Presented by Robi Robichaud

30

Wind Technologies and Innovation for Our Energy Future Evolving Opportunities Robi Robichaud Senior Engineer NREL EL is a national labora ratory ry of the U.S. S. Depart rtme ment of En Energ rgy Office ce of En Energ rgy Ef Effici ciency cy and Renewable En Energ rgy opera rated by the Al Alliance ce for Su Sust stainable En Energ rgy, LLC

-

Upload

doannguyet -

Category

Documents

-

view

226 -

download

3

Transcript of Presented by Robi Robichaud

Wind Technologies and Innovation for Our Energy Future Evolving Opportunities

Robi Robichaud Senior Engineer

NNRRELEL iiss aa nnaattiioonnaall llaabboorarattooryry ooff tthhee UU..S.S. DDeeppaartrtmemenntt ooff EnEneergrgyy OOffffiicece ooff EnEneergrgyy EfEfffiicicieenncycy aanndd RReenneewwaabbllee EnEneergrgyy ooppeeraratteedd bbyy tthhee AlAllliiaanncece ffoorr SuSuststaaiinnaabbllee EnEneergrgyy,, LLLLCC

kj

Opportunities for Wind Technology

• National Wind Technology Center – Research • Blades • Generators • Wind Resource

• Wind – Market Update • PTC • RPS

• Wind Technology Overview • Larger Rotors • Taller Towers • Improved Controls

• Wind Resource • Improved Assessment

2 Innova+on for Our Energy Future

National Wind Technology Center - Research

Innova+on for Our Energy Future

National Wind Technology Center Overview

• Turbine testing since 1977 • Leader in development of

design and analysis codes • Pioneers in component

testing • Unique test facilities

• Blade Testing • Dynamometer • CART turbines

• Modern utility-scale turbines • Approx. 150 staff on-site • Budget approx. $35M • Many CRADAs with

industry • Leadership roles for

international standards

Innova+on for Our Energy Future

National Wind Technology Center Vision

The NWTC will be an essential partner for the technical development and large-scale deployment of wind power.

Goals: • Improve windplant power production • Reduce windplant capital cost LCOE • Improve windplant reliability and lower O&M cost • Eliminate barriers to large-scale deployment

Innova+on for Our Energy Future

Blade Testing Facilities

New Large Blade Test Facility:

• Boston, MA with Massachusetts Technology Collaborative

• Static and Fatigue tests of blades up to 90 m

• NREL staff to operate facility

• NREL has developed and patented advanced blade testing

• NREL supports R&D blade testing for DOE and industry

• Supporting development of new blade test facilities worldwide

Innova+on for Our Energy Future

Drivetrain Testing

• 2.5 MW Dynamometer – Commissioned 1999

– Steady use by industry

– Used in R&D activities

– Key facility for Gearbox

Reliability Collaborative

– Basic shaft load capability

added in FY2010

• Dynamometer Upgrade – $10M Recovery Act funding

– New 5 MW driveline

– Robust shaft loading system

– Commissioniedin 2013

Innova+on for Our Energy Future

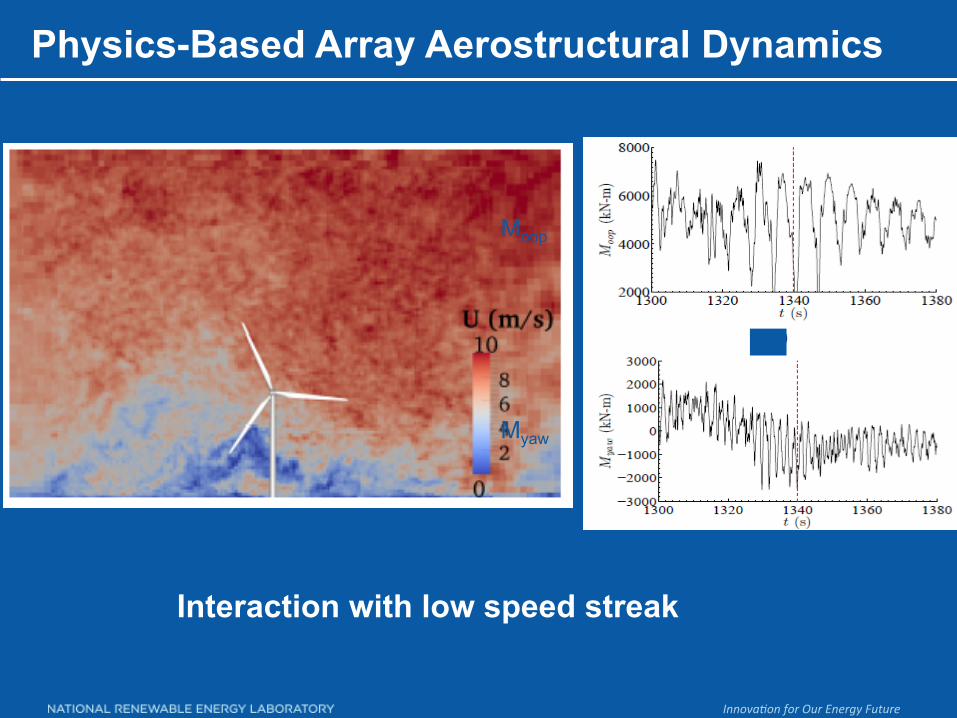

Windplant Aerodynamics Problem

Picture used by permission of Uni-Fly A/S.

Horn’s Rev • Power performance and reliability influenced reduced in arrays.

• Understanding inflow / array interaction is key.

• Computational models, control paradigms and hardware development will be required.

• Requires a detailed understanding of:

– Rotor Wake Interactions – PBL Characteristics – Inflow / Wind farm

Interaction

– Complex Terrain Effects

• Major “Grand Challenge””

Innova+on for Our Energy Future

Physics-Based Array Aerostructural Dynamics

Moop

Myaw

Interaction with low speed streak

Innova+on for Our Energy Future 9

Wind – Market Trends

Innova+on for Our Energy Future

Wind –Market Update - Worldwide

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

Innova+on for Our Energy Future

Innova&on for Our Energy Future 12

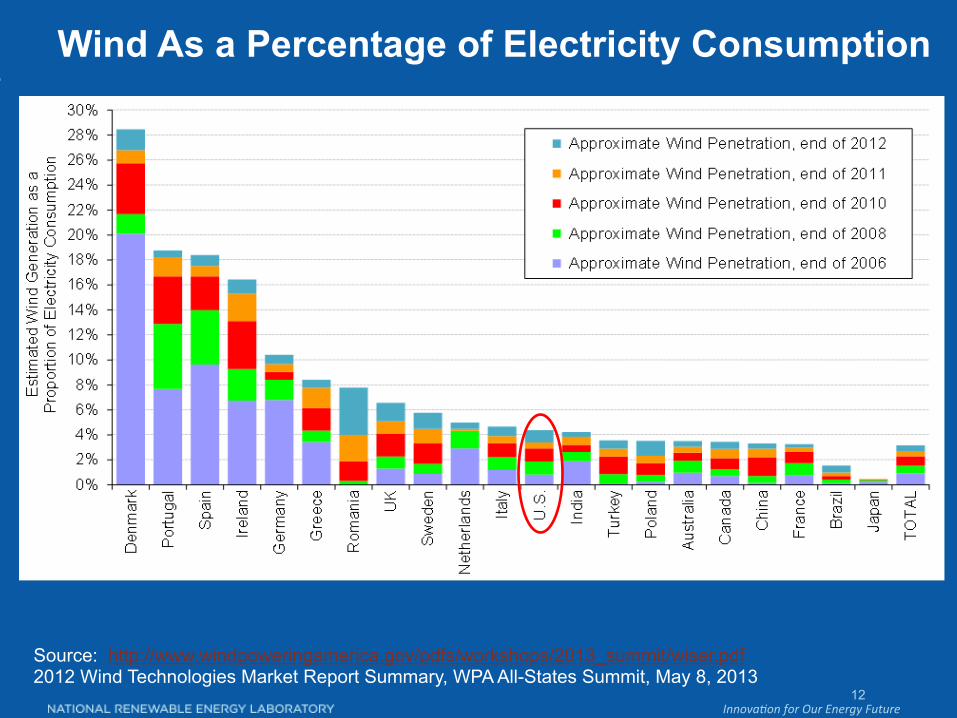

Wind As a Percentage of Electricity Consumption

Note: Figure only includes the countries with the most installed wind power capacity at the end of 2012

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

Innova&on for Our Energy Future 13

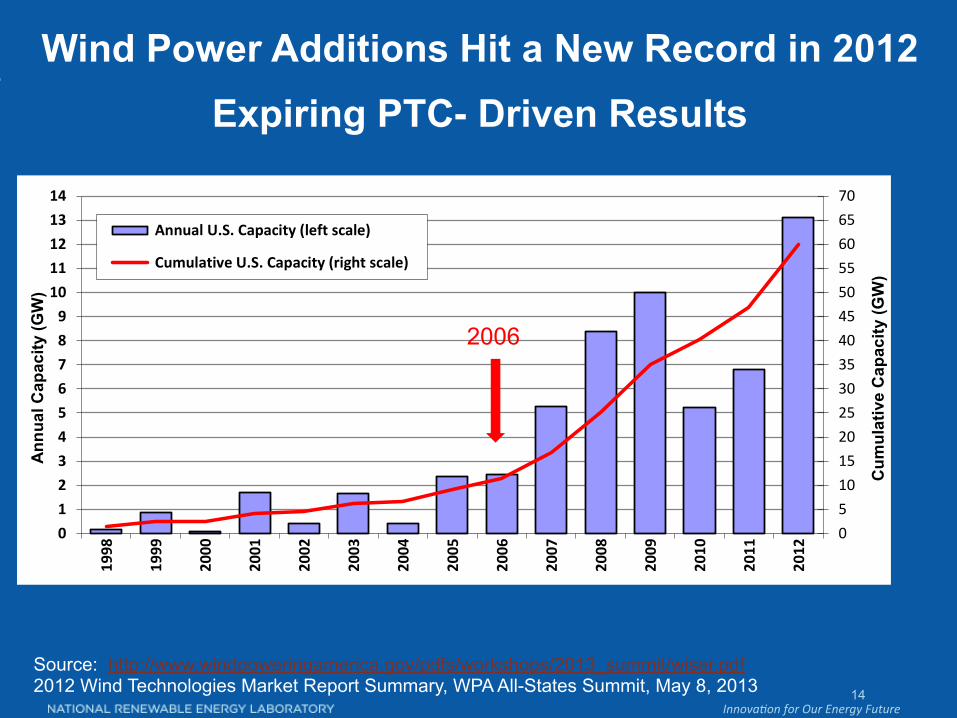

• 13.1 GW of wind added in 2012, more than 90% higher than 2011 • $25 billion invested in wind power project additions • Cumulative wind power capacity up by 28%, bringing total to 60 GW

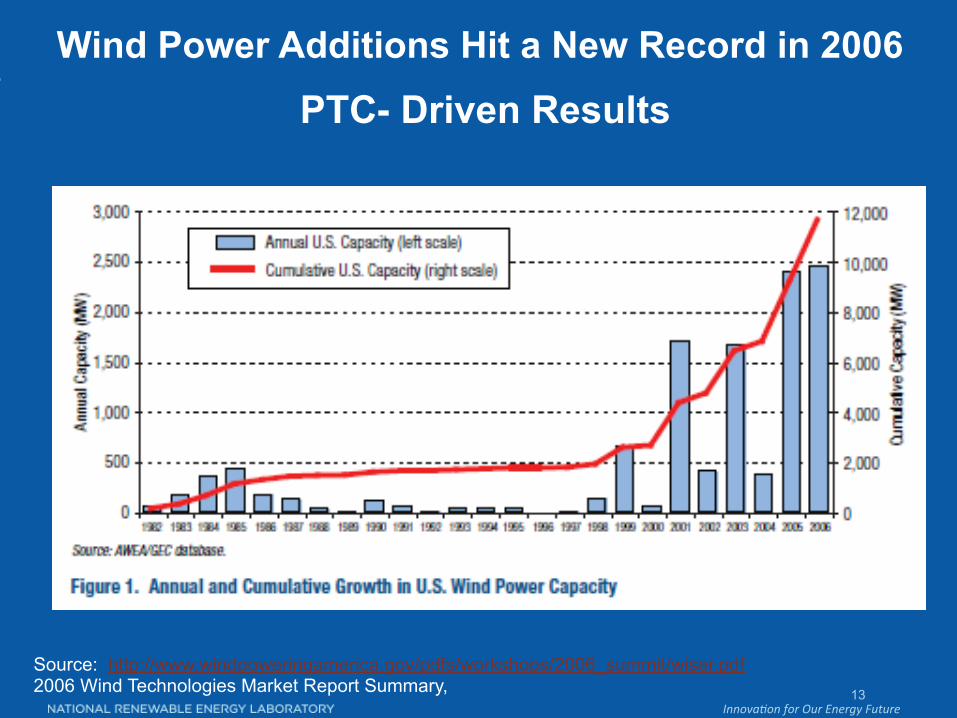

Wind Power Additions Hit a New Record in 2006

PTC- Driven Results

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2006_summit/wiser.pdf 2006 Wind Technologies Market Report Summary,

Innova&on for Our Energy Future 14

• 13.1 GW of wind added in 2012, more than 90% higher than 2011 • $25 billion invested in wind power project additions • Cumulative wind power capacity up by 28%, bringing total to 60 GW

0510152025303540455055606570

01234567891011121314

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Annual U.S. Capacity (left scale)

Cumulative U.S. Capacity (right scale)

Cum

ulat

ive

Cap

acity

(GW

)

Ann

ual C

apac

ity (G

W)

Wind Power Additions Hit a New Record in 2012

Expiring PTC- Driven Results

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

2006

Innova&on for Our Energy Future

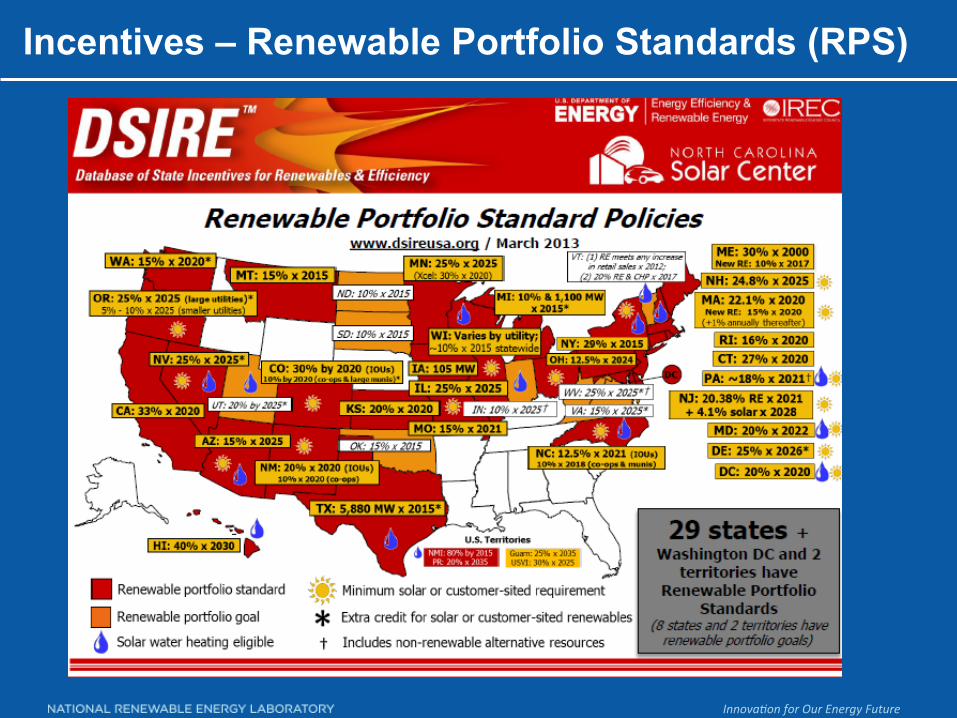

Incentives – Renewable Portfolio Standards (RPS)

Innova&on for Our Energy Future 16

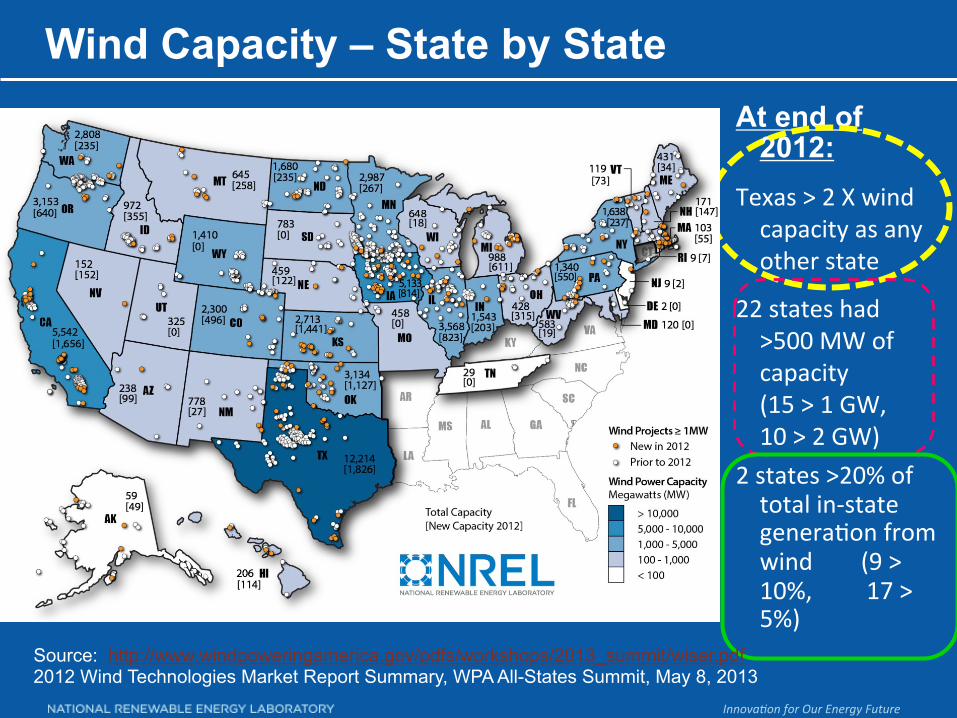

Wind Capacity – State by State At end of

2012: Texas > 2 X wind capacity as any other state

22 states had >500 MW of capacity (15 > 1 GW, 10 > 2 GW)

2 states >20% of total in-‐state generaLon from wind (9 > 10%, 17 > 5%)

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

Innova&on for Our Energy Future 17

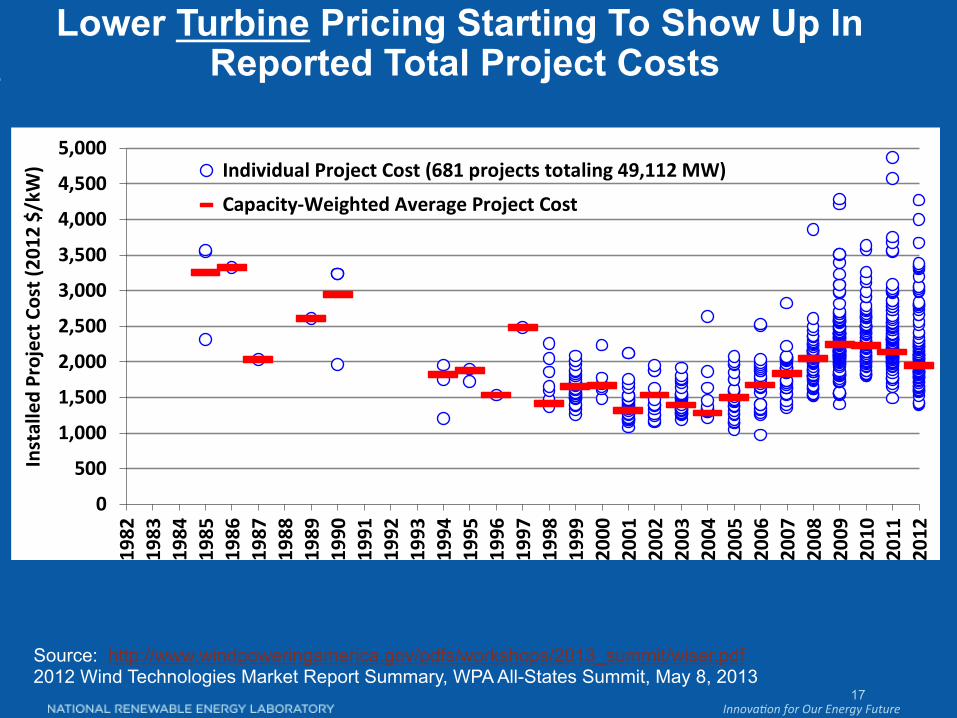

Lower Turbine Pricing Starting To Show Up In Reported Total Project Costs

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,0001982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Installed Project C

ost (20

12 $/kW) Individual Project Cost (681 projects totaling 49,112 MW)

Capacity-‐Weighted Average Project Cost

Source: LBNL

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

Innova&on for Our Energy Future 18

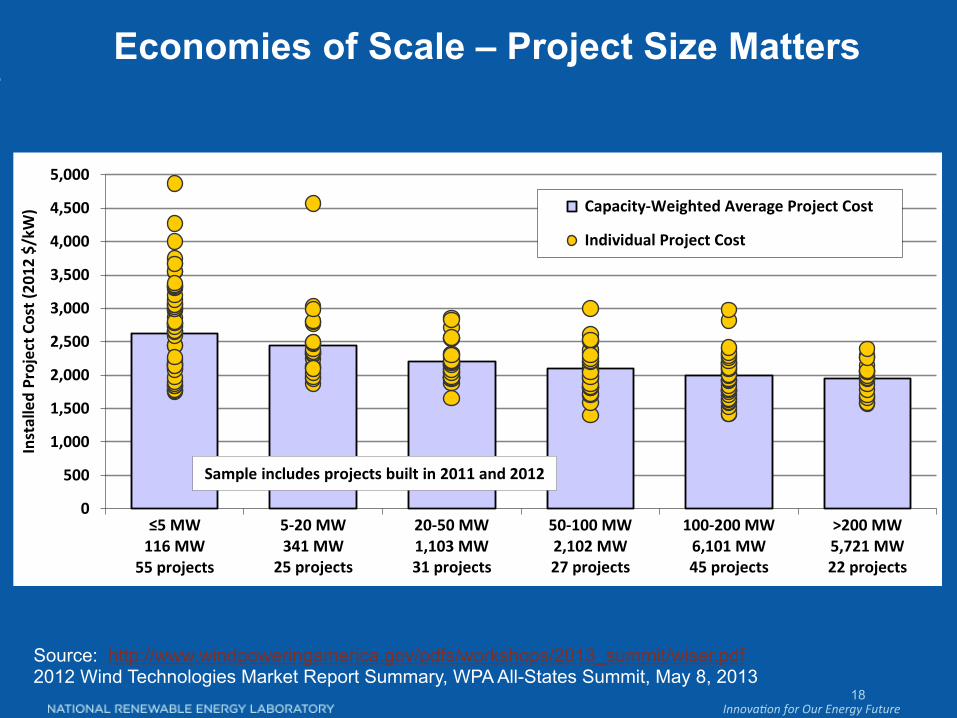

Economies of Scale – Project Size Matters

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

≤5 MW116 MW

55 projects

5-‐20 MW341 MW

25 projects

20-‐50 MW1,103 MW31 projects

50-‐100 MW2,102 MW27 projects

100-‐200 MW6,101 MW45 projects

>200 MW5,721 MW22 projects

Installed Project C

ost (20

12 $/kW) Capacity-‐Weighted Average Project Cost

Individual Project Cost

Sample includes projects built in 2011 and 2012

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

Innova&on for Our Energy Future

Domestic Manufacturing of Wind

Over 160 manufacturing plants capable of producing 12 GW/yr

Source: http://www.windpoweringamerica.gov/pdfs/workshops/2013_summit/wiser.pdf 2012 Wind Technologies Market Report Summary, WPA All-States Summit, May 8, 2013

20

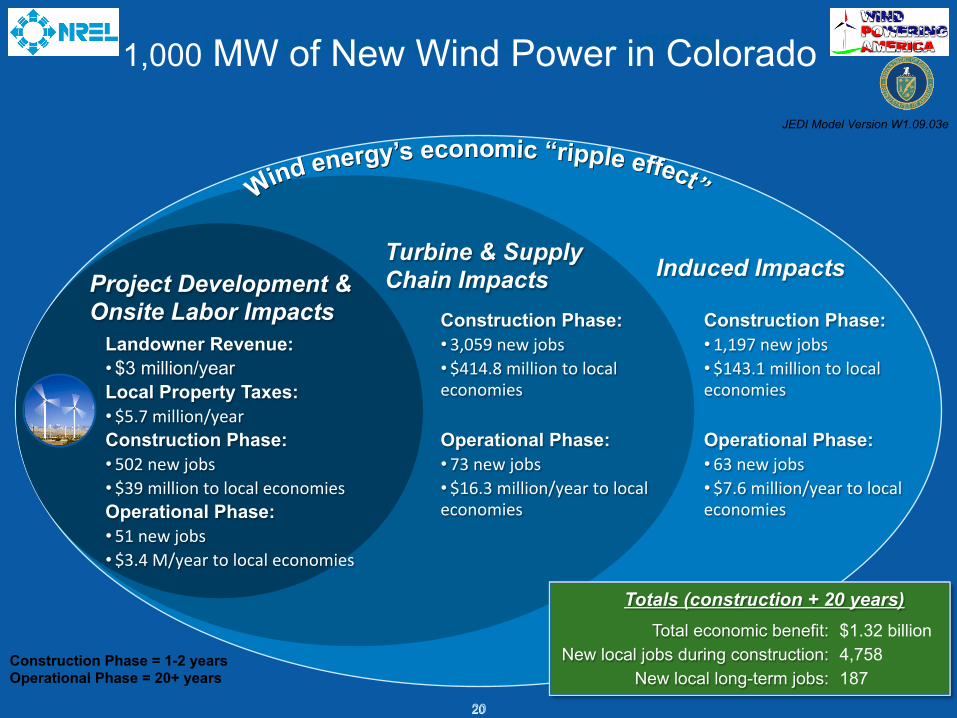

Landowner Revenue:

Project Development & Onsite Labor Impacts

Turbine & Supply Chain Impacts Induced Impacts

Local Property Taxes:

Construction Phase:

Operational Phase:

Construction Phase: Construction Phase:

Operational Phase: Operational Phase:

Jobs and Economic Impacts from the JEDI Model

Construction Phase = 1-2 years Operational Phase = 20+ years

Totals (construction + 20 years)

JEDI Model Version W1.09.03e

Total economic benefit: New local jobs during construction:

New local long-term jobs:

1,000 MW of New Wind Power in Colorado

• 73 new jobs

• $5.7 million/year

• 502 new jobs

• 51 new jobs

• $3 million/year • 3,059 new jobs • 1,197 new jobs

• 63 new jobs • $39 million to local economies

• $3.4 M/year to local economies

• $16.3 million/year to local economies

• $414.8 million to local economies

• $143.1 million to local economies

• $7.6 million/year to local economies

20

$1.32 billion 4,758 187

Innova&on for Our Energy Future

Wind – Technology Trends

Innova&on for Our Energy Future

Derived from K.E. = ½ mv2

P = A * ρ * V3 /2

o P = Power of the wind [Watts] o A = Windswept area of rotor (blades) = πD/4 = πr2 [ m2] o ρ = Density of the air [kg/m3 ] (at sea level at 15°C) o V = Velocity of the wind [m/s]

Wind energy is proportional to velocity cubed (V3): – 25% higher wind speed ≈ 2x’s the power available – If wind speed is doubled, power increases by a factor of eight (23 = 8)!

Small differences in average speed cause big differences in energy production!

Power in Wind Equa/on Wind energy is kinetic energy

-- mass and momentum D

Innova&on for Our Energy Future

This graph is of the GE 1.6-100 1.6 MW with 100m rotor (low wind speed turbine – suitable for Kaneohe) and 82.5m rotor (suitable for sites without extreme wind or turbulence). The enlarged rotor moves the power curve to the left so the turbine produces more power (and energy) at lower wind speeds. At 7 m/s, it might have produced ~500kW with 82.5m rotor, but with 100m rotor it will produce ~700kW – that is a 40% increase !! Over the course of a year, it really makes a difference.

GE 1.6 MW wind turbine

Innova&on for Our Energy Future

Effect of Tower Height

1.0

1.5

2.0

2.5

3.0

3.5

0 50 100 150 200 250Tower Height, ft

Incr

ease

Com

pare

d to

30

ft

Wind Power IncreaseWind Speed Increase

Wind power increase Wind speed increase

Wind Speed and Power Increase with Height Above the Ground

Innova&on for Our Energy Future

Wind – Wind Resource

Innova&on for Our Energy Future

Wind Resource Mapping: Wind Class at 50-m Height

50-m wind mapping (2001-2009)

• Culmination of long-term project that began in 2001; jointly funded by states and DOE/WPA

• Comprehensive validation of WPA maps using available measurement data

• Incorporated state maps by others to produce a national wind map (“patchwork quilt” evident in some regions)

• 50-m wind potential estimates to support U.S. 20% wind scenario study

Innova&on for Our Energy Future 27

Changes in Wind Maps Over Time – Kansas Example

Innova&on for Our Energy Future

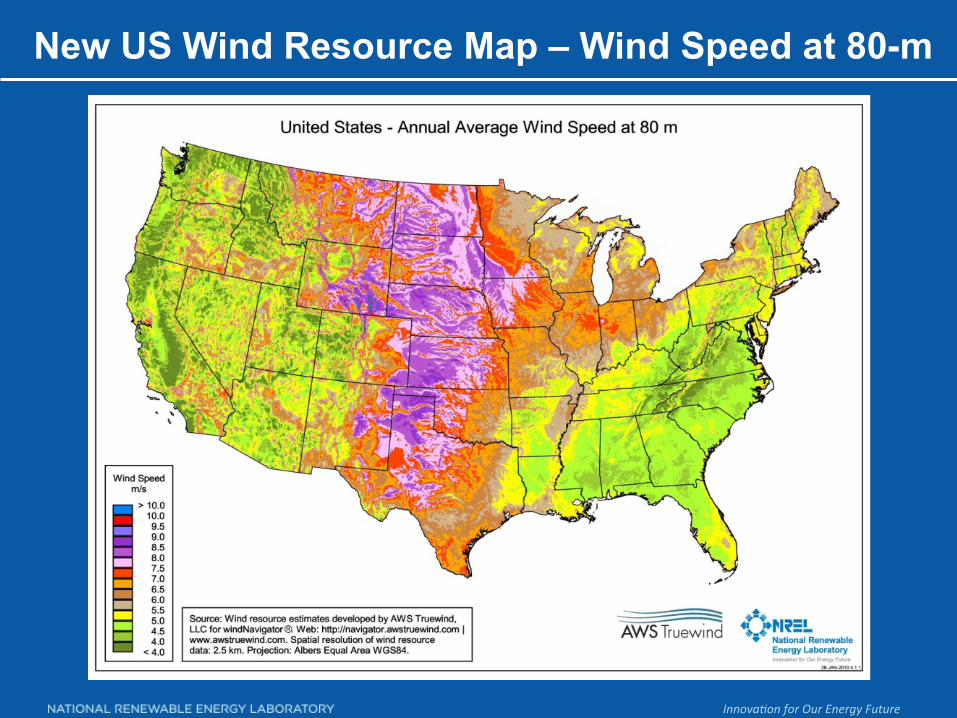

New US Wind Resource Map – Wind Speed at 80-m

Innova&on for Our Energy Future

Georgia – New Turbines Provide Greater Wind Potential

Increasing hub height from 80 to 100m: • Doubles the potential wind capacity in Georgia at sites with a 30% capacity factor from 200 to 400MW

• Quadruples potential wind capacity at 25% capacity factor sites from 500 to 2000 MW

Innova&on for Our Energy Future

• National Wind Technology Center – Research • Wind – Incentives & Markets • Wind Technology Improvements • Wind Resource Assessment Improvements

30

Opportunities for Wind Technology