Presentation North American Natural Gas Production … ihs.com IHS Production ... Production Outlook...

28

© 2015 IHS Presentation ihs.com IHS Production Outlook by Major Basin, and Facilities Options, Edward Kelly, IHS Inc. North American Natural Gas February 2015 ENERGY Ed Kelly, Managing Director, + 1 713 209 4524, [email protected]

-

Upload

phunghuong -

Category

Documents

-

view

223 -

download

1

Transcript of Presentation North American Natural Gas Production … ihs.com IHS Production ... Production Outlook...

© 2015 IHS

Presentation

ihs.com

IHS

Production Outlook by Major Basin, and Facilities Options, Edward Kelly, IHS Inc.

North American Natural Gas

February 2015

ENERGY

Ed Kelly, Managing Director, + 1 713 209 4524, [email protected]

Contents

© 2015 IHS

OUTLINE

THE RESOURCE BASE AND COST STRUCTUREThe Marcellus/Utica, and All Else

A PLAY BY PLAY TOUR of GAS PRODUCTION POTENTIALMarcellusUticaHaynesville

COMMENTS

© 2015 IHS

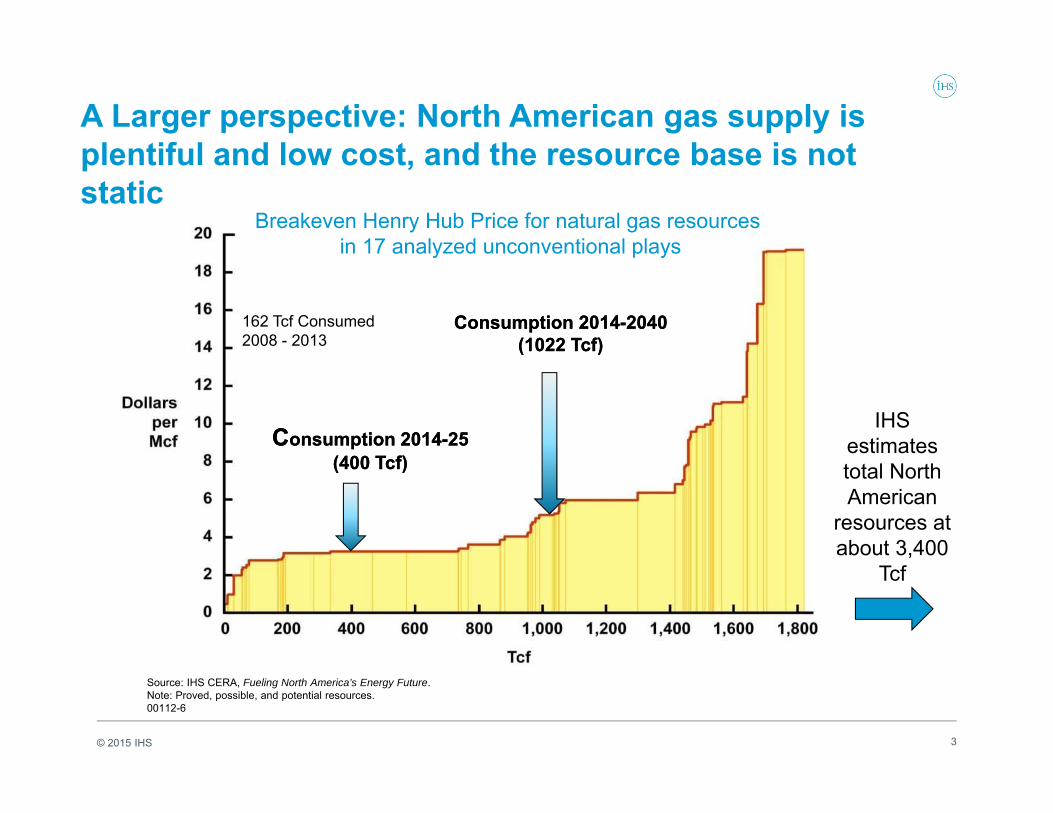

A Larger perspective: North American gas supply is plentiful and low cost, and the resource base is not static

3

Source: IHS CERA, Fueling North America’s Energy Future.Note: Proved, possible, and potential resources.00112-6

Consumption 2014-2040(1022 Tcf)

Consumption 2014-2040(1022 Tcf)

Breakeven Henry Hub Price for natural gas resources in 17 analyzed unconventional plays

IHS estimates total North American

resources at about 3,400

Tcf

Consumption 2014-25(400 Tcf)

Consumption 2014-25(400 Tcf)

162 Tcf Consumed 2008 - 2013

© 2015 IHS 4

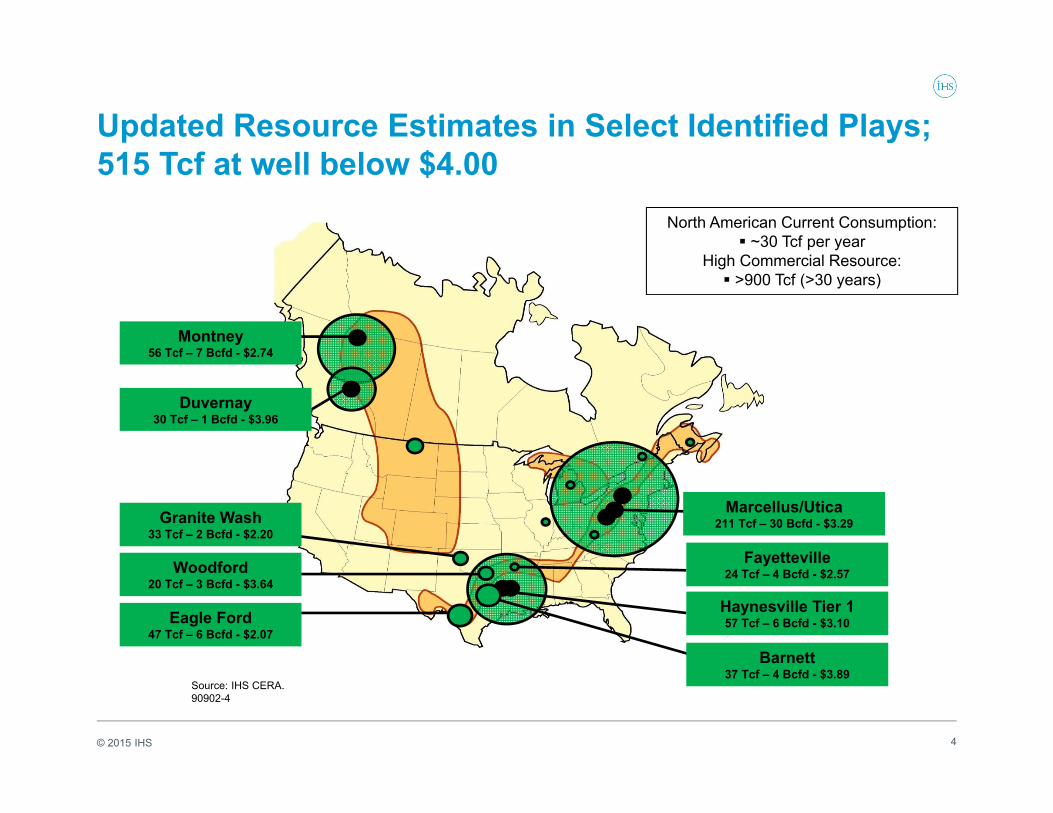

Updated Resource Estimates in Select Identified Plays; 515 Tcf at well below $4.00

Source: IHS CERA.90902-4

Haynesville Tier 157 Tcf – 6 Bcfd - $3.10

Woodford20 Tcf – 3 Bcfd - $3.64

Duvernay30 Tcf – 1 Bcfd - $3.96

Montney56 Tcf – 7 Bcfd - $2.74

Marcellus/Utica211 Tcf – 30 Bcfd - $3.29

Fayetteville24 Tcf – 4 Bcfd - $2.57

Barnett37 Tcf – 4 Bcfd - $3.89

North American Current Consumption: ~30 Tcf per year

High Commercial Resource: >900 Tcf (>30 years)

Eagle Ford47 Tcf – 6 Bcfd - $2.07

Granite Wash33 Tcf – 2 Bcfd - $2.20

© 2015 IHS

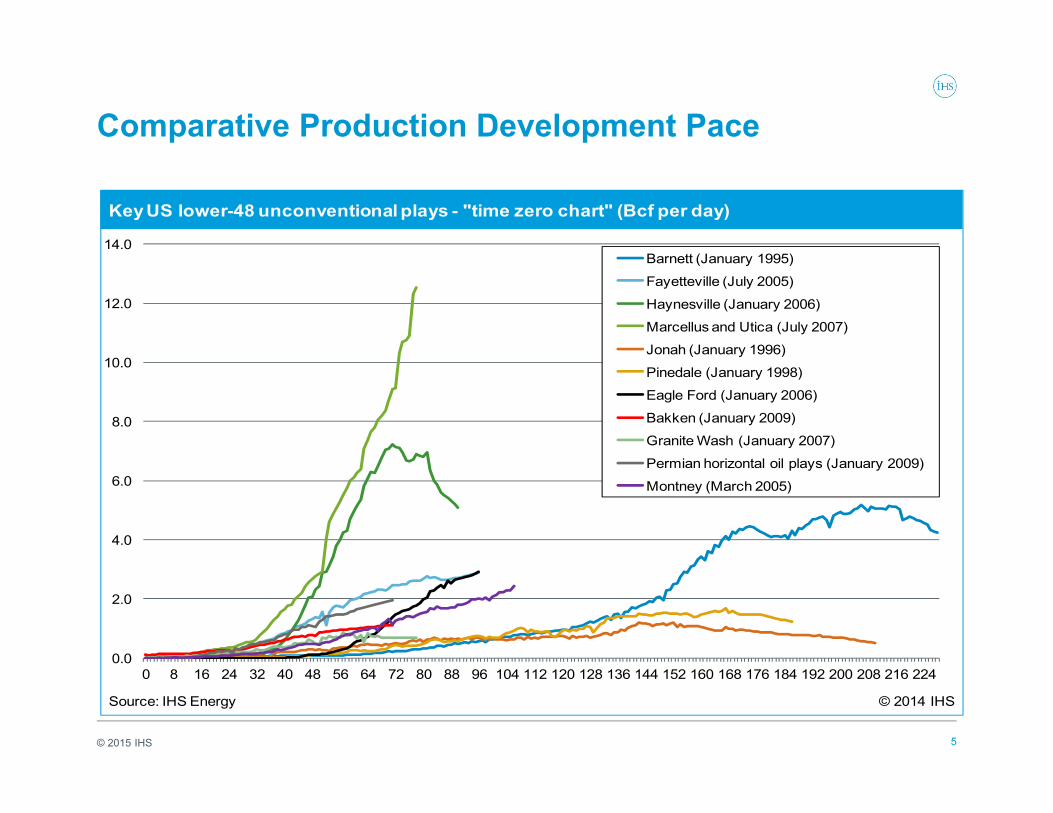

Comparative Production Development Pace

5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0 8 16 24 32 40 48 56 64 72 80 88 96 104 112 120 128 136 144 152 160 168 176 184 192 200 208 216 224

Barnett (January 1995)Fayetteville (July 2005)

Haynesville (January 2006)Marcellus and Utica (July 2007)Jonah (January 1996)Pinedale (January 1998)Eagle Ford (January 2006)Bakken (January 2009)Granite Wash (January 2007)Permian horizontal oil plays (January 2009)

Montney (March 2005)

Key US lower-48 unconventional plays - "time zero chart" (Bcf per day)

Source: IHS Energy © 2014 IHS

© 2015 IHS

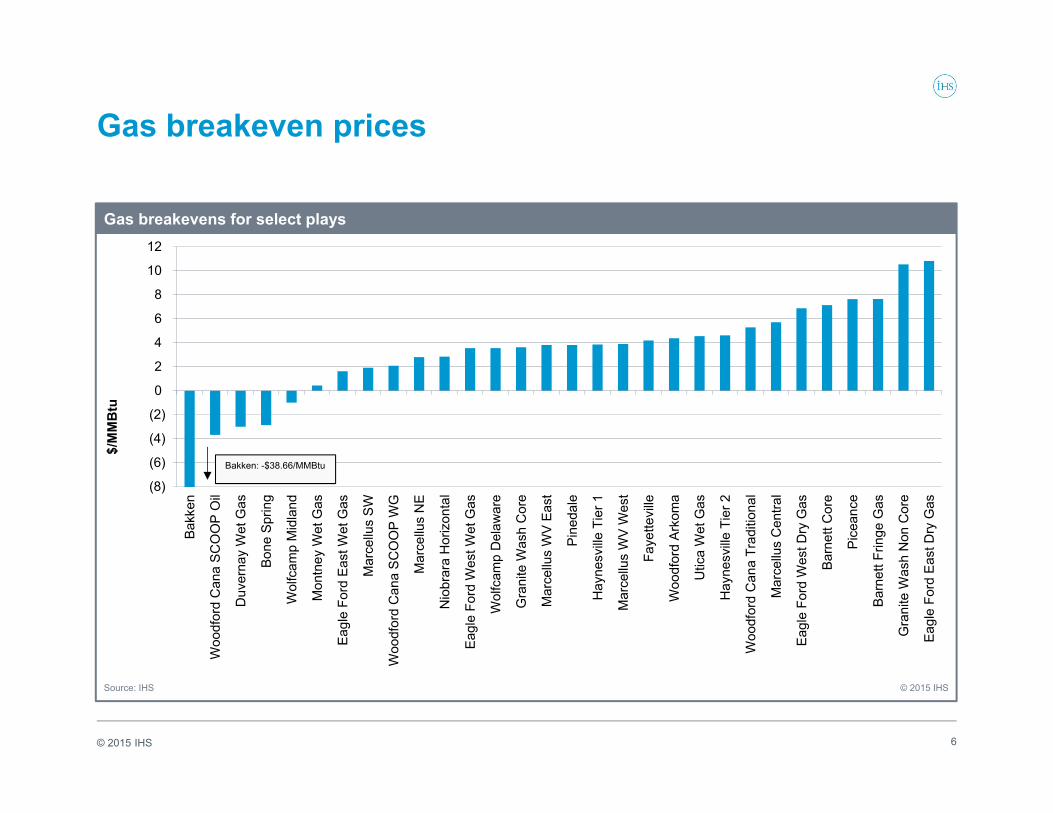

Gas breakeven prices

6

(8)

(6)

(4)

(2)

0

2

4

6

8

10

12

Bakk

en

Woo

dfor

d C

ana

SCO

OP

Oil

Duv

erna

y W

et G

as

Bone

Spr

ing

Wol

fcam

p M

idla

nd

Mon

tney

Wet

Gas

Eagl

e Fo

rd E

ast W

et G

as

Mar

cellu

s SW

Woo

dfor

d C

ana

SCO

OP

WG

Mar

cellu

s N

E

Nio

brar

a H

oriz

onta

l

Eagl

e Fo

rd W

est W

et G

as

Wol

fcam

p D

elaw

are

Gra

nite

Was

h C

ore

Mar

cellu

s W

V Ea

st

Pine

dale

Hay

nesv

ille T

ier 1

Mar

cellu

s W

V W

est

Faye

ttevi

lle

Woo

dfor

d Ar

kom

a

Utic

a W

et G

as

Hay

nesv

ille T

ier 2

Woo

dfor

d C

ana

Trad

ition

al

Mar

cellu

s C

entra

l

Eagl

e Fo

rd W

est D

ry G

as

Barn

ett C

ore

Pice

ance

Barn

ett F

ringe

Gas

Gra

nite

Was

h N

on C

ore

Eagl

e Fo

rd E

ast D

ry G

as

Gas breakevens for select plays

Source: IHS © 2015 IHS

$/M

MB

tu

Bakken: -$38.66/MMBtu

© 2015 IHS

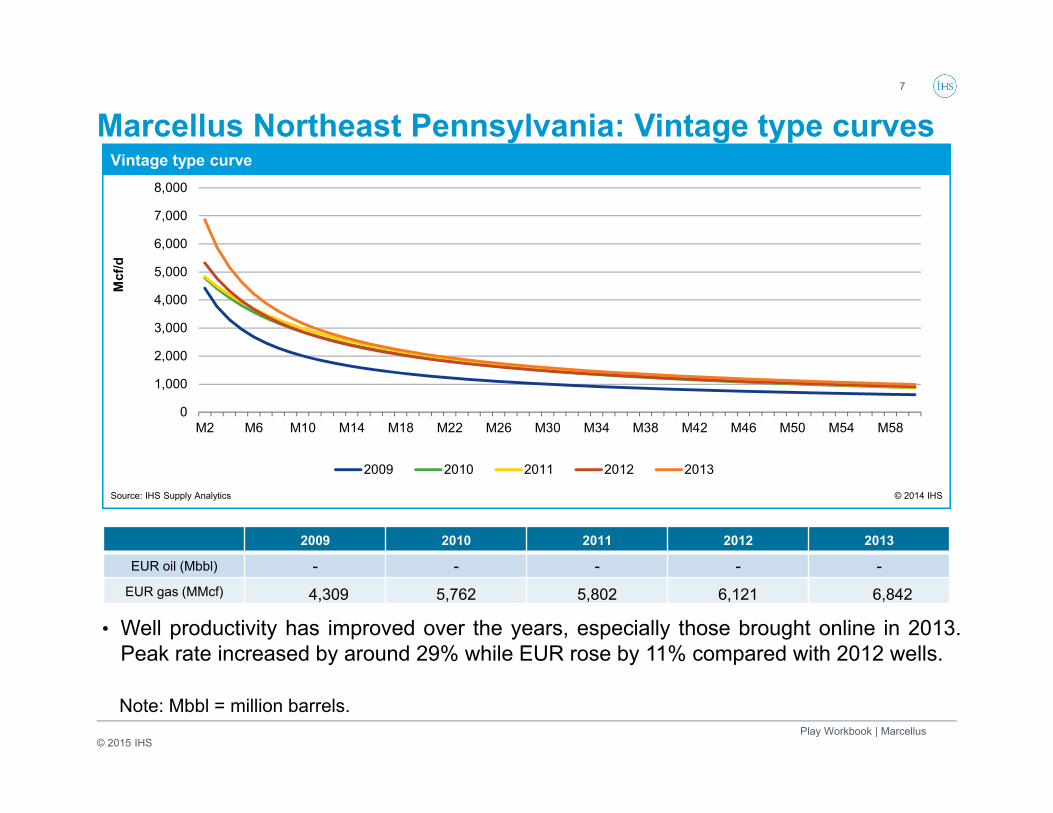

Marcellus Northeast Pennsylvania: Vintage type curves7

• Well productivity has improved over the years, especially those brought online in 2013.Peak rate increased by around 29% while EUR rose by 11% compared with 2012 wells.

2009 2010 2011 2012 2013

EUR oil (Mbbl) - - - - -EUR gas (MMcf) 4,309 5,762 5,802 6,121 6,842

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

M2 M6 M10 M14 M18 M22 M26 M30 M34 M38 M42 M46 M50 M54 M58

2009 2010 2011 2012 2013

Vintage type curve

Source: IHS Supply Analytics © 2014 IHS

Mcf

/d

Note: Mbbl = million barrels.Play Workbook | Marcellus

© 2015 IHS

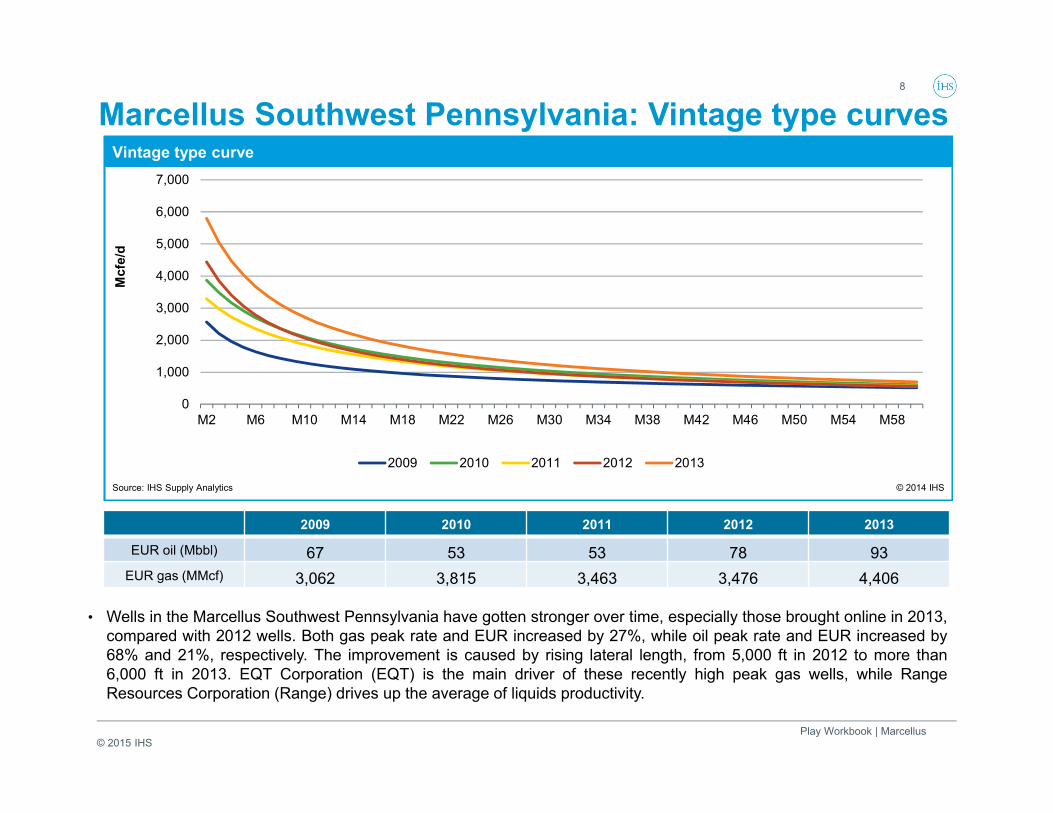

Marcellus Southwest Pennsylvania: Vintage type curves8

• Wells in the Marcellus Southwest Pennsylvania have gotten stronger over time, especially those brought online in 2013,compared with 2012 wells. Both gas peak rate and EUR increased by 27%, while oil peak rate and EUR increased by68% and 21%, respectively. The improvement is caused by rising lateral length, from 5,000 ft in 2012 to more than6,000 ft in 2013. EQT Corporation (EQT) is the main driver of these recently high peak gas wells, while RangeResources Corporation (Range) drives up the average of liquids productivity.

2009 2010 2011 2012 2013

EUR oil (Mbbl) 67 53 53 78 93EUR gas (MMcf) 3,062 3,815 3,463 3,476 4,406

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

M2 M6 M10 M14 M18 M22 M26 M30 M34 M38 M42 M46 M50 M54 M58

2009 2010 2011 2012 2013

Vintage type curve

Source: IHS Supply Analytics © 2014 IHS

Mcf

e/d

Play Workbook | Marcellus

© 2015 IHS

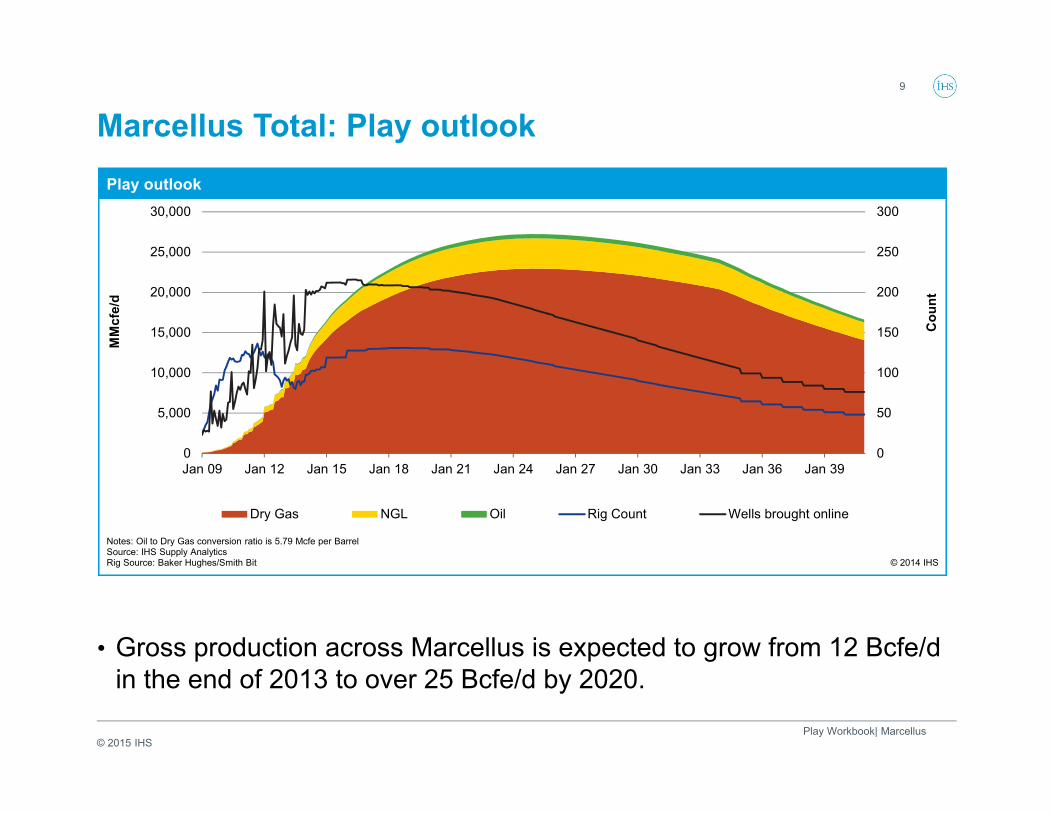

Marcellus Total: Play outlook9

• Gross production across Marcellus is expected to grow from 12 Bcfe/d in the end of 2013 to over 25 Bcfe/d by 2020.

Play Workbook| Marcellus

0

50

100

150

200

250

300

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan 09 Jan 12 Jan 15 Jan 18 Jan 21 Jan 24 Jan 27 Jan 30 Jan 33 Jan 36 Jan 39

Dry Gas NGL Oil Rig Count Wells brought online

Play outlook

Notes: Oil to Dry Gas conversion ratio is 5.79 Mcfe per BarrelSource: IHS Supply AnalyticsRig Source: Baker Hughes/Smith Bit © 2014 IHS

MM

cfe/

d

Cou

nt

© 2015 IHS 10

Play Workbook | Utica

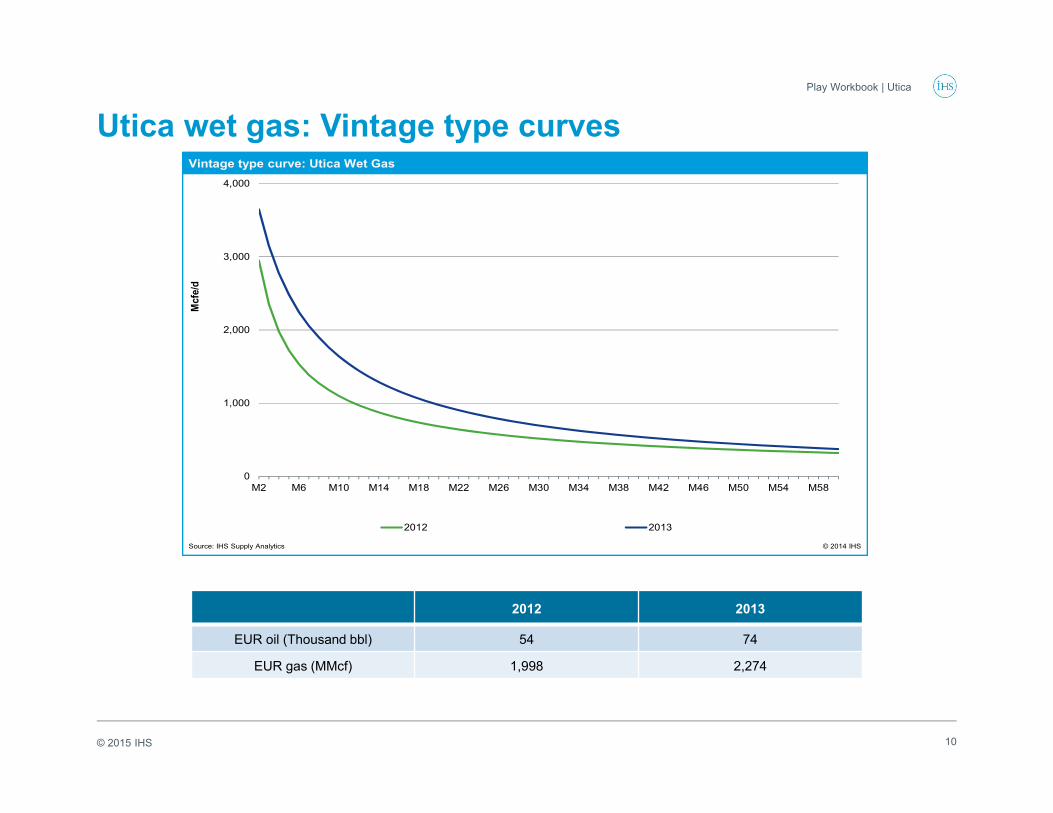

Utica wet gas: Vintage type curves

2012 2013

EUR oil (Thousand bbl) 54 74

EUR gas (MMcf) 1,998 2,274

0

1,000

2,000

3,000

4,000

M2 M6 M10 M14 M18 M22 M26 M30 M34 M38 M42 M46 M50 M54 M58

2012 2013

Vintage type curve: Utica Wet Gas

Source: IHS Supply Analytics © 2014 IHS

Mcf

e/d

© 2015 IHS 11

Play Workbook | Utica

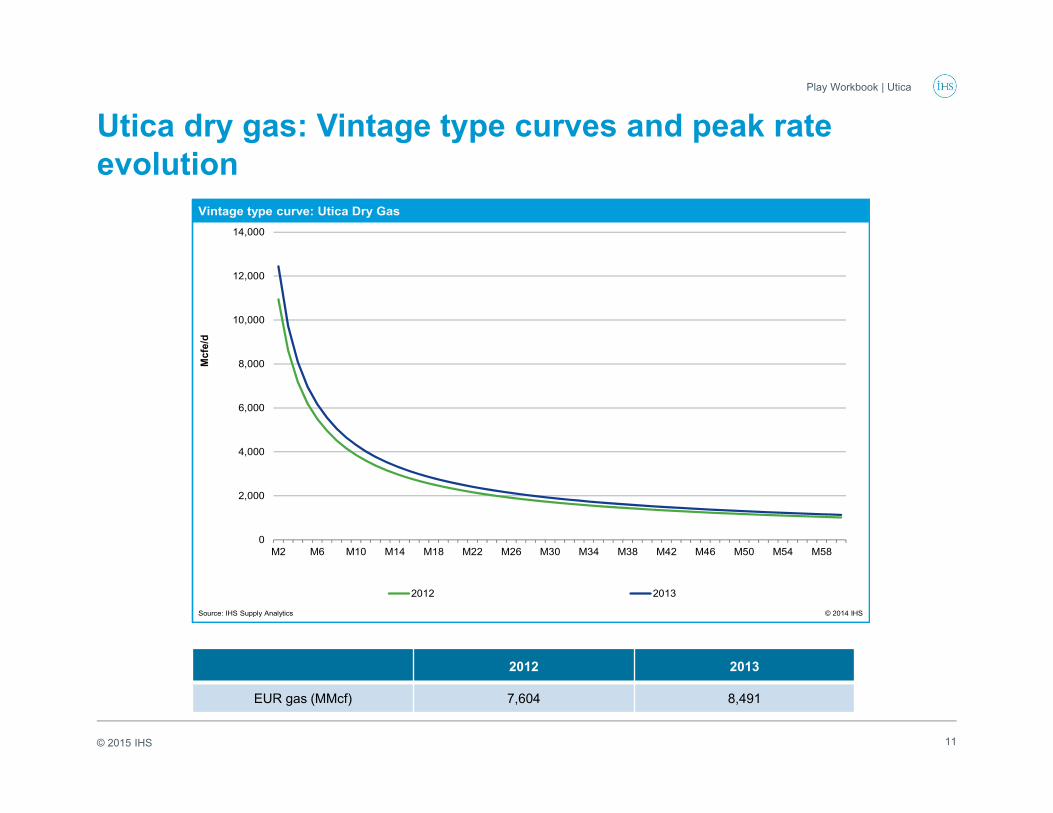

Utica dry gas: Vintage type curves and peak rate evolution

2012 2013

EUR gas (MMcf) 7,604 8,491

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

M2 M6 M10 M14 M18 M22 M26 M30 M34 M38 M42 M46 M50 M54 M58

2012 2013

Vintage type curve: Utica Dry Gas

Source: IHS Supply Analytics © 2014 IHS

Mcf

e/d

© 2015 IHS 12

Play Workbook | Utica

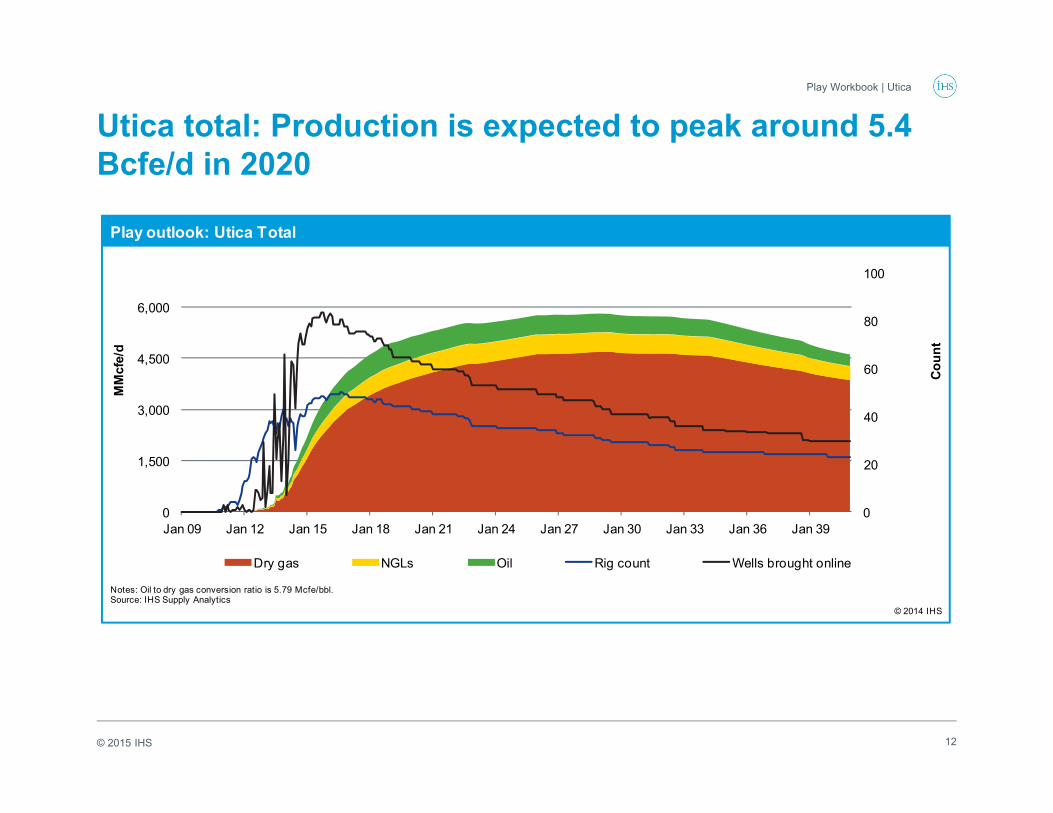

Utica total: Production is expected to peak around 5.4 Bcfe/d in 2020

0

20

40

60

80

100

0

1,500

3,000

4,500

6,000

Jan 09 Jan 12 Jan 15 Jan 18 Jan 21 Jan 24 Jan 27 Jan 30 Jan 33 Jan 36 Jan 39

Dry gas NGLs Oil Rig count Wells brought online

Play outlook: Utica Total

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe/bbl.Source: IHS Supply Analytics

© 2014 IHS

MM

cfe/

d

Coun

t

© 2015 IHS

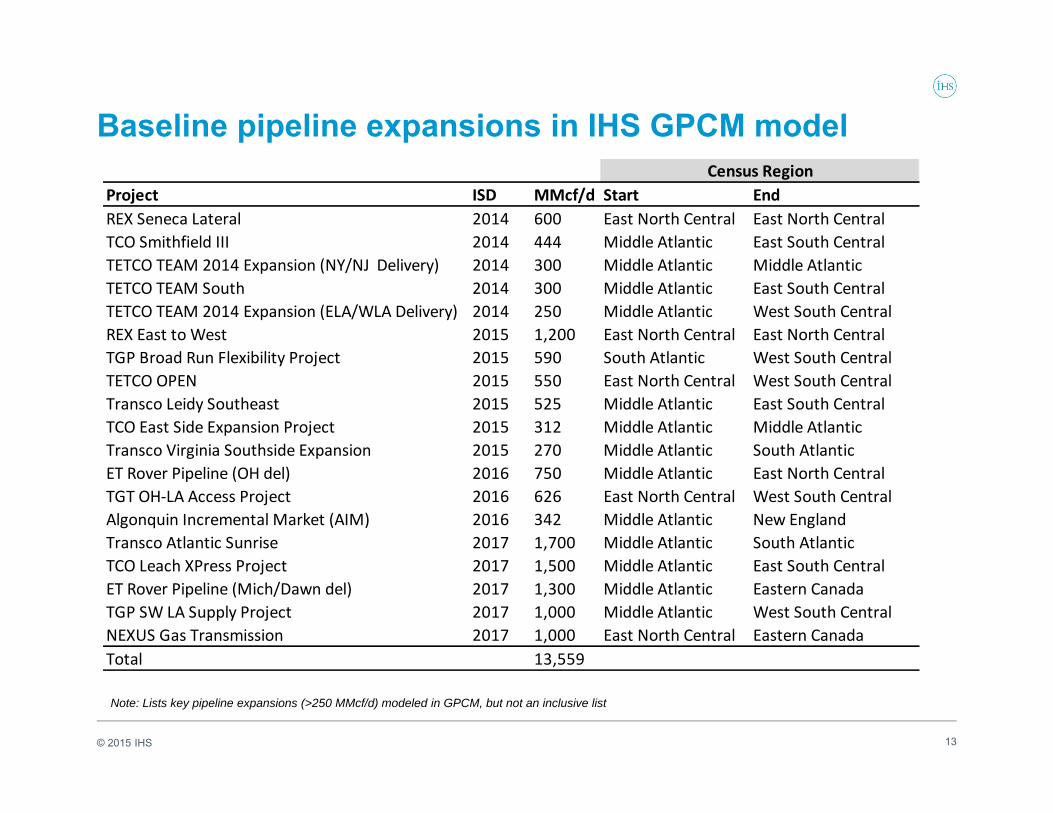

Baseline pipeline expansions in IHS GPCM model

13

Note: Lists key pipeline expansions (>250 MMcf/d) modeled in GPCM, but not an inclusive list

Census RegionProject ISD MMcf/d Start EndREX Seneca Lateral 2014 600 East North Central East North CentralTCO Smithfield III 2014 444 Middle Atlantic East South CentralTETCO TEAM 2014 Expansion (NY/NJ Delivery) 2014 300 Middle Atlantic Middle AtlanticTETCO TEAM South 2014 300 Middle Atlantic East South CentralTETCO TEAM 2014 Expansion (ELA/WLA Delivery) 2014 250 Middle Atlantic West South CentralREX East to West 2015 1,200 East North Central East North CentralTGP Broad Run Flexibility Project 2015 590 South Atlantic West South CentralTETCO OPEN 2015 550 East North Central West South CentralTransco Leidy Southeast 2015 525 Middle Atlantic East South CentralTCO East Side Expansion Project 2015 312 Middle Atlantic Middle AtlanticTransco Virginia Southside Expansion 2015 270 Middle Atlantic South AtlanticET Rover Pipeline (OH del) 2016 750 Middle Atlantic East North CentralTGT OH‐LA Access Project 2016 626 East North Central West South CentralAlgonquin Incremental Market (AIM) 2016 342 Middle Atlantic New EnglandTransco Atlantic Sunrise 2017 1,700 Middle Atlantic South AtlanticTCO Leach XPress Project 2017 1,500 Middle Atlantic East South CentralET Rover Pipeline (Mich/Dawn del) 2017 1,300 Middle Atlantic Eastern CanadaTGP SW LA Supply Project 2017 1,000 Middle Atlantic West South CentralNEXUS Gas Transmission 2017 1,000 East North Central Eastern CanadaTotal 13,559

© 2015 IHS

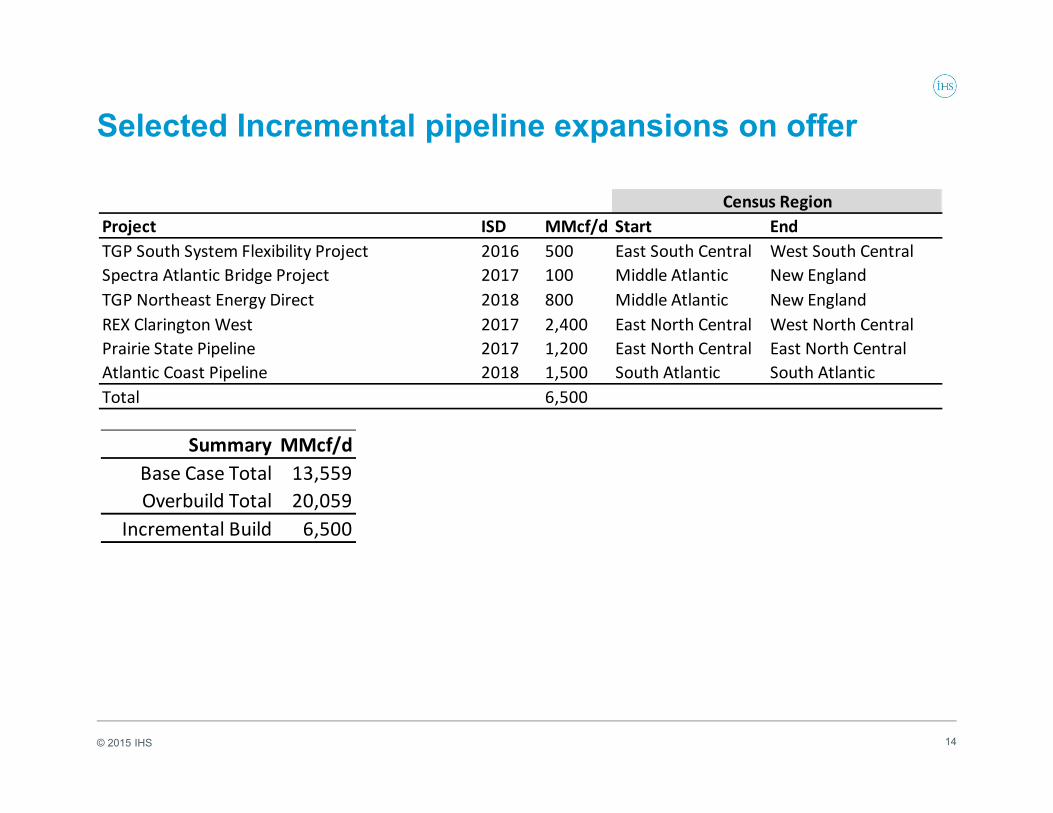

Selected Incremental pipeline expansions on offer

14

Census RegionProject ISD MMcf/d Start EndTGP South System Flexibility Project 2016 500 East South Central West South CentralSpectra Atlantic Bridge Project 2017 100 Middle Atlantic New EnglandTGP Northeast Energy Direct 2018 800 Middle Atlantic New EnglandREX Clarington West 2017 2,400 East North Central West North CentralPrairie State Pipeline 2017 1,200 East North Central East North CentralAtlantic Coast Pipeline 2018 1,500 South Atlantic South AtlanticTotal 6,500

Summary MMcf/dBase Case Total 13,559Overbuild Total 20,059

Incremental Build 6,500

© 2015 IHS

Vintage type well decline curves

15

2009 2010 2011 2012 2013 2014

Max rate: Gas (Mcf/d) 10,353 9,846 9,123 8,758 9,468 10,247

EUR gas (MMcf) 4,920 5,857 6,016 5,735 6,504 6,642Source: IHS © 2015 IHS

Haynesville / February 2015

• Selected operators initiated a practice of choking back wells in 2010, which resulted in lower starting rates but shallower initial declines.

Note: EUR = estimated ultimate recovery.

0

2,000

4,000

6,000

8,000

10,000

12,000

M2 M5 M8 M11 M14 M17 M20 M23 M26 M29 M32 M35 M38 M41 M44 M47 M50 M53 M56 M59

2009 2010 2011 2012 2013 2014

Vintage type curves: Haynesville Tier 1

Notes: 2014 curves made with data till May 2014.Source: IHS © 2015 IHS

Mcf

/d

© 2015 IHS

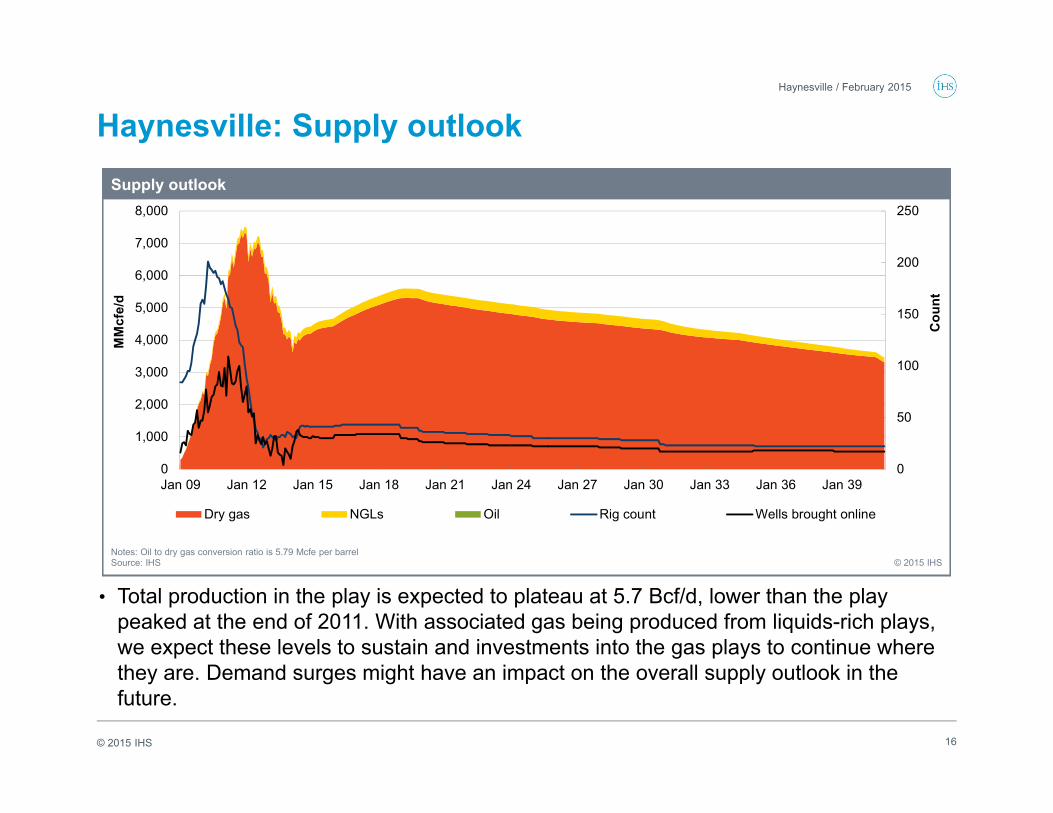

Haynesville: Supply outlook

• Total production in the play is expected to plateau at 5.7 Bcf/d, lower than the play peaked at the end of 2011. With associated gas being produced from liquids-rich plays, we expect these levels to sustain and investments into the gas plays to continue where they are. Demand surges might have an impact on the overall supply outlook in the future.

16

Haynesville / February 2015

0

50

100

150

200

250

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Jan 09 Jan 12 Jan 15 Jan 18 Jan 21 Jan 24 Jan 27 Jan 30 Jan 33 Jan 36 Jan 39

Dry gas NGLs Oil Rig count Wells brought online

Supply outlook

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe per barrelSource: IHS © 2015 IHS

MM

cfe/

d

Cou

nt

© 2015 IHS

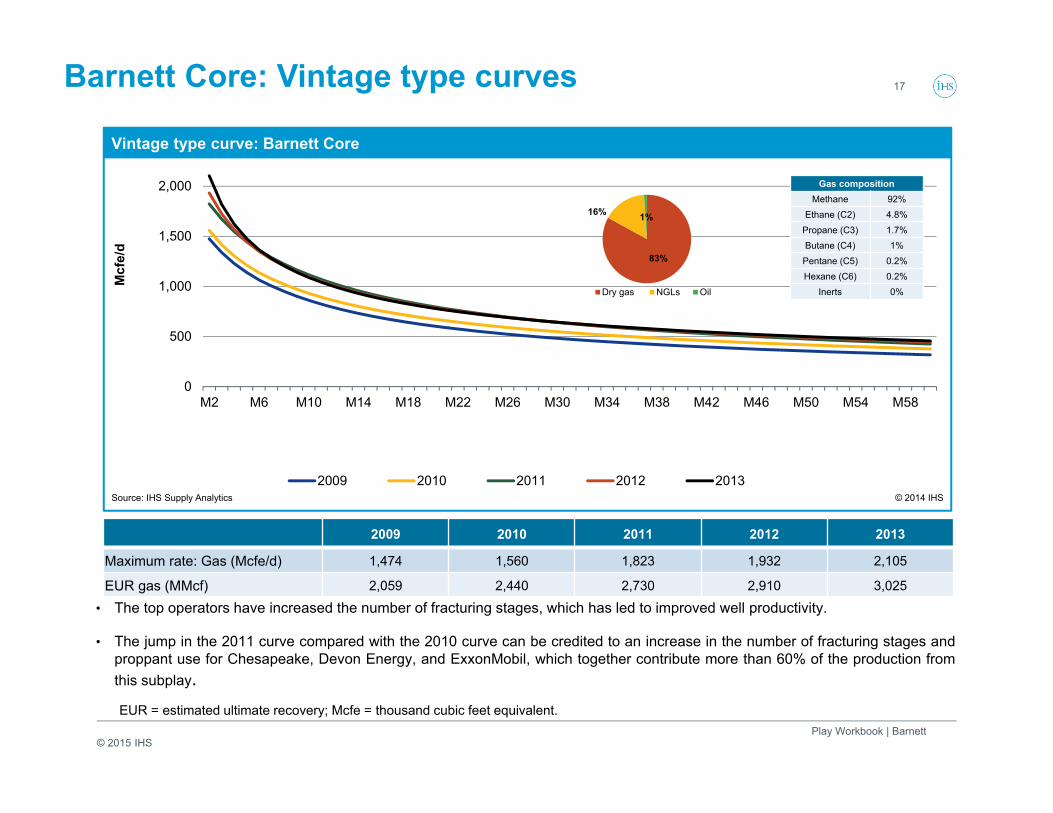

Barnett Core: Vintage type curves 17

Play Workbook | Barnett

2009 2010 2011 2012 2013

Maximum rate: Gas (Mcfe/d) 1,474 1,560 1,823 1,932 2,105

EUR gas (MMcf) 2,059 2,440 2,730 2,910 3,025• The top operators have increased the number of fracturing stages, which has led to improved well productivity.

• The jump in the 2011 curve compared with the 2010 curve can be credited to an increase in the number of fracturing stages andproppant use for Chesapeake, Devon Energy, and ExxonMobil, which together contribute more than 60% of the production fromthis subplay.

0

500

1,000

1,500

2,000

2,500

M2 M6 M10 M14 M18 M22 M26 M30 M34 M38 M42 M46 M50 M54 M58

2009 2010 2011 2012 2013

Vintage type curve: Barnett Core

Source: IHS Supply Analytics © 2014 IHS

Mcf

e/d

Gas compositionMethane 92%

Ethane (C2) 4.8%Propane (C3) 1.7%Butane (C4) 1%Pentane (C5) 0.2%Hexane (C6) 0.2%

Inerts 0%

EUR = estimated ultimate recovery; Mcfe = thousand cubic feet equivalent.

83%

16% 1%

Dry gas NGLs Oil

© 2015 IHS

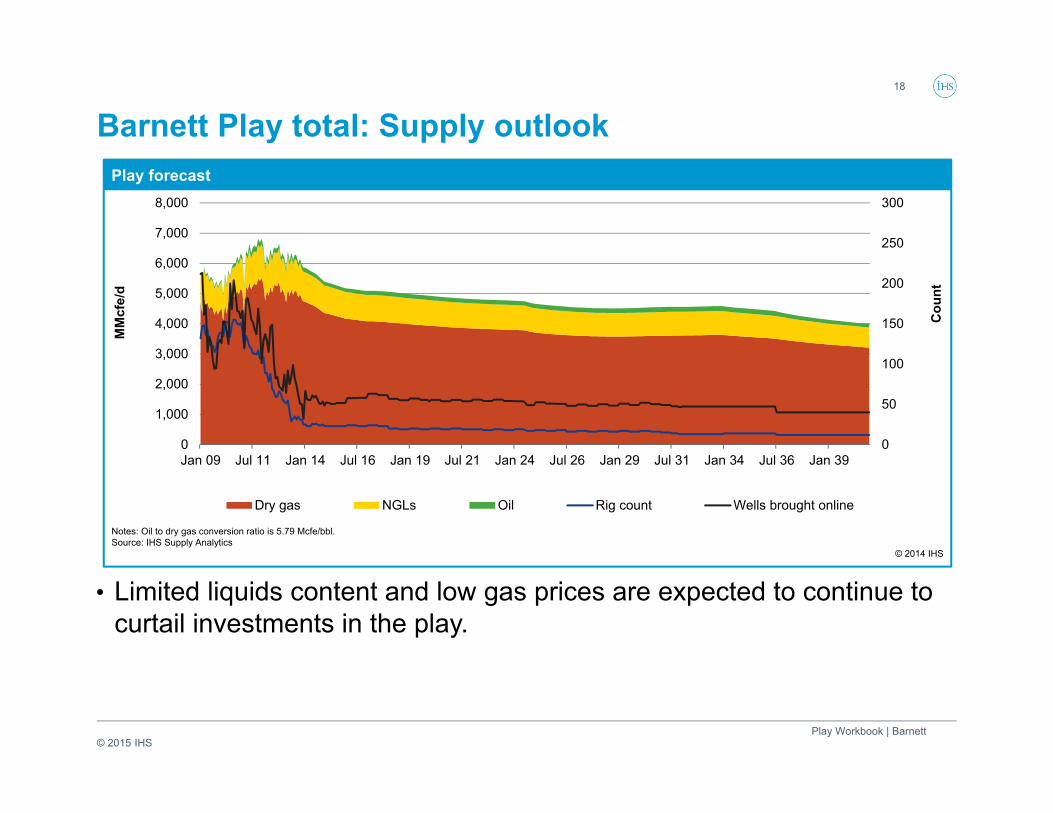

Barnett Play total: Supply outlook18

Play Workbook | Barnett

0

50

100

150

200

250

300

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Jan 09 Jul 11 Jan 14 Jul 16 Jan 19 Jul 21 Jan 24 Jul 26 Jan 29 Jul 31 Jan 34 Jul 36 Jan 39

Dry gas NGLs Oil Rig count Wells brought online

Play forecast

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe/bbl.Source: IHS Supply Analytics

© 2014 IHS

MM

cfe/

d

Cou

nt

• Limited liquids content and low gas prices are expected to continue to curtail investments in the play.

© 2015 IHS

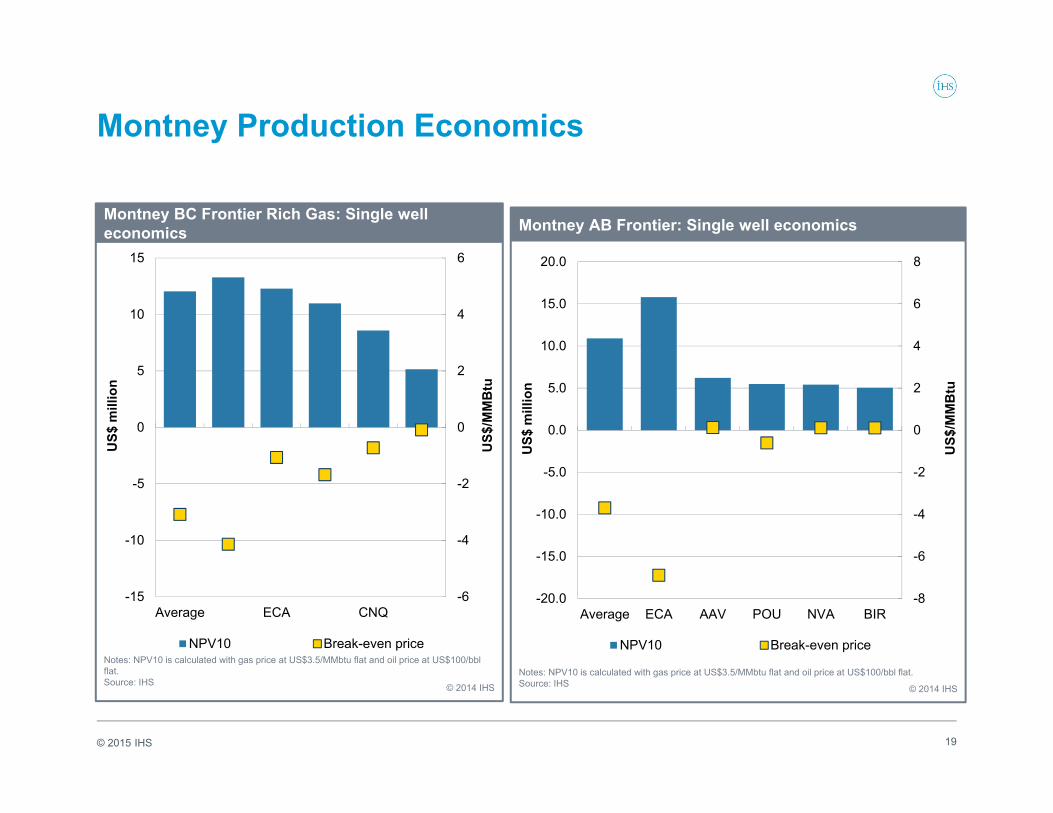

Montney Production Economics

19

-6

-4

-2

0

2

4

6

-15

-10

-5

0

5

10

15

Average ECA CNQ

NPV10 Break-even price

Montney BC Frontier Rich Gas: Single well economics

Notes: NPV10 is calculated with gas price at US$3.5/MMbtu flat and oil price at US$100/bbl flat.Source: IHS © 2014 IHS

US$

mill

ion

US$

/MM

Btu

-8

-6

-4

-2

0

2

4

6

8

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Average ECA AAV POU NVA BIR

NPV10 Break-even price

Montney AB Frontier: Single well economics

Notes: NPV10 is calculated with gas price at US$3.5/MMbtu flat and oil price at US$100/bbl flat.Source: IHS © 2014 IHS

US$

mill

ion

US$

/MM

Btu

© 2015 IHS

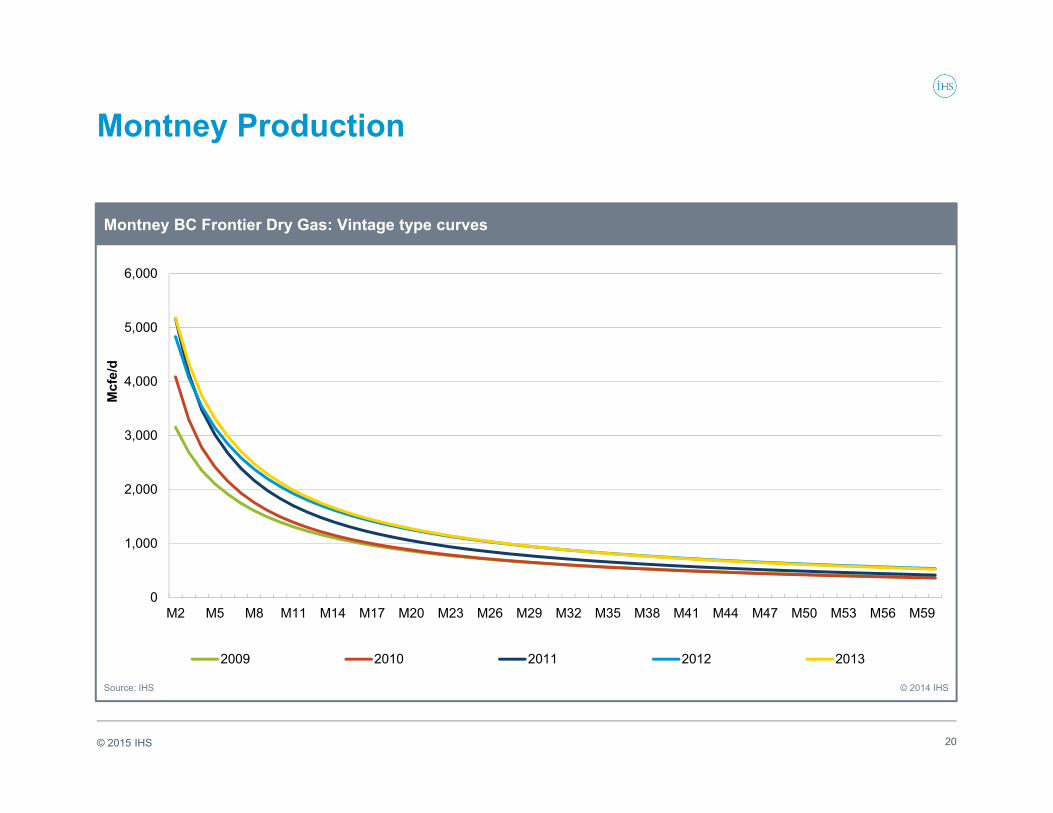

Montney Production

20

0

1,000

2,000

3,000

4,000

5,000

6,000

M2 M5 M8 M11 M14 M17 M20 M23 M26 M29 M32 M35 M38 M41 M44 M47 M50 M53 M56 M59

2009 2010 2011 2012 2013

Montney BC Frontier Dry Gas: Vintage type curves

Source: IHS © 2014 IHS

Mcf

e/d

© 2015 IHS

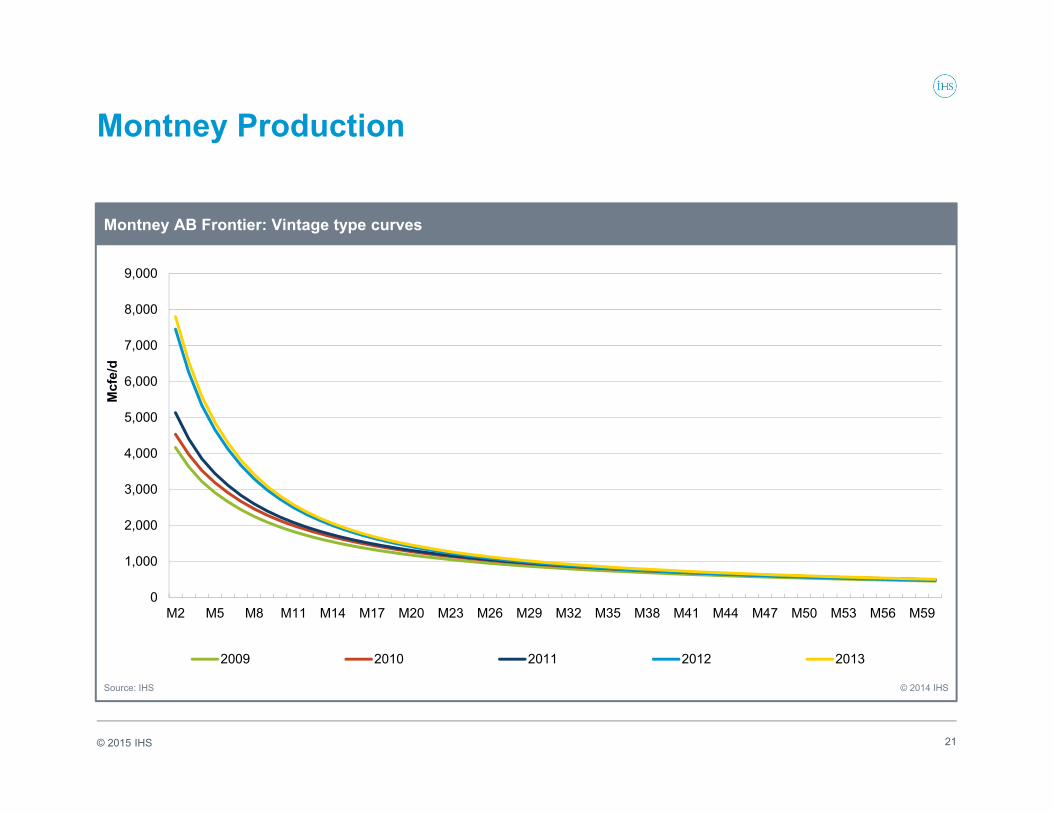

Montney Production

21

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

M2 M5 M8 M11 M14 M17 M20 M23 M26 M29 M32 M35 M38 M41 M44 M47 M50 M53 M56 M59

2009 2010 2011 2012 2013

Montney AB Frontier: Vintage type curves

Source: IHS © 2014 IHS

Mcf

e/d

© 2015 IHS

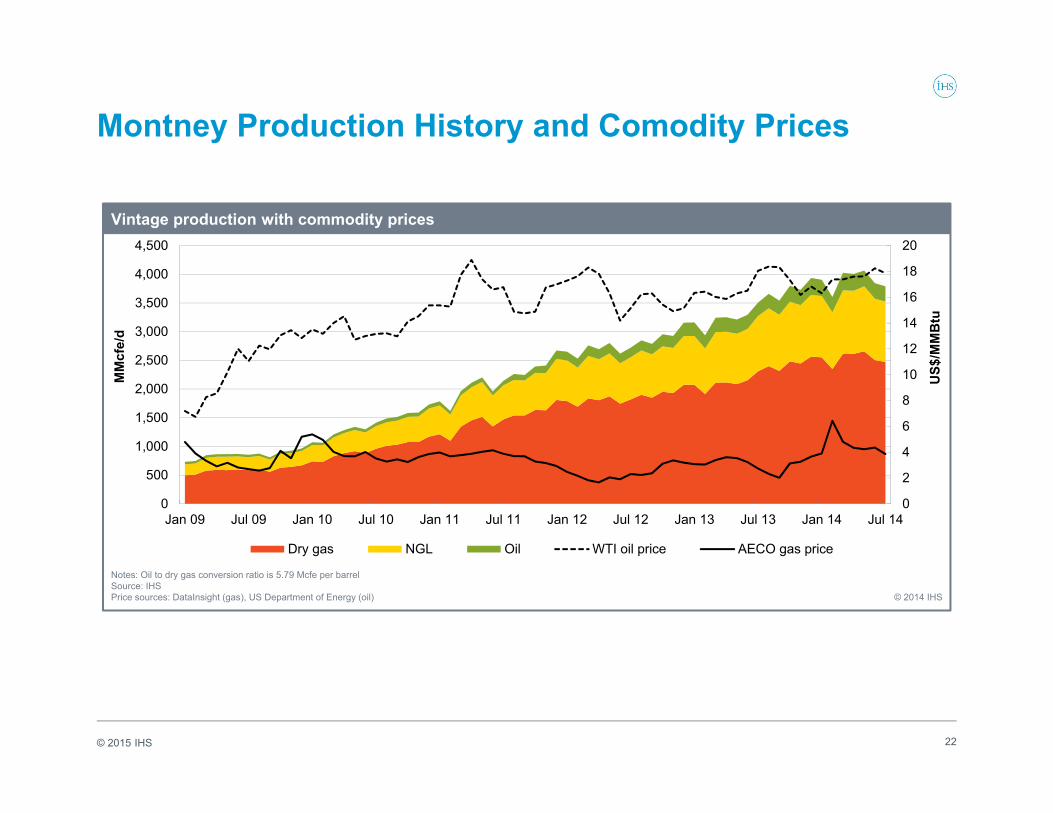

Montney Production History and Comodity Prices

22

0

2

4

6

8

10

12

14

16

18

20

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Jan 09 Jul 09 Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14

Dry gas NGL Oil WTI oil price AECO gas price

Vintage production with commodity prices

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe per barrelSource: IHSPrice sources: DataInsight (gas), US Department of Energy (oil) © 2014 IHS

MM

cfe/

d

US$

/MM

Btu

© 2015 IHS

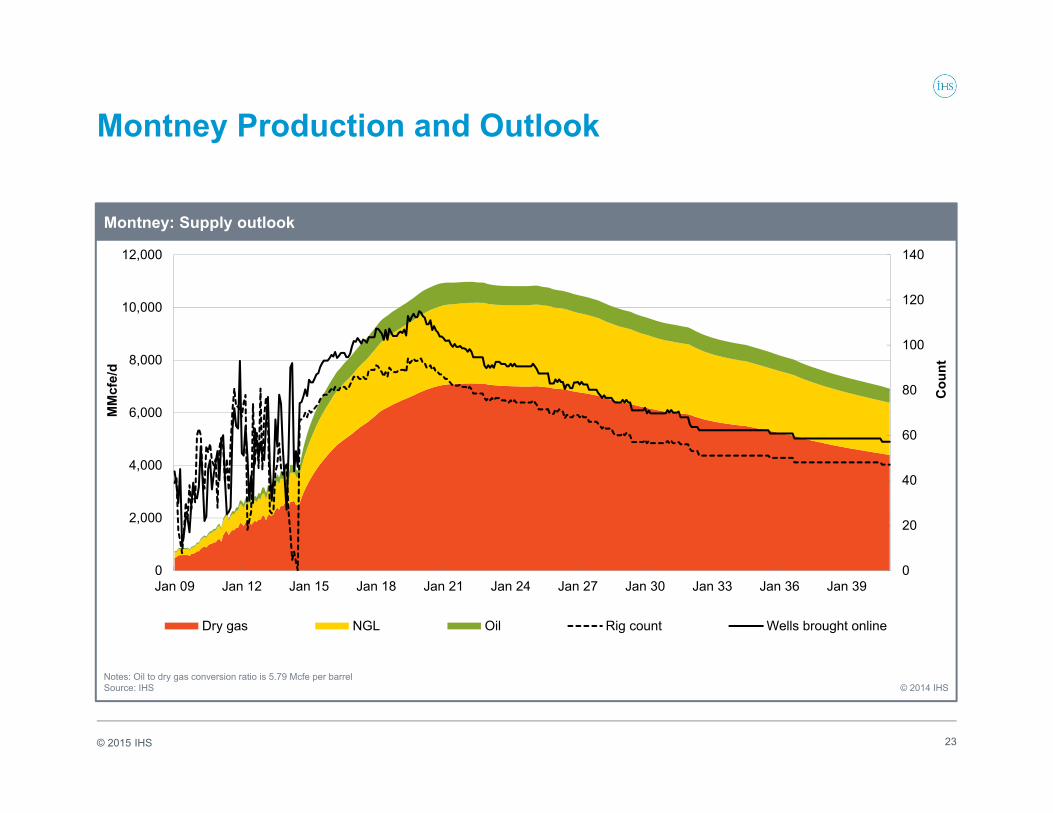

Montney Production and Outlook

23

0

20

40

60

80

100

120

140

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan 09 Jan 12 Jan 15 Jan 18 Jan 21 Jan 24 Jan 27 Jan 30 Jan 33 Jan 36 Jan 39

Dry gas NGL Oil Rig count Wells brought online

Montney: Supply outlook

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe per barrelSource: IHS © 2014 IHS

MM

cfe/

d

Cou

nt

© 2015 IHS

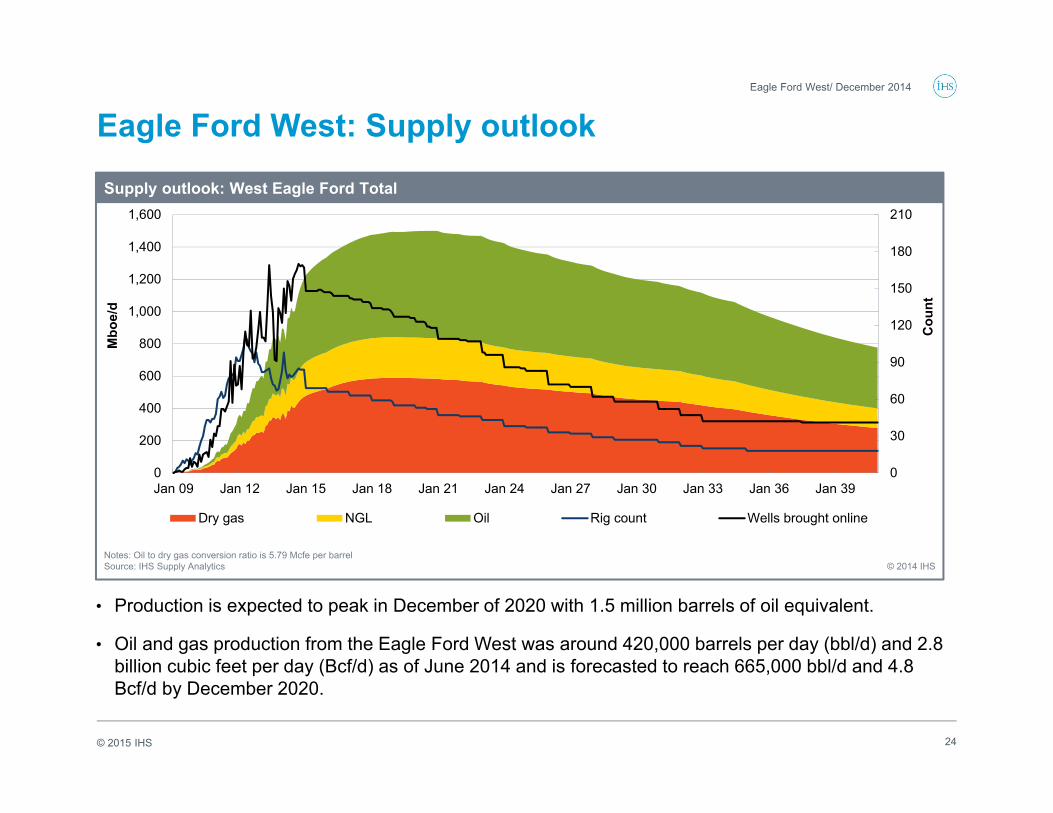

Eagle Ford West: Supply outlook

• Production is expected to peak in December of 2020 with 1.5 million barrels of oil equivalent.

• Oil and gas production from the Eagle Ford West was around 420,000 barrels per day (bbl/d) and 2.8 billion cubic feet per day (Bcf/d) as of June 2014 and is forecasted to reach 665,000 bbl/d and 4.8 Bcf/d by December 2020.

24

Eagle Ford West/ December 2014

0

30

60

90

120

150

180

210

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan 09 Jan 12 Jan 15 Jan 18 Jan 21 Jan 24 Jan 27 Jan 30 Jan 33 Jan 36 Jan 39

Dry gas NGL Oil Rig count Wells brought online

Supply outlook: West Eagle Ford Total

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe per barrelSource: IHS Supply Analytics © 2014 IHS

Mbo

e/d

Cou

nt

© 2015 IHS

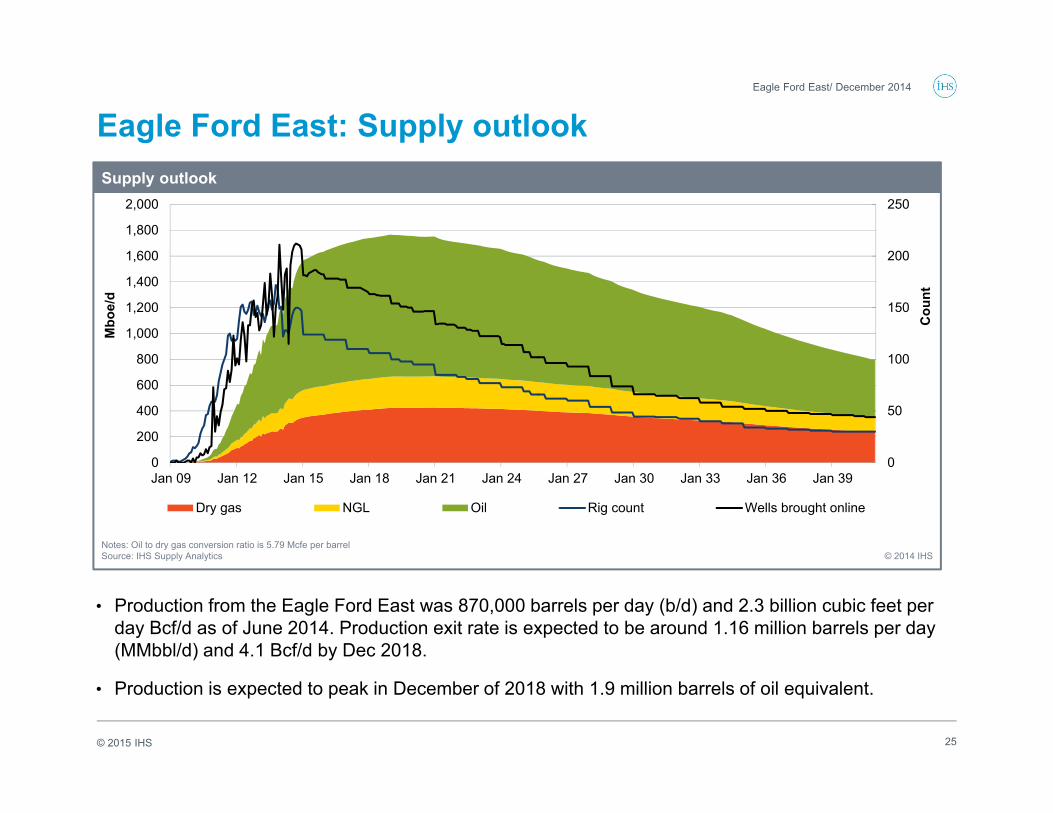

Eagle Ford East: Supply outlook

• Production from the Eagle Ford East was 870,000 barrels per day (b/d) and 2.3 billion cubic feet per day Bcf/d as of June 2014. Production exit rate is expected to be around 1.16 million barrels per day (MMbbl/d) and 4.1 Bcf/d by Dec 2018.

• Production is expected to peak in December of 2018 with 1.9 million barrels of oil equivalent.

25

Eagle Ford East/ December 2014

0

50

100

150

200

250

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan 09 Jan 12 Jan 15 Jan 18 Jan 21 Jan 24 Jan 27 Jan 30 Jan 33 Jan 36 Jan 39

Dry gas NGL Oil Rig count Wells brought online

Supply outlook

Notes: Oil to dry gas conversion ratio is 5.79 Mcfe per barrelSource: IHS Supply Analytics © 2014 IHS

Mbo

e/d

Cou

nt

© 2015 IHS

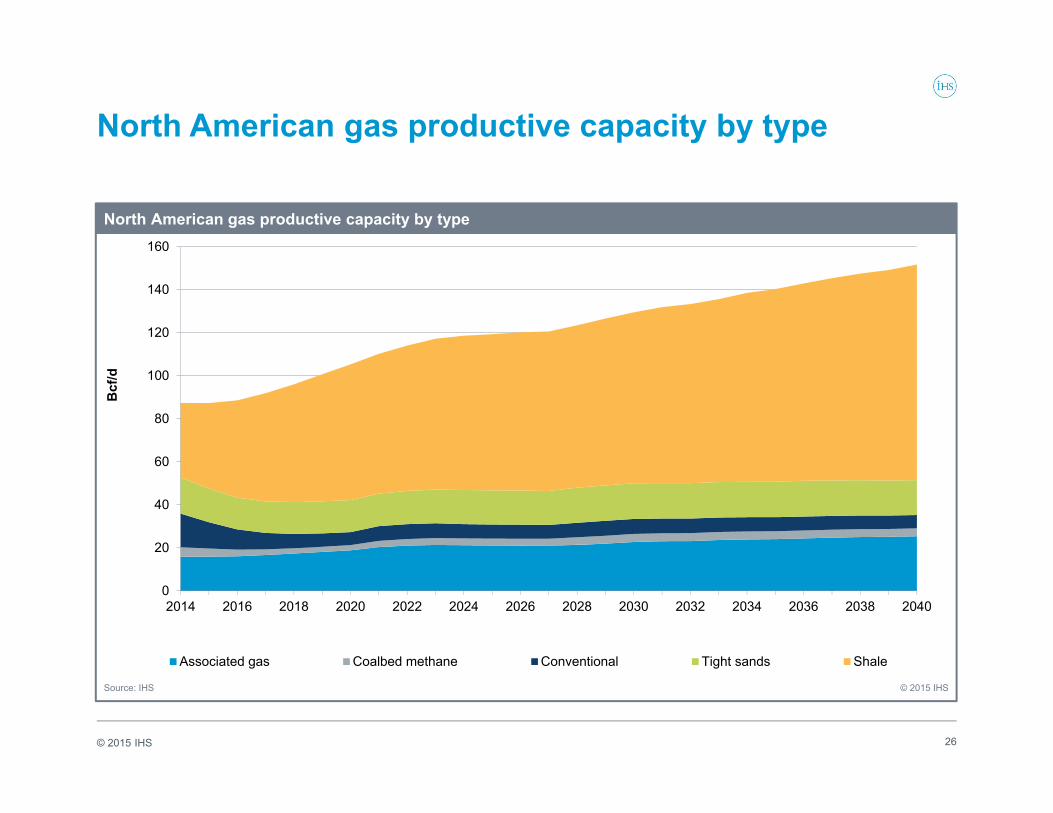

North American gas productive capacity by type

26

0

20

40

60

80

100

120

140

160

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040

Associated gas Coalbed methane Conventional Tight sands Shale

North American gas productive capacity by type

Source: IHS © 2015 IHS

Bcf

/d

© 2015 IHS

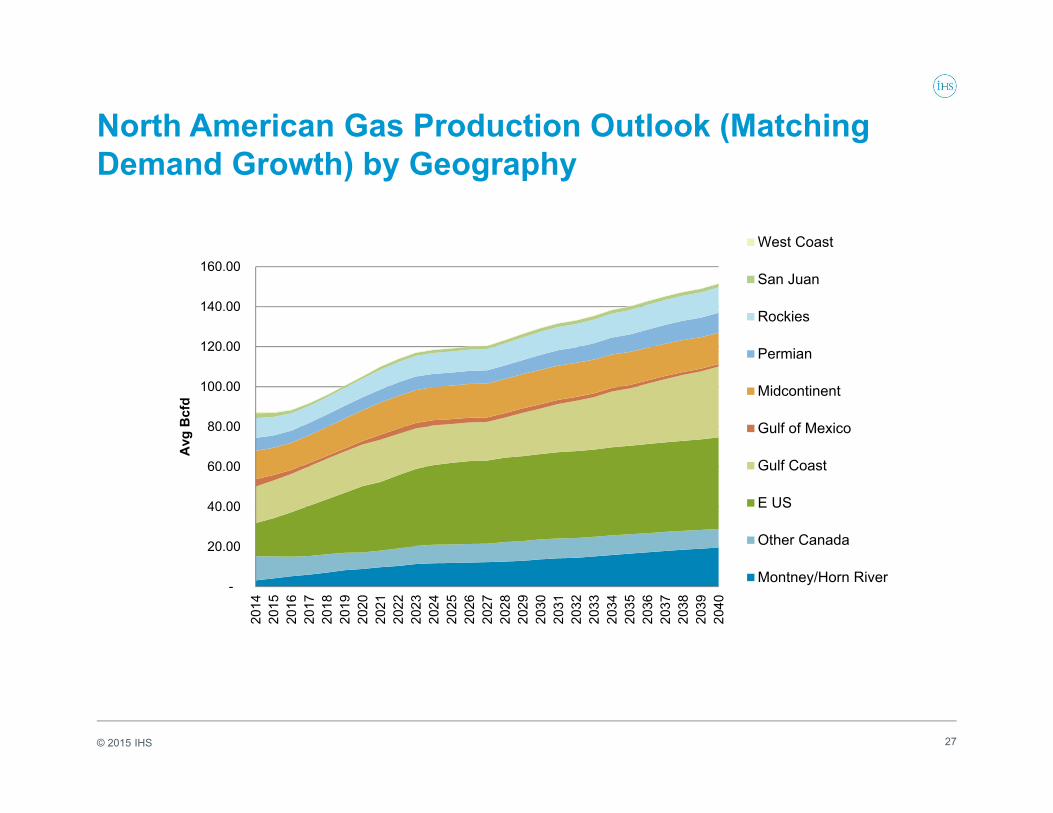

North American Gas Production Outlook (Matching Demand Growth) by Geography

27

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.0020

1420

1520

1620

1720

1820

1920

2020

2120

2220

2320

2420

2520

2620

2720

2820

2920

3020

3120

3220

3320

3420

3520

3620

3720

3820

3920

40

Avg

Bcf

d

West Coast

San Juan

Rockies

Permian

Midcontinent

Gulf of Mexico

Gulf Coast

E US

Other Canada

Montney/Horn River

© 2015 IHS

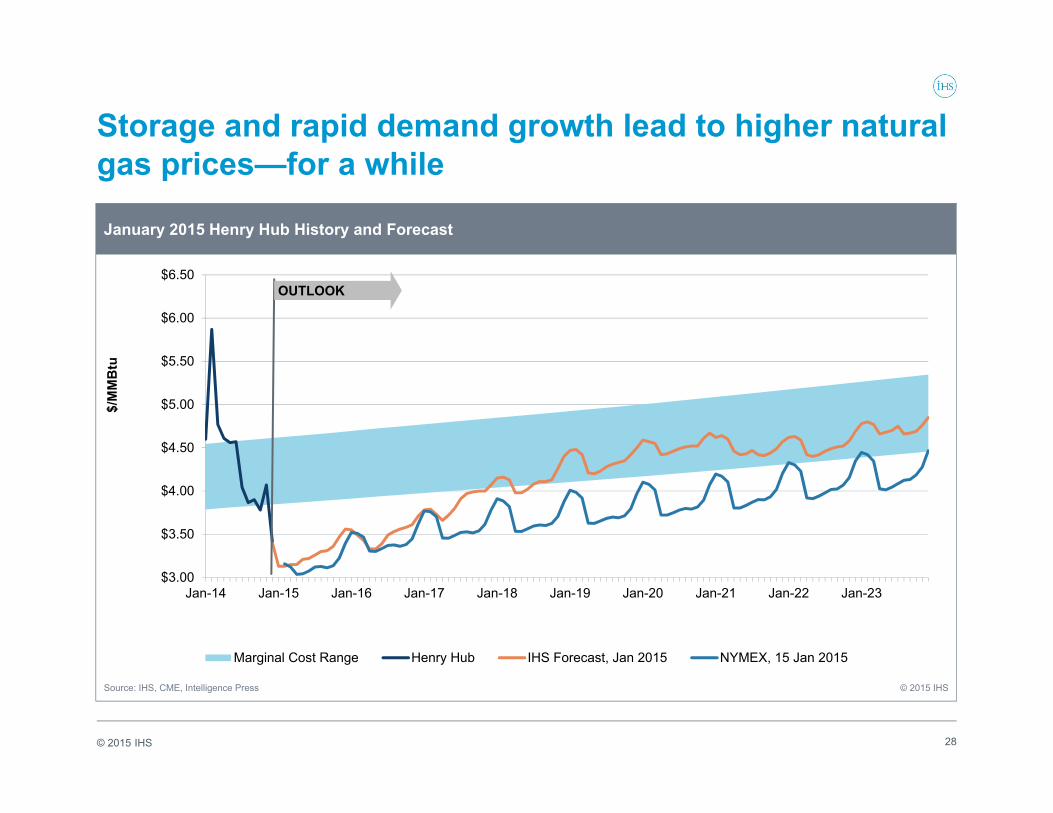

Storage and rapid demand growth lead to higher natural gas prices—for a while

28

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21 Jan-22 Jan-23

Marginal Cost Range Henry Hub IHS Forecast, Jan 2015 NYMEX, 15 Jan 2015

January 2015 Henry Hub History and Forecast

Source: IHS, CME, Intelligence Press © 2015 IHS

$/M

MB

tu

OUTLOOK