECT FINANCE and...

51

January 3, 2011 1 PROJECT FINANCE PROJECT FINANCE and and TERM LOAN ASSESSMENT TERM LOAN ASSESSMENT S. K. Sachdev IDBI Bank Ltd.

Transcript of PROJECT FINANCE and TERM LOAN ASSESSMENT Kumar Sachdev... · January 3, 2011 1 PROJECT FINANCE and...

January 3, 2011 1

PROJECT FINANCE PROJECT FINANCE and and

TERM LOAN ASSESSMENTTERM LOAN ASSESSMENT

S. K. Sachdev

IDBI Bank Ltd.

January 3, 2011 2

During the day………

� Project Financing/Appraisal

� Products of Corporate financing

� Question and answer session

Types of Project

� Green field vs Brown field

� Expansion, Modernisation, Diversification

� Infra vs Non-infra

� Recourse vs Non-recourse

January 3, 2011 3

January 3, 2011 4

PROJECT FINANCEPROJECT FINANCE

� A funding structure that relies on future cashflow from a specific development as theprimary source of repayment, with thatdevelopment’s assets, rights and interestlegally held as collateral security.

� Contrast to conventional corporate lendingwhich looks to the balance sheet and totalbusiness and financial resources of aborrower as the source of repayment.

Pre-requisite if Project Appraisal

� Working Knowledge of Industry

� Industry Dynamics and economics

� Requirement and source of inputs

� Manufacturing process

� Business Environment

� Manufacturing / Operating Cycle

January 3, 2011 5

Pre-requisite if Project Appraisal

� Government Policy Guidelines and updates

� Institutional Norms

� Accounting Concepts and Policies

� Working Knowledge of Spreadsheets and Word Processing Applications

� Effective Communication

� Ability to identify critical elements from general ones, mitigate obvious risks so as to improve viability

January 3, 2011 6

January 3, 2011 7

APPRAISAL – why?

� Project returns are spread over time� Each variable effecting NPV is subject to highlevel of uncertainty.

� Information and data needed for moreaccurate forecasts are costly to acquire.

� Need to reduce the likelihood to undertake a“BAD” project while not failing to accept a“GOOD” project.

� Ultimately leads to Risk Assessment and“credit delivery” decision.

January 3, 2011 8

“Viability” is in the eyes of the beholder

� Appraisal from whose point of view?

� What are the “viability parameters” that needs to be achieved?

� In the range of possibilities:� Best Case scenario

� Worst Case scenario

� Most likely scenario

January 3, 2011 9

APPRAISAL – WHY ?

� Extend assistance to “viable” [“bankable”] projects

� Viability means -

� Ability to service debt

� Ability to service equity

� Co. should earn for itself

� Allocate scarce resources

� Optimally

January 3, 2011 10

STEPS IN APPRAISAL PROCESS

� Receipt of enquiry/application

� Initial screening-accept/reject

� If accepted,conduct detailed appraisal for credit decision

� Issue letter of intent (LoI) [“The Offer”]

January 3, 2011 11

PROJECT APPRAISAL

� Broad areas of appraisal

� Promoters & management

� Market analysis

� Technical analysis

� Financial analysis

� Risk assessment and contracting [“covenant”]

January 3, 2011 12

PROMOTER ASSESSMENT

� Most subjective aspect

� Types of promoters

� Existing companies

� First generation

� Government/PSUs

� Foreign promoters

� Promoters vs Management

January 3, 2011 13

PROMOTER ASSESSMENT

� Existing companies

� Track record of performance

� Analysis of B/S and P& L A/c

� Dealings with FI’s/banks

� Ability to bring in required funds

January 3, 2011 14

PROMOTER ASSESSMENT

� First generation � Individual promoters (limited tools)

� IT/Wealth Tax returns

� Bankers’ report

� Qualifications/past experience

� Technical partner

January 3, 2011 15

MANAGEMENT ASPECTS

� Quality of the Board

� Promoter Directors vs. Independent Directors

� Project execution team

� Management structure during operation

� Chief executive

� Other functional heads

January 3, 2011 16

MARKET ASSESSMENT

� Nature of the product� Applications� Competing products

� Industry structure� Existing & projected unsatisfied demand� Supply scenario & competitors� Product obsolescence� Selling arrangements

January 3, 2011 17

TECHNICAL ASPECTS

� Various areas covered are� Locational aspects

� Process

� Technical arrangements

� Raw materials

� Utilities

� Environmental factors

� Manpower

� Implementation schedule

January 3, 2011 18

LOCATION

� Location� Proximity to markets [e.g perishable products]� Proximity to raw material supplies [resource based, imported raw material]

� Availability of labour [quality, quantity, cost, relations]

� Availability of utilities� Effluent disposal� Other infrastructure [power, transportation, water etc]

� Governmental Policies [restrictions and sops]

January 3, 2011 19

LOCATION -SITE

� Requirement of land area to be assessed based on - Plant layout- Expansion needs

� Soil test report� Load bearing capacity� Extent of development/leveling� Obtaining utility connections [costs] [transmission lines, railway sidings, feeder road, water, effluent disposal]

January 3, 2011 20

PROCESS

� Has relationship to capacity, inputs and product-mix

� Latest and proven

� Cost effective – both from initial investment and production cost

� Alternate processes

� Advantages w.r.to- Cost- Consumption of inputs- Ease of operation/Upgradeable- Pollution aspects

January 3, 2011 21

PROCESS

� New process or processes used first time in the country

� Background of the process know-how supplier

- Financial status

- Technical capability

- Reference plants

� Ad hoc committee of advisers

January 3, 2011 22

TECHNICAL ARRANGEMENTS

� Technical collaboration

� Licensor of know-how/basic engineering

� Patents

� Plant & machinery

� Guarantees/warrantees – Collaborator/ P&M supplier /Detailed engg contractor

� Approach to “force majeure” conditions

� Assignment in case of ownership

� Termination

January 3, 2011 23

TECHNICAL ARRANGEMENTS

� Technical know-how agreement

� Supply/vetting of basic engineering

� Guarantees

� Liquidated damages for non-performance

� Training of personnel

� Royalty

� Indemnity

January 3, 2011 24

TECHNICAL ARRANGEMENTS

� Size of plant

� Minimum economic size which varies with change in technology, products, pricing, demand etc.

� Plant & Machinery

� Suitability & adequacy [transporting, trained personnel availability]

� Reasonableness of cost

� Reputation of suppliers

� Line balancing

� Spare parts

January 3, 2011 25

RAW MATERIALS

� Raw materials & quantity� Sustained availability

� Imported /indigenous� Major suppliers

� Prices of raw material� Price volatility� Past trends� Duties

� Arrangements for supply.

January 3, 2011 26

UTILITIES

� Power supply

� Water

� Labour

� Requirement/availability

� Arrangements

� Measures to augment supplies/fall back [power?]

January 3, 2011 27

EFFLUENT DISPOSAL

� Liquid, gaseous & solid effluents

� Pollutant load needs to be assessed

� Depending on the volume and quality of the effluent suitable treatment measures are designed.

� Environmental impact assessment study

� Clearances from statutory authorities

January 3, 2011 28

IMPLEMENTATION SCHEDULE

� List down all activities from “planning” to “COD”

� Time required for each step

� Scheduling of activities - PERT/CPM

� Resource required [impact of more or less resource]

� Schedule of machinery supply

� Experience of similar plants

January 3, 2011 29

IMPLEMENTATION SCHEDULE

� Consequences of delay

� Increase in project cost

� Funding overrun

� Effect on viability

� Loss of market

� Confidence level of FIs

January 3, 2011 30

PROJECT COST ESTIMATION

� Major heads are

� Land and site development

� Buildings/civil works

� Plant & machinery

� Imported

� Indigenous

� Tech. Know-how fees

January 3, 2011 31

PROJECT COST ESTIMATION

� Expense on foreign technicians & training

� Misc.fixed assets

� Prel. & Pre-op expenses

� Contingency

� Margin money for working capital

Margin Money for Working Capital

Current Assets

� Raw Materials (Imp. - 3 mths/Ind -1 mth)

� Work-in-process( 1 process cycle time)

� Finished goods (1 wk to 1 mth)

� Receivables/ Debtors (30 days to 90 days)

� Other expenses (1 month)

Current Liabilities

� Creditors ( 1 month’s RM & consumables)

January 3, 2011 32

January 3, 2011 33

MEANS OF FINANCE

� Basic criteria

� Promoters’ contribution

� Core promoters’ share

� Debt-equity ratio

� Normal DER – 1.5:1 (max.)

� Flexible for larger projects, infrastructure

January 3, 2011 34

MEANS OF FINANCE

� General considerations

� Capital intensity

� Risk perception

� Serviceability – debt/equity

January 3, 2011 35

MEANS OF FINANCE

� Equity

� Share capital

� Convertible part of PCD

(if converted in 18 months)

� Pref. Share Capital (> 3 yrs)

� Internal accruals

January 3, 2011 36

MEANS OF FINANCE

� Quasi – equity

� Subsidy

� Subordinated loans from promoters

� Incentive loans

January 3, 2011 37

MEANS OF FINANCE

� Debt

� Rupee term loans

� FC loans

� Pref. Capital (< 3 yrs.)

� Debentures

� ECB

� Suppliers’ credit

January 3, 2011 38

MEANS OF FINANCE

� Security package

� First charge on fixed assets

� Second charge on movables

� Personal guarantees

� Corporate guarantees

� Pledge of shares

� Govt. Guarantee/escrow

� Assignment of contracts

January 3, 2011 39

FINANCIAL VIABILITY

� Estimates of profitability, cash-flow and balance sheet

� Assumptions underlying profitability projections

� Critical assumptions� Installed capacity� Capacity utilisation� Product mix� Sales realisation� Consumption of inputs & prices

January 3, 2011 40

FINANCIAL VIABILITY

� Compare profitability with that of existing firms in similar line, particularly the PBIDT margin.

� Computation of IRR

� Rate of discount which equates the pv of capex in the project to pv of net cash flow over the life of the project.

� Is compared with cost of capital

January 3, 2011 41

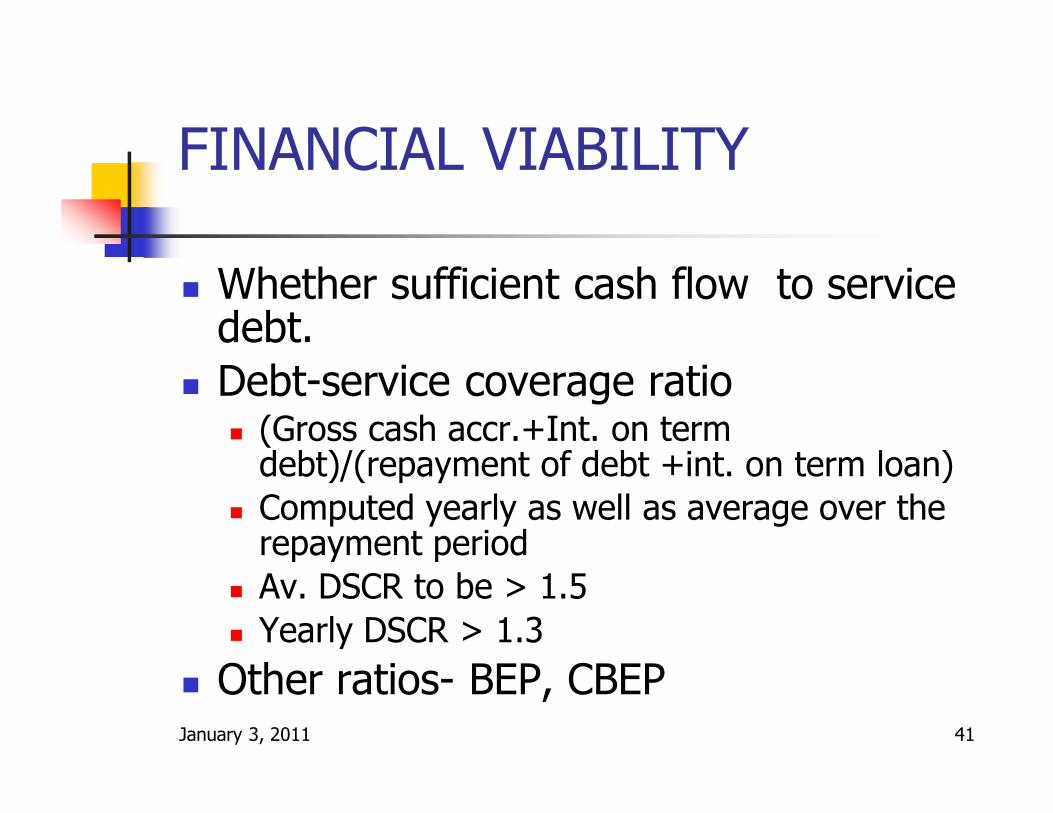

FINANCIAL VIABILITY

� Whether sufficient cash flow to service debt.

� Debt-service coverage ratio� (Gross cash accr.+Int. on term debt)/(repayment of debt +int. on term loan)

� Computed yearly as well as average over the repayment period

� Av. DSCR to be > 1.5

� Yearly DSCR > 1.3

� Other ratios- BEP, CBEP

January 3, 2011 42

FINANCIAL VIABILITY

� Sensitivity analysis

� Effect of adverse variance of critical elements on viability is examined

� Typical tests are� Reducing sales vol./Price� Increasing cost of inputs� Increase in project cost� Effect of FE fluctuation� Reduction in capacity utilisation.

January 3, 2011 43

ECONOMIC APPRAISAL

� Social cost benefit assessment

� Qualitative & Quantitative

Qualitative

� Social costs –= Environmental pollution= Ecological imbalances= Forest degradation= Accidents= Threat to animal life

January 3, 2011 44

Economic appraisal

� Social benefits= Improved facilities like roads, irrigation, sanitation etc.

= Improved transport facilities=More job opportunities=General economic improvement=Better living standards

January 3, 2011 45

Economic appraisal

� Actual cost & benefits not true representation of economic cost

� Two aspects of economic viability -benefits accruing to the economy and international competitiveness

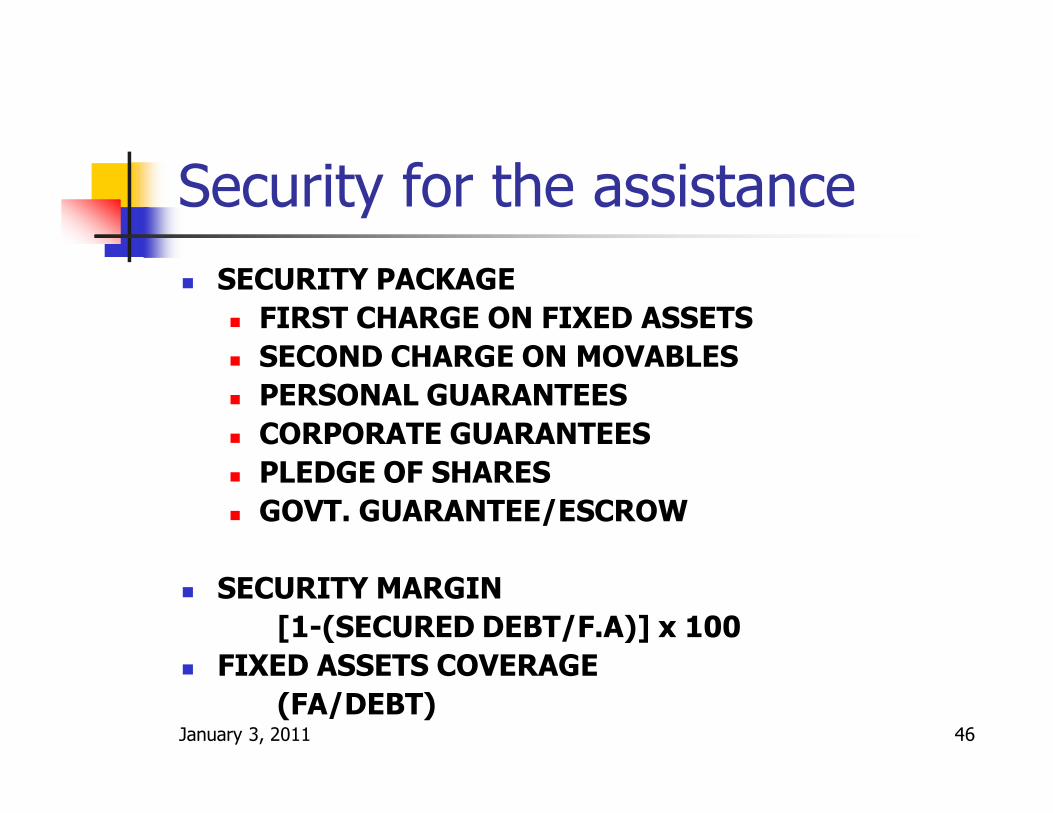

Security for the assistance

� SECURITY PACKAGE

� FIRST CHARGE ON FIXED ASSETS

� SECOND CHARGE ON MOVABLES

� PERSONAL GUARANTEES

� CORPORATE GUARANTEES

� PLEDGE OF SHARES

� GOVT. GUARANTEE/ESCROW

� SECURITY MARGIN

[1-(SECURED DEBT/F.A)] x 100

� FIXED ASSETS COVERAGE

(FA/DEBT)January 3, 2011 46

January 3, 2011 47

Financial Terms

� Rate of interest- Fixed, semi variable or variable

� Reset clause

� ROI on FC loans- LIBOR- Hedging cost

� Upfront fee/ Syndication fee/ Appraisal fee

� LC/BG charges

� Availability period

Financial terms

� Repayment schedule- Moratorium

� Additional interest/ Penal interest/ LDs

� Prepayment clause

� Security creation stipulation

� Financial covenants- Triggers

� Lenders’ Agent/ Security Trustee/ TRA Agent/LIE/ LLC/ LIA

January 3, 2011 48

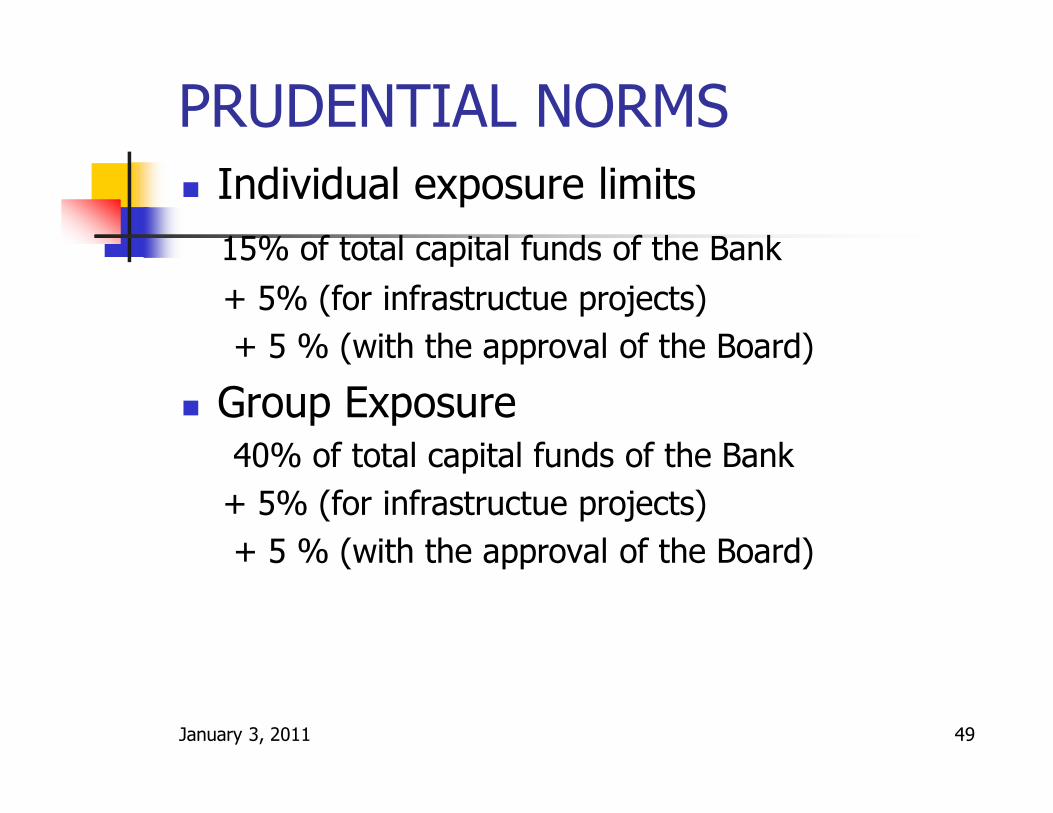

PRUDENTIAL NORMS

� Individual exposure limits

15% of total capital funds of the Bank

+ 5% (for infrastructue projects)

+ 5 % (with the approval of the Board)

� Group Exposure40% of total capital funds of the Bank

+ 5% (for infrastructue projects)

+ 5 % (with the approval of the Board)

January 3, 2011 49

Exposure Norms (Decided by respective Bank)

� Company

Rs.3000 crore + Rs.1000 crore for infrastructure

funding

� Group

Rs.8000 crore + Rs.2000 crore for infrastructure

funding

� Exposure to industry Sector

10% to 15% of total customer Exposure

January 3, 2011 50

THANK YOU

January 3, 2011 51