PRIMARY ALUMINUM DEMAND: THE POWER OF · PDF filePRIMARY ALUMINUM DEMAND: THE POWER OF...

30

Emirates Global Aluminium 0 PRIMARY ALUMINUM DEMAND: THE POWER OF DEMOGRAPHICS…AMERICAS AND ASIA TO LEAD ADEL ABUBAKAR MANAGING DIRECTOR, DUBAL AMERICA INC. PLATTS ALUMINUM SYMPOSIUM 2015

Transcript of PRIMARY ALUMINUM DEMAND: THE POWER OF · PDF filePRIMARY ALUMINUM DEMAND: THE POWER OF...

Emirates Global Aluminium 0

PRIMARY ALUMINUM DEMAND: THE POWER OF DEMOGRAPHICS…AMERICAS AND ASIA TO LEAD ADEL ABUBAKAR MANAGING DIRECTOR, DUBAL AMERICA INC.

PLATTS ALUMINUM SYMPOSIUM 2015

Emirates Global Aluminium 1

Brief overview of DUBAL America Inc & Emirates Global Aluminium

Emirates Global Aluminium 2

DUBAL America Inc.

• DUBAL America is a wholly owned subsidiary of EGA. • Responsible for the marketing and distribution of DUBAL and EMAL

products in North America since 1999. • Offices based in St. Louis, MO providing end-to-end services to customers

on a real-time basis. • Swift decision-making and seamless operations providing superior service

to customers. • Importing products such as billet, foundry, purity grades and rolling slab.

Emirates Global Aluminium 3

Core primary aluminium smelters

• Dubai Aluminium (“DUBAL”) ‒ Commissioned end-1979 ‒ Sequential expansions, advancing technologies ‒ Smelter: 1,573 reduction cells in seven potlines (>1 M tpa) ‒ Casting operations (>1 M tpa) ‒ 2,350 MW power station ‒ 30 million gallon/day desalination plant ‒ Port facilities

• Emirates Aluminium (“EMAL”)

‒ Commissioned end-2010 (phase I) and mid-2014 (phase II) ‒ Smelter: 1,200 reduction cells in three potlines (>1,32 M tpa) ‒ Casting operations (~1.6 M tpa) ‒ 3,100 MW power station ‒ 3.75 million gallon/day desalination plant ‒ Port facilities

Emirates Global Aluminium 4

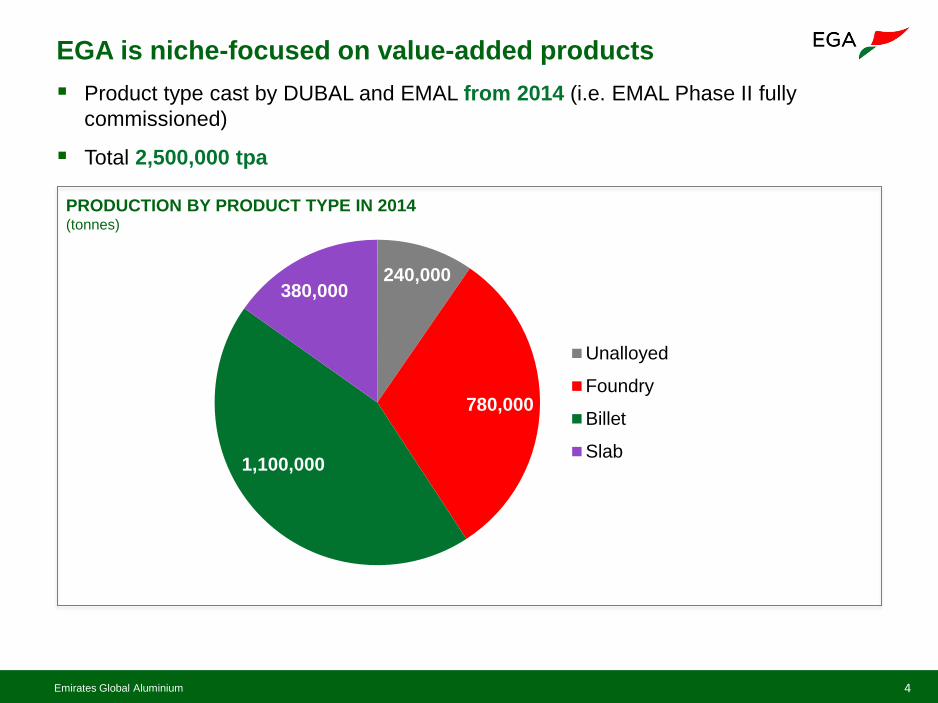

EGA is niche-focused on value-added products Product type cast by DUBAL and EMAL from 2014 (i.e. EMAL Phase II fully

commissioned)

Total 2,500,000 tpa

240,000

780,000

1,100,000

380,000

Unalloyed

Foundry

Billet

Slab

PRODUCTION BY PRODUCT TYPE IN 2014 (tonnes)

Emirates Global Aluminium 5

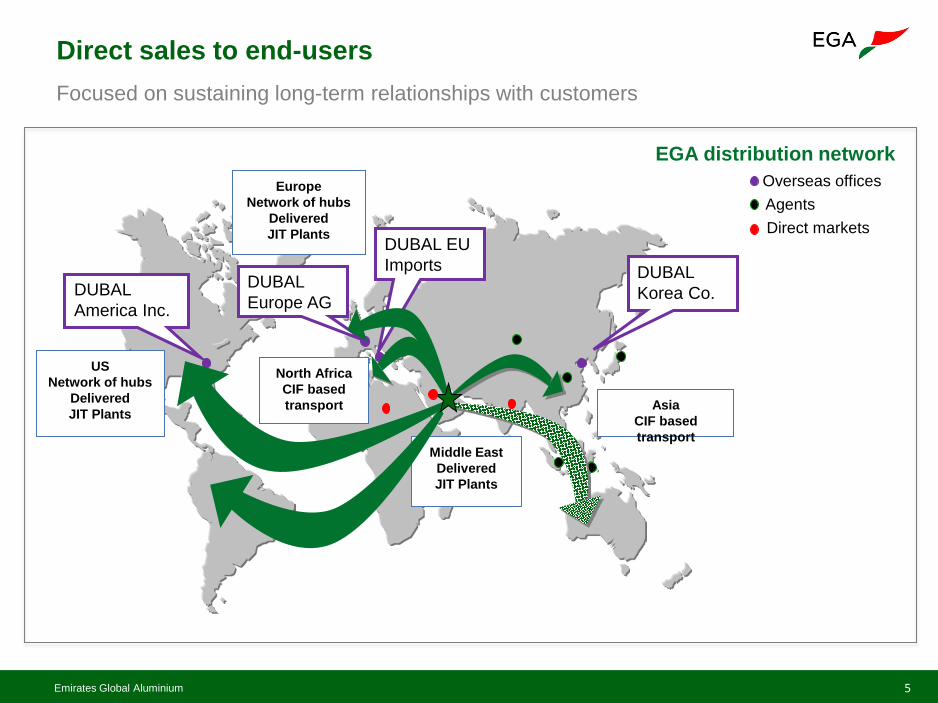

Direct sales to end-users Focused on sustaining long-term relationships with customers

Overseas offices Agents Direct markets

EGA distribution network

DUBAL America Inc.

DUBAL Europe AG

DUBAL Korea Co.

DUBAL EU Imports

US Network of hubs

Delivered JIT Plants

Europe Network of hubs

Delivered JIT Plants

Asia CIF based transport

Middle East Delivered JIT Plants

North Africa CIF based transport

Emirates Global Aluminium 6

PRIMARY ALUMINUM DEMAND: THE POWER OF DEMOGRAPHICS…AMERICAS AND ASIA TO LEAD

Emirates Global Aluminium 7

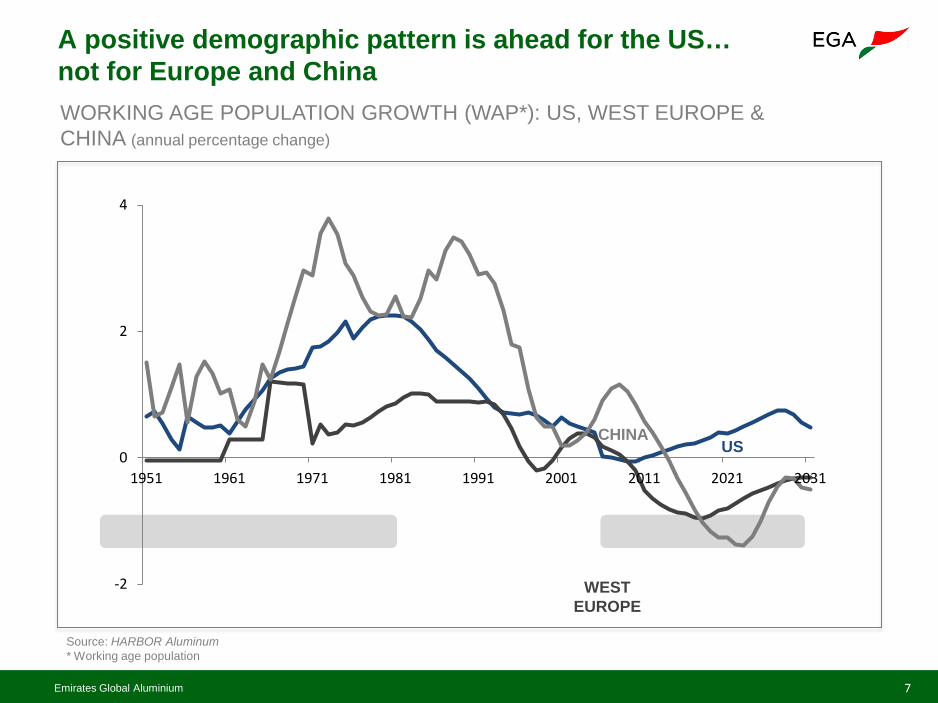

-2

0

2

4

1951 1961 1971 1981 1991 2001 2011 2021 2031

WORKING AGE POPULATION GROWTH (WAP*): US, WEST EUROPE & CHINA (annual percentage change)

Source: HARBOR Aluminum * Working age population

A positive demographic pattern is ahead for the US… not for Europe and China

WEST EUROPE

US CHINA

Emirates Global Aluminium 8

With demographics + income growth combined… the US is again the bright spot

0

2

4

6

8

10

12

14

1

3

5

7

9

11

1970 1980 1990 2000 2010 2020 2030 20402

3

4

5

6

7

8

2

3

4

5

6

7

1970 1980 1990 2000 2010 2020 2030 2040

US WAPI* VS PRIMARY ALUMINUM DEMAND (million dollars vs million tonne)

WEST EUROPE WAPI* VS PRIMARY ALUMINUM DEMAND (million dollars vs million tonne)

Source: HARBOR Aluminum * Working age population multiplied by GDP per capita

FORECAST 2014-2040

FORECAST 2014-2040

PRIMARY ALUMINUM DEMAND (RIGHT SCALE)

Source: HARBOR Aluminum * Working age population multiplied by GDP per capita

PRIMARY ALUMINUM DEMAND (RIGHT SCALE) WAPI

(LEFT SCALE)

WAPI (LEFT SCALE)

Emirates Global Aluminium 9

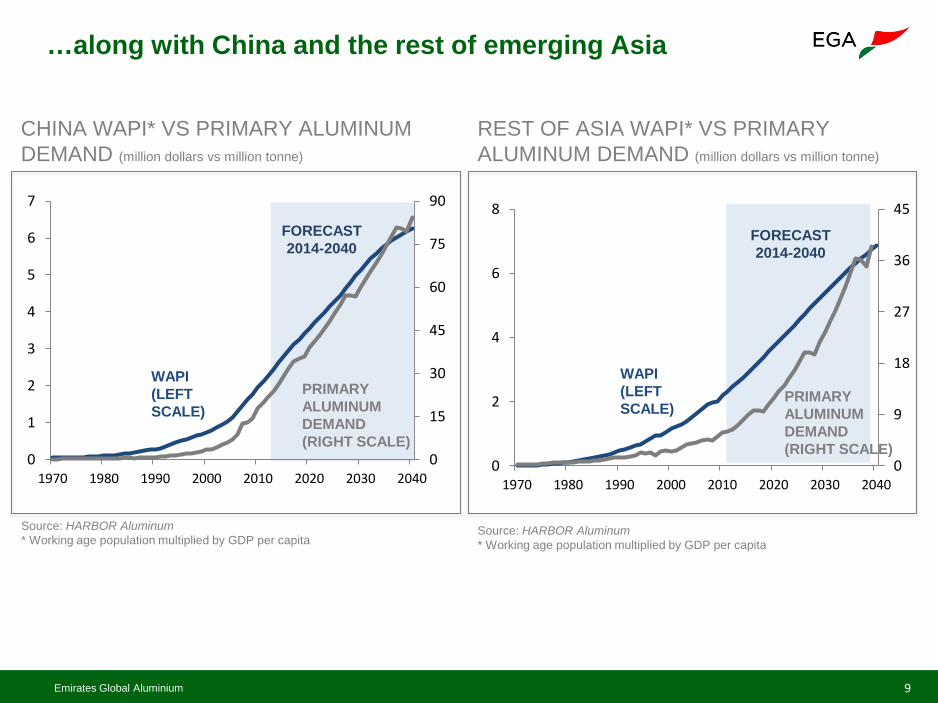

0

15

30

45

60

75

90

0

1

2

3

4

5

6

7

1970 1980 1990 2000 2010 2020 2030 20400

9

18

27

36

45

0

2

4

6

8

1970 1980 1990 2000 2010 2020 2030 2040

CHINA WAPI* VS PRIMARY ALUMINUM DEMAND (million dollars vs million tonne)

REST OF ASIA WAPI* VS PRIMARY ALUMINUM DEMAND (million dollars vs million tonne)

Source: HARBOR Aluminum * Working age population multiplied by GDP per capita

Source: HARBOR Aluminum * Working age population multiplied by GDP per capita

…along with China and the rest of emerging Asia

FORECAST 2014-2040

FORECAST 2014-2040

PRIMARY ALUMINUM DEMAND (RIGHT SCALE)

WAPI (LEFT SCALE)

PRIMARY ALUMINUM DEMAND (RIGHT SCALE)

WAPI (LEFT SCALE)

Emirates Global Aluminium 10

PRIMARY ALUMINUM DEMAND, SUPPLY AND BALANCE TRENDS: PRIMARY DEFICIT TO WIDEN THE MOST IN THE AMERICAS

Emirates Global Aluminium 11

2.0 3%

PRIMARY ALUMINUM CONSUMPTION BY REGION 2017 (million tonne & percentage of global consumption)

7.4 11%

CHINA

35.7 52%

6.1 9%

LATIN AMERICA

2.5 4%

2.7 4%

REST OF ASIA

9.4 14%

MIDDLE EAST

1.7 3%

AFRICA

0.8 1%

OCEANIA

NORTH AMERICA

WESTERN EUROPE

EASTERN EUROPE

JAPAN

0.4 1%

2014-2017: +7.4%

2014-2017: +8.3%

2014-2017: 1.3%

2014-2017: +6.0%

2014-2017: +16%

2014-2017: +9.0%

2014-2017: +0.6%

2014-2017: +0.2%

Source: HARBOR Aluminum

2014-2017: +11%

The Americas and Asia to lead primary demand growth in the world excluding China…

GLOBAL 68.7 MT

2014-2017: +7.6%

CAGR

2014-2017: 5.3%

CAGR during this period

Share of global consumption in 2017

Million mton of annual demand in 2017

Emirates Global Aluminium 12

…in line with expected industrial production dynamics…

INDUSTRIAL PRODUCTION* VS PRIMARY ALUMINUM DEMAND EXPECTED** GROWTH IN 2015 (y/y growth percentage)

7.8

3.7

1.6 1.6

3.3

0.6

8.2

5.9

1.0 0.2

6.3

2.0

0

3

6

9

China USA Eurozone Japan India Brazil

INDUSTRIAL PRODUCTION

PRIMARY ALUMINUM DEMAND

* Consensus forecast reported by Bloomberg **HARBOR’s aluminum demand forecast Source: HARBOR Aluminum and Bloomberg

Emirates Global Aluminium 13

PRIMARY ALUMINUM PRODUCTION BY REGION 2017 (million tonnw & percentage of global production)

5.3 8%

CHINA

35.3 53%

3.8 6%

LATIN AMERICA

1.5 2%

4.4 7%

6.5 10%

MIDDLE

EAST

5.5 8%

AFRICA

OCEANIA

NORTH AMERICA

WESTERN

EUROPE

EASTERN EUROPE

Source: HARBOR Aluminum

1.8 3%

2.0 3%

2014-2017 +1.7%

2014-2017 -5.9%

2014-2017 -0.7%

2014-2017 +2.2%

2014-2017 +0.3%

2014-2017 +6.8%

2014-2017 +9.1%

2014-2017 -1.8%

CAGR

REST OF ASIA

2014-2017 +23.4%

…but practially all the new commited output expansions will take place in Asia…

Share of global production in 2017

Million mton of annual production in 2017

CAGR during this period

Emirates Global Aluminium 14

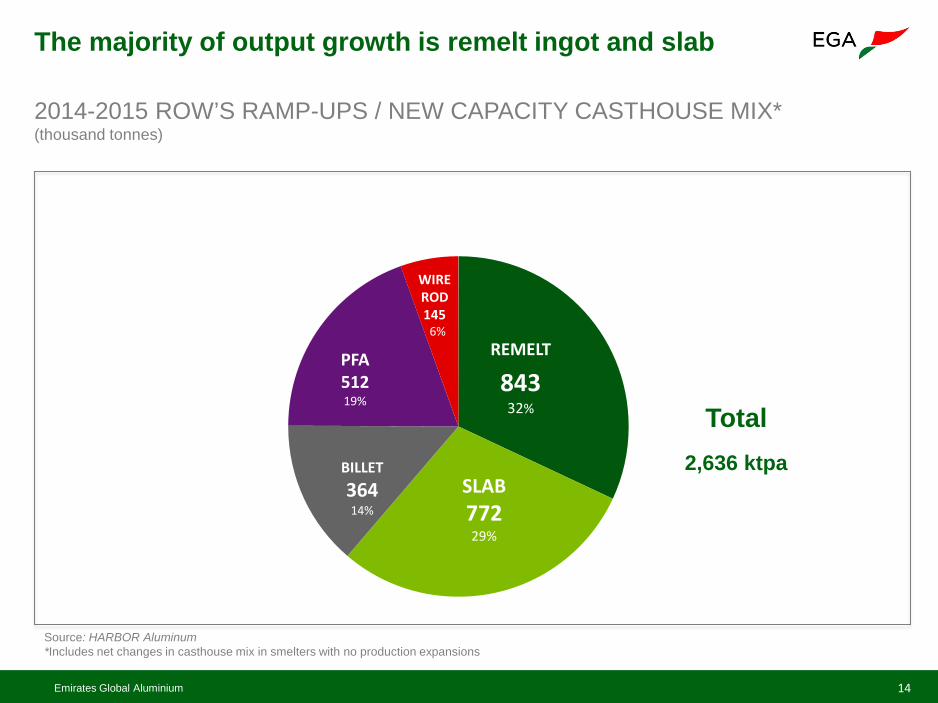

Source: HARBOR Aluminum *Includes net changes in casthouse mix in smelters with no production expansions

The majority of output growth is remelt ingot and slab

2014-2015 ROW’S RAMP-UPS / NEW CAPACITY CASTHOUSE MIX* (thousand tonnes)

843 32%

BILLET 364 14%

PFA 512 19%

SLAB 772 29%

REMELT

Total 2,636 ktpa

WIRE ROD 145 6%

Emirates Global Aluminium 15

HARBOR expects a production shortfall in ROW in the next three years… PRIMARY ALUMINUM MARKET BALANCE (thousand tonne)

-1,383 -1,603

-690

-2,408

10

552 600

-492

-3,000

-2,000

-1,000

0

1,000

2014e 2015f 2016f 2017f

ROW CHINA

Source: HARBOR Aluminum

Emirates Global Aluminium 16

0.1 -0.4 -0.6 -0.7 -1.0

-6

-4

-2

0

2013 2015f 2017f

-5.2 -5.5 -5.2 -4.0

-4.8 -6

-4

-2

02013 2015f 2017f

-1.9 -2.0 -2.0 -2.0 -2.0

-6

-4

-2

02013 2015f 2017f

-2.2 -2.3 -2.2 -2.2 -2.2

-6

-4

-2

02013 2015f 2017f

-1.1 -1.7 -1.8 -2.0 -2.3

-6

-4

-2

02013 2015f 2017f

REGIONAL PRIMARY ALUMINUM MARKET DEFICITS 2013-2017 (annual data; million tonne)

LATIN AMERICA

WESTERN EUROPE

Source: HARBOR Aluminum *USA and Canada

REST OF ASIA

JAPAN NORTH AMERICA*

2013-2017 CHANGE

…with the Americas shortfall expected to widen the most at the margin…

Emirates Global Aluminium 17

1.7 1.7 1.6 1.6 1.6

0

1

2

3

4

5

2013 2015f 2017f

2.2 1.7 1.7 1.8 1.6

0

1

2

3

4

5

2013 2015f 2017f

REGIONAL PRIMARY ALUMINUM MARKET SURPLUSES 2013-2017 (annual data; million tonne)

EASTERN EUROPE

Source: HARBOR Aluminum

…as it is the farthest away region from where regional surpluses are

3.3 4.0 3.9 3.8 3.8

0

1

2

3

4

5

2013 2015f 2017f

MIDDLE EAST

1.2 1.2 1.1 1.0 1.0

0

1

2

3

4

5

2013 2015f 2017f

AFRICA OCEANIA

Emirates Global Aluminium 18

2.26 2.27 2.24 2.06 2.23 2.08 2.21 2.33 2.24

-2.39 -2.87 -2.9 -3.05 -3.33 []0 -4.08 -4.32 -4.57-0.25

-0.38 -0.38-0.44

-0.46-0.49

-0.52-0.56 []0

-6

-3

0

3

2009 2010 2011 2012 2013 2014f 2015f 2016f 2017f

PRIMARY ALUMINUM BALANCE NORTH AMERICA BY COUNTRY (million tonne)

Source: HARBOR Aluminum

If we include Mexico, North America deficit expected at almost 3 million mton by 2017

CANADA

USA

MEXICO

-0.38 -0.98 -1.04 -1.43 -1.56 -2.21 -2.39 -2.55 -2.93 NORTH AMERICA

Emirates Global Aluminium 19

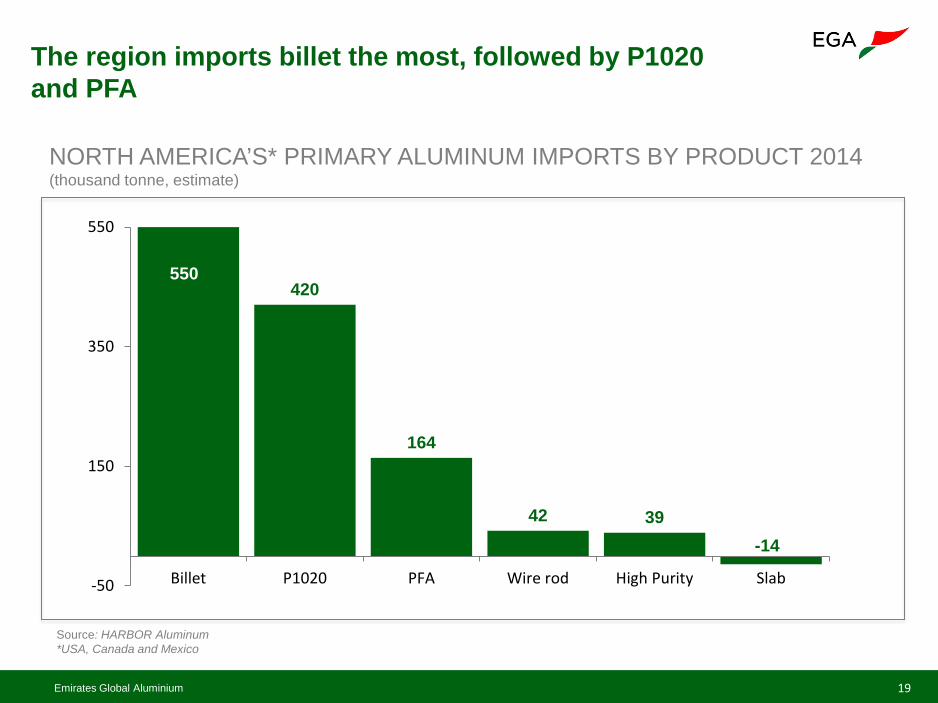

The region imports billet the most, followed by P1020 and PFA

Source: HARBOR Aluminum *USA, Canada and Mexico

NORTH AMERICA’S* PRIMARY ALUMINUM IMPORTS BY PRODUCT 2014 (thousand tonne, estimate)

420

164

42 39 -14

-50

150

350

550

Billet P1020 PFA Wire rod High Purity Slab

550

Emirates Global Aluminium 20

SUBSTITUTION TRENDS: GLOBAL ECONOMY MORE ALUMINUM INTENSIVE THAN EVER TRANSPORTATION THE HOT SPOT

Emirates Global Aluminium 21

The global economy is increasingly aluminum intensive… GLOBAL ECONOMY ALUMINUM INTENSITY (thousand tonne of aluminum consumption per billion dollar of global working age population income)

1.5

2.5

3.5

4.5

1970 1980 1990 2000 2010 2020 2030 2040

1974 3.3

2013 2.9

2009 2.1

2027f 3.5

2040f 3.9

Emirates Global Aluminium 22

24%

10% 15%

24%

13%

9% 4%

…with transportation sector leading at the margin…

GLOBAL SEMIS CONSUMPTION 2012-2017 BY END USE SECTOR (million mton and share of total consumption in 2011)

7.2% Transport

Construction

Packaging

Electrical

Engineering

6.7%

8.1%

5.5%

6.6%

Durables 6.6%

Other 6.6%

7.6 million tonne

2.9 million tonne

5.5 million tonne

6.7 million tonne

2.9 million tonne

2.6 million tonne 1.2 million tonne

Source: HARBOR Aluminum

CAGR ‘12-’17

Global annual demand for aluminum (primary+scrap) from transportation sector will be 7.6 million tonnes higher in 2017 vs 2012.

Emirates Global Aluminium 23

…mainly as more aluminum is being used in vehicles (especially in North America)

ALUMINUM CONTENT PER VEHICLE (kg per vehicle; global average)

0

50

100

150

200

250

30020

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

2020

2120

2220

2320

2420

25

Globally, aluminum content per vehicle could double in 2012-2025 to 250 kg/vehicle, increasing by an average rate of 9 kg/year

107 123

255

Source: HARBOR Aluminum, Ducker Report and Aluminum Association

Emirates Global Aluminium 24

The aluminum content in vehicles in NA to grow around 1.8 million tonne in 2015-2020

TOTAL ALUMINUM CONTENT IN ESTIMATED TOTAL VEHICLE PRODUCTION BY REGION (million tonne)

3.2

5.0

11.4

14.8

0

4

8

12

16

2015f 2020f

Source: HARBOR Aluminum and Ducker Report

Emirates Global Aluminium 25

POTENTIAL OUTPUT RESTARTS AND CHINA´S SEMI PRODUCT EXPORTS: COULD MORE THAN HALVE THE EXPECTED PRIMARY SHORTAGE IN ROW IN 2015

Emirates Global Aluminium 26

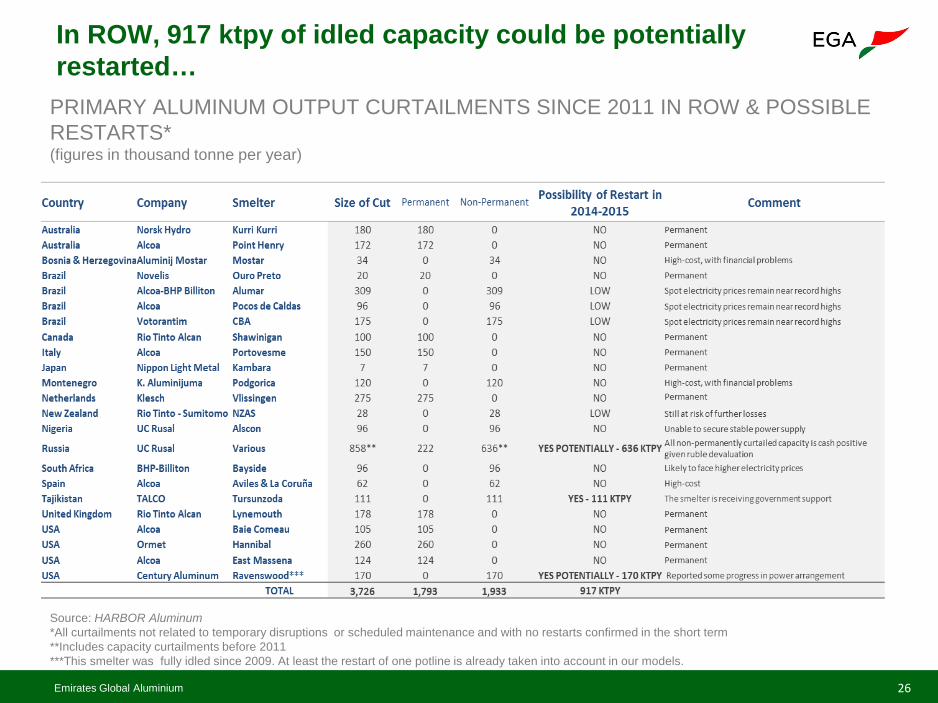

In ROW, 917 ktpy of idled capacity could be potentially restarted…

PRIMARY ALUMINUM OUTPUT CURTAILMENTS SINCE 2011 IN ROW & POSSIBLE RESTARTS* (figures in thousand tonne per year)

Source: HARBOR Aluminum *All curtailments not related to temporary disruptions or scheduled maintenance and with no restarts confirmed in the short term **Includes capacity curtailments before 2011 ***This smelter was fully idled since 2009. At least the restart of one potline is already taken into account in our models.

Emirates Global Aluminium 27

Moreover, Chinese exports could displace 50% of the ROW expected demand growth

CHINESE SEMIS EXPORT GROWTH* AS PERCENTAGE OF EXPECTED REGIONAL PRIMARY DEMAND GROWTH IN 2014 (%)

67

48 48

0

20

40

60

80

Asia exc. China North America Europe

Source: HARBOR Aluminum *In H2 2014

Emirates Global Aluminium 28

China + potential restarts could more than halve ROW´s primary deficit for 2015

EXPECTED ROW PRIMARY ALUMINUM BALANCE IN 2015 VS POTENTIAL CAPACITY RESTARTS AND EFFECT OF CHINESE SEMI EXPORTS (figures in million tonne per year)

1.6

0

0.6

1.2

1.8

Expected 2015 ROW primary aluminum deficit

1.1

0.5

0.6

POTENTIAL RESTARTS (SIBERIAN SMELTERS + RAVENSWOOD)

POTENTIAL DISPLACED ROW DEMAND BY CHINESE SEMI EXPORTS

Source: HARBOR Aluminum

Emirates Global Aluminium 29

THANK YOU Any questions?