Pro snapshot-mar13

12

www.ProsperDiscovery.com Consumer Snapshot march 2013

-

Upload

prosper-business-development -

Category

Documents

-

view

216 -

download

2

Transcript of Pro snapshot-mar13

© 2013, Prosper®

discovery sentiment strategy

march 2013

Disclaimer: Prosper Business Development and its affiliated companies (“Prosper”) make no warranties, either expressed or implied, concerning: data gathered or obtained from any source; the present or future methodology employed in producing the statistics; or the data and estimates represent only the opinion of Prosper and reliance thereon and use thereof shall be at the user’s own risk.

© 2013, Prosper®

sentiment

Source: Monthly Consumer Survey

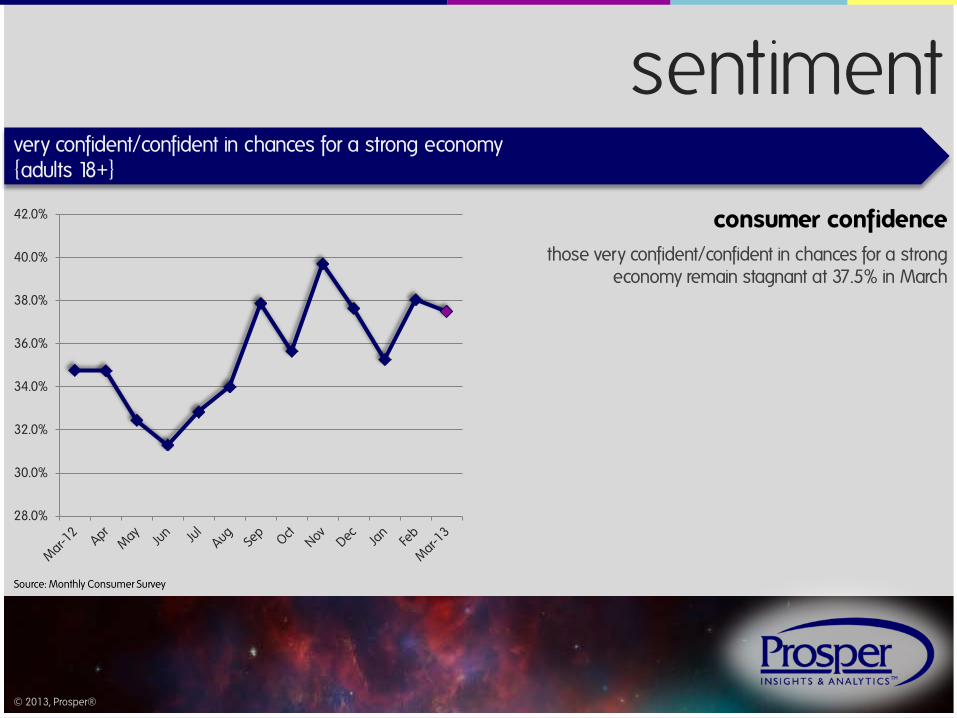

consumer confidence those very confident/confident in chances for a strong

economy remain stagnant at 37.5% in March

very confident/confident in chances for a strong economy {adults 18+}

28.0%

30.0%

32.0%

34.0%

36.0%

38.0%

40.0%

42.0%

© 2013, Prosper®

sentiment

Source: Monthly Consumer Survey

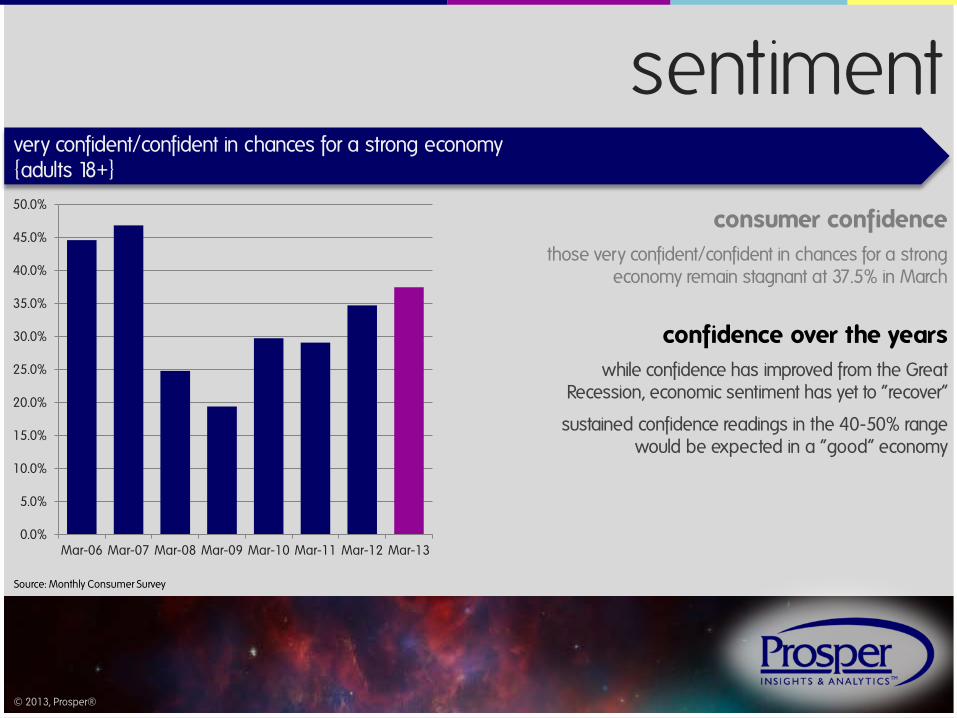

consumer confidence those very confident/confident in chances for a strong

economy remain stagnant at 37.5% in March

very confident/confident in chances for a strong economy {adults 18+}

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13

confidence over the years while confidence has improved from the Great

Recession, economic sentiment has yet to “recover”

sustained confidence readings in the 40-50% range would be expected in a “good” economy

© 2013, Prosper®

sentiment

Source: Monthly Consumer Survey

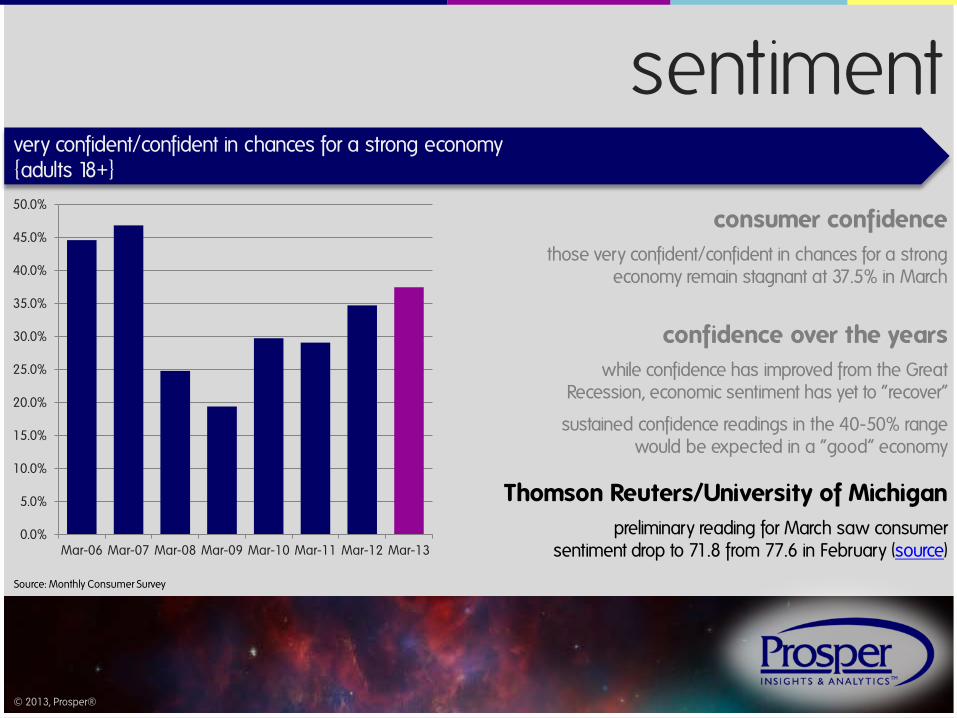

consumer confidence those very confident/confident in chances for a strong

economy remain stagnant at 37.5% in March

very confident/confident in chances for a strong economy {adults 18+}

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13

confidence over the years while confidence has improved from the Great

Recession, economic sentiment has yet to “recover”

sustained confidence readings in the 40-50% range would be expected in a “good” economy

Thomson Reuters/University of Michigan preliminary reading for March saw consumer

sentiment drop to 71.8 from 77.6 in February (source)

- Richard Curtin, Survey Director, Thomson Reuters/University of Michigan Consumer Sentiment Index

The frustrations expressed by consumers essentially involve how little consideration has been given to how the government's inability to reach a compromise affects people's economic situation."

© 2013, Prosper®

strategy

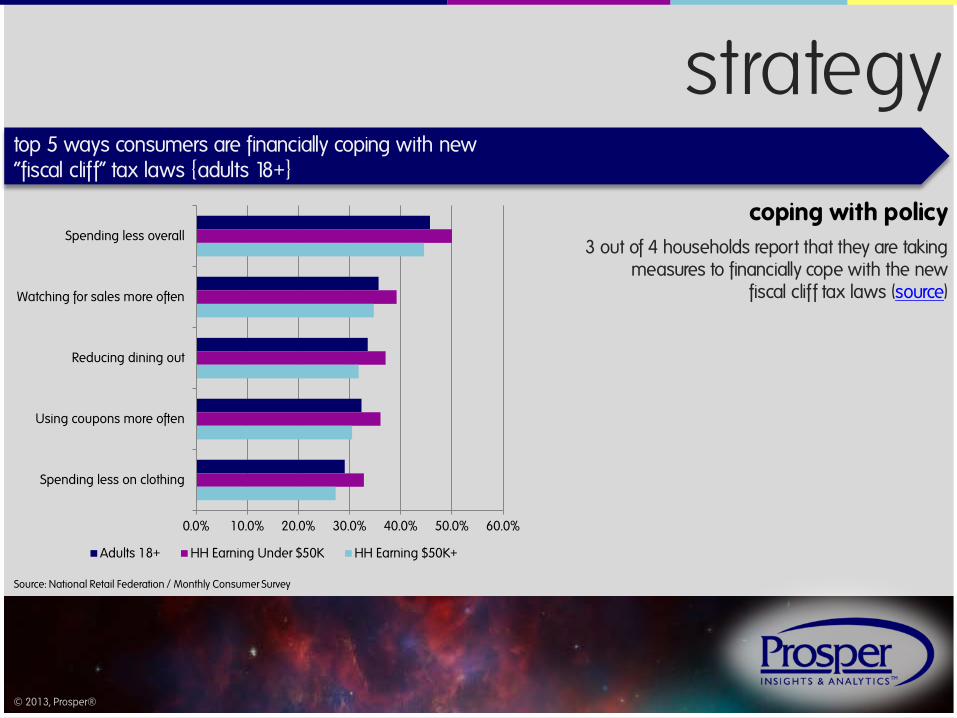

Source: National Retail Federation / Monthly Consumer Survey

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Spending less overall

Watching for sales more often

Reducing dining out

Using coupons more often

Spending less on clothing

Adults 18+ HH Earning Under $50K HH Earning $50K+

top 5 ways consumers are financially coping with new “fiscal clif f” tax laws {adults 18+}

coping with policy 3 out of 4 households report that they are taking

measures to financially cope with the new fiscal clif f tax laws (source)

© 2013, Prosper®

strategy

spending at the expense of savings? january‘s personal saving rate (ratio of personal saving

to disposable personal income) was 2.4%, a low not seen since Q4 2007 (source)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Perc

ent

Source: U.S. Department of Commerce: Bureau of Economic Analysis/FRED

U.S. personal saving rate

coping with policy 3 out of 4 households report that they are taking

measures to financially cope with the new fiscal clif f tax laws (source)

great read: The Resilient Consumer? Not Quite (Wall Street Journal)

© 2013, Prosper®

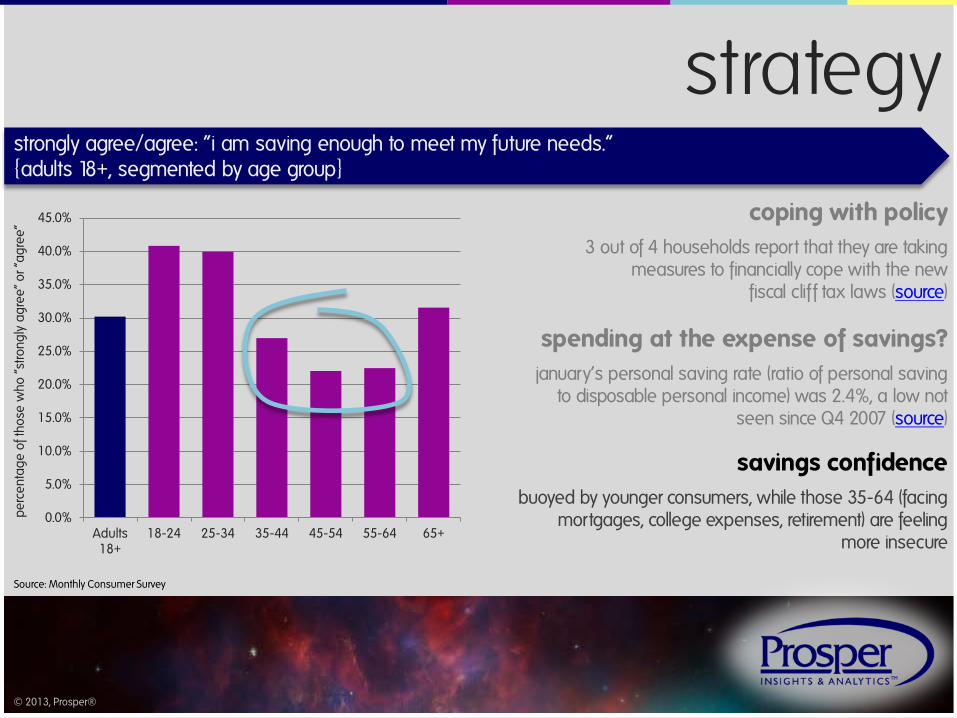

strategy

spending at the expense of savings? january‘s personal saving rate (ratio of personal saving

to disposable personal income) was 2.4%, a low not seen since Q4 2007 (source)

strongly agree/agree: “i am saving enough to meet my future needs.” {adults 18+, segmented by age group}

coping with policy 3 out of 4 households report that they are taking

measures to financially cope with the new fiscal clif f tax laws (source)

Source: Monthly Consumer Survey

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Adults18+

18-24 25-34 35-44 45-54 55-64 65+

per

cent

ag

e of

thos

e w

ho “

stro

ngly

ag

ree”

or “

ag

ree”

savings confidence buoyed by younger consumers, while those 35-64 (facing

mortgages, college expenses, retirement) are feeling more insecure

© 2013, Prosper®

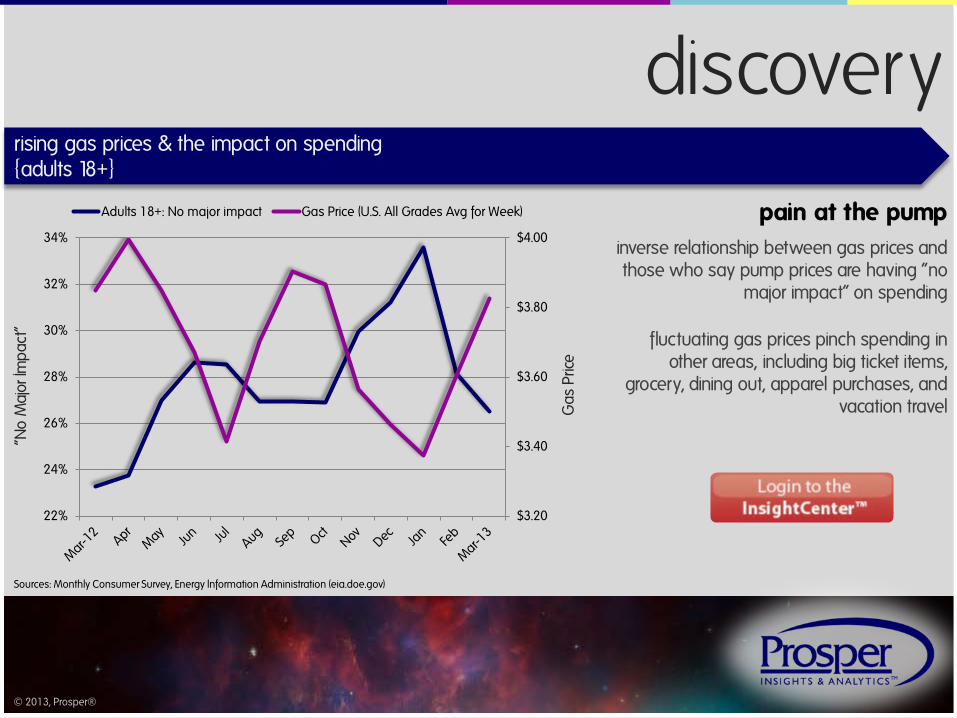

discovery rising gas prices & the impact on spending {adults 18+}

pain at the pump

fluctuating gas prices pinch spending in other areas, including big ticket items,

grocery, dining out, apparel purchases, and vacation travel

inverse relationship between gas prices and those who say pump prices are having “no

major impact” on spending

Sources: Monthly Consumer Survey, Energy Information Administration (eia.doe.gov)

$3.20

$3.40

$3.60

$3.80

$4.00

22%

24%

26%

28%

30%

32%

34%

Adults 18+: No major impact Gas Price (U.S. All Grades Avg for Week)

“No

Maj

or Im

pac

t”

Gas

Pric

e

© 2013, Prosper®

© 2013, Prosper®

thanks

visit ______________________to access: Consumer Snapshot InsightCenter™ PowerPoint Slides …and more

Prosper Insights & Analytics™ 400 W Wilson Bridge Rd, Ste 200

Worthington, OH 43085 [email protected]

ProsperDiscovery.com

ConsumerSnapshot.com

Messier 82 image source

![Mako port mar13[1]](https://static.fdocuments.us/doc/165x107/54622f14b1af9fbc4d8b50c0/mako-port-mar131.jpg)