Presentation

42

Tong-Tai Machine & Tool Co. (4526TT) TARGET PRICE : TWD 18.73 -23.55% DOWNSIDE Sell JUNE 22, 2013

-

Upload

shane-chung -

Category

Documents

-

view

42 -

download

0

Transcript of Presentation

Tong-Tai Machine & Tool Co. (4526TT)

TARGET PRICE : TWD 18.73 -23.55% DOWNSIDE

Sell

JUNE 22, 2013

INVESTMENT THESIS

1. Capex delays in Chinese Auto Market

2. Yen Weakening Enhances Price Competition

3. PCB Drilling Struggles in Transition

1Investment Theses Chinese Auto

Market Yen Depreciation PCB Drilling Valuation

Capex Delays in Chinese Auto Market

• 25% revenue derived from Chinese local auto makers in 2012

• Demand from auto makers expected to plunge

2Investment Theses Chinese Auto

Market Yen Depreciation PCB Drilling Valuation

-75%

-50%

-25%

0%

25%

50%

75%

0

100

200

300

400Ja

n, 2

011

Jul,

2011

Jan,

201

2

Jul,

2012

Jan,

201

3

Sale Volume of Japan Manufacturers YoY

Japanese auto sales in China shrink after anti-JP protest

Customer vehicle sales have weakened since 2011

5.2%

26.0%29.8%

-6.1% -5.5%

3.1% 2.8% 2.8%

-20%

-10%

0%

10%

20%

30%

40%

0.0

1.0

2.0

3.0

4.0

5.0

2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

(Unit: mn) CV Shipments YoY

Source: China Association of Automobile Manufacturers

• Japanese motor sales dropped

• CV market will continue to be flat in next 3 years

• The boost in demand was triggered by stimulus during 2009 to 2010 but growth will revert to double digits in next 3 years

Source: China Association of Automobile Manufacturers

6.7%

45.4%

32.4%

2.5%4.3%

12.4%12.0% 12.0%

0%

10%

20%

30%

40%

50%

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

Car Shipments YoY

Source: CAAM, Team Estimate

Overcapacity limits machinery demand

(Unit: mn)(Unit: k)

3

0%

40%

80%

120%

160%

Indu

stry

Ave

rage

SAIC

Grea

t Wal

l

Dong

feng

Brill

ianc

e

CCAG JA

C

Geel

y

GAC

BYD

FAW

2011 2012(f) 2013(f) 2014(f)

3.4%

18.7%8.0%

72.1%

54.6%

-29.4%

13.6% 16.0%

-40%

-20%

0%

20%

40%

60%

80%

0

10

20

30

40

2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

Capex YoY(RMB bn)

Source: DataStream, Team Estimate

Capex will be postpone to 2H14 • Chinese auto makers have built large capacity through 2012, which leads to falling capacity utilization among the industry

• We expect auto makers will postpone capacity expansion in 2013

-120

-80

-40

0

40

80

Jan,

201

1

Apr,

2011

Jul,

2011

Oct

, 201

1

Jan,

201

2

Apr,

2012

Jul,

2012

Oct

, 201

2

Jan,

201

3

Apr,

2013

(Units: 10k)

Inability to sell high inventory will deter expansion

Source: Goldman Sachs

Auto makers delay expansion on 80% capacity utilization

Source: China Association of Automobile Manufacturers

4

Yen Weakening Enhances Price Competition

5Investment Theses Chinese Auto

Market Yen Depreciation PCB Drilling Valuation

FX Change

Order

• Price competition• Market determination

Shipment• Sales recognition

-25%

-20%

-15%

-10%

-5%

0%

5%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013

JPY/USD TWD/USD KRW/USD

1 Month

22% Yen Depreciation since Oct. 2012

3 Months

Source: Team Estimate

6

-25%

-20%

-15%

-10%

-5%

0%

5%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013

JPY/USD TWD/USD KRW/USD

Taiwanese and Korean Currencies under Depreciation Pressure in Jan. 2013

FX Change

Order

• Price competition• Market determination

Shipment• Sales recognition

1 Month

3 Months

Source: Team Estimate

7

-25%

-20%

-15%

-10%

-5%

0%

5%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013

JPY/USD TWD/USD KRW/USD

FX Change

Order

• Price competition• Market determination

Shipment• Sales recognition

1 Month

3 Months

Price Reduction to be Recognized in May

Source: Team Estimate

8

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

130%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013

JP TW KR

30%

Tong-Tai Competes with 30% Lower Selling Price

Source: Team Estimate

9

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

130%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013

JP TW KR

• Maintain current selling prices

Fall in sales and market share

• Reduce selling prices Fall in gross profit

30%

10%

Price Difference Narrows to 10%

Source: Team Estimate

10

Mechanical Drilling Struggles in Transition

11Investment Theses Chinese Auto

Market Yen Depreciation PCB Drilling Valuation

• ASP decreases under fierce competition

• Shipments remain flat as the demand for laser drilling cannibalizes that for mechanical drilling

(NTD 10k)

(NTD bn)

Drilling machine sales to tumble

Source: Team Estimate

Source: Team EstimateSource: Team Estimate

ASP to drop because of price competition Shipments continue to decline through 2015

$1.22

$1.14$1.13

$1.03

1.00

1.05

1.10

1.15

1.20

1.25

2012 2013(f) 2014(f) 2015(f)

$350.86

$333.32

$323.41

$313.80

300

310

320

330

340

350

360

2012 2013(f) 2014(f) 2015(f)

348

342

348

329

315

320

325

330

335

340

345

350

2012 2013(f) 2014(f) 2015(f)

(Units)

12

306

548

331210

719

325 348 342 348 329

15%

22%

19%

29%

25% 25% 25%23% 22%

20%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

0

100

200

300

400

500

600

700

800

2006 2007 2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

Shipment Market Share • ASP has moved down 12% for Japanese PCB drilling machine manufacturers

• Tong-tai does not retain its price competitiveness and will suffer decreasing market share

• PCB markers are to invested more capex in any layer HDI

Tong-tai’s market share to decrease

(Units)

Any layer HDI cannibalizes market for traditional PCB

(NTD bn)

iPhone 4

Source: Bloomberg

Source: Team Estimate

6.61

2.83

10.59

4.82 4.89 5.22 5.28 5.32

30%

26%

39%

17%19% 19% 18% 17%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

Capex Capex on Mechanical Drilling % of Capex

13

ValuationSell

Share Price (June-14-2013)

Target Price

TWD 24.5

TWD 18.73

Market Cap (TWD mn)

Share Outstanding (mn)

5,549

226.5

2015 EPS2014 EPS2013 EPS

$ -0.36$ -0.49$ -0.16

TP 18.73

BVPS 20.81

$0

$10

$20

$30

$40

$50

$60

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2.20x

0.63x

1.81x

1.42x

1.02x

14Investment Theses Chinese Auto

Market Yen Depreciation PCB Drilling Valuation

Q & A

Market Analysis – Mechanical Drilling

Market Analysis – Laser Drilling

PCB Market Outlook

Upside Case for Tong-tai

Passenger Vehicle Market

Current Headwind in Auto Market

Scooter Market in Vietnam

Auto Market in India

Machinery Market Outlook

Comparable Companies

Shareholder Structure

Subsidiaries

Korea’s Free Trade Agreements

Light-Duty Truck Market

PMI & BCI

Drilling Machine Market Outlook

PCB Drilling

Auto Market

Politics

Financials Macro

Balance Sheet

Income Statement

Statement of Cash FlowAuto Market Customers

Capex Forecast

FX Change Analysis

Key Financial Ratios

Sensitivity Analysis

28.9%

30.0%

21.9%

7.3%

52.9%

33.2%

5.2%

7.1%

14.1%

13.0%

12.2%

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

2005

2006

2007

2008

2009

2010

2011

2012

2013

(f)

2014

(f)

2015

(f)

(Unit: mn) PV Sale Volume YoY

China

IndiaIndonesia

Japan

Malaysia

Russia

Taiwan

Thailand

The U.S.

0

200

400

600

800

$0 $15,000 $30,000 $45,000 $60,000GDP Per Capita: Dollars in USD

(Vehicle per 1,000 people)

PV demand to see strong growth Vehicle penetration follows GDP per capita

PV Market Still on the Rise

2001

2005

2010 2012

2013(f)

2014(f)

2015 (f)

R² = 0.9851

0

5

10

15

20

25

¥0 ¥20,000 ¥40,000 ¥60,000 ¥80,000

14.3%

14.6%

18.5%

16.9%

11.6%

13.3%14.4%

11.9%12.0%

11.0%10.0%

0%

5%

10%

15%

20%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

(f)

2014

(f)

2015

(f)

Average Wage YoY

Average Wage: Dollars in RMB

PV Sales Volume (mn)

Growing wages will promote PV sales Wages are highly correlated with PV sales

Conclusion: Increasing wages still support growth in auto market

PV Market Still on the Rise

(Dollars in RMB)

0.0

0.5

1.0

1.5

2.0

Jan, 2008 Jan, 2009 Jan, 2010 Jan, 2011 Jan, 2012 Jan, 2013

(Units: mn)

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0%

10%

20%

30%

40%

Jan,2002

Apr,2003

Jul,2004

Oct,2005

Jan,2007

Apr,2008

Jul,2009

Oct,2010

Jan,2012

Apr,2013

Money Supply (M2) Car Sales Volume YoY

Growth in monthly sales have slowed down since 2011

M2 moves ahead of car sales

Short-term Headwinds• Car sales YoY have shown

little growth since 2011• Low money supply growth

deters consumers’ willingness to retire their old vehicles

• Limitations on car purchase in big cities

0.0

0.5

1.0

1.5

2.0

Jan,

200

9

Jul,

2009

Jan,

201

0

Jul,

2010

Jan,

201

1

Jul,

2011

Jan,

201

2

Jul,

2012

(Units: mn) PV Sales Volume

Beijing Guangzhou

Restrictions do little impact on car sales

Age 2012 2015(F) Growth rate

15-19 121,090 121,728 1%20-24 116,568 119,172 2%25-29 108,186 112,869 4%30-34 98,203 103,381 5%35-39 86,742 93,046 7%40-44 76,598 81,313 6%45-49 67,124 71,973 7%50-54 57,934 61,948 7%55-59 49,468 52,728 7%60-64 36,362 42,791 18%Total 818,275 860,949 5%

Active Population

Source: BMI(Units: k)

Auto Market in India

2.48 3.19 3.43 3.44 3.64 3.93 4.320.0

1.0

2.0

3.0

4.0

5.0

2009 2010 2011 2012 2013(F) 2014(F) 2015(F)

Vehicle Sales

9.37 11.77 13.44 14.11 15.28 16.50 17.760.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

20.0

2009 2010 2011 2012 2013(F) 2014(F) 2015(F)

Scooter Sales

Source: BMI

(Units: mn) (Units: mn)

Population: 1.2 bn

Motorcycle: 0.21 bn

Vehicle: 0.06 ~ 0.12 bn

Penetration Rate:

Motor (17%), Vehicle (5%~10%)

I. Tightened Monetary Policy Reverse

II. Penetration Rate

Source: BMI

I. Penetration Rate

II. Active Population

2.37 2.87 2.55 2.69 3.00 3.31 3.11 2.95 2.86 2.830.0

1.0

2.0

3.0

4.0

2006 2007 2008 2009 2010 2011 2012 2013(F) 2014(F) 2015(F)

Scooter Sales

Source: BMI, Team Estimate

Age 2012 2015(F) Growth Rate

15-19 8,161 6,806 -17%20-24 9,115 8,892 -2%25-29 8,602 8,862 3%30-34 7,575 8,202 8%35-39 6,770 6,991 3%40-44 6,304 6,609 5%45-49 5,761 6,012 4%50-54 4,936 5,449 10%55-59 4,001 4,446 11%60-64 2,573 3,455 34%Total 63,798 65,724 3%

Low Growth Rate in Active Population

Source: BMI

(Unit: mn)

(Units: k)

Population: 90 mn

Motorcycle: 25 mn

Penetration Rate: 27.7%

3.6 persons / unit

Scooter Market in Vietnam

• Chinese businesses in rural area buy LDTs for transportation and logistics

• Manufacturers have cut demand for trucks owing to shrinking export activities

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-10%

0%

10%

20%

30%

40%

50%

60%

Jan,2010

Jul,2010

Jan,2011

Jul,2011

Jan,2012

Jul,2012

Jan,2013

China Export YoY LDT Sales Volume YoY

Light-Duty Truck Market

1

0

5

10

15

20

Jan, 2010 Jul, 2010 Jan, 2011 Jul, 2011 Jan, 2012

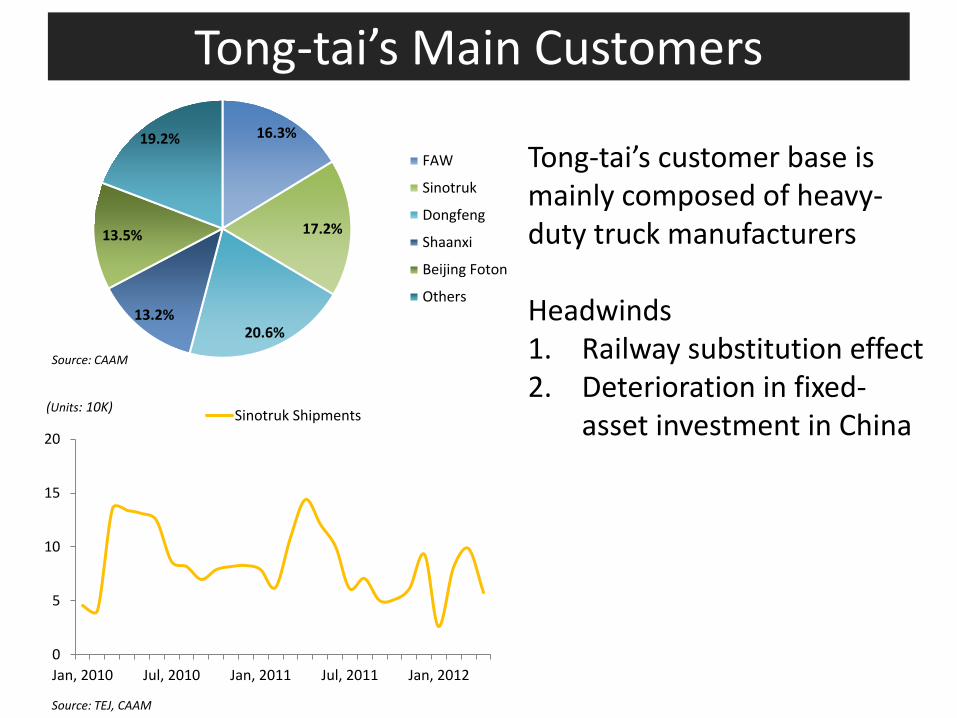

(Units: 10K) Sinotruk Shipments

16.3%

17.2%

20.6%13.2%

13.5%

19.2%FAW

Sinotruk

Dongfeng

Shaanxi

Beijing Foton

Others

Tong-tai’s customer base is mainly composed of heavy-duty truck manufacturers

Headwinds1. Railway substitution effect2. Deterioration in fixed-

asset investment in China

Source: CAAM

Source: TEJ, CAAM

Tong-tai’s Main Customers

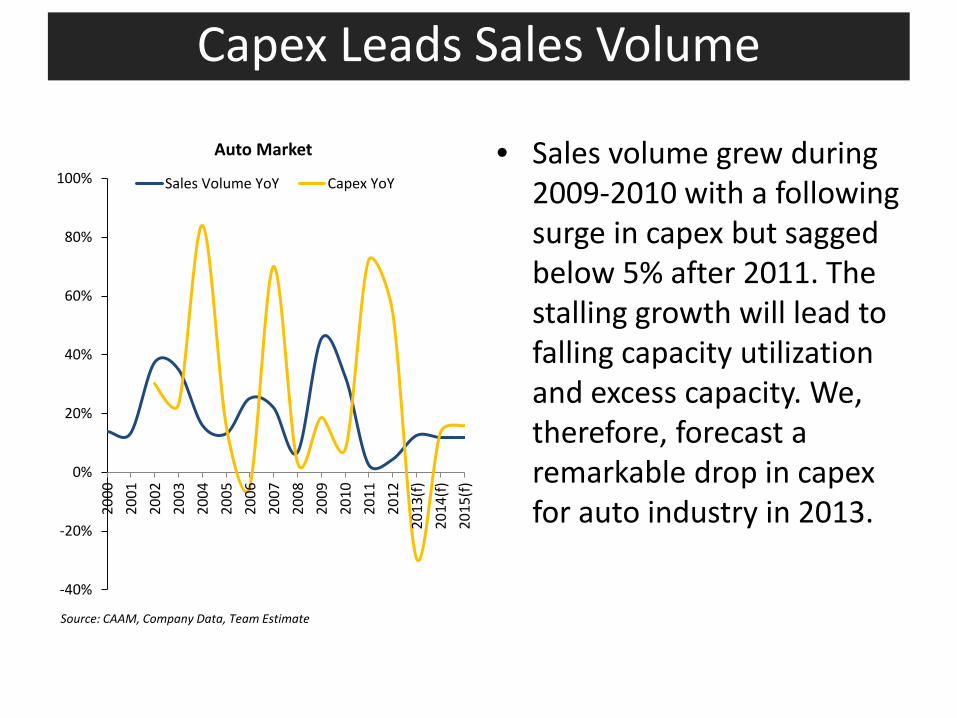

• Sales volume grew during 2009-2010 with a following surge in capex but sagged below 5% after 2011. The stalling growth will lead to falling capacity utilization and excess capacity. We, therefore, forecast a remarkable drop in capex for auto industry in 2013.

-40%

-20%

0%

20%

40%

60%

80%

100%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

(f)20

14(f)

2015

(f)

Auto Market

Sales Volume YoY Capex YoY

Capex Leads Sales Volume

Source: CAAM, Company Data, Team Estimate

Europe The U.S. India

Lathe 2.7% 4.2%、4.4%

12.5%

Machine Center 2.7% 4.2%

Sawing Machine 2.7% 4.4%、3.3%

Bench Grinders 1.7%、8% 4.4%、3.3%

Drilling Machine 2.7%、8% 4.2%

Milling Machine 2.7% 、8% 4.2%

Grinding Machine 2.7% 、8% 4.4%

Boring Machine 1.7%、8% 4.2%

Milling & Boring Machine 1.7% 4.2%

Electric Discharge Machine 8% 3.5%、2.4%

Hydraulic Presses 8%、2.7%、1.7% 4.4%

Shearing Machine 8%、2.7%、1.7% 4.4%

Korea’s Free Trade Agreements

1

Shareholder Structure

II. Low QFII

I. Stable Composition

11.32%

15.83%

0.93%

6.98%

0.02%

64.92%

Directors and Supervisors

Large Shareholders

Managers

Foreign Institutional Investors

Domestic Institutional Investors

Individuals

1

• HONOR SEIKI CO., LTD (52%)– CNC vertical lathes & single purpose CNC lathes– Customization

• Asia Pacific Elite Corp. (100%)– Gantry machining center & motor drive high speed gantry machining

• Quick-TECH Machinery Co., Ltd(100%)– CNC Lathes

Net Income Contribution to Parent Company2007 2008 2009 2010 2011 2012

HONOR SEIKI CO., LTD 5.1% 11.3% 35.0% 4.9% 6.6% 25.9%

Asia Pacific Elite Corp. -1.3% -3.2% -27.6% -9.2% -8.4% -1.8%

Quick-TECH Machinery Co., Ltd - - - 0.1% 3.4% 1.5%

Source: Company Data

Subsidiaries

Components Ticker Market Cap (NTD mn) P/E P/B

Hiwin TT:2049 118,631 N.M 0.75NSK JP:6471 149,509 29.38 1.44THK JP:6481 86,262 26.38 1.37Fanuc JP:6954 1,075,280 23.01 2.54

Machine ToolsAwea TT:1530 2,910 10.41 1.18Goodway TT:1583 4,036 10.16 1.37Tongtai TT:4526 5,311 27.54 1.11Takisawa TT:6609 1,339 10.60 0.89Okuma JP:6103 38,394 15.53 1.13Mori Seiki JP:6141 40,952 23.07 1.15Doosan Infra KS:042670 54,424 11.73 1.00Gildemeister GY:GIL 41,112 13.01 1.44

Shieh Yih TT:4533 1,807 10.38 0.83

Source: Bloomberg, TEJ

Comparable Companies

(NT$ in mn) 2Q12 3Q12 4Q12 1Q13 2Q13(f) 3Q13(f) 4Q13(f) 1Q14(f)Net Sales 1,771 1,882 1,891 1,453 1,837 1,818 1,751 1,678Cost of Goods Sold -1,363 -1,419 -1,378 -1,133 -1,414 -1,404 -1,312 -1,303

Gross Profit 408 463 512 320 423 413 439 375Operating Exp -301 -320 -440 -311 -310 -309 -305 -299Marketing Expense -127 -128 -208 -140 -144 -143 -139 -135G&A -135 -116 -172 -125 -129 -128 -127 -126R&D -39 -76 -59 -47 -38 -38 -38 -38

Operating Income 107 143 73 9 113 104 134 75Net Interest -9 -8 -1 -7 -11 -13 -18 -15Exchange Gain and Loss 25 -33 -11 47 -3 1 1 1Others 29 -3 -16 -39 8 9 9 9

Pretax Income 152 98 45 60 95 88 107 54Income Tax -85 -15 36 -22 -20 -18 -23 -9

Earning from Continuing Ops 68 83 81 38 75 70 84 45Minority -22 -18 -28 -12 -10 -10 -10 -9

Net Income 45 66 54 27 65 60 74 36EPS 0.20 0.29 0.24 0.12 0.29 0.26 0.32 0.15Ratio(%) 2Q12 3Q12 4Q12 1Q13 2Q13(f) 3Q13(f) 4Q13(f) 1Q14(f)Sales Growth (YoY) -34.4% -19.1% -1.7% -13.7% 3.7% -3.4% -7.4% 15.5%Sales Growth (QoQ) 5.2% 6.3% 0.5% -23.2% 26.4% -1.0% -3.7% -4.2%Gross Margin 23.0% 24.6% 27.1% 22.0% 23.0% 22.7% 25.1% 22.3%Operating Margin 6.0% 7.6% 3.9% 0.6% 6.1% 5.7% 7.7% 4.5%Net income Margin 2.6% 3.5% 2.8% 1.8% 3.6% 3.3% 4.2% 2.1%Tax Rate 18.4% 55.6% 15.3% -80.1% 36.3% 20.8% 20.3% 21.5%

Financial Summary

(NT$ in mn) 2011 2012 2013(f) 2014(f) 2015(f)Cash & Short-term Investment 1,099 1,105 1,013 1,016 1,091Accounts Receivable 3,169 2,534 2,776 2,957 3,197Inventory 3,967 3,698 3,471 3,619 3,784Others 445 578 503 526 557

Current Asset 8,680 7,914 7,762 8,118 8,630Net PP&E 2,647 2,775 2,881 3,031 3,179Other Non-Current Assets 497 466 473 473 473

Total Asset 11,786 11,120 11,117 11,623 12,283

Accounts Payable 1,492 1,231 1,334 1,476 1,664ST. Borrowing 1,859 1,734 1,893 2,051 2,260Current Portion of LT. Debt 264 507 89 85 80Other Current Liability 1,328 1,256 0 0 0

Current Liability 4,944 4,728 3,315 3,611 4,004LT. Debt 1,371 965 832 832 832Bond 0 0 0 0 0Other Long-Term Liability 0 0 0 0 0

Long-Term Liability 1,371 965 832 832 832Other Non-Current Liability 176 158 242 242 242

Total Liability 6,490 5,850 4,389 4,685 5,078Total Equity 5,296 5,270 6,728 6,938 7,205

Balance Sheet

(NT$ in mn) 2011 2012 2013(f) 2014(f) 2015(f)Net Sales 8,717 7,226 6,858 7,459 8,099

Cost of Goods Sold (6,563) (5,427) (5,263) (5,753) (6,248)Gross Profit 2,154 1,799 1,595 1,706 1,851 Operating Exp (1,400) (1,336) (1,235) (1,249) (1,294)

Marketing Expense (709) (586) (566) (582) (618)G&A (570) (542) (509) (516) (524)R&D (121) (207) (161) (152) (151)

Operating Income 753 463 360 456 557 Net Interest (24) (26) (50) (58) (59)Exchange Gain and Loss 66 (60) 45 3 4 Others (15) 11 (14) 28 17

Pretax Income 780 389 351 371 460 Income Tax (201) (81) (83) (77) (100)

Earnings from Continuing Ops 578 308 268 294 360 Minority (2) (87) (41) (36) (40)

Net Income 576 221 227 258 320

NOPAT 594 242 265 305 366EBIT 738 474 392 488 577EBITDA 895 652 580 669 761EPS 2.60 0.98 0.99 1.12 1.38BVPS 23.89 23.27 29.41 30.03 31.19Shares Outstanding (mn) 222 227 229 231 231

Income Statement

(NT$ in mn) 2011 2012 2013(f) 2014(f) 2015(f)Net Income 578 308 268 294 360 DD&A 170 193 188 181 184 Working Capital Investment (751) 644 87 (187) (217)Other Adjustment 596 (150) (147) 56 98

Cash Flow from Operation 593 995 396 344 425 Capex (396) (319) (272) (331) (332)Other Adjustment (175) (66) 31 (12) (55)

Cash Flow from Investment (571) (385) (241) (343) (387)Debt Increase (Decrease) (7) (289) (48) 158 209 Stock Issuance (Repurchase) 30 10 0 0 0 Cash Dividend (264) (287) (226) (136) (155)Other Adjustment 44 (3) (22) (20) (16)

Cash Flow from Financing (197) (570) (297) 2 38 Exchange Influence 72 (35) 49 (0) (1)

Net Change in Cash (103) 6 (93) 3 75 FCFF (138) 477 182 (0) (11)FCFE (163) 169 96 111 153

Statement of Cash Flow

Ratio(%) 2011 2012 2013(f) 2014(f) 2015(f)

Growth-YoYNet Sales 1.5% -17.1% -5.1% 8.8% 8.6%NOPAT -3.7% -59.3% 9.6% 15.0% 20.0%EBIT -27.7% -35.8% -17.4% 24.5% 18.4%EBITDA -22.7% -27.1% -11.1% 15.4% 13.8%EPS -11.9% -62.3% 1.3% 12.7% 23.7%ProfitabilityGross Margin 24.7% 24.9% 23.3% 22.9% 22.9%Operating Margin 8.6% 6.4% 5.3% 6.1% 6.9%Net Income Margin 6.6% 3.1% 3.3% 3.5% 3.9%Capital StructureDebt Ratio 29.6% 28.8% 25.3% 25.5% 25.8%Current Ratio 175.6% 167.4% 234.1% 224.8% 215.6%Quick Ratio 95.3% 89.2% 129.4% 124.6% 121.0%

Financial Ratios

Source: Company Data, TEJ

Exchange Gain and Loss

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%1Q

08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

FX chg Exchange gain and loss/Sales

Slope = -88%

Sensitivity Analysis

Optimistic Neutral Pessimistic

Scenarios

1. TWD/JPY drops 10%2. JPMT fix prices

1. TWD/JPY is fixed2. JPMT lower prices

based on Yen depreciation

1. TWD/JPY rises 10%2. JPMT lower prices

based on Yen depreciation

2013 Gross Margin 28.6% 23.2% 21.6%

2013 EPS $2.73 $0.99 $0.13

2014 EPS $3.37 $1.12 $0.34

2015 EPS $3.90 $1.38 $0.52

Source: Team Estimates

0

3,000

6,000

9,000

12,000

15,000

Japa

n

Germ

any

Italy

Taiw

an

Switz

erla

nd

Chin

a

Kore

a

U.S

Spai

n

Belg

ium

2011 2012

0

3,000

6,000

9,000

12,000

15,000

Chin

a

U.S

Germ

any

Indi

a

Kore

a

Braz

il

Mex

ico

Turk

ey

Russ

ia

Fran

ce

2011 2012

0

8,000

16,000

24,000

32,000

Chin

a

Japa

n

Germ

any

Kore

a

Italy

Taiw

an U.S

Switz

erla

nd

Spai

n

Aust

ria

2011 2012

(USD: mn)

0

10,000

20,000

30,000

40,000

50,000

Chin

a

U.S

Japa

n

Germ

any

Kore

a

Indi

a

Italy

Braz

il

Taiw

an

Mex

ico

2011 2012

Source: Gardner

Machinery Tool Export Machinery Tool Import

Machinery Tool Production Machinery Tool Consumption

+5.9%

+5.2%

Machinery Market Outlook

Source: Gardner

(USD: mn)

(USD: mn) (USD: mn)

Source: Gardner Source: Gardner

0

10

20

30

40

50

60

70

2009 2010 2011 2012 201360%

65%

70%

75%

80%

85%

2009 2010 2011 2012 2013

Source: USMTO Source: TEJ

0

10

20

30

40

50

60

70

2009 2010 2011 2012 201397.0

97.5

98.0

98.5

99.0

99.5

100.0

100.5

101.0

101.5

102.0

2011 2012 2013 May-13

Source: TEJSource: CECIMO

The U.S. Machinery MarketIndustry capacity utilization is below 80% PMI sustains above 50

PMI is below 50BCI has been decreasing

The U.S. Machinery Market

1

• The market comprises four laser drilling machine manufacturers

• Market Share– 80% Hitachi and Mitsubishi– 20% Han’s Laser and Tong-tai

• Tong-tai’s laser drilling machines are on average 15% - 20% cheaper than those of Hitachi

• Tong-tai’s ASP: NT$ 1.4 – 1.6 billion• Gross Margin: 30%

0

2

8

1

2009 2010 2011 2012

Tong-tai’s Laser Drilling Machine Shipment

Source: Company Data

PCB Laser Drilling Machines

Tong-tai’s Laser Drilling Machine Shipments

(Units)

Source: Company Data

306

548

331

210

719

325348

2006 2007 2008 2009 2010 2011 2012

(Units)

PCB Mechanical Drilling Machines

• Tong-tai competes with Hitachi and Han’s Laser

• Market Share– 25% Tong-tai– 15% Hitachi– 19% Han’s Laser

• Tong-tai’s mechanical drilling machines are on average 15% -20% cheaper than those of Hitachi

• Tong-tai’s ASP: NT$ 3.0-4.0 million• Gross Margin: 20% - 25%

Tong-tai’s Mechanical Drilling Machine Shipments

CAGR6.5%

CAGR7.5%

CAGR4.1%

CAGR2.0%

CAGR1.5%

CAGR8.2%

0.0

3.0

6.0

9.0

12.0

15.0

IC S

ubst

rate

FPC

Mul

tilay

er

Doub

le S

ide

Sing

le S

ide

HDI

HDI and IC substrate are new focus

PCB Market Outlook

$22.85 $23.02 $21.85 $29.26 $32.06 $33.58 $35.82 $38.22 $40.79

12.93%

0.77%

-5.11%

33.94%

9.57%

4.73%6.70% 6.70% 6.70%

-10%

0%

10%

20%

30%

40%

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

PCB Sales

China and Taiwan Sales YoY(USD bn) (USD bn)

20.23 22.85 23.02 21.85 29.26 32.06 33.58 35.82 38.22 40.79

2109

2476

1755

732

2838

13001387

14871599

1651

222

529

311158

259

548

793

1147

1660

2401

0

5

10

15

20

25

30

35

40

45

0

500

1000

1500

2000

2500

3000

2006 2007 2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

PCB Sales (incl. only China & Taiwan) Mechanical Drilling Machine Shipments (LHS) Laser Drilling Machine Shipments (LHS)

Drilling Machine Market Outlook

(US$ bn)(Units)

Source: Prismark

HDI Debuted

Financial Crisis

iPhone adoptedAny Layer HDI

iPad adoptedAny Layer HDI

8 1 34 83 120

1.5%

3.0%

5.0% 5.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

25

50

75

100

125

150

2011 2012 2013(f) 2014(f) 2015(f)

Production yield improves of Tong-tai's laser

Laser Drilling Machine Shipments Market Share

1.22

1.77

2.49

3.00

0.8%

44.9%40.8%

20.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2012 2013(f) 2014(f) 2015(f)

Sales: 35.4% upside potential

Mechanical Drilling Machine Sales Sales YoY

Upside for Tong-tai’s PCB Drilling Machines

(NTD bn)

(Units)

(Units)

325 348 372 430 446

25% 25% 25%

26% 26%

24.0%

25.0%

26.0%

27.0%

0

100

200

300

400

500

2011 2012 2013(f) 2014(f) 2015(f)

Tong-tai's market share stabilizes at 25% - 26%

Mechanical Drilling Machine Shipments Market Share

Production yield improves of Tong-tai’s laser drilling machines