Product intervention: Consumer protection agenda - Global …€¦ · Product intervention Consumer...

12

Product intervention Consumer protection agenda: Global regulatory reform

Transcript of Product intervention: Consumer protection agenda - Global …€¦ · Product intervention Consumer...

Product intervention Consumer protection agenda: Global regulatory reform

1 Product intervention Consumer protection agenda: Global regulatory reform

In pursuit of its objectives to protect consumers, the Financial Conduct Authority (FCA) is taking an increasingly interventionist approach to product design, governance and oversight with the aim of anticipating consumer detriment where possible and stopping it before it occurs.There is no doubt that this is high on the regulatory agenda. The FCA is already asserting its authority in this area where it believes the approach being taken by firms to product design, approval, delivery and review is not sufficiently robust. Interventions that have already taken place include:

► Instructions to amend products ahead of launch

► Requests for copies of product governance processes

► Requests for explanations and clarification of product features

It has also been given new statutory powers to ban products on a temporary basis without consultation. Product intervention will apply across the life cycle of a product, and firms will need defined controls in place to manage products at every stage.

2Product intervention Consumer protection agenda: Global regulatory reform

The rationale for interventionRetail regulation traditionally focused on information provided at the point of sale on the premise that, if sales processes are fair and product disclosures are transparent, the results would be effective customer protection. However, “waves of major customer detriment”, such as PPI and endowment mis-selling and interest rate hedging products, show that reactive regulation has not been sufficiently effective.

Product intervention is based on the premise that disclosure is not sufficient given consumer behaviors. It is about moving toward being proactive rather than reactive. The ultimate intention is to complement the traditional focus on sales and marketing and the disclosure of information throughout the product life cycle. The product intervention regime recognizes that decisions taken by firms when designing new products, and managing existing products, have an impact on subsequent distribution and consumer outcomes. The interventionist regime will apply to all product types and sectors.

Product intervention is an integral part of the FCA’s consumer protection strategy, which is closely aligned to what is happening throughout Europe. It is designed to ensure the retail market works better for consumers and to increase confidence in the financial services sector. Firms need to be prepared for the challenge.

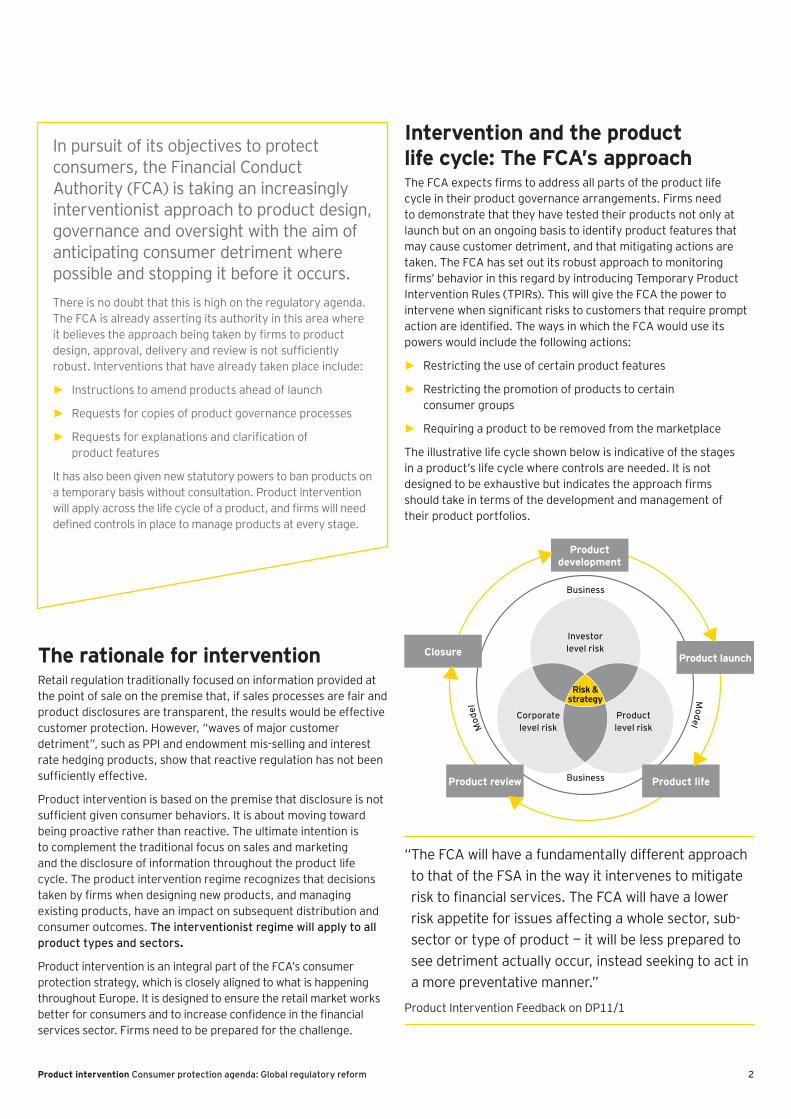

Intervention and the product life cycle: The FCA’s approachThe FCA expects firms to address all parts of the product life cycle in their product governance arrangements. Firms need to demonstrate that they have tested their products not only at launch but on an ongoing basis to identify product features that may cause customer detriment, and that mitigating actions are taken. The FCA has set out its robust approach to monitoring firms’ behavior in this regard by introducing Temporary Product Intervention Rules (TPIRs). This will give the FCA the power to intervene when significant risks to customers that require prompt action are identified. The ways in which the FCA would use its powers would include the following actions:

► Restricting the use of certain product features

► Restricting the promotion of products to certain consumer groups

► Requiring a product to be removed from the marketplace

The illustrative life cycle shown below is indicative of the stages in a product’s life cycle where controls are needed. It is not designed to be exhaustive but indicates the approach firms should take in terms of the development and management of their product portfolios.

Product development

Business

Business

Product launchClosure

Product review Product life

Risk & strategy

Investor level risk

Corporate level risk

Product level riskM

odel

Model

“ The FCA will have a fundamentally different approach to that of the FSA in the way it intervenes to mitigate risk to financial services. The FCA will have a lower risk appetite for issues affecting a whole sector, sub-sector or type of product — it will be less prepared to see detriment actually occur, instead seeking to act in a more preventative manner.”

Product Intervention Feedback on DP11/1

3 Product intervention Consumer protection agenda: Global regulatory reform

Product intervention throughout EuropeThe European Union and Member States across Europe are also responding to the financial crisis and enhancing customer protection through EU-level regulation. MiFID II, the Insurance Mediation Directive and the PRIPS proposals will define rules relating to product transparency (pre-contractual disclosure)and selling practices. These include:

► Powers to ESMA to intervene in local markets to ban certain products and practices temporarily

► New powers for national regulators to ban the sale of products where there is evidence or potential for customer detriment

► Increasing the requirements to prevent complex funds being sold without an assessment of their appropriateness for the client

► Enhanced definition of what constitutes a non-complex product sale where a retail suitability assessment is not required

► Defining rules relating to product transparency (pre-contractual disclosure)

Ahead of EU-level regulations, national regulators such as Belgium and Denmark have put in place their own initiatives to strengthen customer protection.

In addition, European Supervisory Authorities have published several documents on the subject of product intervention, most notably the Joint Position on Product Oversight and Governance Processes, which outlines key considerations that should be considered by firms designing and/or distributing products. In addition it highlights the importance of reviewing these processes and ensures correct operations of these products on the behalf of their customers.

Strategy and business modelA firm’s strategy sits at the heart of the firm’s ability to successfully meet the regulator’s objectives and should be reviewed alongside its business model to ensure both are aligned.

The regulator will want to review how a firm’s strategy is reflected in its business model and will interrogate firms’ business models to identify the conduct risks that may be inherent in them, often using a “follow the money” approach. Firms will also need to evidence how they have developed their product strategy. This is likely to include evidencing:

► Who their target market is

► The rationale for the products being sold

► Why the method of distribution is appropriate

► The systems and controls a firm has to ensure the product is meeting the desired objectives

However, the firms’ responsibilities do not stop there. A firm should build into their product business model and strategy post-launch reviews and feedback loops to ensure the product is working in practice and getting into the hands of the right people. Lastly, firms will need to build in the ability to remove products in response to imminent customer detriment.

4Product intervention Consumer protection agenda: Global regulatory reform

Value for money — pricingThe FSA’s 2012 Retail Conduct Risk Outlook continues to highlight concerns previously raised in their 2011 Retail Conduct Risk Outlook, particularly about products that may have limited value.These include:

► Bundled products

► General insurance products that have limited use to customers

A firm will need to consider how the pricing of products will feature in their business model. The FCA has expressed concerns about products that generate high revenue for firms but offer little value to customers: “the regulation of firms was not able to overcome the inherent conflict of interest that arises in financial transactions. PPI is a clear example of this — hugely profitable to firms; of limited value (most of the time) to individuals.” Another example of abuse with regards to value for money of pricing includes the recently emerged toxic loans that were bundled on to mortgage securities sold by a leading investment bank. Currently it faces a record-breaking £8b fine with regulators. The impact surfaced during 2008 when the housing market plunged, resulting in major customer detriment that helped lead to a financial crisis.

Product governanceThe importance of product development and product manufacture within the governance arrangements of the firm need to be considered. Firms must ensure that governance arrangements take full account of product issues and that oversight and reporting arrangements are fit for purpose. Lack of governance in particular with regards to product development and marketing processes increases the risk of firms developing poorly designed products. This, in turn, would inevitably lead to mis-selling, highlighting the need for firms to place product governance at the core of their business models and thus ensure that strategies aligned with governance are integrated and embedded.

The control environmentFirms should not underestimate the importance of understanding the life cycle of each product they manufacture, market, sell, and/or administer, to avoid customer detriment and large-scale remediation exercises. A complete understanding of the target market, risks and demographic that is actually purchasing the product is vital. Firms need to ensure controls are in place to manage these issues throughout the life cycle, and that full account is taken of risks that, when aggregated, indicate the risk profile of a product is higher than was originally foreseen.

5 Product intervention Consumer protection agenda: Global regulatory reform

Existing products also need to be considered and so firms need to take account of the different strategies to be adopted depending on whether the product is existing, part of the legacy book, or in development. Some of the differing factors that need to be taken into account include:

New products Existing products

Product stress testing Risk identification

Outcome testing Distribution strategies

Product profitability Ongoing review

Target market assessment Product performance

Management information Management information

Operational requirements Customer service offering

Legacy books of business may pose particular problems for firms where the products within them have not been subject to the same strict governance processes that the FCA now expects. Firms need to ensure they fully understand any product risks within their legacy books of business and that they are tackled where and when necessary. In addition, products that are closed to new business but are open for existing customers to “top-up” or switch from, will also need to be considered in light of current regulatory standards and managed appropriately, where applicable.

In addition, products that are closed to new business but are open for existing customers to “top-up” or switch from will also need to be considered in light of current regulatory standards and managed appropriately, where applicable.

Firms need to pay particular attention where legacy products are outside their current product strategy or where products are sold to groups of customers that do not fit their strategy for ongoing market penetration. These issues may result in the firm taking on customers whose needs they are unable to address in the longer term, or whose expectations may not be met by either the product they have purchased or the service they receive. The current low-interest-rate environment in the UK is bringing this issue to light as investors move out of deposits into structured and other products that carry an increased investment risk to chase potentially higher returns.

6Product intervention Consumer protection agenda: Global regulatory reform

7 Product intervention Consumer protection agenda: Global regulatory reform

Common points of failureIn our experience, there are a number of common points of failure across both development and management activities, including:

► Not identifying the target market: firms frequently market products without a clear understanding of who should be purchasing the product and why it is suitable for that group.

► Failure in risk profiling: firms fail to risk-rate products appropriately, which can lead to products being sold to the wrong customers, who are unaware of the potential volatility of the product or the potential risk of loss of investment. For example, structured complex products being marked as “medium” risk targeted to customers whose level of sophistication is out of line with the risk profile of the product, i.e., a customer with a low risk appetite.

► Failure to recognize responsibility of a product by those in the distribution chain: even when a value chain is heavily intermediated, the FCA doesn’t expect that those further down the chain to say that they have no responsibility for the end client — firms will be expected to show that they have considered their target market and take steps to ensure that the product is not sold outside that market. The distribution strategy needs to be appropriate; they need to be honest with distributors about the nature of the product and have some responsibility for ensuring that the intermediaries understand and are competent to offer such products. In addition, it is required that all those within the chain are aware of and understand any changes in the nature of the product.

► Failure to understand distribution chain: confusion between manufacturers and distributors of products may lead to required disclosure of product features and risks not effectively relayed from manufacturers to distributors as well as miscommunication regarding correct target audience for products. In addition, a lack of clarity as to who is accountable for each stage of the distribution chain may arise.

► Fee charging structure: firms need to clearly disclose the end-to-end fee charging structure of products, where applicable, to customers to ensure that prices are clear and transparent from the beginning of the transaction. The level of disclosure should have due regard to the sophistication of the target customer.

► Failure to disclose: firms must ensure that all disclosures regarding performance of the product due to prevailing market conditions have been communicated clearly and in good time to customers. This includes clear statements about how the product is likely to perform in different market conditions and drawing particular attention to the fact that reliance on past performance of the product is not always an indicator of future performance.

► Pricing structure: firms should review the pricing structures of previous, existing and new products to ensure that hidden mark-ups are not embedded within the pricing where there is little or no real value to the end customer or that particular component.

► Excessive reliance on add-on products: “Add-ons” refer to any product sold alongside another product, which are also commonly known as packaged products — for example, current accounts with added mobile phone insurance or travel insurance. The terms for the tied product can be, or become, uncompetitive and may not be required by the customer. Institutions rely on these ancillary revenues to increase the profitability of the main product (due to the low-cost production and easy maintenance of the tied product), but often without ensuring that appropriate controls and assessment are in place for their sale. The FCA has called for tighter regulations on the sale of these add-ons in particular to insurance policies.

► Failure to monitor who is purchasing the product: where the target market has been identified firms fail to ensure it is being sold to that market.

► Failing to act where it is identified that a product is being mis-sold: the FCA has already identified that firms are slow to remove or amend products where failings are identified and conduct adequate remediation on consumers impacted.

► Underestimating product sales following launch: where take-up is underestimated customer service offerings suffer.

► Not investigating reasons for higher-than-expected sales: higher-than-expected sales may be an indication the product is being purchased by groups of customers outside the intended target market.

8Product intervention Consumer protection agenda: Global regulatory reform

► Reward and incentivization: strategies that do not take account of the need to balance quality against sales performance may lead to inappropriate sales.

► Failing to update product guidance to take account of economic factors: factors outside of the firms’ control can often lead to products becoming attractive for groups they weren’t intended for or unattractive to groups to whom they have already been sold.

► Ineffective Root cause analysis: failing to take account of expressions of dissatisfaction in identifying product failings.

► Failing to include the option to withdraw from products or markets even where management information indicates this should be considered: this should be actively considered, particularly where existing strategies are causing customer detriment.

► Failure to adequately stress-test products: firms will need to stress-test products under different scenarios. This should not just be at product development stage but at different stages once the product has embedded.

► Insufficient outcomes testing and management information: firms need to ensure rigorous outcomes testing to see how products are likely to behave in different market conditions as well as to monitor whether products have been sold appropriately to the right customers. The appropriate analysis of this information should be used to inform customers and others in the value chain and where relevant to drive ongoing improvements for the customer and the firm.

► Not tracking regulatory changes: firms will need to keep track of the different regulation being implemented by their home regulators, the EU and national regulators where their products may be sold.

► Due diligence: firms will need to ensure the appropriate level of due diligence is undertaken to understand the potential product risks that may be inherent in a proposed acquisition.

Development instigation

Checkpoint one

Checkpoint two

Post-launch review

Regular checkpoints

Issue identification Closure

Market testing

Product specification

Initial business case proposal

Target market identified

Market testing outcome

Distribution strategy

Marketing material

Training — sales and service

MI developed

Servicing issues identified

MI review Review/challenge key metrics

Ongoing client management

Sales issues identified

Defined governance process including stress and scenario testing and profitability reviews

Sales vs. target market review

Distribution strategy/Incentives

Proposals for resolution Run off plan

Laun

chDesign and build

Key metrics defined

Distribution strategy ratified

Product design ratified

Product and customer strategy

Go/no go decision

Go/no go decision

9 Product intervention Consumer protection agenda: Global regulatory reform

Recommended next stepsWhile there are a number of commercial pressures and regulatory priorities, as a minimum, firms should focus on the following:

► A review of their product strategy and business model

► A review of their product governance arrangements

► A review of product development processes

► Existing product book review

► Closed-book reviews

► A review of the risk rating of products

► Define MI requirements to support ongoing product governance

A review of product strategy should be completed to ensure that the target market groups for products marketed match your strategy and long-term customer acquisition targets.

By proactively managing your firm’s regulatory product risk it is less likely that you will be subject to regulatory remediation or the sanctions that the FCA can impose on firms or individuals (in significant influence functions) that are unable to demonstrate compliance.

How EY can helpWe have the most integrated EMEIA Financial Services practice. We can quickly deploy teams that are aligned to your market segment and can draw upon our full breadth of experience. Ways that we can help include:

► Advice on product strategy and business models

► Advice on governance arrangements

► Governance reviews

► Advice on product stress and outcome testing

► Risk reviews

► Distribution strategy reviews

► Product strategy reviews

► Outcome testing

► Product life cycle assessments

► Reviews of your root-cause analysis processes

► Review of reward and incentivization schemes

These are a sample of the services that we provide. We will of course work with you to tailor our services to meet your identified needs.

“I do not expect us to use this power frequently, but both industry and consumers need to be clear that we will not hesitate to use these powers where we have serious concerns.”

Martin Wheatley, Chief Executive of the FCA. March 2013

10Product intervention Consumer protection agenda: Global regulatory reform

Responding to Global Regulatory Reform In response to the financial crisis, and the relentless pace of regulatory change, we have teams of dedicated professionals across the globe looking at the key challenges of Global Regulatory Reform (GRR). Our GRR focus includes personnel skilled in regulation, risk, performance management, tax, assurance, and transactions, who work together to deliver insights and thought leadership to our clients to help them determine the best response to their immediate and longer term business needs. Our global network of professionals offers an integration of regulatory and technical skills that sets us apart in advising and helping clients to achieve compliance and growth.

To access insights on Global Regulatory Reform and how we can help visit: www.ey.com/financialreform

For further information contact:Retail banking firms

Jenny Clayton Partner + 44 20 7951 9016 [email protected]

Nahid Kausar Director + 44 20 7951 5793 [email protected]

Heather Alleyne Director + 44 20 7951 3827 [email protected]

Asset managers, wealth managers and private banking

Tim Rooke Partner + 44 20 7951 1472 [email protected]

Anthony Kirby Director + 44 20 7951 9729 [email protected]

Insurance firms

Steve Southall Executive Director + 44 20 7951 1004 [email protected]

David Nancarrow Senior Manager + 44 20 7951 7377 [email protected]

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2014 EYGM Limited. All Rights Reserved.

EYG No. CQ0157

1378999.indd (UK) 06/14. Artwork by Creative Services Group Design.

ED 0615

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com