Progressing towards profitable growth

20

© Wärtsilä Progressing towards profitable growth Jaakko Eskola President & CEO 29 September 2016 Jaakko Eskola 1

Transcript of Progressing towards profitable growth

© Wärtsilä

Progressing towards profitable growthJaakko EskolaPresident & CEO

29 September 2016 Jaakko Eskola1

© Wärtsilä 29 September 2016 Jaakko Eskola2

OUR STRATEGIC GROWTH AGENDA

Well-positioned to benefit

from market trends

affecting our customers

Focused on fostering a

high performance culture

committed to continuous

improvement, and on

leveraging our global

presenceCommitted to

achieving

profitable growth

Key growth areas defined

around global megatrends

© Wärtsilä 29 September 2016 Jaakko Eskola3

Future energy investments will favor renewable power production

0

100

200

300

400

500

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Traditional baseload Gas Wind Solar Other Batteries Other flexible capacity

MARKET TRENDS

Source: Bloomberg New Energy Finance

Traditional baseload = coal, oil, nuclear, hydro

Other = geothermal, biomass, waste to energy, other REs

Other flexible capacity = demand response and other potential sources

Global annual gross capacity additions(GW)

© Wärtsilä

Marine emission regulations are driving a shift towards gas-fuelled vessels

MARKET TRENDS

LNG capable fleet

Source: Clarksons Research

29 September 2016 Jaakko Eskola4

2069

2826

268

3603

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Fleet Order book LOW CASE SCENARIO BASE CASE SCENARIO HIGH CASE SCENARIO

Fleet growth based on

current order book

© Wärtsilä 29 September 2016 Jaakko Eskola5

MARKET TRENDS

Average OPEX breakdown of a utility power plant

Environmental and economic considerations are increasingthe focus on efficiency

Voyage cost breakdown of a container ship

Source: CMA CGM Annual report 2015, data for 2014

Bunker

fuel and

consumables

41%

Handling and

stevedoring

45%

Port and canal

14%

Source: EIA, https://www.eia.gov/electricity/annual/html/epa_08_04.html, data for 2014

Fuel 87%

Maintenance 7%

Operation 6%

© Wärtsilä 29 September 2016 Jaakko Eskola6

OUR STRATEGIC GROWTH AGENDA

Well-positioned to benefit

from market trends

affecting our customers

Key growth areas defined

around global megatrends

• Gas-based technology

• Energy efficient solutions

• Innovative solutions

© Wärtsilä

WE SUPPORT OUR CUSTOMERS THROUGHOUT THE GAS VALUE CHAIN

Exploration& Drilling

Production &Liquefaction

Transport &storage

Receiving terminals& Regasification

Distribution &transport to the users

Gas-based powergeneration

29 September 2016 Jaakko Eskola7

POWER PLANT

LNG PEAK

SHAVING PLANT

RELIQUEFACTION UNIT

BUNKERING

TERMINAL

LNG FUELLED

PASSENGER SHIP

SATELLITE TERMINAL

MINI LIQUEFACTION

PLANT

SMALL LIQUEFACTION

PLANT

OFFSHORE SERVICE

VESSEL (OSV)

PLATFORM SUPPLY

VESSEL (PSV)

OIL & GAS PLATFORM

LNG CARRIER

POWER BARGE

STORAGE AND

REGASIFICATION

BARGE

SATELLITE

TERMINAL

POWER PLANT

SMALL LNG

CARRIER

FLOATING STORAGE &

(REGESIFICATION) UNIT

(FSRU/FSU)

LARGE

TERMINALSMALL LNG

CARRIER

BUNKERING

VESSEL

JETTY

SMALL/MEDIUM

TERMINAL

LNG FUELLED

CARGO SHIP

BUNKERING

TERMINAL

LNG FILLING

STATION

LBG FILLING

STATION

BIOGAS

LIQUEFACTION

PLANTSATELLITE AND

BUNKERING TERMINAL

REGASIFICATION

UNIT

RELIQUEFACTION

UNIT

POWER PLANT

POWER PLANT

© Wärtsilä

GAS-BASED TECHNOLOGY

Market share in gas engine power plants

0

50

100

150

200

250

85 86 88 91 00 03 04 06 07 08 09 10 11 12 13 14 15 16

Wärtsilä's deliveries Others

We are a leader in the gas equipment markets…

Cumulative gas-fuelled vessel deliveries

Wärtsilä77%

Other internal

combustion engines

23%

29 September 2016 Jaakko Eskola8

© Wärtsilä 29 September 2016 Jaakko Eskola9

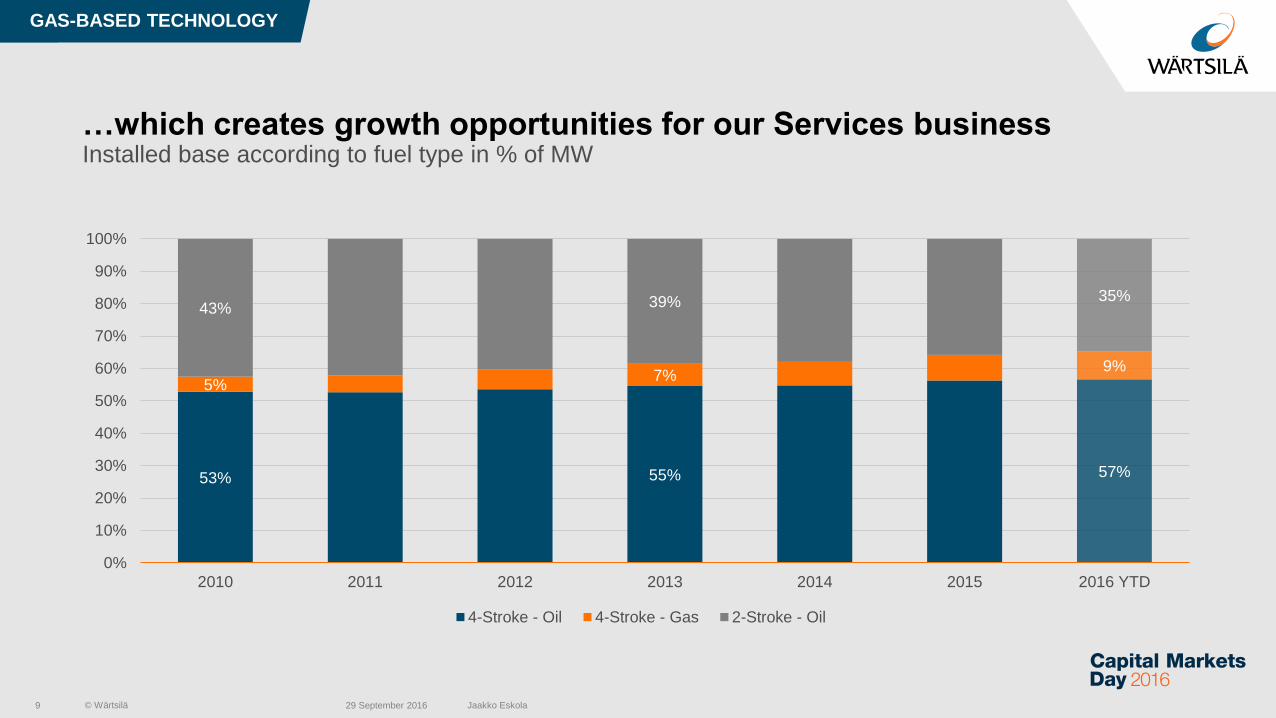

…which creates growth opportunities for our Services businessInstalled base according to fuel type in % of MW

53% 55% 57%

5%7%

9%

43% 39% 35%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 YTD

4-Stroke - Oil 4-Stroke - Gas 2-Stroke - Oil

GAS-BASED TECHNOLOGY

© Wärtsilä

Improving efficiency is a key cornerstone in our product development

ENERGY EFFICIENT SOLUTIONS

WST14

29 September 2016 Jaakko Eskola10

WST-14 STEERABLE

THRUSTER

WÄRTSILÄ 31 NACOS PLATINUM SHIP DESIGN

© Wärtsilä

Our new innovations in hybrid solutions increase customer efficiency

INNOVATIVE SOLUTIONS

Benefits of hybrid solutions:

• Fuel savings and reduced emissions

• Optimised engine operation

• Thermal power generation

optimisation

29 September 2016 Jaakko Eskola11

250 MW

ENGINE UNIT

46 MW SOLAR

PV UNIT

INTERCONNECTING

CABLES

© Wärtsilä 29 September 2016 Jaakko Eskola12

INNOVATIVE SOLUTIONS

Moving from hardware to software – Our digital journey

Products

equipped with

sensors, enabling

condition-based

monitoring

Developing our

digital service

offering

Expanding

our portfolio with

software-based

products

Extending

data analysis

& modelling to

external

factors

Creating customer value

through optimised performance

© Wärtsilä

Digitalisation increases our overall productivity

29 September 201613 Jaakko Eskola

INNOVATIVE SOLUTIONS

Manufacturing models

(Robotics, Manufacturing

execution system, 3D printing)

Infrastructure enablers

(Simulation clusters,

connectivity, big data storage,

cyber security)

Productivity enablers

(Engine component

traceability, parameter

management)

Building blocks for

digitalisation

(Smart sensors,

simple user

interfaces)

Integrated

product solutions(Eniram, Genius,

UNIC)

Diverse research areas

(Engine simulation models,

performance, big data

analytics, IoT)

Product

platforms

Components

Research

Manufacturing

Infrastructure

Tools & way

of working

© Wärtsilä 29 September 2016 Jaakko Eskola14

OUR STRATEGIC GROWTH AGENDA

Well-positioned to benefit

from market trends

affecting our customers

Focused on fostering a

high performance culture

committed to continuous

improvement, and on

leveraging our global

presence

Key growth areas defined

around global megatrends

© Wärtsilä© Wärtsilä

REACHING OUR FINANCIAL TARGETS THROUGH CONTINUOUS IMPROVEMENT

Value for

customers

Demand

driven flow

First time

right

Make it

visual

29 September 2016 Jaakko Eskola15

© Wärtsilä© Wärtsilä

… AND STRENGTHENING OUR HIGH PERFORMANCE CULTURE

Leadership

Developing excellent leaders

with common goals

Continuous development

Ensuring competent and

motivated personnel

Diversity

Building an inclusive

company culture

29 September 2016 Jaakko Eskola16

Over 130

nationalities in

70 countries

Over 55,000

learning days

in 2015

© Wärtsilä© Wärtsilä

… AND STRENGTHENING OUR HIGH PERFORMANCE CULTURE

High ethical standards

Ensuring responsible actions

and integrity among our

people

Quality

Providing the most reliable

products and services in our

industry

Safety

Creating a hazard-free

working environment

29 September 2016 Jaakko Eskola17

11 12 13 14 15

LOST TIME INJURY

FREQUENCY

-10%6.3

2.8

2014 2015

QUALITY

COSTS

© Wärtsilä 29 September 2016 Jaakko Eskola18

…AS WELL AS OUR UNRIVALLED GLOBAL NETWORK

Asia:

• Increasing energy demand

• Target market for solar

applications

• Significant shipping market,

growing cruise industry

• Large installed base

• Local presence through

partnerships

North America:

• Changing energy mix

• Growing installed base

• Opportunities in

environmental solutions

South America:

• Increasing energy demand

• Target market for solar applications

• Large installed base

Europe:

• Changing energy mix

• LNG infrastructure development

• Significant shipping market

• Opportunities in environmental

solutions

Middle East & Africa:

• Increasing energy demand

• Target market for solar applications

• Growing installed base

© Wärtsilä 29 September 2016 Jaakko Eskola19

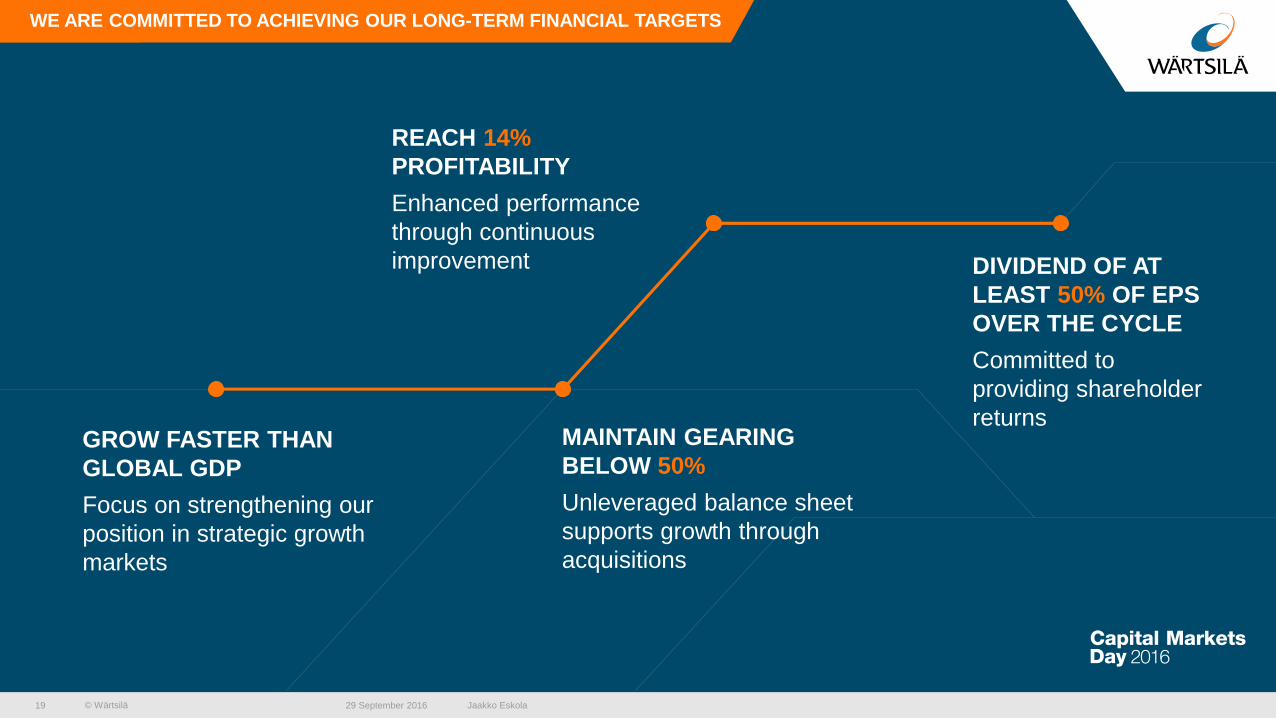

WE ARE COMMITTED TO ACHIEVING OUR LONG-TERM FINANCIAL TARGETS

GROW FASTER THAN

GLOBAL GDP

Focus on strengthening our

position in strategic growth

markets

REACH 14%

PROFITABILITY

Enhanced performance

through continuous

improvement DIVIDEND OF AT

LEAST 50% OF EPS

OVER THE CYCLE

Committed to

providing shareholder

returnsMAINTAIN GEARING

BELOW 50%

Unleveraged balance sheet

supports growth through

acquisitions

THANK YOU