Productivity Growth and the New Economy

56

Productivity Growth and the New Economy What, another paper on the new economy? When financial markets are raking through the debris of $8 trillion in lost equity value, and “.com” is a reviled four-symbol word, a paper on the impact of the new economy on productivity would seem as welcome as an analysis of the role of whales in the lighting revolution. In fact, the new economy (or, more precisely, information technolo- gies) continues to raise important puzzles about productivity growth. Variations in productivity growth have proved to be one of the most durable puzzles in macroeconomics. After a period of rapid growth fol- lowing World War II, productivity stagnated in the early 1970s. There was no shortage of explanations offered, including rising energy prices, high and unpredictable inflation, rising tax rates, growing government, burdensome environmental and health regulation, declining research and development, deteriorating labor skills, depleted possibilities for inven- tion, and societal laziness. 1 Yet these explanations seemed increasingly inadequate as inflation fell, tax rates were cut, regulatory burdens stabi- lized, government’s share of output fell, research and development and patents granted grew sharply, real energy prices fell back to pre-1973 lev- els, and a burst of invention in the new economy and other sectors fueled an investment boom in the 1990s. The productivity slowdown puzzle of the 1980s evolved into the Solow paradox of the early 1990s: computers were everywhere except in the 211 WILLIAM D. NORDHAUS Yale University The author is grateful for comments from Ray Fair, Robert Yuskavage, and members of the Brookings Panel. 1. See Nordhaus (1972), Baily (1982), and Denison (1980).

Transcript of Productivity Growth and the New Economy

Productivity Growth and the New Economy

What, another paper on the new economy? When financial marketsare raking through the debris of $8 trillion in lost equity value, and “.com”is a reviled four-symbol word, a paper on the impact of the new economyon productivity would seem as welcome as an analysis of the role ofwhales in the lighting revolution.

In fact, the new economy (or, more precisely, information technolo-gies) continues to raise important puzzles about productivity growth.Variations in productivity growth have proved to be one of the mostdurable puzzles in macroeconomics. After a period of rapid growth fol-lowing World War II, productivity stagnated in the early 1970s. Therewas no shortage of explanations offered, including rising energy prices,high and unpredictable inflation, rising tax rates, growing government,burdensome environmental and health regulation, declining research anddevelopment, deteriorating labor skills, depleted possibilities for inven-tion, and societal laziness.1 Yet these explanations seemed increasinglyinadequate as inflation fell, tax rates were cut, regulatory burdens stabi-lized, government’s share of output fell, research and development andpatents granted grew sharply, real energy prices fell back to pre-1973 lev-els, and a burst of invention in the new economy and other sectors fueledan investment boom in the 1990s.

The productivity slowdown puzzle of the 1980s evolved into the Solowparadox of the early 1990s: computers were everywhere except in the

211

W I L L I A M D . N O R D H A U SYale University

The author is grateful for comments from Ray Fair, Robert Yuskavage, and members ofthe Brookings Panel.

1. See Nordhaus (1972), Baily (1982), and Denison (1980).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 211

productivity statistics. The penetration of the American workplace byincreasingly sophisticated and powerful computers and software appar-ently failed to give an upward boost to productivity growth, for throughthin and thick, labor productivity growth seemed to be on a stable track ofslightly over 1 percent a year.

Then, in the mid-1990s, productivity growth rebounded sharply.Beginning in 1995, productivity in the business sector grew at a rateclose to that in the pre-1973 period. The causes of the rebound werewidely debated, but at least part was clearly due to astonishing produc-tivity growth in the new economy sectors of information technology andcommunications. This period led to yet another paradox, identified byRobert Gordon, who argued that, after correcting for computers, thebusiness cycle, and changes in measurement techniques, there was noproductivity rebound outside the computer industry.

This paper attempts to sort out the productivity disputes by using a newtechnique for decomposing sectoral productivity growth rates and using anew data set that relies primarily on value added by industry. In additionto examining the recent behavior of productivity, the paper adds a fewnew features to the analysis.

First, it lays out a different way of decomposing productivity growth,one that divides aggregate productivity trends into factors that increaseaverage productivity growth through changes in the shares of differentsectors. Second, it develops an alternative way of measuring aggregateand industrial productivity based on industrial data built up from theincome side rather than the product side of the national accounts. By rely-ing on the industrial data, I can focus on different definitions of outputand get sharper estimates of the sources of productivity growth. Third, byworking with the new industrial data, I can make more accurate adjust-ments for the contribution of the new economy than has been possible inearlier studies. Finally, this new data set allows creation of a new eco-nomic aggregate, which I call “well-measured output,” that excludesthose sectors where output is poorly measured or measured by inputs.

Productivity Accounting

Measuring productivity would appear to be a straightforward issue ofdividing output by inputs. In fact, particularly with the introduction of

212 Brookings Papers on Economic Activity, 2:2002

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 212

chain-weighted output measures, disentangling the different componentsof productivity growth has become quite complex. In this section Iexplore how to decompose productivity growth into three components: afixed-weight aggregate productivity index, a “Baumol effect” that reflectsthe effect of changing shares of output, and a “Denison effect” thatreflects the effect of differences between output and input weights.2

Consider indexes for the major aggregates. Define aggregate output asXt , composite inputs (here, hours of work) as St , and aggregate productiv-ity as At = Xt /St. The share of output of sector i in nominal GDP is σi,t , andthe growth of output or other variables is designated by g(X). Output ismeasured as a chained index, whereas labor inputs and productivity aresums and ratios, respectively. In this paper all growth rates will be calcu-lated in logarithmic terms, so that g(Xt) = ∆ln(Xt) = ln(Xt) – ln(Xt–1).

The growth of labor productivity in logarithmic terms is

Considering only the first term, after some manipulation I get

Using the same methodology, I derive the growth of productivity asg(At) = ∆ ln(At), which after some manipulation gives

where wi,t–1 is the share of inputs in sector i in total inputs. The interpreta-tion of equation 1 is that the rate of aggregate productivity growth is equalto the weighted-average productivity growth of the individual sectors plusthe difference-weighted average of input growth. The weights on produc-tivity growth are the lagged shares of nominal outputs, whereas the differ-ence weights on input growth are the differences between output andinput shares. (A symmetrical formula could be derived where the roles ofinput and output shares are reversed.)

( ) ( ) ln( ) ( ) ( )( – ),, – , – , –1 1 1 1g A A g A g S wt t it i t it i t i tii

= = + ∑∑∆ σ σ

∆ ln( ) ln ( ) ( ) ., – , –X g X g Xt it i ti

it i ti

= +

≈∑ ∑1 1 1σ σ

∆ ∆ ∆ln( ) ln( ) – ln( ).A X St t t=

William D. Nordhaus 213

2. The formulas in this section are derived and discussed more extensively in Nordhaus(2002).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 213

It will be convenient to add a term to capture the role of changingshares of output. Add and subtract from equation 1 and

rearrange terms, where “base” indicates a base year. This yields

Interpretation

Equation 2 shows that aggregate productivity growth can be brokendown into three components: a pure (fixed-weight) productivity growthterm that uses fixed base-year nominal output weights, a term that reflectsthe difference between current nominal output weights and base-yearnominal output weights, and a term that reflects the interaction betweenthe growth of inputs and the difference between output and input weights.For convenience, I will designate these three terms as follows.

the pure productivity effect. The first term on the right-hand sideof equation 2 is a fixed-weighted average of the productivity growth ratesof different sectors. More precisely, this term measures the sum of thegrowth rates of different industries weighted by base-year nominal outputshares of each industry. Another way of interpreting the pure productivityeffect is as the productivity effect that would occur if there were nochange in the shares of nominal output among industries.

the baumol effect. The second term captures the interaction be-tween the differences in productivity growth and the changing shares ofnominal output among different industries over time. This effect has beenemphasized by William Baumol in his work on unbalanced growth.3

According to Baumol, those industries that have relatively slow outputgrowth are generally accompanied by relatively slow productivity growth(services being a generic example, and live performances of a Mozartstring quartet a much-cited specific example). This conjunction of factorsleads to Baumol’s “cost disease,” a syndrome in which the drag of slow-

( ) ( ) ( ) ( )( – )

( )( – ).

, , , – ,

, – , –

2 1

1 1

g A g A g A

g S w

t i t ii

it i t ii

it i t i ti

= +

+

∑ ∑∑

σ σ σ

σ

base base

g Aii

i( ), , base base∑ σ

214 Brookings Papers on Economic Activity, 2:2002

3. See Baumol (1967). This study was updated and revised in Baumol, Blackman, andWolff (1985). A recent discussion focusing on the services sector is contained in Triplettand Bosworth (2002).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 214

productivity-growth industries retards the growth of aggregate productiv-ity. In terms of equation 2, if the share of nominal output σi,t devoted toslow-productivity-growth industries rises over time, the second term willalso be rising, and overall growth will thereby be driven downward.

the denison effect. The third term in equation 2 captures leveleffects due to differences in shares. I label this the Denison effect, after Edward Denison, who pointed out that the movement from low-productivity-level agriculture to high-productivity-level industry wouldraise productivity even if the productivity growth rates in the two sectorswere zero. Denison showed that this effect was an important componentof overall productivity growth when fixed-weight indexes are used tomeasure output.4

Earlier work on productivity decomposition implicitly or explicitlyincluded a fourth effect, called the fixed-weight drift term.5 That effectarises when real output is measured using Laspeyres indexes of output.Real output measured with a Laspeyres fixed-base quantity index tends togrow more slowly than output measured by a chain index in periodsbefore the base year and more rapidly in periods after the base year. Thedivergence of relative real outputs from relative nominal outputs with“old-style” fixed-weight quantity indexes motivates the name. This termvanishes (or almost vanishes) with the introduction of chain indexes (or,more precisely, well-constructed superlative index numbers) because realoutput shares used in calculating the growth rates are equal (or almostequal) to nominal output shares. A careful examination of the measure ofproductivity growth that most closely corresponds to the welfare-theoreticmeasure of the growth of real income shows as well that the fixed-weightdrift term should be omitted.6 All in all, moving to chain weights andremoving the fixed-weight drift term marked a major advance in produc-tivity measures.

William D. Nordhaus 215

4. A number of studies found this syndrome. See in particular Denison’s studies ofpostwar Europe (Denison, 1967).

5. More precisely, when output is measured using fixed weights, the fixed-weight drift

term is where zit is the share of industry i in total output when output is

measured by a Laspeyres index. This term is zero when output is measured using chainweights.

6. See Nordhaus (2002).

g X zit it it

i

( )[ – ],σ∑

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 215

Review of Alternative Productivity Measures

The Underlying Productivity Data

The productivity data used in this paper differ from standard measuresused to track productivity. The output data are based on income-sidevalue-added data (gross domestic income, or GDI) developed by theBureau of Economic Analysis (BEA).7 The BEA provides data on nomi-nal output by industry (value added), Fisher indexes of real output andprices by industry, and hours of work. For this paper I have created Fisherindexes of output for different aggregates as well as estimates of laborproductivity by industry and for different aggregates.8

The major advantage of the income-side measures is that they present aconsistent set of detailed industrial accounts in which the nominal valuessum to nominal GDP; by contrast, very little industrial detail is availableon the product side of the accounts. The disadvantage is that the real out-put data using chain weights are available only for the period 1977–2000.

Because of interest in the new economy, I have also constructed a setof new economy accounts. For the purpose of this paper, I define the neweconomy as machinery, electric equipment, telephone and telegraph, andsoftware. The combined share of these sectors in real GDP grew from2.9 percent in 1977 to 10.6 percent in 2000. These sectors are somewhatmore inclusive than a narrow definition of the new economy but are thenarrowest definition for which a complete set of accounts is available. Idiscuss details of the new economy below.

In addition, I develop productivity measures for three different broadoutput concepts that can be used in productivity studies. One of these isstandard GDP (measured from the income side of the accounts). A secondis what the Bureau of Labor Statistics (BLS) defines as nonfarm businesssector output. A third concept responds to concerns in productivity stud-ies about the poor quality of the price deflation in several sectors. For thispurpose I have constructed a set of accounts that I call “well-measuredoutput,” which includes only those sectors for which output is relativelywell measured. I begin with a review of standard labor productivity mea-

216 Brookings Papers on Economic Activity, 2:2002

7. The BEA data are available on the BEA website. Details on the construction of thedata sets are provided in Nordhaus (2002).

8. A discussion of the use of Fisher indexes in the national income and productaccounts is found in Triplett (1992) and Landefeld and Parker (1997).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 216

sures and then turn to a comparison of standard measures with themeasures constructed for this study.

The BLS Productivity Data

The most widely followed productivity measures are constructed andpublished by the BLS. Figure 1 shows the behavior of the BLS series forthe business sector; for this purpose I have used a three-year moving aver-age of labor productivity growth. Table 1 shows a simple regression withtwo breaks in trend, one in 1973 and another in 1995.

Three points are worth noting. First, the labor productivity growth datain figure 1 do not show dramatic and obvious breaks in trend. Labor pro-ductivity began deteriorating in the late 1960s, and the really terribleperiod was in the early 1980s. An untutored analyst would probably notrecognize any sharp break in trend labor productivity after 1973. Second,the productivity upsurge in the late 1990s was not a particularly rareevent. Productivity accelerations of greater magnitude were seen in theearly 1960s, the early 1970s, and the early 1980s—indeed, there werechanges in “trend” in virtually every decade. The volatile nature of pro-ductivity growth is a warning that one should not read too much into aperiod even as long as five years. Third, even with the rapid productivitygrowth observed since 1995, labor productivity growth is still below fourother postwar highs. The early 1950s, the mid-1960s, the early 1970s(briefly), and the mid-1980s were periods when labor productivity grewmore rapidly than it has in the last three years.

Notwithstanding these cautions, it is important to examine the currentupturn in productivity with an eye to understanding its sources. In partic-ular, we will want to determine the role of the new economy in the recentproductivity rebound.

Comparison of Labor Productivity Growth Rates between Product Side and Income Side

The BLS business output series is a product-side index provided by theBEA. It is useful to compare the standard BLS series with the income-sideproductivity measures developed here. This is not straightforwardbecause (in addition to the problem of dealing with the statistical discrep-ancy) the BLS business output (“Bus-Prod”) series does not correspond toa straightforward combination of the income-side industries. I have

William D. Nordhaus 217

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 217

prepared an income-side business output measure (“Bus-Inc”) by combin-ing the major industries as best I can. The nominal values of the twoaggregates are reasonably close, with a root mean square error of0.16 percent over the 1977–2000 period.9

As far as productivity per hour worked is concerned, the two seriesagree reasonably well. For the entire 1977–2000 period the income-sideproductivity growth of nonfarm business output was about 0.07 percent ayear faster. On the whole, the income-side and the product-side data arereasonably consistent. Table 2 shows a comparison of estimates ofproductivity growth from the two series for three subperiods of the1977–2000 period. The basic story is the same except in the last period,when the income-side measure grew substantially faster; this difference is

218 Brookings Papers on Economic Activity, 2:2002

9. The Bus-Inc variable excludes general government and private households alongwith most of housing and the nonprofit sectors of the service industries. For the comparisonin the text, I have subtracted the statistical discrepancy from the income-side measure.

Figure 1. Labor Productivity Growth in the Business Sectora

Source: Bureau of Labor Statistics.a. Three-year moving average of logarithmic growth rates.

0

1

2

3

4

5

6

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Percent a year

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 218

due primarily to the mysterious statistical discrepancy, which rose sharplyfrom 1977 to 2000.

Well-Measured Output

The final output measure is one that includes only those sectors whereoutput is relatively well measured. It is widely accepted today that, inmany sectors, real output is poorly measured in the national incomeaccounts. In some cases, such as general government and education, thereis no serious attempt to measure output, and instead the indexes of activ-ity are inputs such as employment. In other cases the BEA (or the BLS,which prepares the underlying price data) uses deflation techniques thatare potentially defective.

The idea of well versus poorly measured sectors was introduced by ZviGriliches in his 1994 presidential address to the American EconomicAssociation:

Imagine a “degrees of measurability” scale, with wheat production at one endand lawyer services at the other. One can draw a rough dividing line on thisscale between what I shall call “reasonably measurable” sectors and the rest,where the situation is not much better today than it was at the beginning of thenational income accounts.10

Defective deflation occurs for two quite different reasons. First, in somesectors, of which construction, insurance, and banking are examples, the

William D. Nordhaus 219

10. Griliches (1994, p. 10).

Table 1. Trends in Labor Productivity in the Business Sector, 1948–2002

Regression Standard Variablea coefficient error t Statistic

Constant 3.34 0.36 9.4DUM73b –1.93 0.52 –3.7DUM95c 1.17 0.77 1.5

Summary statisticR2 0.060Standard error of regression 3.58No. of observations 218

Source: Author’s regressions using data from the Bureau of Labor Statistics.a. The dependent variable is the annualized one-quarter change in the logarithm of labor productivity. The sample period is

1948:1 to 2002:2.b. Dummy variable that takes the value of 1 after 1973:2.c. Dummy variable that takes the value of 1 after 1995:2.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 219

BEA does use price indexes for deflation of nominal magnitudes, but theprice indexes are for goods or services that are not representative of therange of outputs in that sector. Second, and this has received much moreattention, in some sectors the underlying price index does not adequatelycapture quality change or the introduction of new goods and services. Anexcellent historical example of this syndrome is computers. Beforehedonic techniques were introduced, the government assumed that theprice of computers was constant in nominal terms. When hedonic priceindexes for computers were introduced, the earlier assumption was foundto overstate the “true” price increase by around 20 percent a year for thelast three decades.

It is difficult for an outsider to assess the quality of the deflation of eachsector included in the industrial accounts. There have been many studiesof this issue.11 Nonetheless, after discussion with experts inside and out-side the BEA, I have constructed a new measure of output for sectors thathave relatively well measured outputs. The sectors included are

Agriculture, forestry, and fishingMiningManufacturingTransportation and public utilitiesWholesale trade

220 Brookings Papers on Economic Activity, 2:2002

11. Griliches’s (1994) definition of “measurable” sectors is identical to that of well-measured output except that he puts trade in the unmeasurable sector.

Table 2. Alternative Measures of Productivity Growth in the Nonfarm Business Sector, 1977–2000a

Percent a year

Change, Change,1977–89 to 1977–89 to

Measure 1977–89 1989–95 1995–2000 1989–95 1995–2000

BLS (product side)b 1.21 1.46 2.45 0.25 1.24BEA (income side)c 1.26 1.26 2.87 0.00 1.61Difference –0.05 0.20 –0.41 0.25 –0.36

Source: Bureau of Economic Analysis data.a. Growth in output per hour worked; annual averages.b. Product-side output of the nonfarm business sector, based on BLS hours-worked measures, and used by the BLS in its busi-

ness sector productivity measures.c. Uses income-side output and hours measures derived in this paper and using BEA hours data.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 220

Retail tradeCertain services (software, other business services, hotels, repair).

Five major sectors are excluded:

Construction*Finance,* insurance,* and real estateMost services*General governmentGovernment enterprises*.

The sectors marked by asterisks are included in the BLS’s measure ofbusiness output. Nonfarm business output remained about 75 percent ofnominal GDP over the 1977–2000 period, whereas well-measured outputdeclined from 68 percent of nominal GDP in 1948 to 57 percent in 1977and 50 percent in 2000. Thus, well-measured output is currently onlyabout half of GDP, and the share of output that is well measured has beendeclining steadily since World War II. This trend confirms, using a differ-ent approach and data set, Griliches’s observation that the degree of“measurability” of real output has been declining over time. At the sametime, the BEA has made considerable progress in introducing improveddeflation techniques. Whether the progress of improved deflation has out-stripped the decline in measurability is an interesting but open question.

Table 3 shows the growth of output per hour for the three majoraggregates—GDP, nonfarm business output, and well-measured output—for different subperiods of the 1977–2000 period. Productivity in thebusiness sector has grown faster than productivity for total GDP, primar-ily because of the slow growth of productivity in the government sector.Productivity in the well-measured sectors has grown about 0.65 percent-age point a year faster than in the nonfarm business economy because ofpoor performance in the construction and services industries.

The New Economy

This study also develops input and output data for the new economy.For the purpose of this study, I use the following formal definition: Thenew economy involves acquisition, processing and transformation, anddistribution of information. The three major components are the hardware(primarily computers) that processes the information, the communications

William D. Nordhaus 221

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 221

Tab

le 3

.P

rodu

ctiv

ity

Gro

wth

for

Alt

erna

tive

Mea

sure

s of

Agg

rega

te O

utpu

t an

d th

e N

ew E

cono

my,

197

7–20

00a

Per

cent

a y

ear

Cha

nge,

C

hang

e,

Cha

nge,

19

77–8

9 to

1977

–89

to19

89–9

5 to

Mea

sure

1977

–89

1989

–95

1995

–200

019

77–2

000

1989

–95

1995

–200

019

95–2

000

Tot

al e

cono

my

GD

P1.

201.

111.

731.

29–0

.09

0.53

0.62

GD

I1.

210.

962.

241.

37–0

.25

1.04

1.28

Non

farm

bus

ines

s se

ctor

Inco

me-

side

1.26

1.26

2.87

1.61

0.00

1.61

1.61

BL

S m

easu

re1.

211.

462.

451.

540.

251.

240.

99W

ell-

mea

sure

d ou

tput

2.00

1.93

3.29

2.26

–0.0

71.

291.

36N

ew e

cono

my

6.25

6.37

9.98

7.09

0.12

3.73

3.61

Sou

rce:

Aut

hor’

s ca

lcul

atio

ns u

sing

BE

A a

nd B

LS

dat

a.a.

Gro

wth

in o

utpu

t per

hou

r w

orke

d; d

ata

are

annu

al a

vera

ges.

Det

ails

may

not

sum

to to

tals

bec

ause

of

roun

ding

.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 222

systems that acquire and distribute the information, and the software that,with human help, manages the entire system.

Which sectors are included in practice under this definition? Table A1in the appendix shows the new economy sectors as defined by the Com-merce Department for its study The Emerging Digital Economy.12 Thatdefinition overlaps with the formal definition, and it includes some oldeconomy sectors as well as some sectors with questionable price indexes.

For purposes of this study, we are hamstrung because comprehensivedata are limited to major industries. I therefore include in the new econ-omy the four major industries that contain the new economy industries:industrial machinery and equipment (Standard Industrial Classifica-tion 35), electronic and other electric equipment (SIC 36), telephone andtelegraph (SIC 48), and software (SIC 873). The BEA has developeddetailed industrial data for the first three of these, but there is incompletedetail for software.

This definition of the new economy is somewhat broader than wouldbe ideal for the present purposes. For example, SIC 35 contains comput-ers and office equipment, but the computer industry accounts for less than25 percent of the total 1996 value added in that sector. Other parts ofSIC 35 include ball bearings and heating and garden equipment, whichare dubious candidates for inclusion in the new economy. A prominentcomponent of SIC 36 is semiconductors, an industry central to the neweconomy, but semiconductors constitute only 8 percent of the 1996 valueadded in SIC 36. This sector includes communications equipment, onepart of which has hedonic deflation. This sector also contains many oldeconomy industries, including incandescent bulbs, and a wide array ofconsumer electronics, whose prices are probably poorly measured. Simi-larly, although the telephone and telegraph sector is central to the com-munications components of the new economy, it also includes somepaleoindustries like telegraph, whose commercial applications date from1844, and telephone, which premiered in 1876.

Software is genuinely a new economy industry. However, only the datafor the prepackaged component (slightly larger than one-fourth of thetotal) are hedonically deflated at present. The data on software are incom-plete, and some crude assumptions are necessary to fit software into thepresent database.

William D. Nordhaus 223

12. U.S. Department of Commerce (2000).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 223

Because of the importance of the new economy in the present analysis,it is worth emphasizing that relatively few industries are measured usinghedonic price indexes that systematically attempt to capture new goodsand components or quality change. The BEA reports that systematichedonic prices are used for only four major industries (all in new econ-omy sectors): computers and peripheral equipment, semiconductors,prepackaged software, and digital switching equipment. In 1998 thesesectors accounted for about 2.2 percent of GDP, while the four industriesincluded in the broad definition of the new economy in this studyaccounted for 9.6 percent of GDP. This suggests that only a quarter ofwhat I have labeled as the new economy has careful hedonic measure-ment of prices and output.

Productivity Resurgence and the New Economy

I now turn to the central questions about productivity performance inthe late 1990s: What was the magnitude of the productivity upturn? Howmuch of it was due to each of the three factors derived above—pure pro-ductivity acceleration, the Baumol effect, and the Denison effect? Whatwas the contribution of the new economy to the productivity acceleration?And is there a different view for the well-measured part of the economythan for the entire economy?

How Large a Productivity Acceleration?

Returning to table 3, we see that labor productivity growth in the threemajor aggregates showed little change in the two subperiods between1977 and 1995, averaging around 1.1 percent a year for the income-sidemeasure of the total economy and around 1.3 percent a year for income-side nonfarm business output. Well-measured output showed more robustproductivity growth, averaging around 2.0 percent a year, but was rela-tively stable over this period. The new economy showed substantialproductivity growth, averaging over 6 percent a year in the first two sub-periods, but with little acceleration.

The last five years of the period showed a dramatic upturn in labor pro-ductivity growth in all of the measures (last column of table 3). For thetotal economy the acceleration from the first to the last subperiod was

224 Brookings Papers on Economic Activity, 2:2002

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 224

0.53 percentage point using the output-side measure and almost twice asmuch, 1.04 percentage points, using the income-side measure. Account-ing for the difference is the huge growth in the statistical discrepancyfrom 1997 to 2000.

The nonfarm business sector showed an upturn of 1.61 percentagepoints using the income-side measure and a slightly smaller increase of1.24 percentage points according to the BLS measure. The differencebetween the two estimates is partly due to more rapid growth in theincome-side estimate of nonfarm business output and partly due to some-what faster growth in the BLS’s estimate of hours for that sector.

Well-measured output is estimated to have seen faster productivitygrowth over the entire period than the other major aggregates. Over theentire period, productivity growth was 0.65 percentage point faster in thewell-measured sectors than in the income-side measure of nonfarm busi-ness, and 0.89 percentage point faster than in income-side total output.The acceleration in productivity in the last five years of the period in thewell-measured sectors was slightly smaller than that in income-side non-farm business output, but larger than for either of the definitions of theentire economy. The new economy logged a breathtaking acceleration inproductivity of 3.7 percentage points a year over the last five years of theperiod, to a growth rate of 10 percent a year. In short, the last five years ofthe period witnessed a major upturn in productivity growth for all themajor aggregates.

Decomposition of the Productivity Acceleration

Productivity growth is determined both by the rates of productivitygrowth within industries and by changes in the composition of industries.How much of the recent growth in productivity was due to each of thethree factors—pure productivity growth, the Baumol effect, and the Deni-son effect—derived above?

The first panel of table 4 shows the basic results for the overall econ-omy, as measured from the income side. The pure productivity effect wasvirtually identical to overall productivity growth over the entire period.However, the pure productivity effect was slightly (0.15 percentage point)higher than conventionally measured average productivity growth in themost recent period. Even larger differences are seen for the nonfarm busi-ness sector and for well-measured output (bottom two panels of table 4).

William D. Nordhaus 225

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 225

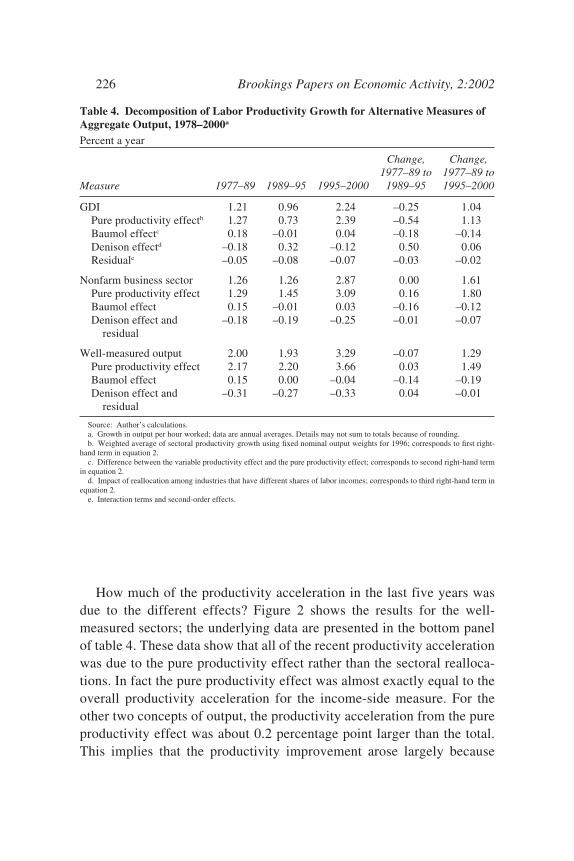

How much of the productivity acceleration in the last five years wasdue to the different effects? Figure 2 shows the results for the well-measured sectors; the underlying data are presented in the bottom panelof table 4. These data show that all of the recent productivity accelerationwas due to the pure productivity effect rather than the sectoral realloca-tions. In fact the pure productivity effect was almost exactly equal to theoverall productivity acceleration for the income-side measure. For theother two concepts of output, the productivity acceleration from the pureproductivity effect was about 0.2 percentage point larger than the total.This implies that the productivity improvement arose largely because

226 Brookings Papers on Economic Activity, 2:2002

Table 4. Decomposition of Labor Productivity Growth for Alternative Measures ofAggregate Output, 1978–2000a

Percent a year

Change, Change, 1977–89 to 1977–89 to

Measure 1977–89 1989–95 1995–2000 1989–95 1995–2000

GDI 1.21 0.96 2.24 –0.25 1.04Pure productivity effectb 1.27 0.73 2.39 –0.54 1.13Baumol effectc 0.18 –0.01 0.04 –0.18 –0.14Denison effectd –0.18 0.32 –0.12 0.50 0.06Residuale –0.05 –0.08 –0.07 –0.03 –0.02

Nonfarm business sector 1.26 1.26 2.87 0.00 1.61Pure productivity effect 1.29 1.45 3.09 0.16 1.80Baumol effect 0.15 –0.01 0.03 –0.16 –0.12Denison effect and –0.18 –0.19 –0.25 –0.01 –0.07

residual

Well-measured output 2.00 1.93 3.29 –0.07 1.29Pure productivity effect 2.17 2.20 3.66 0.03 1.49Baumol effect 0.15 0.00 –0.04 –0.14 –0.19Denison effect and –0.31 –0.27 –0.33 0.04 –0.01

residual

Source: Author’s calculations.a. Growth in output per hour worked; data are annual averages. Details may not sum to totals because of rounding.b. Weighted average of sectoral productivity growth using fixed nominal output weights for 1996; corresponds to first right-

hand term in equation 2.c. Difference between the variable productivity effect and the pure productivity effect; corresponds to second right-hand term

in equation 2.d. Impact of reallocation among industries that have different shares of labor incomes; corresponds to third right-hand term in

equation 2.e. Interaction terms and second-order effects.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 226

weighted-average productivity growth in the underlying industriesincreased, not because of sectoral shifts or other factors.

The basic conclusion regarding the decomposition of productivitygrowth is that pure productivity growth in the most recent period hasbeen even more rapid than total productivity growth. This is most clearlyseen for overall output, where the conventional product-side estimates ofproductivity growth (table 3) are well below pure productivity growth(table 4) because of the statistical discrepancy as well as modest Baumoland Denison effects. The understatement is even larger for the nonfarmbusiness sector and for the well-measured sector.

We can also use these results to determine the gravity of the Baumoleffect. In a series of pioneering works, William Baumol analyzed theimpact of differential productivity growth on different sectors and institu-

William D. Nordhaus 227

Figure 2. Components of Productivity Growth in Well-Measured Output, 1977–2000

Sources: Author’s calculations using data from Bureau of Economic Analysis.

0

1

2

3

1977–89 1989–95 1995–2000

Total

Pure productivity effect

Baumol effect

Denison effect and residual

Percent a year

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 227

tions such as services, health care, the cities, and the performing arts.13

His basic story is that those sectors whose productivity growth rates arebelow the economy’s average will tend to experience above-average costincreases and a growing share of total spending. The resulting “cost dis-ease” may, according to Baumol, lead to above-average price increases,financial pressures on suppliers, and a reduction in the economy’s overallrate of productivity growth.

Table 4 shows the Baumol effect over the 1977–2000 period. In factthe effect was slightly positive over the period as a whole for all three out-put concepts, indicating that changing sectoral shares added slightly toaggregate productivity. Recall from equation 2 that the Baumol effectcaptures the interaction of changing shares of nominal output and produc-tivity growth. As it turns out, those sectors with rising nominal outputshares have experienced higher than average productivity growth rates(the new economy sectors are a good example). Baumol’s cost disease hasbeen cured, or at least is in remission.

Contribution of the New Economy to the Productivity Rebound

The next question involves using the new data set to ask, What is thecontribution of the new economy to the remarkable resurgence in produc-tivity over the last few years? In this exercise the answer is limited to thedirect contribution of more rapid productivity growth in new economyindustries, or to the production of new economy goods and services. Thisanalysis omits the important question, addressed later in this paper, of theuse of new economy goods and services elsewhere in the economy,through the contribution of capital deepening and of spillover effects fromthe information economy to productivity.

The technique for calculating the impact of the new economy is as fol-lows. For each output concept, output and hours indexes are calculatedwith and without the four new economy sectors. In other words, in calcu-lating the chain indexes, the index with the new economy sectors takes theFisher index including the four industries, whereas the index without thenew economy omits those and rescales the weights and recalculatesFisher indexes so that the output and labor indexes sum to 100 percent ofthe total. This entire procedure is conceptually straightforward primarilybecause I have constructed a consistent set of value-added accounts.

228 Brookings Papers on Economic Activity, 2:2002

13. See the references in note 3.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 228

Figure 3 shows the pattern of productivity growth in the four neweconomy sectors. The most impressive acceleration in the late 1990s wasin the electronics sector (SIC 36), which contains microprocessors. Inaddition, industrial machinery (SIC 35), which contains computers,showed impressive gains in the late 1990s. The other two new economysectors had healthy but not spectacular measured productivity gains. Thesoftware sector contains one component (prepackaged software) withrapid price declines, but the other two components (custom and own-account software) do not have hedonic estimates of prices and show mod-est price declines.

Table 5 shows the results for all three major sectors. Focusing first onthe nonfarm business sector, we see that relatively little of the productiv-ity acceleration in that sector in the late 1990s was due to the new econ-omy. Productivity in the nonfarm business output measure that includesthe new economy accelerated by 1.61 percentage points from the 1977–89period to the 1995–2000 period. But only 0.29 percentage point, or one-sixth, was due to acceleration in the new economy sectors. The balance of1.32 percentage points came in old economy sectors. The results areroughly the same for the overall economy. For the well-measured sectors,one-third of the productivity acceleration from the first half to the secondhalf of the 1990s was due to the new economy.

Although the new economy contributed relatively little to the accelera-tion in productivity growth, it nonetheless provided a substantial part oftotal productivity growth. In the last five years of the period, as shown intable 5, the new economy contributed 0.64, 0.78, and 1.16 percentagepoints to the total for GDP, nonfarm business, and well-measured output,respectively.

Figure 4 shows the contribution of the four new economy sectors tooverall GDP productivity. These calculations weight the productivitygrowth rates of each of the four sectors by its share in nominal GDP (fol-lowing the approach of the ideal welfare-theoretic formula). The totalimpact on GDP productivity, shown in the far-right-hand bar in eachgroup, was 0.46 percentage point in the first two subperiods and then roseto 0.72 percentage point for the 1995–2000 period. The largest single con-tributor for the period as a whole was electric and electronic equipment,followed by machinery, except electrical.14

William D. Nordhaus 229

14. The estimates here vary from those in the tables because the weighting procedure isslightly different.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 229

Evaluation of the Gordon Hypothesis

Equipped with this new data set, I can now evaluate the Gordonhypothesis. This view holds that most if not all of the productivity accel-eration in the late 1990s was due to higher productivity in the computerindustry. As summarized in The Economist:

Robert Gordon of Northwestern University, one of the country’s top authoritieson the subject, has found that more than 100% of the acceleration in productiv-ity since 1995 happened not across the economy as a whole, nor even across IT[information technology] at large, but in computer manufacturing, barely 1% ofthe economy. Elsewhere, growth in productivity has stalled or fallen.15

Since the first statement of the Gordon hypothesis in 1999, there hasbeen some backtracking. The most recent estimates associated with the

230 Brookings Papers on Economic Activity, 2:2002

15. “How Real Is the New Economy?” The Economist, July 24, 1999. Also see Gordon(2000). Further discussions can be found in Oliner and Sichel (2000). The latest publishedversion is Gordon (2002).

Figure 3. Productivity Growth in Four New Economy Industries, 1980–98

Source: Author’s calculations using Bureau of Economic Analysis data.

5

10

15

1985 1990 1995

Percent a year

Electronic and other electric equipment

Software

Industrial machinery and equipment

Telephone and telegraph

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 230

Gordon hypothesis (presented by Gordon in his comment on this paper)find that, outside of durable manufacturing, private business experiencedan acceleration of labor productivity growth of only 0.22 percentage pointfor the period 1995:4 to 2000:4 relative to the period 1972:2 to 1995:4;this estimate has drifted upward since Gordon’s early calculations.

The results developed here definitely reject the Gordon hypothesisover the period studied. For all three broad output concepts (GDP, thenonfarm business sector, and well-measured output), labor productivitygrowth in the economy excluding the new economy showed a markedupturn over 1995–2000 relative to the 1977–95 period (table 5). Theacceleration in non–new economy productivity growth was 0.85 percent-age point for the overall economy (measured from the income side),1.33 percentage points for nonfarm business output, and 0.80 percentagepoint for well-measured output (these can be calculated from the data intable 5). The new economy contributed directly about one-quarter of thetotal acceleration in labor productivity growth for total output, one-sixthfor nonfarm business, and two-fifths for well-measured output.

A final decomposition of productivity growth examines how mucheach industry contributes to the total. Table 6 does this for the nonfarm

William D. Nordhaus 231

Table 5. Productivity Growth with and without the New Economy for AlternativeMeasures of Aggregate Output, 1978–2000a

Percent a year

Change, Change, 1977–89 to 1977–89 to

Measure 1977–89 1989–95 1995–2000 1989–95 1995–2000

GDIWith new economy 1.21 0.96 2.24 –0.25 1.04Without new economy 0.84 0.56 1.60 –0.28 0.76Difference 0.37 0.39 0.64 0.03 0.27

Nonfarm business sectorWith new economy 1.26 1.26 2.87 0.00 1.61Without new economy 0.76 0.73 2.08 –0.03 1.32Difference 0.50 0.53 0.78 0.03 0.29

Well–measured outputWith new economy 2.00 1.93 3.29 –0.07 1.29Without new economy 1.38 1.21 2.13 –0.17 0.74Difference 0.61 0.72 1.16 0.10 0.55

Source: Author’s calculations.a. Growth in output per hour worked; data are annual averages. Details may not sum to totals because of rounding.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 231

business sector. For this calculation I measured productivity growth as thechain-weighted average of sectoral productivity growth rates; this is equalto the pure productivity effect plus the Baumol effect (see the discussionabove). This measure is the closest to the welfare-theoretical ideal of thedifferent indexes. The advantage of using this measure is that the sum ofthe individual-sector figures equals the total.

Not surprisingly, three of the four new economy sectors are among thetop ten contributors to the productivity upturn. Some of the other sectorsare more surprising. For example, retail and wholesale trade have eachmade a major contribution to overall productivity growth in the latestperiod. Indeed, the contribution of each of these two sectors to the accel-eration of productivity for the 1995–2000 period was larger than that ofany of the new economy sectors. The data in these sectors are somewhatof a mystery, however, which emphasizes the importance of closer atten-

232 Brookings Papers on Economic Activity, 2:2002

Figure 4. Contribution of New Economy Industries to Productivity Growth for theTotal Economy, 1977–2000a

Source: Bureau of Economic Analysis.a. Total economy is measured by income-side GDP. Estimates use nominal output weights.

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1977–89 1989–95 1995–2000

Industrial machinery and equipment

Electronic and other electric equipment

Telephone and telegraph

Software

Total

Percentage points

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 232

tion to measuring their output. At the bottom of the league, meanwhile,are food manufacturing, petroleum and coal, and nonfarm housing ser-vices. These sectors generally show a negative contribution because ofvery good productivity performance in the first subperiod followed by apoor performance in recent years.16 This is a reminder that the underlyingindustrial data are noisy and should be viewed as at best an approximationto the true performance.

Productivity growth in manufacturing has been an important contribu-tor to growth in aggregate labor productivity. Manufacturing productivity

William D. Nordhaus 233

16. These results are on the whole similar to the results of Jorgenson and Stiroh(2000a), who use an accounting framework that includes all inputs and explains the move-ment of gross output.

Table 6. Contribution of Selected Industries to Productivity Acceleration in theNonfarm Business Economya

Percent a year except where stated otherwise

Contribution toproductivityacceleration

Industry 1975–89 1995–2000 (percentage points)

LeadersRetail trade 1.30 5.25 0.46Security and commodity brokers 2.80 18.15 0.32Wholesale trade 2.80 5.86 0.27Electronic and other electric 8.49 17.87 0.23

equipmentOther real estate 1.01 5.64 0.18Other services –1.12 1.40 0.08Electric, gas, and sanitary services –0.08 2.59 0.08Industrial machinery and 7.17 13.07 0.08

equipmentSoftware 2.01 4.36 0.08Chemicals and allied products 2.56 4.87 0.06

LaggardsNonfarm housing services 2.52 –0.62 –0.06Petroleum and coal products 8.43 1.32 –0.07Other services 0.86 –1.59 –0.09Food and kindred products 3.85 –2.94 –0.15

All other n.a. n.a. 0.22

All industries 1.26 2.87 1.61

Source: Bureau of Economic Analysis data.a. New economy sectors are shown in boldface.

Productivity growth

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 233

growth clocked 4.1 percent a year in the 1977–95 period according to theincome-side data, and that rate moved up to 5.5 percent a year in the1995–2000 period. Figure 5 shows the major contributors by industry inmanufacturing. The importance of industrial machinery (notably comput-ers) and electronic machinery (notably semiconductors) is striking: thesetwo industries contributed 4.5 percentage points of the 5.5-percentage-point total growth.17 Manufacturing productivity growth outside of thenew economy was positive if modest.

On the other hand, the totality of non–new economy manufacturingindustries showed a marked productivity deceleration in the latestperiod, from 2.00 to 0.97 percent a year between 1977–89 and1995–2000. (This result was shown by Gordon using a different dataset.) Of this 1.03-percentage-point slowdown, food processing is respon-sible for 0.81 percentage point, which raises questions about either thedata or the performance of that industry. If the two major new economyindustries and the oldest old economy industry (food) are removed fromthe total, the latest data for manufacturing do not appear to show a majorchange in productivity growth. It seems reasonable to conclude, as hasbeen argued by Gordon, that up through 2000 the acceleration in manu-facturing productivity was limited to the two major new economy sectorsled by computers and semiconductors.

Qualifications

The present study is but one of many that have analyzed recent produc-tivity trends and the role of the new economy. Before concluding, it willbe useful to highlight some of the qualifications that attach to the results.

To begin with some technical details, the data for this study pertainexclusively to gross product (that is, value added), which is derived fromthe industry accounts and primarily based on income rather than productdata. Moreover, in these data the nominal output data are directly esti-mated from income data, whereas the real output data are derived fromgross output and intermediate inputs by double deflation.18 In the aggre-

234 Brookings Papers on Economic Activity, 2:2002

17. Within SIC 35 and 36, appendix table A2 shows the major data on shipments andthe price of shipments. The industries with sharply falling price indexes have hedonictreatment.

18. Yuskavage (2000, 2002).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 234

gate, the income-side industry data differ from the conventional product-side data by the statistical discrepancy; this discrepancy has moved insuch a way that nominal GDI grew 0.33 percentage point a year morerapidly than nominal GDP over the 1995–2000 period. Additionally,because of technical issues involving aggregation and differences indeflators, estimates of chained real GDP based on industry real grossproduct numbers differ somewhat from product-side real GDP even aftercorrecting for the statistical discrepancy. Finally, the industry accounts

William D. Nordhaus 235

Figure 5. Contribution to Manufacturing Productivity Growth by Industry,1995–2000a

Source: Bureau of Economic Analysis.a. Each bar measures productivity growth in one industry times the share of that industry in total manufacturing output. Shaded

bars indicate new economy industries.

0.0 0.5 1.0 1.5 2.0 2.5

Lumber and wood products

Percentage points

Furniture and fixtures

Stone, clay, and glass products

Primary metals

Fabricated metal

Industrial machinery

Electronic and electrical

Motor vehicles

Other transport

Instruments

Miscellaneous manufacturing

Food and kindred products

Tobacco products

Textile mill products

Apparel and other textile products

Paper and allied products

Printing and publishing

Chemicals and allied products

Petroleum and coal

Rubber and miscellaneous plastics

Leather and leather products

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 235

are on a different revision cycle from the product accounts, and it seemslikely that some of the downward product account revisions in mid-2002will also occur in the industry accounts revision.

From an operational point of view, the major implication of usingincome-side industry data is that real GDI calculated from these data isestimated to have grown faster than the usual product-side estimates.Over the 1995–2000 period, real income-side GDI had an average annualgrowth rate of 4.46 percent, versus 3.95 percent for real GDP, for anaverage difference of 0.51 percentage point. Since this difference is asubstantial part of the 1.04-percentage-point acceleration in GDI produc-tivity, these numbers are subject to substantial uncertainty and potentialrevision.

A second qualification is that the productivity estimates presented hererefer to gross product (value added) rather than total output—the differ-ence being purchased goods and services. In principle, there should be nodifference between the two approaches if the aggregation technique andthe source data are perfect, since it makes no difference whether theweighted sum of inputs is subtracted from the left side or the right side ofthe total factor input productivity equation. Subtle differences can creepin, however, if purchased goods and services are not measured accuratelyor if the index numbers suffer from aggregation nonneutrality,19 both ofwhich apply to the data and to the Fisher indexes. I am unaware of anystudies indicating which approach is less prone to aggregation nonneutral-ity or which approach is more accurate given the inaccuracies of thesource data on purchased goods and services.

A third and more important qualification concerns omitting the contri-bution of capital services to the productivity upturn. This omission is par-ticularly important given the substantial increase in measured capitalservices in recent years. Studies by Stephen Oliner and Daniel Sichel,Dale Jorgenson, and Kevin Stiroh, among others, suggest that most if notall of the acceleration in labor productivity in the late 1990s was due tocapital deepening.20

Although estimating total factor productivity is a central technique forunderstanding trends in productivity, labor productivity also has a useful,

236 Brookings Papers on Economic Activity, 2:2002

19. An index is aggregation neutral if F(x1, x2, x3, x4) = F[F(x1, x2), F(x3, x4)] for all ele-mental series x1, x2, … , where F is an aggregator such as the Fisher or Tornqvist index.

20. Oliner and Sichel (2000); Jorgenson and Stiroh (2000a, 2000b); Jorgenson (2001);Stiroh (forthcoming).

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 236

independent role to play. To begin with, growth in labor productivity is acentral policy concern given its strong linkage to the growth of realwages. Moreover, from a technical point of view, it should be recalledthat total factor productivity depends upon estimating rather than measur-ing the inputs of capital services. Estimates of capital services dependupon several important and often-criticized assumptions. The majorassumptions implicit in this model include such things as the existence ofperfect rental markets for capital, no difference between ex ante and expost substitutability, no break-in or adjustment costs or learning costs,perfect competition, factor rewards proportional to marginal products,and so forth.

These assumptions are likely to be stretched particularly in periods,such as the late 1990s, when new technologies with very high rates ofdepreciation dominate the data on the growth of capital services. Fur-thermore, measures of capital services generally use a cost-of-capitalformula based on interest rates and therefore do not reflect the extraordi-nary equity valuations of the late 1990s; the effect of this is to overesti-mate the user cost and implicit marginal cost of capital, particularly inhigh-technology industries. The data for this period are especially prob-lematical given that the high-technology stock market bubble probablyled to overinvestment in several sectors, telecommunications in particu-lar, and that some of the investments (such as the ominous sounding“dark fiber”) turned out to be useless and have zero productivity.

A final shortcoming is that the production function includes only thereturn to fixed capital as a nonlabor market input. It excludes the return toother assets such as land, inventories, intangible assets (such as patentsand trademarks, brand value, and marketing), and subsoil assets such asoil and gas reserves. Given the list of unrealistic assumptions that under-lie the total factor productivity model, it is useful to examine techniques,such as estimation of labor productivity, that do not depend on the multi-tude of assumptions that underpin that model.

One can illustrate the issues involved in moving from labor productiv-ity to total factor productivity by estimating the extent to which capitaldeepening was associated with the recent changes in labor productivity.For this question I looked at the relationship between output growth andthe growth of labor and capital inputs over the 1977–2000 period in thosetwenty-nine industries included in well-measured output for which theBEA prepares net capital stock data. Pooling the data with industry and

William D. Nordhaus 237

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 237

time effects along with cross-sectional equation weighting yields the fol-lowing estimated equation:

R2 = 0.515; n = 667,

where g(Xi,t ), g(Li,t ), and g(Ki,t ) are growth of gross output, growth ofhours worked, and growth of the net capital stock, respectively, for indus-try i in year t.

If the assumptions underlying the calculation of total factor productiv-ity were correct, the coefficients on g(Li,t ) and g(Ki,t ) should correspond tothe factor shares in the different industries. Although the coefficient onlabor is close to the average share of compensation for all industries, thecoefficient on capital is negative. This equation indicates that the acceler-ation in the net capital stock made a small but insignificant negative con-tribution to the growth of gross output in these industries in the sampleperiod. Since the average share of property-type income is around 40 per-cent of total output, the estimated coefficient is around four standarderrors from accepting the null hypothesis that the coefficient equals theincome share of capital; this indicates that, although the coefficient is notwell determined, it is significantly different from the theoretical assump-tions that underpin the calculation of total factor productivity.

An alternative specification defines capital inputs as proportional to thedepreciation of fixed capital plus an opportunity cost of fixed capital; thisspecification, however, did not improve the estimates on capital growth.The coefficient on capital in this specification was very close to zero, witha standard error of the coefficient of 0.048, again significantly differentfrom the theoretical coefficient of around 0.4. Other specifications did notcome to the rescue of the standard model.

These results should not be taken too seriously, as they involve a highlyoversimplified specification of the link between capital and productivity.Moreover, they do not affect the accounting relationship involved in totalfactor productivity indexes that depend basically on some identities and ahost of underlying assumptions. But they should caution practitioners thatthe empirical relationship between the capital stock or capital services andproductivity is at best weak and at worst unrelated to the model underlyingtypical total factor productivity calculations.

g X g L g Ki t i t i t( ) . ( ) – . ( )( . ) ( . )

, , ,= +0 605 0 03080 049 0 085

industry effects + year effects

238 Brookings Papers on Economic Activity, 2:2002

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 238

A final qualification concerns the role of business cycles in productiv-ity growth. This issue is particularly relevant given the strong economicexpansion during the 1995–2000 period. Annual growth of real GDPaveraged 4.0 percent in that period, compared with 2.9 percent in the1977–95 period. The reason for concern is that productivity growth hastypically been procyclical.

I have not undertaken a systematic assessment of the cyclical effectsfor the industry data. Doing this would require confronting the potentiallyserious estimation bias due to measurement errors in output at the indus-try level. For example, because of data peculiarities involving indirecttaxes, the gross output of the tobacco industry fell by 63 percent (in loga-rithmic terms) in 1999. Productivity in that year also fell sharply, by53 percent, primarily because of the strange output numbers. Not surpris-ingly, therefore, there is a strong positive association of output and pro-ductivity in tobacco manufacturing.

A full investigation of the cyclical properties of productivity on anindustry level is beyond the scope of this study. It is possible, however, toperform two simple tests to determine whether introducing an aggregatecyclical term in the industry productivity equations changes the pattern ofproductivity growth shown in the tables and figures. For the first test Iestimated a productivity equation adding the growth of real GDP, as aproxy for aggregate cyclical conditions, into industry equations. The ideahere is that shocks to aggregate demand will change real GDP in the shortrun, and these changes in real GDP will in turn affect the demand for out-put in different industries. This test led to the following result:

R2 = 0.256; n = 667.

This test is not entirely satisfactory because the estimates from thepooled regressions are inverse variance-weighted averages of industryproductivity growth rates rather than averages weighted by nominal out-put shares. The coefficient estimates will therefore not correspondexactly to the aggregate productivity estimates in the tables and figures.Moreover, there will be some residual spurious correlation betweenaggregate output and industry output. Nonetheless, the test is illumi-nating. It is clear that introducing growth of real GDP as a cyclical vari-

g A gi t t( ) . ( )( . )

, = +industry effects GDP0 0930 060

William D. Nordhaus 239

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 239

able makes very little difference to average productivity growth. Thecoefficient on aggregate output indicates that a 1 percent increase inaggregate output would increase productivity in the average industry byonly 0.09 percent. Real GDP grew at a rate of 0.80 percentage point a yearfaster in 1995–2000 than the average for the sample period. This indicatesthat the rapid growth in the 1995–2000 period raised average productivitygrowth by 0.072 percentage point; this compares with an acceleration of0.44 percentage point in GDP productivity and 0.92 percentage point inGDI productivity.

An alternative approach is to use the overall unemployment rate as thecyclical variable; this approach has the advantage of completely removingany spurious measurement error that infects both aggregate and industryoutput. Additionally, it is particularly illuminating to the extent thatmovements in the unemployment rate are a good index of movements inaggregate demand. This equation yields

Using the unemployment rate as a cyclical variable indicates thatindustrial productivity is anticyclical. Using an Okun’s Law coefficient of2, this equation indicates that growth in aggregate output by 1 percentwould decrease productivity in the average industry by 0.1 percent.

In summary, although these tests of the cyclical impact are hardlydefinitive, they do suggest that, on average, cyclical forces played but asmall role in the productivity upsurge in the 1995–2000 period. However,more work needs to be done at the industry level to test the role of cycli-cal conditions.

Conclusion

This paper has considered issues in the recent behavior of productivityand productivity growth. The major points can be summarized as follows.

First, the paper introduces a new approach to measuring industrial pro-ductivity. It develops an income-side database on output, hours worked,and labor productivity, relying on data published by the BEA. The data

g A U

R n

i t t( )( . )

. ; .

, =

= =

industry effects + 0.218 0 084

0 253 6672

240 Brookings Papers on Economic Activity, 2:2002

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 240

are internally consistent and add up to income-side GDP. The advantageof the unified income-side measures is that they present a consistent set ofindustrial accounts. The disadvantage is that they are available only forthe period 1977–2000.

Second, the paper presents a set of labor productivity measures for fourdifferent definitions of output:

—GDP from the income side (GDI)—The BLS’s nonfarm business sector output from the income side—A new measure called well-measured output, which includes only

those sectors for which output is relatively well measured—The “new economy.”Third, there has definitely been a rebound in productivity growth since

1995. The rebound is observed in all three broad aggregates developed forthis study. The labor productivity acceleration in the last five years of theperiod (1995–2000) relative to the 1977–95 period was 1.12 percentagepoints for income-side GDP, 1.61 percentage points for the nonfarm busi-ness sector, and 1.31 percentage points for well-measured output.

Fourth, the paper explores a new technique for decomposing changesin labor productivity growth by source. This decomposition identifies apure productivity effect (which is a fixed-weighted average of the produc-tivity growth rates of different industries), a Baumol effect (which cap-tures the effect of changing shares of nominal output on aggregateproductivity), and a Denison effect (which captures the interactionbetween the differences in productivity growth and the changing hoursshares of different industries over time). Total productivity growth is thesum of these three effects.

Fifth, the estimates show that the pure productivity effect in recentyears has exceeded total productivity growth. For example, in the non-farm business sector for the period 1995–2000, total labor productivitygrowth was 2.87 percent a year, and the pure productivity effect was3.09 percent a year. The difference was due to a mixture of the Baumoland Denison effects. Moreover, in analyses using the data for all indus-tries, the Baumol effect has been very close to zero over this period, indi-cating that composition shifts in output have had little effect on aggregateproductivity growth over the last quarter century.

Sixth, a key question is the contribution of the new economy to theproductivity rebound. For the purpose of this study I have defined thenew economy as machinery, electric equipment, telephone and tele-

William D. Nordhaus 241

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 241

graph, and software. These sectors grew from 3 percent of real GDP in1977 to 11 percent in 2000. Productivity growth in the new economy sec-tors has made a significant contribution to economy-wide productivitygrowth. In the nonfarm business sector over the last five years, labor pro-ductivity growth excluding the new economy sectors was 2.08 percent ayear compared with 2.87 percent a year including the new economy.

Seventh, the major new economy contributors to the productivityrebound have been nonelectric and electric machinery, the major sub-sectors of which are computers and semiconductors. These two sectors,which accounted for less than 4 percent of nominal GDP, contributed0.56 percentage point to income-side GDP productivity growth of2.24 percent a year in the 1995–2000 period.

Finally, to what extent has there been an acceleration of productivitygrowth outside the new economy? According to all three output measures,there has been a substantial upturn in non–new economy productivitygrowth. After the new economy sectors are stripped out, the productivityacceleration from 1977 to 1989 was 0.76 percentage point for income-side GDP, 1.32 percentage points for business output, and 0.74 percent-age point for well-measured output. It is clear that the productivityrebound is not narrowly focused in a few new economy sectors.

242 Brookings Papers on Economic Activity, 2:2002

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 242

William D. Nordhaus 243

Table A1. Value Added by Information Technology Industries, 1995 and 1998Millions of current dollars except where stated otherwise

Industry SIC code 1995 1998

HardwareComputers and equipment 3571,2,5,7 32,931.2 45,081.8Computers and equipment, wholesale sales 5045 (part) 50,756.0 74,173.3Computers and equipment, retail sales 5734 (part) 2,513.6 3,441.3Calculating and office machines, n.e.c.a 3578–9 3,036.2 3,478.1Electron tubes 3671 1,472.9 1,716.8Printed circuit boards 3672 5,718.5 7,602.8Semiconductors 3674 51,272.0 70,092.0Passive electronic components 3675–9 19,097.6 29,801.9Industrial instruments for measurement 3823 4,998.5 5,546.9Instruments for measuring electricity 3825 7,512.3 8,399.0Laboratory analytical instruments 3826 4,270.6 4,780.9

Total 183,579.6 254,115.0

Software and servicesComputer programming services 7371 26,178.3 n.a.b

Prepackaged software 7372 19,971.7 n.a.Prepackaged software, wholesale sales 5045 (part) 2,564.0 n.a.Prepackaged software, retail sales 5734 (part) 126.1 n.a.Computer integrated systems design 7373 15,025.1 n.a.Computer processing and data preparation 7374 17,924.5 n.a.Information retrieval services 7375 3,768.5 n.a.Computer services management 7376 2,135.2 n.a.Computer rental and leasing 7377 1,329.0 n.a.Computer maintenance and repair 7378 5,023.7 n.a.Computer-related services, n.e.c. 7379 8,549.1 n.a.

Total 7371–9 102,595.2 151,999.3

Communications hardware Household audio and video equipment 3651 2,343.0 2,767.6Telephone and telegraph equipment 3661 14,925.2 17,373.7Radio and television and communications 3663 19,862.0 27,854.3

equipmentMagnetic and optical recording media 3695 2,787.8 3,293.0

Total 39,918.0 51,288.0(continued)

A P P E N D I X A

Supplemental Tables

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 243

244 Brookings Papers on Economic Activity, 2:2002

Table A2. Shipments by Selected New Economy Industries and Changes in OutputPrices, 1987–98Units as indicated

Change in price Shipments, 1998 index, 1987–98a

Industry SIC code (millions of dollars) (percent a year)

SIC 35Electronic computers 3571 74,720 –17.9Computer storage devices 3572 15,734 –7.2Computer terminals 3575 1,180 –10.7Computer peripheral equipment, 3577 31,100 –12.0

n.e.c.Calculating and accounting 3578 2,308 –1.5

machinesTotal for included industries 125,042 –14.5Total for SIC 35 442,315 –2.3

SIC 36Household audio and video 3651 9,882 –1.0

equipmentPhonograph records and audio 3652 2,504 –0.1Telephone and telegraph apparatus 3661 40,080 –3.4Printed circuit boards 3672 12,916 –2.0Semiconductors 3674 86,189 –20.1Electronic components, n.e.c. 3679 39,790 –1.5Magnetic and optical recording 3695 5,143 –1.0

mediaTotal for included industries 196,504 –7.4Total for SIC 36 375,968 –4.2

Source: Bureau of Economic Analysis at www.bea.doc.gov/bea/dn2/gpo.htm.a. Price indexes for totals are “mongrels” rather than true chain indexes, and they double-count because they are based on

gross output rather than value-added weights.

Table A1. Value Added by Information Technology Industries, 1995 and 1998(continued)Millions of current dollars except where stated otherwise

Industry SIC code 1995 1998

Communications servicesTelephone and telegraph communications 481,22,99 144,100.0 163,674.4Radio broadcasting 4832 6,149.6 8,695.8Television broadcasting 4833 17,102.7 20,975.6Cable and other pay television services 4841 24,247.7 31,838.3

Total 191,600.0 225,184.0

All information technologies 517,692.8 225,184.0As a share of the economy (percent) 7.1 8.1

Source: U.S. Department of Commerce (2000).a. Not elsewhere classified.b. Not available.

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 244

Comments andDiscussion

Robert J. Gordon: Economists were slow to recognize the post-1995productivity growth revival in its early stages. Those of us who partici-pated in panels on productivity issues at the January 1998 meetings of theAmerican Economic Association recall no such recognition. Rather therewas a singular focus on explaining the long, dismal period of slow pro-ductivity growth dating from 1972, especially in the context of RobertSolow’s much-cited quip that “we can see the computer age everywhereexcept in the productivity statistics.” From today’s perspective it is under-standable that several years had to elapse before the post-1995 revivalcould be distinguished from previous short-lived upward blips in produc-tivity growth such as occurred in 1991–92.

Since 1999, however, the analysis of the post-1995 revival hasbecome a growth industry, featuring an outpouring of analyses thatattempt to quantify the sources of the revival, and especially the contri-bution of the “new economy,” that is, of investment in information tech-nology (IT). The paper by William Nordhaus joins a substantial literaturethat assesses the role of the new economy in the revival; it also providesoriginal analyses of other aspects of the revival that have previously beenignored. I will begin by discussing Nordhaus’s findings on these otherissues and then turn to his controversial treatment of the new economy’scontribution. Along the way I will try to reconcile Nordhaus’s finding ofa small new economy contribution with contrasting results in research bySteven Oliner and Daniel Sichel that the new economy overexplains therevival. I will conclude with the suggestion that Oliner and Sichel mayhave exaggerated the role of IT investment in the revival, thus leaving

245

1017-04 BPEA/Nordhaus 12/30/02 15:01 Page 245

open some support for Nordhaus’s contrary conclusion, through anotherline of reasoning.

Nordhaus’s paper is based on what he calls a “new approach to mea-suring industrial productivity.” This measures productivity as the ratio ofreal value added by industry divided by hours of labor input, with both thenumerator and denominator taken from published tables in the NationalIncome and Product Accounts (NIPA). As Nordhaus emphasizes in hisconcluding section, this industrial decomposition of productivity growthin the NIPA provides a measure of the income side of GDP, which issmaller than the product side of GDP by the amount of the NIPA statisti-cal discrepancy. Since the statistical discrepancy shifted from 0.4 percentof GDP in 1995 to –1.3 percent in 2000 (that is, the income measure wassmaller than the product measure in 1995 and larger in 2000), the exclu-sive use of income-side measures in Nordhaus’s paper adds 0.34 percent-age point a year to the annual growth rate of productivity during the1995–2000 interval compared with studies based on product-side data.

Three caveats apply to his approach. First, it differs from other analy-ses, for example those in the 2000 and 2001 Economic Report of the Pres-ident, which regard an average of the product-side and the income-sidemeasures as superior to exclusive reliance on one or the other; to use onlythe income-side measure assumes knowledge about the sources of the sta-tistical discrepancy that does not exist. Second, this approach is not“new.” Use of NIPA data to analyze productivity behavior by industrygoes back at least three decades to Nordhaus’s own pioneering paper onthis topic,1 if not before, and the same data have been compiled in thesame way in several recent papers.2 Third, Nordhaus’s database is limitedto output and hours and contains no information on capital input by indus-try; so, unlike the recent paper by Jack Triplett and Barry Bosworth,3