Profitable ideas in North American equities Danny Bubis, CFA.

22

Profitable ideas in North American equities

-

Upload

geraldine-moody -

Category

Documents

-

view

216 -

download

2

Transcript of Profitable ideas in North American equities Danny Bubis, CFA.

Profitable ideas in North American equities

Agenda

Energy – secular outlook remains strong

Financials – past the worst

Gold – losing its luster?

Mega-cap technology – it ain’t 1999 anymore!

Tetrem – Who we are

Value investors

North American

Independent

Established

0%

2%

4%

6%

8%

10%

12%

'85 '88 '91 '94 '97 '00 '03 '06 '09 '12

Equity Risk Premium (NTM Earnings Yield less Real Bond Yield)

Stocks are cheap versus bonds

Source: Strategas. As of March 31, 2012.

Equity risk premium (forward earnings yield less real bond yield)

Bear markets precede secular bull markets

Source: Strategas. As of March 31, 2012.

-5%

0%

5%

10%

15%

20%

25%

'20 '30 '40 '50 '60 '70 '80 '90 '00 '10

S&P 500 10-Year Returns (1920 - Q1 2012)

S&P 500 10-year returns(1920 – Q1 2012)

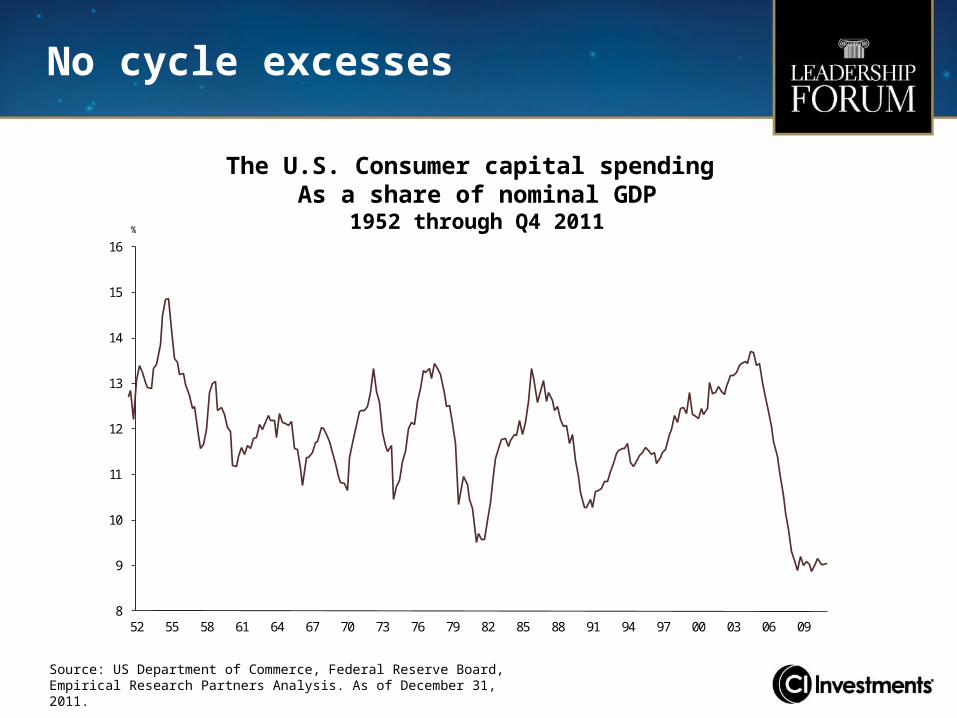

No cycle excesses

8

9

10

11

12

13

14

15

16

52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09

The US Consumer Capital Spendingas a Share of Nominal-GDP

1952 Through Q4 2011%

Source: US Department of Commerce, Federal Reserve Board, Empirical Research Partners Analysis. As of December 31, 2011.

The U.S. Consumer capital spending As a share of nominal GDP

1952 through Q4 2011

Corporate balance sheets are strong

Source: Strategas Research Partners. As of December 31, 2011.

U.S. Non-financial corporationsCash as a percent of total assets

Energy stocks are contrarian

Source: Empirical Research Partners. As of April 13, 2012.

Relative price to book of E&P stocks1952-2012

2.4

2.0

1.6

1.2

0.8

0.40 6 11 17 22 28 33 39 44 50 55 61 66 72 77 83 89 94 100

E&P Stocks More Expensive

Current:All E&PStocks Current:

Natural GasE&P Stocks

Percentile (100 = Lowest Price-to-Book Ratios)

Secular demand growth

Source: US Energy Information Administration. As of December 31, 2011.

World energy consumption, 1990 – 2035(quadrillion Btu)

Moving towards equilibrium

Source: Bloomberg. As of March 30, 2012.

Oil to natural gas ratio

Suncor: cash flow is coming

Unmatched assets• 27 billion barrels of resource base• No exploration required• 40-year resource life• Low-risk regulatory environment

Financially strong• $4B cash on balance sheet• Next material debt maturity 2018

Harvesting the cash• Expect $3B free cash flow in 2012• Ample room to raise dividend (10% payout ratio)• Long-term cash flow can hit 25% of current market cap

Source: Scotiabank. Canadian Banks include: BMO, BNS, CM, NA, RY and TDUS Banks include: BAC, C, JPM, USB and WFC

Financials – past the worst

U.S. and Canadian banks Tier 1 capital ratio2007 – fourth quarter 2011

CIBC: do you see what we see?

Compelling value• 19% P/E discount vs. peers • 4.8% dividend yield, safe and growing

Industry leading returns and capital levels• 22% ROE (group average 18%)• Highest capital ratios

Opportunity to differentiate through capital return• Expect meaningful share repurchase announcement• Room for future dividend increases

Source: Dow Jones Indexes and KBW Estimates.

U.S. Banks are cheap on valuation

KBW Bank Index – Price to tangible book value

-$500

-$300

-$100

$100

$300

$500

$700

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

2008 Credit Crisis April 2012

Source: 13D Research, Bloomberg. As of April 25, 2012.

Spread Between NYSE Arca Gold Miners Index and Spot Gold

Gold stocks lagging bullion

Spread between NYSE Arca Gold Miners Index and Spot Gold

Source: Market Vane Corporation. As of April 17, 2012.

0

20

40

60

80

100

5-Jan-00 5-Jan-01 5-Jan-02 5-Jan-03 5-Jan-04 5-Jan-05 5-Jan-06 5-Jan-07 5-Jan-08 5-Jan-09 5-Jan-10 5-Jan-11 5-Jan-12

Gold Sentiment (% bullish)

+1 Standard Deviation

-1 Standard Deviation

Average

Gold sentiment (% bullish)

Gold sentiment getting contrarian

0

5

10

15

20

25

30

For

war

d P

/E

March 2012

0

30

60

90

120

150

For

war

d P

/E

March 2000

Average is calculated as median. Highest outlier in each period not shown: Yahoo! Inc. in 2000 (P/E of 441x) and Amazon.com Inc. in 2012 (P/E of 164x).Source: Strategas. As of March 2012.

Overall Average: 31.0x

Overall Average: 13.6x

Tech Average: 73.1x

Tech Average: 13.8x

March 2000

March 2012

Mega-cap technology – It ain’t 1999 anymore!

Source: Capital IQ: data.Rolling 5 year standard deviation.Companies contained in Tech Basket: ORCL, IBM, MSFT, CSCO, INTC. Companies contained in Consumer Basket: KO, GIS, WMT, PG.

EPS Volatility – Tech vs. Consumer Staples

Mega-cap technology – stable earnings

FY 1999 FY2012 Change

Price $58.37 $30.35 -48%

Revenue $23B $72B 213%

EPS $0.85 $2.76 225%

P/E 68.7x 11.3x -84%

Dividend Yield

NA 2.60%

Dividend 3 Year CAGR

NA 15.40%

Microsoft

Revenge of the nerds revisited – Nerds in Paradise

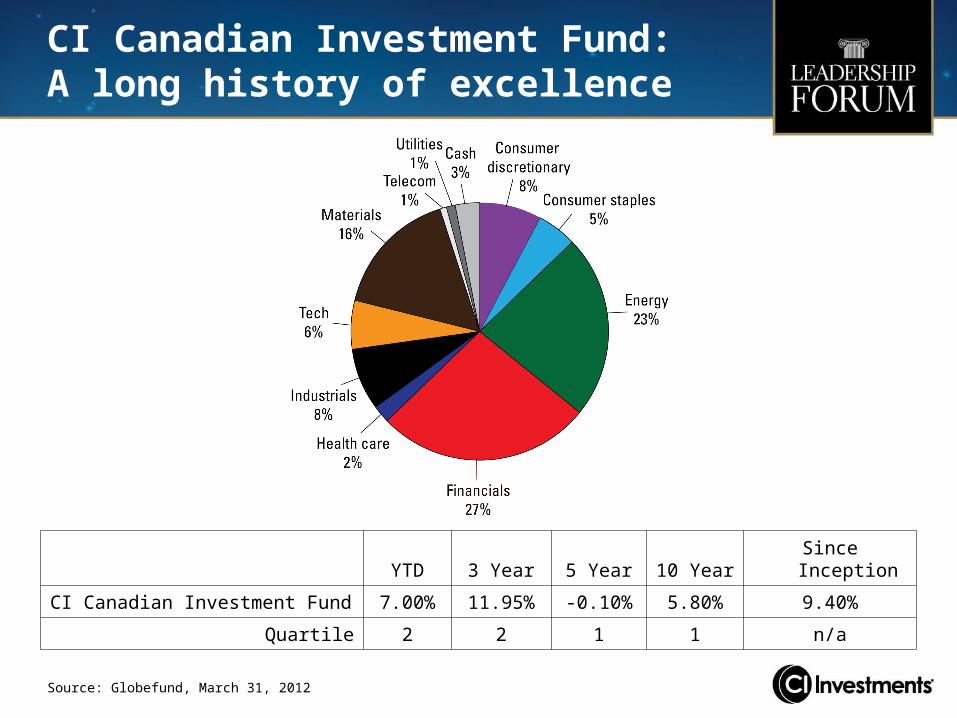

CI Canadian Investment Fund: A long history of excellence

YTD 3 Year 5 Year 10 Year Since Inception

CI Canadian Investment Fund 7.00% 11.95% -0.10% 5.80% 9.40%

Quartile 2 2 1 1 n/a

Source: Globefund, March 31, 2012

Tetrem’s new mandates

YTD 1 Year 3 Year 5 Year

Castlerock Canadian Dividend Fund B 6.3% 2.6% 15.1% 1.9%

Quartile 1 1 2 2

Castlerock Capital Appreciation Fund B 9.0% -3.3% 9.3% -3.4%

Quartile 3 3 3 2

Castlerock Canadian Dividend B Castlerock Capital Appreciation B

Tetrem assumed management of the funds April, 2012Source: Globefund, March 31, 2012

Thank you

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise indicated and except for returns for periods less than one year, the indicated rates of return are the historical annual compounded total returns including changes in security value. All performance data assume reinvestment of all distributions or dividends and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

®CI Investments and the CI Investments design are registered trademarks of CI Investments Inc.