Price Envelopes for European Gas - Gazprom Export · Price Envelopes for European Gas Flame,...

21

Price Envelopes for European Gas Flame, Amsterdam , May 8, 2017 Sergei Komlev Head Contract Structuring and Price Formation Directorate Gazprom Export* *Views expressed in this presentation are the author’s sole responsibility and do not necessarily represent that of Gazprom Export

Transcript of Price Envelopes for European Gas - Gazprom Export · Price Envelopes for European Gas Flame,...

Price Envelopes for European Gas

Flame,

Amsterdam , May 8, 2017

Sergei Komlev Head Contract Structuring and Price Formation Directorate

Gazprom Export*

*Views expressed in this presentation are the author’s sole responsibility

and do not necessarily represent that of Gazprom Export

© ZMB 2

Market Tightness is Inadequate Criteria for Division of European Gas History into Periods

1) ‘Global gas glut’ (Jun ‘08 – Dec ‘10) only strengthened European gas prices despite the LNG flood. European gas prices just followed oil price recovery prior to Fukushima.

2) ‘Fukushima tightness’ (Mar ‘11 – Dec ‘14) gave no special momentum to gas price developments: erratic fluctuations of gas prices completely ignored outflow of large LNG volumes from Europe.

3) ‘Oversupply and price convergence’ (Dec ’14 – current): although gas prices start to weaken prior to September 2014 due to abnormally warm Q1 2013, their collapse coincided with oil price drop on the market which has already rebalanced itself.

Use of market tightness indicator for periodization of European gas history creates parallel reality. It drives to an absurd conclusion that oversupply leads to higher prices.

Source: Adapted from Timera Energy

© ZMB 3

Inter-Fuel Competition Defines Upper and Lower Price Range Levels for Natural Gas

Ceiling

Floor

Oil/Oil products parity

Coal parity

Source: Gazprom Export

© ZMB 4

Gas Price Corridor Width is Determined Mainly by Oil Price Volatility

and Stretched from 0.8 MMBTU in 1998 to 15 MMBTU in 2012

4

Source: BP

Source: BP, Gazprom Export Source: BP, Gazprom Export

© ZMB 5

Oil Price Sets a Resistance Level for Natural Gas Prices

•

Source: BP, Gazprom Export

© ZMB 6

Coal Price Sets a Support Level for Natural Gas Prices

•

Source: BP, Gazprom Export

© ZMB 7

Depressed NA Natural Gas Prices are Competitive with ‘Expensive’ Grades of Coal Only

* Coal and natural gas prices compared on an equivalent energy content and efficiency basis

© ZMB 8

Competition with Other Hydrocarbons Locks Natural Gas in Price Envelope

8 Source: Shell Source: Shell

© ZMB 9

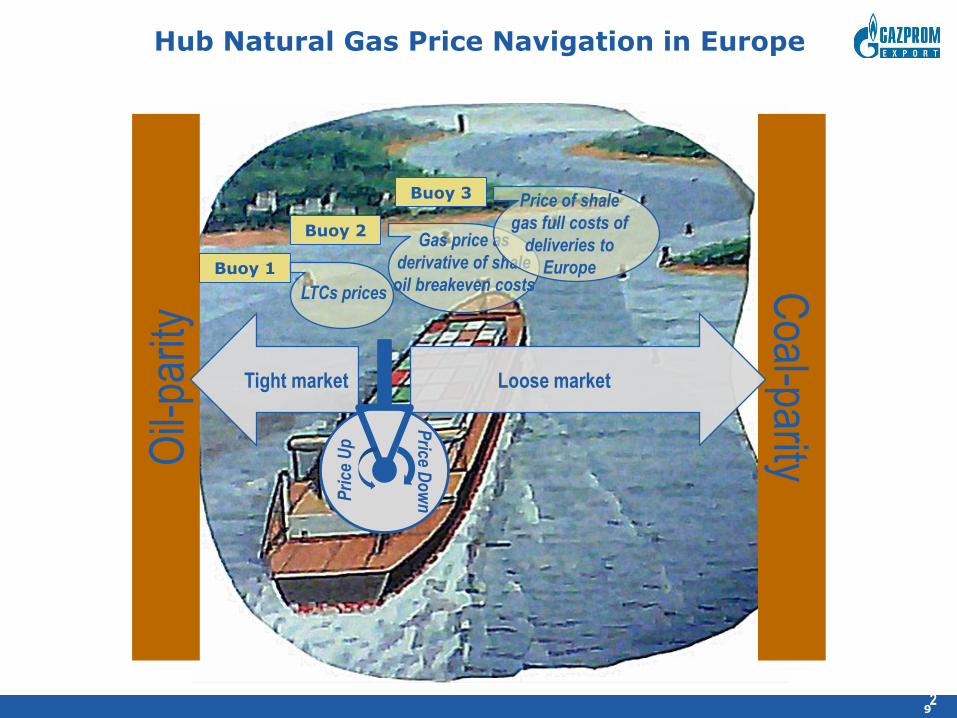

Hub Natural Gas Price Navigation in Europe

2

Oil-

parit

y C

oal-parity

Loose market Tight market

Buoy 1

Buoy 2

Buoy 3

LTCs prices

Gas price as

derivative of shale

oil breakeven costs

Price of shale

gas full costs of

deliveries to

Europe

Pri

ce U

p

Price D

ow

n

© ZMB 10

Bouy#1. Prices of Long-Term Supply Contracts set a Strong Resistance Level for Hub Prices in Europe

© ZMB 11

Bouy #1. Hub-Based Gas Prices in Europe Move in Tandem with Oil/Quasi Oil-Indexed Contract Prices

Even if oil-indexation elements are being substituted by hub ones, prices of LTCs exercise strong influence over hub prices and are setting up a trajectory for their movement by acting as “price anchor”. Hub prices are therefore not independent: they are derivatives of the contract prices that set a baseline trend for their behavior. Supply and demand only mutate their changes

Source: BAFA, Bloomberg, World Bank

© ZMB 12

Bouy #1. Extreme Weather Conditioned Pushed TTF Prices above BAFA for Nearly Two Months

Source: BAFA, Bloomberg

© ZMB 13

Bouy#2. ACER 2016 Report: Correlation between Oil and Gas Prices is High

© ZMB 14

Bouy #2. Correlation and Regression Analysis Indicates that TTF Price Dependence on Oil Prices is Increasing

Correlation

(TTF MA,

USD/mcm)

Time period Brent,

USD/barrel

Oil Price:

Six month

moving

average

Oil Price:

Nine month

moving

average

2008-2016 76.6% 85.5% 83.3%

2008-2013 69.9% 84.7% 81.9%

2014-2016 79.5% 87.3% 88.7%

R Squared

(TTF MA,

USD/mcm)

2008-2016 58.6% 73.1% 69.4%

2008-2013 48.9% 71.8% 67.1%

2014-2016 63.2% 76.3% 78.6%

This effectively means that NA shale breakeven costs which emerged as the major determinant for global oil prices are setting price rage for European hub prices

© ZMB 15 15

Bouy#3. Full Costs of NA LNG Deliveries to Europe

Sources: Bloomberg, Wood McKenzie * P = HH forwards * 115% + liquefaction + shipping to Europe + regasification

Full costs of US LNG delivered to Europe are higher than prices on the European hubs (NBP). NA LNG deliveries are profitable on short-run marginal costs.

Henry

Hub

115%

plant

losses

Ship-

ping to

Europe

Regas Toll Fee

Short-

run Mar-

ginal

Costs

Total

costs NBP MA

Feb-17 2,82 3,24 0,67 0,40 2,37 4,31 6,68 6,36

Jan-17 3,26 3,75 0,67 0,40 2,37 4,82 7,19 6,58

Dec-16 3,58 4,12 0,67 0,40 2,37 5,18 7,55 5,83

Nov-16 2,50 2,88 0,67 0,40 2,37 3,94 6,31 6,19

$/MMBTU

© ZMB 16 16

Bouy#3. Outlook for NA LNG Export to Europe

Sources: Bloomberg, Wood McKenzie

* P = HH forwards * 115% + liquefaction + shipping to Europe + regasification

Full costs of US LNG delivered to Europe are higher than European hub prices on a forward curve, although are profitable when tolling fees are excluded.

© ZMB 17

Growing Importance of Forward Market Compared to Prompt Market:

Trading Volumes by Utilities/Midstreamers are Higher than Gas Consumption

Source: IEA, Companies’ Annual Reports

78.0

46.0

35.7

113.6

63.3 58.4

36.2

167.1

40.9

8.0

80.6 80.6

43.7

8.6

84.7 84.7

0

20

40

60

80

100

120

140

160

180

Engie OMV VNG Uniper Engie OMV VNG Uniper

2014 2015

Total Sales Indigenous Consumption

Bcm

© ZMB 18

*Demand Includes import contracts and indigenous production

Source: Cedigaz, Eurostat, IEA, Gazprom Export LLC Database

Overcontraction as Factor of Hub Price Degradation

560

578 577 589

604 601 583 579 575

562

587

609

559 553 546 557

522

561

506 494

486

431 449

486

400

450

500

550

600

650

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

bcm

Contracted volume Consumption

Under-contracted

market

Balanced market Over-contracted market

1

25 31 32

82

39

77 85 89

131 138 123

0

50

100

150

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Delta,

bcm

© ZMB 19

Illusion of Oversupply Created by Monetization of Contract Commitments on the European Forward Market

© ZMB 20

There is Need to Rebalance Market by Eliminating Paper and Physical Gas Disconnect

Source: Gazprom Export

Midstreamers LTC Contracts

End-users

Hub

Year-ahead contract

Portfolio

optimization

Sell Q1 volume on

hubs under a

forward contract

that equals MAQ+

Buy back Q2

volume of paper

gas that equals

physical demand

by end-users

Under current market conditions:

Q1 > Q2

THANK YOU FOR YOUR ATTENTION!

![INDEX [indianembassyreykjavik.gov.in]indianembassyreykjavik.gov.in/.../Tender-Document... · scribed “Price Bid”.Both these envelopes shall be enclosed in a single sealed envelope](https://static.fdocuments.us/doc/165x107/5f0d59617e708231d439e8e0/index-in-in-scribed-aoeprice-bidaboth-these-envelopes-shall-be-enclosed-in.jpg)