Presentation Association of Unified Telecom Service Providers of India November 8, 2006.

25

Presentation Association of Unified Telecom Service Providers of India November 8, 2006

-

Upload

jerome-shields -

Category

Documents

-

view

218 -

download

1

Transcript of Presentation Association of Unified Telecom Service Providers of India November 8, 2006.

Presentation

Association of Unified Telecom Service Providers of India

November 8, 2006

“Delivering the promise of improved Access, Coverage and Teledensity in India”

Our Aim

2

3

About AUSPI• Established in 1997• Core Members

– HFCL Infotel Ltd– Reliance Communications Ltd– Reliance Telecom Ltd– Tata Teleservices Ltd– Tata Teleservices (M) Ltd

• Associate Members– Huawei Telecommunications (I) Co Pvt Ltd– Lucent Technologies Hindustan Pvt Ltd– Qualcomm India Pvt Ltd– ZTE Telecom India Pvt Ltd

4

To enable its members to build world class

telecom capabilities in India to help meet

national teledensity goals and play a larger

role in shaping global developments in the

telecom sector.

Vision

5

Mission

• Support promotion of CDMA technology towards achievement of national goals on Telecom services.

• Facilitate bridging of the digital divide. • Facilitate the implementation of the latest technologies in the

telecom space. • Establish strategic relationships with Government, Regulator, policy

makers and industry decision makers to help formulate best policies and practices to promote co-operation and to resolve issues necessary for the growth of the industry.

• Serve as a worldwide resource base for information on innovative products and applications for improving reach by providing differentiation in services provided.

6

Pursuit

AUSPI facilitates the adoption of advanced telecom technologies, to accelerate India’s

transition into a knowledge economy

Vendor

National / International Players

Policy MakerRegulator

International organizations

Mr. Anil D AmbaniMr. Ratan N Tata

Prominent Leadership

7

8

Enhanced value for customers

• Affordable service.

• Innovative products.

• Innovative applications & solutions.

9

CDMA Worldwide Subscriber Statistics: June 2006 [Second Quarter]

270,200,000Total

4,400,000Europe, Middle East & Africa

49,200,000Caribbean & Latin America

100,400,000North America

116,200,000Asia Pacific

335 Mn Total

6 MnEurope, Middle East & Africa

70 MnCaribbean & Latin America

116 MnNorth America

143 Mn Asia Pacific

Total: 335 Mn

Asia Pacific 42.6%

Caribbean & Latin America 21.0%

North America 34.6%

Europe, Middle East & Africa 1.8%

10

• Private operators introduced CDMA mobile service in 2003.

• CDMA created a competitive landscape that made wireless affordable.

• Created increased and better coverage.

• Created new markets for mobile services.

• India is emerging as the key driver of growth for CDMA.

• Operational in India with 43 private networks.

• Has more than 37 Mn subscribers in the country.

• 2 Mn PCOs operational – Private CDMA operators are heralding growth

[44% of total PCOs in India]

CDMA in India

11

Phenomenal growth of CDMA - At a glance

Percentage of Growth Rate

GSM CDMA

Quarter Ended Mar 05 18.29 20.00

Quarter Ended Dec 05 15.05 22.79

Quarter Ended Jun 06 13.00 28.00

CDMA is growing much faster than GSM in the Indian Market

Source:TRAI

12

Affordability of CDMA

MoU per subscriber per month [QE June 06]

CDMA443

GSM414

Affordability of CDMA is leading to much higher usage for CDMA based services.

Source:TRAI

13

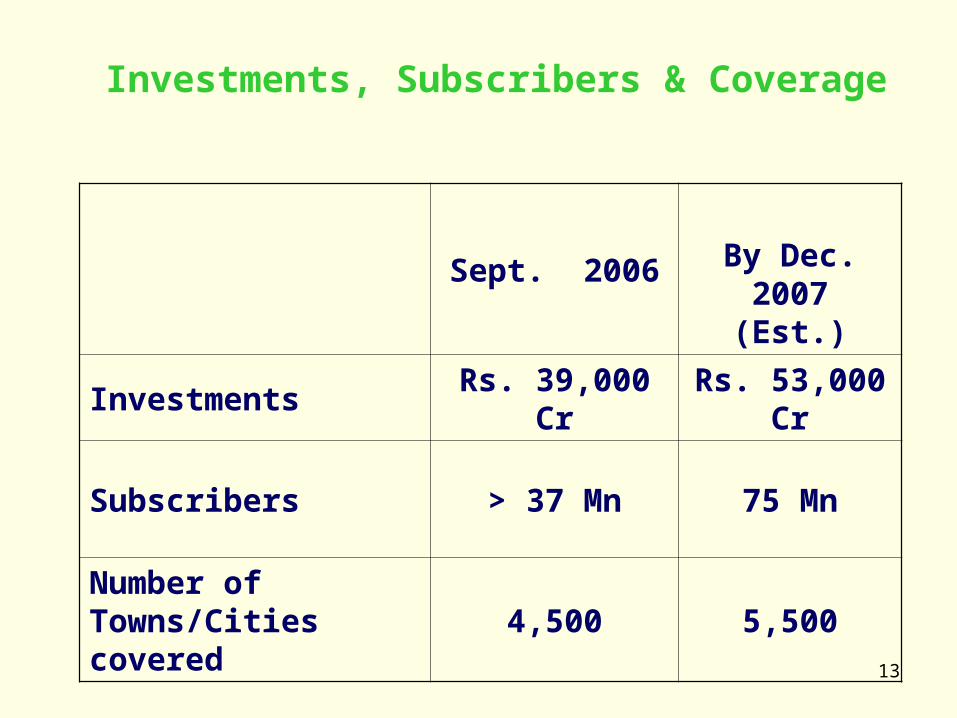

Investments, Subscribers & Coverage

Sept. 2006 By Dec. 2007 (Est.)

Investments Rs. 39,000 Cr Rs. 53,000 Cr

Subscribers > 37 Mn 75 Mn

Number of Towns/Cities covered

4,500 5,500

14

• Simplification of SACFA siting procedure Issues pending for so many years have been resolved.

• Wireless operating license for BTS enhanced to 5 years from 3 months.

• Reduced delay in import clearance from WPC.

• Effective inputs for 11th Five Year Plan on various issues.

• Recommendation for 1900 MHz band for CDMA. Allocation on successful completion of field trial

• Initiated exercise for establishment of interconnect exchange.

Achievements

15

• Submission to Hon’ble Parliamentary Standing Committee on Information Technology which ultimately recommended appropriate spectrum for CDMA.

• Proper Definition for Adjusted Gross Revenue.

• Interconnection issues with PSUs – resolution of some issues.

• Provisioning of passive link for interconnection by BSNL.

• Extension of benefit under section 801A of Income Tax Act.

• Initiated case for reduction of port charges for POIs.

16

• Acceptance of our request for equality in spectrum charging on revenue share basis for MW access and backbone for all technologies.

• Industry Associations on common platform for mobile growth in a proper and disciplined manner-ACT.

• Project ‘MOST’ initiated to capture the potential rich benefit of infrastructure sharing.

• Role of CDMA in USO was 38% of the SSAs tendered by USO Administration.

17

Challenges Ahead

• Future focus includes the following key enablers for enhanced teledensity:Early resolution of spectrum issues including re-farming.Allowing technology innovation to flourish – case of

Broadband.Enhancement of rural teledensity, including the use of

USO funds.Sharing of National resources.Reduction in Revenue Sharing & spectrum charges. Identification and sharing of global best practices.

18

Spectrum Issues• Transparent, non-discriminatory, technology neutral and judicious

allocation of spectrum to all service providers - Equality principle for all technologies.

• Time bound road map for making available additional and sufficient spectrum based on international average.

• Broadband wireless spectrum to existing UASL licensees only on circle basis. to make available 200 MHz spectrum to meet growth requirement until

2007 and additional 100 MHz of spectrum by 2010.

• Spectrum usage charges to be reduced to cover only cost of administration and management of spectrum.

• Delinking of corDECT and CDMA frequency allocation.• Further simplification of SACFA procedure (Proper constitution of

SACFA)

19

Allowing technology innovation to flourish - Broadband

• For an increasingly knowledge based society like ours, enhancing broadband penetration is a high priority.

• Broadband would create jobs, and increase productivity, and provide access to new and improved services for the population.

• To increase broadband penetration, AUSPI suggests: Nil Custom Duty with no CVD for broadband equipment. 100% depreciation in CPEs like PCs in the first year. Government subsidy in rural and semi urban areas for CPEs. Encouragement of e-governance by Government. Adequate spectrum for wireless broadband.

20

Enhancement of Rural teledensity

To bridge the Urban-Rural divide, Cost to Serve should be reduced.

Innovative mechanisms like sharing of infrastructure etc need to be introduced, including effective utilization of the USO Fund.

Our members are committed to playing their role in this effort – won 38% of the SSAs tendered by USO Administration in Feb. 2005, in stiff competition with incumbent.

21

Sharing of National Resources

Infrastructure sharing is prevalent in countries like Malaysia, Hong Kong, Singapore, Australia. This is driven by a “Code of Access to Telecom Infrastructure”.

Infrastructure sharing reduces duplication & waste of national resources.

Infrastructure sharing can be on reasonable commercial terms.

Uniformity in law required from the Central and State Governments to facilitate development of telecom infrastructure – e.g. cell site installation, Right of Way (ROW) permission.

• India has one of the highest tax regimens in the World, and levies must be reduced to bring them in line with International best practices.

* Backbone spectrum charges extra with additional proposal of 1% for 3G **Est. from Spectrum fees & revenue of China Mobile (Source: TRAI)

• High percentage of revenue share to be brought down to 6% including levy for USO fund.• Service tax in telecom sector of 12% + Education Cess be brought down (already 1/3 of the total

collection of service tax is estimated to be from telecom services).• With growth in subscribers every month, the additional revenues will in any event compensate for

reduced taxes and levies.

Reduction in levies

Pakistan Sri Lanka China India

Regulatory charges

% age of revenue % age of revenue % age of revenue % age of revenue

Service tax, GST GST VAT 3% 10% + CST

License Fee 0.5% + 0.5% R & D

0.3% of turnover + 1% of capital invested (inv)

Nil 5 – 10%

Spectrum Charge Cost recovery ~1.1% to turnover ~0.5%** (China Mobile)

2 ~ 6%*

USO 1.5% Nil (only on ISD calls) Nil Incl in license fees

Total Regulatory charges

2.5% +GST+ cost recovery

1.3% turnover +1% inv + VAT

0.5%+3% (Tax) 19%~28% + CST

22

23

Identification &Sharing of Global best practices

• Level Playing field between all operators specially incumbent.

• Self Certification / Testing.• Expeditious interconnection as a right on reciprocal

terms.• Elimination of ADC.

24

Conclusion

• AUSPI is committed to play its role in the fulfillment of Government’s vision for enhanced telecom connectivity in India.

• AUSPI members have contributed a sizable proportion of the growth seen in the Indian market.

• AUSPI will continue to embrace the latest technologies with a view to speeding up the transition of the Indian economy into a knowledge-based information society.

Contact us at : [email protected]