Présentation PowerPoint - engie.com · Net recurring income group share In €bn NRIgs...

36

April 2018

Transcript of Présentation PowerPoint - engie.com · Net recurring income group share In €bn NRIgs...

April 2018

SUMMARY

At a glance

- ENGIE today 4

- Low CO2 power generation 5

- Leader in global infrastructure 6

- Integrated customer solutions 7

- ENGIE around the world 8

Strategy &

transformation plan

- Sectorial context 10-13

- Strategy 14

- Transformation plan 15-17

- CSR objectives 18

2017 full year

results

- Transformation plan 90 % completed after 2 years 20

- Key figures 21

- Breakdown of Ebitda 22

- Investments focused on growth businesses 23

- Signifiant progress made on portfolio rotation 24

- 2018 guidance: sustain organic growth 25

- 2018 Dividend increase 26

ENGIE and you- Stock reporting 28-32

- bonus dividend 33

- 2018 General Meeting 34

- Useful information 35

- Agenda 36

Navigation through this document is facilitated by an interactive summary that takes you directly to the pages you want

and allows you to return to the summary at any time, using the arrow in the bottom right-hand corner of each page.

Clickable links also provide more details about some subjects

At a glance

ENGIE TODAY

4

CUSTOMER SOLUTIONSLOW CO2 POWER

GENERATIONGLOBAL INFRASTRUCTURE

ENGIE is focused on its 3 core businesses to lead the global energy transition

LOW CO2 POWER GENERATION

5

Natural gas

Renewables

Nuclear

Coal

Other(3)

8%

7% (vs 13 % in 2015)

6%

23% (vs 18 % en 20158)

56%

89% low CO2

102.7 GW(1)

World’s leading independent

producer

102.7 GW(1) installed

> 89% low CO2

23% renewables(2)

(1) figures at 100% as of 12/31/2017

(2) Excluding pumped-storage hydroelectric capacity

(3) Including pumped-storage hydroelectric capacity

Capacity breakdown

As of 12/31/2017

LEADER IN GLOBAL INFRASTRUCTURE

6

3.4

0.2

1.8

1.1

0.3

Europe EBITDA

Infrastructures

2017, in € billions

ca. 32,500 km of network - no. 2

in Europe

ca. 21 billion m3 of regas

capacity - no. 2 in Europe

ca. 12 billion m3 of storage

capacity - no. 1 in Europe

ca. 200,000 km of grid – no. 1

in Europe

€3.8 bn EBITDA on global infrastructure worldwide

France distribution

Transmission

Storage

LNG terminals

24 million of customers in

the world

Global leader in energy

solutions for cities

320 DHC networks worldwide

INTEGRATED CUSTOMER SOLUTIONS

7

EBITDA

by activity

2017, in € billion

0.7

0.4

1.1

2.3

B2B Business to Business

B2T Business to Territories

B2C Business to Customers

Solutions for individuals: green electricity offers, energy and breakdown services, My Power (photovoltaic panels for self-consumption), Elec Car …

Solutions for companies: energy and comsumption management solutions, intelligent digital control, blu.e solution, the software platform to help energy management ...

Solutions for territories: micro-grids, combined storage solutions for solar electricity and batteries, heating and cooling networks, green mobility ...

Breakdown of revenues by

geographic area

ENGIE AROUND THE WORLD

8

€65 bn in 2017

3.9North

America

Latin

America

A

f

r

i

c

a

EuropeAsia, Middle East

&Oceania

4.3

50.95.5

0.4

€65 bn

2017

Strategy

& transformation plan

10

OPPORTUNITIES ARISING FROM A REVOLUTION

DECARBONISATION DECENTRALISATION DIGITALISATION

This energy revolution is intensifying and becoming global, structured by three major trends

10,000

8,000

6,000

4,000

2,000

0

16%

12%

8%

4%

0%

Aggregate Additional capacity in GW

Low CO2 technologies

Coal Gas Other Wind Solar

Renewables Nuclear Gas Wind Solar Other renewables

2015 2020 2025 2030

Sources: Bloomberg New Energy Finance, AIE, ENGIE 2015

(1) CAGR:compound annual growth rate

11

Development of the global energy mix up until 2030

Additional capacity 2015-2030

(CAGR (1) by technology)

Natural gas & renewable energies, drivers of a global energy transition

44%(80% today)

36%

20%

Decentralised solutions

In 2030

12

SIGNIFICANT INCREASE IN DECENTRALISED SOLUTIONS WORLDWIDE

Source: AIE, Energy for All, 2011; MIT 2015

B2C, off-grid solutions

Centralised power generation

B2T & B2B microgrids

• The revolution in energy storage and

generation technologies is prompting the

emergence of smaller, competitive,

decentralised infrastructure.

• Consequently, infrastructure and offers need

to be adapted to the coexistence of centralised

and decentralised energy solutions.

13

DIGITALISATION, A PIVOTAL ELEMENT IN THE ENERGYREVOLUTION

• In a world where infrastructure is

becoming smaller, digital technology is

accelerating this trend and occupying

a central role, especially with regard to

guaranteeing a balance between

energy generation and consumption at

all times.

• For example, the number of

connected objects in the world will

quadruple by 2020 to total 25 billion*.

Big Data

Autonomousgeneration

Predictive

maintenance

Energyoptimisation

Smarthomes

Smartcities

Seamlesscustomerjourneys

* Source Gartner 2015

AMBITIONS for 2018

LOWER EXPOSURE

TO COMMODITY PRICES

DOWNSTREAMPRIORITY TO

LOWEST CO2 OPTIONS

CO2 LIGHT ACTIVITIES(2)

EBITDA >90%

CO2

CONTRACTED/REGULATED(1)

EBITDA > 85%

CUSTOMER SOLUTIONS DEVELOPMENT

(1) Excluding merchant power generation, E&P and LNG supply & sales

(2) Low CO2 power generation, gas infrastructures & LNG, downstream

14

3 CLEAR DIRECTIONS

15

A 3-year transformation plan based on 4 pillars

* Net of DBSO proceeds; excluding Capex related to E&P and upstream / midstream LNG (including Touat and Cameron) for EUR 0.3 billion and Corporate Capex for EUR 0.2 billion

15

Agile and connected

Technology-focused

Talent-oriented

Adapt

the Group

Redesign

and simplify

the portfolio

€14,3 billion*

Growth in CAPEX

€15 billion

Portfolio rotation

(net debt reduction)

Pave the way for

the future

€1billion

Spendings in

innovation/digital

Improve

efficiency

€1.3 billion

(net EBITDA increase)

16

FOCUS OUR STRENGTHS ON OUR 3 CORE BUSINESSES

Coal

Activities with

exposure to commodity

prices

Exploration & production

LNG upstream activities

CAPEX

PORTFOLIO

ROTATION

Integrated solutions

for customers:

- Energy efficiency

- Energy supply

- Cities and customers

- Decentralised

renewables

- Heating/cooling networks

Gas distribution

Transmission

LNG terminals & sales

Storage

Solar

hydraulic, wind

Gas

GLOBAL

INFRASTRUCTURE

LOW CO2 POWER

GENERATION

CUSTOMER

SOLUTIONS

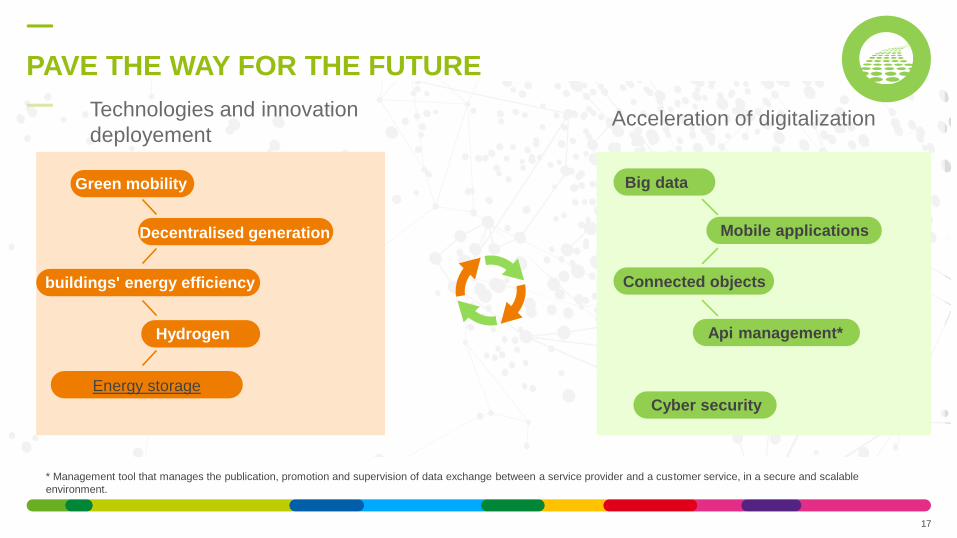

Acceleration of digitalizationTechnologies and innovation

deployement

17

PAVE THE WAY FOR THE FUTURE

Green mobility

Decentralised generation

buildings' energy efficiency

Hydrogen

Energy storage

Big data

Mobile applications

Connected objects

Api management*

Cyber security

* Management tool that manages the publication, promotion and supervision of data exchange between a service provider and a customer service, in a secure and scalable

environment.

18

CSR OBJECTIVES TO SUPPORT THE GROUP PERFORMANCE

Objective Indicator

Target value in

2020

Effective value in

2016

Effective value in

2017

Supporting our

customers in the energy

transition

Satisfaction rate among our B2C customers 85% 81% 83%

Renewables Share of renewable energy in the generating capacity 25% 19.5% 23.1%

Greenhouse gasemissions

% reduction in ratio of CO2 emissions to energy production compared with 2012

-20% -11.3% -18.1%

Stakeholder dialogue% of industrial activities covered by a suitable dialogue

and consultation mechanism100% 20% 48%

Gender diversity % of women in the Group’s workforce 25% 21.9% 22.2%

Health and safety Internal frequency rate for occupational accidents <3 3.6 3.3

2017 FY Results

20

• Acquisitions on new

promising markets (EV

Box, Icomera)

• A Business Unit

dedicated to renewable

hydrogen

• Lean 2018:

Identified

• Target raised by €100

million, for a total or

€1.3 billion of net gains

expected at Ebitda

level by 2018

• HQ adaptation to the

Group's new

challenges

• Involvement of

managers in the

Group’s transformation

PAVE THE WAY FOR THE FUTURE

IMPROVE EFFICIENCY

REDESIGN AND SIMPLIFY THE PORTFOLIO

ADAPT THE GROUP

Additional Medium-term

growth drivers

Improve

competitiveness

Refocus on

growth engines Agile organization

• Rotation program well

advanced

• Investment program

well engaged

• Growth engines

already account for

of EBITDA

90%

97%

91%

100%

in €bn

REVENUES 65.0 + 1.7%

EBITDA 9.3 + 5.3%

NET RECURRING INCOME GROUP SHARE(1) 2.6(1) 2.4-2.6

CASH-FLOW FROM OPERATIONS 8.3

NET DEBT / EBITDA 2.25 x 2.5 x

CREDIT RATING A- / A2 «A » Category

DIVIDEND €0.70 / action €0.70 / action

NET INCOME RESULT, GROUP SHARE 1.4 €bn

KEY FIGURES

21

2017 Results ∆ organic

2017/2016 Indication/Guidance 2017

(1) NRIgs excluding IFRS 5 treatment for E&P, i.e. excluding the D&A upside (EUR 0.1 billion) from IFRS 5 accounting treatment (ENGIE E&P International business classified as “discontinued operations”), therefore underlying contribution of of E&P of EUR 0.2 billion

9.3-9.9

BREAKDOWN OF EBITDA

22

EBITDA by métiers In €bn

2.3

3.8

(0.8) Others

9.3(1)

4,1

Global Infrastructure (3)

Client Solutions

Low CO2 Power generation(2)

(1) Excluding others and low co2 merchant power generation for €1bn (2) including €1bn of low co2 merchant power generation(3) Including €0.03bn upstream

INVESTMENTS FOCUSED ON GROWTH BUSINESSES

23

2.2

1.8

0.5

4.5

1.8 0.7

€14.3bn(1)

(1)Net of DBSO proceeds; excl. E&P and LNG upstream/midstream Capex (including Touat and Cameron) for €0.3bn and corporate Capex for €0.2bn

B2T

B2C

RES

Thermal

contracted

Thermal

Merchant*

€7.1bn 50%

B2B

€4.6bn 32%

€2.6bn 18%

Growth Capex 2016-18

In €bn

Capex plan by geographies

France

36%

Latam

33%

Rest

of the world

16%

Europe

15%

Customer soluitions Infrastructures

Power generation– Renewable & thermal contracted

Power generation– Merchant

* exposure to commodity prices

SIGNIFICANT PROGRESS MADE ON PORTFOLIO

ROTATION

24

Bookedas of Dec

2017

Closed2018 YTD

Signed(closing

in progress)

Processlaunched

Total netdebt

reduction

8.7

+3.0

15

+1.6

€13.2bn of disposals executed Ahead of plan with already ~ 90% executed to date

~ € 9bn closed in 2016-17,

mainly:

US merchant & coal assets

€ 3bn closed to date in 2018:

E&P, Loy Yang B, Egaz-Degaz

LNG diposal expected to close

in 2018

Net debt impact

In €bn

25

2018 GUIDANCE: SUSTAINED ORGANIC GROWTH

Net recurring income group share

In €bnNRIgs €2.45-2.65bn

without E&P and LNG contributions

Dividend:

Final dividend 2017 to be paid in May New

policy in 2018

Leverage & rating:

“A” category rating Net debt / EBITDA ≤

2.5xexcluding E&P

and LNG2018e

2.36(2)

2.45-2.65(3)

2017reported

2.660,10 D&A uplift(1)

+ 8 %

(1) Coming from IFRS 5 treatment of E&P(2) Without E&P and LNG contributions and without IFRS 9 and IFRS 15 treatments(3) Main assumptions: no E&P and LNG contributions, average weather in France, full pass through of supply costs in French regulated gas tariffs,

no significant accounting treatment changes except for IFRS 9 and IFRS 15, no major regulatory and macro-economic changes, market commodity prices as of 12/31/2017, average forex for 2018: €/$: 1.22; €/BRL: 3.89, no significant impacts from disposals not already announced.

* ENGIE completed the sale of its exploration & production

activities in 2018 and the sale of its LNG upstream activities is

underway.

*

2018 DIVIDEND INCREASE

26

0.7 0.7

2017 2018 2018 - upgraded

0.75

Dividend per share (DPS) in € per share

+7.1%

71%Indicative pay

out ratio(1)70%66%

(1) Basé sur le RNRpg des activités poursuivies ; calculé sur le milieu de fourchette de la guidance 2018

Previous DPS policy

Upgraded

2018 DPS

ENGIE and you

IndicesMarkets2017 Stock market information

THE SHARE

28

ISIN code*: FR0010208488

Ticker symbol**: ENGI

2017 higher: €15.16

2017 lower: €10.77

Last (12/29/2017) : €14.34

Market capitalization as of 31/12/2017:

35 €bn

ca. 6,500,000 shares traded per day on

average in 2017

Euronext paris (compartiment A)

Euronext Bruxelles

Eligible for the deferred settlement

service (SRD) and equity savings plan

(PEA)

Indices : CAC 40, BEL 20, Euro Stoxx

50, Stoxx Europe 600, MSCI Europe,

Euronext 100, FTSE Eurotop 100,

Euro Stoxx Utilities, Stoxx Europe

600 Utilities

EGS indices : Dow Jones

sustainability(World, Europe),

Euronext Vigeo Eiris (World 120,

Eurozone 120, Europe 120, France

20, CAC 40 Governance)

*The ISIN (International Securities Identification Numbers) code is an international standard for identifying and tracking a financial

instrument.

**The ticker symbol is an initials (diminutive of the name) appearing beside the ISIN code of the values facilitating their

identification.

2017 PERFORMANCE

29

10,5

11

11,5

12

12,5

13

13,5

14

14,5

15

15,5

02/01/2017 02/04/2017 02/07/2017 02/10/2017

ENGIE Euro Stoxx Utilities CAC 40 BEL 20

29/12/2017

Gross

Perf

Total

Shareholder

Return

ENGIE +18% +25,5%Euro Stoxx

Utilities +16% +16%

BEL 20 +10% +10%

CAC 40 +9% +13%

Source : Thomson Reuters – based on ENGIE shareprice

* Sectoral benchmark indexing European companies producing and distributing gas, electricity and water : A2A, EDP-Energias, EDF, Enagas, Endesa, Enel, ENGIE, E.ON, Iberdrola, Innogy, Italgas, Gas Natural SDG, RED

Electrica, Rubis, RWE, SNAM, SUEZ, Terna, Uniper, Véolia Environnement

*

PERFORMANCE SINCE 2018

30

BEL 20 -3%

FY Results

03/08/2018

12

12,5

13

13,5

14

14,5

15

02/01/2018 17/01/2018 01/02/2018 16/02/2018 03/03/2018 18/03/2018 02/04/2018

ENGIE Euro Stoxx Utilities CAC 40 BEL 20*

CAC 40 -1%

ENGIE -1%

Euro Stoxx

Utilities -2%

Source : Thomson Reuters – based on ENGIE shareprice

* Sectoral benchmark indexing European companies producing and distributing gas, electricity and water : A2A, EDP-Energias, EDF, Enagas, Endesa, Enel, ENGIE, E.ON, Iberdrola, Innogy, Italgas, Gas Natural SDG, RED

Electrica, Rubis, RWE, SNAM, SUEZ, Terna, Uniper, Véolia Environnement

In 2017, ENGIE achieved one of the best performances of the CAC 40, driven by significant advances in its transformation plan.

Since the beginning of 2018, the sector and the share have been penalized by:

renewed pressure on interest rates in Europe benefiting so-called "cyclical" values to the detriment of so-called "defensive"

values (sectorial rotation)

the recent rise of the euro against the dollar

SUEZ profit warning ( 23 January 2018) of its 2017 earnings objectives and 2018 outlook

The publication of the Group's results on March 8 was welcomed with a rise of 3.8% at closing, outperforming the CAC 40 and

the sector by around 250 basis points. The growth outlook and the rise in the dividend of 7.1% for 2018 have positively

surprised.

SHARE PRICE EVOLUTION ANALYSYS

31

PERFORMANCE COMPARED TO THE MAIN INDICES

32

En %

ENGIE* 5%

Euro Stoxx

Utilities 4,7%

BEL 20 3,6%

CAC 40 3,3%

Return to April 6

Source : Thomson Reuters

* Based on dividends paid in 2017

OAT 10 years

France 0,9%

2

3

4

5

6

7

8

9

10

02/01/2017 02/04/2017 02/07/2017 02/10/2017 02/01/2018 02/04/2018

Rendement ENGIE Rendement Euro Stoxx Utilities Rendement CAC 40 Rendement BEL 20

A BONUS DIVIDEND

33

Register your shares prior to December 31, 2018 to benefit in 2021 from the bonus dividend related

to 2020.

ENGIE rewards the sharehoders’ loyalty

+ 10%bonus dividend for all shareholders who registered shares

(directly or indirectly for at least 2 continuous years

For more information on the dividend policy, go to engie.com

ANNUAL GENERAL MEETING: FRIDAY, 18 MAY, 2018

34

An Internet area, secured and dedicated to the vote

prior to the General Assembly will be open from April

30 9am until May 17 at 3pm.

If you are a bearer shareholder: Log in to your bank's

website, you can vote online if your institution has

signed up for the Votaccess system.

If you are a registered shareholder: connect to the site

sharinbox.societegenerale.com

Access the live or deferred broadcast of the

General Assembly from 2.30 pm

The Annual General Meeting will be held on May 18 at the Palais

des Congrès in Paris at 2.30 pm

An Assembly that will open a new page in the history of ENGIE,

with the last term of Gérard Mestrallet as Chairman of the Group;

the appointment of a new independent director, Jean-Pierre

Clamadieu, who will transition into the role of chairman, will thus be

submitted for approval to shareholders.

Find all the documentation on engie.com/ag

Discover all the terms and conditions of participation in

the General Meeting and the resolutions on the agenda

in the digital version of the Notice of Meeting 2018,

available on engie.com/ag.

PRACTICAL INFORMATION

35

ENGIE shrae price

Holding registered securities

The dividend

The loyalty bonus

General Meeting

The tax framework for your shares

Press releases

Publications by ENGIE

ETRE ACTIONNAIRE ENGIE LIENS UTILES

engie.com/actionnaires

engie.com/club

Mes questions d’argent (in french)

Euronext, Paris stock exchange

L’Ecole de la Bourse (in French)

placedesactionnaires.com (in French)

Lexicon (in French)

facebook.com/actionnairesengie

[email protected] (France)

(from France)

[email protected] (Belgium)

(from Belgium)

0 800 300 030

0 800 25 125

BEING AN ENGIE SHAREHOLDER

USEFUL LINKS CONTACT US

AGENDA

36

Thursday, may 24

Payment of the balance dividend:

€0.35 per shareTueday, may 15

Financial information as of 31 March 2018

Friday, may 18

Annual General Meeting

Friday, July 27

2018 first Half results