PRESENTATION ON NIS GROUP’S RESULTS -...

26

PRESENTATION ON NIS GROUP’S RESULTS for Q1 2017 May 10 th , 2017 Anton Federov Finance, Economics, Planning and Accounting Function

Transcript of PRESENTATION ON NIS GROUP’S RESULTS -...

PRESENTATION ON NIS GROUP’S RESULTS for Q1 2017

May 10th, 2017 Anton Federov Finance, Economics, Planning and Accounting Function

• Well Is-X-5 (in a recently discovered oil reservoir Idjos) tested and pre-commissioning started

• 3D data acquisition completed in South Banat I

• 3D data acquisition started at Turija III

• Gas field Ostrovo – reservoir Sm-4 (GGS/CNG) pre-commissioning started

• GGS Velika Greda South pre-commissioning started

• Drilling of well Тeremia-1000 in block Ex-7 finished

2

NIS in Q1 2017 Exploration and Production

3

NIS in Q1 2017 Refining

• Workover of Bitumen plant

• Catalyst at С-400 regenerated

• EPCm bids received in a bidding procedure for work package 2 in the Bottom of the Barrel project

• The process of implementation of OMS action plan started

• Revitalization of plant Old Claus

• New crude oil type Novy Port tested in the refining process

• The approval of a new XS format of refuelling stations is under way

• The share of the „On the Road with Us“ loyalty programme in the sales to individuals is 46% as of March 31st, 2017

• Development of sales of branded fuels in foreign assets – G-Drive Diesel at NIS Petrol PS,

• Marketing activities (in Serbia – 20, in Bosnia – 20, in Romania – 12, in Bulgaria – 7)

• Introduction of 4 new sales items under the own brand Drive Café

• Successful Introduction into the market of winter-grade G-Drive Diesel

• Losses were reduced at storages by 40% and those in transportation by 77% on Q1 2016.

4

NIS in Q1 2017 Sales and Distribution

• Preparation and reconciliation of EPC contract with the selected contractor and project financing contract for CHPP Pancevo is ongoing.

• Negotiations started for the construction project of small power plant Novo Milosevo by BOOT model

• With regard to the small power plant Velebit 3 the design required for obtaining a building permit completed; feasibility study prepared

• Pre-commissioning of CNG plant at reservoir Ostrovo started

• Simplified mining design (URP) and factory testing of equipment for CNG Zarkovo 2 finished

• Agreed electricity trading volume amounting to 1.78 TWh

5

NIS in Q1 2017 Energy

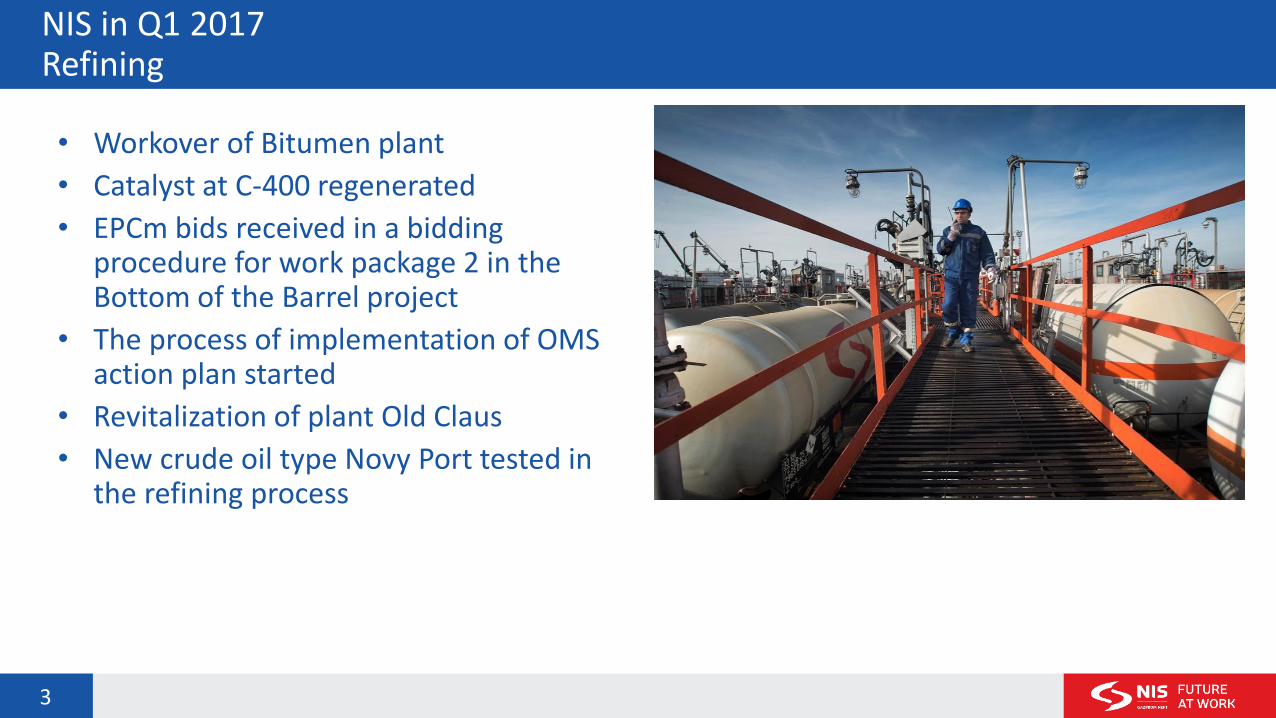

Exchange rate USD/RSD

+4% Price of crude oil type Urals RCMB, $/bbl

+62%

Macroeconomic indicators Stable exchange rate, higher oil price

6

20

30

40

50

60

1/3 1/19 2/6 2/22 3/10 3/28

2016

Average 2016

2017

Average 2017

105

110

115

120

1/1 1/16 1/31 2/15 3/1 3/16 3/31

2016

Average 2016

2017

Average 2017

HSE indicators Positive trend

7

Transparency increase LTIF RAR

Q1 2016 Q1 2017

13,862 15,181

206 235

20 25

4 2 Major incidents

Medium Incidents

Minor incidents

Near miss incidents

1.96

1.30 1.71

Q1 2016 Q1 2017 Plan2017

2017

Plan2017

2016

0.32 0.30 0.31

Q1 2016 Q1 2017 Plan2017

2017

Plan2017

2016

13% 3% 3%

32%

Key indicators NIS Group

8

Key indicators Unit of measurement

Q1 2017 Q1 2016 ∆

Urals $/bbl 52.2 32.2 +62%

Net profit bn RSD 5.4 0.3 +18x

EBITDA bn RSD 11.1 3.8 +3x

OCF bn RSD 4.5 3.6 +25%

Calculated commitments related to public revenue bn RSD 35.6 32.8 +8%

Oil and gas production thousand TOE 343 377 -9%

Crude oil and semi-finished products refining volume thousand tons 765 776 -1%

Total turnover of petroleum products thousand tons 717 703 +2%

CAPEX bn RSD 4.7 4.6 +1%

Total indebtedness to banks (the overall debt to banks + letters of credit)

mn USD 664 633 +5%

Trends in the motor fuel market Q1 2017/Q1 2016

9

Regional consumption of motor fuels is on the rise: - macroeconomic trends - fuel consumption growth in the transport

sector, processing industries, construction industry

Serbia

• Diesel consumption growth: — better results in the construction and processing

industries — transport growth

• Some diesel fuel consumption remains in the grey economy

Slovenia

3.1%

Croatia

1.9%

Bosnia and Herzegovina

1.3% Bulgaria

1.2%

Romania

1.4%

Hungary

2.9%

Serbia 1%

Market share – Serbia Petroleum products market

• The total consumption of petroleum products is on the rise

• Growth in consumption of jet fuel, straight-run gasoline, and motor gasoline, diesel, heating fuel, heavy fuel oil and lubricants:

— lower prices

— infrastructure works

• Lower consumption of LPG, bitumen, coke and other petroleum products

10

195 (26%)

193 (25%)

556 (74%)

582 (75%)

751 775

Q1 2016 Q1 2017estimate

NIS

Others

3.2%

Volume of petroleum products market, thousand tons

Market share of NIS shows a growing trend. If grey market suppression measures prove effective and the sales return to the normal distribution channels, further market share growth of NIS may be expected.

Market share – Serbia Retail market

• Retail market growth by 2.8%

• Fuel consumption growth owing to: — transport growth

— increase in the number of vehicles

— increase in transit traffic

11

191 (56%)

195 (56%)

150 (44%)

155 (44%)

341 350

Q1 2016 Q1 2017estimate

NIS

Others

2.8% Retail market, thousand tons

NIS has increased slightly its market share by 0.2%.

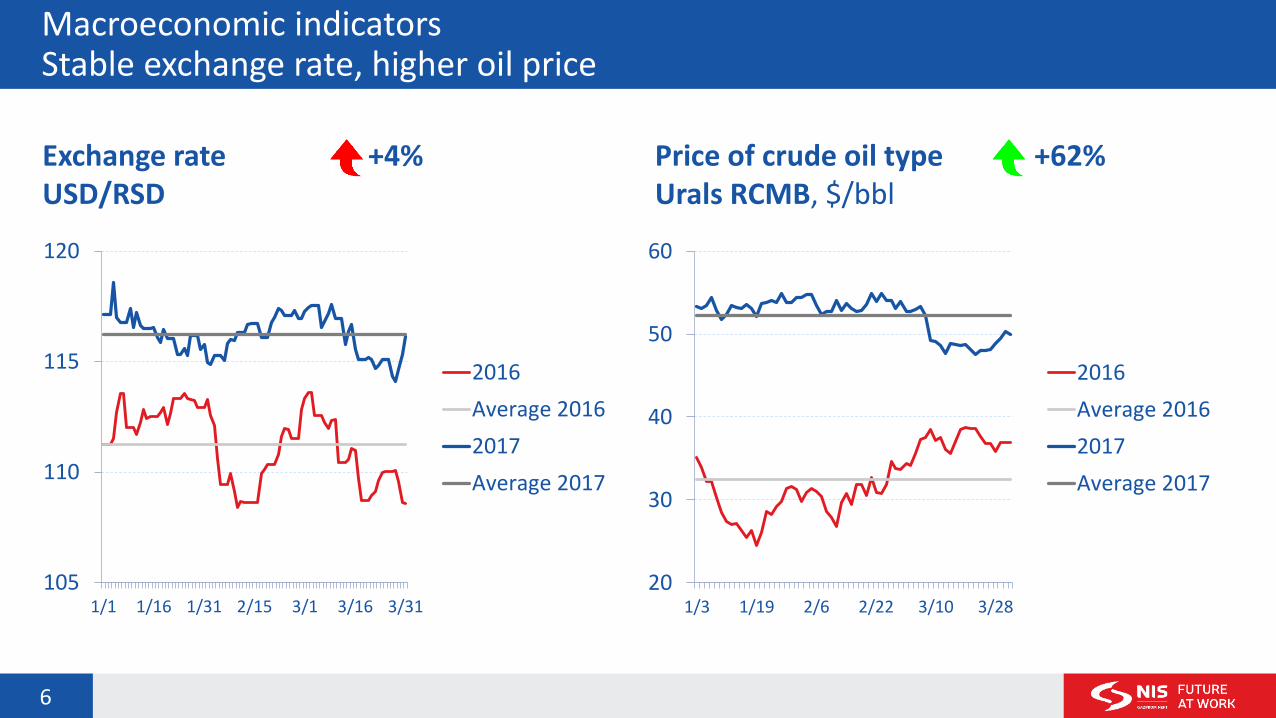

Market share – region Q1 2017/Q1 2016

12

Bosnia and Herzegovina

Number of PS: 35* Total market %: 11.1% Retail market %: 10.7%

Romania

Number of PS: 18 Total market %: 0.9% Retail market %: 1.5%

Bulgaria

Number of PS: 35 Total market %: 6.4% Retail market %: 4.8%

*and two petrol stations in DODO operating model

Operation indicators Exploration and Production

• Volume of oil and gas production in first quarter of 2017 was down by 9% compared with same period previous year.

13

251 227

112 105

14 11

377 343

Q1 2016 Q1 2017

Angola

Domesticgas

Domesticoil

Oil and gas production, thous. TOE -9%

Operation indicators Refining

• The volume of refining is a result of meeting the needs of the market, available stocks and optimisation of the basket of raw materials (growth in crude oil refining, reduction of additional raw material)

14

-1 %

245 224

474 491

56 51

776 765

Q1 2016 Q1 2017

Semi-FinishedProducts

Imported Crude

Domestic Crude

Refining of crude oil and semi-finished products, thousand tons

Operation indicators Sales and Distribution

• Retail in Serbia – growth 3%

• Wholesale in Serbia – growth 2%

• Export – drop 16%

• Foreign assets – growth 25%

15

151 156

56 70

411 420

86 72 703 717

Q1 2016 Q1 2017

Export

Wholesale -Serbia

Foreign assets

Retail - Serbia

+2% Sales volume*, thousand tons

*Including internal sales

Financial indicators Net profit

• Growth in the price of crude oil and petroleum products

• Measures to increase operational efficiency and decrease costs

• Growth in the volume of sales

• Positive foreign exchange differences

16

0.3

5.4

Q1 2016 Q1 2017.

18x Net profit, bn RSD

Financial indicators EBITDA

• Growth in the price of crude oil and petroleum products

• Measures to increase operational efficiency and decrease costs

• Growth in the volume of sales

17

3.8

11.1

Q1 2016 Q1 2017

3x EBITDA, bn RSD

Financial indicators OCF

• Higher inflows — higher prices of petroleum products

— higher EBITDA

18

3.6 4.5

Q1 2016 Q1 2017

+25% OCF, bn RSD

Financial indicators CAPEX

19

4.6 4.7

Q1 2016 Q1 2017

+0.7% CAPEX, bn RSD

66% 4%

24%

4% 1% 1% Exploration andProduction

Services

Refining

Sales andDistribution

Energy

Corporate Centre

CAPEX by segment

Financial indicators CAPEX for 2017

20

+10% CAPEX, bn RSD CAPEX by segments, bn RSD

28.6 31.5

2017Plan

2017Estimate

Segment Estimate Business

Plan ∆

Exploration and Production 18.9 16.7 +2.2

Services 1.2 1.0 +0.2

Refining 6.0 5.7 +0.3

Sales and Distribution 3.9 4.0 -0.1

Energy 0.8 0.9 -0.04

Corporate Centre 0.6 0.4 +0.2

31.5 28.6 +2.9

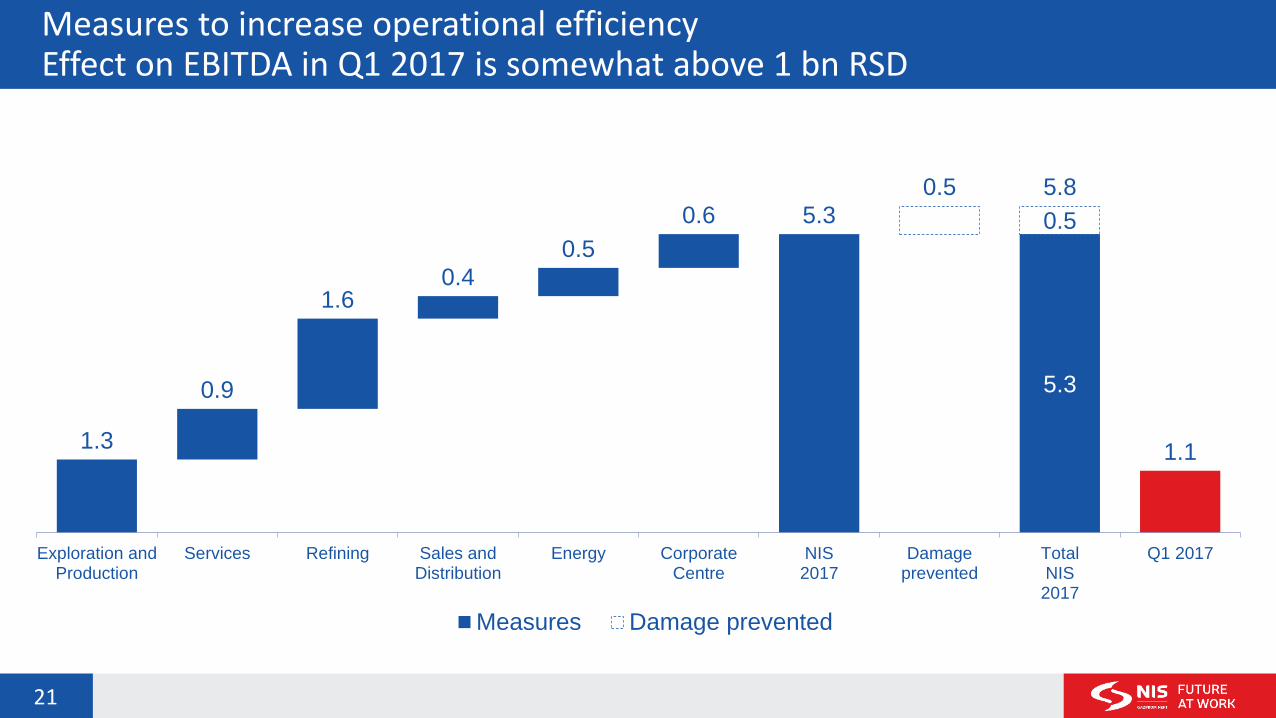

Measures to increase operational efficiency Effect on EBITDA in Q1 2017 is somewhat above 1 bn RSD

21

5.3

0.5

1.3

0.9

1.6 0.4

0.5

0.6 5.3

0.5 5.8

1.1

Exploration andProduction

Services Refining Sales andDistribution

Energy CorporateCentre

NIS2017

Damageprevented

TotalNIS2017

Q1 2017

Measures Damage prevented

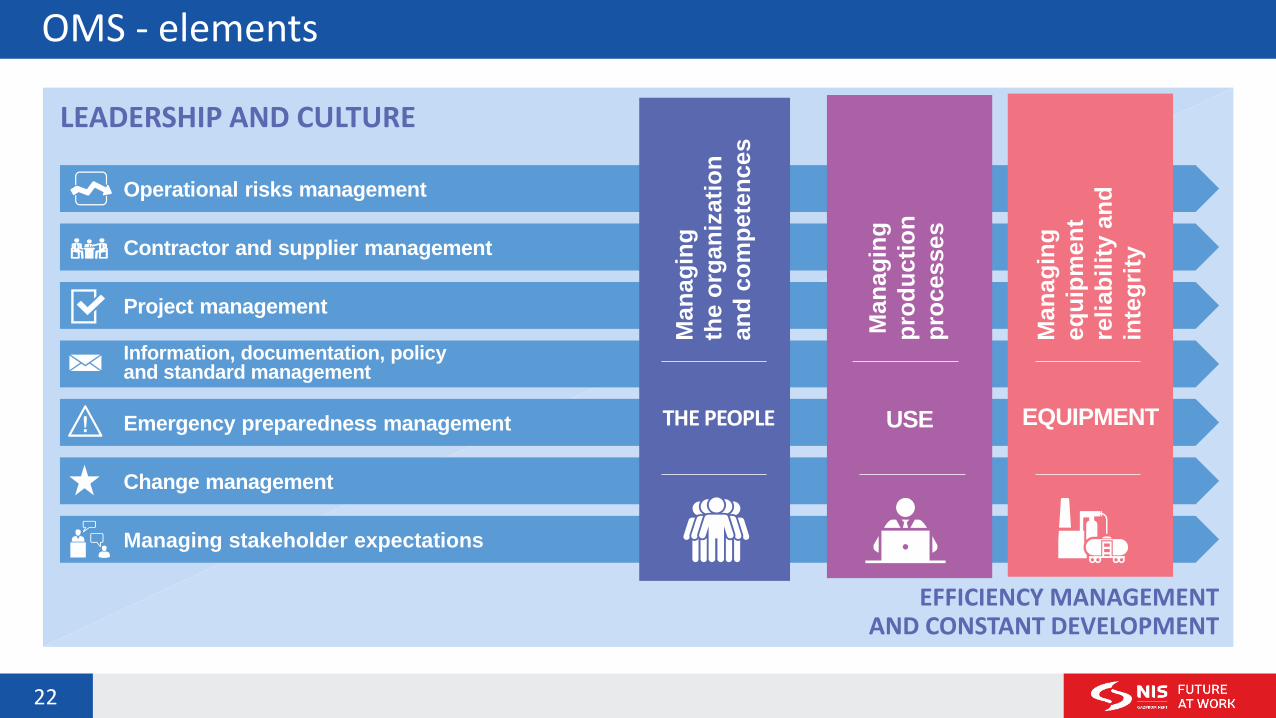

OMS - elements

22

Operational risks management

Change management

Contractor and supplier management

Project management

Information, documentation, policy and standard management

Emergency preparedness management

Managing stakeholder expectations

LEADERSHIP AND CULTURE

EFFICIENCY MANAGEMENT AND CONSTANT DEVELOPMENT

Man

ag

ing

the o

rgan

izati

on

an

d c

om

pete

nces

Man

ag

ing

pro

du

cti

on

pro

cesses

Man

ag

ing

eq

uip

men

t

reli

ab

ilit

y a

nd

inte

gri

ty

THE PEOPLE USE EQUIPMENT

Bank indebtedness Structure of loan portfolio in terms of maturity and currency

23

278

275

28

47

271

91

153

186

116

516

336

418

356

184

507

511

477

543

793

611

446

403

456

598

664

662

659

12/31/'09

12/31/'10

12/31/'11

12/31/'12

12/31/'13

12/31/'14

12/31/'15

12/31/'16

3/31/'17

up to 1 year

over 1 year

-0.4%

Debt to banks, mn USD

233

33

13

14

34

28

12

3

4

793

611

446

403

455

598

664

662

659

1,026

644

458

418

489

626

675

666

664

12/31/'09

12/31/'10

12/31/'11

12/31/'12

12/31/'13

12/31/'14

12/31/'15

12/31/'16

3/31/'17

Letters of credit

Debt to banks

-0.3%

Bank indebtedness, mn USD

Debt structure: USD 51% EUR 48% Other 1%

GPN Loan -4% 291 mn EUR

Comparative analysis

24

EBITDA margin(%) 2. EBITDA/FTE* (thous. USD) 4. Daily turnover (t/day) 3.&6.

30.4

22.1

17.0

17.0

14.2

19.9

160.5

82.9

82.3

63.7

30.0

83.9

8.9 7.5

6.6 5.9 5.6 5.3

6.7

Share of light products (%) 5. OPEX ($/boe) 2.

86.8

84.9

78.1

77.7

73.9

80.3 11.9

11.6

5.4

6.3

N/A

1.0 6.4

9.1 *Data for 2016

Wrap up

25

Limited opportunities for getting long-terms loans

Intensified competitors’ activities

Weather conditions in January and February

Growth of financial indicators

Sales volume growth

New model of measures to increase operational efficiency

Disclaimer

This presentation has been prepared by NIS j.s.c. Novi Sad ("Company") and consists of slides containing the information about NIS Group for the purpose of presentation to investors. This presentations does not represent any bid or invitation to bid, or any encouragement for submitting a bid for the sale or purchase or registration of shares or other securities of the Company, and furthermore, this presentation or any part of it or the fact that this presentation is made available or distributed, may not represent a basis for any contract or investment decision and for these purposes it cannot be relied on.

All visitors to this presentation who consider purchase or sale of securities are warned hereby that any purchase or sale should be performed on the basis of the information contained in other publicly available documents which should be used in accordance with the restrictions indicated in these documents. There may be no relying for any purposes whatsoever on the information contained in this presentation or any information given during its presentation, or on its completeness, accuracy or correctness. The information given in this presentation may not be treated as the provision of investment advice or recommendation. All reasonable measures have been taken to ensure the correctness of the facts given in this presentation and the correctness and fairness of considerations therein. This presentation has not been adopted by the Company bodies. Consequently, no statement or guarantee, explicit or implicit, with regard to the accuracy, completeness or correctness of the information or opinions contained or considered in this presentation is not given by or on behalf of the Company or any of its shareholders, directors, representatives, employees or any other person. Neither the Company nor any of its shareholders, directors, representatives, employees or any other persons accept any responsibility for any loss that may occur on the basis or in relation to the use of this presentation or its content or in any other way related to this presentation.

The information in this presentation contains statements on uncertain future events. The Statements on uncertain future events include the statements that are not historical facts, statements related to the intentions of the Company and NIS Group, beliefs and current expectations with regard to, inter alia, the performance results of NIS Group, financial situation and liquidity, prospects, growth, strategies and the areas of industry in which the NIS Group operates. In view of the fact that they refer to the events and depend on the circumstances which may or may not happen in the future, statements on uncertain future events by their nature imply risks and uncertainty, including but not limited to the risks and uncertainties identified by the Company and NIS Group in other publicly available documents. The Company warns that there is no guarantee that the statements on uncertain future events will happen in the future and that the actual performance results, financial situation and liquidity, as well as the development of the area of industry in which the Company and NIS Group operate may significantly differ from those presented or assumed in the statements on uncertain future events contained in this presentation. Additionally, even if the performance results of NIS group, its financial liquidity and liquidity, as well as the development of the area of industry in which the Company and NIS Group operate come to be in accordance with the statements given here on uncertain future events, such results and development are not indicative for the results and development in the coming periods. The information contained in this presentation is given on the date hereof and is subject to changes without notice.

No person has any obligation to update and keep updated the data contained herein.

By visiting this presentation you are considered to be acquiainted with the above mentioned disclaimer.