Presentation On Admission of a Partner PREPARED BY: NAVDEEP KAUR PGT COMMERCE KV 2, PATHANKOT.

30

-

Upload

colleen-cannon -

Category

Documents

-

view

218 -

download

2

Transcript of Presentation On Admission of a Partner PREPARED BY: NAVDEEP KAUR PGT COMMERCE KV 2, PATHANKOT.

PresentationOn

Admission of a Partner

PREPARED BY: NAVDEEP KAUR PGT COMMERCEKV 2, PATHANKOT

ADMISSION OF A PARTNER ADMISSION OF A PARTNER Admission of a partner means reconstitution of the firm because with admission of a partner, the existing agreement comes to an end and a new agreement among all the partners (including incoming or new partner) comes into effect. The capital contribution by the new partner, his share of profits and other conditions are agreed upon. The new partner on joining becomes liable for the liabilities of the firm and entitled to assets and profits of the firm.

Section 31 of the Indian Partnership Act, 1932 provides that a new partner shall not be inducted into a firm without the consent of all the existing partners, unless it is a agreed otherwise by the partners in the Partnership Deed. Thus, a new partner can be admitted into a partnership firm with the consent of all the partners.

Effects of Admission of a PartnerEffects of Admission of a PartnerThe effects of admission of a new partner are:1.The old partnership comes to an end and new partnership comes into existence.2.New or Incoming partner becomes entitled to share future profits of the firm and the combined share of the old partners gets reduced.3.New or Incoming partner contributes an agreed amount of capital to the firm.Adjustments made on the Admission of a Partner1.Change in the profit-sharing ratio.2.Goodwill.3.Adjustment of accumulated profits, reserves and losses.4.Adjustments of capital (if agreed).

CHANGE IN PROFIT-SHARING RATIOCHANGE IN PROFIT-SHARING RATIOThe new or incoming partner is entitled to a share in the future profits of the firm. In effect, there will be a change in the old profit-sharing ratio. Since, the new or incoming partner acquires his share from the old partners, therefore, it becomes necessary to determine the new profit-sharing ratio and also the sacrificing ratio.New Profit-Sharing RatioThe new profit-sharing ratio is the ratio in which all the partners, including the new or incoming partner, share the future profits and losses o the firm.1.In their old profit-sharing ratio; or2.In a particular ratio or the surrendered ratio; or3.In a particular fraction from some of the partners.Let us now discuss each of the above cases in detail.

Case 1: When a new or incoming partner acquires his share from the old or existing partners in their old profit-sharing ratio.In such a situation, the share of the new partner is given and it is assumed that the new partner has acquired his share from the old partners in their old profit-sharing ratio.The old partners, therefore, continue t share the balance profits or losses in their old profit-sharing ratio. In other words, unless otherwise agreed, the profit-sharing ratio among the existing partners remains unchanged. The new profit-sharing ratio among all the partners is determined by deducting the new or incoming partner’s share from 1 and then dividing the balance in old profit-sharing ratio of the old partners.Illustration 1 A and B are partners sharing profits in the ratio of 5 : 3. C is admitted for 1/4th share in the profits.

Case 2: When a new or incoming partner acquires his share from the old or existing partners in a particulars ratio.If new or incoming partner acquires a part of share of profits from one partner and a part of share of profits form another partner. In such a case, the existing partner’s profit-sharing ratio will change to the extent of share sacrificed on admission of the new or incoming partner. The existing partner’s share of profits in the reconstituted firm is determined by deducting the sacrificed made from the existing share of profits.

Illustration: A and B are in partnership sharing profits and losses in the ratio of 5 :3. C is admitted as a partner for 1/5th share which he takes 1/10th from A and 1/10th form B.Calculate the new profit-sharing ratio of the partners.

Sacrificing RatioSacrificing RatioSacrificing Ratio is the ratio in which the told or existing partners forego, i.e., sacrifice their share of profit in favour of the new or incoming partner. Thus, Sacrificing Ratio can be defined as the ratio in which the new partner is given the share by the old partners. This share may be given to the new or incoming partner by all the old partners equally or by all or some of the partners in agreed share. Let us discuss how the sacrificing ratio is determined.1. When share of a new partner is given without giving the details of the sacrifice made by the old partners.2. When the old ratio of the old partners and the new ratio of all the partners if given; and3. When the new or incoming partner acquires his share by surrender of a particular fraction of shares by old partners.

Situation 1: When share of a new or incoming partner is given without giving the details of the sacrifice made by the old or existing partners.In this situation, it is assumed that the old partners make sacrifice in their old profit-sharing ratio. Therefore, the sacrificing ratio is always in the old profit-sharing ratio.Illustration:- (Partners make sacrifice in the old ratio). A and B are partners sharing profits in the ratio of 3:1. C is admitted into partnership for 1/8th of the profits. Calculate the sacrificing ratio and the new ratio.Solution:- Since, C’s share is given without mentioning as to what c acquires from A and B separately, It is assumed that c takes it from the partners in their old-profit sharing ratio. Therefore, the sacrifice made by A and b is in the ratio of 3:1.

Situation 2: When the old ratio of the old or existing partners and the new ratio of all the partners are given.In this situation, sacrificing ratio of the old partners is the difference between old ratio and the new ratio, i.e, it is calculated by deducting the new share from the old share of the old partners.Illustration: (New ratio of all partners are given). A and B are partners sharing profits in the ratio of 3:2. C is admitted into partnership. The new-profit sharing ratio among A.B and c is 5:3:2. Find out the sacrificing ratio.

Situation: When the new or incoming partner acquires the share by surrender of a particular fraction of shares by old partners.In this situation, shares surrendered by the old partners in favour of a incoming partner are added. It is the share of the new partner. The share surrendered by the old partner is deducted from his old share to determine the share of new or incoming partner in the reconstruction firm.Illustration:- (Old partners surrender a particular fraction of their shares in Favour of a new Partner). A and B are partners in a firm sharing profits and losses in the ratio of 5:3. A surrenders 1/20th of his share, whereas b surrenders 1/24th of his share in favour of c, a new partner. Calculate the new profit-sharing ratio and the sacrificing ratio.

Distinction between Sacrificing Ratio and new Distinction between Sacrificing Ratio and new Profit-Sharing RatioProfit-Sharing Ratio

Basis Sacrificing Ratio New Profit-Sharing Ratio

1. Meaning It is the ratio in which the old partners agree to sacrifice their shares in profits in favour of a new partner.

It is the ratio in which all partners including the incoming partner share the future profits and losses.

2. Related Partners It is related to the old partners only. It is related to all partners including the new partner

3. Calculation Sacrificing Ratio=Old Ratio-New Ratio

TREATMENT OF GOODWILLTREATMENT OF GOODWILLAS-26 prescribes that goodwill be recorded in the books only when consideration in money or money’s worth has been paid for it, i.e., goodwill is purchased. Thus in case of admission or retirement/death of a partner or in case of change in the profit-sharing ratio among partners, goodwill, should not be raised in the books of the firm because no consideration in money or money’s worth is paid for it. If any partner brings any premium over and above his capital contribution at the time of his admission, such premium should be distributed among the existing partners in their sacrificing ratios.If goodwill is evaluated at the time of change in the constitution of the firm (by way of admission/retirement/death/change in profit-sharing ratio), the goodwill should not be brought in books since it is inherent goodwill. The value of goodwill should be adjusted through partners capital accounts.

1. Goodwill (premium for goodwill) paid privately: when goodwill premium is paid privately (i.e.. Outside the business) by the new or incoming partner to the old partners, no entry is recorded in the banks of accounts.

2. Goodwill/Premium for goodwill brought in cash by the new or incoming partner and retained in the business: when the new partner brings cash for his share of goodwill, it is transferred to the capital accounts of the sacrificing partners. In other words, the amount of goodwill brought in by the partner is shared by the sacrificing partners in their sacrificing ratio.

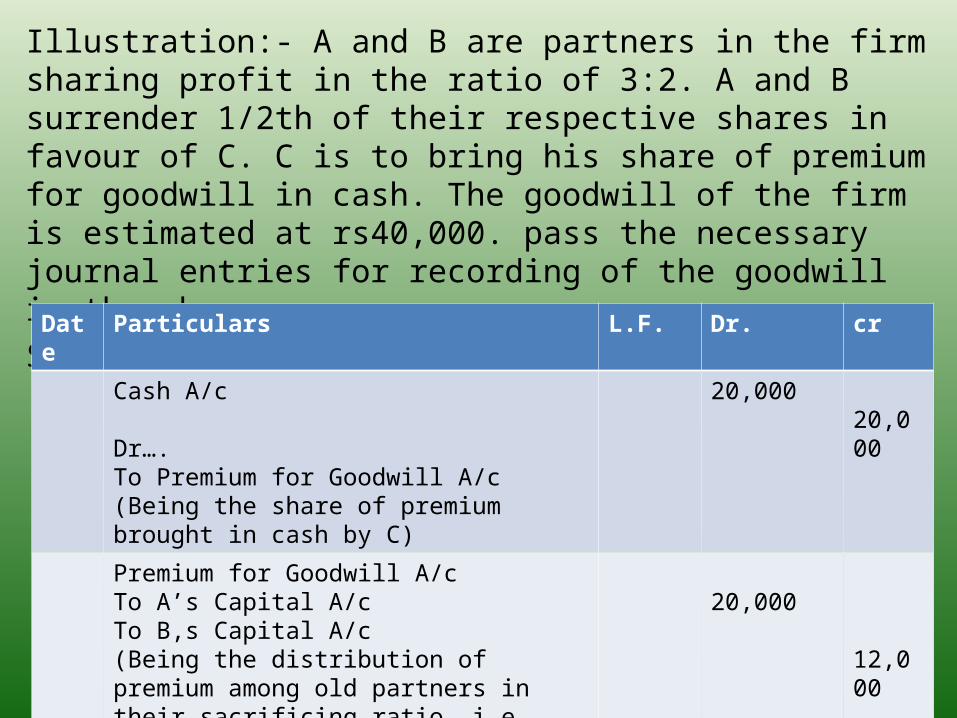

Illustration:- A and B are partners in the firm sharing profit in the ratio of 3:2. A and B surrender 1/2th of their respective shares in favour of C. C is to bring his share of premium for goodwill in cash. The goodwill of the firm is estimated at rs40,000. pass the necessary journal entries for recording of the goodwill in the above case.Solution:- JOURNAL

Date Particulars L.F. Dr. cr

Cash A/c Dr….To Premium for Goodwill A/c(Being the share of premium brought in cash by C)

20,00020,000

Premium for Goodwill A/cTo A’s Capital A/cTo B,s Capital A/c(Being the distribution of premium among old partners in their sacrificing ratio, i.e., 3:2) (Note)

20,000

12,000 8,000

3. Premium for Goodwill (Goodwill) brought in Kind: New or incoming partner may bring his share of premium for goodwill in the form of assets. In this situation, the value of assets brought in is debited and premium for goodwill or goodwill account is credited for his share of goodwill besides crediting the new partner’s capital account for his capital. Thereafter, premium (Share of Goodwill) is transferred to the capital accounts of the sacrificing partners in their sacrificing ratio.Accounting EntriesFor assets brought in by the new partner:Assets A/c

To New partner’s capitalTo Premium for Goodwill A/c

For giving credit of goodwill to sacrificing partners in their sacrificing ratio:

PREMIUM FOR GOODWILL A/CPREMIUM FOR GOODWILL A/C

To Sacrificing Partner’s Capital A/csTo Sacrificing Partner’s Capital A/cs

Illustration:- (Premium brought in Kind). X and Y are partners in a firm sharing profits in the ratio of 3:2. on 1st April, 2012, they admit Z as a new partner for 3/13th share in the profits. The new ratio will be 5:5:3. Z contributed the following assets to his capital and his share for goodwill: stock rs80,000. debtors rs1,20,000; Land rs2,00,000; Plant and Machinery rs1,20,000. on the date of admission of Z, goodwill of firm was valued at rs10,00,000. record the necessary journal entries in the books of the firm on Z’s admission.

SolutionSolution

Date Particulars L.F. Dr. Cr.

2012April Stock A/c …..Dr

Debtors A/c …..Dr.Land A/c …..Dr.Plant and Machinery A/c …..Dr. To Z,s Capital A/c To Premium for Goodwill A/c (WN 1)(Being the assets contributed by Z on his admission as his capital and his share of goodwill premium)

80,0001,20,0002,00,0001,20,000

2,80,0002,40,000

Premium for Goodwill A/c ……Dr.. To X’s capital A/c To Y’s capital A/c(Being the goodwill premium transferred to the capital accounts of X and Y on Z’s admission in their sacrificing ratio) (WN 2)

2,40,0002,24,000 16,000

4. Goodwill/Premium for goodwill is brought by the New or Incoming Partner and is withdrawn by the old partners fully or partly: The premium brought by the new or incoming partner is shared by the old partners in the sacrificing ratio. The sacrificing partners may withdraw the premium amount fully or partly.Accounting entriesFor premium for goodwill brought in cash by the partner:Cash/Bank A/c Dr. Amount of premiumTo premium for goodwill A/cFor sharing of premium for goodwillPremium for goodwill A/c Dr. Amount of premium

For withdrawal of premium money fully/partly Dr. Amount withdrawalSacrificing partner’s capital A/cs

5. When only a part of the Goodwill/ Premium for Goodwill is brought by a New or Incoming partner in cash: The new or incoming partner may not be able to bring the full amount of his share of goodwill/premium for goodwill in cash, i.e. brings only a part in cash. In this case, the premium for goodwill account is credited for the amount of premium brought by him. At the time of recording the transfer entry, the new or incoming partner’s Capital Account is debited with his unpaid share of premium besides debiting the premium for goodwill account with the amount of premium brought by him.Illustration 25 And B are partners sharing profits and losses in the ratio of 3:2. they admit C into the firm for 1/4th share in profits which he takes 1/6th from A and 1/12th from B. C brings Rs. 18,000 as goodwill out of his share of Rs. 30,000.No Goodwill Account appears in the books of the firm.

SolutionSolution

Date

Particulars L.F. Dr. (Rs.) Cr. (Rs.)

Cash A/c …..DrTo premium for goodwill A/c(Being the amount brought in by C as his share of goodwill

18,00018,000

Premium for Goodwill A/c ……Dr.. C’s Capital A/c (Rs.30,000-Rs.18000) …….Dr. To A’s capital A/c To B’s capital A/c(Being the goodwill credited to the sacrificing partners in their sacrificing ratio, i.e., 2:1)

18,00012,000 20,000

10,000

3.Revaluation of assets and reassessment of 3.Revaluation of assets and reassessment of liabilitiesliabilities

The value of assets may be different from its book value because with the time, value of some assets increases while of some decreases. In the case of liabilities, It is possible that the amount payable is different from the value recorded in the books. It is also possible that some assets or liabilities are not recorded in the books. The value of assets and the liabilities payable need to be brought to their correct value so that the incoming partner is not put to an advantage or a disadvantage. For this purpose, a Revaluation Account or Profit and Loss Adjustment Account is opened in the books of the firm. The value of assets and liabilities nor recorded in the books is accounted through the Revaluation Account. The profits' losses arising there from are adjusted in the Old Partners’ Capital Accounts in their old profit-sharing ratio.

When the assets and liabilities Appear in the Books at the New ValuesThe adjustments in the value of assets and liabilities are effected through an account called Revaluation Account or Profit and Loss Adjustments account. It is debited by decrease in the value of assets and increase in the amount of liabilities and credited by the increase in the value of assets of decrease in the amount of liabilities.

Accounting EntriesAccounting Entries

1. For an increase in the value of assets Assets A/c (Individually) …Dr.To Revaluation (or Profit and Loss Adjustment) A/c

2. For a decrease in the value of assets Revaluation (or Profit and Loss Adjustment) A/c ...…Dr.To assets A/c (Individually)

3. For an increase in the amount of liabilities Revaluation (or Profit and Loss Adjustment) A/c ………Dr.To Liabilities A/c (Individually)

4. For a decrease in the amount of liabilities Liabilities A/c (Individually) …….Dr.To Revaluation (or Profit and Loss Adjustment) A/c

5. For accounting unrecorded assets Assets A/c (Individually) ……..Dr.To Revaluation (or Profit and Loss Adjustment) A/c

6. For accounting unrecorded liabilities Revaluation (or Profit and Loss Adjustment) A/c …….Dr.To Liabilities A/c (Individually)

Reserves and Accumulated (Undistributed) Reserves and Accumulated (Undistributed) Profit/LossesProfit/LossesIf, before the admission of a new partner, there is balance in a Reserve Fund and accumulated profit/losses in the Balance Sheet, they are transferred to the Old Partners’ Capital Accounts in their old ratio. They are transferred the Old Partners’ Capital Accounts because they had been set aside out of the profits in the earlier periods, i.e., before the new partner was admitted.Thus the Journey will be:

Profit and Loss A/c ……Dr.Reserve Fund or General Reserve ……Dr.Workmen’s Compensation Reserve ..Dr.{Excess of Reserve over Actual Liability}Investments Fluctuation Reserve ……Dr. {Excess of Reserve over the difference

between Book Value and Market Value}

[In old ratio]To Old Partners’ Capital A/cs

Adjustment of CapitalAdjustment of CapitalIt may be decided on the admission of a new partner that either the new partner will contribute as capital an amount in proportion to his share of profit or that the capitals of other partners will be adjusted to make them proportionate to their respective shares of profit. So, we shall discuss adjustment of capital as under”1.Adjustment of old partners’ capitals on the basis of incoming partners’ capital or2.Calculating the capital of incoming partner on the basis of the old partners’ capitals.1. Adjustment of the Old Partners’ Capital Accounts on the Basis of the Incoming Partners’ Capital: For this, we take the following steps:Step2. Determine the new capital of each partner. Total capital is divided in their new profit-sharing ratio.

Step3: Ascertain the present capital of the old partners (after all adjustment).Step4: Find out the surplus capital/deficit capital by comparing the proportionate capital (ascertained by step 2) and the present capital (ascertained in Step 3).

Surplus= Present capital > Proportionate Capital (New capital) Deficit= Present capital< Proportionate Capital (New capital)

Step5: Pass the necessary Journal entry for adjusting the above surplus/deficit.

Journal EntryJournal Entry(i) In case the present capital in less than the New Capital:Cash A/c or Concerned partner’s current A/c ..Dr.To Concerned Partner’s capital A/c(ii) In case the present capital is more than the new Capital:Concerned Partner’s Capital A/c ..Dr.To Cash A/c or concerned Partner’s Current A/cIllustration 52: X and Y are partners in a firm sharing profits in the ratio of 3:2. The remaining capitals of X and Y after adjustment are Rs. 80,000 and Rs. 60,000 respectively. They admit Z as a partner on his contribution of Rs. 35,000 as capital for 1/5th share of profits to be acquired equally from both X and Y.

Solution:Solution:(i) Calculation of New PROFIT-SHARING Ratio:

(a) Their Existing Shares X Y(b) Share transferred to Z 3/5 2/5(c) Their New Share (a-b) 1/10 1/10(d) New Profit-Sharing ratio of X, Y and

Z=5/10 :3/10:1/5= 5: 3: 2.(ii) Calculation of Total capital of the Reconstituted Firm:Total capital of the firm = Capital of the new partner x Reciprocal of share of profit of the partner Total capital = Rs. 35,000x5/1=Rs. 1,75,000.(iii) Calculation of New Capitals of All Partners:

X Y ZNew capitals (Rs.1,75,000 in ratio of 5:3:2) Rs. 57,500, Rs.52,500, Rs.35,000

(iv) Calculation of Actual Cash to be Paid off/Brought in by Old Partners:

X (Rs.) Y (Rs.)(a)New Capitals 87,500 52,500(b)Existing Capitals 80,000 60,000(c)Cash to be paid (to be brought in) 7,500 7,500