Priori Data State of the (App) Union - July 2015

38

JULY 2015 STATE OF THE (APP) UNION www.prioridata.com @prioridata Patrick Kane Founder & CEO @pdkane

-

Upload

patrick-kane -

Category

Internet

-

view

565 -

download

1

Transcript of Priori Data State of the (App) Union - July 2015

JULY 2015

STATE OF THE (APP) UNION

www.prioridata.com@prioridata

Patrick KaneFounder & CEO@pdkane

Agenda1. Introduction2. Macro Trends in the App Store3. State-of-the-Top Charts4. A Rallying Cry for Berlin!5. Q&A

1.AN INTRODUCTION

AN INTRODUCTION

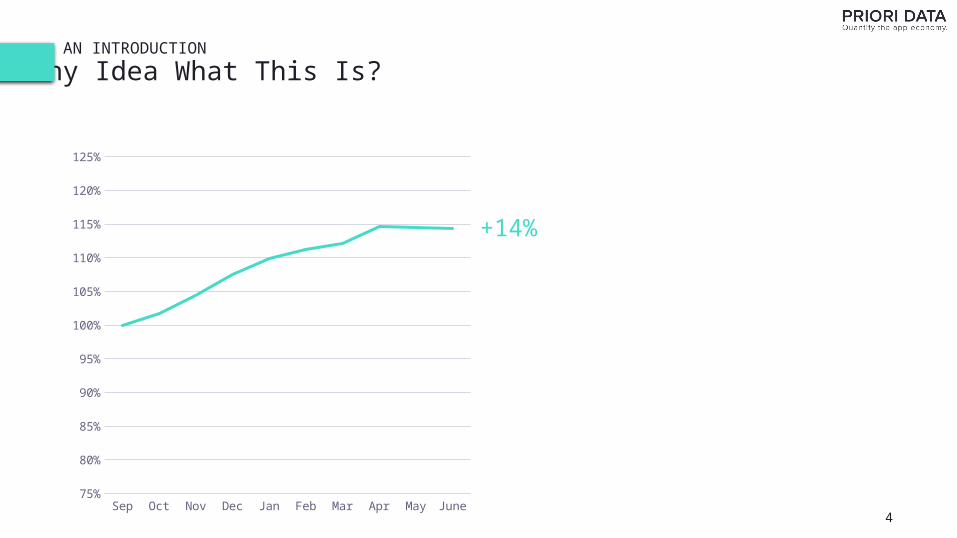

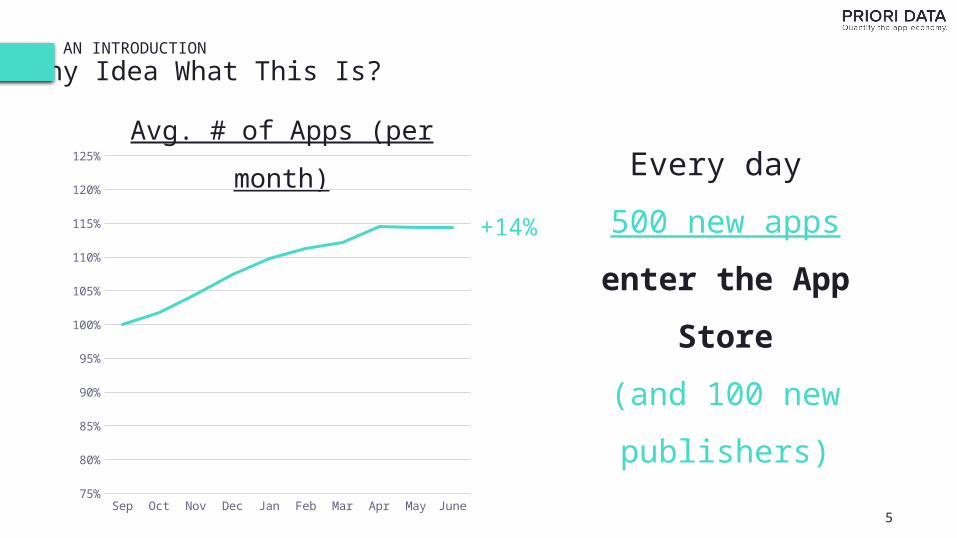

Any Idea What This Is?

4

+14%

Sep Oct Nov Dec Jan Feb Mar Apr May June75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

AN INTRODUCTION

Any Idea What This Is?

5

Every day

500 new apps

enter the App

Store

(and 100 new

publishers)

Avg. # of Apps (per month)

+14%

Sep Oct Nov Dec Jan Feb Mar Apr May June75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

AN INTRODUCTION

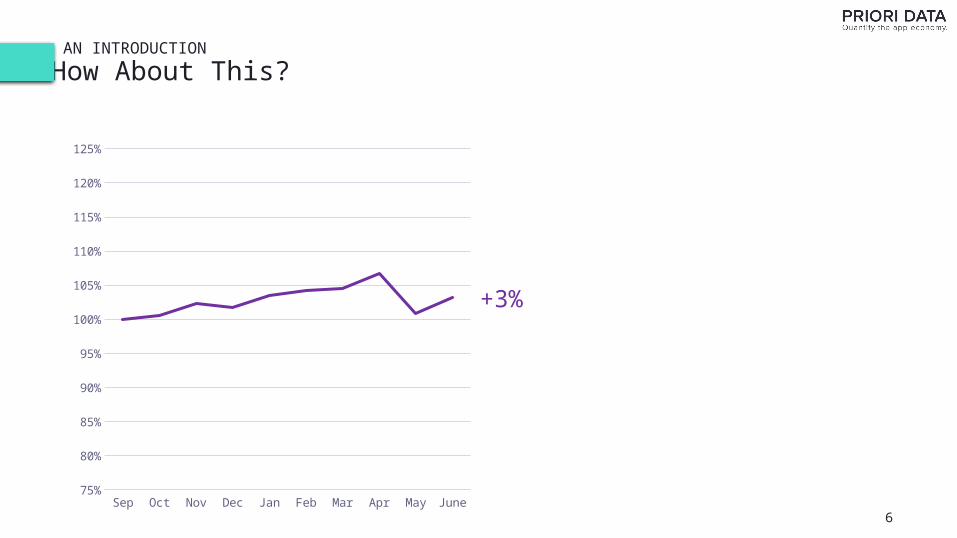

How About This?

6Sep Oct Nov Dec Jan Feb Mar Apr May June

75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

+3%

AN INTRODUCTION

How About This?

7

Average Monthly

Downloads

are flat

Since Sep. 2014

Sep Oct Nov Dec Jan Feb Mar Apr May June75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

Avg. Monthly Downloads

+3%

AN INTRODUCTION

The Result is More Competition

8

+14%

More

(and higher quality)

Companies are

Fighting for the

Same Users

Increased Supply, Flat

Demand

+3%

Sep Oct Nov Dec Jan Feb Mar Apr May June75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

Avg. Monthly Downloads Avg. # of Apps

9

If there was ever a traditional App Store narrative of bright fluffy clouds…

…it is most definitely a thing of the past.

(except for about ~300 companies, more on that later)

2.WHAT WE ARE SEEING AT A MACRO LEVEL

MACRO TRENDS IN THE APP STORE

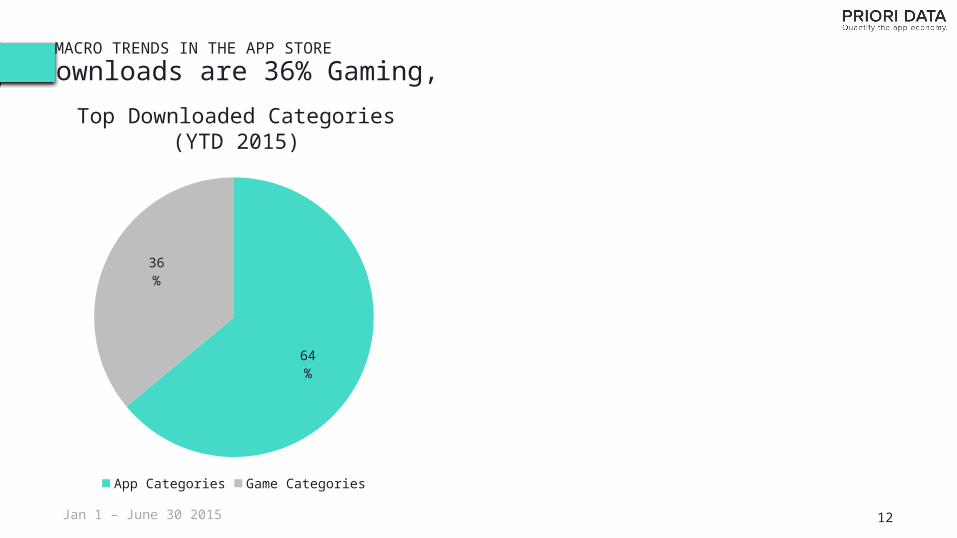

Downloads are 36% Gaming,

12

Top Downloaded Categories(YTD 2015)

Jan 1 – June 30 2015

64%

36%

App Categories Game Categories

MACRO TRENDS IN THE APP STORE

Downloads are 36% Gaming, but Gaming most Volatile Growth

13

Top Downloaded Categories(YTD 2015)

Quarterly Download Growth by Category

(Q2 2015 vs. Q1 2015)

Jan 1 – June 30 2015

Top 5 Categories +12%

Bottom 5 Categories -8%

64%

36%

App Categories Game Categories

MACRO TRENDS IN THE APP STORE

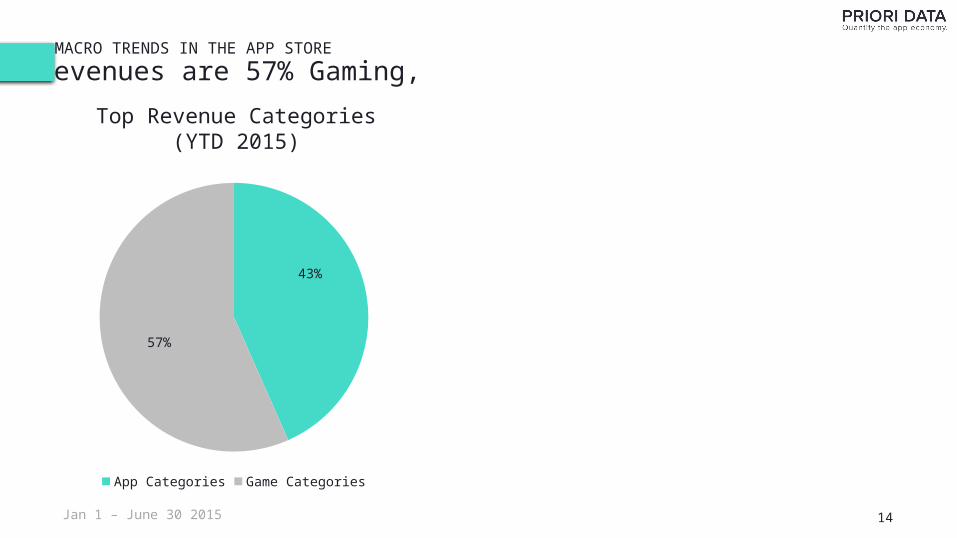

Revenues are 57% Gaming,

14

Top Revenue Categories(YTD 2015)

43%

57%

App Categories Game Categories

Jan 1 – June 30 2015

MACRO TRENDS IN THE APP STORE

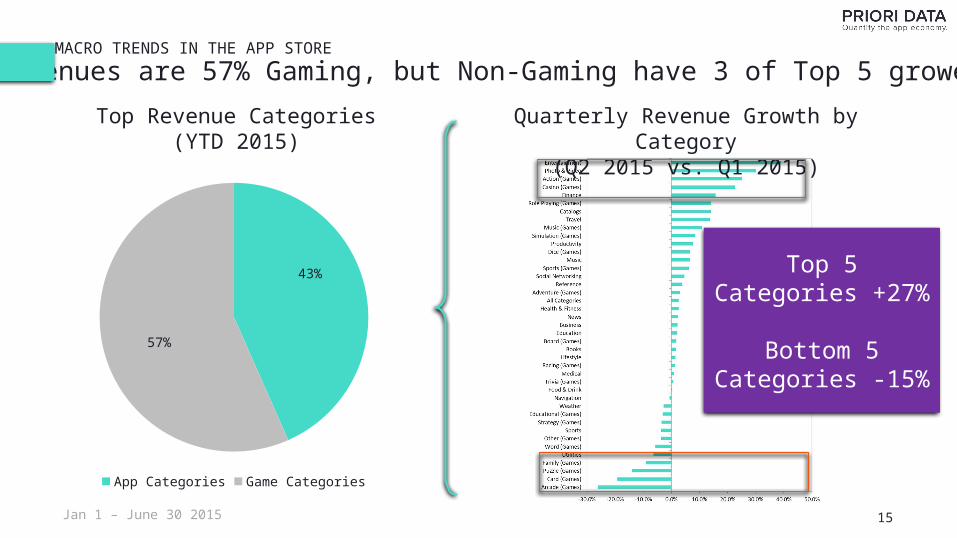

Revenues are 57% Gaming, but Non-Gaming have 3 of Top 5 growers

15

Top Revenue Categories(YTD 2015)

Quarterly Revenue Growth by Category

(Q2 2015 vs. Q1 2015)

Top 5 Categories +27%

Bottom 5 Categories -15%

43%

57%

App Categories Game Categories

Jan 1 – June 30 2015

MACRO TRENDS IN THE APP STORE

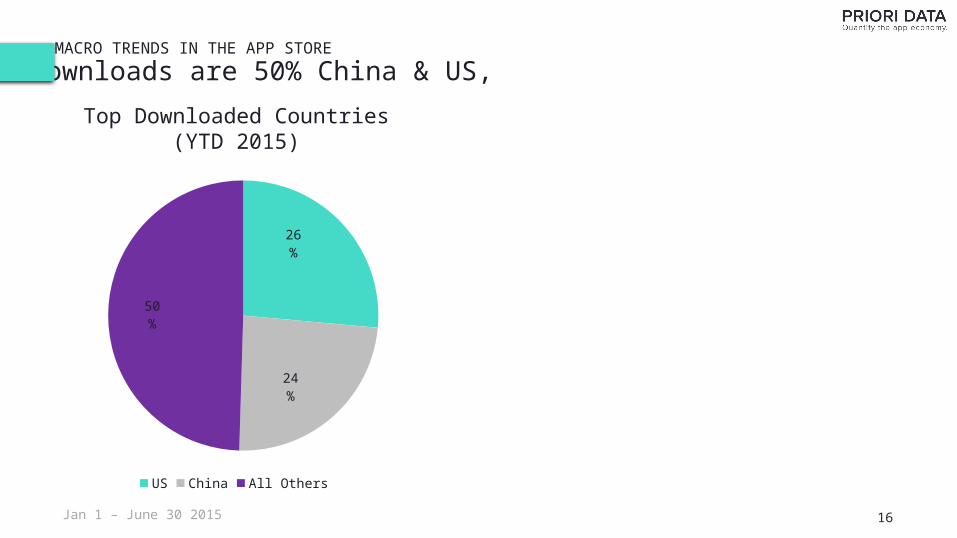

Downloads are 50% China & US,

16

Top Downloaded Countries(YTD 2015)

Jan 1 – June 30 2015

26%

24%

50%

US China All Others

MACRO TRENDS IN THE APP STORE

Downloads are 50% China & US, but no country is growing >4%

17

Top Downloaded Countries(YTD 2015)

Quarterly Downloads by Country(Q2 2015 vs. Q1 2015)

Jan 1 – June 30 2015

Top 5 Countries

+3%

Bottom 5 Countries

-5%

26%

24%

50%

US China All Others

MACRO TRENDS IN THE APP STORE

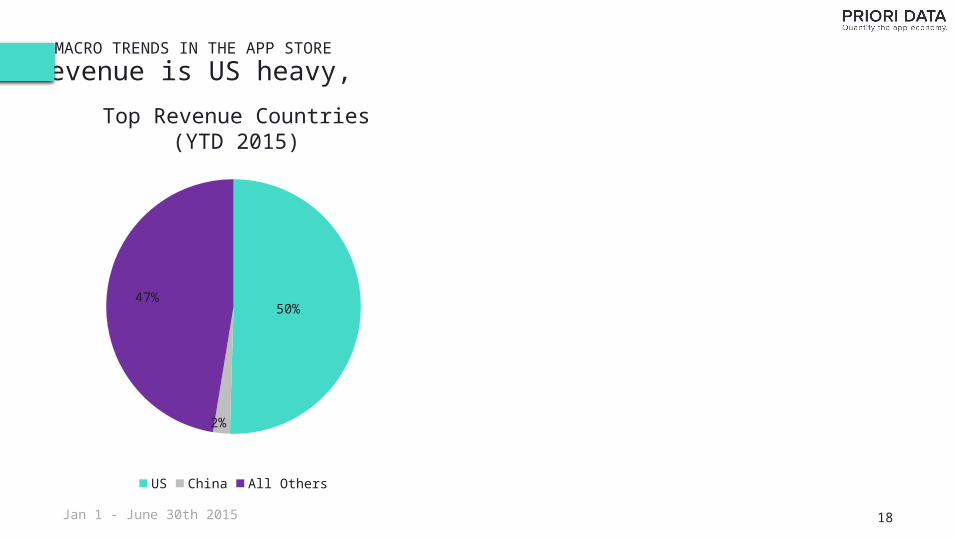

Revenue is US heavy,

18

Top Revenue Countries(YTD 2015)

Jan 1 - June 30th 2015

50%

2%

47%

US China All Others

MACRO TRENDS IN THE APP STORE

Revenue is US heavy, Growth is Mixed Across Emerging/Developed

19

Top Revenue Countries(YTD 2015)

Quarterly Revenue by Country(Q2 2015 vs. Q1 2015)

Jan 1 - June 30th 2015

Top 5 Countries

+5%

Bottom 5 Countries

-3%

50%

2%

47%

US China All Others

MACRO TRENDS IN THE APP STORE

Some Things Change, Some Things Stay The Same...

20

• Revenue is growing faster than downloads in most categories, suggesting better monetization strategies and/or more consumer willingness to pay

• The United States is still the largest revenue market (by a factor of 4x), and Japan and the UK are both larger than China by revenue

• Demand growth (downloads and revenues) is no longer just geography specific. It is rather defined by consumer trends for certain types of apps in local geographic markets

And how does this distill to the individual publisher level?

MACRO TRENDS IN THE APP STORE

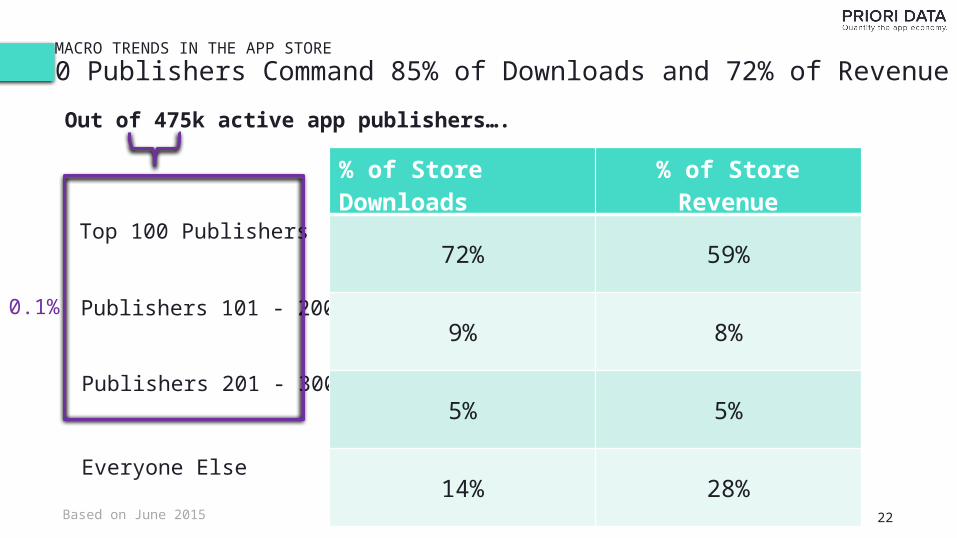

300 Publishers Command 85% of Downloads and 72% of Revenue

22

Top 100 Publishers

Publishers 101 - 200

Publishers 201 - 300

Everyone Else

% of Store Downloads

% of Store Revenue

72% 59%

9% 8%

5% 5%

14% 28%

Out of 475k active app publishers….

Based on June 2015

0.1%

3.STATE-OF-THE-TOP CHARTS

So we‘ve seen demand is flattening while app supply continues to

increase.

What‘s key to breaking through?

And how does this distill to the individual publisher level?

Visibility

26

STATE-OF-THE-TOP CHARTS

The PRIORI DATA Top Chart Framework

The three questions we ask to measure visibility (and success) of an app in the App Store Top Charts:

"Who gets in?""Where do they land?""How long do they stay?"

STATE-OF-THE-TOP CHARTS

Part 1: Who Gets In?

27

DE US GB0

50

100

150

200

250

300

350

400

186

97

180

115

194

123

301 291303

Series1 Free Charts Paid Charts

Daily # of New Apps in Top 200~300 New Apps

Achieve a Top 200 Category Position

Every Day.

Top 50 positions command ~85% of

all Category downloads.

STATE-OF-THE-TOP CHARTS

Part 2: Where do They Land?

28

Landing Ranks for New Apps

>150 [100,150] [50,100] [20,50)] <20

0%

10%

20%

30%

40%

50%

60%

51%

25%

14%

6%4%

27%24%

26%

16%

7%

Average Free App Average Paid App

Only 4% of free apps arrive in a Top

20 position

Paid apps are 2x as likely to appear in a Top 100 position vs.

free apps

STATE-OF-THE-TOP CHARTS

Part 3: How Long Do They Stay?

29

Average Length of Stay per New App

>2 weeks 1-2 weeks <1 week one day

0%

10%

20%

30%

40%

50%

60%

70%

80%

3%7%

41%

49%

1%3%

71%

25%

Average Free App Average Paid App

50% of new free apps are in and out of the charts within

1 day, and 90% within 1 week.

Only 4% of new apps last more

than 2 weeks in the charts. That’s 350 a month, globally.

STATE-OF-THE-TOP CHARTS

Implications for App Publishers

30

• Yes, new apps can claim space in the precious Top Charts.

• The core question is not whether you can get in, but rather how long you can last.

• Failure is expensive: UA costs continue to go up - FIKSU: $3 per install for free to play games.

• Do the research, set expectations right: There is no reason to be taken by surprise. Data can give you an indication as to your entry costs and ultimate market size.

• Data alone won’t do it. You need people who can phrase the right questions: What is our optimal rank, where is local demand for our niche app on the rise? What is the necessary budget to reach our goal?

So that‘s it? Pretty bleak outlook…

So that‘s it? Pretty bleak outlook…

Not entirely!

RE-EMERGENCE OF THE LONG TAIL

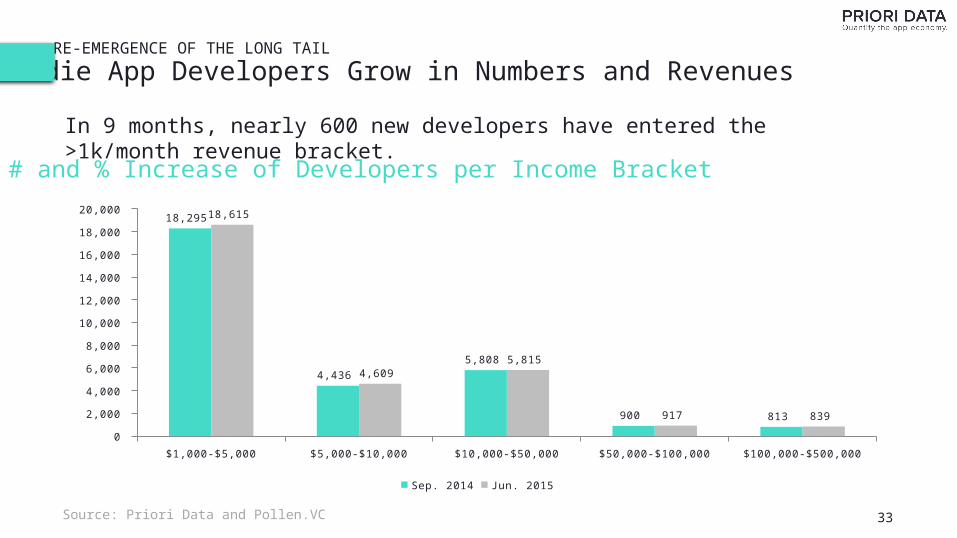

Indie App Developers Grow in Numbers and Revenues

33

In 9 months, nearly 600 new developers have entered the >1k/month revenue bracket.

# and % Increase of Developers per Income Bracket

Source: Priori Data and Pollen.VC

$1,000-$5,000 $5,000-$10,000 $10,000-$50,000 $50,000-$100,000 $100,000-$500,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000 18,295

4,436

5,808

900 813

18,615

4,609 5,815

917 839

Sep. 2014 Jun. 2015

4.A RALLYING CRY FOR BERLIN!

A RALLYING CRY FOR BERLIN!

What We Believe

35

• The market imbalances we see are the consequence of flaws in the industry

• Lack of access to competitive benchmarking and market data perpetuates these imbalances

• Data itself is a commodity, but access to the data is unequal. Only companies with $$$$$$ can get access in today’s app economy

A RALLYING CRY FOR BERLIN!

We Are Changing The Status Quo

36

• We want to play a transformational role in breaking the barriers of exclusivity and “pay-to-play” models that are plaguing our industry.

• In the era of big data and the sharing economy, it is time for a new approach. We want to define it together with the leading mobile minds in Berlin.

5.Q&A