Process-Costing Chapter 8 Systems. Process costing Characteristics Identical units Continuous...

27

Process-Costing Process-Costing Chapter 8 Chapter 8 Systems Systems

-

Upload

eugene-weaver -

Category

Documents

-

view

231 -

download

0

Transcript of Process-Costing Chapter 8 Systems. Process costing Characteristics Identical units Continuous...

Process-CostingProcess-Costing

Chapter 8Chapter 8

SystemsSystems

Process costing

CharacteristicsIdentical units

Continuous flow productionNever “complete”

Move from process (or department) to process

Costs are accumulated by process for a time periodAllocated to “equivalent units” of output during the

period

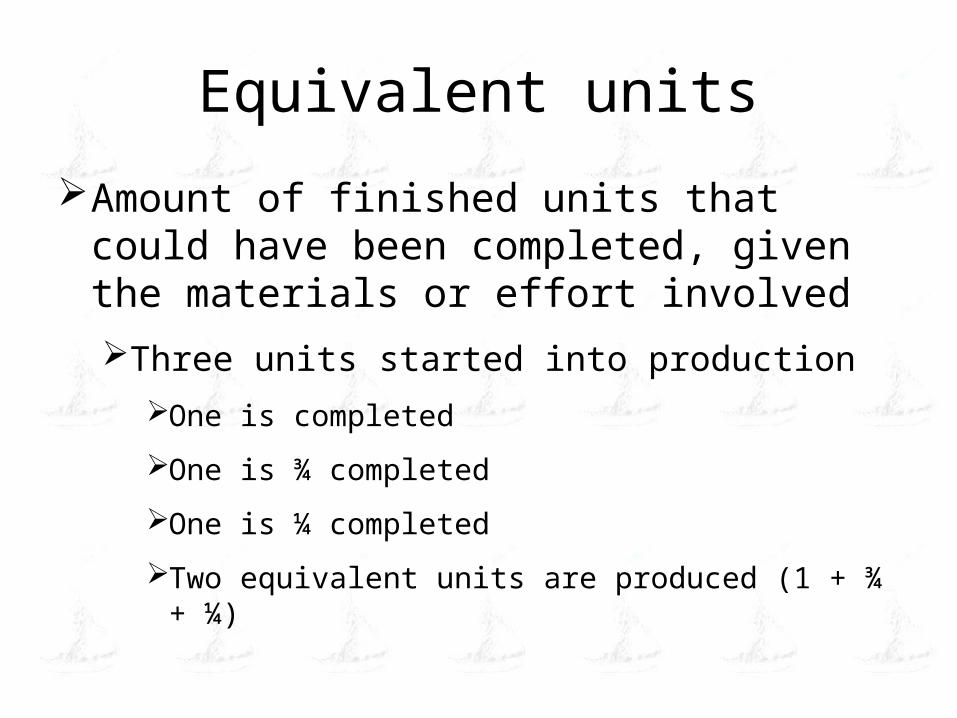

Equivalent units

Amount of finished units that could have been completed, given the materials or effort involved

Three units started into production

One is completed

One is ¾ completed

One is ¼ completed

Two equivalent units are produced (1 + ¾ + ¼)

Equivalent units

May have different number of equivalent units for materials, labor and overheadUsing the previous example, assume

all materials are added at the beginning

1 + 1 + 1 = 3 equivalent units for materials

conversion costs are added throughout the process

1 + ¾ + ¼ = 2 equivalent units for conversion costs

Equivalent units

Try this oneAt the beginning of the period

5 units, each ½ complete, are in process

During the period27 more units are put into production

At the end of the period6 units, each ¾ complete, are still in process

How many equivalent units were produced?

The processStep 1 – Summarize flow of physical units

How many were in beginning inventory?How many were started?How many are still in ending inventory?

Step 2 – Calculate equivalent unitsBeginning inventory was completedOf the units started

Some were completedSome are in ending inventory

The process

Step 3 – Summarize costs to be accounted forCost in beginning inventoryCost added during the period

Step 4 – Calculate cost per equivalent unit

Step 5 – Assign costs to completed units and ending inventory

Production cost reportPart 1 – Units

Summary of physical and equivalent unitsWhere did they come from?Where did they go?

Part 2 – CostsSummary of costsCalculation of cost per equivalent unitsAssignment of costs

Transferred outWork in process

(Step 1)

Flow of unitsPhysical

unitsDirect

materialsConversion

costsUnits to be accounted for: Beginning work in process inventory Units started this period Total units to be accounted for -

Units accounted for: (Step 3) Completed and transferred out In ending work in process inventory Total units accounted for - - -

Flow of costsCosts to be accounted for: Cost in beginning work in process inventory Cost added in current period Total costs to be accounted for -$ -$ -$

Cost per equivalent unit (Step 4)

Costs accounted for: (Step 5) Cost assigned to units transferred out Cost in ending work in process inventory Total costs accounted for -$

Equivalent units(Step 2)

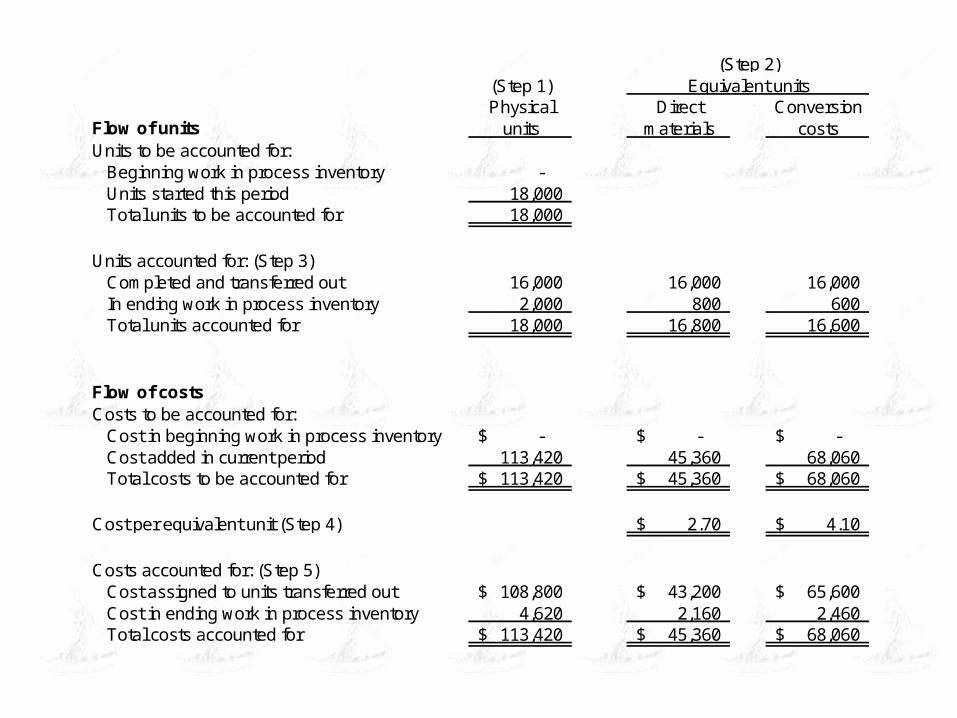

Example 1

No beginning inventory18,000 units started2,000 in ending work in process inventory

40% complete as to materials30% complete as to conversion cost

Current period costsMaterials - $45,360Conversion costs - $68,060

(Step 1)

Flow of unitsPhysical

unitsDirect

materialsConversion

costsUnits to be accounted for: Beginning work in process inventory - Units started this period 18,000 Total units to be accounted for 18,000

Units accounted for: (Step 3) Completed and transferred out 16,000 16,000 16,000 In ending work in process inventory 2,000 800 600 Total units accounted for 18,000 16,800 16,600

Flow of costsCosts to be accounted for: Cost in beginning work in process inventory -$ -$ -$ Cost added in current period 113,420 45,360 68,060 Total costs to be accounted for 113,420$ 45,360$ 68,060$

Cost per equivalent unit (Step 4) 2.70$ 4.10$

Costs accounted for: (Step 5) Cost assigned to units transferred out 108,800$ 43,200$ 65,600$ Cost in ending work in process inventory 4,620 2,160 2,460 Total costs accounted for 113,420$ 45,360$ 68,060$

Equivalent units(Step 2)

Example 2Beginning and ending inventories

4,000 units in beginning work in process80% complete as to materials50% complete as to conversion costs

25,000 units started3,000 units in ending work in process

60% complete as to materials50% complete as to conversion costs

CostsMaterials: Beg. WIP - $7,040, current - $51,660Conversion: Beg. WIP - $1,500, current - $20,400

(Step 1)

Flow of unitsPhysical

unitsDirect

materialsConversion

costsUnits to be accounted for: Beginning work in process inventory 4,000 Units started this period 25,000 Total units to be accounted for 29,000

Units accounted for: (Step 3) Completed and transferred out 26,000 26,000 26,000 In ending work in process inventory 3,000 1,800 1,500 Total units accounted for 29,000 27,800 27,500

Flow of costsCosts to be accounted for: Cost in beginning work in process inventory 8,320$ 6,720$ 1,600$ Cost added in current period 72,060 51,660 20,400 Total costs to be accounted for 80,380$ 58,380$ 22,000$

Cost per equivalent unit (Step 4) 2.10$ 0.80$

Costs accounted for: (Step 5) Cost assigned to units transferred out 75,400$ 54,600$ 20,800$ Cost in ending work in process inventory 4,980 3,780 1,200 Total costs accounted for 80,380$ 58,380$ 22,000$

Equivalent units(Step 2)

Example 3

Costs transferred from prior department

Units and costs transferred out of previous department (example 2) to department 2

Cumulative costs from prior department are treated as a separate cost category in current department

Units are 100% complete as to prior department

Transferred-in units are the “units started” in the current department

Example 3

In department 21,000 units in beginning work in process

70% complete as to materials60% complete as to conversion costs

2,000 units in ending work in process30% complete as to materials20% complete as to conversion costs

CostsMaterials: Beg. WIP - $420, current - $14,940Conversion: Beg. WIP - $840, current - $34,720

(Step 1)

Flow of unitsPhysical

unitsPrior

departmentDirect

materialsConversion

costsUnits to be accounted for: Beginning work in process inventory 1,000 Units started this period 26,000 Total units to be accounted for 27,000

Units accounted for: (Step 3) Completed and transferred out 25,000 25,000 25,000 25,000 In ending work in process inventory 2,000 2,000 600 400 Total units accounted for 27,000 27,000 25,600 25,400

Flow of costsCosts to be accounted for: Cost in beginning work in process inventory 3,890$ 2,630$ 420$ 840$ Cost added in current period 125,060$ 75,400 14,940 34,720 Total costs to be accounted for 128,950$ 78,030$ 15,360$ 35,560$

Cost per equivalent unit (Step 4) 2.89$ 0.60$ 1.40$

Costs accounted for: (Step 5) Cost assigned to units transferred out 122,250$ 72,250$ 15,000$ 35,000$ Cost in ending work in process inventory 6,700 5,780 360 560 Total costs accounted for 128,950$ 78,030$ 15,360$ 35,560$

(Step 2)Equivalent units

First-in, first-out method

Previous examples used weighted average method

Costs in beginning inventory were combined with current period costs

First-in, first-out method separates the two

Assumes units in beginning inventory were finished first

First-in, first-out method

Equivalent unit calculation includes

Work done to complete the units in beginning inventory

Work done on new units started

100% for those started and completed

<100% for those started but not completed

First-in, first-out method

Beginning inventory costs are only assigned to units in beginning inventorySome current period costs are added to complete them

Units started are only assigned current period costs

Costs accounted for includesBeginning inventory cost transferred outCurrent costs added to complete beginning inventoryCurrent costs of units started and completedCurrent costs in ending inventory

First-in, first-out method

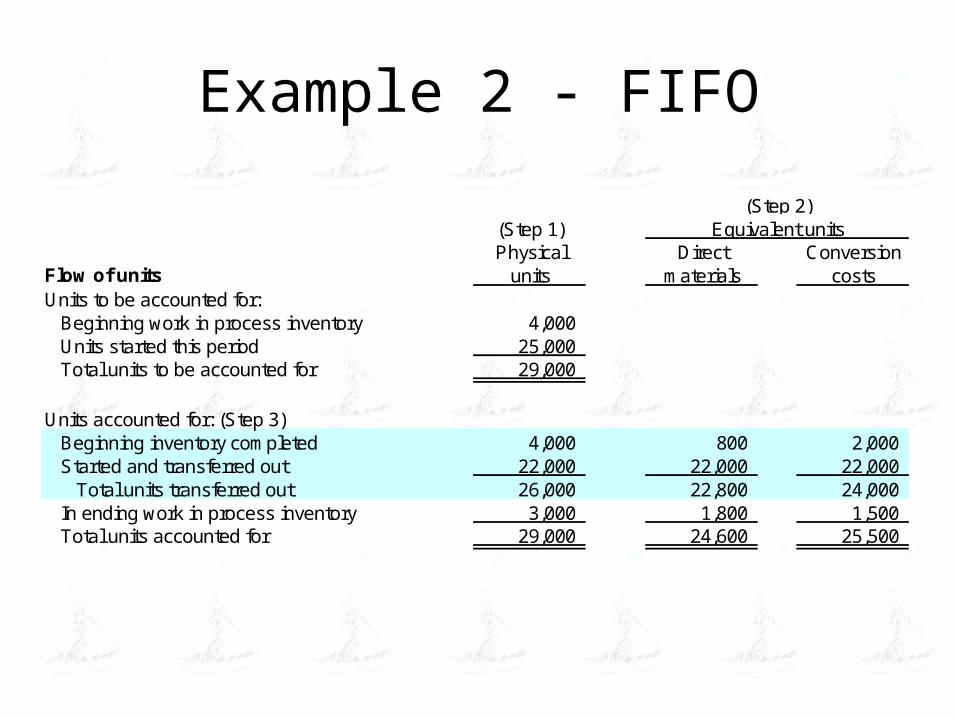

Example 2 using FIFO method4,000 units in beginning work in process

80% complete as to materials50% complete as to conversion costs

25,000 units started3,000 units in ending work in process

60% complete as to materials50% complete as to conversion costs

CostsMaterials: Beg. WIP - $7,040, current - $51,660Conversion: Beg. WIP - $1,500, current - $20,400

Example 2 - FIFO

(Step 1)

Flow of unitsPhysical

unitsDirect

materialsConversion

costsUnits to be accounted for: Beginning work in process inventory 4,000 Units started this period 25,000 Total units to be accounted for 29,000

Units accounted for: (Step 3) Beginning inventory completed 4,000 800 2,000 Started and transferred out 22,000 22,000 22,000 Total units transferred out 26,000 22,800 24,000 In ending work in process inventory 3,000 1,800 1,500 Total units accounted for 29,000 24,600 25,500

Equivalent units(Step 2)

Example 2 - FIFOFlow of costsCosts to be accounted for: Cost in beginning work in process inventory 8,540$ 7,040$ 1,500$ Cost added in current period 72,060 51,660 20,400 Total costs to be accounted for 80,600$ 58,700$ 21,900$

Cost per equivalent unit (Step 4) (Current period costs / equivalent units) 2.1000$ 0.8000$

Costs accounted for: (Step 5) Cost from beginning inventory transferred out 8,540$ 7,040$ 1,500$ Cost to complete beginning inventory 3,280 1,680 1,600 Total cost for beginning inventory 11,820$ 8,720$ 3,100$ Cost assigned to units started and completed 63,800 46,200 17,600 Total cost of units transferred out 75,620$ 54,920$ 20,700$ Cost in ending work in process inventory 4,980 3,780 1,200 Total costs accounted for 80,600$ 58,700$ 21,900$

Accounting for spoilage

Spoiled units have incurred some cost but are not transferred to the next stage

Treated as a separate line item for

Units accounted for

Equivalent units

Costs accounted for

Accounting for spoilage

Example 2 with spoilage4,000 units in beginning work in process

80% complete as to materials, 50% as to conversion costs25,000 units started800 units spoiled

50% complete as to materials, 30% as to conversion costs2,200 units in ending work in process

60% complete as to materials, 50% as to conversion costsCosts

Materials: Beg. WIP - $7,040, current - $51,660Conversion: Beg. WIP - $1,500, current - $20,400

(Step 1)

Flow of unitsPhysical

unitsDirect

materialsConversion

costsUnits to be accounted for: Beginning work in process inventory 4,000 Units started this period 25,000 Total units to be accounted for 29,000

Units accounted for: (Step 3) Completed and transferred out 26,000 26,000 26,000 Spoiled units 800 400 240 In ending work in process inventory 2,200 1,320 1,100 Total units accounted for 29,000 27,720 27,340

Flow of costsCosts to be accounted for: Cost in beginning work in process inventory 8,540$ 7,040$ 1,500$ Cost added in current period 72,060 51,660 20,400 Total costs to be accounted for 80,600$ 58,700$ 21,900$

Cost per equivalent unit (Step 4) 2.1176$ 0.8010$

Costs accounted for: (Step 5) Cost assigned to units transferred out 75,884$ 55,058$ 20,827$ Cost assigned to spoiled units 1,039$ 847$ 192$ Cost in ending work in process inventory 3,676 2,795 881 Total costs accounted for 80,600$ 58,700$ 21,900$

Equivalent units(Step 2)

Journal entries

Same as for job-order costingDollar value of units transferred out

represents the cost moving from WIP to the next stage in the processAnother WIP account (department)Finished goods inventory

Dollar value of spoiled goods is debited to an expense account

Operation costing

Hybrid of job-order and process-costing

Products goes through a combination of common processes and individual processes

No special accounting required

Units may be transferred out of a process to become a separate job or vice-versa